Key Takeaways

- Uganda's corporate tax framework under the Income Tax Act, Cap 340 applies defined rates within a territorial system, meaning foreign-sourced income falls outside the domestic tax base and reduces overall liability for internationally structured businesses.

- Registration through the Uganda Registration Services Bureau's online portal compresses the administrative burden of company formation, giving foreign investors a faster path to legal operability than many comparable sub-Saharan African jurisdictions.

- Membership in both the EAC and COMESA trade blocs means a single Uganda-registered entity can access preferential trade conditions across a combined market of hundreds of millions of consumers without requiring separate incorporations in each member state.

- The Investment Code Act provides a formalised legal basis through the Uganda Investment Authority for capital protection and sector-specific incentives, reducing financial exposure at the stage when operational costs are highest.

Situated in East Africa and bordered by Kenya, Tanzania, Rwanda, the Democratic Republic of Congo, and South Sudan, Uganda is a landlocked sovereign republic that has steadily attracted foreign direct investment over the past two decades. Company registration is administered by the Uganda Registration Services Bureau, the statutory body responsible for business registration, intellectual property, and related corporate filings. Foreign businesses incorporating here most commonly do so through a private limited company. The country operates a territorial tax system with defined rates under the Income Tax Act, Cap 340, making its posture broadly low-tax relative to regional peers.

Uganda's legal framework actively permits foreign ownership across most commercial sectors, and the government has taken measurable steps through the Uganda Investment Authority to signal openness to external capital. Restrictions exist in certain reserved sectors, but the general position toward foreign direct investment remains permissive. This article examines the key advantages that make the benefits of incorporating in Uganda a relevant consideration for businesses seeking a presence in sub-Saharan Africa.

