Key Takeaways

- Antigua and Barbuda's International Business Corporations Act establishes a territorial tax framework under which foreign-sourced income is fully exempt from local corporate taxation, making it a structurally sound base for international holding, trading, and consulting operations.

- Statutory privacy protections for shareholders and directors reduce exposure to public disclosure, a meaningful operational advantage for businesses where ownership confidentiality carries legal or commercial weight.

- Registered IBCs face no minimum capital requirements and no restrictions on director nationality, which lowers both the cost and administrative complexity of establishing and maintaining a compliant corporate structure.

- Membership in CARICOM and a legal system grounded in English common law give companies incorporated through the Intellectual Property and Commerce Office access to a predictable contract enforcement environment with established regional credibility.

Antigua and Barbuda is an independent twin-island nation in the Eastern Caribbean, operating as a sovereign state within the Commonwealth with a legal system grounded in English common law. Company registration falls under the oversight of the Intellectual Property and Commerce Office, the authority responsible for corporate filings and registry administration. Foreign businesses looking to establish a presence here most commonly do so through an International Business Company.

The jurisdiction follows a territorial tax posture, meaning income generated outside its borders is generally not subject to local corporate taxation. Foreign ownership of locally registered entities faces no statutory restrictions, and the regulatory framework is structured to permit full foreign control without mandatory local partnership requirements.

This article examines the principal benefits of incorporating in Antigua and Barbuda, drawing on the relevant legislative provisions and registration procedures that shape the experience for international businesses operating through this jurisdiction.

