Key Takeaways

- Anguilla's corporate framework spans multiple distinct entity types — including the IBC, LLC, Ordinary Resident Company, and partnerships — each established under separate legislation and carrying different liability and operational characteristics.

- The International Business Company (IBC) is the most registered entity type in Anguilla, primarily used by non-resident entrepreneurs due to the territory's zero-tax treatment of offshore income.

- Company registration in Anguilla is governed by the Financial Services Commission (FSC) and the Registrar of Companies, operating under an English common law legal system as a British Overseas Territory.

- Ordinary Resident Companies are the appropriate structure for businesses conducting active local operations in Anguilla, distinguishing them from IBCs and LLCs, which serve primarily international or flexible governance purposes.

Introduction to Entity Types in Anguilla

Anguilla is a British Overseas Territory located in the northeastern Caribbean, situated near Saint Martin and Saint Kitts and Nevis. As a territory of the United Kingdom, it operates under its own legal system based on English common law, with company registration governed by the Anguilla Financial Services Commission (FSC) and the Registrar of Companies. The territory maintains a zero-tax regime for most corporate structures, with no income, capital gains, or corporate tax levied on qualifying entities.

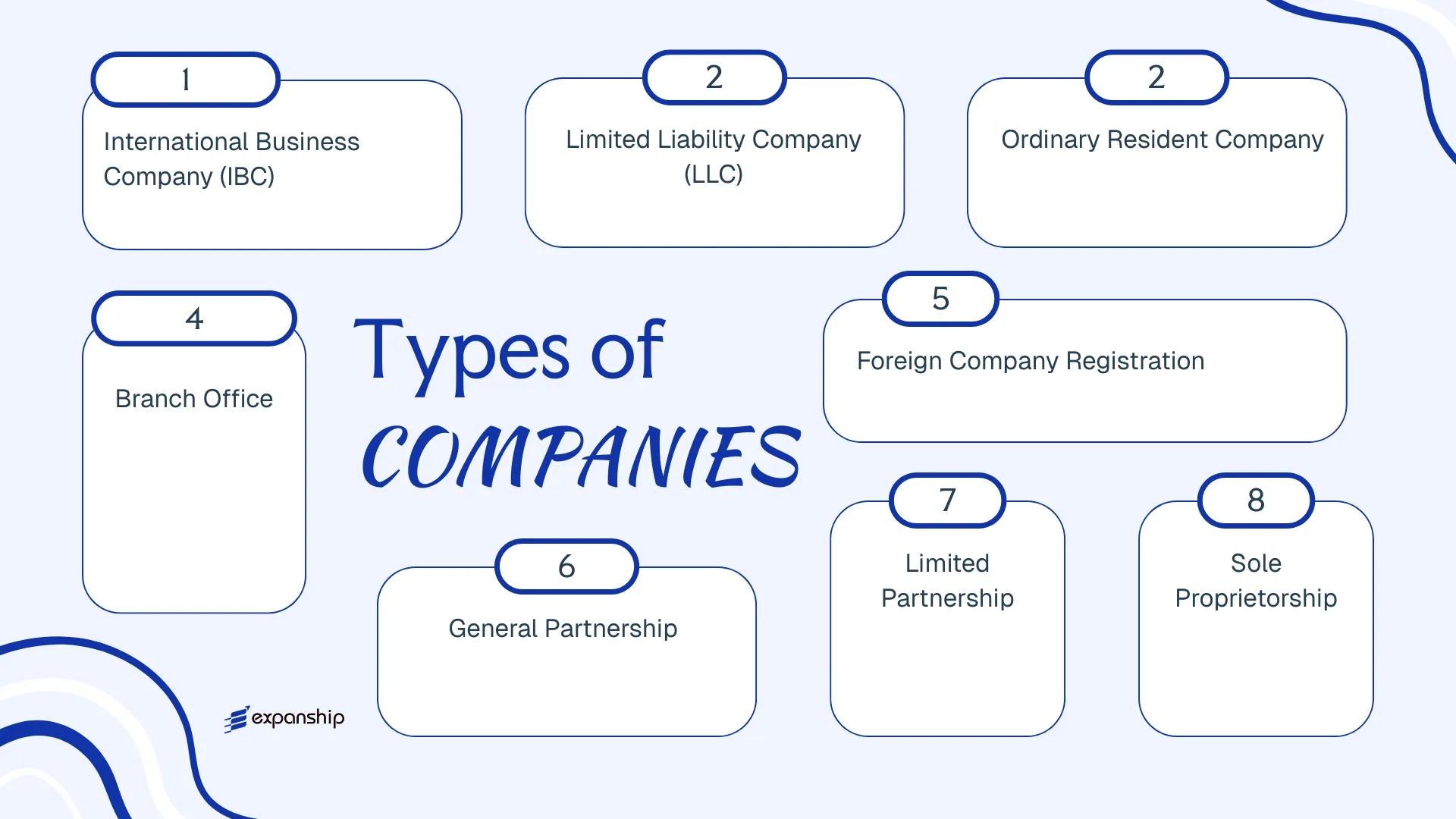

The types of business entities in Anguilla span several distinct structures, each established under separate legislation. These include the International Business Company (IBC), the Limited Liability Company (LLC), the Ordinary Resident Company, branch offices and foreign company registrations, general and limited partnerships, and sole proprietorships.