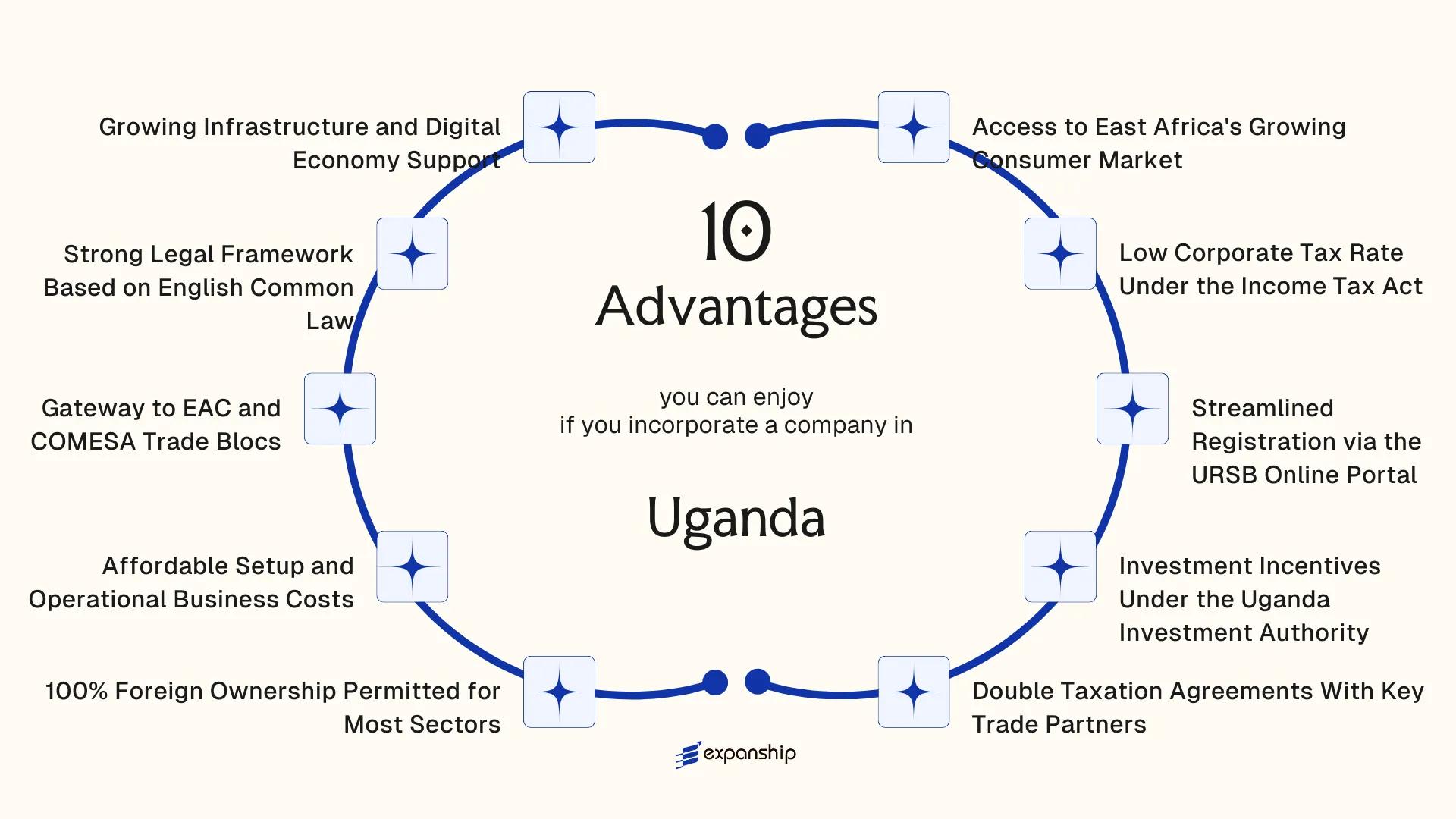

Access to East Africa's Growing Consumer Market

Uganda's geographic position at the heart of the continent's eastern corridor gives businesses incorporated there direct commercial reach into a regional population exceeding 300 million people. Uganda access to East Africa's consumer market is a structural advantage grounded in formal treaty membership, not proximity alone.

Regional Treaty Membership and What It Opens

Uganda is a founding member of the East African Community (EAC), which under the EAC Customs Union Protocol eliminates internal tariffs on qualifying goods traded between member states. A company registered in Uganda can move products into Kenya, Tanzania, Rwanda, Burundi, and South Sudan under preferential terms that a firm incorporated outside the bloc cannot access by default.

Commercial Reach Into Landlocked Markets

South Sudan and the Democratic Republic of Congo, both significant emerging consumer markets, rely heavily on Ugandan trade corridors for import supply chains. Your business can serve these markets through established overland routes without the logistical detour that a non-EAC base would require.

EAC treaty membership means your Uganda-registered company trades across multiple sovereign markets under a single preferential tariff framework.

Low Corporate Tax Rate Under the Income Tax Act

Uganda's standard corporate tax rate sits at 30% under the Income Tax Act, Cap. 340. While that figure is not the lowest globally, it applies uniformly to resident companies and mirrors rates found across several developed economies, making it a predictable and structured environment for foreign-owned entities.

For companies operating in designated sectors, the effective rate can fall well below 30%. The Uganda Investment Authority administers incentive programs that allow qualifying businesses to reduce taxable income through capital deductions, initial allowances, and depreciation rules built into the Act itself. This means your tax position is shaped by statute, not by discretionary negotiation.

The Income Tax Act also provides specific treatment for branch profits, royalties, and dividends, each carrying defined withholding rates. Foreign investors benefit from knowing these figures in advance, since the framework removes ambiguity when structuring cross-border returns.

Several structural features make the tax regime workable for foreign-owned firms:

- Depreciation allowances reduce taxable profit from the first year of operation

- Losses can be carried forward, softening the tax burden during early trading years

- The Act's definitions of residency and source income are codified, limiting interpretive disputes

- Agricultural and agro-processing activities attract accelerated deduction treatment

Company Incorporation in Uganda

Register your company in Uganda with full compliance support, from name reservation through certificate issuance.

Streamlined Registration via the URSB Online Portal

Uganda's URSB online portal registration benefits begin where most African jurisdictions still rely on in-person queues. The Uganda Registration Services Bureau operates a centralised digital platform that allows foreign nationals and local promoters alike to reserve a company name, submit incorporation documents, and pay the required fees entirely online. This removes the geographic constraint that previously made physical presence in Kampala a practical necessity.

