Key Takeaways

- Zambia's corporate tax framework, administered by the Zambia Revenue Authority, includes sector-specific relief provisions that can materially reduce the effective tax burden for qualifying investors in manufacturing, agriculture, and priority industries.

- Foreign nationals may hold 100% equity in a locally registered Zambian entity without mandatory local partnership requirements across most sectors, preserving full operational and structural control from the point of incorporation.

- Registration through the Patents and Companies Registration Agency (PACRA) provides a defined administrative pathway for establishing a private limited company, reducing setup friction compared to jurisdictions with less codified incorporation procedures.

- Membership in both COMESA and SADC gives Zambia-incorporated entities preferential trade access across a combined bloc of more than 40 African countries, which can eliminate the need for multiple subsidiary structures when operating regionally.

Zambia is a landlocked sovereign republic in sub-Saharan Africa, bordering eight countries and governed under a presidential constitutional framework. Company registration falls under the jurisdiction of the Patents and Companies Registration Agency, the statutory body responsible for administering business registration and intellectual property matters. Foreign investors most commonly establish a private limited company when entering the market.

The country's tax posture is treaty-based and residence-linked, administered by the Zambia Revenue Authority under a domestic framework that includes provisions for sector-specific relief. On the question of foreign ownership, the general regulatory position is open — outside of a defined list of reserved sectors, foreign nationals may hold equity stakes in locally registered entities without mandatory local partnership requirements.

This article examines the principal advantages that make Zambia company formation a practical consideration for internationally operating businesses, covering the regulatory, commercial, and structural factors relevant to incorporation here.

