Key Takeaways

- Sierra Leone's company formation framework is governed by the Companies Act 2009 and administered by the Corporate Affairs Commission, which maintains the national register for both domestic and foreign entities.

- Private companies limited by shares represent the most common registration choice for foreign and domestic investors under Sierra Leone's corporate legal framework.

- Foreign entities seeking a direct operational presence in Sierra Leone can structure their entry as an external company or branch office, rather than incorporating a new domestic entity.

- Companies limited by guarantee serve non-profit and membership-based purposes, while unlimited companies remain rare due to the full personal liability exposure they impose on members.

Introduction to Entity Types in Sierra Leone

Sierra Leone is a coastal West African nation bordered by Guinea to the north and east, and Liberia to the southeast. An independent republic since 1961, it operates under a legal framework that draws from English common law tradition, with company formation governed by the Companies Act 2009. Business registration falls under the jurisdiction of the Corporate Affairs Commission, which maintains the national register of companies and oversees compliance obligations for both domestic and foreign entities.

The country applies a territorial-based tax system, meaning resident companies are taxed on income sourced within the country.

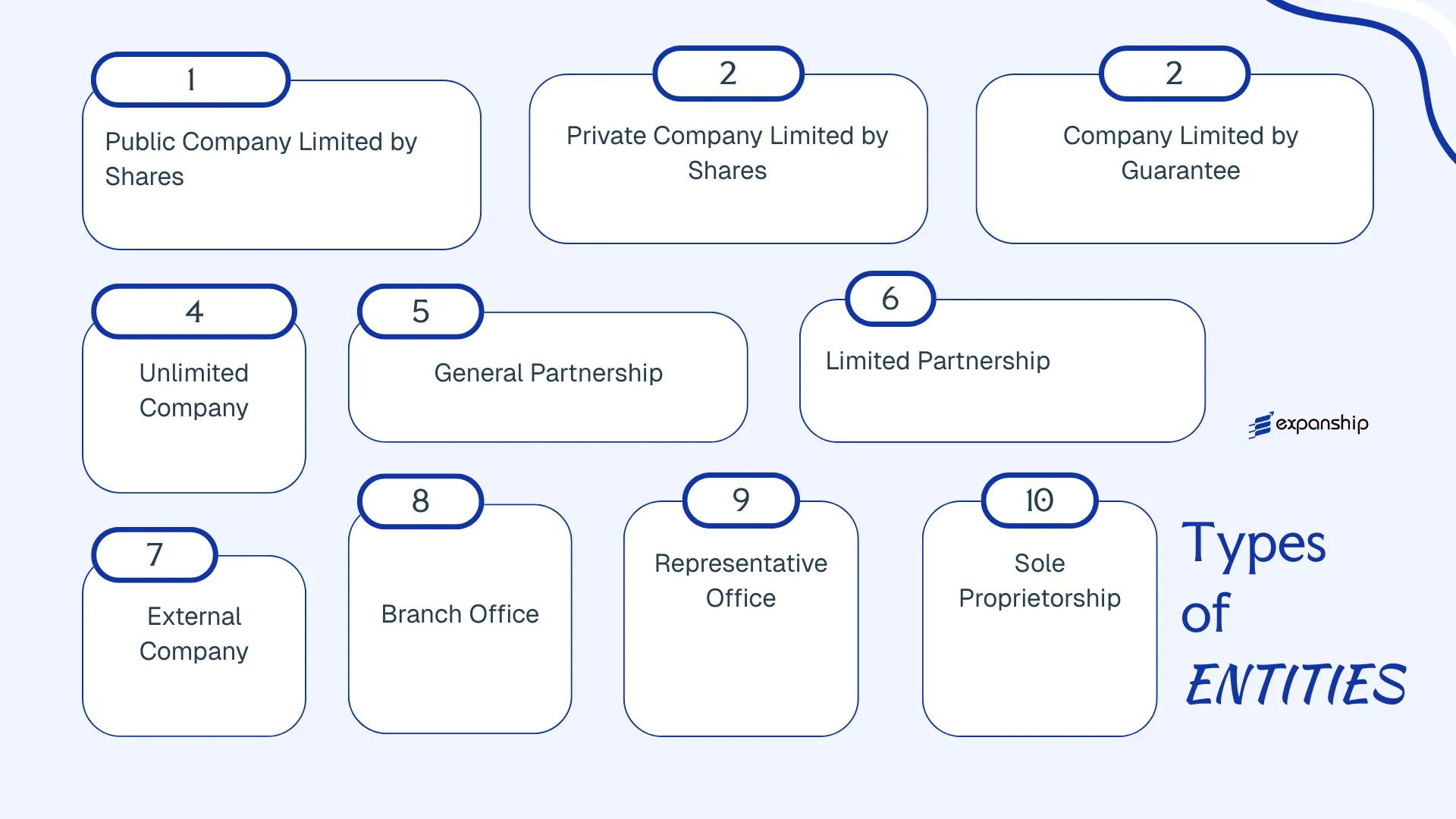

Available business entity types in Sierra Leone include the public company limited by shares, private company limited by shares, company limited by guarantee, unlimited company, general partnership, limited partnership, external company, branch office, representative office, and sole proprietorship. Each structure carries distinct liability, governance, and registration requirements that directly affect how your business operates and what obligations it carries. This article examines each of these legal entities in detail — covering formation requirements, ownership rules, and practical use cases.

