Key Takeaways

- Zambia's corporate formation framework is governed by the Companies Act No. 10 of 2017, administered by the Patents and Companies Registration Agency (PACRA), which oversees all registered business structures in the country.

- The private limited company is the most commonly registered entity in Zambia, favoured by both resident entrepreneurs and foreign investors for its liability protection and structural flexibility.

- Foreign businesses can establish a presence in Zambia without incorporating a separate local entity by registering a branch office or external company under the same legislative framework.

- Cooperative societies, companies limited by guarantee, partnerships, and sole proprietorships remain available for specific operational purposes, each carrying distinct requirements around ownership, liability, and compliance under Zambian law.

Introduction to Entity Types in Zambia

Zambia is a landlocked country in sub-Saharan Africa, bordered by eight nations including Tanzania, Zimbabwe, and the Democratic Republic of the Congo. It is an independent republic and a member of the Common Market for Eastern and Southern Africa (COMESA). Understanding the types of business entities in Zambia starts with the regulatory framework: company registration falls under the Patents and Companies Registration Agency (PACRA), which administers the Companies Act No. 10 of 2017 — the primary legislation governing corporate formation and compliance.

Zambia operates a residence-based tax system, with corporate income tax applicable to profits earned within the country.

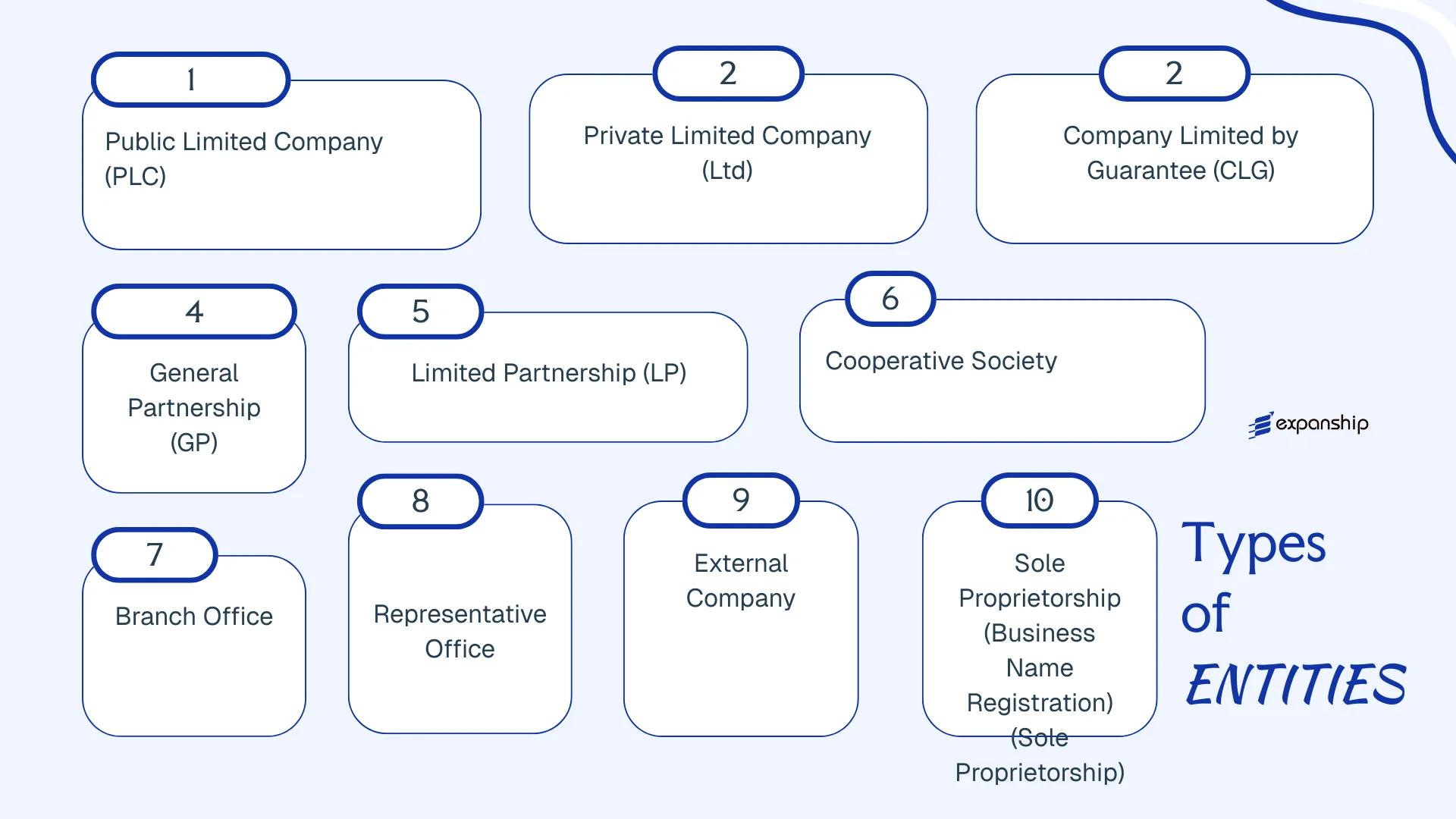

Available Zambia legal entity types include the Public Limited Company, Private Limited Company, Company Limited by Guarantee, General Partnership, Limited Partnership, Cooperative Society, Sole Proprietorship (Business Name), and foreign business structures such as Branch Offices, Representative Offices, and External Companies.

