Key Takeaways

- Antigua and Barbuda's International Business Corporations Act restricts the range of permitted activities for IBCs, which limits structural flexibility for businesses requiring active trading or locally-directed operations.

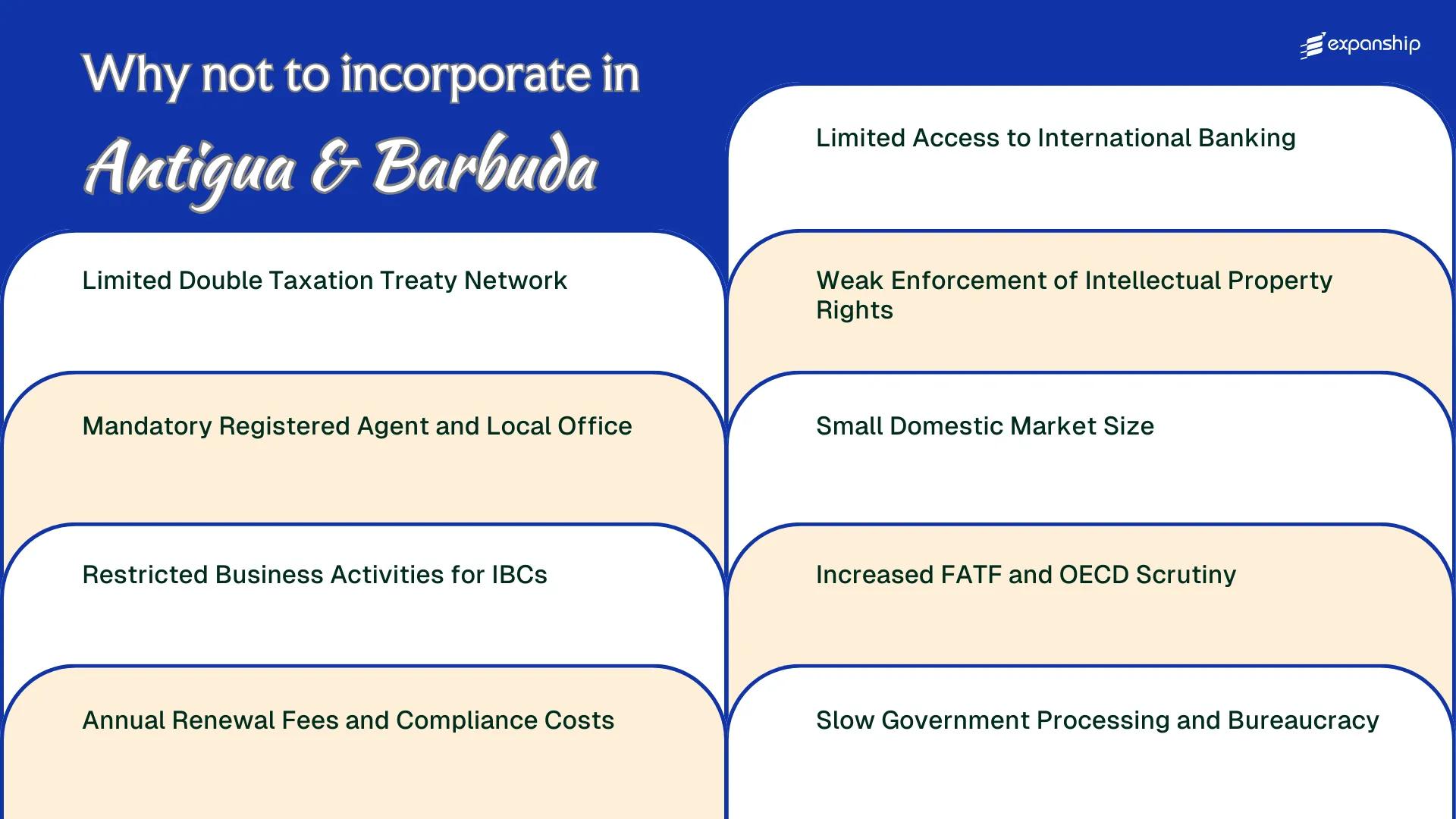

- With a minimal network of double taxation treaties, companies incorporated in Antigua and Barbuda face a higher risk of being taxed in multiple jurisdictions on the same income, increasing the effective tax burden on cross-border transactions.

