Key Takeaways

- Antigua and Barbuda's Financial Services Regulatory Commission (FSRC) oversees corporate registration across all entity types, including the International Business Corporation, Private Limited Company, and LLC.

- The International Business Corporation (IBC) is the most registered structure in Antigua and Barbuda, designed for non-resident entrepreneurs seeking tax-neutral treatment on foreign-sourced income under the jurisdiction's territorial tax system.

- Limited partnerships in Antigua and Barbuda allow passive investors to cap their liability exposure, distinguishing them from general partnerships where all partners carry unlimited joint liability.

- Branch and representative offices provide foreign companies with a registered presence in Antigua and Barbuda without requiring the incorporation of a separate legal entity.

Introduction to Entity Types in Antigua and Barbuda

Antigua and Barbuda is a two-island nation in the eastern Caribbean, situated in the Lesser Antilles between the islands of Saint Kitts and Nevis to the west and Barbuda to the north. It is an independent sovereign state and a member of the Commonwealth, with English common law forming the foundation of its legal system.

Understanding the available business entity types in Antigua and Barbuda starts with knowing which authority oversees registration. The Financial Services Regulatory Commission (FSRC) administers corporate registration and licensing, with the Registrar of Companies handling the formal incorporation of local entities.

From a tax standpoint, the jurisdiction operates a territorial tax system, and certain entity types — most notably the International Business Corporation — are structured to carry no tax liability on foreign-sourced income.

Antigua and Barbuda corporate structures available to residents and non-residents include the International Business Corporation (IBC), Public Limited Company, Private Limited Company, Limited Liability Company (LLC), General Partnership, Limited Partnership, Branch Office, Representative Office, and Sole Proprietorship. Each structure carries distinct registration requirements, ownership rules, and compliance obligations that this article examines in turn.

An Overview of Business Structures in Antigua and Barbuda

Antigua and Barbuda recognises several distinct entity types under its company law framework, with the principal legislation being the Companies Act (Cap. 79) for domestic entities and the International Business Corporations Act (Cap. 222) for offshore structures. Each entity type carries different implications for liability, taxation, ownership, and permitted activities. The sections that follow examine each structure in full.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| IBC | Corporation | Limited | Exempt | No | 1 shareholder | Financial Services Regulatory Commission | IBC Act (Cap. 222) |

| Public Limited Company | Corporation | Limited | Taxed | Yes | 7 shareholders | Registrar of Companies | Companies Act (Cap. 79) |

| Private Limited Company | Corporation | Limited | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Act (Cap. 79) |

| LLC | Hybrid entity | Limited | Taxed | Yes | 1 member | Registrar of Companies | Companies Act (Cap. 79) |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | Registrar of Companies | Partnership Act |

| Branch Office | Foreign entity | Parent liable | Taxed | Yes | N/A | Registrar of Companies | Companies Act (Cap. 79) |

| Representative Office | Foreign entity | Parent liable | Exempt | No | N/A | Registrar of Companies | Companies Act (Cap. 79) |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | Registrar of Companies | Business Names Act |

Each of these structures is examined in full in the sections below.

International Business Corporation (IBC) in Antigua and Barbuda

Meeting Antigua IBC registration requirements is governed by the International Business Corporations Act, Cap. 222 (originally enacted in 1982 and subsequently amended). Under this legislation, an IBC is a distinct legal entity, meaning it can hold assets, enter contracts, and incur liabilities in its own name.

The structure combines limited liability protection for shareholders with considerable operational flexibility. It is classified as a hybrid offshore vehicle — capable of conducting international business while being restricted from trading within the domestic market.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (separate legal personality) | Governed by the IBC Act, Cap. 222 |

| Members & Officers | Minimum 1 shareholder; minimum 1 director; no maximum | Shareholders and directors may be the same person; corporate directors are permitted |

| Local Presence | Registered agent required; no requirement for a local office | Registered agent must be licensed in Antigua and Barbuda |

| Capital | No statutory minimum share capital; shares may be denominated in any currency | Par value and no-par-value shares both permitted |

| Privacy | Shareholder and director names are not part of the public register | Nominee services are commonly used |

| Restrictions | Prohibited from conducting business with residents or owning local real estate without special permission | Cannot engage in banking, insurance, or trust business without a separate licence |

Focus Points

- Taxation: IBCs are exempt from corporate income tax, withholding tax, and stamp duty on transactions conducted outside the jurisdiction for a defined period from incorporation; VAT does not apply to offshore activities.