Each structure carries different formation requirements, liability characteristics, and operational constraints. This article examines each entity type in detail — covering its governing legislation, ownership rules, permissible activities, and practical use cases — to help you determine which structure aligns with your business objectives.

An Overview of Business Structures in Anguilla

Anguilla's corporate formation options span several distinct entity types, governed primarily by legislation including the International Business Companies Act, the Limited Liability Company Act, and the Companies Act. Each structure carries different rules around liability, taxation, and permitted activities, making the choice a function of your specific operational and ownership requirements.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| IBC | Corporation | Limited | Exempt | No | 1 shareholder | FSC | IBC Act |

| LLC | Hybrid entity | Limited | Exempt | Permitted | 1 member | FSC | LLC Act |

| Ordinary Resident Company | Corporation | Limited | Taxed | Yes | 1 shareholder | FSC | Companies Act |

| Branch Office | Foreign branch | Parent liable | Depends on parent | Yes | N/A | FSC | Companies Act |

| Foreign Company Registration | Registered foreign entity | Parent liable | Depends on parent | Yes | N/A | FSC | Companies Act |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | FSC | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 1 GP, 1 LP | FSC | Partnership Act |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | Local registry | N/A |

Each of these structures is examined in full in the sections below.

International Business Company (IBC)

The Anguilla International Business Company IBC is governed by the International Business Companies Act (Cap. B.65), which consolidates earlier IBC legislation and defines the framework for offshore company formation and operation. The entity carries a separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name, with shareholders' exposure limited to their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (limited by shares) | Separate legal personality; shareholders not personally liable for company debts |

| Members | Minimum 1 shareholder, 1 director; no maximum | Director and shareholder can be the same person; corporate directors and shareholders permitted |

| Local Presence | Registered Agent required; no registered office required separately | Registered Agent must be licensed in Anguilla; physical office not mandatory |

| Capital | No minimum share capital; shares can be in any currency | Par value or no-par-value shares both permitted |

| Privacy | Shareholder and director details not on public record | Beneficial ownership information held by the Registered Agent, not publicly disclosed |

Focus Points

- Taxation: IBCs are exempt from corporate income tax, withholding tax, capital gains tax, and stamp duty on income and transactions conducted outside Anguilla; no VAT applies to offshore activities.

- Economic Substance: IBCs conducting relevant activities as defined under Anguilla's Economic Substance Act must demonstrate adequate substance; pure holding or passive investment structures face lighter obligations.

- Annual Compliance: Annual renewal fees are payable to maintain the company in good standing; no audited financial statements are required by default.

- Treaty Access: Anguilla has a limited tax treaty network, which may restrict access to reduced withholding rates in counterparty jurisdictions.

- Restrictions: IBCs are prohibited from conducting business with persons resident in Anguilla or owning local real property without specific authorisation.

Closing

IBCs are commonly used for international trading, holding intellectual property, investment holding, and asset protection structures where activities occur entirely outside Anguilla. The absence of corporate tax on offshore income is a clear structural advantage, though the limited treaty network can reduce the entity's utility for structures that depend on treaty-based withholding relief.

This entity suits non-resident founders seeking a tax-neutral offshore vehicle for international trade, investment, or holding activities with no intention of operating locally.

Company Incorporation in Anguilla

Incorporate an IBC or other entity type in Anguilla with Expanship's end-to-end formation service.

