Key Takeaways

- Uganda's business entities are registered and maintained by the Uganda Registration Services Bureau (URSB) under the Companies Act 2012, with taxation administered by the Uganda Revenue Authority under the Income Tax Act Cap 340.

- The private limited company is the most commonly registered entity in Uganda, offering liability protection with fewer public disclosure obligations than a public limited company.

- Foreign entities can establish a presence in Uganda without full incorporation by registering as an external company (branch office) or representative office through the URSB.

- Partnerships, sole proprietorships, and companies limited by guarantee remain available for professionals, individual traders, and non-profit or membership organisations respectively, each carrying distinct implications for liability and governance.

Introduction to Entity Types in Uganda

Uganda is a landlocked East African nation bordered by Kenya, Tanzania, Rwanda, the Democratic Republic of Congo, and South Sudan. It operates as an independent republic, and business registration falls under the jurisdiction of the Uganda Registration Services Bureau (URSB), the statutory body responsible for incorporating and maintaining records of all legal entities in the country.

The tax regime is resident-based, with corporate income tax, withholding tax, and value-added tax administered by the Uganda Revenue Authority under the Income Tax Act Cap 340.

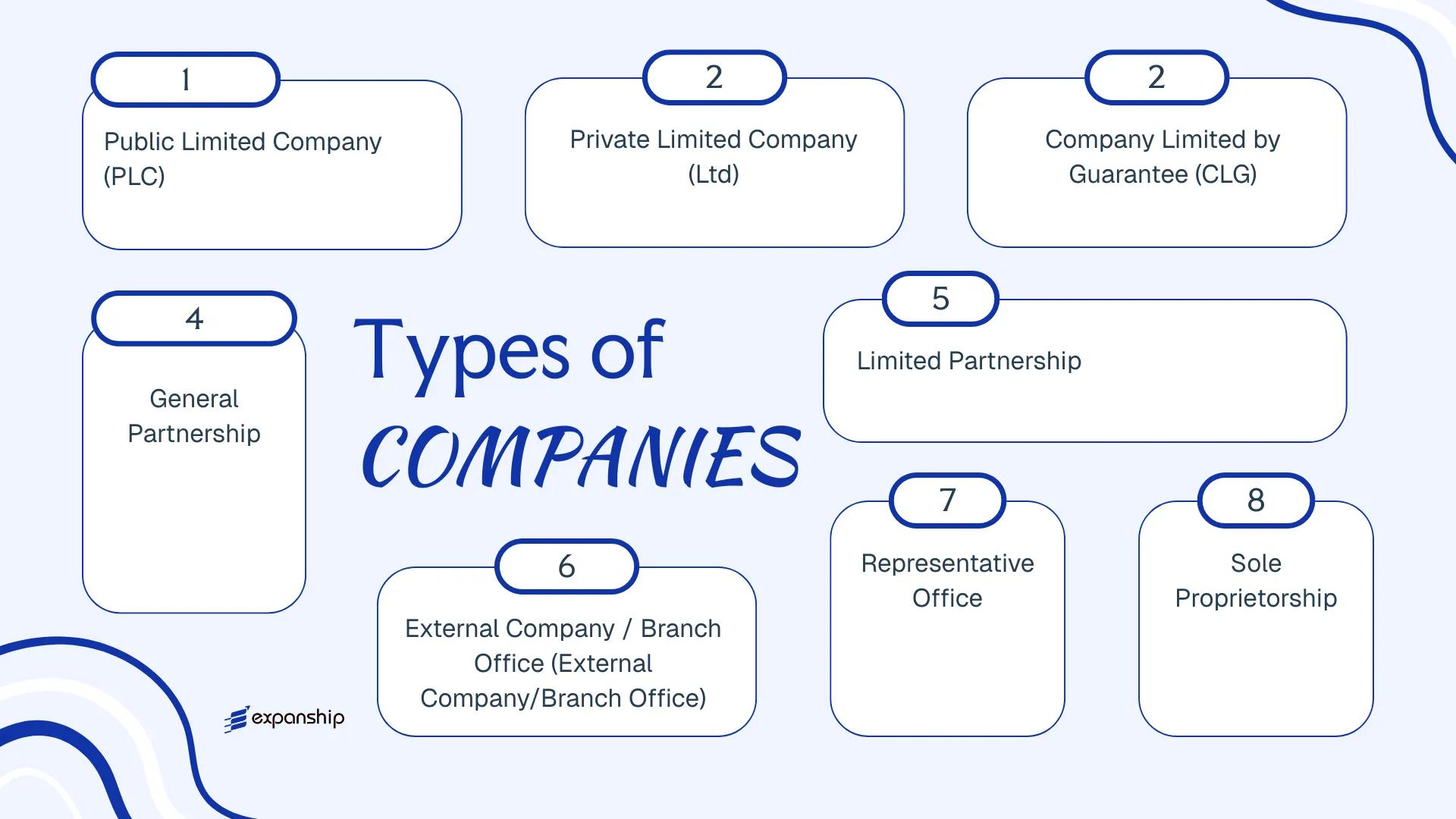

Understanding the types of business entities in Uganda is a prerequisite for any investor, entrepreneur, or foreign firm planning to establish a presence in the country. The available structures include the Public Limited Company, Private Limited Company, Company Limited by Guarantee, General Partnership, Limited Partnership, External Company (Branch Office), Representative Office, and Sole Proprietorship.

Each structure carries distinct implications for liability, governance, taxation, and foreign ownership — and this article examines each in detail.

An Overview of Business Structures in Uganda

Uganda's legal framework provides several distinct entity types, each governed primarily by the Companies Act 2012 and, for partnerships, the Partnership Act. The Registration Services Bureau (URSB) administers company formation and maintains the official register of businesses. Each structure carries different implications for liability, ownership, and permitted commercial activity.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated body | Limited to shares | Taxed | Yes | 7 shareholders | URSB | Companies Act 2012 |

| Private Limited Company (Ltd) | Incorporated body | Limited to shares | Taxed | Yes | 1 shareholder | URSB | Companies Act 2012 |

| Company Limited by Guarantee | Incorporated body | Limited to guarantee | Taxed / Exempt | Restricted | 1 member | URSB | Companies Act 2012 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | URSB | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | URSB | Partnership Act |

| External Company / Branch | Foreign entity extension | Parent liable | Taxed | Yes | N/A | URSB | Companies Act 2012 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | URSB | Companies Act 2012 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | URSB | Registration of Business Names Act |

Each of these structures is examined in full in the sections below.