- Economic Substance: IBCs engaged in relevant activities as defined under Antigua and Barbuda's economic substance legislation may be required to demonstrate adequate local substance.

- Annual Compliance: Annual renewal fees are payable to maintain good standing; financial statements are not required to be filed publicly.

- Treaty Access: Antigua and Barbuda has a limited tax treaty network, which restricts IBC access to double taxation relief in many jurisdictions.

- Conversion: An IBC may be continued or re-domiciled from or to another jurisdiction under the Act's continuance provisions.

Closing

An International Business Corporation suits holding structures, international trading operations, and intellectual property ownership where cross-border activity is conducted entirely outside the domestic market. The absence of a minimum capital requirement lowers the entry threshold, though the restricted treaty network limits its utility for structures that depend on treaty-based withholding tax reductions.

An IBC is best suited for non-resident entrepreneurs and international holding groups seeking a tax-neutral structure for offshore asset management or cross-border trade, provided they do not require access to an extensive double tax treaty network.

Company Incorporation in Antigua and Barbuda

Incorporate an IBC or other entity type in Antigua and Barbuda with full compliance support.

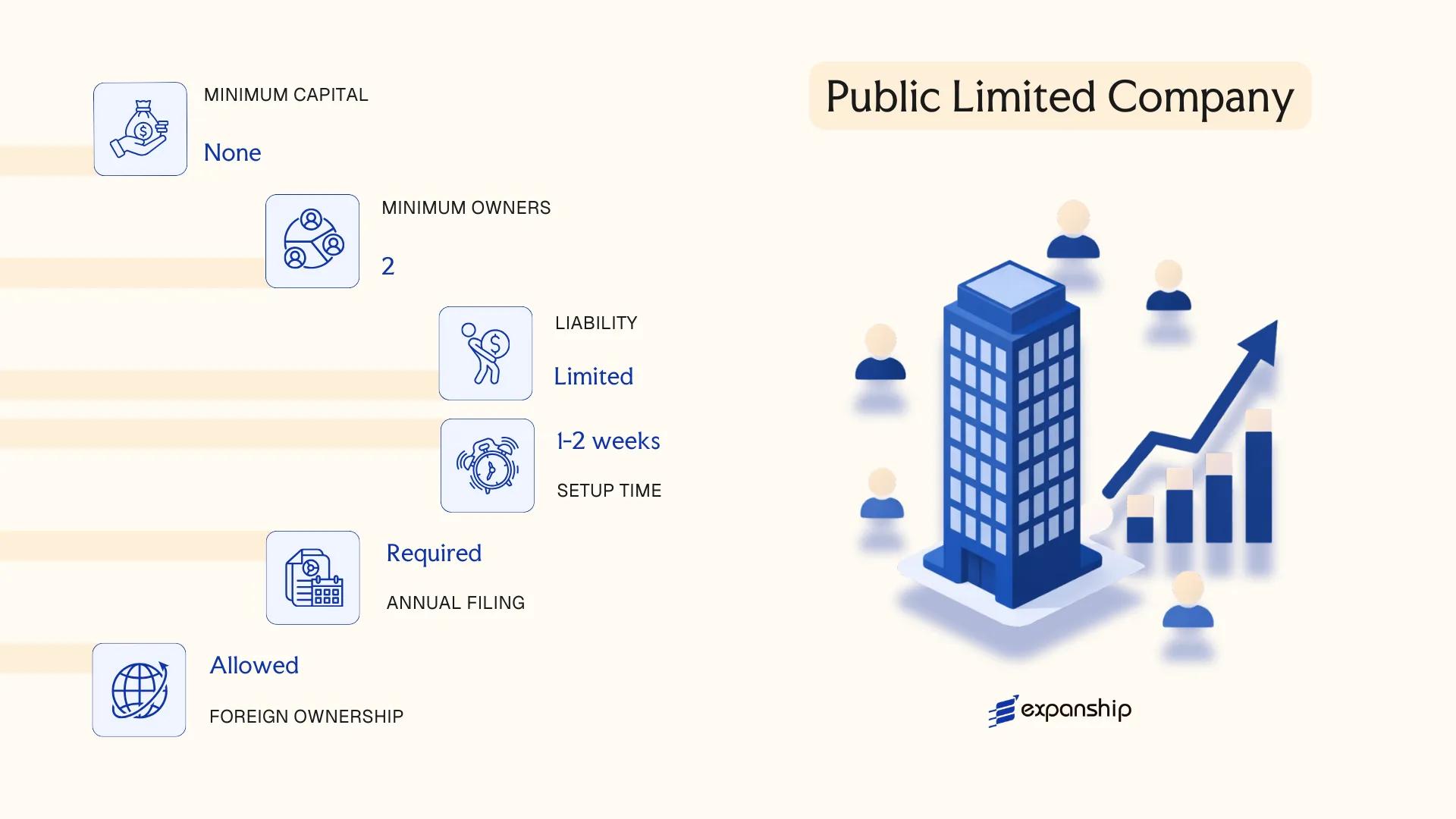

Public Limited Company in Antigua and Barbuda

A public limited company in Antigua and Barbuda is governed by the Companies Act, Cap. 249 of the Laws of Antigua and Barbuda, which provides the statutory framework for its formation and ongoing operation. As a separate legal entity, it carries limited liability for its shareholders and is distinguished from private companies primarily by its ability to offer shares to the general public.

Public offer capacity makes this structure suitable for larger enterprises requiring access to capital markets, though listing obligations add a layer of regulatory accountability that private structures do not carry.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company (separate legal person) | Incorporated under Companies Act, Cap. 249 |

| Members | Shareholders; minimum 1 shareholder, no maximum | Directors separate; minimum 1 director required |

| Local Presence | Registered office in Antigua and Barbuda required | Registered agent not mandatory under the same rules as an IBC |

| Capital | No statutory minimum share capital; denominated in Eastern Caribbean dollars or any currency | Shares may be offered to the public |

| Privacy | Shareholder and director information filed with the Registrar of Companies; publicly accessible | Less privacy than private structures |

| Securities Regulation | Public offerings subject to oversight by the Financial Services Regulatory Commission (FSRC) | Prospectus requirements apply for public share issuance |

Focus Points

- Taxation: Subject to corporate income tax; no capital gains tax; stamp duty applies to share transfers; VAT may apply depending on business activities; withholding tax applies to dividends paid to non-residents.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Registrar of Companies.