- Heightened scrutiny from FATF and the OECD means that Antigua and Barbuda-incorporated entities are subject to enhanced due diligence requirements by foreign banks and counterparties, creating material friction in opening and maintaining international accounts.

- Mandatory registered agent and local office requirements impose recurring operational costs on non-resident owners who derive no commercial benefit from a physical presence in the jurisdiction.

Antigua and Barbuda operates under an evolving regulatory framework, shaped partly by its International Business Corporations Act and ongoing pressure from multilateral bodies to align with global transparency standards. The disadvantages of incorporating in Antigua and Barbuda span several distinct categories, from treaty limitations to banking access and compliance obligations.

Not every drawback applies equally to all business types. A holding company faces a different set of friction points than an active trading entity or a firm requiring third-party financing.

This article is most relevant to foreign investors and non-resident business owners considering an IBC or similar structure for cross-border operations. For the governing legislation, refer directly to the Companies Act on the government's official legal database.

Limited Double Taxation Treaty Network

Antigua and Barbuda tax treaty limitations present a structural problem that many offshore incorporators underestimate before committing to this jurisdiction. The country maintains a very narrow bilateral tax treaty network, leaving most IBCs exposed to double taxation on cross-border income.

No Treaty Coverage for Key Trading Partners

The absence of treaties with major economies — including the United States, the United Kingdom, Germany, and most of the EU — means withholding taxes applied by those countries on dividends, royalties, and interest payments cannot be reduced or credited back through treaty relief. For a business with revenue streams flowing from Europe or North America, this creates a direct cost that compounds annually.

Antigua and Barbuda's IBC framework, governed under the International Business Corporations Act, offers no domestic mechanism to offset this foreign tax exposure.

Structural Risk for Holding and Royalty Structures

Royalty-holding entities and passive income structures are particularly exposed, since withholding rates in source countries often reach 15 to 30 percent with no treaty reduction available. This materially erodes the tax efficiency that offshore structuring is meant to achieve.

Without treaty access to major economies, foreign withholding taxes on dividends, royalties, and interest are fully borne by the IBC, with no legal mechanism under Antiguan law to offset or recover them.

Mandatory Registered Agent and Local Office

Antigua and Barbuda registered agent requirements apply to all International Business Companies under the International Business Corporations Act. Every IBC must appoint a licensed registered agent and maintain a registered office address within the jurisdiction. Neither can be waived.

This creates a recurring cost that exists entirely outside your core business operations. Registered agent fees in Antigua typically range from a few hundred to over a thousand US dollars annually, depending on the provider and scope of services.

For a foreign owner who has no physical presence, no staff, and no actual activity on the island, these costs produce no operational value. You are paying to satisfy a local compliance formality, not to run a business.

The practical friction this creates includes:

- Dependence on a third-party agent for official correspondence, which introduces delays if notices or filings are not forwarded promptly

- Inability to change your registered office without filing formal notification, adding administrative steps for routine updates

- Agent fees accumulate year over year regardless of whether the company conducts any transactions

- Limited choice among licensed providers can reduce your ability to negotiate service costs downward

Mandatory local office restrictions under Antigua IBC rules also mean your registered address cannot simply be a foreign address or a virtual mailbox outside the jurisdiction.

Company Incorporation in Antigua and Barbuda

Set up your IBC in Antigua and Barbuda with full registered agent coordination and compliance support from day one.

Restricted Business Activities for IBCs

Under the International Business Corporations Act of Antigua and Barbuda, an IBC faces hard prohibitions on the types of commercial activity it can conduct. Antigua and Barbuda IBC business restrictions bar these entities from carrying on business with residents, owning real property locally, or operating as a bank, insurance company, or trust without separate licensing under distinct regulatory frameworks.

These are not procedural hurdles. They are statutory exclusions that remove entire business categories from reach before you begin structuring your operations.

| Activity | IBC Status | Regulatory Basis |

|---|---|---|

| Banking / deposit-taking | Prohibited without separate licence | Financial Services Regulatory Commission |

| Insurance underwriting | Prohibited without separate licence | Financial Services Regulatory Commission |

| Trust services | Prohibited without separate licence | Separate trust licensing required |

| Domestic trade with Antigua residents | Prohibited | IBC Act structural restriction |

| Local real property ownership | Prohibited | IBC Act structural restriction |

If your business model depends on serving local customers or holding physical assets on-island, an IBC cannot accommodate that without converting to a different corporate structure. The restricted activities for Antigua offshore companies are not edge cases; banking and insurance alone represent sectors that many holding or investment vehicles need peripheral access to.