An Overview of Business Structures in Sierra Leone

Several distinct entity types are available to businesses operating under the Companies Act 2009, which serves as the primary legislation governing corporate formation and conduct. The Corporate Affairs Commission (CAC) administers registration across these structures, each of which is designed for a different commercial purpose.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company Limited by Shares | Incorporated company | Limited to shares | Taxable | Permitted | 7 shareholders | Corporate Affairs Commission | Companies Act 2009 |

| Private Company Limited by Shares | Incorporated company | Limited to shares | Taxable | Permitted | 1 shareholder | Corporate Affairs Commission | Companies Act 2009 |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxable / Exempt | Permitted | 1 member | Corporate Affairs Commission | Companies Act 2009 |

| Unlimited Company | Incorporated company | Unlimited | Taxable | Permitted | 1 member | Corporate Affairs Commission | Companies Act 2009 |

| General Partnership | Unincorporated entity | Joint and several | Taxable | Permitted | 2 partners | Corporate Affairs Commission | Partnership Act |

| Limited Partnership | Unincorporated entity | Mixed liability | Taxable | Permitted | 2 partners | Corporate Affairs Commission | Partnership Act |

| External Company | Foreign corporate entity | Per home jurisdiction | Taxable | Permitted | N/A | Corporate Affairs Commission | Companies Act 2009 |

| Branch Office | Foreign company extension | Per parent company | Taxable | Permitted | N/A | Corporate Affairs Commission | Companies Act 2009 |

| Representative Office | Non-trading presence | Per parent company | Generally exempt | Not permitted | N/A | Corporate Affairs Commission | Companies Act 2009 |

| Sole Proprietorship | Unincorporated entity | Unlimited personal | Taxable | Permitted | 1 owner | Corporate Affairs Commission | Business Registration |

Each of these structures is examined in full in the sections below.