- Economic Substance: Entities conducting relevant activities must satisfy economic substance requirements under the Economic Substance (Companies and Limited Partnerships) Act, 2019.

- Conversion: A public company may be re-registered as a private company subject to shareholder approval and Registrar confirmation under the Companies Act.

- Restrictions: Cannot restrict the transfer of its shares; public offerings require FSRC compliance, including prospectus filing.

Closing

A public limited company suits enterprises seeking to raise capital through public share issuance, including operating businesses targeting institutional or retail investors. The ability to list shares is a structural advantage, though the associated disclosure obligations and regulatory compliance burden are considerably higher than those of a private firm.

This structure is best suited for established businesses with significant capital requirements that intend to access public markets or attract a broad investor base in or from Antigua and Barbuda.

Private Limited Company in Antigua and Barbuda

A private limited company in Antigua and Barbuda is governed by the Companies Act, Cap. 79 of the Laws of Antigua and Barbuda. It exists as a separate legal entity, meaning the company holds its own rights, obligations, and liabilities distinct from its shareholders.

Liability exposure for shareholders is capped at the value of their unpaid share capital. This structure suits businesses seeking a locally recognized, domestically oriented corporate form rather than an offshore vehicle.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Cannot offer shares to the general public |

| Members | Shareholders (min. 1, max. 50) | Directors min. 1; no residency requirement for directors or shareholders |

| Local Presence | Registered office address required in Antigua and Barbuda | A registered agent is standard practice |

| Capital | Eastern Caribbean Dollar (XCD); no statutory minimum | Shares must be issued upon incorporation |

| Privacy | Shareholder details filed with the Intellectual Property and Commerce Office (IPCO) | Not publicly indexed in a searchable registry |

Focus Points

- Taxation: No corporate income tax, no capital gains tax, no withholding tax on dividends; stamp duty may apply to certain instruments.

- Annual Compliance: Annual return and financial statements must be filed with IPCO; a local registered office must be maintained continuously.

- Economic Substance: Domestic private companies are not subject to the economic substance requirements applicable to IBCs.

- Restrictions: Share transfers are restricted by the articles of association; public subscription of shares is prohibited.

- Conversion: A private company may re-register as a public company under the Companies Act if statutory thresholds and procedural requirements are met.

Closing

A private limited company suits local trading, service businesses, and holding structures where domestic legal recognition is a priority. The single-member option lowers the formation threshold, though the restriction on public share issuance limits future capital-raising options.

