Key Takeaways

- The Companies Act 71 of 2008, administered by the Companies and Intellectual Property Commission (CIPC), governs the registration and ongoing compliance of all formally incorporated entities in South Africa.

- Among the available structures, the private company (Pty Ltd) is the most widely registered entity due to its flexible governance requirements and accessibility to both domestic and foreign owners.

- Partnerships and sole proprietorships operate outside the Companies Act framework entirely, meaning owners bear unlimited personal liability with no statutory separation between personal and business obligations.

- South Africa taxes resident companies on their worldwide income under a residence-based system enforced by the South African Revenue Service (SARS), a factor that directly shapes how international structures involving South African entities are assessed.

Introduction to Entity Types in South Africa

Located at the southern tip of the African continent, South Africa shares borders with Namibia, Botswana, Zimbabwe, Mozambique, and Eswatini, and entirely surrounds the Kingdom of Lesotho. It is an independent republic and a member of the G20, with one of the largest economies on the continent.

Understanding the types of business entities in South Africa starts with knowing which authority governs registration. The Companies and Intellectual Property Commission (CIPC) administers company registration under the Companies Act 71 of 2008, which is the primary legislation governing corporate structures in the country. The CIPC also maintains the official companies register and oversees ongoing compliance obligations.

South Africa operates a residence-based tax system, with corporate income tax levied by the South African Revenue Service (SARS) on resident companies' worldwide income.

The business structures available in South Africa include the following entity types:

- Public Company (Ltd)

- State-Owned Company (SOC Ltd)

- Private Company (Pty Ltd)

- Personal Liability Company (Inc.)

- Non-Profit Company (NPC)

- Co-operative (Co-op)

- General Partnership

- Limited Partnership

- Partnership en Commandite

- External Company

- Sole Proprietorship

Each structure carries distinct implications for liability, ownership, governance, and tax treatment — this article examines each one in detail.

An Overview of Business Structures in South Africa

South Africa's company law framework provides several distinct business structures, each governed primarily by the Companies Act 71 of 2008 and, for co-operatives, the Co-operatives Act 14 of 2005. The Companies and Intellectual Property Commission (CIPC) administers registration for most entity types, while the Financial Sector Conduct Authority (FSCA) holds oversight for certain financial services co-operatives. Each structure carries different implications for liability, taxation, governance, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (Ltd) | Incorporated company | Limited | Taxed | Yes | 3 directors, 1 shareholder | CIPC | Companies Act 71 of 2008 |

| State-Owned Company (SOC Ltd) | Incorporated company | Limited | Taxed | Yes | State as shareholder | CIPC / relevant ministry | Companies Act 71 of 2008 |

| Private Company (Pty Ltd) | Incorporated company | Limited | Taxed | Yes | 1 director, 1 shareholder | CIPC | Companies Act 71 of 2008 |

| Personal Liability Company (Inc.) | Incorporated company | Joint & several | Taxed | Yes | 1 director | CIPC | Companies Act 71 of 2008 |

| Non-Profit Company (NPC) | Incorporated entity | Limited | Conditionally exempt | Yes | 3 incorporators | CIPC / SARS | Companies Act 71 of 2008 |

| Co-operative (Co-op) | Incorporated entity | Limited | Taxed / partial exemption | Yes | 5 members (primary) | CIPC / FSCA | Co-operatives Act 14 of 2005 |

| General Partnership | Unincorporated | Unlimited | Taxed (partners) | Yes | 2 partners | None (contract-based) | Common law |

| Limited Partnership | Unincorporated | Mixed | Taxed (partners) | Yes | 1 general, 1 limited partner | None (contract-based) | Common law |

| Partnership en Commandite | Unincorporated | Mixed | Taxed (partners) | Yes | 1 general, 1 silent partner | None (contract-based) | Common law |

| External Company | Foreign entity | Parent liability | Taxed | Yes | 1 foreign company | CIPC | Companies Act 71 of 2008 |

| Branch Office | Foreign entity | Parent liability | Taxed | Yes | 1 foreign company | CIPC / SARS | Companies Act 71 of 2008 |

| Representative Office | Foreign entity | Parent liability | Limited / exempt | Restricted | 1 foreign company | CIPC / SARS | Companies Act 71 of 2008 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed (individual) | Yes | 1 individual | SARS | Common law |

Each of these structures is examined in full in the sections below.