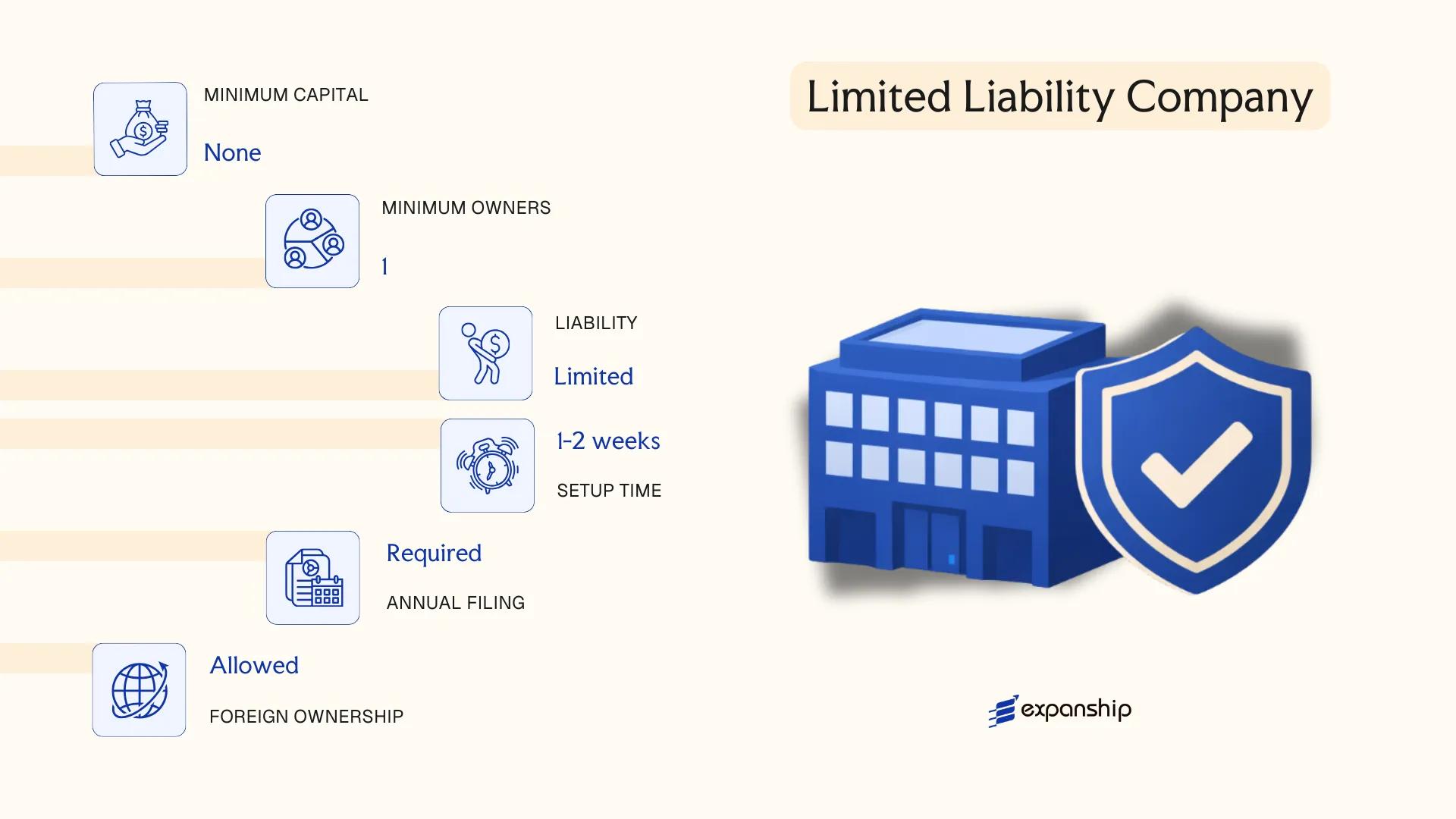

Limited Liability Company (LLC)

Anguilla's LLC framework is governed by the Limited Liability Company Act, enacted in 2000. Anguilla LLC formation requirements differ from IBC requirements in one significant respect: the LLC is a hybrid structure that draws on both corporate and partnership principles, giving members flexibility in how the entity is internally organized and managed.

The LLC possesses separate legal personality, meaning it can contract, hold property, and incur obligations in its own name. Member liability is confined to each member's capital contribution, and the internal governance terms are set out in a written operating agreement rather than fixed statutory rules.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Hybrid structure; separate legal personality |

| Members | Minimum 1; no maximum | Members may manage directly or appoint managers |

| Management | Member-managed or manager-managed | Defined in the operating agreement |

| Local Presence | Registered Agent required; registered office in Anguilla | No requirement for local directors |

| Capital | No minimum capital requirement; USD common | No par value obligations |

| Privacy | Member and manager names not on public record | Confidentiality maintained through registered agent |

Focus Points

- Taxation: LLCs are generally treated as tax-transparent pass-through entities; Anguilla imposes no corporate income tax, capital gains tax, withholding tax, or VAT on qualifying offshore LLCs.

- Economic Substance: LLCs engaged in relevant activities as defined under Anguilla's economic substance legislation must demonstrate adequate local substance.

- Annual Compliance: Annual fees are payable to the Anguilla Financial Services Commission; no requirement to file audited financial statements for standard offshore LLCs.

- Treaty Access: Anguilla has limited double tax treaty coverage, which may restrict treaty-based withholding tax relief for distributions or royalties.

- Conversion: An LLC may generally be converted to another entity type or continued into a foreign jurisdiction under Anguilla's legislation, subject to regulatory approval.

Closing

The limited liability company Anguilla offshore structure suits holding arrangements, joint ventures, and fund vehicles where members require pass-through tax treatment alongside liability protection. The operating agreement's flexibility is a practical advantage; the restricted treaty network remains a constraint for structures dependent on treaty-reduced withholding rates.

This entity type is most appropriate for international joint ventures, asset holding structures, and fund arrangements where partners require contractual governance flexibility and tax transparency.