Best suited for resident entrepreneurs, domestic trading businesses, or foreign investors establishing a locally incorporated operating entity in Antigua and Barbuda.

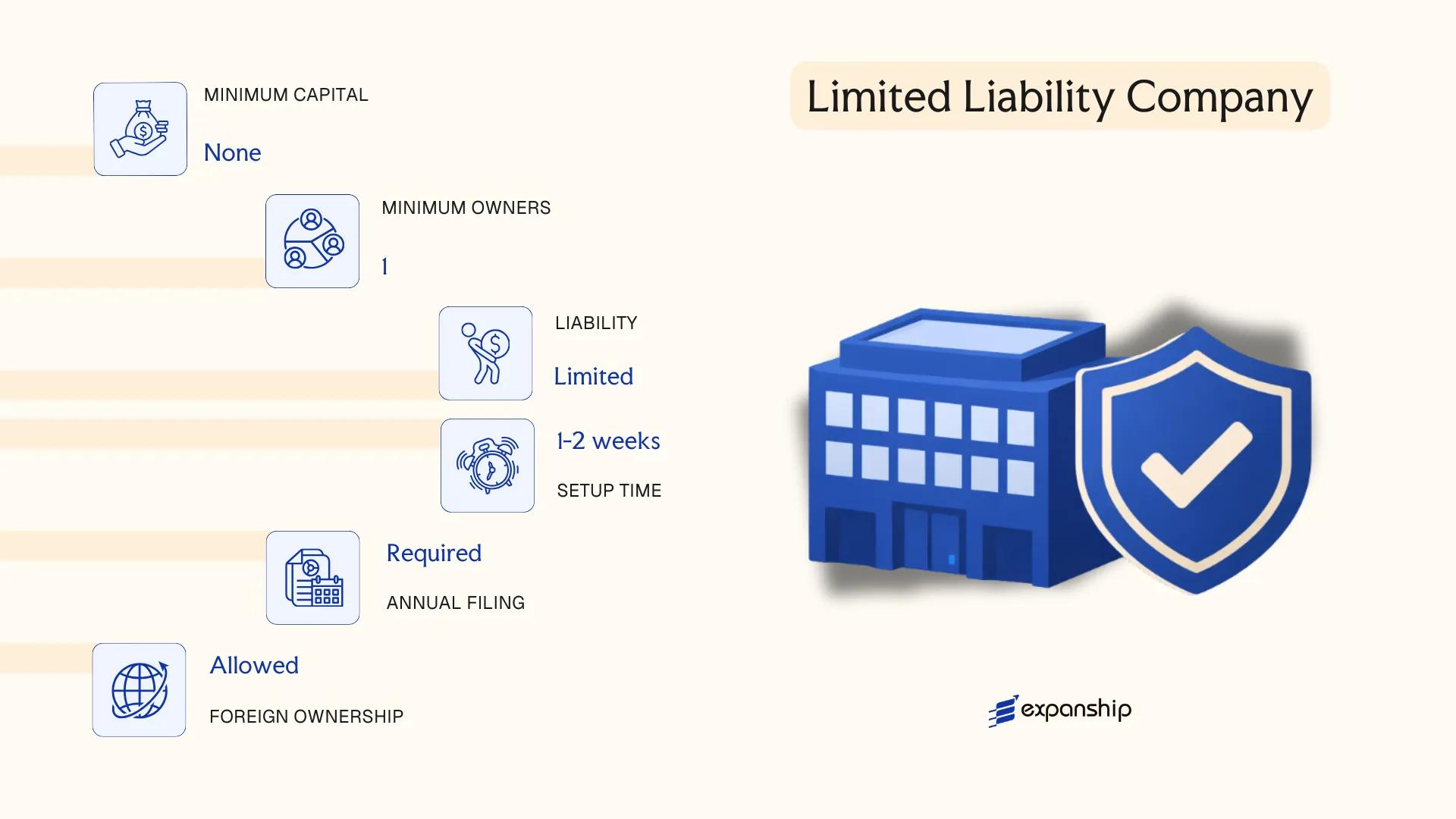

Limited Liability Company (LLC) in Antigua and Barbuda

Antigua and Barbuda does not maintain a standalone LLC statute in the same form as many common law jurisdictions. The LLC formation Antigua and Barbuda framework is instead derived from the Companies Act (Cap. 79), which governs limited liability structures more broadly, with members enjoying protection from personal liability beyond their capital contribution.