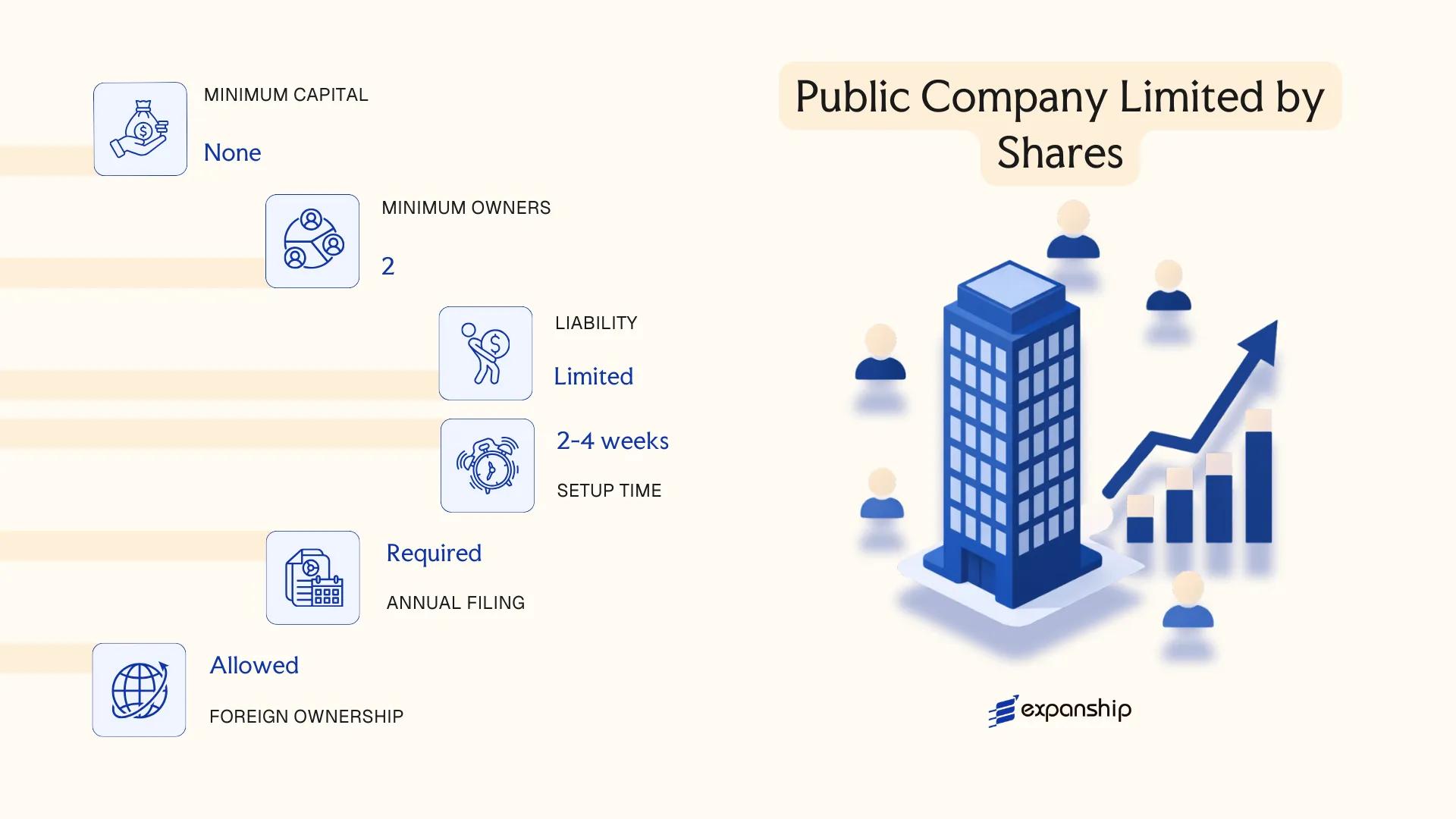

Public Company Limited by Shares

A public limited company Sierra Leone framework is governed by the Companies Act 2009, which consolidates the rules for formation, governance, and dissolution of companies registered in the country. This structure carries separate legal personality, meaning the entity exists independently of its shareholders, and liability is confined to the amount unpaid on shares held.

Registered with the Corporate Affairs Commission (CAC) of Sierra Leone, a public company may offer its shares to the general public and, subject to regulatory approval, list on the Sierra Leone Stock Exchange (SLSE). This makes it the appropriate vehicle for large-scale capital mobilisation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under the Companies Act 2009 |

| Members | Shareholders (min. 7; no statutory maximum) | Directors: min. 2; a company secretary is required |

| Local Presence | Registered office in Sierra Leone | Must maintain a physical registered address |

| Capital | Leone (SLL); no statutory minimum paid-up capital prescribed | Authorised capital stated in memorandum; shares must be fully described in articles |

| Disclosure | Accounts and annual returns filed publicly with CAC | Lower privacy than private structures |

Focus Points

- Taxation: Subject to corporate income tax (currently 30% standard rate), VAT at 15%, withholding taxes on dividends, interest and royalties, and stamp duty on share transfers.

- Annual Compliance: Must hold AGMs, file audited financial statements, and submit annual returns to CAC within prescribed deadlines.

- Stock Exchange Listing: Sierra Leone PLC registration on the SLSE requires additional approval from the Bank of Sierra Leone and compliance with SLSE listing rules.

- Conversion: Can convert to a private company by special resolution, subject to CAC approval under the Companies Act 2009.

- Restrictions: Cannot commence business until a trading certificate is issued by CAC following incorporation.

Closing

This structure suits businesses seeking broad public investment, including large trading operations, financial institutions, and infrastructure ventures. The ability to access public capital markets is the principal advantage; however, mandatory public disclosure of financials and the higher compliance burden make it unsuitable for closely-held or confidentiality-sensitive operations.