The practical consequence is that companies with diversified revenue models may require parallel entities under different licensing regimes, which multiplies compliance obligations and cost.

Annual Renewal Fees and Compliance Costs

Antigua and Barbuda IBC annual renewal costs are governed under the International Business Corporations Act, which requires IBCs to pay government renewal fees each year to maintain active status. Missing this deadline results in penalties and can lead to administrative strike-off, meaning your company loses its legal standing without prior resolution of outstanding liabilities.

Beyond the government fee itself, your business must also pay its registered agent annually to retain a valid registered address. This is a non-negotiable structural cost, not an optional service.

IBC maintenance costs in Antigua and Barbuda tend to compound when you factor in mandatory registered agent retainers alongside document preparation and filing fees. For companies with no active operations in the jurisdiction, these recurring costs produce no corresponding operational benefit.

- Annual government renewal fees must be paid by the prescribed deadline under the IBC Act

- A licensed registered agent must be retained and paid continuously throughout the company's life

- Failure to renew on time triggers late penalties before eventual strike-off

- Compliance obligations persist regardless of whether the IBC conducts any business activity

Even a dormant IBC with zero transactions must pay full annual renewal fees, the same amount applies whether your company earned nothing or operated globally.

Limited Access to International Banking

Antigua and Barbuda offshore banking challenges affect IBCs more acutely than many comparable offshore jurisdictions, largely because of how international correspondent banks assess Caribbean-registered entities.

Why IBCs Face Rejection or Restricted Access

Banks in the United States, United Kingdom, and European Union routinely apply enhanced due diligence to companies registered under Antigua's International Business Corporations Act. Your entity may be classified as high-risk by default, not because of its actual activity, but because of its jurisdiction of incorporation, making account opening difficult regardless of your business's legitimacy.

The Practical Consequences for Your Business

Correspondent banking relationships have narrowed significantly across the Caribbean following global de-risking trends, leaving even local banks with fewer options to facilitate international transfers for offshore companies. An IBC that cannot access a functional multi-currency account faces real constraints on receiving client payments, settling invoices, or holding operating capital in usable form.

Some banks will consider accounts for IBCs with demonstrated economic substance or institutional backing, though this does not eliminate the screening burden your business must still clear.

Addressing Banking Access Challenges for Your Antigua Entity

Understand the banking limitations affecting IBCs in Antigua and Barbuda and get guidance on structuring your entity to improve international account access.

Weak Enforcement of Intellectual Property Rights

Antigua and Barbuda intellectual property risks are a practical concern for any foreign firm that holds trademarks, patents, or proprietary software and plans to use an IBC as the holding or licensing vehicle. The country's IP enforcement framework is limited in both institutional capacity and international reach.

- The Intellectual Property Office operates under the Trademarks Act and Patents Act, but independent assessments have consistently flagged gaps in enforcement resources that leave registered rights difficult to defend against infringement.

- No bilateral IP enforcement treaty with major trading partners means that protection secured locally carries little automatic weight in foreign courts.

- Customs-level border enforcement against counterfeit or infringing goods remains weak, exposing IP-dependent businesses to material loss without effective administrative recourse.

- Litigation to defend a registered trademark or patent requires engaging local counsel and navigating a court system that lacks a dedicated IP tribunal, adding cost and delay.

- This limitation applies even when IP assets are formally registered, since registration alone does not guarantee enforceable protection under current institutional conditions.

Small Domestic Market Size

Antigua and Barbuda's small market limitations are a structural reality that directly constrains revenue potential for foreign businesses. With a population of roughly 100,000 people, the local consumer base cannot support scale-dependent business models across most sectors.

IBCs incorporated under the International Business Corporations Act are legally restricted from conducting business with residents, which means your entity cannot even access the limited domestic demand that exists. The local market is therefore not a fallback option when international revenue slows.

GDP figures from the World Bank consistently place the country among the smallest economies in the Western Hemisphere, with total output under USD 2 billion. For businesses that require a minimum addressable market to justify fixed operational costs, this creates a structural mismatch from the outset.

Service firms, retailers, and consumer-facing entities face the sharpest exposure to this limitation. Any business model that depends on organic local growth rather than cross-border revenue will find the economic base insufficient to sustain operations.