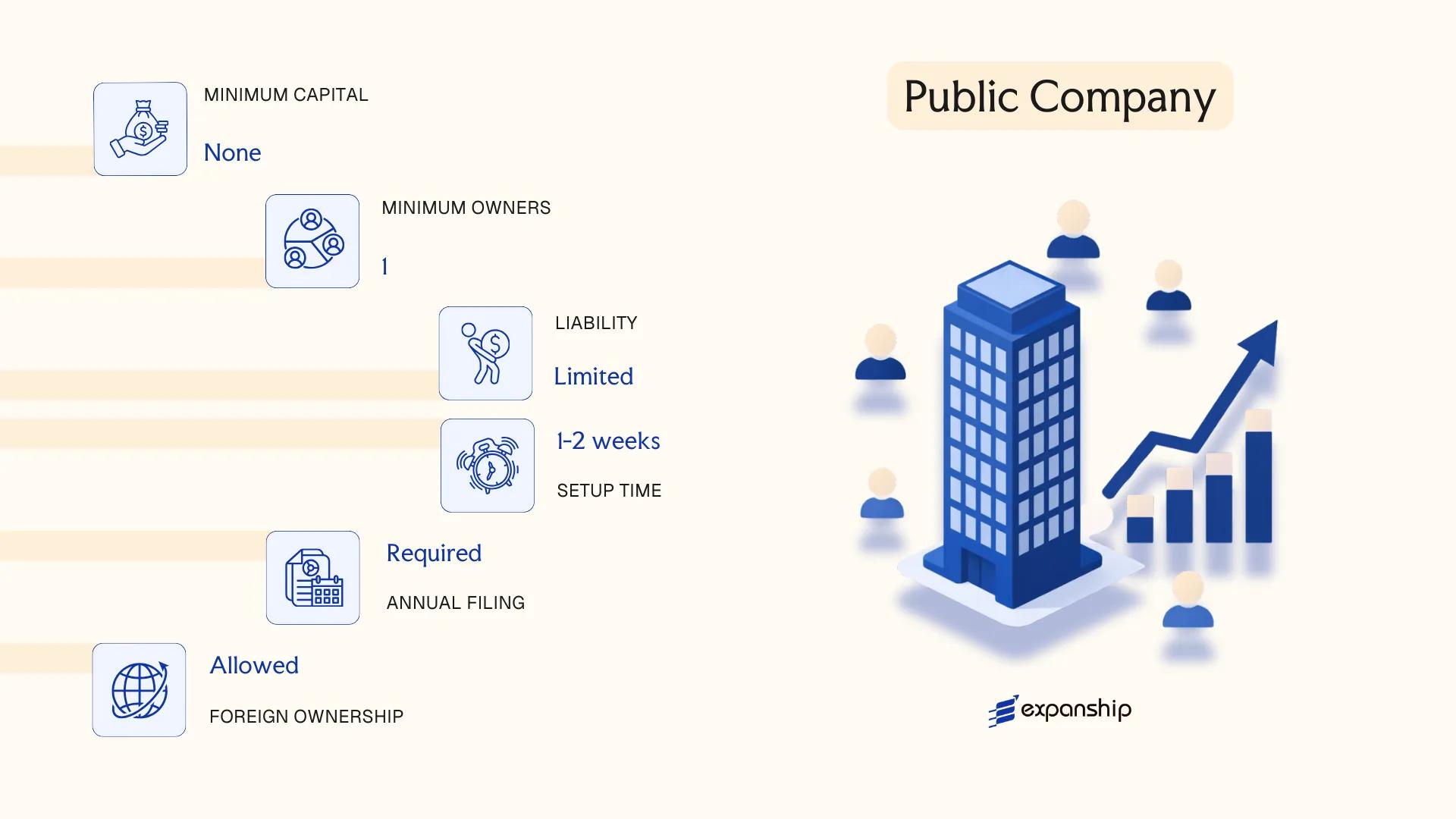

Public Company (Ltd)

Governed by the Companies Act 71 of 2008 and regulated by the Companies and Intellectual Property Commission (CIPC), a public company is a separately incorporated legal entity that can offer its securities to the general public. South Africa public company Ltd registration is distinct from private incorporation in that the entity must comply with significantly more rigorous disclosure and governance requirements from inception.

Limited liability applies to shareholders, meaning personal assets are not exposed to company debts. If the company seeks a stock exchange listing, it must additionally satisfy the JSE Limited Listing Requirements, which operate alongside the Act's statutory obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company (Ltd) | Separate legal personality; shareholders not liable for company debts |

| Governance Roles | Minimum 3 directors; no maximum | At least one director must be ordinarily resident in South Africa |

| Shareholders | Minimum 1; no statutory maximum | Securities may be offered to the public; freely transferable |

| Local Presence | Registered office in South Africa required | A company secretary (natural person or juristic entity) is mandatory |

| Share Capital | No minimum prescribed capital | Shares issued at par or no par value; authorised shares stated in MOI |

| Financial Reporting | Audited annual financial statements mandatory | Must be filed with CIPC; public inspection rights apply |

Focus Points

- Taxation: Subject to corporate income tax at 27%, VAT at 15% on taxable supplies, dividends withholding tax at 20%, and securities transfer tax at 0.25% on share transfers.

- Annual Compliance: Annual returns to CIPC, audited financials, and an AGM are mandatory each financial year.

- Listing Requirements: Exchange listing is optional but triggers JSE oversight, additional prospectus obligations, and continuous disclosure rules.

- Treaty Access: Qualifies as a resident entity for purposes of South Africa's tax treaty network, subject to beneficial ownership rules.

- Conversion: A public company may convert to a private company by special resolution and MOI amendment, subject to CIPC approval.

Closing

A public company suits large-scale commercial operations, group holding structures, or businesses intending to raise capital from external investors or public markets. The ability to offer shares openly is the primary structural advantage; the mandatory audit, AGM, and public disclosure obligations represent a material compliance burden for smaller operations.

Best suited for businesses planning a JSE listing, broad shareholder bases, or operations that require public capital-raising capacity.

Company Incorporation in South Africa

Incorporate a public or private company in South Africa with CIPC-compliant documentation and end-to-end filing support.