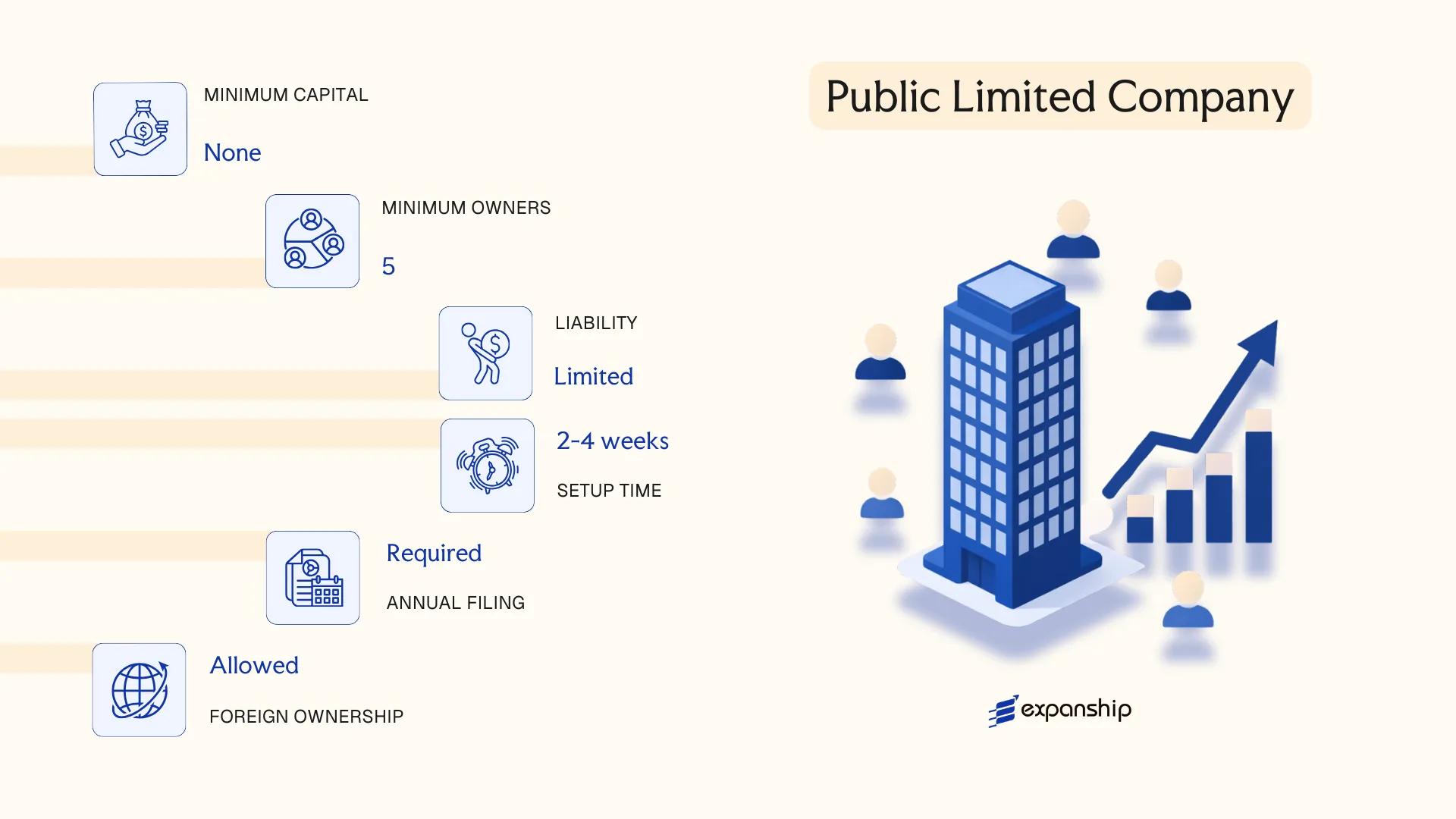

Public Limited Company (PLC) Under the Companies Act 2012

Governed by the Companies Act 2012, a Public Limited Company (PLC) is the vehicle used for Uganda public limited company PLC registration where public capital access is the primary objective. The entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the nominal value of shares held.

Unlike its private counterpart, a PLC may offer shares to the general public and, subject to approval by the Capital Markets Authority (CMA), list on the Uganda Securities Exchange (USE).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Incorporated under the Companies Act 2012; separate legal personality |

| Members & Directors | Min. 2 shareholders; no statutory maximum | Min. 2 directors required; at least 1 must ordinarily reside in Uganda |

| Share Capital | No statutory minimum prescribed under the Act | Sufficient authorised capital required for CMA listing; stated in Uganda Shillings (UGX) |

| Local Presence | Registered office in Uganda required | Physical address; not a P.O. Box |

| Share Transferability | Shares freely transferable | No restrictions on transfer, unlike a private company |

| Privacy | Accounts and shareholder register are publicly accessible | Filed with the Uganda Registration Services Bureau (URSB) |

Focus Points

- Taxation: Corporate income tax applies at 30%; VAT at 18% on taxable supplies; withholding tax rates vary by payment type; stamp duty applies on share transfers and certain instruments.

- Annual Compliance: Annual returns and audited financial statements must be filed with URSB; listed PLCs face additional continuous disclosure obligations under CMA regulations.

- Listing Requirements: CMA approval and USE rules govern any public offering; the entity must meet minimum capital, governance, and disclosure thresholds before listing.

- Treaty Access: Uganda has double taxation agreements with several jurisdictions, including the EAC member states, which a PLC may access on qualifying income.

- Conversion: A PLC may be re-registered as a private company under the Companies Act 2012, provided shares are no longer publicly held and statutory conditions are satisfied.

Closing Paragraph

A PLC suits large-scale commercial enterprises, institutional joint ventures, and businesses intending to raise equity through public markets or the Uganda Securities Exchange. The ability to access public capital is its principal structural advantage; however, the ongoing regulatory burden, mandatory audited disclosures, and CMA oversight make it a disproportionately complex structure for businesses that do not require public financing.

PLCs are best suited for established businesses with significant capital requirements that intend to list publicly or attract institutional investors in Uganda.

Company Incorporation in Uganda

Expanship assists with end-to-end incorporation of Ugandan companies, including PLC formation and URSB registration.