A foreign-owned retail or professional services firm requiring a domestic customer base of at least 500,000 to break even on fixed costs of USD 150,000 annually would face an immediate structural deficit, given that the entire national population falls below that threshold.

Increased FATF and OECD Scrutiny

Antigua and Barbuda FATF scrutiny risks are a concrete operational concern for any foreign business owner using the jurisdiction for offshore structuring. The Financial Action Task Force has previously identified the country as requiring closer monitoring, and while its status has shifted over time, the underlying perception among correspondent banks and institutional counterparties remains cautious.

IBCs registered under the International Business Corporations Act face heightened due diligence requirements from foreign banks and payment processors precisely because of this history. Transactions routed through an Antigua-registered entity can trigger additional compliance reviews, slowing settlement times and increasing administrative costs on the counterparty side.

OECD compliance challenges for Antigua offshore companies extend to substance requirements and information exchange obligations. The jurisdiction is a signatory to the Common Reporting Standard (CRS), meaning financial account data is automatically shared with tax authorities in participating countries.

Your home country's tax authority will likely receive information about accounts held through your Antigua structure. For businesses assuming offshore confidentiality, this renders that assumption operationally false.

- Entities that fail to demonstrate genuine economic substance risk being reclassified by foreign tax authorities, regardless of their legal standing under local law.

If your Antigua-registered IBC holds accounts in CRS-participating jurisdictions, financial information will be reported automatically to your home country's tax authority, making any assumption of confidentiality legally and practically unsound.

Slow Government Processing and Bureaucracy

Antigua and Barbuda bureaucracy incorporation problems are not isolated complaints — they reflect a structural pattern within the Financial Services Regulatory Commission (FSRC), the body responsible for IBC registrations and ongoing supervision. Processing times for new company formations can extend beyond standard offshore benchmarks, creating unpredictable timelines for businesses that need to operationalize quickly.

Delays at the registry level mean your entity may sit in a pending state while commercial opportunities or contractual deadlines pass. This is particularly disruptive for businesses using the IBC as a vehicle for time-sensitive transactions.

Government offices also have limited digital infrastructure for tracking application status, which forces reliance on your registered agent as the primary communication channel. That dependency adds an indirect cost layer, since agents typically charge for follow-up correspondence and status inquiries beyond their base retainer.

Strategies to Overcome These Challenges

Overcoming Antigua and Barbuda incorporation challenges requires structural planning before the entity is formed, not after complications arise. The disadvantages covered in this blog — from banking access difficulties to FATF scrutiny — each have addressable responses within the existing legal and regulatory framework.

- Register your IBC under the International Business Corporations Act with a licensed registered agent who maintains a physical local office, satisfying the mandatory presence requirement.

- Open correspondent banking relationships through jurisdictions with stronger treaty networks to compensate for the limited double taxation agreements available.

- Restrict your IBC's activities at incorporation to those explicitly permitted under the Act, avoiding any scope that could trigger restrictions on domestic trading.

- File annual returns and renewal fees on schedule with the Financial Services Regulatory Commission to avoid penalties and maintain good standing.

- Register intellectual property rights in jurisdictions with enforceable IP frameworks, rather than relying solely on local protections.

These steps operate within the oversight of the Financial Services Regulatory Commission and align with international compliance expectations set by FATF and the OECD. Structural preparation reduces exposure but does not eliminate the inherent limitations of this jurisdiction.

Antigua and Barbuda's Overall Business Value

Antigua and Barbuda's position as an International Business Company (IBC) jurisdiction is credible but conditional. The International Business Corporations Act and the broader regulatory environment offer genuine structural benefits, yet the disadvantages documented across this blog are real constraints that affect operational outcomes, not theoretical risks.

| Pros | Cons |

|---|---|

| IBCs pay zero corporate tax on foreign-sourced income under the IBC Act | No meaningful double taxation treaty network limits cross-border tax relief |

| Incorporation process is straightforward for standard IBC structures | Government processing delays add unpredictable timelines to filings and renewals |

| The jurisdiction maintains a stable common law legal framework | FATF and OECD scrutiny increases due diligence burdens for banking and counterparty relationships |

| Annual compliance costs are relatively low in absolute terms | Mandatory registered agent and local office fees are unavoidable recurring expenses |

| English is the official language, reducing administrative friction | International banking access remains restricted, with few correspondent banking options |

| The ABLP and regulatory bodies maintain a functioning corporate registry | IBCs face statutory restrictions on conducting business within the domestic market |

Your assessment of Antigua and Barbuda incorporation value depends on how directly these friction points intersect with your specific operating model.