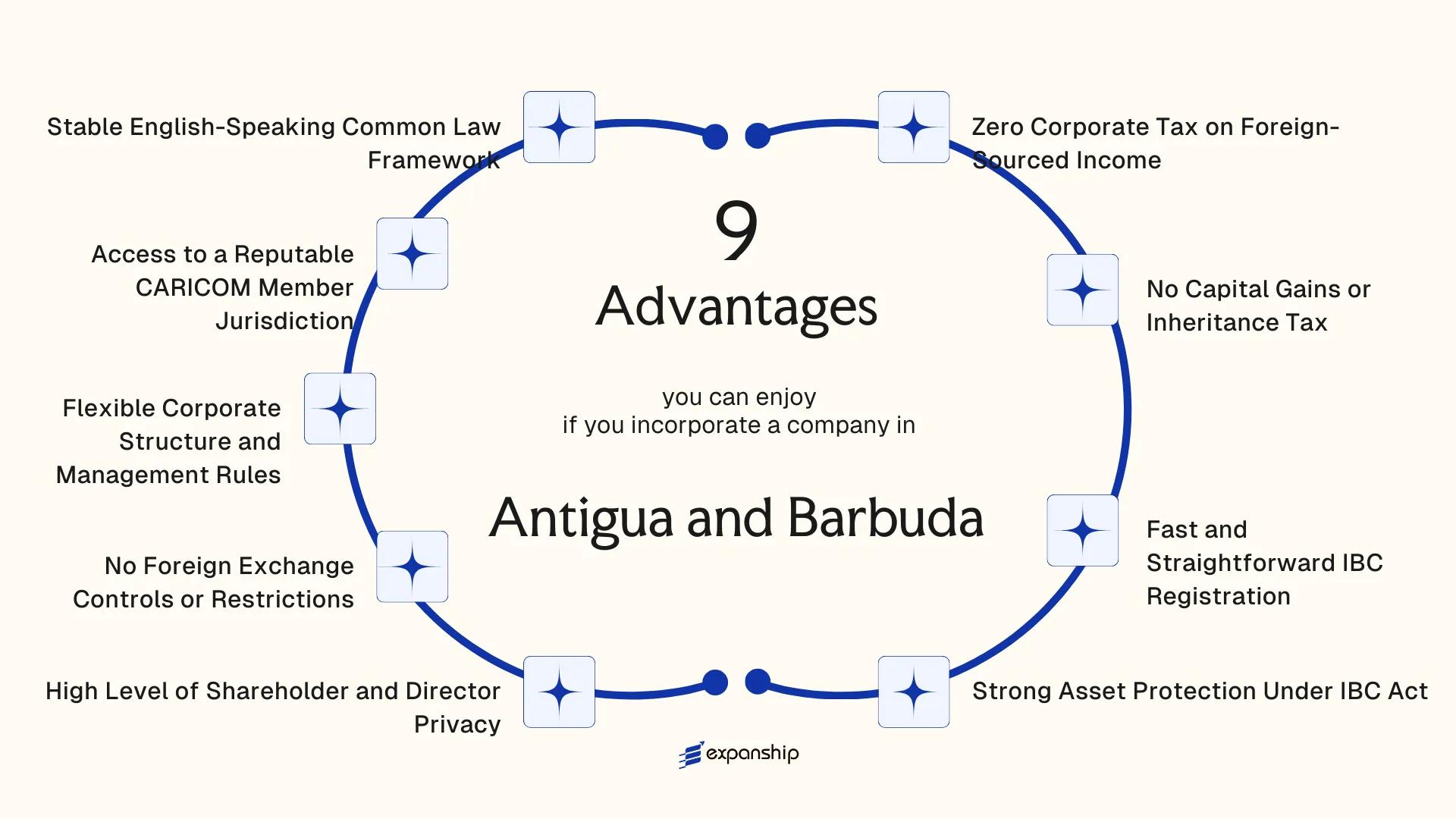

Zero Corporate Tax on Foreign-Sourced Income

Under the International Business Corporations Act (Cap. 222), an IBC registered in Antigua and Barbuda is fully exempt from corporate income tax on profits earned outside the country. This is the structural foundation of the Antigua and Barbuda zero tax on foreign income regime.

What the Exemption Covers

The exemption applies to income derived from foreign sources, meaning revenue generated through business activity conducted outside Antigua. For a firm with international clients, cross-border contracts, or overseas investment returns, no portion of that income is subject to local corporate tax.

Why This Matters Structurally

Most OECD-aligned jurisdictions tax resident companies on worldwide income, with rates ranging from 19% to over 30%. By contrast, an Antigua IBC foreign-sourced income tax exemption effectively removes the local tax burden on qualifying offshore earnings, preserving capital that would otherwise flow to a home-country treasury. The exemption is tied to the source of income, not the residency of shareholders, which gives the structure practical flexibility for multinational arrangements.

Foreign profits earned through your Antigua IBC are not subject to local corporate tax under the IBC Act.

No Capital Gains or Inheritance Tax

Antigua and Barbuda imposes no capital gains tax on profits derived from the disposal of assets held within an International Business Company. Under the International Business Corporations Act, IBCs are explicitly exempt from capital gains levies, meaning profits generated through the sale of shares, securities, real estate held offshore, or other capital assets are not subject to local taxation. For investors actively managing portfolios or executing cross-border transactions, this removes a significant cost that would otherwise erode returns at the point of disposal.

Inheritance and estate transfer are equally unencumbered. No inheritance tax applies to the transfer of IBC shares or assets upon the death of a shareholder, which has direct consequences for succession planning. Wealth accumulated within a corporate structure can pass to designated beneficiaries without a statutory tax event being triggered at the jurisdiction level.

These features combine to create a structurally efficient environment for holding appreciating assets over time. The practical advantages for foreign business owners include:

- Capital gains remain fully retained within the entity rather than being partially remitted to local tax authorities

- Generational wealth transfer through an IBC does not create an automatic tax liability in the jurisdiction

- Share disposals and corporate restructurings can be executed without triggering a local taxable event

- Estate planning arrangements can be built around the IBC without requiring complex tax-mitigation overlays

The exemptions under the IBC Act apply to qualifying foreign-owned entities conducting business outside the jurisdiction.

Incorporate an IBC in Antigua and Barbuda

Register your International Business Company in Antigua and Barbuda and benefit from capital gains and inheritance tax exemptions under the IBC Act.

Fast and Straightforward IBC Registration

Antigua and Barbuda IBC registration advantages begin with how quickly your business can become legally operational. Under the International Business Corporations Act, an IBC can typically be incorporated within one to two business days once documentation is submitted to the Registrar of Companies. For businesses that need to open bank accounts, sign contracts, or respond to time-sensitive commercial opportunities, that speed carries real operational value.

The process does not require you to be physically present. A licensed registered agent based in Antigua and Barbuda handles the filing on your behalf, which means your entity can be formed remotely without delays tied to travel or in-person appointments. This structure suits foreign owners managing operations across multiple time zones.

| Parameter | Detail |

|---|---|

| Governing Legislation | International Business Corporations Act |

| Typical Incorporation Timeline | 1 to 2 business days |

| Minimum Shareholders Required | 1 |

| Minimum Directors Required | 1 |

| Physical Presence Required | No |

| Registered Agent Required | Yes, must be locally licensed |

A single shareholder and one director are sufficient to form a valid IBC, and both roles can be held by the same individual. There is no requirement for local directors or resident shareholders. Documentation requirements are straightforward, generally consisting of identification, proof of address, and a memorandum and articles of incorporation filed through your registered agent. This low administrative threshold means your firm spends less time on formation procedures and more time conducting actual business.