As a hybrid structure, the LLC combines the liability shield of a corporation with pass-through flexibility in certain configurations. The entity holds separate legal personality, meaning it can own assets, enter contracts, and incur obligations in its own name, independent of its members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Governed under the Companies Act (Cap. 79) |

| Members | Minimum 1; no statutory maximum | Members hold ownership interests; managers may be appointed separately |

| Local Presence | Registered Agent and Registered Office required | Must be maintained continuously within the jurisdiction |

| Capital | No mandated minimum share capital; Eastern Caribbean Dollar (XCD) | Capital structure is flexible at incorporation |

| Privacy | Member details not on public register in standard filings | Beneficial ownership reported to authorities, not publicly disclosed |

Focus Points

- Taxation: No corporate income tax, capital gains tax, or withholding tax on distributions; VAT applies to domestic transactions at the standard rate; stamp duty may apply on certain instruments.

- Economic Substance: Entities conducting relevant activities are subject to the Economic Substance Act, 2019 and must demonstrate adequate local substance.

- Annual Compliance: Annual returns must be filed with the Antigua and Barbuda Intellectual Property and Commerce Office (ABIPCO).

- Treaty Access: Antigua and Barbuda has a limited tax treaty network, which may restrict access to reduced withholding rates in counterparty jurisdictions.

- Restrictions: LLCs engaged in certain regulated sectors, including banking and insurance, require additional licensing from the Financial Services Regulatory Commission (FSRC).

Closing

The LLC structure suits holding arrangements, investment vehicles, and asset-owning entities where liability separation is the primary objective, though its limited treaty network restricts utility for active trading operations requiring double tax relief.

Best suited for investors and entrepreneurs seeking a flexible, liability-protected structure for holding assets or conducting non-regulated business without requiring access to an extensive treaty network.

Partnerships in Antigua and Barbuda [General Partnership, Limited Partnership]

Partnership registration Antigua Barbuda is governed by the Partnership Act, which establishes the framework for both general and limited partnerships. Neither structure carries separate legal personality under the Act, meaning partners bear direct exposure to the firm's obligations.

Liability exposure differs significantly between the two forms. In a general partnership, all partners carry unlimited personal liability for the debts of the business. A limited partnership introduces a two-tier structure, separating general partners who manage the firm and accept full liability from limited partners whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business association | No separate legal personality |

| Partners | General Partners (GP), Limited Partners (LP) | GP: min. 1, unlimited; LP: min. 1 in a limited partnership |

| Local Presence | Registered office address required | Registered agent recommended for compliance |

| Capital | No statutory minimum; no prescribed currency | Capital contributions defined in partnership agreement |

| Privacy | Partner details filed with the registry | Beneficial ownership obligations apply |

Focus Points

- Taxation: Partnerships are generally treated as tax-transparent; partners are taxed individually on their share of profits, and no corporate tax applies at the entity level.

- Annual Compliance: Annual renewal filings and fee payments are required to maintain good standing with the Antigua and Barbuda Companies Registry.

- Economic Substance: Trading partnerships with foreign-sourced income should assess whether substance requirements apply under local economic substance legislation.

- Treaty Access: Partnerships, lacking corporate status, may face restrictions accessing double tax treaty benefits available to incorporated entities.

- Conversion: A general partnership may be converted to a limited partnership by registering a partnership agreement that designates limited partners and their capital contributions.

Sub-Types

General Partnership

Every partner in this structure participates in management and carries unlimited personal liability. It is typically used by small professional practices or domestic trading operations where all principals are actively involved.

Limited Partnership

A limited partnership separates management from passive investment. General partners run the business and accept full liability, while limited partners contribute capital without taking on management responsibilities, making this structure common for investment vehicles and project financing arrangements.

Partnerships suit joint ventures, professional services, and domestic trading arrangements where formal corporate structure is unnecessary or cost-prohibitive. The tax-transparent treatment simplifies profit distribution, but unlimited liability for general partners remains a material drawback for higher-risk commercial activities.

Partnerships in Antigua and Barbuda are best suited for small professional firms, domestic joint ventures, or investment arrangements where two or more parties seek a straightforward operating structure without corporate formalities.