Each of these structures carries distinct requirements around ownership, liability, governance, and registration — all of which the sections below examine in detail.

An Overview of Business Structures in Zambia

Zambia's company law framework provides several distinct entity types, each governed primarily by the Companies Act No. 10 of 2017 and administered by the Patents and Companies Registration Agency (PACRA). Additional structures such as cooperative societies fall under separate legislation, including the Co-operatives Societies Act. Each entity type serves a different commercial purpose, and the sections that follow examine each in full.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Corporate body | Limited to shares | Taxed | Yes | 2 shareholders | PACRA | Companies Act No. 10 of 2017 |

| Private Limited Company (Ltd) | Corporate body | Limited to shares | Taxed | Yes | 1 shareholder | PACRA | Companies Act No. 10 of 2017 |

| Company Limited by Guarantee | Corporate body | Limited to guarantee | Taxed / Exempt | Yes | 1 member | PACRA | Companies Act No. 10 of 2017 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | PACRA | Registration of Business Names Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | PACRA | Registration of Business Names Act |

| Cooperative Society | Incorporated body | Limited | Taxed / Exempt | Yes | 10 members | PACRA / Ministry | Co-operative Societies Act |

| Branch Office | Foreign body extension | Parent liable | Taxed | Yes | N/A | PACRA | Companies Act No. 10 of 2017 |

| Representative Office | Non-trading entity | Parent liable | Generally exempt | No | N/A | PACRA | Companies Act No. 10 of 2017 |

| External Company | Registered foreign entity | Parent liable | Taxed | Yes | N/A | PACRA | Companies Act No. 10 of 2017 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | PACRA | Registration of Business Names Act |

Each of these structures is examined in full in the sections below.