Large enterprises, financial institutions, or ventures intending to raise capital from the public or pursue a Sierra Leone Stock Exchange listing.

Company Incorporation in Sierra Leone

Incorporate a public or private company in Sierra Leone with end-to-end support from entity selection through CAC registration.

Private Company Limited by Shares

A private company limited by shares Sierra Leone is governed by the Companies Act 2009, administered by the Corporate Affairs Commission (CAC). The entity holds separate legal personality, meaning it can own property, enter contracts, and sue or be sued in its own name, distinct from its shareholders.

Shareholder liability is capped at the amount unpaid on their shares. This structure combines the protection of limited liability with operational flexibility suited to closely held businesses, making it the most commonly registered commercial entity in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under the Companies Act 2009 |

| Members | Shareholders: min. 1, max. 50 | Shares cannot be offered to the general public |

| Directors | Min. 1 director required | At least one director must be a natural person |

| Local Presence | Registered office in Sierra Leone | Must maintain a physical local address; registered agent not mandated by statute but commonly used |

| Capital | Leone (SLE); no statutory minimum | Capital structure is flexible; shares must be denominated in a currency stated in the articles |

| Privacy | Beneficial ownership disclosure required | Filed with the CAC; not necessarily part of a public register |

Focus Points

- Taxation: Subject to corporate income tax on chargeable profits; standard rate is 30% for most sectors, with reduced rates for certain qualifying activities; VAT registration required once turnover thresholds are met; withholding tax applies to dividends, interest, and management fees paid to non-residents.

- Annual Compliance: Annual returns and audited financial statements must be filed with the CAC; failure to file attracts penalties.

- Treaty Access: Sierra Leone has a limited tax treaty network; treaty benefits should be verified before structuring cross-border payments.

- Restrictions: Cannot offer shares to the public or list on a stock exchange without converting to a public company.

- Conversion: The Companies Act 2009 permits re-registration from private to public company status subject to CAC approval and statutory requirements.

Closing Paragraph

The private company structure suits trading operations, holding arrangements, and service businesses where a small group of shareholders requires limited liability without public disclosure obligations. One clear limitation is the 50-shareholder cap, which restricts equity fundraising from a broad investor base.

Best suited for foreign investors and resident entrepreneurs establishing a closely held operating or holding business in Sierra Leone with no intention of public fundraising.

Company Limited by Guarantee

A company limited by guarantee Sierra Leone is governed by the Companies Act 2009, which provides the legal framework for its formation, governance, and dissolution. Unlike share capital companies, this structure has no shareholders. Instead, members undertake to contribute a specified sum toward the company's debts if it is wound up. The entity carries full separate legal personality and limits member liability to that guaranteed amount.

Registered under the Corporate Affairs Commission (CAC), this structure is used predominantly for nonprofit purposes — charities, professional associations, educational bodies, and NGOs. Because it does not distribute profits to members, it functions as a non-share capital company suited to organizations reinvesting surplus into their stated objectives.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Guarantee | Governed by the Companies Act 2009 |

| Members | Minimum 2; no statutory maximum | Referred to as "members"; no shareholders |

| Directors | Minimum 2 | At least one must be ordinarily resident in Sierra Leone |

| Local Presence | Registered office within Sierra Leone | Registered with the Corporate Affairs Commission |

| Capital | No share capital; members provide a guarantee amount | Guarantee is typically a nominal sum (e.g., Le 1) |

| Profit Distribution | Not permitted | Surplus must be applied toward the entity's objectives |

Focus Points

- Taxation: Exempt from corporate income tax on qualifying nonprofit income; however, commercial activities may attract standard corporate tax; VAT obligations apply where taxable supplies exceed the registration threshold; withholding tax rules apply to payments made to third parties.

- Annual Compliance: Annual returns and audited financial statements must be filed with the CAC; failure to comply can result in penalties or striking off.

- Economic Substance: No specific economic substance regime applies to guarantee companies, but local operational activity is generally expected given the nonprofit mandate.

- Conversion: Conversion to a share capital company is not permitted under the Companies Act 2009.

- Restrictions: Cannot distribute income or assets to members during operation or on dissolution; residual assets must pass to a similar nonprofit entity.

Closing

This structure is used primarily by NGOs, professional bodies, and charitable organizations operating within or through Sierra Leone. The absence of share capital simplifies ownership governance, though the prohibition on profit distribution makes it unsuitable for any commercial or investor-backed purpose.