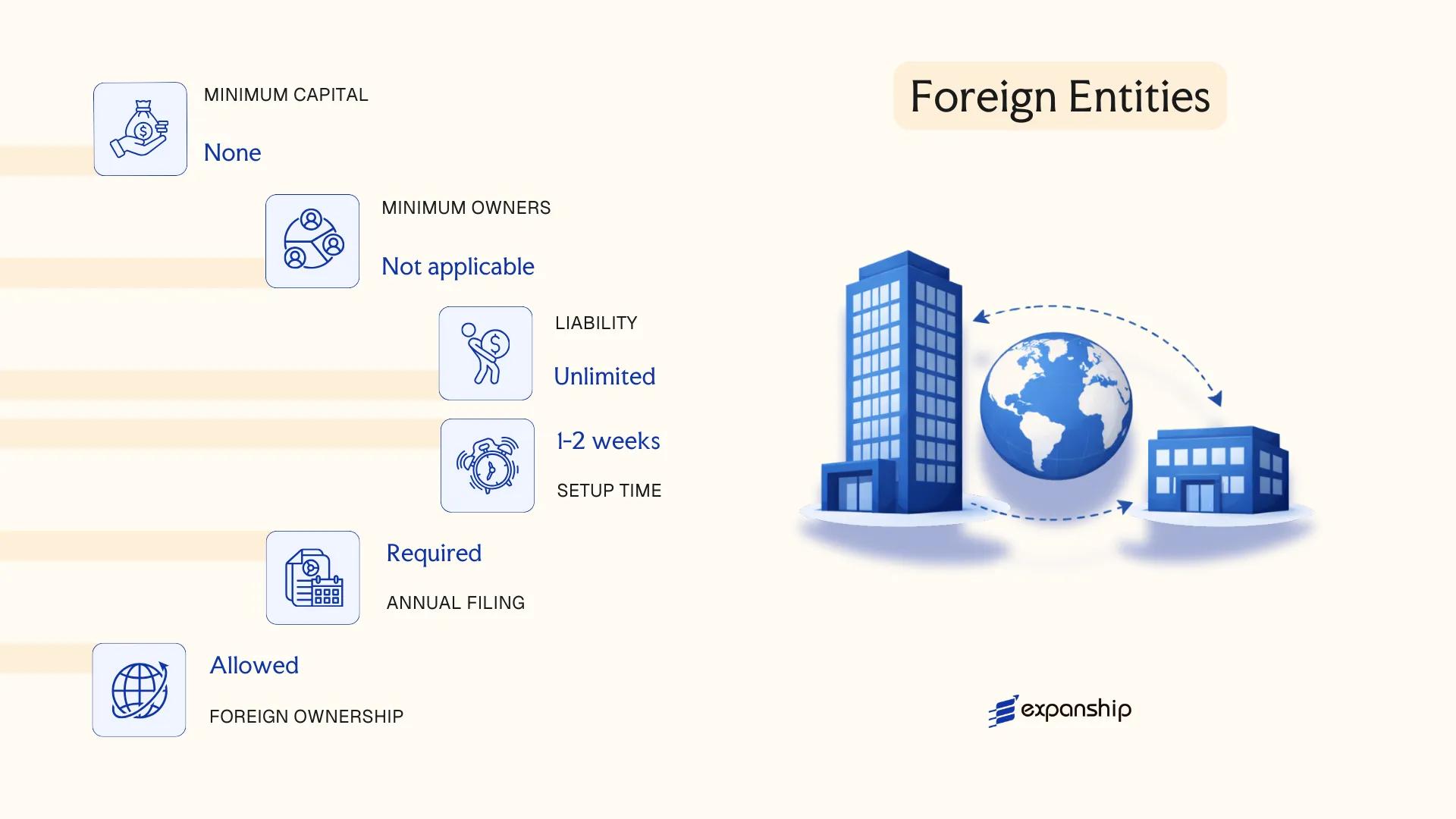

Foreign Entities in Antigua and Barbuda [Branch Office, Representative Office]

Foreign companies seeking a physical presence without incorporating a new local entity can register as a foreign company under the Companies Act 1995. A foreign company branch office Antigua registration does not create a separate legal entity — the parent company remains fully liable for all obligations incurred through the branch. This distinction has direct implications for liability exposure and governance structure.

Registration of foreign entities is administered through the Intellectual Property and Commerce Office (IPCO). Both branch offices and representative offices must file with IPCO, though their permitted activities differ significantly.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch or Representative Office | Neither is a separate legal entity from the parent |

| Parent Liability | Unlimited | The foreign parent bears full legal and financial responsibility |

| Local Presence | Registered Agent required | A local registered address must be maintained at all times |

| Authorized Representative | At least one local agent or officer | Must be appointed and notified to IPCO |

| Capital Requirement | None prescribed | No minimum capital injection required for registration |

| Privacy | Parent company documents filed publicly | Memorandum, articles, and directors disclosed to IPCO |

Focus Points

- Taxation: Branches are generally subject to the same tax treatment as locally incorporated companies on Antiguan-source income; no separate withholding tax regime applies specifically to branches, though stamp duty may apply to transactions.