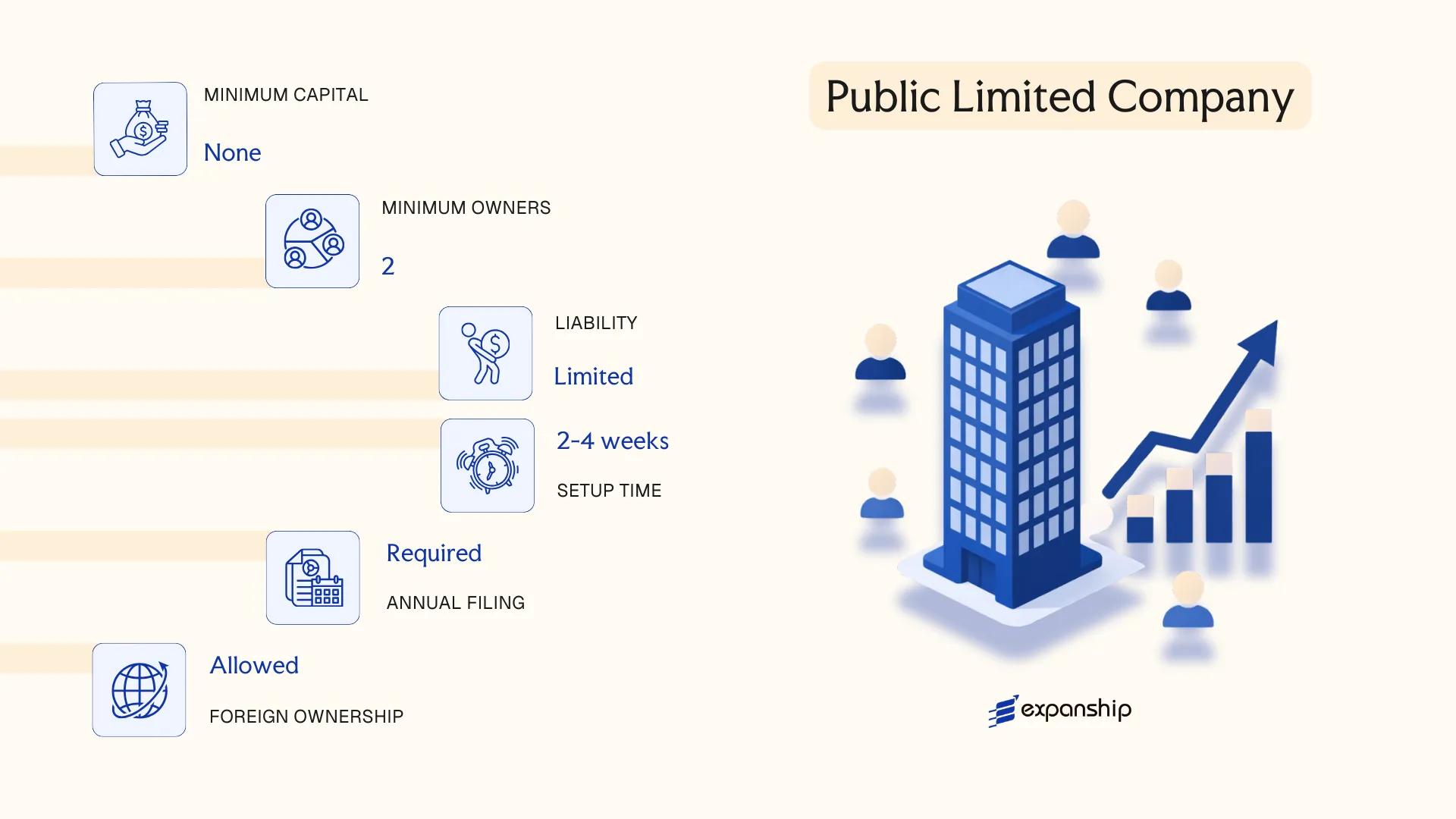

Public Limited Company (PLC)

A public limited company Zambia PLC is governed by the Companies Act No. 10 of 2017, which replaced the earlier 1994 legislation and modernised the corporate framework. This structure carries separate legal personality, meaning the company can hold assets, enter contracts, and incur liabilities independently of its shareholders. Liability is limited to the amount unpaid on shares, making it a structure suited to large-scale capital mobilisation.

PLCs are the only entity type in Zambia permitted to offer shares to the general public or list on the Lusaka Securities Exchange (LuSE). The Securities Act and the LuSE Listing Requirements impose additional disclosure and governance obligations on listed firms, layered on top of the Companies Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under the Companies Act No. 10 of 2017 |

| Shareholders | Minimum 2; no statutory maximum | Shares may be offered to the public |

| Directors | Minimum 2 directors required | At least one must be ordinarily resident in Zambia |

| Registered Office | Physical registered address in Zambia required | Must be maintained at all times; P.O. Box alone insufficient |

| Share Capital | No prescribed statutory minimum for general PLCs; LuSE listing requirements impose their own capital thresholds | Capital denominated in Zambian Kwacha (ZMW) |

| Privacy | Shareholder register and financial statements are publicly accessible | Annual returns filed with PACRA are public record |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT registration is mandatory above the prescribed turnover threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents — refer to the Zambia Revenue Authority for current rates and exemptions.

- Annual Compliance: Annual returns must be filed with the Patents and Companies Registration Agency (PACRA); audited financial statements are required and must be prepared under IFRS.

- Securities Regulation: Any public offer of shares requires a prospectus approved by the Securities and Exchange Commission of Zambia (SEC Zambia) under the Securities Act.

- Conversion: A PLC may be converted to a private limited company by special resolution and re-registration with PACRA, provided it meets the private company criteria.

- Foreign Ownership: No general restriction on foreign shareholding, though sector-specific regulations may apply in areas such as mining and media.

Closing

A PLC is primarily used for large trading operations, financial institutions, and businesses seeking access to public capital markets, including a LuSE listing. The ability to raise equity from the public is a structural advantage not available to any other entity form, though the corresponding disclosure, audit, and securities compliance obligations carry significant ongoing costs and administrative burden.

Best suited for large enterprises or investor groups that require access to public equity capital or plan to pursue a listing on the Lusaka Securities Exchange.

Company Incorporation in Zambia

Expanship assists with the full incorporation process for Zambian entities, including PLCs, through PACRA and related regulatory bodies.