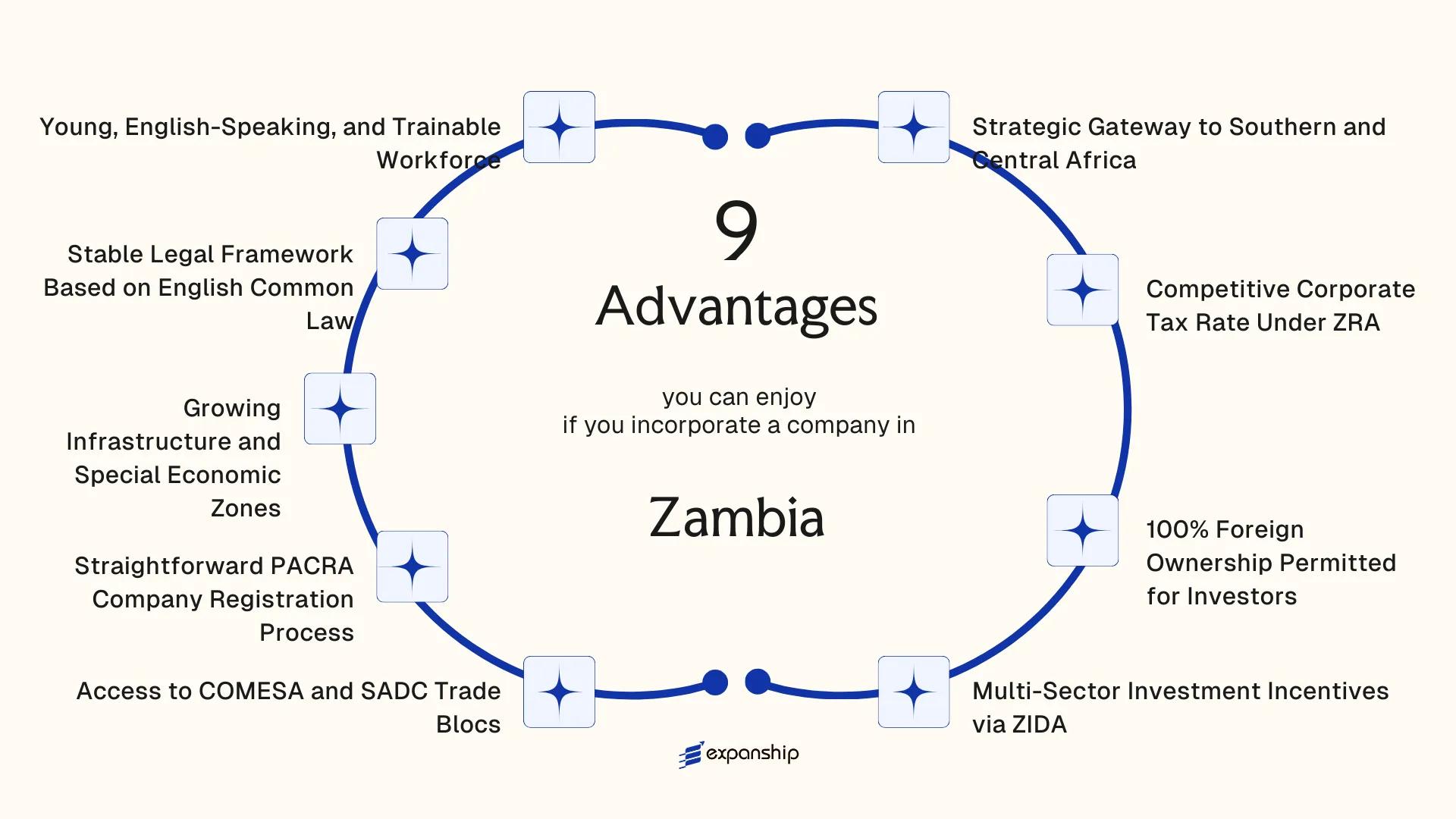

Strategic Gateway to Southern and Central Africa

Zambia's central position within sub-Saharan Africa makes it a functional entry point for businesses targeting multiple regional markets simultaneously. Registering a company here gives your business physical and commercial access to over 700 million consumers across neighboring trade corridors.

Geographic Position as a Commercial Advantage

Zambia shares borders with eight countries, including Tanzania, Zimbabwe, the Democratic Republic of Congo, and Mozambique. This means goods, services, and capital can move across several major African economies from a single registered base without requiring separate operational footholds in each market.

For a foreign firm managing regional distribution or service delivery, this reduces structural overhead considerably. Operating from a centrally located jurisdiction cuts transit distances to both East and Southern African markets compared to coastal alternatives.

Regional Market Access Through Trade Alignment

Membership in both COMESA and SADC gives Zambia-registered entities preferential tariff treatment across 21+ countries in total. This treaty coverage, supported by the African Continental Free Trade Area (AfCFTA) framework, means your entity can price goods more competitively within the region than a firm incorporated outside these agreements.

A company registered in Zambia can access reduced or zero-rated tariffs across COMESA and SADC member states, lowering the cost of cross-border trade from day one.

Competitive Corporate Tax Rate Under ZRA

Zambia's standard corporate tax rate sits at 30% for most companies, administered by the Zambia Revenue Authority (ZRA) under the Income Tax Act. For context, this rate is competitive relative to several sub-Saharan African peers and falls below the global average corporate rate of approximately 23–25% when sector-specific reductions are factored in.

Certain industries attract reduced rates. Mining companies, farming operations, and companies listed on the Lusaka Securities Exchange may qualify for preferential rates, meaning your effective tax burden depends significantly on sector and structure. The ZRA corporate tax advantages for businesses extend further through capital allowances, which permit accelerated depreciation on qualifying assets, reducing taxable income in early operational years.

These features translate directly into higher retained earnings for reinvestment, without requiring complex offshore structuring.

The tax framework offers practical advantages because of how it is built:

- Dividends paid to non-resident shareholders are subject to withholding tax, but Zambia maintains double taxation agreements with several countries, reducing treaty-eligible investors' exposure

- Capital gains on most asset disposals are not taxed under a separate CGT regime, which simplifies exit planning

- The ZRA operates a self-assessment system, reducing administrative dependency on tax authority scheduling

Incorporate Your Company in Zambia

Set up your Zambia-registered company with full ZRA compliance and proper tax structuring from day one.

100% Foreign Ownership Permitted for Investors

Under the Companies Act of 2017, foreign nationals may hold 100% of the shares in a Zambian private limited company, with no obligation to bring in a local partner or cede equity to a citizen shareholder. This statutory right, administered through PACRA (Patents and Companies Registration Agency), gives your business complete control over decision-making, profit distribution, and governance structure from day one.

That degree of ownership purity has a direct consequence for investors: there is no dilution of returns, no need to negotiate shareholder agreements with compulsory local partners, and no structural dependency on third parties who may not share your commercial priorities.

| Parameter | Rule |

|---|---|

| Minimum foreign shareholding allowed | 1% |

| Maximum foreign shareholding allowed | 100% |

| Local partner requirement | None |

| Governing legislation | Companies Act No. 10 of 2017 |

| Administering body | PACRA |

Repatriation of dividends and profits is permitted, and foreign investors are generally entitled to transfer funds abroad under the Bank of Zambia's foreign exchange framework, meaning full ownership extends to full access to your returns. For sectors outside any restricted category defined by ZIDA, this applies across most industries open to private capital. Where restrictions do exist in specific regulated sectors, ZIDA's investment approval process clarifies eligibility before registration proceeds.