Private Limited Company (Ltd) Under the Companies Act 2012

A Uganda private limited company Ltd formation is governed by the Companies Act 2012, which replaced the earlier Companies Act (Cap. 110) and brought the country's corporate framework broadly in line with modern Commonwealth standards. The Act establishes the private limited company as a separate legal entity, meaning the firm holds rights, obligations, and liabilities in its own name, distinct from its shareholders.

Liability of members is capped at the amount unpaid on their shares, providing a defined ceiling on personal exposure. This structure suits both domestic and foreign-owned businesses seeking formal legal standing without the disclosure obligations of a public company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Ltd) | Incorporated under the Companies Act 2012 |

| Members | Shareholders: min. 1, max. 50 | Excludes employees who are shareholders; shareholder can also serve as director |

| Directors | Min. 1 director | No statutory requirement for a local director, though a local contact is advisable |

| Local Presence | Registered office address in Uganda | Must be a physical address; PO Box alone is not sufficient |

| Share Capital | No statutory minimum; denominated in UGX | Shares must be fully described in the Memorandum and Articles of Association |

| Privacy | Shareholder and director details filed with URSB | Register of members is not publicly searchable online but accessible upon formal request |

Focus Points

- Taxation: Subject to corporate income tax at 30% on net profits; VAT applies at 18% on taxable supplies above the registration threshold; withholding tax rates vary by payment type (typically 6–15%); stamp duty applies on share transfers and certain instruments.

- Annual Compliance: Required to file annual returns with the Uganda Registration Services Bureau (URSB) and maintain audited accounts where applicable under the Act.

- Treaty Access: Uganda has a limited double tax treaty network; treaty availability depends on the jurisdiction of the parent or counterparty.

- Restrictions: Share transfer to non-members requires board or shareholder approval per the company's Articles; public share offerings are prohibited.

- Conversion: A private limited company may convert to a public limited company through a formal procedure under the Companies Act 2012, subject to URSB approval.

Closing

Private limited companies are the most widely used structure for trading operations, subsidiary establishments, and joint ventures in Uganda. The entity offers defined liability protection and full legal standing, though the 50-shareholder cap restricts its use for larger capital-raising exercises.

This structure suits small-to-medium enterprises, foreign subsidiaries, and joint venture vehicles where ownership is concentrated and public fundraising is not required.

Company Limited by Guarantee

A company limited by guarantee Uganda is governed by the Companies Act 2012, the same legislation that regulates share-based companies, though the structural mechanics differ substantially. Rather than issuing share capital, this entity type relies on members who each commit to a fixed guarantee amount payable in the event of winding up.

Registered under the Uganda Registration Services Bureau (URSB), this structure carries separate legal personality and limited liability. It sits at the intersection of corporate law and civil society, making it a common vehicle for non-governmental, charitable, and membership-based organisations that require formal legal standing without profit distribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated body corporate | Separate legal personality; not a partnership or association |

| Members | Minimum 2; no statutory maximum | No shareholders; members hold governance rights, not equity |

| Directors | Minimum 2 directors required | At least one director must ordinarily reside in Uganda |

| Local Presence | Registered office in Uganda | Physical address required; P.O. Box alone is not sufficient |

| Capital | No share capital; guarantee amount typically UGX 100,000–500,000 per member | Guarantee is a contingent liability, not paid-up capital |

| Privacy | Director and member details filed with URSB | Register of members is not fully public but regulatory disclosures apply |

Focus Points

- Taxation: Exempt from income tax if registered as a public benefit organisation under the Income Tax Act, but must apply separately for that status; VAT obligations apply where taxable supplies are made; withholding tax rules still apply to payments made by the entity.

- Annual Compliance: Annual returns must be filed with URSB; financial statements are required; entities receiving donor funding may face additional reporting requirements from the NGO Bureau.

- NGO Registration: Organisations carrying out NGO activities must also register with the NGO Bureau under the Non-Governmental Organisations Act 2016, a separate process from URSB incorporation.

- Profit Distribution: Surplus funds must be reinvested into the stated objects; distribution to members is prohibited by the constitutional documents.

- Conversion: Conversion to a share-based company is not a standard procedure under the Companies Act 2012; dissolution and re-incorporation is the typical route if the business purpose changes.