Ordinary Resident Company

Anguilla ordinary resident company registration is governed by the Companies Act (R.S.A. c. C65), the primary legislation regulating locally incorporated entities that conduct business within the territory. Unlike an International Business Company, this structure is designed for operations that have a genuine domestic nexus.

As a separate legal entity, the ordinary resident company confers limited liability on its shareholders, meaning personal assets remain distinct from corporate obligations. The firm can own property, enter contracts, and sue or be sued in its own name under Anguillan law.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company with separate legal personality | Incorporated under the Companies Act (R.S.A. c. C65) |

| Members | Shareholders (min. 1, no statutory maximum) | Corporate shareholders permitted |

| Directors | Min. 1 director; no residency requirement specified under general provisions | At least one director must be appointed at all times |

| Local Presence | Registered office and registered agent required in Anguilla | Must maintain a physical registered address locally |

| Capital | No mandatory minimum share capital; denominated in any currency | Shares can be par value or no-par value |

| Privacy | Shareholder and director details filed with the Registrar of Companies | Records are generally accessible; not a high-privacy structure |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT is levied; stamp duty may apply to certain instruments.

- Economic Substance: Entities conducting relevant activities may be subject to economic substance requirements under Anguilla's substance legislation.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; failure to file can result in penalties or striking off.

- Treaty Access: Anguilla has a limited tax treaty network; access to double taxation agreements is generally restricted.

- Restrictions: The entity is permitted to conduct business locally, unlike an IBC, but requires relevant trade or business licences for regulated activities.

Closing

The ordinary resident company suits businesses with active local operations, domestic trading activity, or those supplying goods and services within the territory. Its primary advantage is unrestricted local trading rights; its key limitation is reduced privacy compared to offshore structures.

This entity type is best suited for entrepreneurs and businesses conducting trade, services, or operations directly within Anguilla's domestic market.