For a foreign investor, the time implication is direct. Incorporation of a private limited company through the portal can be completed within a matter of days when documentation is in order, rather than the weeks common under manual filing systems. Your business can be registered, assigned a Certificate of Incorporation, and issued a Tax Identification Number through coordinated government systems without requiring a local agent to physically appear at a bureau counter.

| Registration Output | Issuing Authority | Practical Value |

|---|---|---|

| Certificate of Incorporation | Uganda Registration Services Bureau | Legal proof of entity existence |

| Company PIN / TIN | Uganda Revenue Authority | Required to open a business bank account |

| Business Trading Licence | Local Authority (via URSB integration) | Authorises commercial operations |

Underlying this process is the Companies Act, 2012, which governs the formation and registration of companies in Uganda and defines the documentation standards the portal enforces. Because the Act specifies prescribed forms, your submission follows a structured format that reduces back-and-forth with the registry. Faster registration translates directly into an earlier operational start date, which reduces the cost of your pre-revenue period.

Investment Incentives Under the Uganda Investment Authority

Uganda Investment Authority (UIA) incentives for businesses extend well beyond simple registration support. The UIA, established under the Uganda Investment Code Act of 2019, administers a structured incentives framework specifically designed to reduce the cost burden on qualifying foreign investors and licensed project operators.

One of the most significant benefits under this framework is access to investment licenses that grant holders preferential treatment in land acquisition and utility connections. For capital-intensive projects, that administrative access translates directly into reduced lead time before operations begin.

Qualifying investors in priority sectors, including agro-processing, tourism, and manufacturing, may access the Investment Code's provisions for capital allowances and deductions under the Income Tax Act. These deductions reduce taxable profit in early operational years, which is material for businesses with high upfront capital expenditure.

The UIA also issues investment certificates that facilitate work permit processing for expatriate staff, reducing friction in building a cross-border management team.

Keep the following in mind:

- A minimum capital threshold applies: USD 250,000 for foreign investors to qualify for a UIA investment license

- Incentives are sector-specific; not all business types receive the same treatment

- The investment license is separate from company registration with the URSB

- Benefits apply to licensed projects, not automatically to all registered companies

Uganda's Investment Code Act 2019 allows foreign investors to hold investment licenses even before a local company is formally incorporated, enabling parallel processing of registration and licensing.

Double Taxation Agreements With Key Trade Partners

Uganda double taxation agreement benefits are most relevant when profits, dividends, royalties, or interest payments cross borders. Without treaty protection, the same income can be taxed twice: once in the country where it's earned and again where the recipient is resident. Uganda has concluded tax treaties with several significant trading and investment partners, including the United Kingdom, the Netherlands, Denmark, Norway, South Africa, India, and Mauritius, each reducing or eliminating this dual tax exposure.

Reduced Withholding Tax on Cross-Border Payments

Under Uganda's domestic Income Tax Act, withholding tax on dividends paid to non-residents is generally set at 15%. Where a treaty applies, this rate can be reduced, depending on the specific agreement and the ownership threshold met by the foreign recipient. For a holding company structured through a treaty jurisdiction such as Mauritius or the Netherlands, the reduction in withholding tax directly lowers the cost of repatriating profits.

Interest and royalty payments follow a similar pattern. Treaty provisions cap the tax withheld at source, which matters considerably if your firm licenses intellectual property into Uganda or provides intercompany financing.

Certainty on Permanent Establishment Rules

Each treaty also defines when a foreign entity's activities in Uganda constitute a taxable permanent establishment. This definition determines whether your business becomes liable for corporate income tax locally. Clearer boundaries reduce the risk of unexpected tax assessments, giving foreign-owned entities a more predictable operating position under the Uganda Revenue Authority's jurisdiction.

Understand Your Treaty Position Before You Structure

Speak with Expanship to map how Uganda's tax treaties apply to your specific ownership structure, profit flows, and investor residency before incorporation.