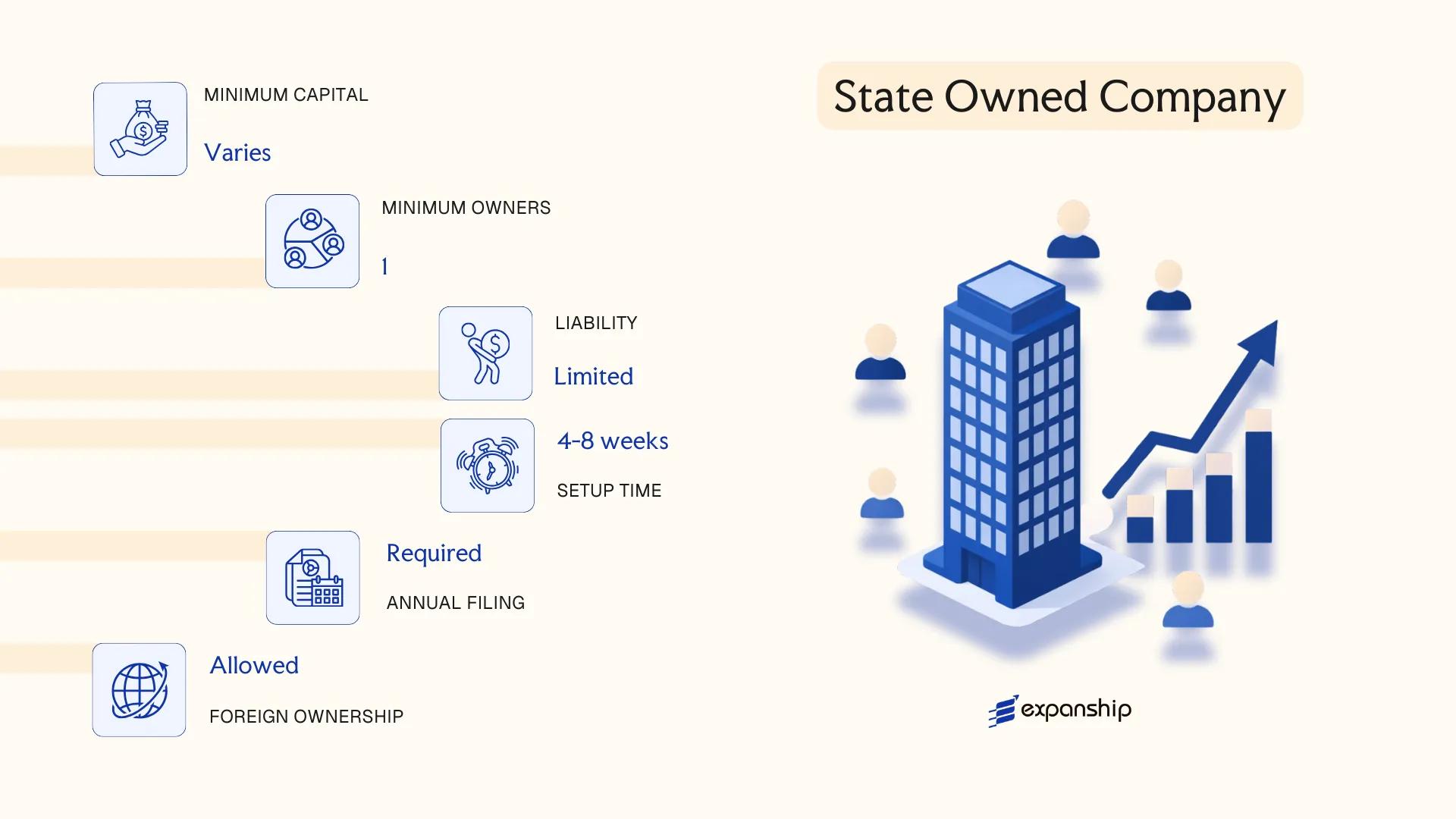

State-Owned Company (SOC Ltd)

A South Africa state-owned company, designated by the suffix "SOC Ltd," is governed by the Companies Act 71 of 2008. Schedule 1 of that Act defines it as a company in which the state is either the sole shareholder or holds a majority interest, making it a hybrid form that combines private company mechanics with public accountability obligations.

Separate legal personality applies to an SOC Ltd in the same way it does to other incorporated entities, meaning the company can own assets, incur liabilities, and enter contracts in its own name. Limited liability of shareholders is preserved in principle, though state ownership introduces layers of oversight absent from purely private entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company | Governed by the Companies Act 71 of 2008 |

| Members | Directors and shareholders | Sole or majority shareholder must be the state (national, provincial, or municipal) |

| Local Presence | Registered office in South Africa | Must maintain a registered address; subject to oversight by the relevant government department |

| Capital | ZAR; no statutory minimum | Capital structure defined in Memorandum of Incorporation (MOI) |

| Governance | Board of directors | Board accountability extends to the relevant public authority and, where listed functions apply, to the Public Finance Management Act (PFMA) |

| Privacy | Moderate | Annual financial statements must be audited; subject to public disclosure requirements under the PFMA or Municipal Finance Management Act (MFMA) |

Focus Points

- Taxation: SOC Ltd entities are generally subject to corporate income tax at the standard rate of 27%; specific exemptions may apply depending on the enabling legislation; VAT registration is required once the mandatory turnover threshold is met.

- Oversight and Compliance: Entities falling under national or provincial government are regulated by the Public Finance Management Act 1 of 1999; those under local government fall under the MFMA; both require annual reports and audits by the Auditor-General of South Africa.

- Conversion: An SOC Ltd cannot convert to a private company without legislative or executive authority approving divestiture of the state's shareholding.

- Treaty Access: SOC Ltd entities may access South Africa's tax treaty network, though treaty benefits can be denied or restricted where specific anti-abuse provisions apply to state entities.