Multi-Sector Investment Incentives via ZIDA

The Zambia Investment and Development Agency, established under the ZIDA Act No. 17 of 2020, functions as the primary gateway for foreign investors seeking sector-specific incentives. ZIDA investment incentives Zambia multi-sector framework consolidates what were previously fragmented incentive regimes under the Zambia Development Agency into a single, unified investment entry point. For your business, this means one agency handles approvals, licensing facilitation, and incentive qualification across multiple sectors simultaneously.

Under ZIDA, qualifying investors in priority sectors, including agro-processing, tourism, manufacturing, and energy, can access fiscal benefits such as import duty exemptions on capital equipment and VAT zero-rating on certain inputs. These exemptions directly reduce capital expenditure during the setup phase, which is when a new foreign entity carries its highest cost exposure.

Investment thresholds determine eligibility. The ZIDA Act prescribes minimum investment amounts that vary by sector and location, with rural and strategic investments often qualifying under lower thresholds.

Keep these points in mind:

- Register your investment with ZIDA before claiming any sector-specific fiscal incentive

- Confirm whether your sector qualifies under the current ZIDA priority list, as it is subject to periodic revision

- Retain all capital equipment import documentation; duty exemptions require post-import verification

- Incentive certificates issued by ZIDA are time-bound and must be renewed upon expiry

ZIDA's one-stop shop mandate legally requires participating government ministries to process investor approvals within defined statutory timelines, making administrative delay a compliance issue rather than simply an operational inconvenience.

Access to COMESA and SADC Trade Blocs

Zambia holds active membership in both the Common Market for Eastern and Southern Africa (COMESA) and the Southern African Development Community (SADC). For a foreign-owned entity incorporated there, this dual membership translates into preferential market access across a combined footprint of over 40 countries, without requiring separate trade negotiations or additional licensing arrangements in each member state.

What COMESA Membership Means for Your Business

Under the COMESA Free Trade Area, qualifying goods originating from member states benefit from zero or significantly reduced tariffs when traded across participating countries. A company registered in Zambia and meeting the applicable rules of origin criteria can export to markets such as Egypt, Kenya, Ethiopia, and Zimbabwe under these preferential terms, rather than standard WTO most-favoured-nation rates.

COMESA's rules of origin generally require that goods either be wholly produced in a member state or undergo sufficient processing there, with value addition thresholds defined under the COMESA Treaty framework. This means your production or processing operations must have genuine local substance to qualify.

How SADC Trade Advantages Extend Your Reach Further

The SADC Protocol on Trade, which governs tariff liberalisation among SADC member states, adds a further layer of preferential access covering markets including South Africa, Mozambique, Tanzania, and Botswana. South Africa alone represents a consumer market of significant scale, and accessing it at reduced tariff rates through SADC rather than standard duties lowers the cost structure for goods-based businesses.

Because both agreements operate simultaneously, a Zambia-registered firm can assess which arrangement offers more favourable terms for a specific trade corridor and apply accordingly.

Unlock COMESA and SADC Trade Benefits Through Zambia Incorporation

Speak with an Expanship specialist about structuring your Zambia company to qualify for preferential trade access under COMESA and SADC agreements.

Straightforward PACRA Company Registration Process

PACRA company registration benefits Zambia trace directly to how the agency is structured. The Patents and Companies Registration Agency operates as a statutory body under the Patents and Companies Registration Agency Act, and its mandate covers business name registration, company incorporation, and related filings under a single institutional roof. That consolidation reduces the administrative friction that typically arises when registration functions are split across multiple government departments.

- A private limited company can be incorporated through PACRA's e-Registry portal, which accepts applications and supporting documents online. For foreign investors, this means the initial incorporation stage does not require physical presence in the country.

- The e-Registry system issues a certificate of incorporation upon approval, and standard processing timelines for straightforward applications are generally short, allowing your business to move toward operational setup without extended delays.

- PACRA also maintains a public register, which means your company's legal status can be verified by banks, counterparties, and regulators without requiring bespoke confirmation letters.

- The registration framework operates under the Companies Act No. 10 of 2017, which modernised the prior legislative structure and aligned incorporation procedures closer to internationally recognised standards.

That statutory foundation gives foreign-owned entities a legally predictable starting point, with documented procedures and a publicly accessible regulatory record from day one.

Growing Infrastructure and Special Economic Zones

Zambia's Multi-Facility Economic Zones (MFEZs) offer a structured entry point for foreign companies seeking Zambia Special Economic Zones business advantages. Designated zones such as Lusaka South MFEZ and Chambishi MFEZ provide allocated industrial land, shared utilities, and on-site customs facilities. For a foreign firm, this removes the overhead of sourcing infrastructure independently in an unfamiliar market.