100% Foreign Ownership Permitted for Most Sectors

Under the Companies Act 2012, foreign nationals can hold 100% of the shares in a Ugandan private limited company. No mandatory local partner is required. This structural freedom is one of the more consequential Uganda 100 percent foreign ownership benefits, because it means you retain full control over decision-making, profit distribution, and business strategy from the outset.

- You are not required to dilute equity to a local shareholder to satisfy incorporation rules, which protects your ownership position and simplifies governance.

- Full ownership means all declared dividends flow to foreign shareholders without a statutory split, subject to applicable withholding tax under the Income Tax Act Cap 340.

- Because no joint venture is legally mandated, you avoid the negotiation, legal structuring, and ongoing relationship management that co-ownership arrangements typically require.

- Foreign investor ownership rights in Uganda extend to repatriation of profits and capital, governed by the Foreign Exchange Act and the Bank of Uganda's exchange control framework.

- Certain sectors, including sugar production, grain milling, and some public utilities, carry restrictions or licensing conditions under sectoral legislation, so confirming eligibility before incorporating is necessary.

This ownership model is not universal across East Africa. Kenya and Tanzania impose local ownership requirements in specific regulated industries, making the general permissiveness under Ugandan company law a structurally distinct feature for fully foreign-owned companies.

Affordable Setup and Operational Business Costs

Affordable business setup costs Uganda offers are a material factor for foreign companies evaluating entry into East Africa. Registering a private limited company through the Uganda Registration Services Bureau currently requires a nominal government filing fee, and the minimum share capital requirement for most private entities is not prescribed by statute at a fixed high threshold, keeping initial capitalization flexible.

Beyond registration, day-to-day operational expenses remain comparatively low. Office rental rates in Kampala's secondary business districts run significantly below equivalent space in Nairobi or Lagos, and local professional service fees — legal, accounting, secretarial — reflect a cost base that reduces the overhead burden on smaller foreign entities establishing a regional presence.

Labour costs also contribute to the overall cost structure. Uganda's wage levels for skilled administrative and mid-level professional staff are modest relative to most other Sub-Saharan African commercial hubs, without compromising the availability of English-speaking talent.

A foreign-owned private limited company in Uganda operating with five local employees, a leased Kampala office, and standard professional service retainers can realistically maintain annual operational overhead below USD 30,000 — a threshold that would be difficult to match in comparable East African commercial capitals.

Gateway to EAC and COMESA Trade Blocs

Uganda's dual membership in the East African Community (EAC) and the Common Market for Eastern and Southern Africa (COMESA) gives companies incorporated there preferential access to a combined market of over 800 million people. For a foreign business owner, this means your entity can export goods across member states at reduced or zero tariff rates without negotiating bilateral trade terms independently.

Under the COMESA Free Trade Area, qualifying goods traded between member states attract zero import duties. The EAC Customs Union further eliminates internal tariffs among its six partner states — Kenya, Tanzania, Rwanda, Burundi, South Sudan, and Uganda — while applying a Common External Tariff on imports from outside the bloc. A firm incorporated locally and meeting rules-of-origin requirements under these frameworks gains a structural cost advantage over foreign competitors supplying the same markets from outside the blocs.

COMESA membership advantages for businesses extend beyond tariffs. The bloc's trade facilitation instruments, including the COMESA Regional Payment and Settlement System (REPSS) and harmonized customs documentation, reduce transaction costs for cross-border trade.

Preferential tariff treatment under both the EAC Customs Union and COMESA requires your goods to meet the applicable rules-of-origin criteria; incorporation alone does not automatically qualify your products for reduced duty rates.

Strong Legal Framework Based on English Common Law

Uganda's legal system is grounded in English common law, a heritage that carries direct practical value for foreign investors. Contracts, corporate structures, and dispute resolution mechanisms follow principles recognizable to businesses from the UK, Commonwealth countries, and any jurisdiction with comparable legal traditions. This shared foundation reduces the interpretation risk that often complicates cross-border commercial relationships.

The Companies Act 2012

The primary statute governing corporate entities is the Companies Act 2012, which regulates incorporation, shareholder rights, director duties, and company administration. Because this Act draws from established Commonwealth company law principles, your legal counsel in a home jurisdiction such as the UK, Australia, or Canada will find the structural concepts familiar. This reduces the cost and time required to conduct legal due diligence before entering the market.