- Restrictions: Shares cannot be freely transferred without government approval; the entity cannot be listed on a public exchange without separate enabling legislation.

Closing

An SOC Ltd is the designated structure for government-mandated commercial activities, including utilities, infrastructure, and strategic industry functions. The structure provides the state with direct control over commercially operated assets, but the dual accountability to corporate law and public finance legislation creates significant governance complexity.

This entity type is suited exclusively to government bodies establishing or maintaining a commercial entity under state ownership — not available to private investors.

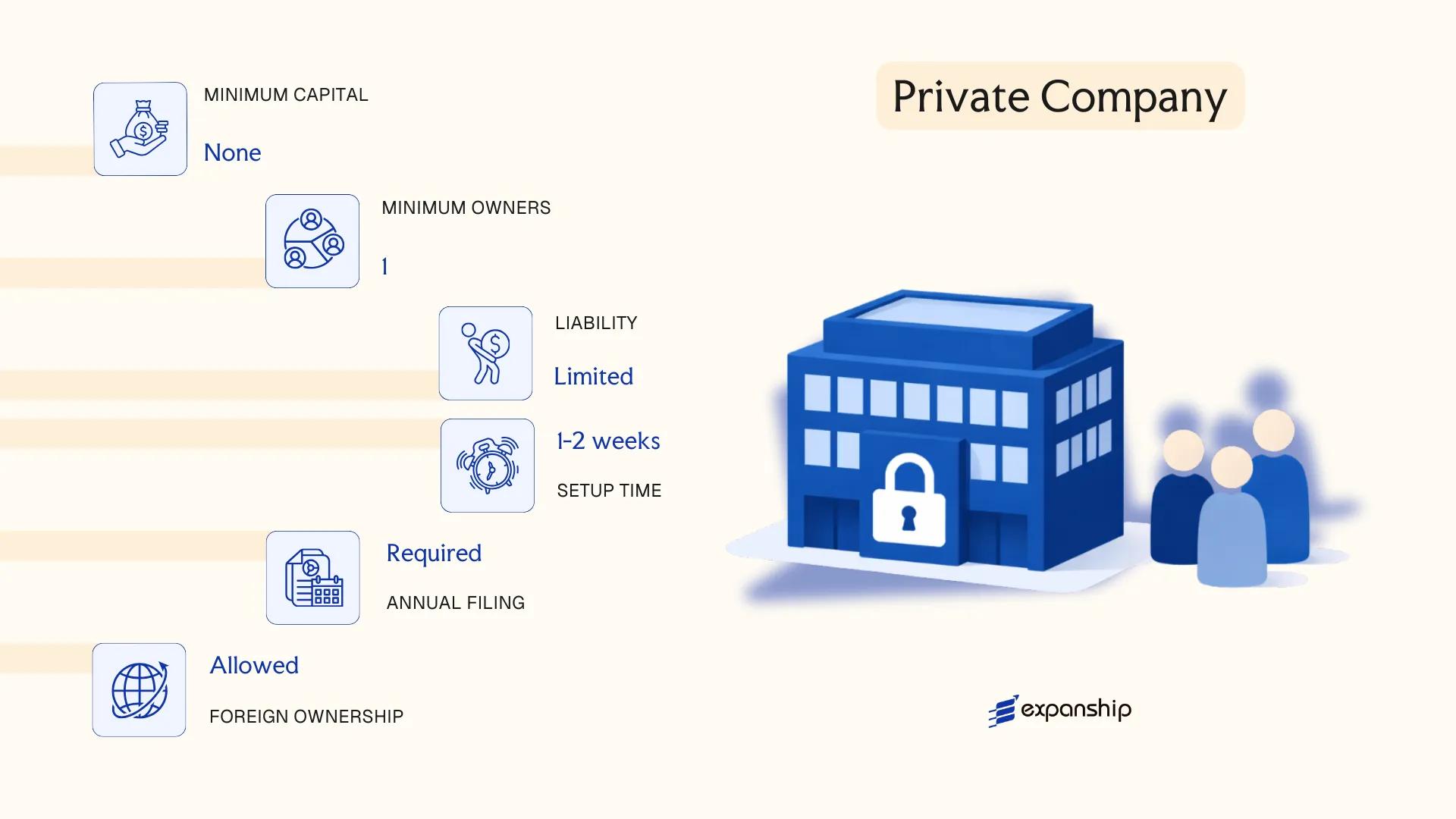

Private Company (Pty Ltd)

The private company, designated as a proprietary limited company under South African law, is the most widely registered business structure for commercial activity. South Africa Pty Ltd company registration is governed by the Companies Act 71 of 2008, administered by the Companies and Intellectual Property Commission (CIPC). As a distinct legal entity, it carries its own rights and obligations, with shareholders' liability limited to their subscribed share capital.

A private Pty Ltd in South Africa cannot offer its securities to the public and must restrict the transferability of its shares through its Memorandum of Incorporation (MOI).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company | Separate legal personality; limited liability |

| Members | Shareholders (owners) and Directors (managers) | Minimum 1 shareholder; maximum 50 non-employee shareholders; minimum 1 director |

| Local Presence | Registered office address in South Africa | Must be a physical address; no registered agent requirement under the Act |

| Capital | ZAR; no minimum share capital | Shares may be issued at any value; no par value shares permitted |

| Privacy | Beneficial ownership disclosure required | Beneficial ownership register filed with CIPC since 2023 |

| Company Secretary | Not mandatory for private companies | Recommended for governance; mandatory only for public companies |

Focus Points

- Taxation: Subject to corporate income tax at 27%; VAT registration mandatory once turnover exceeds ZAR 1 million; dividends withholding tax at 20%; no stamp duty on share transfers.