Private Limited Company (Ltd)

Governed by the Companies Act No. 10 of 2017, administered by the Patents and Companies Registration Agency (PACRA), a private limited company Zambia Ltd is the most widely used corporate structure for both domestic and foreign investors. The entity holds separate legal personality distinct from its shareholders, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares.

Zambia Ltd company registration requires at least one shareholder and one director, with no upper limit on shareholders prescribed under the 2017 Act, though the constitution may impose its own cap. Share transfers are restricted by default, preventing public subscription.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality; liability limited to unpaid share amount |

| Members | Min. 1 shareholder; no statutory maximum | Constitution may restrict share transfers |

| Governing Body | Min. 1 director; no residency requirement | At least one company secretary required |

| Local Presence | Registered office address in Zambia required | Must be maintained at all times with PACRA |

| Share Capital | No statutory minimum; denominated in ZMW | Shares must be fully described in the share register |

| Privacy | Beneficial ownership disclosure required | Register of members filed with PACRA; publicly accessible |

Focus Points

- Taxation: Subject to 30% corporate income tax on Zambia-sourced profits; standard VAT rate of 16%; withholding tax applies to dividends (15%), interest (15%), and royalties (15%); transfer pricing rules apply to related-party transactions.

- Annual Compliance: Annual returns and audited financial statements must be filed with PACRA; failure attracts penalties and potential deregistration.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions, but transfer pricing and tax residency rules require genuine operational presence for treaty benefits.

- Treaty Access: Zambia maintains double taxation agreements with several countries; a Zambia Ltd entity qualifies for treaty access subject to residency and beneficial ownership conditions.

- Conversion: A private limited company may be re-registered as a public limited company under the Companies Act 2017 by special resolution and regulatory approval from PACRA.

A private limited company suits trading operations, subsidiary structures, and holding arrangements where liability containment and separate legal identity are priorities. The restricted share transfer mechanism provides ownership control, though the public accessibility of the members register limits confidentiality for sensitive ownership structures.

Best suited for foreign investors incorporating a Zambian operating subsidiary or a locally active trading entity requiring straightforward governance and shareholder protection.

Company Limited by Guarantee

A company limited by guarantee Zambia incorporations fall under is governed by the Companies Act No. 10 of 2017, administered by the Patents and Companies Registration Agency (PACRA). Unlike a share-based company, this structure has no share capital. Members commit to contributing a fixed amount toward the company's liabilities if it winds up, rather than purchasing equity.

This entity carries separate legal personality, meaning it can own property, enter contracts, and sue or be sued in its own name. It is the standard vehicle for non-profit organisations, charitable foundations, professional associations, and trade bodies operating within the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | No share capital; liability capped at each member's guaranteed contribution |

| Members | Referred to as Members; minimum of 1, no statutory maximum | No shareholders; governance typically vested in a board of directors or trustees |

| Local Presence | Registered office in Zambia; registered with PACRA | Physical address required; PO Box alone is not sufficient |

| Capital | No minimum share capital; members' guarantee amount stated in Memorandum | Guarantee amount is often nominal (e.g., ZMW 20–100 per member) |

| Privacy | Director and member details filed with PACRA and appear on public record | Beneficial ownership disclosure required under the 2017 Act |

Focus Points

- Taxation: Exempt from income tax if registered as a non-profit with the Zambia Revenue Authority (ZRA), provided income is applied solely to the entity's objectives; commercial activities may attract corporate tax at 35% and VAT registration is required if taxable turnover exceeds the statutory threshold.

- Annual Compliance: Annual returns must be filed with PACRA; audited financial statements are generally required for entities receiving donor or public funds.

- Conversion: The Companies Act 2017 does not provide a straightforward mechanism to convert a guarantee company into a share company; restructuring typically requires dissolution and re-incorporation.

- Restrictions: May not distribute profits or surpluses to members; all funds must be applied toward stated objects.

- Treaty Access: As a non-profit structure, access to Zambia's double tax agreements is limited and context-dependent; treaty benefits are generally not available on exempt income.

Closing

This structure is used predominantly by NGOs, professional regulatory bodies, charitable organisations, and membership associations where profit distribution is prohibited and accountability to a broader public interest is required. The separate legal personality offers organisational continuity, but the prohibition on profit distribution makes it unsuitable for any commercial venture seeking returns for its founders.

Best suited for non-governmental organisations, foundations, and membership bodies that require a formal legal structure without share capital or profit distribution.