Under the Zambia Development Agency Act (now administered through ZIDA), businesses operating within designated MFEZs and SEZs qualify for specific fiscal incentives tied to their zone status. Qualifying entities are exempt from corporate income tax for periods determined by investment thresholds, and customs duty exemptions apply to imported capital equipment used within the zone.

Beyond fiscal terms, the Zambia infrastructure growth investment benefits extend to physical connectivity. Ongoing road and energy projects, including upgrades along key freight corridors, reduce logistics costs for export-oriented manufacturers based inside SEZ boundaries.

A manufacturing firm establishing inside Lusaka South MFEZ with $2 million in capital equipment imports could avoid customs duties that, at Zambia's standard import duty rates, would otherwise add an estimated $200,000 or more to initial setup costs, depending on equipment classification under the Customs and Excise Act.

Stable Legal Framework Based on English Common Law

Zambia's legal system is rooted in English common law, inherited through its colonial history and preserved through post-independence legislation. For foreign business owners, this matters because common law systems produce a body of case precedent that makes judicial outcomes more predictable. Contracts, disputes, and property rights are interpreted within a framework that many international investors, particularly those from the UK, Commonwealth nations, and countries with similar legal traditions, already understand.

The Companies Act No. 10 of 2017 governs corporate formation and conduct, codifying director duties, shareholder rights, and fiduciary obligations with reasonable clarity. Courts can draw on both domestic precedent and persuasive English case law where local authority is limited, which reduces interpretive uncertainty for cross-border transactions.

Intellectual property, contractual enforcement, and minority shareholder protections each have defined statutory bases. Your legal counsel operating under a familiar framework spends less time interpreting foundational principles and more time addressing transaction-specific issues.

- Contract enforcement follows recognized common law doctrine

- The High Court has commercial jurisdiction over corporate disputes

- Foreign judgments can be registered and enforced under applicable statutory provisions

While the legal framework draws on English common law principles, Zambia's courts apply local statute first, and procedural timelines may differ from those in other common law jurisdictions.

Young, English-Speaking, and Trainable Workforce

Zambia's official language is English, used across government, courts, education, and commerce. For a foreign business owner, this eliminates a layer of operational friction that exists in many other African markets — contracts, regulatory correspondence, and staff communication all proceed in a single shared language without translation overhead.

The median age of the population sits at approximately 17 years, meaning the majority of the labour force entering the market is young and at the beginning of its working life. Recruiting at this stage allows your firm to train staff around its own systems and standards rather than working against entrenched habits from prior employment.

Education in Zambia is conducted in English from primary school onward, producing graduates who can function in professional environments without language retraining. The country's universities, including the University of Zambia (UNZA) and Copperbelt University (CBU), supply graduates across engineering, law, accounting, and business disciplines.

Wage levels in the formal sector remain competitive relative to comparable markets, particularly within the Southern African Development Community (SADC) region. This matters most for businesses in services, processing, and administration, where labour costs constitute a significant share of operating expenses.

The Zambia Qualifications Authority (ZQA) oversees the recognition and standardisation of qualifications, which gives employers a framework for verifying the credentials of prospective hires. Under the Zambia Development Agency Act and successor legislation through the Zambia Investment and Development Agency (ZIDA), certain investor categories may also access support related to skills development and local workforce integration.

Why Zambia Stands Out Among African Incorporation Destinations

Compared to other African incorporation destinations, foreign investors evaluating Zambia tend to also consider Mauritius, Kenya, and South Africa. Mauritius attracts holding company structures through its global business licence regime, Kenya draws East African market entrants, and South Africa remains the continent's largest economy. Placing Zambia against these three reveals where its regulatory and structural features create a distinct position for businesses targeting Southern and Central Africa.

What the table below shows is not simply a feature checklist. It reflects where Zambia's combination of COMESA and SADC membership, ZIDA-administered incentives, and a PACRA registration framework converge to offer a profile that differs meaningfully from its neighbours, particularly for manufacturing, agribusiness, and regional distribution operations.

| Parameter | Zambia | Mauritius | Kenya | South Africa |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 30% (15% for some SEZ operators) | 15% | 30% | 27% |

| Foreign Ownership | 100% permitted | 100% permitted | 100% (most sectors) | 100% (most sectors) |

| Regional Trade Bloc Access | COMESA + SADC | COMESA + SADC | COMESA + EAC | SADC + AfCFTA |

| Investment Promotion Body | ZIDA | Economic Development Board | KenInvest | InvestSA |

| Company Registry | PACRA | Registrar of Companies | Business Registration Service | CIPC |

| Legal System | English Common Law | Mixed (Civil + Common Law) | English Common Law | Mixed (Roman-Dutch + Common Law) |

| Special Economic Zones | Yes, multi-sector | Yes, financial services focus | Yes | Yes |

Compliance Services for Companies in Zambia

Stay current with ZRA filings, PACRA annual returns, and ZIDA reporting obligations for your Zambia-registered entity.