- Annual Compliance: Annual return filed with CIPC; financial statements required; audit mandatory only if public interest score exceeds 350 or if the MOI requires it.

- Treaty Access: Qualifies as a South African tax resident entity, granting access to South Africa's network of double taxation agreements.

- Conversion: Can convert to a public company or a non-profit company by amending the MOI and filing the prescribed form with CIPC.

- Restrictions: Cannot offer shares to the public; share transfer restrictions must be embedded in the MOI.

Closing Paragraph

A private Pty Ltd suits trading operations, holding structures, joint ventures, and foreign subsidiaries entering the South African market. The limited liability structure and straightforward incorporation process are clear operational advantages, though the 50-shareholder cap restricts growth for businesses seeking broad equity participation.

Best suited for foreign investors establishing a subsidiary, SMEs, and entrepreneurs seeking a scalable, liability-protected operating entity in South Africa.

Personal Liability Company (Inc.)

Governed by the Companies Act 71 of 2008, a personal liability company (Inc.) in South Africa is a registered company with full separate legal personality — yet it departs from standard limited liability protection in one significant respect. Directors, both current and past, remain jointly and severally liable with the company for debts arising from their own acts or omissions during their tenure.

This hybrid structure was designed specifically for licensed professionals who are required by their regulatory or professional bodies to remain personally accountable to clients. Attorneys, auditors, and certain other practitioners commonly adopt this form where the relevant professional statute mandates or permits it.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company with separate legal personality | Directors bear personal joint and several liability for debts from their own conduct |

| Members | Directors (minimum 1; no statutory maximum) | No shareholders in the traditional sense; the company issues shares but membership is tied to directorship |

| Local Presence | Registered office address in South Africa | Must maintain a registered office; CIPC registration required |

| Capital | No minimum share capital (ZAR) | Shares may be issued at any value; no par value shares permitted under the 2008 Act |

| Privacy | Director names filed with CIPC | Publicly searchable via the CIPC register |

| Name Requirement | Must end with "Incorporated" or "Inc." | Distinguishes the entity from a private company |

Focus Points

- Taxation: Subject to corporate income tax at 27%, VAT registration required once turnover exceeds ZAR 1 million, and standard withholding taxes on dividends (20%) and royalties apply; no special tax treatment relative to a private company.

- Annual Compliance: Must file an annual return with CIPC and prepare annual financial statements; audit or independent review requirements depend on the company's public interest score.

- Conversion: Can be converted to another company form under the Companies Act, though professional regulatory bodies may restrict or require approval before conversion.

- Restrictions: Use is generally limited to professions where personal accountability is a regulatory requirement; not suitable for general commercial trading.

- Treaty Access: Qualifies as a South African tax resident entity and may access double tax agreement benefits under standard residency criteria.

Closing Paragraph

A personal liability company suits professional service firms — particularly legal and accounting practices — where regulatory obligations require practitioners to remain personally accountable. The key advantage is that it provides a recognised corporate structure while satisfying professional liability requirements; the principal limitation is that directors cannot rely on the corporate veil to shield themselves from liability arising from their own professional conduct.

Licensed professionals — particularly attorneys and auditors — who are required by their governing regulatory body to operate under a personal liability structure.

Non-Profit Company (NPC)

A Non-Profit Company (NPC) is incorporated under the Companies Act 71 of 2008 and carries separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Directors and members are not personally liable for the entity's debts, provided they act within their fiduciary duties.

Unlike an NPO registered under the Non-Profit Organisations Act 71 of 1997 with the Department of Social Development, an NPC is a registered company under the CIPC. The NPC vs NPO difference is structural: an NPC is a legal entity; an NPO registration is a voluntary accreditation. An NPC can simultaneously hold NPO status, which is required to access certain public funding streams.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Non-Profit Company | Governed by Companies Act 71 of 2008 |

| Governing Members | Directors (minimum 3) | No shareholders; income may not be distributed to members or directors |

| Incorporators | Minimum 3 persons or juristic persons | Incorporators sign the MOI and need not be directors |

| Registered Office | Physical address in South Africa required | Must be maintained with CIPC |

| Capital | No share capital | Assets and income are tied to the stated public benefit or non-profit objective |

| Privacy | Directors listed in public CIPC records | Annual financial statements may require independent review or audit |

Focus Points

- Taxation: NPCs are not automatically tax-exempt; Public Benefit Organisation (PBO) status must be applied for separately with SARS under section 30 of the Income Tax Act to access income tax exemption, donation tax exemption, and potential VAT relief.

- Annual Compliance: Must file an Annual Return with CIPC and hold at least one directors' meeting per year; financial statements are required and may need independent review depending on Public Interest Score.

- NPO Accreditation: Voluntary registration with the Department of Social Development under the NPO Act unlocks access to government grants and donor funding.

- Conversion: An NPC can be converted to a profit company only under specific circumstances prescribed in the Companies Act, subject to CIPC approval.

- Restrictions: Income, property, and assets may never be distributed to incorporators, members, directors, or officers, either directly or indirectly.

Closing

An NPC suits charities, foundations, religious organisations, professional associations, and public benefit initiatives where income must remain tied to an organisational purpose rather than returned to any individual. The non-distribution constraint is the defining structural limitation.