Partnerships (General Partnership, Limited Partnership)

Partnership registration in Zambia is governed by the Partnership Act, Chapter 388 of the Laws of Zambia. A partnership does not constitute a separate legal entity from its partners — each partner remains personally bound by the obligations of the firm. This absence of separate legal personality is the defining structural feature that distinguishes partnerships from limited companies.

Registration is handled through the Patents and Companies Registration Agency (PACRA). A partnership name must be registered before trading begins, particularly where the firm operates under a name other than that of the partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality from its partners |

| Members | Partners (minimum 2, maximum 20) | Exceeding 20 partners generally requires incorporation as a company |

| Local Presence | Registered business address in Zambia | Must be a physical address; PACRA filing address required |

| Capital | No statutory minimum; denominated in ZMW | Capital contributions are governed by the partnership agreement |

| Liability | Unlimited (general partners) | Limited partners have liability capped at their capital contribution |

| Privacy | Partnership agreement not publicly filed | Partner names are on public record via PACRA |

Focus Points

- Taxation: Partnerships are taxed at the partner level; each partner declares their share of income under the Income Tax Act and is subject to the applicable individual or corporate rate. VAT registration is required if annual turnover exceeds the ZRA threshold.

- Annual Compliance: Partners must file annual returns with PACRA and submit tax returns to the Zambia Revenue Authority (ZRA).

- Restrictions: Financial services and certain regulated sectors restrict or prohibit partnership structures.

- Conversion: A partnership may convert to a private limited company under the Companies Act No. 10 of 2017 through a formal re-registration process with PACRA.

- Treaty Access: Partnerships generally do not access double tax treaty benefits as entities; treaty eligibility depends on the residency status of individual partners.

Sub-Types

General Partnership

All partners carry unlimited personal liability for the debts and obligations of the firm. Management rights and profit-sharing are typically set out in a written partnership agreement, though the Partnership Act implies default terms where no agreement exists.

Limited Partnership

At least one general partner with unlimited liability must exist alongside one or more limited partners whose liability is capped at their agreed capital contribution. Limited partners may not participate in management without risking loss of their limited liability status.

A partnership structure suits professional service providers — such as legal or accounting practices — and small joint ventures where two to a limited number of parties wish to operate with minimal formation formality. The primary advantage is structural simplicity; the principal drawback is the unlimited personal exposure carried by general partners.

A partnership is best suited for licensed professionals or small-scale collaborators who require a straightforward shared structure and are comfortable with personal liability exposure.

Cooperative Society

Cooperative society registration Zambia falls under the Cooperatives Act, Chapter 397 of the Laws of Zambia, which is administered by the Registrar of Cooperatives under the Ministry of Small and Medium Enterprise Development. A cooperative society holds separate legal personality upon registration, meaning it can own property, enter contracts, and sue or be sued in its own name. Members benefit from limited liability, and the structure is inherently hybrid — combining commercial activity with mutual benefit principles.

Cooperatives are formed on the basis of voluntary membership, democratic control, and equitable distribution of surplus. They are particularly common in agriculture, savings and credit, and consumer supply sectors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Registered under the Cooperatives Act, Cap. 397 |

| Members | Referred to as Members; minimum 10 individuals required | No statutory maximum; must share a common bond or purpose |

| Governance | Managed by an elected Board of Directors | Officers include Chairperson, Secretary, and Treasurer |

| Local Presence | Registered office within Zambia required | Must maintain books and records at the registered address |

| Capital | No prescribed minimum share capital; contributions via member shares | Share value and structure defined in the society's by-laws |

| Privacy | Member register maintained internally; financial statements filed with the Registrar | Not publicly listed but subject to regulatory inspection |

Focus Points

- Taxation: Cooperative societies are subject to corporate income tax at the standard rate of 35%; agricultural cooperatives may qualify for reduced rates or exemptions under the Income Tax Act, and VAT registration applies once the turnover threshold is met.

- Annual Compliance: Societies must hold an Annual General Meeting, submit audited financial statements, and file an annual return with the Registrar of Cooperatives.

- Audit Requirement: External audits are mandatory; the Registrar may also conduct its own inspection or audit.

- Conversion: Conversion to a company or other entity type is not straightforward and generally requires dissolution and fresh incorporation.

- Restrictions: A cooperative society cannot list on a stock exchange or distribute profits in the same manner as a company; surplus distribution must follow cooperative principles.

Sub-Types

Primary Cooperative Society

The base-level structure formed directly by individual members. This is the most common form and is used for agricultural marketing, savings and credit (SACCOs), and consumer supply activities.