Conclusion

Zambia's position as a Southern and Central African market entry point, combined with its English common law legal system and COMESA/SADC trade access, forms a coherent case for incorporation. The benefits of incorporating in Zambia are most tangible for businesses that need regional reach without the administrative overhead of multiple subsidiary structures.

ZIDA's sector-specific incentive framework and the registration process administered by PACRA reduce both setup friction and ongoing compliance costs in ways that directly affect your bottom line. Foreign-owned entities can hold 100% of their shares without local partnership requirements in most sectors, which preserves operational control from day one.

The extent to which these Zambia company formation advantages apply to your specific situation depends on your industry classification, intended trading activity, and the tax position of your home jurisdiction. A business in extractive industries will face a different incentive structure than one operating in manufacturing or technology services. Identifying the right corporate vehicle, whether a private limited company or a branch structure, and mapping it against applicable ZIDA approvals and ZRA obligations is the step that determines whether the theoretical advantages translate into practical outcomes for your firm.

Let Expanship Handle Your Zambia Company Formation

Expanship Zambia company formation services cover the full cycle of establishing a business entity in the country, from initial name reservation with the Patents and Companies Registration Agency (PACRA) through to post-incorporation compliance under the Companies Act No. 10 of 2017. The entity types discussed throughout this blog, including private limited companies and branch offices, each carry distinct registration requirements, and Expanship manages those requirements directly with the relevant authorities on your behalf.

Our service scope across the incorporation and maintenance process includes:

- Preparation and legalization of all formation documents

- Registered office and resident agent provision in Lusaka

- Direct filing and liaison with PACRA and ZIDA

- Post-incorporation compliance management, including annual returns

- Tax registration coordination with the Zambia Revenue Authority (ZRA)

- Banking introduction assistance for new corporate accounts

Your business does not need to be physically present in Zambia for most stages of this process. Expanship coordinates documentation, notarization, and submission requirements on behalf of foreign principals, reducing delays that typically arise from unfamiliarity with local procedural requirements. Where ZIDA investment licensing or sector-specific permits are required, the firm handles the coordination with those bodies as well.

Reach out to [Expanship Zambia](external:/zm/contact-us) to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Patents and Companies Registration Agency (PACRA) processes straightforward company registrations within a few business days when documentation is in order, though timelines can extend depending on the business structure and completeness of submitted forms. Name reservation, director and shareholder details, and the memorandum of association must all be filed correctly to avoid delays. Registrations are handled through PACRA's online portal, which supports remote submission.

The standard corporate income tax rate administered by the Zambia Revenue Authority (ZRA) is 30% for most companies. Reduced rates apply in priority sectors, and entities operating within Multi-Facility Economic Zones or qualifying under ZIDA incentive frameworks may access lower rates or tax holidays depending on the nature and scale of their investment.

ZIDA administers sector-specific investment incentives under the Investment and Business Development Act No. 14 of 2022, meaning the benefits available to your firm vary according to industry classification. Agribusiness, manufacturing, tourism, and technology each carry distinct qualifying thresholds and corresponding fiscal benefits. You must apply for investment certification through ZIDA to access the formal incentive regime.

Registration alone does not automatically confer preferential trade status under COMESA or SADC. Your business must meet the applicable rules of origin requirements set by each trade bloc to qualify for reduced or zero-rated tariffs when trading across member states. Compliance with these origin criteria is assessed on a transaction-by-transaction basis and requires supporting documentation at the point of export or import.

Commercial disputes are governed under a legal framework derived from English common law, which Zambia retained following independence. The courts apply established principles of contract, tort, and company law that are broadly familiar to investors from Commonwealth jurisdictions. This foundation provides a degree of predictability in contractual enforcement and dispute resolution.

Failure to file annual returns with PACRA can result in penalties and, in persistent cases, the administrative striking off of the company from the register. A deregistered entity loses its legal standing, which affects its ability to enter contracts, hold assets, or operate bank accounts. Restoration to the register is possible but requires a formal application and settlement of outstanding obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.