- Economic Substance: Foreign entities conducting relevant activities may be subject to economic substance requirements under the Economic Substance Act.

- Annual Compliance: Annual returns and updated parent company documents must be filed with IPCO to maintain active status.

- Permitted Activities: Representative offices are restricted to non-commercial activities such as market research and liaison; revenue-generating operations require branch registration.

- Conversion: Neither structure can be directly converted into a locally incorporated company without a separate incorporation process.

Sub-Types

Branch Office

A branch office operates as a direct extension of the foreign parent and may conduct full commercial activities within the jurisdiction. It is suited to companies requiring an operational presence — executing contracts, generating local revenue, or employing staff — while maintaining a single consolidated corporate structure.

Representative Office

A representative office is limited to promotional, liaison, or research activities and cannot enter into commercial contracts or earn local income. This structure is typically used by foreign firms conducting preliminary market assessment before committing to a full operational setup.

Closing Remarks

Registering a foreign entity suits companies that need a formal presence without the administrative overhead of local incorporation, though the absence of limited liability for branch operations represents a significant structural risk. A representative office removes commercial risk but also removes commercial capability.

Foreign companies testing the local market or maintaining a liaison function, where full incorporation is not yet warranted.

Sole Proprietorship in Antigua and Barbuda

A sole proprietorship in Antigua and Barbuda is the most elementary business structure available, governed primarily by the Business Names Act. Unlike a company, the business has no separate legal personality — the proprietor and the business are the same legal entity, meaning personal assets are directly exposed to business liabilities.

Registration is handled through the Intellectual Property and Commerce Office (IPCO). Where the business operates under a name other than the proprietor's own, that name must be registered as a business name under the Business Names Act. Sole trader registration in Antigua is straightforward relative to corporate structures, with minimal documentation required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the proprietor |

| Members | Single proprietor | No minimum capital partners or shareholders |

| Local Presence | Registered business name (where applicable) | Physical address required for registration |

| Capital | No statutory minimum; Eastern Caribbean Dollar (XCD) | Proprietor funds the business directly |

| Liability | Unlimited personal liability | Personal assets fully exposed to business debts |

| Privacy | Business name is publicly registered | Proprietor's identity linked to the business name |

Focus Points

- Taxation: Subject to personal income tax; no separate corporate tax filing. VAT registration is required once turnover exceeds the statutory threshold.

- Annual Compliance: No formal annual returns to a corporate registry; tax filings with the Inland Revenue Department apply.

- Economic Substance: No substance obligations apply, as this structure falls outside the scope of corporate substance legislation.

- Conversion: Can be converted into a private limited company or other corporate structure, though assets and liabilities must be formally transferred.

- Restrictions: Cannot raise equity capital from external investors or issue shares.

Closing

A sole proprietorship suits resident individuals running small-scale, domestic trading or service businesses where administrative simplicity outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, but unlimited personal liability remains a significant structural constraint for any business carrying meaningful financial risk.

Local residents operating low-risk, owner-managed businesses who prioritise minimal compliance overhead over liability protection.

How to Choose the Right Entity Type in Antigua and Barbuda

Choosing the right business entity in Antigua and Barbuda requires matching the structure to your specific operational, tax, and compliance profile — not simply selecting the most common or most familiar form.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering an International Business Corporation when you intend to trade locally means operating in breach of the Companies Act, which can result in penalties or striking off the register.

- Selecting a tax-exempt entity — such as an IBC — when your business requires access to double taxation treaties means you cannot claim withholding tax reductions in counterpart countries, as exempt entities are typically excluded from treaty benefits.

- Forming a private limited company when your objective is estate planning or asset protection locks you into ongoing shareholder obligations and annual filing requirements that would not apply under a trust or foundation structure.

- Choosing an entity that mandates audited financial statements for a single-person consultancy adds recurring professional costs that serve no regulatory purpose at that scale.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated sectors such as banking or insurance each point to a structurally different vehicle under Antiguan law.

- Local vs. Offshore Operations: If your firm will transact with Antiguan residents, an IBC is legally prohibited from doing so without separate authorisation.