Strong Asset Protection Under IBC Act

The International Business Corporations Act (IBC Act) of Antigua and Barbuda provides a statutory framework specifically designed to protect the assets of foreign-owned entities from external claims. Under this legislation, an IBC's assets are shielded from foreign court judgments unless those judgments are re-litigated and proven valid under local jurisdiction. This matters because a creditor who secures a ruling against your business in another country cannot automatically enforce that judgment against assets held within an Antigua IBC.

The IBC Act also restricts fraudulent transfer claims. Creditors must generally demonstrate that an asset transfer into the IBC structure was made with intent to defraud — and that claim must be established within a defined limitation period. This places a meaningful procedural burden on any party attempting to reach assets held under the structure.

Keep these points in mind:

- Asset protection applies only to foreign-sourced income and offshore operations; domestic Antiguan business activity is not covered.

- Transfers made shortly before a known creditor claim may be subject to challenge under fraudulent conveyance provisions.

- Protection is strongest when the IBC structure is established before any dispute arises, not in response to one.

- The entity must remain in good standing under the IBC Act for protections to remain operative.

An Antigua IBC can hold shares in other offshore entities, allowing multi-layered asset segregation across jurisdictions within a single holding structure.

High Level of Shareholder and Director Privacy

Antigua and Barbuda shareholder privacy benefits are grounded in statute, not discretionary policy. Under the International Business Corporations Act (Cap. 222), neither the names of shareholders nor the details of directors are filed with any public registry. That structural exclusion means ownership information stays outside public reach by default, without requiring additional legal arrangements.

What the IBC Act Withholds from Public Disclosure

The Registrar of Companies in Antigua maintains corporate records, but the IBC framework does not require beneficial ownership to appear in publicly accessible filings. Your company's register of members and directors is held internally, accessible only to authorized parties. For a foreign business owner, this means competitors, counterparties, and general public searches cannot trace equity ownership back to you through local registry data.

Antigua IBC director confidentiality advantages extend further through the lawful use of nominee arrangements. Nominee shareholders and directors are permitted under the IBC Act, allowing a third party to appear on any required documentation in place of the beneficial owner. A formal nominee agreement governs the relationship and preserves your control, while the public-facing record reflects the nominee's details rather than yours.

Practical Value of Structural Privacy

Privacy of this nature is particularly relevant for business owners operating in jurisdictions where disclosed ownership can create legal exposure, reputational risk, or competitive disadvantage. The statutory basis for confidentiality under Cap. 222 means protection is not dependent on administrative discretion — it is written into the governing legislation itself.

Understand Your Privacy Protections Before You Incorporate in Antigua and Barbuda

Speak with an Expanship specialist to understand exactly how shareholder and director confidentiality applies to your structure under the IBC Act.

No Foreign Exchange Controls or Restrictions

Antigua and Barbuda imposes no foreign exchange controls or restrictions on International Business Companies. Under the International Business Corporations Act, an IBC registered in the jurisdiction can hold accounts in any currency, move funds across borders freely, and repatriate profits without seeking prior approval from any regulatory authority.

For a foreign business owner, this has direct operational consequences:

- Your company can receive payments in USD, EUR, GBP, or any other currency without conversion mandates or central bank reporting thresholds that would otherwise reduce net receipts.

- Capital contributed to the IBC can be returned to shareholders or parent entities without withholding at source or bureaucratic clearance processes, reducing the cost and time of intercompany fund movements.

- Treasury functions, such as holding multicurrency reserves or routing working capital across subsidiaries in different countries, can be managed from within a single IBC structure without triggering currency control compliance obligations.

- There is no requirement to maintain a local bank account denominated in Eastern Caribbean Dollars, giving your firm full discretion over banking arrangements and currency exposure.

This freedom applies specifically to IBCs engaged in business conducted outside the jurisdiction. Entities operating domestically fall under a different regulatory scope and would not carry the same unrestricted status.

Flexible Corporate Structure and Management Rules

Under the International Business Corporations Act (Cap. 222), an Antigua and Barbuda flexible IBC corporate structure permits a single individual to serve simultaneously as the sole director and sole shareholder. For foreign owners operating lean international operations, this eliminates the need to appoint nominee officers or maintain a local board, reducing both administrative overhead and recurring costs.