Best suited for public benefit organisations, foundations, and civil society entities that intend to apply for PBO status with SARS and require a formal legal structure with limited liability.

Co-operative (Co-op) [Worker Co-op, Consumer Co-op, Financial Services Co-op, Housing Co-op, Social Co-op]

Co-operatives in South Africa are governed by the Co-operatives Act 14 of 2005, as amended by the Co-operatives Amendment Act 6 of 2013. To register a co-operative in South Africa, the entity must be formed around a common economic interest shared by its members, and upon registration with the Companies and Intellectual Property Commission (CIPC), it acquires separate legal personality with limited liability for its members.

Unlike investor-driven entities, a co-operative distributes surplus based on member participation rather than capital contribution, making its financial structure fundamentally different from a standard company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Juristic person | Registered under the Co-operatives Act 14 of 2005 |

| Members | Referred to as members; minimum 5 for primary co-operatives | Secondary co-ops require at least 2 primary co-ops; tertiary co-ops require at least 2 secondary co-ops |

| Governance | Board of directors elected by members | One member, one vote — regardless of capital contributed |

| Local Presence | Registered office within South Africa required | Must be maintained throughout the entity's life |

| Capital | No prescribed minimum share capital | Members contribute via membership fees or share purchases as defined in the constitution |

| Privacy | Constitution and annual returns filed with CIPC | Publicly accessible documents |

Focus Points

- Taxation: Co-operatives are subject to standard corporate income tax at 27%; agricultural co-ops may qualify for specific exemptions under the Income Tax Act; VAT registration is required once the R1 million threshold is met.

- Annual Compliance: Annual financial statements and returns must be submitted to CIPC; larger co-operatives may require an independent review or audit.

- Surplus Distribution: Surplus is distributed as patronage proportional to member transactions, not shareholding.

- Conversion: A co-operative may convert to a company under prescribed procedures, subject to CIPC approval.

- Restrictions: Financial services co-operatives accepting member deposits are additionally regulated by the Prudential Authority under the Co-operative Banks Act 40 of 2007.

Sub-Types

Worker Co-operative

Owned and controlled by its employees, a worker co-operative exists to provide sustainable employment to its members. Governance rights and surplus distribution are tied to labour contribution rather than external investment.

Consumer Co-operative

Members are the customers of the business, collectively owning an entity that supplies goods or services primarily for their own benefit. Retail buying clubs and community stores are common applications.

Financial Services Co-operative

These entities provide savings, credit, and related financial services exclusively to their members. Those accepting deposits are subject to additional oversight by the Prudential Authority under the Co-operative Banks Act 40 of 2007.

Housing Co-operative

A housing co-operative holds or manages residential property collectively on behalf of its members, who occupy units without holding individual title. Registration requires compliance with both the Co-operatives Act and applicable housing regulations.

Social co-operatives also exist under the framework to address community social needs.

Closing

Co-operatives suit community-based enterprises, employee-owned businesses, and member-driven service organisations where democratic governance is a structural priority. The one-member-one-vote model provides equitable internal control, though it can slow decision-making as membership grows.

Best suited for groups of five or more individuals or entities with a shared economic purpose who require a democratically governed, member-owned legal structure.

Partnership Structures [General Partnership, Limited Partnership, Partnership en Commandite]

Unlike incorporated entities, partnership structures in South Africa are governed primarily by common law rather than a dedicated statute. Partnerships do not possess separate legal personality, meaning partners bear personal liability for the firm's obligations. This absence of statutory regulation gives partnerships considerable structural flexibility, though it also limits the protections available to those involved.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Common law entity; no separate legal personality | Partners are jointly and severally liable unless structured otherwise |

| Members | Called partners; minimum 2, maximum 20 (general rule) | Professions such as law and accounting may exceed 20 under regulatory exemptions |

| Local Presence | No statutory registered office requirement | Practical business address typically required for correspondence |

| Capital | No minimum capital; contributions in cash, kind, or skill | Capital structure defined by partnership agreement |

| Registration | No mandatory registration with CIPC | Some sectors (e.g., financial services) require regulatory licensing |

| Privacy | Partnership agreement is private | No public disclosure obligation under company law |

Focus Points

- Taxation: Partnerships are fiscally transparent; each partner is taxed individually on their share of profit at applicable personal or corporate income tax rates. VAT registration is required if annual turnover exceeds the statutory threshold (currently ZAR 1 million).

- Annual Compliance: No annual returns filed with CIPC; compliance obligations depend on sector-specific licensing requirements.

- Treaty Access: Partnerships generally do not access South Africa's tax treaty network directly, as treaties apply to tax residents rather than transparent entities.

- Conversion: A partnership can convert to a private company under the Companies Act 71 of 2008, though this requires fresh incorporation rather than a statutory conversion process.

- Restrictions: Partnerships cannot own immovable property in the firm's name; property must be registered in the names of individual partners.

Sub-Types

General Partnership

All partners participate in management and share unlimited joint and several liability for the firm's debts. This structure is common among professional service providers operating under a shared practice.

Limited Partnership

Modelled on the Silent Partnership concept under common law, a limited partnership includes at least one general partner with unlimited liability and one or more limited partners whose liability is capped at their capital contribution, provided they take no active role in management.

Partnership en Commandite

A partnership en commandite is a specific South African common law form in which the silent partner (the commanditarian) contributes capital but remains undisclosed and takes no part in management. Unlike a standard limited partnership, the commanditarian's identity is not publicly known, making this structure relevant where investor anonymity within the partnership agreement is a priority.