Nonprofit company registration in Sierra Leone is most appropriate for charities, industry associations, and NGOs that require legal personality without a profit-distribution mandate.

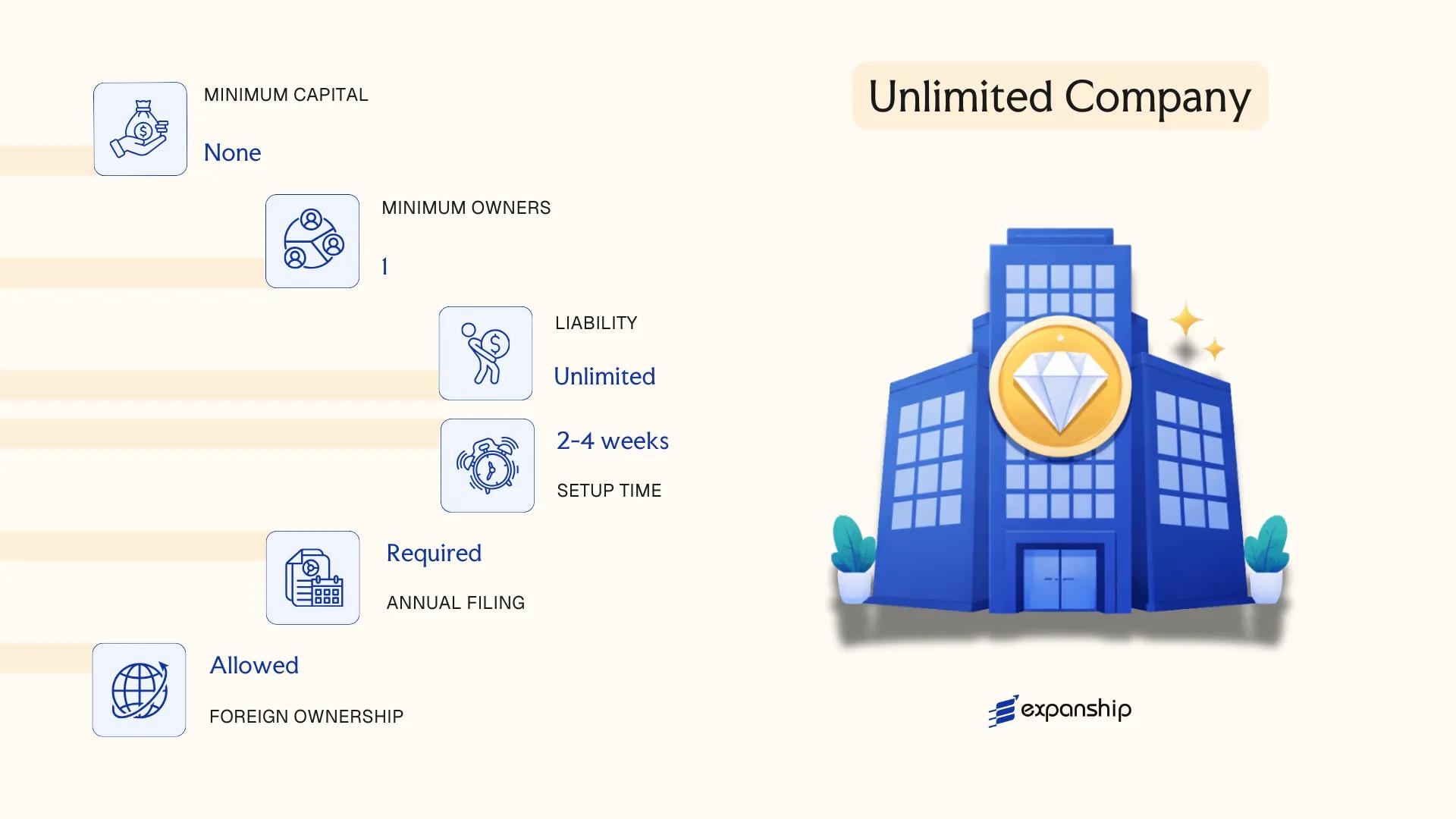

Unlimited Company

Unlimited company registration Sierra Leone follows the framework established under the Companies Act 2009, administered by the Corporate Affairs Commission (CAC). Unlike limited structures, an unlimited company carries no cap on the liability of its members — each member remains personally liable for the company's debts to the full extent of their personal assets.