- Ownership and Management: Single-owner operations and multi-party arrangements have different governance demands — an LLC or partnership offers flexible management, while a company requires a formal board.

- Tax Objectives: Full tax exemption, participation in a specific regime, and treaty eligibility are mutually exclusive in some structures, so your tax position must be confirmed before registration.

- Privacy Requirements: The public register in Antigua and Barbuda discloses certain director and shareholder information; nominee arrangements are available but add cost and administrative layers.

- Exit Strategy: Not all structures permit redomiciliation or conversion — confirm whether your chosen form allows these options before incorporating.

Corporate Compliance Services in Antigua and Barbuda

Ongoing compliance support for companies registered in Antigua and Barbuda, including annual filings, registered agent obligations, and regulatory reporting.

Conclusion

Incorporating a company in Antigua and Barbuda means choosing from a well-defined set of structures, each governed by distinct legislation. The IBC remains the default for non-resident entrepreneurs seeking tax-neutral holding or trading arrangements. Private limited companies suit locally active businesses with a small number of shareholders, while public limited companies apply where broader capital access is required. LLCs offer members limited liability under a flexible management framework. General partnerships carry unlimited joint liability, whereas limited partnerships allow passive investors to cap their exposure. Branch and representative offices give foreign firms a registered presence without incorporating a separate entity. Sole proprietorships serve individual operators with straightforward registration requirements.

Among these, the IBC is by far the most registered structure in Antigua and Barbuda. The jurisdiction has shown a continued commitment to treaty expansion and financial services regulation, trends that will affect entity selection going forward. Expanship's formation and compliance services are structured to address each of these structures directly.

How Expanship Can Assist You

Expanship company incorporation Antigua covers the full process — from selecting the right structure under the Companies Act or the International Business Corporations Act to submitting your application directly with the Antigua and Barbuda Intellectual Property and Commerce Office (ABIPCO). Your choice of entity, whether an IBC, private limited company, or LLC, carries distinct compliance obligations that require accurate handling from the outset.

Expanship manages each stage of your business setup in Antigua and Barbuda, so nothing falls through the gaps.

- Document preparation and notarization

- Registered agent and registered office provision

- Government filing and ABIPCO liaison

- Post-incorporation compliance management

- Banking introduction assistance

- Ongoing annual return and maintenance support

Ready to move forward? Reach out through our [Expanship Antigua and Barbuda](ag/contact-us) contact page and a specialist will respond with guidance specific to your situation.

Frequently Asked Questions (FAQ)

The International Business Corporation (IBC) is the most registered structure, governed by the International Business Corporations Act. Its appeal rests primarily on full foreign ownership, zero corporate tax on foreign-sourced income, and minimal ongoing disclosure requirements.

An IBC is restricted from trading with Antigua and Barbuda residents or owning local real estate without a license, while a Private Limited Company faces no such restrictions and can conduct domestic commerce freely. The Private Limited Company carries broader compliance obligations, including annual returns filed with the Antigua and Barbuda Companies Registry, and is subject to standard corporate tax on locally sourced profits.

The IBC offers the highest degree of confidentiality. Beneficial ownership details are not disclosed on the public register, and nominee directors and shareholders are permitted under the IBC Act.

A sole individual can form an IBC or Private Limited Company, as both require a single shareholder and director. Partnerships, by definition, require at least two partners, making sole formation structurally impossible.

Foreign nationals may register an IBC, Private Limited Company, LLC, or branch office without a local partner requirement. Sole proprietorships are technically available to foreigners but require a trade license, and operating approval may depend on residency status or sector-specific restrictions under local licensing law.

Conversion procedures are not uniformly codified across all entity categories. A Private Limited Company may re-register or restructure, but converting an IBC into a domestic company type generally requires dissolution and fresh incorporation rather than a statutory continuation process.

IBCs, Private Limited Companies, Public Limited Companies, and LLCs all carry separate legal personality, meaning they can own assets, enter contracts, and incur liabilities independently of their members. General partnerships do not possess separate legal personality under Antiguan law; partners remain personally liable for firm obligations.

The IBC imposes the lightest ongoing requirements: no mandatory audit, no public filing of accounts, and no annual general meeting requirement unless the articles specify otherwise. By contrast, Public Limited Companies must hold annual general meetings and file audited financial statements.

For tailored guidance on selecting and registering the appropriate structure, Expanship's corporate services team covers the full incorporation process across all entity types available in this jurisdiction.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.