Closing

Partnerships are used mainly by professional firms, joint ventures, and investment arrangements where pass-through taxation and structural simplicity outweigh the absence of limited liability. The primary limitation is that partners remain personally exposed to business debts, with no statutory liability shield available to general partners.

Partnership structures are most appropriate for licensed professionals (attorneys, accountants) and private joint venture arrangements where two or more parties seek a low-cost, contractually governed operating structure without the formalities of incorporation.

Foreign Business Presence [External Company, Branch Office, Representative Office, Liaison Office]

Foreign company registration in South Africa is governed by the Companies Act 71 of 2008, specifically Chapter 2, Part D, which deals with "external companies." A foreign company conducting business within the country must register with the Companies and Intellectual Property Commission (CIPC) within 20 business days of first commencing business activities.

An external company does not acquire a separate South African legal personality upon registration; it remains a legal extension of the foreign parent entity. This means the parent bears full liability for the South African operations, which distinguishes this structure from incorporating a locally domiciled subsidiary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External Company (registered foreign entity) | Registered under Companies Act 71 of 2008, Part D |

| Designated Representative | Minimum one South African resident representative | Accountable to CIPC; must be a natural person |

| Registered Office | Physical address in South Africa required | Cannot use a P.O. Box as registered address |

| Share Capital | Determined by the foreign parent entity | No separate local capital requirement |

| Disclosure | Parent company financials may require filing | CIPC can request audited financial statements |

Focus Points

- Taxation: External companies are taxed on South African-sourced income at the standard corporate rate of 27%; VAT registration is required if annual taxable turnover exceeds ZAR 1 million; withholding taxes apply to royalties (15%), dividends, and interest paid to the foreign parent.

- Transfer Pricing: Transactions between the external company and its foreign parent are subject to SARS transfer pricing rules under Section 31 of the Income Tax Act.

- Annual Compliance: Annual returns must be filed with CIPC; failure to file can result in deregistration of the external company registration.

- Double Tax Treaties: South Africa's network of Double Taxation Agreements may reduce withholding tax rates, depending on the parent's jurisdiction of incorporation.

- Deregistration: The external company registration lapses if the foreign parent dissolves or if CIPC is notified of cessation of South African business activities.

Sub-Types

Branch Office

A branch is the most common operational form of an external company. It can enter contracts, generate revenue, and employ staff locally, but all liabilities trace back to the foreign parent without any liability shield at the South African level.

Representative Office

A representative office may only conduct non-revenue-generating activities such as market research or liaison functions. It cannot sign commercial contracts or invoice clients directly, and SARS typically does not treat it as creating a taxable permanent establishment, provided its scope remains strictly promotional or preparatory.

Liaison Office

Functionally similar to a representative office, a liaison office is used to maintain communication between the foreign parent and local partners or suppliers. Its permitted activities are narrower still, generally limited to administrative coordination rather than any form of commercial engagement.

An external company structure is suited to multinationals testing market entry or maintaining limited operational presence without the administrative overhead of incorporating a separate subsidiary. The primary drawback is unlimited parental liability, since the foreign entity remains fully exposed to any South African obligations incurred by the branch.

Multinational corporations seeking a direct operational footprint in South Africa without establishing a separately incorporated local entity.

Sole Proprietorship

A sole proprietorship in South Africa is the simplest form of business operation and exists without a dedicated governing statute. Unlike registered companies under the Companies Act 71 of 2008, this structure carries no separate legal personality — you and the business are the same legal person, which means personal assets are fully exposed to business liabilities.

Registration requirements are minimal. There is no formal incorporation process with the Companies and Intellectual Property Commission (CIPC), though you must register with SARS for income tax and, where applicable, VAT. Trading under a name other than your own requires registration of that name under the Business Names Act, and sector-specific licences may apply depending on the nature of the trade.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No legal separation between owner and business |

| Members | Single proprietor | No co-owners permitted; cannot issue shares |

| Local Presence | Physical business address | No registered agent requirement |

| Capital | No minimum | ZAR; funded entirely by the proprietor |

| Liability | Unlimited personal liability | Personal assets at risk for all business debts |

| Privacy | No public disclosure | No filings with CIPC; SARS records remain confidential |

Focus Points

- Taxation: Profits taxed as personal income under individual income tax rates (up to 45%); VAT registration required once turnover exceeds ZAR 1 million; no separate corporate tax applies.

- Annual Compliance: Annual personal income tax return to SARS; provisional tax payments required twice yearly; no annual return to CIPC.

- Treaty Access: No access to South Africa's tax treaty network as a separate entity; treaties apply only to the individual proprietor's personal capacity.

- Conversion: Can be converted into a private company (Pty Ltd) by registering a new entity with CIPC and transferring business assets; no statutory conversion mechanism exists.

- Restrictions: Cannot raise equity capital, bring in partners, or offer ownership stakes; growth financing is limited to personal funds or debt.

Recommendations

A sole proprietorship suits freelancers, consultants, and early-stage traders operating at low turnover with limited liability exposure. The absence of CIPC registration reduces administrative overhead, but unlimited personal liability makes it unsuitable once the business carries meaningful financial risk.

Individuals testing a business concept or operating a low-risk, owner-managed trade before committing to a formal corporate structure.

How to Choose the Right Entity Type in South Africa

Selecting how to choose a business structure in South Africa is not a procedural formality — the choice produces binding legal, tax, and compliance consequences that persist for the life of the business.