Secondary Cooperative Society

Formed by a union of primary cooperative societies rather than individual members. This structure is used to consolidate operations, negotiate at scale, or provide shared services across multiple primary societies.

Tertiary Cooperative Society (Apex)

An apex body formed by secondary societies at the national level. It typically engages in policy representation, wholesale trade, or national coordination functions.

Closing

A cooperative society suits member-based enterprises operating in agriculture, microfinance, or community supply chains, where profit distribution is secondary to collective benefit. The democratic governance structure supports member accountability, though it can slow decision-making in larger societies.

Best suited for groups of farmers, artisans, or community-based entrepreneurs seeking a formally registered collective structure with shared ownership and mutual benefit objectives.

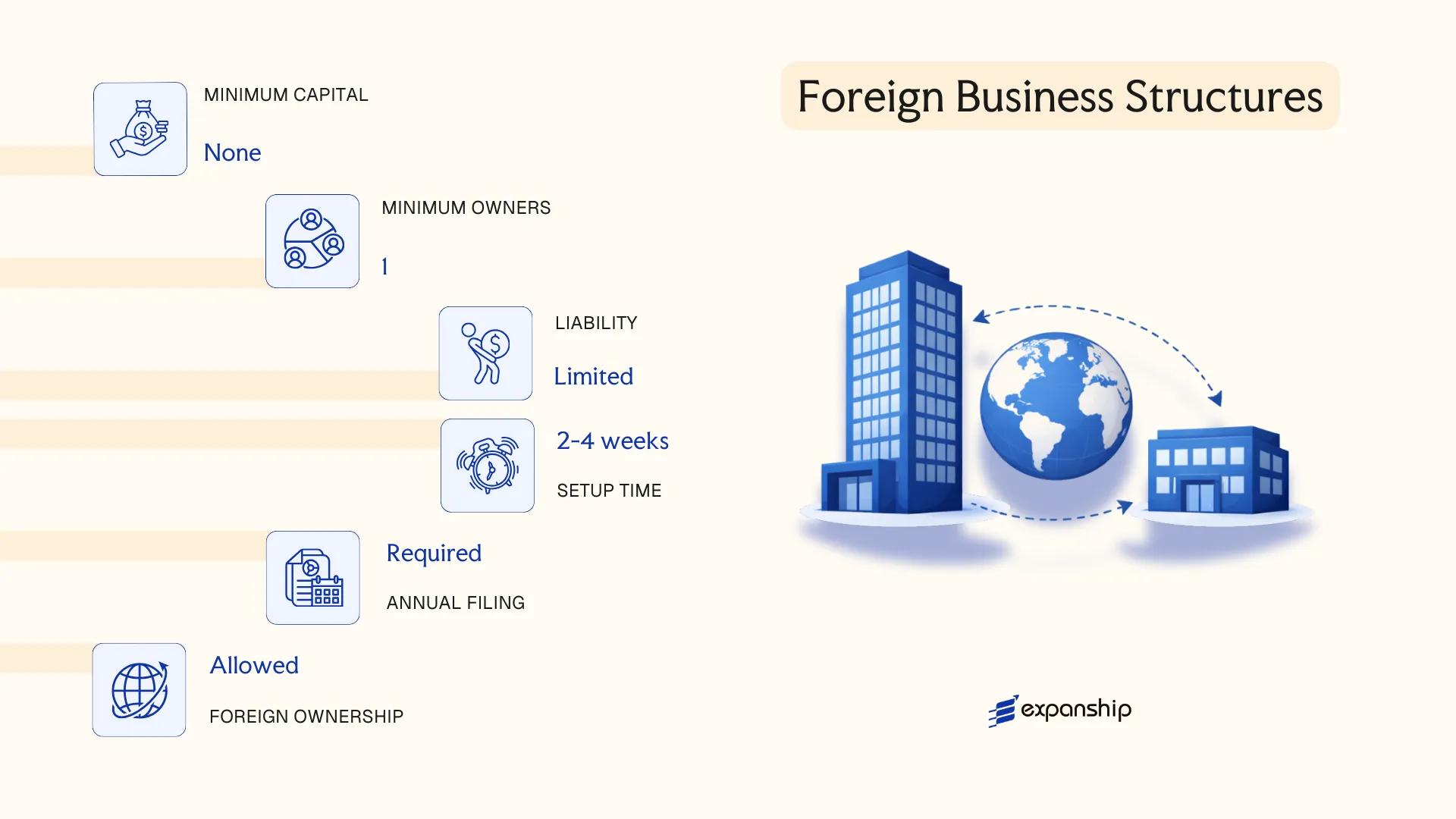

Foreign Business Structures (Branch Office, Representative Office, External Company)

Foreign entities operating in Zambia are governed primarily by the Companies Act No. 10 of 2017, which classifies them under the category of "external companies." Registering a foreign company branch office Zambia requires compliance with Part XII of this Act, which mandates registration with the Patents and Companies Registration Agency (PACRA) within 21 days of establishing a place of business in the country.