Closing Paragraph

This structure is used primarily by associations, foundations, professional bodies, and civil society organisations that require legal standing to own property, enter contracts, and receive funding. The absence of share capital simplifies governance, but the dual registration requirement under both URSB and the NGO Bureau adds administrative complexity that organisations should account for at formation stage.

Best suited for non-profits, membership associations, and civil society organisations that need formal legal personality without equity ownership.

Partnerships in Uganda [General Partnership, Limited Partnership]

Partnership registration in Uganda is governed by the Partnership Act, Cap 114, which recognises two distinct structures: general partnerships and limited partnerships. Neither structure carries a separate legal personality from its partners under the Act, which has direct implications for liability exposure and debt obligations.

Formed without mandatory incorporation, a partnership comes into existence through agreement, written or oral. Registration with the Uganda Registration Services Bureau (URSB) is required for limited partnerships, while general partnerships operating under a business name must also register that name.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality |

| Members | Partners (minimum 2, no statutory maximum for most sectors) | Min. 1 general partner + 1 limited partner; no statutory maximum |

| Liability | All partners bear unlimited joint liability | General partners: unlimited; limited partners: capped at capital contribution |

| Local Presence | Registered business address in Uganda required | Registered business address in Uganda required |

| Capital | No minimum capital prescribed by statute | No minimum capital prescribed; limited partner's contribution defines liability ceiling |

| Privacy | Partner details filed with URSB; publicly accessible | Same as general partnership |

Focus Points

- Taxation: Partnerships are fiscally transparent; income is taxed at the partner level under the Income Tax Act, Cap 340, at applicable individual or corporate rates. VAT registration applies if annual turnover exceeds the prescribed threshold.

- Annual Compliance: Business name renewal and filing of any prescribed returns with URSB apply; limited partnerships have additional filing obligations tied to partner changes.

- Restrictions: Banking and certain regulated sectors restrict or prohibit the partnership structure; check sector-specific licensing requirements.

- Conversion: No automatic conversion mechanism exists; dissolution and re-incorporation are typically required to transition to a limited liability structure.

Sub-Types

General Partnership

All partners contribute to management and carry unlimited personal liability for the firm's debts and obligations. This structure suits professional service arrangements, such as legal or accounting practices, where active participation across partners is expected.

Limited Partnership

At least one general partner manages the business with unlimited liability, while limited partners contribute capital and remain passive. The limited partner's liability is confined to their contributed amount, making this structure relevant for investment vehicles or joint ventures where capital contributors seek defined risk exposure.

Closing

Partnerships suit smaller trading operations, professional services, and joint ventures where administrative simplicity outweighs the need for limited liability. The absence of separate legal personality, however, exposes general partners to personal liability for all business obligations.

This structure is best suited for small professional firms or two-party ventures where partners have high mutual trust and a low appetite for administrative overhead.

Foreign Business Presence in Uganda [External Company/Branch Office, Representative Office]

Registering a foreign company branch office Uganda falls under the Companies Act 2012, specifically Part X, which governs "external companies." An external company is a foreign-incorporated entity that establishes a place of business within the country. It does not acquire separate legal personality distinct from its parent; the parent company remains fully liable for the branch's obligations.

Registration is handled by the Uganda Registration Services Bureau (URSB). Once registered, the external company must file its parent's constitutional documents, particulars of local directors or agents, and a registered office address with URSB.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign-incorporated entity | No separate legal personality; parent bears full liability |

| Designated Representative | At least one locally resident authorised agent or director | Must be registered with URSB |

| Local Presence | Registered physical office address in Uganda | Cannot use a P.O. Box as sole address |

| Capital | No statutory minimum capital requirement | Parent's capital structure applies |

| Annual Filings | Financial statements of the parent company filed with URSB | Local accounts may also be required |

| Privacy | Parent company documents become part of public record at URSB | Limited confidentiality |

Focus Points

- Taxation: Branch profits are subject to corporation tax at 30%; VAT registration is required if annual taxable turnover exceeds UGX 150 million; withholding tax applies to remittances and payments to non-residents at rates ranging from 6% to 15% depending on the payment type.

- Economic Substance: The branch must demonstrate genuine operational activity in Uganda; purely passive registrations attract scrutiny from the Uganda Revenue Authority (URA).