Contract Enforcement and Judicial Precedent

Uganda's courts apply the doctrine of binding precedent, meaning judicial decisions follow an established body of case law rather than being decided arbitrarily. For a foreign firm entering commercial agreements, this predictability matters: contract terms are interpreted against a consistent legal standard. The High Court of Uganda has a dedicated Commercial Division that handles business disputes, providing a specialized forum rather than a generalist court process.

Regulatory Oversight Structures

- The Uganda Registration Services Bureau administers company law compliance.

- The Judicature Act and Civil Procedure Act provide the procedural framework for enforcing judgments.

- Arbitration is recognized under the Arbitration and Conciliation Act, Cap 4, giving parties an alternative to litigation for resolving commercial disputes.

Growing Infrastructure and Digital Economy Support

Uganda's digital economy infrastructure benefits are increasingly relevant to foreign-owned companies that depend on connectivity, payments, and digital operations. The National Information Technology Authority (NITA-U) governs ICT infrastructure development, and the country has made measurable progress in extending fibre optic coverage, particularly in urban and peri-urban corridors.

Mobile money penetration in Uganda is among the highest on the continent, with platforms like MTN Mobile Money and Airtel Money deeply integrated into commercial transactions. For a foreign firm operating without an established local banking relationship, this infrastructure means payment collection and disbursement can function from day one.

The National Payments Act, 2020, provides a formal legal basis for digital financial services, giving businesses operating in fintech or e-commerce a defined regulatory environment rather than legal ambiguity. This reduces compliance uncertainty for firms structuring digital products for the local market.

Under the National Development Plan III (2020/21-2024/25), the government has allocated specific targets for digital infrastructure expansion, including last-mile internet connectivity and e-government services. Your firm can build on this public investment without carrying the underlying cost.

Key infrastructure and digital economy advantages for incorporated entities include:

- NITA-U manages a national data centre and provides shared hosting infrastructure that licensed operators can access

- The Uganda Communications Commission (UCC) regulates internet service providers, maintaining a structured licensing regime for digital businesses

- Mobile internet coverage extends to over 90% of the population, supporting digital-first business models

- The e-tax portal managed by the Uganda Revenue Authority (URA) allows online tax filing, reducing administrative friction for remote business owners

Why Uganda Stands Out Among African Business Destinations

Positioned within East Africa, Uganda draws comparison most naturally against Kenya, Rwanda, and Tanzania — three jurisdictions that target a similar profile of foreign investor and offer comparable regional market access. These are the countries a business owner evaluating incorporation options in the sub-region would realistically weigh. The comparison reveals that across several structural parameters, Uganda holds a competitive position, particularly on ownership rules, tax rates, and trade bloc membership.

Where Uganda vs other African countries business benefits become most visible is in the combination of factors rather than any single metric. A 30% corporate tax rate applies under the Income Tax Act, Rwanda sits at 30% as well, while Kenya's headline rate reaches 30% for resident companies with surcharges applicable in certain sectors. Full foreign ownership is permitted across most sectors without a mandatory local partner requirement, a condition that does not apply uniformly across all comparable jurisdictions. Simultaneous membership in both the EAC and COMESA gives incorporated entities preferential access to a combined market that neither a Rwanda-only nor Tanzania-only structure replicates in full. These factors, taken together, form the basis of Uganda's profile as a Uganda top African business destination advantages context rather than any single headline figure.

| Parameter | Uganda | Kenya | Rwanda | Tanzania |

|---|---|---|---|---|

| Corporate Tax Rate | 30% | 30% (plus levies) | 30% | 30% |

| Foreign Ownership | 100% most sectors | 100% most sectors | 100% most sectors | Restrictions in select sectors |

| EAC Membership | Yes | Yes | Yes | Yes |

| COMESA Membership | Yes | Yes | Yes | No |

| Common Law Framework | Yes | Yes | No (Civil Law hybrid) | Yes |

| Company Registration Body | URSB | Business Registration Service | RDB | BRELA |

Compliance Services for Companies in Uganda

Maintain your Uganda company's good standing with ongoing statutory filings, annual returns, and regulatory obligations managed through Expanship.