The IBC Act places no nationality or residency requirements on directors or shareholders. Your company can be governed entirely by foreign nationals, which matters when you need operational continuity across different time zones without anchoring decision-making to a local representative.

Shareholder meetings and director meetings may be held anywhere in the world, or conducted by written resolution without convening at all. That procedural flexibility allows a sole founder to execute corporate decisions without scheduling formal meetings, which is a practical advantage for businesses with no physical office presence.

Shares may be issued in multiple classes with varying rights, including non-voting shares, preference shares, and redeemable shares, all configurable within the articles of incorporation. This gives founders meaningful control over equity distribution and capital structuring from the outset.

A foreign-owned IBC with a single director-shareholder, no residency requirements, and no mandatory annual general meeting faces significantly lower governance costs than a comparable entity in most EU jurisdictions, where multi-member boards, local registered officers, and formal AGMs are often statutory requirements.

Access to a Reputable CARICOM Member Jurisdiction

Antigua and Barbuda CARICOM membership benefits extend beyond regional trade. As a full member of the Caribbean Community, businesses incorporated here operate within a framework that carries institutional recognition across 15 member states, including Jamaica, Trinidad and Tobago, and Barbados.

Under the CARICOM Single Market and Economy (CSME), eligible companies gain access to the free movement of goods, services, capital, and skilled labor across participating member states. For a foreign business owner, this means a single corporate structure can support commercial activity across multiple Caribbean markets without requiring separate registrations in each territory.

CARICOM membership also lends reputational weight. The jurisdiction participates in regional bodies such as the Caribbean Court of Justice and aligns with standards set by the Caribbean Financial Action Task Force (CFATF), which strengthens the credibility of entities formed here in the eyes of international counterparties and financial institutions.

- Full CARICOM membership since the organization's founding in 1973

- Access to CSME provisions for qualifying business activities

- Recognition under CFATF-aligned AML/CFT frameworks

CSME benefits apply to qualifying entities and nationals; not all IBC structures automatically receive full single market access, so eligibility should be confirmed against current CARICOM protocols.

Stable English-Speaking Common Law Framework

Antigua and Barbuda common law framework benefits begin with legal predictability. The country inherited its legal system from English common law, which remains the governing tradition for commercial and civil matters. For a foreign business owner, this means contracts, corporate governance, and dispute resolution operate within a framework whose principles are widely understood by lawyers, courts, and counterparties across dozens of jurisdictions.

English as the Sole Official Language

All legislation, court proceedings, and regulatory filings are conducted in English. This eliminates the translation costs and interpretation risks that arise in civil law jurisdictions operating in other languages. Contracts drafted in English carry their intended meaning without passing through a foreign legal tradition.

Common Law Familiarity for International Counterparties

Foreign investors from the UK, Canada, Australia, and the United States will find the underlying legal concepts directly transferable. Concepts such as fiduciary duty, beneficial ownership, and corporate veil are applied consistently with established English common law precedent. Banks and institutional counterparties in those markets are more likely to recognize and accept corporate structures formed under familiar legal principles.

Judicial Framework and Institutional Stability

The Eastern Caribbean Supreme Court serves as the superior court for civil and commercial matters, with appeals available to the Caribbean Court of Justice or the Privy Council in London. Access to an appellate body with international standing provides a credible enforcement path for contractual disputes, which matters when third parties are assessing counterparty risk in cross-border transactions.

Why Antigua and Barbuda Stands Out Among Offshore Jurisdictions

Three Caribbean jurisdictions dominate the conversation when foreign investors consider offshore incorporation in the region: the British Virgin Islands, the Cayman Islands, and Antigua and Barbuda. The BVI and Cayman are older, higher-volume markets, but volume alone does not determine suitability. For businesses that prioritise CARICOM membership, common law protections, and no foreign exchange controls, the comparison shifts considerably.

What the table below reveals is not simply competitive parity but a distinct positioning. Antigua and Barbuda top offshore jurisdiction advantages become clearer when measured against jurisdictions targeting identical investor profiles. The International Business Corporations Act underpins several parameters in this comparison, and its provisions hold up well against equivalent legislation in competing markets.

| Parameter | Antigua and Barbuda | British Virgin Islands | Cayman Islands |

|---|---|---|---|

| Corporate Tax on Foreign Income | 0% | 0% | 0% |

| Capital Gains Tax | None | None | None |

| CARICOM Membership | Yes | No | No |

| Exchange Controls | None | None | None |

| Common Law Framework | Yes | Yes | Yes |

| Director Privacy | High | High | Moderate |

| Shareholder Register Public | No | No | Yes (partial) |

| Annual Government Fee Structure | Low to moderate | Moderate to high | High |

| IBC Legislative Framework | IBC Act (Cap. 222) | BCA 2004 | Companies Law (2023 Revision) |

Compliance Services for Companies in Antigua and Barbuda

Stay current with annual filing obligations, registered agent requirements, and regulatory deadlines under the IBC Act.