- Annual Compliance: Annual returns, updated parent financials, and any changes to authorised agents must be lodged with URSB within prescribed deadlines.

- Treaty Access: Uganda has double tax agreements with select jurisdictions; treaty benefits available to the parent may extend to branch income, subject to URA interpretation.

- Restrictions: Certain regulated sectors, including banking and insurance, require additional licensing from sector-specific regulators such as the Bank of Uganda or the Insurance Regulatory Authority of Uganda before a branch can operate.

Sub-Types

External Company (Branch Office)

An external company actively conducting trade or business in Uganda registers as a branch under Part X of the Companies Act 2012. This structure is used by foreign firms seeking operational presence, including sales, service delivery, or project execution, without incorporating a separate local entity.

Representative Office

A representative office is a lighter-footprint option used for market research, liaison, and promotional activities. It cannot generate revenue or enter into commercial contracts on behalf of the parent. Regulatory treatment is less clearly codified in statute compared to the branch, so its permissible activities should be confirmed with URSB and relevant sector regulators prior to setup.

Closing

External companies suit foreign businesses that need operational presence without the administrative structure of a locally incorporated entity, though the absence of limited liability protection for the parent is a material drawback for higher-risk activities.

Foreign companies entering Uganda for project-based work, government contracts, or initial market entry before committing to full local incorporation.

Sole Proprietorship

Sole proprietorship registration Uganda falls under the Registration of Business Names Act, Cap 116, which requires any individual trading under a name other than their own to register with the Uganda Registration Services Bureau (URSB). This structure carries no separate legal personality — the owner and the business are treated as one legal person, meaning personal assets are directly exposed to business liabilities.

Registration is straightforward. You submit a Business Name Registration form to the URSB, pay the prescribed fee, and receive a certificate of registration. No minimum capital is required, and the process does not demand a local partner or co-owner.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | Single proprietor | One individual only; no shareholders or directors |

| Local Presence | Physical address required | Registered business address in Uganda |

| Capital | No statutory minimum | Owner funds operations personally |

| Liability | Unlimited personal liability | Personal assets at risk for business debts |

| Privacy | Business name publicly registered at URSB | Owner's details on public record |

Focus Points

- Taxation: Subject to individual income tax under the Income Tax Act, Cap 340; VAT registration is mandatory if annual turnover exceeds UGX 150 million; no corporate income tax applies.

- Annual Compliance: Annual renewal of the business name registration with URSB is required to maintain active status.

- Treaty Access: No access to double tax treaties, as sole proprietorships are not recognised as qualifying entities under Uganda's tax agreements.

- Conversion: Can be converted into a private limited company upon incorporation under the Companies Act 2012, though assets must be formally transferred.

- Restrictions: Cannot raise equity capital or admit investors without restructuring into a different entity form.

Closing

A sole proprietorship suits individual traders, freelancers, and small service providers who operate domestically with limited transactional complexity. The structure offers minimal administrative overhead but provides no liability protection whatsoever.

Best suited for Uganda-resident individuals testing a local business concept at small scale before committing to formal incorporation.

How to Choose the Right Entity Type in Uganda

Selecting the right structure at the outset shapes your tax position, liability exposure, and regulatory obligations for the life of the business — getting it wrong has concrete, recoverable but costly consequences.

Why Your Entity Choice Matters

The wrong entity creates real operational and legal problems:

- Registering an external company without filing the required documents with the Uganda Registration Services Bureau (URSB) while actively trading locally constitutes a breach of the Companies Act 2012 and can result in striking off or financial penalties.

- Choosing a structure that does not qualify as a resident entity under Uganda's Income Tax Act Cap 340 may disqualify your business from accessing Uganda's double tax agreements, meaning withholding tax reductions available to counterparts cannot be claimed.

- Forming a company where a trust or other vehicle would better serve asset protection locks you into annual shareholder obligations, statutory filings, and potential audit requirements that would not otherwise apply.

- Selecting a private limited company when your operations are conducted by a single consultant adds mandatory annual return obligations and, where audited accounts are required, recurring professional costs that a sole proprietorship would not carry.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, or operation in a licensed sector such as banking or insurance each points toward a distinct structure under Ugandan law.

- Ownership Structure: A sole founder with no plans for external investment has different requirements than a multi-party venture that needs a defined board and shareholder agreement.