Conclusion

The benefits of incorporating in Uganda rest on a convergence of structural and regulatory factors that are directly relevant to foreign investors. Access to EAC and COMESA trade blocs through a single registered entity extends your commercial reach across markets representing hundreds of millions of consumers. The Uganda Investment Authority's incentive framework, underpinned by the Investment Code Act, provides a formalised basis for capital protection and sector-specific reliefs that reduce early-stage financial exposure.

Permitted 100% foreign ownership across most sectors removes a structural barrier that restricts foreign participation in numerous comparable African markets. Combined with a corporate tax rate governed by the Income Tax Act and a registration process administered through the Uganda Registration Services Bureau, the cost and time involved in establishing a presence here are materially lower than in many regional alternatives.

What determines suitability is your specific industry, ownership structure, and trade orientation. A firm focused on regional goods distribution will engage these advantages differently than one operating in financial services or digital commerce. The legal foundation in English common law also means that contracts, dispute mechanisms, and entity structures are interpretable within a framework familiar to common-law jurisdictions globally. For businesses assessing their next incorporation decision, Uganda presents a defined and verifiable set of conditions worth examining against your operational requirements.

Start Your Uganda Company Formation With Expanship Today

Expanship handles Uganda company formation end-to-end, covering the entity structures and compliance obligations examined throughout this blog. Whether your business qualifies as a Private Limited Company under the Companies Act 2012, or falls under sector-specific licensing governed by the Uganda Investment Authority, Expanship manages the process in direct coordination with the Uganda Registration Services Bureau.

Expanship's service scope across Uganda business registration includes:

- Document preparation, notarisation, and apostille or consular legalisation where required

- Registered office address and local registered agent provision

- Filing and liaison with the URSB, including name reservation and certificate of incorporation

- Post-incorporation compliance management covering annual returns and regulatory renewals

- Introduction to local banking institutions for corporate account opening

Reach out to Expanship Uganda to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Registration through the Uganda Registration Services Bureau online portal can be completed within one to three working days once all required documents are submitted correctly. The process covers name reservation, filing of the Memorandum and Articles of Association, and issuance of a certificate of incorporation. Delays typically arise from incomplete submissions or name conflicts, not from the registration system itself.

The standard corporate income tax rate is 30% under the Income Tax Act, Cap. 340. Companies in designated sectors or free zones may qualify for reduced rates or exemptions administered through the Uganda Investment Authority. The applicable rate depends on the nature of the business activity and whether an investment license with associated incentives has been granted.

Uganda's tax treaties can reduce withholding tax rates on dividends, interest, and royalties paid to residents of treaty partner countries. Without a treaty, the standard withholding tax rates under the Income Tax Act apply. The actual rate a foreign investor faces on repatriated profits depends on whether a relevant tax treaty exists between Uganda and the investor's country of residence.

No statutory requirement mandates that a locally resident director be appointed for a private limited company registered under the Companies Act, 2012. A company may be incorporated with entirely foreign directors, provided the prescribed registration documents are properly executed and filed with the URSB. Certain regulated sectors may impose additional director residency conditions, which are set by the relevant sector-specific regulator rather than the Companies Act.

The Uganda Investment Authority administers incentives under the Investment Code Act, 2019, including capital allowances, VAT exemptions on certain capital equipment, and preferential corporate tax treatment for qualifying investments in priority sectors. Access to these incentives generally requires obtaining an investment license from the UIA and meeting minimum capital thresholds, which differ between domestic and foreign investors. Businesses operating in sectors such as manufacturing, agro-processing, and ICT are among those that may qualify.

As a member of both the East African Community and COMESA, a company registered in Uganda may benefit from preferential tariff arrangements and reduced trade barriers when exporting to member states. The EAC Customs Union protocol, for instance, establishes a common external tariff and eliminates most internal duties among partner states. The extent of preferential access depends on the rules of origin requirements applicable to your specific goods or services.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.