Separate legal personality is retained, which distinguishes this structure from a simple partnership. The entity can own property, enter contracts, and sue or be sued in its own name, yet members bear residual personal exposure if the company cannot meet its obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company | Incorporated body with separate legal personality; no liability cap on members |

| Members | Shareholders; minimum 2, no statutory maximum | No restriction on individual or corporate membership |

| Directors | Minimum 1 director required | At least one director must be a natural person |

| Local Presence | Registered office in Sierra Leone required | Must maintain a physical address on record with the CAC |

| Share Capital | No prescribed minimum; denominated in Leones (SLL) | Shares may or may not have nominal value |

| Privacy | Member and director details filed with CAC | Public register; limited privacy compared to offshore structures |

Focus Points

- Taxation: Subject to standard corporate income tax (currently 30% for most sectors), VAT where applicable, withholding tax on dividends and service payments, and stamp duty on instruments — no special tax treatment applies by virtue of the unlimited structure.

- Annual Compliance: Annual returns must be filed with the CAC; financial statements are required to be maintained and submitted in accordance with the Companies Act 2009.

- Conversion: An unlimited company may be re-registered as a limited company under the Companies Act 2009, subject to CAC approval and prescribed procedural requirements.

- Economic Substance: No specific economic substance regime targets unlimited companies at present, though general tax residency and anti-avoidance provisions apply.

- Restrictions: This structure is uncommon in commercial practice and is generally unsuitable for external investment due to the unrestricted personal liability exposure of its members.

Closing

Unlimited companies in Sierra Leone are occasionally used by professional firms or closely held businesses where full disclosure of financial affairs is not a concern and members are willing to accept personal liability exposure. The absence of a liability cap is a significant deterrent for most commercial operators.

This structure suits closely held professional or family-run businesses whose members have full control and a high tolerance for personal financial exposure.

Partnerships [General Partnership, Limited Partnership]

Governed by the Business Registration Act 2007 and related partnership provisions, a general and limited partnership in Sierra Leone does not confer separate legal personality on the firm — partners remain personally bound by the obligations of the business. This distinction has direct consequences for liability exposure and structural planning.

Registration is handled through the Corporate Affairs Commission (CAC) of Sierra Leone. A partnership must be registered before commencing operations, and the CAC maintains records of both the firm and its partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unregistered legal entity (no separate legal personality) | Partners contract in their own names |

| Partners | Referred to as partners; minimum 2, maximum 20 | General partnerships have no limited partners |

| Local Presence | Registered business address required | No mandatory local partner requirement for foreign nationals |

| Capital | No statutory minimum; denominated in Sierra Leonean Leone (SLL) | Contributions defined by partnership agreement |

| Privacy | Partner names disclosed to CAC | Not publicly searchable in a centralised online registry |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are assessed at the partner level under the Income Tax Act 2000, with no entity-level corporate tax; VAT registration applies if turnover thresholds are met.

- Annual Compliance: Annual renewal of business registration with the CAC is required.

- Liability: General partners bear unlimited personal liability; limited partners in a limited partnership are liable only to the extent of their capital contribution.

- Treaty Access: Partnerships generally do not access Sierra Leone's tax treaties directly, as treaty benefits apply to residents rather than pass-through entities.

- Restrictions: Certain regulated sectors, including banking and insurance, prohibit operation through a partnership structure.

Sub-Types

General Partnership

All partners share equal management rights and unlimited liability for firm obligations. This structure suits small professional practices or family-run trading operations where partners maintain active control.

Limited Partnership

At least one general partner retains unlimited liability and management authority, while one or more limited partners contribute capital and bear liability only up to their invested amount. Limited partners may not participate in management without risking reclassification as general partners.

Closing

Partnerships suit joint ventures, professional services, and small trading operations where operational simplicity outweighs the absence of liability protection. The pass-through tax treatment is an advantage for structuring multi-party investments, though unlimited personal liability for general partners remains a material constraint for higher-risk activities.

A limited partnership structure is best suited to investment arrangements or joint ventures where at least one party requires liability containment while others take an active management role.

Foreign Business Structures [External Company, Branch Office, Representative Office]

Foreign company registration in Sierra Leone is governed by the Companies Act 2009, which dedicates specific provisions to "external companies" — defined as any body corporate incorporated outside the country that establishes a place of business within its territory. Such entities do not form a new legal person under Sierra Leonean law; the parent company retains its original legal personality and remains liable for all obligations incurred locally.