- Tax Objectives: Your need for treaty access, a specific tax regime, or exemption status under the Income Tax Act Cap 340 should directly inform which entity you register.

- Public Disclosure Tolerance: URSB maintains a public register of directors and shareholders; if confidentiality is a priority, nominee arrangements or alternative structures warrant consideration.

- Substance Capacity: If your business cannot realistically maintain staff, a physical office, and decision-making functions in-country, certain regulated structures may impose compliance obligations your setup cannot meet.

- Exit and Restructuring: Not all Ugandan entities support redomiciliation or conversion; confirm that your chosen structure permits the exit route you may need before registering.

Compliance Services for Companies in Uganda

Ongoing compliance support for Ugandan companies, including annual returns, statutory filings, and URSB obligations.

Conclusion

Setting up a company in Uganda requires matching your operational model to the right legal structure under the Companies Act 2012, administered by the Uganda Registration Services Bureau (URSB).

The private limited company is the most commonly registered entity, suited to resident and foreign entrepreneurs seeking liability protection with fewer disclosure obligations than a public company. A public limited company fits businesses intending to raise capital from the public. A company limited by guarantee serves non-profit and membership organisations. Partnerships offer a straightforward structure for professionals operating under shared ownership, while a sole proprietorship suits individual traders with limited scale. External companies and representative offices address foreign entities requiring a local footprint without full incorporation.

URSB has progressively digitised registration processes, and Uganda's expanding double taxation agreement network continues to develop. Expanship's team works directly with these frameworks to support your entity selection and formation.

How Expanship Can Assist You

Expanship Uganda company incorporation services cover the full registration process under the Companies Act 2012, from selecting the right entity structure to filing with the Uganda Registration Services Bureau (URSB). Whether your business involves a private limited company, an external company branch, or a company limited by guarantee, our team handles the procedural and legal requirements specific to each structure.

From initial document preparation through to post-incorporation obligations, our corporate services in Uganda include:

- Memorandum and Articles of Association drafting and notarization

- URSB filing and company registration liaison

- Registered office and local agent provision

- Tax Identification Number (TIN) registration with the Uganda Revenue Authority

- Ongoing annual returns and compliance management

- Banking introduction assistance for your newly registered entity

Get in touch with Expanship Uganda to discuss your specific business setup requirements.

Frequently Asked Questions (FAQ)

The private limited company (Ltd) is the most frequently incorporated entity type, registered under the Companies Act 2012. Its appeal stems from limited liability protection for shareholders combined with a straightforward compliance structure that suits both local entrepreneurs and foreign investors.

A Private Limited Company restricts share transferability and cannot offer shares to the public, whereas a Public Limited Company (PLC) may list on the Uganda Securities Exchange and raise capital from public investors. Both structures carry equivalent corporate tax obligations under the Income Tax Act, but the PLC faces considerably more disclosure and governance requirements, including audited financial statements filed with URSB.

Among registered structures, the Company Limited by Guarantee does not issue shares, meaning no shareholder register is publicly associated with equity ownership. Nominee arrangements are permissible under Ugandan law, though beneficial ownership disclosure requirements have expanded in recent years under anti-money laundering regulations.

A sole proprietorship and a private limited company can each be formed by one individual. General partnerships require a minimum of two partners, and a PLC requires at least two shareholders, making these structures unsuitable for single-person ownership.

Foreigners may register a private limited company, a PLC, or a company limited by guarantee under the Companies Act 2012. An external company (branch office) is also available for foreign corporations that wish to operate without incorporating a separate local entity, subject to registration with URSB and compliance with the Investment Code Act.

The Companies Act 2012 provides for the re-registration of a private company as a public company and vice versa, subject to URSB approval and satisfaction of the relevant share capital and governance requirements. Conversion from a company structure to a partnership or sole proprietorship is not a direct statutory process and would require dissolution and fresh registration.

Private limited companies, PLCs, and companies limited by guarantee each hold separate legal personality distinct from their members. Sole proprietorships and general partnerships do not — the owner or partners remain personally liable for all obligations of the business.

A sole proprietorship registered under the Registration of Business Names Act faces the lightest compliance burden, with no annual return filing requirement comparable to that imposed on companies. General partnerships sit in a similar position, though the absence of limited liability makes both structures less suitable for higher-risk commercial activities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.