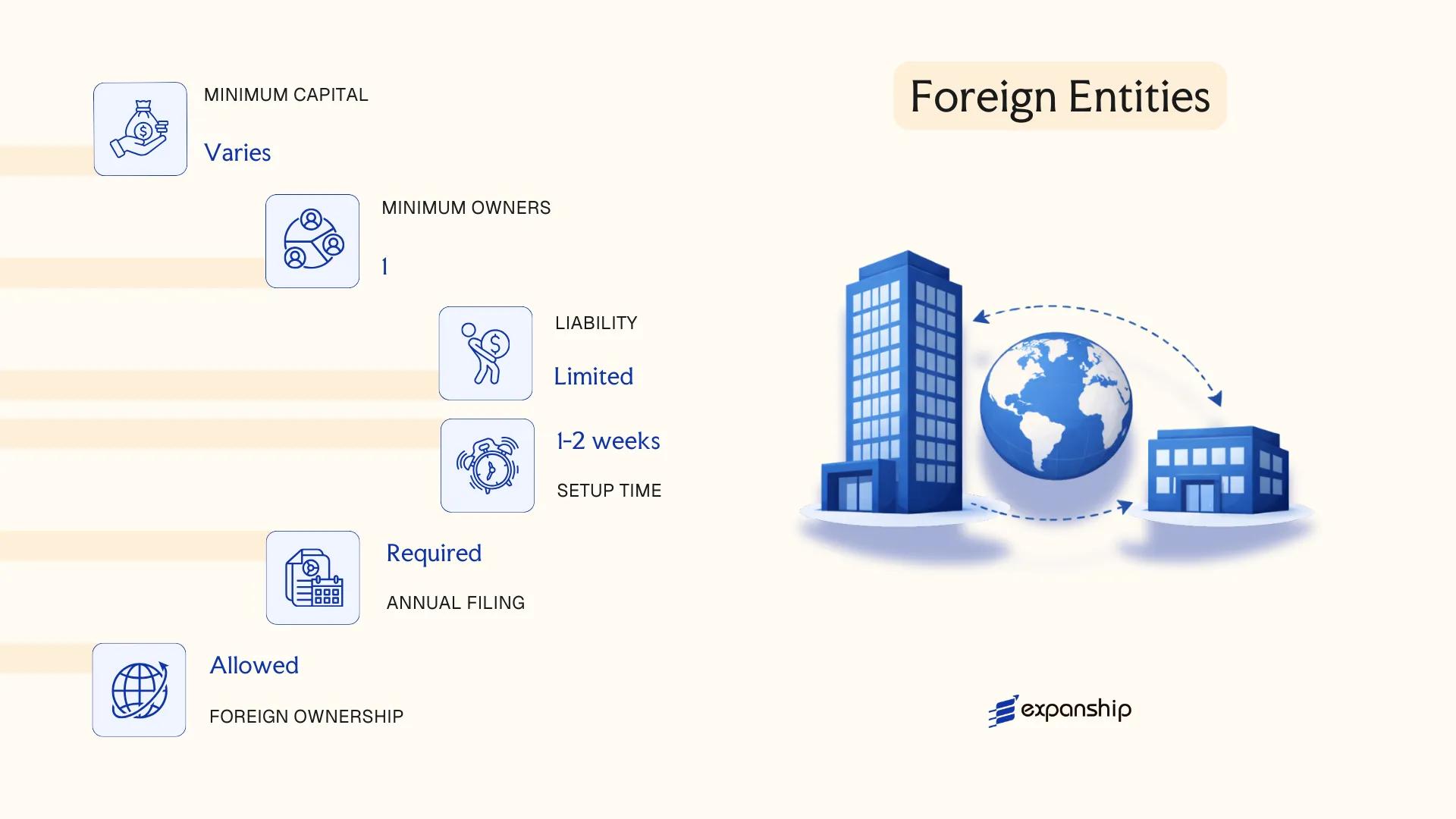

Foreign Entities in Anguilla [Branch Office, Foreign Company Registration]

Foreign companies seeking a presence in the territory without forming a new local entity have two primary routes available: registering a branch office or registering as a foreign company under Anguillian law. Both options are governed by the Companies Act (R.S.A. c. C65), which sets out the obligations for overseas businesses operating within the jurisdiction. A branch is not a separate legal entity — it remains part of the parent company, which retains full liability for its operations.

Foreign company registration in Anguilla requires filing with the Registrar of Companies, submitting certified copies of the parent company's constitutional documents, appointing a local registered agent, and maintaining a registered office address within the territory.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Registered Foreign Company | Not a separate legal entity; parent bears full liability |

| Governing Authority | Registrar of Companies, Anguilla | Filing and ongoing compliance managed through the Registrar |

| Local Presence | Registered agent and registered office required | Must be maintained throughout the registration period |

| Directors / Officers | Parent company's officers govern the branch | No separate local director mandatory, but a local agent is required |

| Capital | No separate minimum capital for the branch | Parent company's capital structure applies |

| Privacy | Parent company documents become part of public record upon registration | Less privacy than a locally incorporated IBC or LLC |

Focus Points

- Taxation: Anguilla imposes no corporate income tax, withholding tax, or VAT on foreign company branches; however, the parent's home jurisdiction may tax branch profits on a flow-through basis.

- Economic Substance: Foreign companies engaged in relevant activities may be subject to economic substance requirements under the Economic Substance (Companies and Partnerships) Act 2019.

- Annual Compliance: Registered foreign companies must file annual returns with the Registrar and keep local records current.

- Treaty Access: Anguilla has a limited tax treaty network; branches generally do not gain additional treaty benefits through Anguilla registration.

- Restrictions: A branch cannot issue shares locally or raise capital independently from the parent entity.

Closing

A registered branch suits foreign businesses that need a formalised presence for operational or regulatory reasons without the administrative overhead of incorporating a separate subsidiary. The primary limitation is unlimited parental liability — the parent company is fully exposed to any obligations the branch incurs.

Best suited for established foreign companies that require a recognised local presence for contracting or regulatory purposes and are prepared to accept that the parent entity bears direct legal and financial responsibility for the branch's activities.