An external company does not form a separate legal entity — it remains an extension of the parent corporation, which retains full legal and financial liability for its operations within the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External Company / Branch | Not a separate legal entity; parent company bears full liability |

| Designated Officer | Local representative (natural person) | Must be resident in Zambia and authorised to accept legal service |

| Registered Office | Physical local address required | P.O. Box addresses are not accepted |

| Capital | No minimum capital prescribed | Parent company financials govern creditworthiness |

| Disclosure | Parent company documents must be filed | Includes certified copies of constitution and audited accounts |

| Privacy | Limited — public filings required at PACRA | External company register is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at 30% on Zambia-sourced income; VAT registration required if turnover thresholds are met; withholding taxes apply to remitted profits and cross-border payments.

- Treaty access: Zambia has a network of double taxation agreements; branch structures may access these, though treaty entitlement depends on the parent's country of residence.

- Annual compliance: Annual returns and updated parent company documents must be filed with PACRA; failure attracts penalties.

- Restrictions: Certain sectors — including telecommunications and mining — impose additional licensing requirements on foreign entities beyond standard PACRA registration.

- Conversion: An external company may subsequently incorporate a local subsidiary under the Companies Act if operational needs change.

Sub-Types

Branch Office

A branch office conducts active commercial operations in Zambia under the parent company's name and legal identity. It is the structure used when the foreign entity intends to generate revenue directly within the country.

Representative Office

A representative office is limited to non-commercial activities such as market research, liaison, and promotion. It cannot enter into contracts or generate income locally, making it suitable for preliminary market-entry activities before committing to full establishment.

Closing

Foreign business structures are most commonly used by multinationals testing market entry, companies executing project-based contracts, or firms in sectors where a full local subsidiary is not yet warranted. The primary advantage is speed of setup relative to incorporating a new entity; the key limitation is that the parent company bears unrestricted liability for all local obligations.

Foreign companies seeking a presence in Zambia for revenue-generating operations without incorporating locally — particularly those on fixed-term contracts or in early-stage market assessment.

Sole Proprietorship (Business Name Registration)

A sole proprietorship in Zambia is governed by the Registration of Business Names Act, which requires any individual trading under a name other than their own to register that name with the Patents and Companies Registration Agency (PACRA). Registering a sole proprietorship business name in Zambia does not create a separate legal entity — the business and its owner are legally the same person, meaning personal assets remain exposed to business liabilities.

Unlike incorporated structures, there is no share capital, no board, and no constitutional document beyond the registration record itself. Sole trader registration in Zambia is among the more straightforward entry points for self-employed individuals and micro-business operators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business name | No separate legal personality from the owner |

| Referred To As | Proprietor | Single individual; no concept of shareholders or directors |

| Membership | 1 proprietor only | Cannot have co-owners under this structure |

| Local Presence | Registered business address in Zambia required | PACRA registration is linked to a physical address |

| Capital | No minimum capital requirement | Entirely funded by the proprietor |

| Privacy | Owner details filed with PACRA | Information is accessible through PACRA's public registry |

Focus Points

- Taxation: Subject to personal income tax on business profits under Zambia Revenue Authority (ZRA) rules; VAT registration is required once turnover exceeds the prescribed threshold; no corporate income tax applies.

- Annual Compliance: Business name renewal is required periodically with PACRA; failure to renew can result in de-registration.

- Liability: Unlimited personal liability — the proprietor's personal assets are at risk for all business debts and obligations.

- Conversion: Can be converted into a private limited company by incorporating a new entity and transferring assets; no automatic conversion mechanism exists.

- Treaty Access: No access to double tax treaty benefits, as those apply to corporate entities, not individuals operating as sole traders.

Closing

This structure suits small-scale traders, freelancers, and self-employed professionals who operate locally with limited financial exposure. The primary advantage is low setup cost and administrative simplicity; the significant drawback is unlimited personal liability with no legal separation between the individual and the business.

Sole proprietorship registration is best suited for individual operators running low-risk, domestic businesses who do not require external investment or liability protection.

How to Choose the Right Entity Type in Zambia

Selecting how to structure your business in Zambia is a decision with direct legal, tax, and operational consequences — not simply an administrative step.