Why Your Entity Choice Matters

Registering the wrong structure carries concrete costs:

- Registering an external company while conducting day-to-day trade through it without proper registration under the Companies Act 71 of 2008 exposes the business to deregistration by the Companies and Intellectual Property Commission (CIPC) and civil penalties.

- Choosing a Non-Profit Company for its tax-exempt status when you need access to double taxation agreements means the entity cannot claim withholding tax reductions available under those treaties.

- Selecting a Private Company for a single-person professional practice may trigger mandatory audit requirements depending on the entity's Public Interest Score, adding costs that a sole proprietorship or partnership would not incur.

- Structuring through a company when a trust would serve the underlying estate planning purpose locks the principals into annual director obligations, statutory meetings, and CIPC filing duties that trusts do not carry.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or collective investment schemes each require distinct entity forms under South African law.

- Ownership Structure: A sole founder with no intention of raising equity has different structural needs than a multi-party venture requiring a formal board and defined shareholder rights.

- Tax Objectives: Whether you require full tax exemption under Section 10 of the Income Tax Act, standard corporate tax treatment, or small business corporation rates under Section 12E shapes the viable options.

- Public Disclosure Tolerance: Director and shareholder information filed with CIPC appears on the public register; entities requiring confidentiality must account for this through nominee arrangements.

- Substance Capacity: If you cannot maintain a genuine office and decision-making presence locally, certain structures carry greater compliance risk under SARS transfer pricing and residency rules.

- Exit Flexibility: Not all entities permit conversion or redomiciliation — a Private Company can be converted under the Companies Act 71 of 2008, but other structures have more restrictive exit paths.

The full text of the Companies Act 71 of 2008 is available on the South African Government's official portal.

Compliance Services for Companies in South Africa

Ongoing statutory compliance, CIPC filings, and regulatory maintenance for companies registered in South Africa.

Conclusion

South Africa's company registration framework, as set out in the Companies Act 71 of 2008, offers a structured range of options suited to different operational and ownership profiles. The private company remains the most commonly registered entity, reflecting its straightforward governance requirements and suitability for both domestic and foreign-owned businesses. Public companies serve organisations seeking capital from external shareholders, while state-owned companies operate under a distinct accountability framework tied to government ownership. Personal liability companies address the specific needs of licensed professionals. Non-profit companies provide a formal structure for public benefit activities, and co-operatives serve member-based economic ventures. Partnerships and sole proprietorships function outside the Companies Act, carrying unlimited liability. External companies accommodate foreign firms operating directly within the jurisdiction.

The Companies and Intellectual Property Commission continues to refine its digital filing infrastructure, and South Africa's expanding tax treaty network shapes how international structures are assessed. Expanship works within this framework to help you determine which structure fits your situation.

How Expanship Can Assist You

Expanship company incorporation South Africa services are built around the full range of entities governed by the Companies Act 71 of 2008 — from private companies (Pty Ltd) to external company registrations for foreign entrants. Every filing runs through the Companies and Intellectual Property Commission (CIPC), and your assigned team manages that relationship directly on your behalf.

Depending on your structure and goals, Expanship's scope of work typically includes:

- Document preparation, notarization, and apostille legalization

- Registered address and resident public officer provision

- CIPC filing and post-registration amendments

- SARS tax registration and ongoing compliance support

- Statutory record-keeping and annual return submissions

- Banking introduction assistance with South African financial institutions

Each engagement is scoped to what your specific entity actually requires — nothing standardized, nothing surplus.

To discuss your South African setup, reach out through Expanship South Africa.

Frequently Asked Questions (FAQ)

The Private Company (Pty Ltd) is the most frequently incorporated structure, registered through the Companies and Intellectual Property Commission (CIPC). Its combination of limited liability, a single-shareholder minimum, and relatively light disclosure requirements makes it the default choice for both domestic entrepreneurs and foreign investors.

A Private Company restricts the transferability of its shares and cannot offer securities to the public, whereas a Public Company (Ltd) may list on the Johannesburg Stock Exchange and must comply with more extensive financial reporting and audit obligations. Both are subject to the Companies Act 71 of 2008, but Public Companies carry significantly higher ongoing compliance costs.

Among registered entities, the Private Company (Pty Ltd) offers the greatest degree of privacy. Beneficial ownership information must be filed with CIPC under the General Laws (Anti-Money Laundering and Combating Terrorism Financing) Amendment Act, 2022, but shareholder details are not published in searchable public registers accessible to third parties.

A sole proprietorship and a Private Company can each be established by one individual. Partnerships, including General Partnerships and the Partnership en Commandite, require at least two parties by legal definition, while a Co-operative requires a minimum of five members under the Co-operatives Act 14 of 2005.

Foreigners may register a Private Company, incorporate a Non-Profit Company, or establish an External Company through CIPC. A non-resident may serve as the sole director and shareholder of a Pty Ltd, though the entity will require a registered office address within the country and may need a tax representative appointed with the South African Revenue Service (SARS).

The Companies Act 71 of 2008 provides for the conversion of one company type to another by filing a Notice of Conversion (Form CoR 64.1) with CIPC. A Private Company may convert to a Public Company or Personal Liability Company, and vice versa, without forming an entirely new legal entity.

Companies registered under the Companies Act, including the Pty Ltd, Ltd, NPC, and SOC Ltd, each hold legal personality distinct from their members. Partnerships and sole proprietorships do not; in those structures, the owners remain personally liable for all business obligations without the separation that incorporation provides.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.