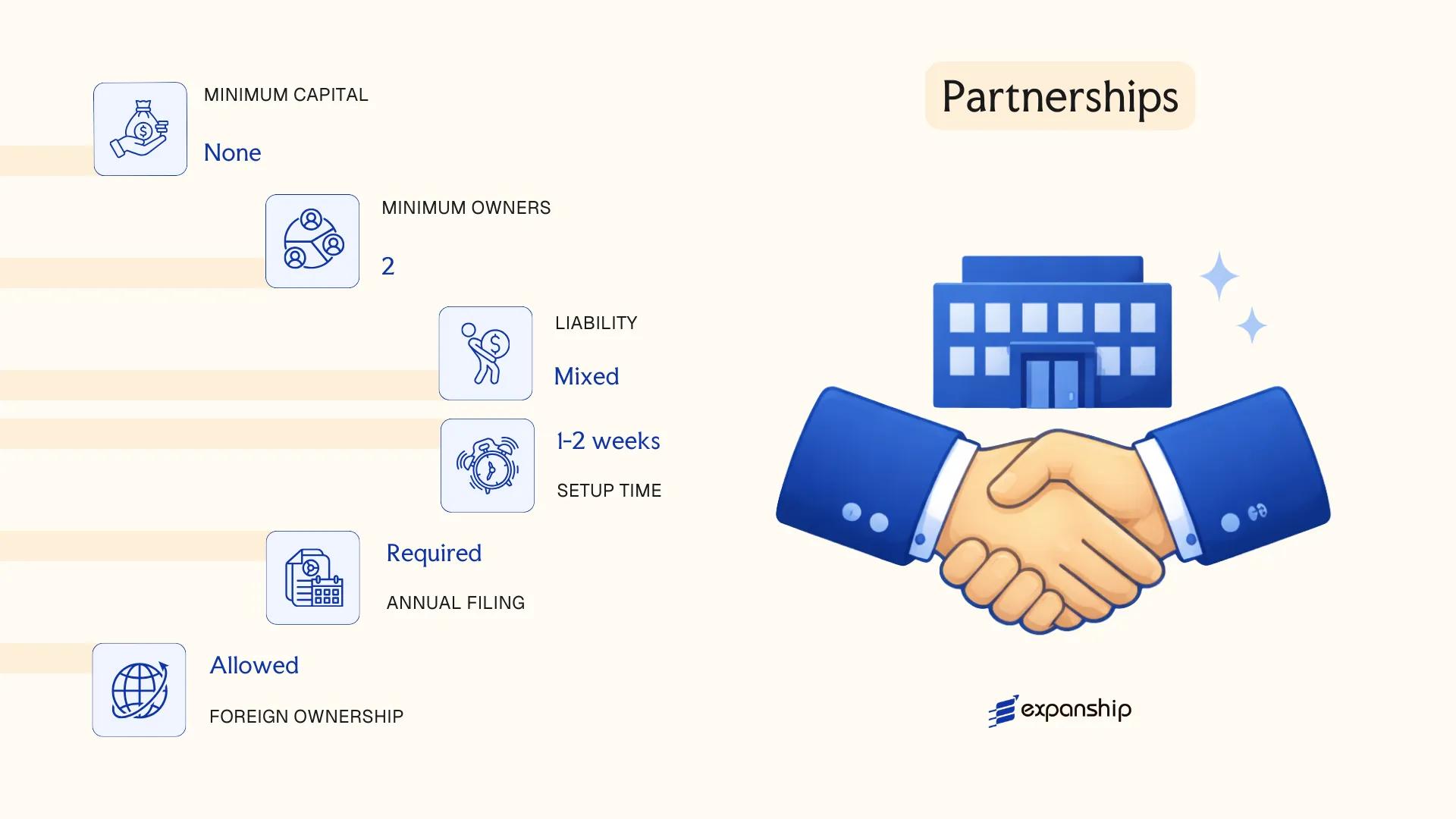

Partnerships in Anguilla [General Partnership, Limited Partnership]

Anguilla limited partnership registration is governed by the Limited Partnerships Act (R.S.A. c. L60), which provides the statutory framework for forming LPs in the territory. General partnerships, by contrast, operate under common law principles without a dedicated registration statute, though they must comply with business licensing requirements administered by the Financial Services Commission (FSC). A limited partnership is a distinct legal arrangement comprising at least one general partner with unlimited liability and one limited partner whose exposure is capped at their capital contribution.

Unlike an LLC, a partnership does not automatically possess separate legal personality under Anguillian law — its contractual and liability position depends on the specific structure chosen and how the partnership agreement is drafted.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual arrangement; LP has statutory recognition | General partnership lacks separate legal personality |

| Partners | GP: unlimited liability; LP: liability limited to contribution | Minimum 1 general partner + 1 limited partner for LP |

| Local Presence | Registered Agent required | Physical office not mandated; registered address suffices |

| Capital | No prescribed minimum; no specified currency | Contributions defined in the partnership agreement |

| Privacy | Partner details not on public register for LPs | General partnership details may be more accessible |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT applies to partnerships; profits are taxed solely at the partner level in their home jurisdiction.

- Economic Substance: Partnerships engaged in relevant activities under the Economic Substance Act 2019 must satisfy substance requirements in Anguilla.

- Annual Compliance: LPs must file annual returns with the FSC and maintain a registered agent; failure to comply can result in striking off.

- Treaty Access: Anguilla has no broad double tax treaty network, limiting treaty-based withholding tax relief for partners.

- Restrictions: Limited partners who participate in management risk losing their liability protection and may be reclassified as general partners.

Sub-Types

General Partnership

All partners share joint and unlimited liability for the firm's obligations. This structure is uncommon for offshore use given the absence of liability protection, but it may suit professional practices or arrangements between closely related parties where simplicity outweighs the liability risk.

Limited Partnership

One or more general partners manage operations and bear unlimited liability, while limited partners contribute capital and remain passive. This structure is frequently used for private equity vehicles, fund structures, and family wealth arrangements where investors require defined liability exposure.

Closing

Partnerships suit fund structuring, collective investment arrangements, and asset-holding vehicles where pass-through taxation and flexible profit allocation are priorities. The absence of a minimum capital requirement lowers the barrier to formation, though the unlimited liability of general partners remains a material structural exposure.

An Anguilla LP is best suited for private fund managers and investors who need a tax-transparent vehicle with flexible profit distribution and are prepared to appoint a dedicated general partner entity to contain liability.