Why Your Entity Choice Matters

The structure you register determines what obligations attach to your business from day one. Choosing the wrong entity type can produce concrete, costly outcomes:

- Registering as an external company without fulfilling the requirements under the Companies Act No. 10 of 2017 can result in penalties or striking off by the Patents and Companies Registration Agency (PACRA).

- Selecting a tax-exempt entity when your transactions require access to Zambia's double taxation agreement network means withholding tax reductions in counterpart countries will not be available to your business.

- Forming a private limited company when the underlying purpose is asset protection or succession planning locks your business into annual shareholder obligations that a trust or similar structure would not carry.

- Choosing an entity that mandates audited financial statements for a single-director consultancy introduces annual compliance costs that would not apply under a sole proprietorship registered through PACRA.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point toward a distinct entity type under Zambian law.

- Ownership and Management: A sole operator has little reason for a board structure, while multi-party ventures with external investors require the governance framework that a private or public limited company provides.

- Tax Objectives: Your need for full tax exemption, treaty access, or eligibility under the Zambia Revenue Authority's specific sector incentives will narrow the viable structures considerably.

- Public Disclosure Tolerance: PACRA maintains a public register of directors and shareholders; if disclosure is a concern, nominee arrangements within a private limited company may be worth examining.

- Exit Strategy: Some structures permit redomiciliation or conversion; others require full dissolution and re-registration, which affects how you plan for future restructuring.

Compliance Services for Companies in Zambia

Ongoing compliance support for Zambian entities, including annual returns, PACRA filings, and ZRA obligations.

Conclusion

This starting a company in Zambia guide has covered every registered structure available under the Companies Act No. 10 of 2017 and related legislation. Among these, the private limited company remains the most widely registered form, favoured by both resident entrepreneurs and foreign investors for its liability protection and structural flexibility. A branch or external company registration suits multinationals seeking a direct operational presence without incorporating a separate local entity. Cooperative societies serve member-based economic ventures, while companies limited by guarantee address non-commercial purposes. Partnerships and sole proprietorships fit smaller, lower-risk operations with simpler compliance obligations.

Zambia's regulatory direction, guided by PACRA and the Zambia Revenue Authority, continues to trend toward digitised filing and improved treaty alignment. For those planning company formation in Zambia, understanding which structure matches your ownership model and operational scope is the necessary first step before engaging any registration process.

How Expanship Can Assist You

Expanship company registration Zambia covers the full process — from selecting between a Private Limited Company, Public Limited Company, or external company structure, through to filing with the Patents and Companies Registration Agency (PACRA). Your choice of entity carries distinct compliance obligations, and having a structured process from day one reduces the risk of delays or procedural errors.

Expanship handles the administrative and regulatory workload on your behalf, so you can focus on your business operations.

- Document preparation and notarization

- Registered office and local agent provision

- PACRA filing and company name reservation

- Post-incorporation compliance management

- Tax registration with the Zambia Revenue Authority (ZRA)

- Banking introduction assistance

Get in touch with Expanship Zambia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The private limited company (Ltd) is the most frequently incorporated entity, registered through the Patents and Companies Registration Agency (PACRA). Its liability protection, straightforward compliance structure, and suitability for both domestic and foreign-owned businesses account for its prevalence.

A branch is not a separate legal entity — the foreign parent company bears full liability for its Zambian operations. A private limited company is locally incorporated with independent legal personality, which generally reduces the parent's exposure and may present a cleaner profile for local contracting.

Among registered structures, the private limited company permits the use of nominee shareholders, which limits public disclosure of beneficial ownership at the register level. Beneficial ownership details are, however, subject to disclosure requirements under anti-money laundering regulations administered by the Financial Intelligence Centre (FIC).

A private limited company requires a minimum of one shareholder and one director, making sole formation possible. Partnerships, by definition under the Partnership Act, require at least two partners, so a single individual cannot form one unilaterally.

Foreign individuals and entities may incorporate a private limited company, register a branch, or establish a representative office. Certain regulated sectors require additional approvals from bodies such as the Zambia Development Agency (ZDA), and activities in reserved sectors may require local participation.

PACRA does not provide a universal automatic conversion mechanism between all entity types. Re-registration or dissolution followed by fresh incorporation is the more common route when changing structure, though professional legal advice should guide any such transition.

No. General partnerships and sole proprietorships do not possess separate legal personality under Zambian law. Incorporated entities — including private and public limited companies and companies limited by guarantee — hold legal personality distinct from their members.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.