Registration is administered by the Corporate Affairs Commission (CAC). Once registered, an external company must maintain a registered office address within the jurisdiction and appoint a local agent authorised to accept service of process on its behalf.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External Company (Branch) | Not a separate legal entity; the parent bears full liability |

| Local Representative | Appointed local agent required | Must be resident in Sierra Leone and authorised to accept legal notices |

| Registered Office | Local address mandatory | Must be maintained for the duration of operations |

| Capital | No prescribed minimum | Parent company's capital structure applies |

| Filing Obligations | Certified constitutional documents, list of directors, and agent details | Must be filed with the CAC within 28 days of establishing a place of business |

| Privacy | Directors and agent details on public record | Parent company documents also filed publicly |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; withholding tax applies to remittances to the parent, and VAT registration is required if turnover thresholds are met.

- Annual Compliance: Annual returns and updated financial statements must be filed with the CAC; failure to file attracts statutory penalties.

- Treaty Access: Sierra Leone's limited double tax treaty network may restrict the parent's ability to claim relief on branch-sourced income.

- Restrictions: Certain regulated sectors require additional ministerial or sector-specific approval before an external company may commence operations.

- Conversion: An external company may subsequently incorporate a separate local subsidiary under the Companies Act 2009 if full legal separation becomes necessary.

Sub-Types

Branch Office

A branch office is the standard operational form for an external company actively conducting business locally. It executes contracts, generates revenue, and engages employees directly under the parent's legal identity.

Representative Office

A representative office is used for market research, liaison, and promotional activities only. It cannot enter into commercial contracts or earn local revenue; its scope is strictly non-trading, which limits both tax exposure and regulatory obligations.

Closing

An external company structure suits multinationals testing the local market or executing a defined project without committing to full local incorporation. The primary advantage is operational speed, as no new share capital or local shareholders are required; the key drawback is that the parent company bears unlimited liability for all Sierra Leonean obligations.

Foreign firms with existing operations elsewhere that require a temporary or project-specific presence before deciding on permanent local incorporation.

Sole Proprietorship

Sole proprietorship registration in Sierra Leone is governed by the Business Registration Act 2007, administered by the Corporate Affairs Commission (CAC). Unlike registered companies, a sole proprietorship carries no separate legal personality — the business and its owner are treated as a single legal unit, meaning the proprietor bears unlimited personal liability for all business debts and obligations.

Registration is relatively straightforward. You submit a business name registration application to the CAC along with the applicable fee, and upon approval, the business name is recorded in the register. Operating under a trading name without registration is prohibited under the Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Proprietor | Single individual only; no co-owners |

| Membership | 1 (minimum and maximum) | Cannot have multiple owners; use a partnership for shared ownership |

| Local Presence | Business address required | Registered with CAC; local address mandatory |

| Capital | No statutory minimum | No prescribed paid-up or share capital requirement |

| Liability | Unlimited personal liability | Owner's personal assets are fully exposed to business debts |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act 2000 at progressive individual rates; GST registration required if annual turnover exceeds the prescribed threshold; no corporate income tax applies.

- Annual Compliance: Business name renewal is required periodically with the CAC; failure to renew can result in deregistration.

- Conversion: Can be converted to a private limited company by incorporating a new entity and transferring business assets; no direct statutory conversion mechanism exists.

- Treaty Access: As an unincorporated entity, a sole proprietorship does not access Sierra Leone's double taxation agreements in the same manner a resident company would.

- Restrictions: Cannot raise equity capital or issue shares; unsuitable for businesses seeking external investment.

Closing

A sole proprietorship suits local traders, freelancers, and self-employed individuals operating small-scale businesses with limited transaction complexity or risk exposure. The absence of incorporation formalities reduces setup cost, but unlimited personal liability remains a significant structural constraint for any business carrying financial or contractual risk.

Local sole traders and self-employed individuals running low-risk, single-owner businesses who do not require a separate legal entity or external investment capacity.

How to Choose the Right Entity Type in Sierra Leone

Choosing the right business entity in Sierra Leone is a structural decision with direct legal, tax, and operational consequences — not a formality to resolve after funding or operations begin.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations from day one. Selecting the wrong form can produce concrete, costly outcomes:

- Registering an external company or branch when you intend to conduct substantive local trade without proper registration under the Companies Act 2009 can expose the firm to penalties or deregistration by the Corporate Affairs Commission.