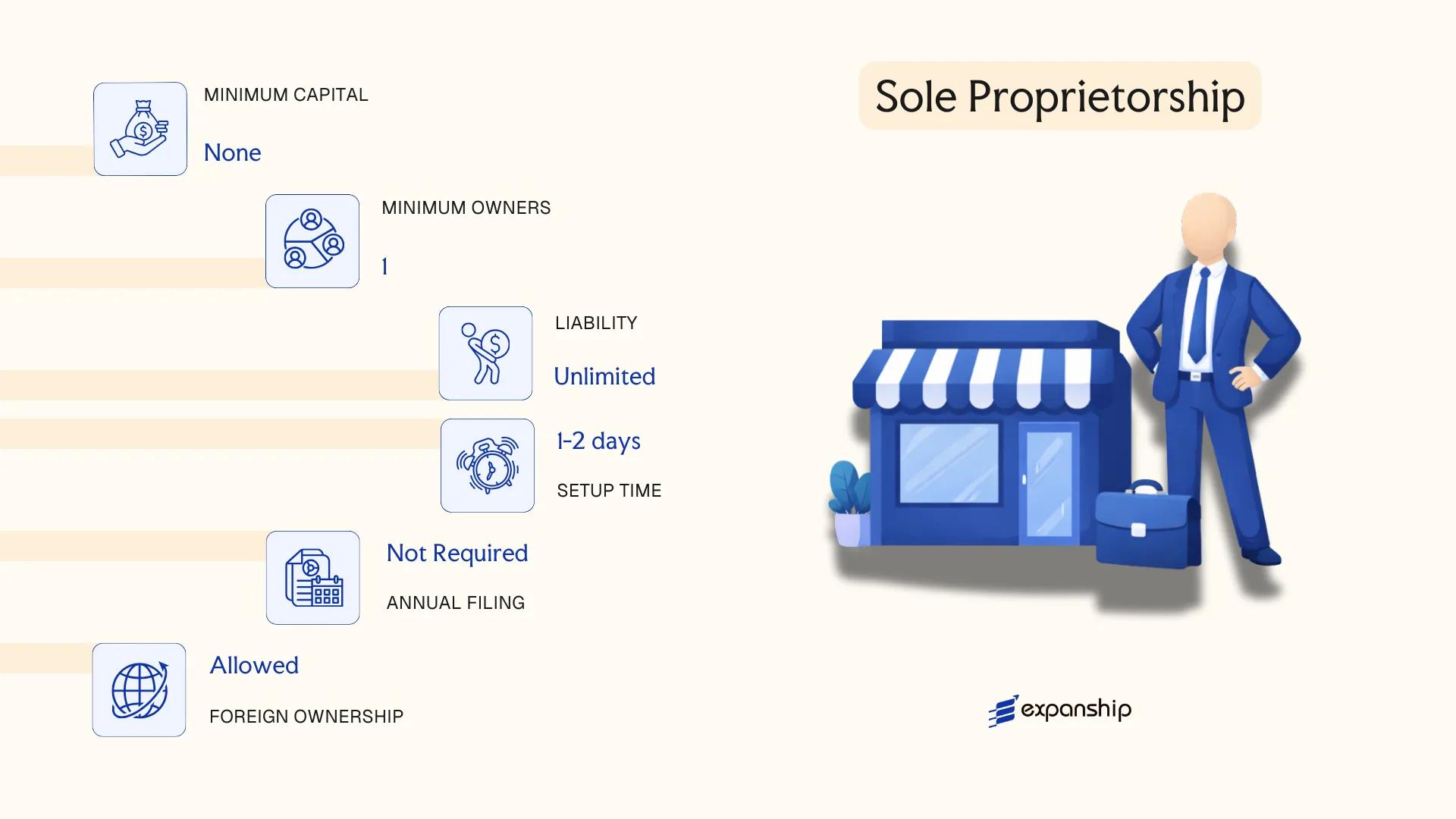

Sole Proprietorship

A sole proprietorship in Anguilla is the simplest form of business registration available to individuals operating under their own name or a trade name. Unlike incorporated structures, it does not create a separate legal entity — the owner and the business are legally the same person, meaning personal assets are directly exposed to business liabilities.

Registration is administered through the Anguilla Commercial Registry under the Business Names Act. If you trade under a name other than your own, that name must be registered. Operating without registration where it is required constitutes a breach of the Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated | No separate legal personality from the owner |

| Owner | Sole proprietor | Single individual only; no co-owners |

| Local Presence | Registered business name (if applicable) | Required if trading under a name other than the owner's legal name |

| Capital | No statutory minimum | Funded entirely by the individual owner |

| Privacy | Owner's name on public record | Trade name registration is publicly searchable |

Focus Points

- Taxation: No corporate income tax, capital gains tax, VAT, or withholding tax applies in Anguilla; the proprietor is taxed on personal income if applicable under local rules.

- Liability: Unlimited personal liability — business debts are the owner's debts.

- Annual Compliance: Business name renewals may be required to maintain active registration status.

- Conversion: Can be converted into a formal incorporated structure, though assets must be formally transferred as there is no automatic continuance mechanism.

- Treaty Access: No access to tax treaty benefits, as the structure lacks corporate status.

Closing

This structure suits freelancers, consultants, and micro-scale traders who operate locally with minimal overhead and low liability exposure. The primary advantage is administrative simplicity; the clear drawback is unlimited personal liability.