Corporate Compliance Services in Antigua and Barbuda

Maintain your IBC's good standing with annual filings, registered agent coordination, and regulatory reporting under Antigua and Barbuda's corporate framework.

Conclusion

Antigua and Barbuda's IBC framework offers genuine structural advantages, but the Antigua and Barbuda company formation drawbacks summary presented across this blog reflects a pattern of meaningful constraints. The absence of substantive double taxation treaties limits tax planning utility for cross-border operations. Banking access remains an ongoing friction point, with correspondent banking restrictions affecting how funds move internationally. Heightened FATF and OECD scrutiny adds compliance obligations that did not exist a decade ago. Structural preparation and informed professional guidance determine whether your entity functions as intended within these boundaries.

Expanship's Services for Your Antigua and Barbuda Expansion

Expanship's Antigua and Barbuda company formation services are built around the specific compliance demands this jurisdiction places on foreign-owned entities, from satisfying the registered agent requirements under the International Business Corporations Act to managing annual renewal obligations with the Financial Services Regulatory Commission. These are not formalities you can defer. Expanship reduces the operational weight of staying compliant, particularly for businesses managing these requirements remotely.

Our service scope covers the full incorporation and post-incorporation cycle for your business in Antigua and Barbuda:

- Your company registration and corporate document preparation are handled end to end.

- We provide a qualified registered agent and a local office address to meet statutory requirements.

- Our team liaises directly with the FSRC and other relevant government bodies on your behalf.

- Ongoing compliance management keeps your entity in good standing year to year.

- We facilitate introductions to banking institutions familiar with Antiguan corporate structures.

- Tax registration and coordination with local authorities are managed as part of your setup.

Reach out to Expanship Antigua and Barbuda to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The restrictions apply specifically to International Business Companies incorporated under the International Business Corporations Act. An IBC cannot conduct business with Antiguan residents, own real estate in Antigua and Barbuda, or operate as a bank or insurance company without separate licensing. Other entity types, such as a domestic company registered under the Companies Act, operate under a different regulatory framework but lose the tax exemptions that make an IBC attractive.

Failure to pay annual fees to the Intellectual Property and Commerce Office (IPCO) will result in your company being struck off the register. Reinstatement is possible but incurs additional fees and administrative delays. Operating while struck off exposes directors and shareholders to personal liability for obligations incurred during that period.

Ongoing costs include the mandatory registered agent fee, the government's annual renewal fee payable to IPCO, and any local office maintenance charges. Combined, these can range from approximately USD 1,000 to USD 2,500 annually depending on the registered agent's pricing and the level of compliance support required. These figures do not include accounting, audit, or banking fees, which add further to the annual cost base.

Antigua and Barbuda has faced increased monitoring pressure and has appeared on enhanced scrutiny lists, which places it at a disadvantage relative to jurisdictions like the British Virgin Islands or Cayman Islands that have invested more heavily in regulatory infrastructure to satisfy FATF and OECD standards. Correspondent banks and institutional counterparties often apply heightened due diligence to entities from jurisdictions under monitoring, which directly affects your firm's ability to open and maintain bank accounts. The reputational overhang can complicate commercial relationships even where the underlying structure is fully compliant.

No. Under the International Business Corporations Act, maintaining a registered agent with a physical address in Antigua and Barbuda is a statutory requirement, not an optional service. Your entity cannot legally exist on the register without one. Attempting to operate without a compliant registered agent puts the company at risk of administrative dissolution.

Antigua and Barbuda has introduced beneficial ownership registration obligations in response to international pressure, and failure to maintain accurate records can result in fines and potential strike-off of the entity. The specific penalty thresholds are set by the IPCO and can be updated by regulation, so the figures are subject to change. Beyond the formal penalties, non-compliance creates serious obstacles when dealing with banks and institutional counterparties who require clean compliance histories before onboarding.

It disproportionately affects businesses whose primary assets are trademarks, patents, or proprietary technology. A holding company using an Antigua IBC to own IP faces real risk if local enforcement mechanisms are inadequate to deter infringement or if court proceedings are slow to resolve disputes. Businesses that use the structure purely for trading or asset holding unrelated to IP are less exposed to this specific disadvantage.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.