Conclusion

Antigua and Barbuda presents a coherent case for foreign business owners who want a tax-neutral, English-language jurisdiction with a codified legal framework and a credible regional standing. The combination of zero tax on foreign-sourced income under the International Business Corporations Act and strong statutory privacy protections makes the IBC structure particularly well-suited to holding, trading, and consulting operations that generate income outside the territory.

The common law foundation, drawn from English legal tradition, gives your business access to predictable contract enforcement and settled corporate law principles without the uncertainty that can accompany civil law systems. For entities that require structural flexibility, the absence of minimum capital requirements and the freedom to appoint directors of any nationality add practical utility that directly reduces setup and operational friction.

Whether the jurisdiction fits your specific situation depends on your industry, the nature of your income flows, and any reporting obligations in your home country. The benefits of incorporating in Antigua and Barbuda are most pronounced for businesses with genuinely international operations and income that originates outside its borders. Getting the structure right from the outset, including correct classification of income and proper maintenance of statutory records, determines how effectively those advantages translate into real outcomes.

Start Your Antigua and Barbuda Company with Expanship Today

Expanship handles the full cycle of IBC formation in Antigua and Barbuda, from preparing and legalizing corporate documents to filing directly with the Intellectual Property and Commerce Office (IPCO), which administers IBC registrations under the International Business Corporations Act. The benefits covered in this blog — tax exemptions on foreign-sourced income, director privacy, asset protection provisions, and the absence of foreign exchange controls — each carry specific compliance requirements that must be met and maintained annually to preserve their legal effect.

Expanship's services for your IBC formation and ongoing compliance include:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Antigua and Barbuda

- Filing and liaison with IPCO on your behalf

- Post-incorporation compliance management, including annual return filings

- Corporate secretarial support for ongoing governance requirements

- Banking introduction assistance for business account setup

To discuss your incorporation requirements with Expanship Antigua and Barbuda, contact the team directly.

Frequently Asked Questions (FAQ)

IBCs that derive income exclusively from sources outside Antigua and Barbuda are exempt from corporate income tax under the International Business Corporations Act. This exemption is a defined feature of the IBC regime, not a discretionary concession. The exemption does not automatically extend to income earned within the local market, so the source of revenue is the determining factor.

The International Business Corporations Act does not impose a residency requirement on directors or shareholders. A single individual can serve as both the sole director and sole shareholder of an IBC. There is no statutory minimum requiring any officer or equity holder to be a citizen or resident of the jurisdiction.

Registration under the IBC Act can generally be completed within a few business days once the required documentation is submitted to the Registrar of Companies. The timeline may extend if supporting documents require notarization or apostille certification. Formation timelines are generally shorter than those in many onshore jurisdictions given the streamlined statutory process.

Under the IBC Act, details of shareholders and directors are not part of the public registry record, which means third parties cannot access this information through a standard registry search. Confidentiality is a statutory feature of the IBC structure rather than a discretionary arrangement. Disclosure obligations may arise under mutual legal assistance treaties or in response to a valid court order.

Antigua and Barbuda does not impose foreign exchange controls on IBCs, and the IBC Act places no restriction on the currencies an entity may use for international transactions. An IBC may hold multi-currency bank accounts and move funds across borders without seeking regulatory approval from a local authority. This applies to both capital transfers and operating payments made in connection with foreign business activities.

CARICOM membership primarily benefits companies engaged in trade or investment within the Caribbean Single Market and Economy, rather than pure offshore IBCs focused on external markets. An IBC conducting business exclusively outside the region does not automatically access CARICOM trade preferences, as those apply to entities engaged in intra-regional commerce. The membership does, however, contribute to the jurisdiction's standing within established regional legal and regulatory frameworks.

The IBC Act, together with the broader legal framework governing companies in Antigua and Barbuda, provides structural separation between the assets held within a properly constituted IBC and the personal liabilities of its shareholders. This separation means that, absent fraud or improper conduct, creditors of a shareholder generally cannot reach assets held at the corporate level. The enforceability of these protections in cross-border disputes depends on the applicable private international law rules in the creditor's jurisdiction.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.