- Choosing a structure that lacks access to Sierra Leone's applicable tax treaty provisions means withholding tax reductions available to qualifying entities cannot be claimed on cross-border payments.

- Forming a company when a partnership or sole proprietorship structure would serve a single-person consultancy adds annual audit and filing obligations that carry recurring professional fees without commensurate benefit.

- Selecting a structure with a public register of members when confidentiality is a commercial priority creates disclosure that cannot be undone retrospectively.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each attract different permissible structures under Sierra Leonean law.

- Ownership and Management: Single-founder operations and multi-party joint ventures have materially different governance requirements, which push toward sole proprietorships, partnerships, or companies respectively.

- Tax Objectives: Your need for full tax exemption, treaty eligibility, or a standard corporate tax position under the Income Tax Act 2000 determines which structures are appropriate.

- Liability Exposure: Whether unlimited personal liability is acceptable or a separate legal personality with limited liability is necessary affects the choice between partnerships, unlimited companies, and companies limited by shares.

- Exit Strategy: Not all Sierra Leonean entity types support redomiciliation or conversion; confirming that a structure permits your intended exit mechanism before incorporation avoids costly restructuring later.

Corporate Compliance Services in Sierra Leone

Ongoing compliance support for companies registered in Sierra Leone, including annual filings, Corporate Affairs Commission obligations, and statutory record maintenance.

Conclusion

A Sierra Leone company formation summary looks different depending on the structure you choose. Private companies limited by shares dominate registrations under the Companies Act 2009, making them the default choice for most foreign and domestic investors. Public companies suit larger capital-raising ambitions, while companies limited by guarantee serve non-profit and membership-based purposes. Unlimited companies remain rare, used where members accept full liability. General partnerships offer simplicity without separate legal personality; limited partnerships protect passive partners. External companies and branch offices serve foreign entities maintaining a direct operational presence.

Administered through the Corporate Affairs Commission, the registration framework continues to evolve, with gradual digitisation of filing processes signalling a shift toward greater procedural efficiency. Expanship's team works directly within this regulatory environment to support your corporate setup from entity selection through to ongoing compliance.

How Expanship Can Assist You

Expanship company incorporation Sierra Leone covers the full process of establishing your entity under the Companies Act 2009, from selecting the appropriate structure — private limited, company limited by guarantee, or an external company registration — to filing with the Corporate Affairs Commission (CAC). Every structure discussed in this guide carries distinct obligations, and getting the foundation right matters from day one.

Our corporate services in Sierra Leone span the entire setup and maintenance cycle:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and CAC liaison

- Post-incorporation compliance management

- Banking introduction assistance

Sierra Leone business registration assistance through Expanship means your entity is filed correctly, maintained in good standing, and supported beyond the certificate of incorporation.

Reach out to Expanship Sierra Leone to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently registered structure. Its relatively low capital requirements, restricted share transferability, and suitability for both resident and non-resident founders make it the default choice for most commercial ventures.

A private company cannot offer shares to the public and faces fewer disclosure obligations than a public company limited by shares. Public companies must meet higher minimum capital thresholds, file more extensive annual returns, and appoint at least two directors.

The private company limited by shares provides comparatively greater confidentiality than a public company. Beneficial ownership disclosure requirements exist under Sierra Leone's anti-money laundering framework, though nominee arrangements remain legally permissible for directorship and shareholding purposes.

A sole proprietorship and a private company limited by shares can be formed by one individual. Partnerships, by definition under the relevant statutory provisions, require a minimum of two partners, making single-person formation legally impermissible for that structure.

Foreign nationals may register a private company, public company, company limited by guarantee, or an unlimited company. External companies and branch offices require prior registration with the CAC as a foreign entity and must designate a local agent for service of process.

The Companies Act 2009 allows a private company to re-register as a public company, and vice versa, subject to CAC approval and compliance with the applicable share capital and governance requirements. Conversion from a company structure to a partnership is not a straightforward statutory process and would generally require dissolution and fresh registration.

Companies incorporated under the Companies Act 2009, including private, public, guarantee, and unlimited companies, possess distinct legal personality separate from their members. General partnerships and sole proprietorships do not, meaning personal liability exposure remains a material consideration for those structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.