Local individual operators and self-employed professionals in Anguilla seeking a low-cost, low-formality setup for small-scale activity.

How to Choose the Right Entity Type in Anguilla

Knowing how to choose a business entity in Anguilla before you incorporate prevents regulatory, tax, and operational problems that are difficult to unwind after formation.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering an IBC while intending to trade with Anguillan residents places you in breach of the International Business Companies Act, which can result in striking off or financial penalties.

- Choosing a tax-exempt entity when your business requires access to double taxation treaty benefits means withholding tax reductions in counterpart countries are unavailable to you.

- Forming a company when a trust or foundation would better serve asset protection or estate planning locks your structure into annual shareholder obligations that neither of those alternatives impose.

- Selecting an entity that mandates audited financial statements for a single-person consultancy creates recurring compliance costs with no corresponding regulatory benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated activities such as insurance or funds management each require a distinct structure under Anguillan law.

- Local vs. Offshore Operations: If your firm will transact with Anguilla residents, an offshore-only entity is legally prohibited from doing so.

- Tax Objectives: Whether you need full tax exemption or eligibility under a specific regime determines which entity qualifies.

- Ownership and Management: Single-owner consultancies and multi-party joint ventures have different governance needs, which an LLC or partnership may satisfy more efficiently than a company.

- Privacy Requirements: Public register disclosure of directors and shareholders applies differently across entity types; nominee structures remain available for some.

- Exit Strategy: Redomiciliation, conversion, and voluntary winding-up procedures vary by entity type, so your anticipated exit route should inform your formation decision.

Compliance Services for Companies in Anguilla

Maintain good standing and meet your ongoing filing obligations under Anguillan law.

Conclusion

Incorporating a company in Anguilla presents a range of structurally distinct options, each suited to different ownership profiles and commercial purposes. The IBC remains the most registered entity type on the island, favored by non-resident entrepreneurs for its tax-neutral treatment of offshore income. LLCs serve those who need contractual flexibility in member governance, while Ordinary Resident Companies suit businesses with active local operations. Partnerships and sole proprietorships address simpler arrangements where limited liability is not a requirement.

Regulated by the Financial Services Commission under frameworks including the International Business Companies Act and the Limited Liability Company Act, the jurisdiction has maintained a consistent compliance posture. Ongoing engagement with international transparency standards signals a regulatory direction oriented toward institutional credibility. For your business, understanding which structure aligns with your operational and tax position is the starting point for any registration decision.

How Expanship Can Assist You

Expanship's Anguilla company formation services cover the full spectrum of entity types examined in this guide — from International Business Companies registered under the International Business Companies Act to Limited Liability Companies, Ordinary Resident Companies, and partnerships. Every formation path involves filings with the Anguilla Financial Services Commission, and getting those submissions right from the outset matters.

Expanship handles the procedural and compliance workload on your behalf:

- Document preparation and notarization or apostille legalization

- Registered agent and registered office provision in Anguilla

- Government filing and liaison with the Financial Services Commission

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for your new entity

Our corporate services in Anguilla extend beyond incorporation — your business receives ongoing support as regulatory obligations evolve after registration.

Reach out through Expanship Anguilla to discuss which structure fits your situation.

Frequently Asked Questions (FAQ)

The International Business Company (IBC) is by far the most frequently incorporated entity, governed by the International Business Companies Act. Its appeal rests on full tax exemption for non-resident-derived income and minimal ongoing reporting obligations.

An IBC cannot trade with Anguilla residents or own local real estate, while an Ordinary Resident Company faces no such restrictions on local commerce. The resident entity is subject to domestic tax obligations and carries a higher compliance burden, whereas the IBC operates in a tax-exempt environment provided it conducts no business within the territory.

The IBC provides the strongest confidentiality posture. Beneficial ownership details are not part of the public register, and nominee directors and shareholders are permitted under the Act. Share registers remain private unless disclosure is compelled by a competent authority.

One person can incorporate an IBC or LLC as the sole director and shareholder. General Partnerships and Limited Partnerships require at least two partners, making single-person formation legally impermissible for those structures.

Foreign nationals may form IBCs, LLCs, and register foreign company branches without restriction. Ordinary Resident Companies are also available to non-residents, though operating locally may trigger additional licensing requirements depending on the activity.

Anguilla's legislation permits continuation and re-registration in certain circumstances, allowing a foreign company to re-domicile as an Anguilla IBC. Direct statutory conversion between, for example, an IBC and an LLC is subject to the specific procedural requirements set out in the relevant governing acts.

The IBC carries the lightest compliance load among registered entities. There are no mandatory audit requirements, no public financial disclosure obligations, and annual renewal fees replace the more detailed reporting frameworks that apply to resident companies.

IBCs, LLCs, and Ordinary Resident Companies each have distinct legal personality, separate from their members or shareholders. General Partnerships do not have separate legal personality under Anguilla law, meaning partners bear direct liability for the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.