Key Takeaways

- Saudi Arabia's company formation framework is governed by the Ministry of Commerce under the Companies Law issued by Royal Decree No. M/3 of 2022, with foreign investment activity subject to additional licensing by the Ministry of Investment of Saudi Arabia (MISA).

- The Limited Liability Company remains the most widely registered entity form in the Kingdom, favored for its flexibility in capital requirements and shareholding arrangements among both domestic and foreign investors.

- Foreign firms entering Saudi Arabia without establishing a locally incorporated entity may do so through a Branch Office or Representative Office, each carrying distinct operational limitations.

- Vision 2030 reforms and ongoing liberalization of foreign ownership rules are continuing to shape the regulatory environment, with the Companies Law having undergone substantial revision as recently as 2022.

Introduction to Entity Types in Saudi Arabia

Saudi Arabia sits in the southwestern corner of the Arabian Peninsula, bordered by Jordan, Iraq, Kuwait, Bahrain, Qatar, the UAE, Oman, and Yemen, with coastlines along both the Red Sea and the Arabian Gulf. It is an independent sovereign state governed as an absolute monarchy under the Al Saud family. Understanding the types of business entities in Saudi Arabia is foundational for any foreign investor or domestic entrepreneur structuring a new venture in the Kingdom.

Company registration and commercial licensing fall under the authority of the Ministry of Commerce (MoC), which maintains the commercial register and governs entity formation under the Companies Law issued by Royal Decree No. M/3 of 2022. Foreign investment activity is additionally regulated by the Ministry of Investment of Saudi Arabia (MISA), which issues the licenses required for non-Saudi entities operating in the Kingdom.

Saudi Arabia operates a territorial-based tax system with a standard corporate income tax rate applicable to foreign-owned profits, alongside a Zakat obligation imposed on Saudi and GCC national shareholders.

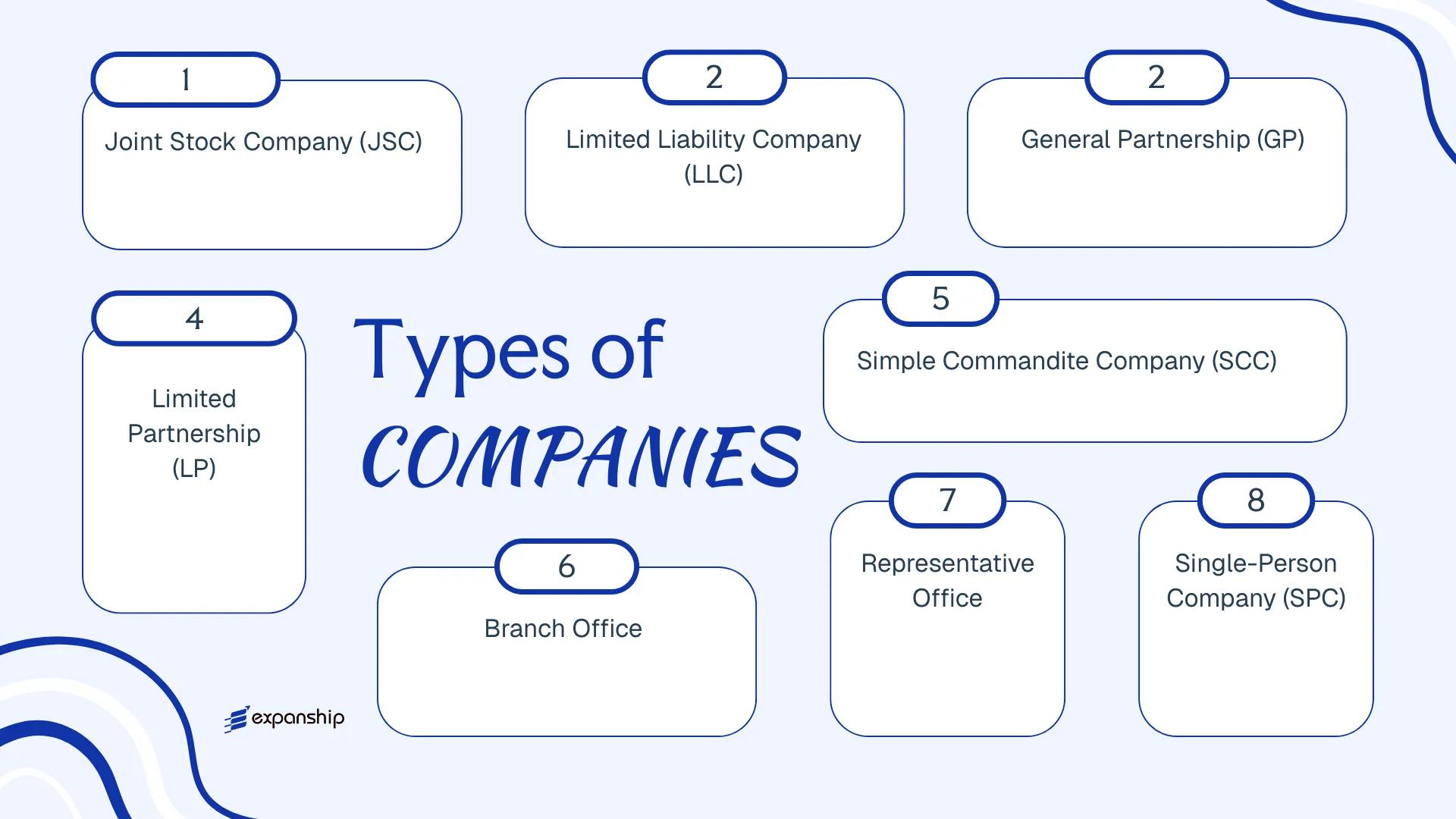

Available corporate structures include the Joint Stock Company, Limited Liability Company, General Partnership, Limited Partnership, Simple Commandite Company, Single-Person Company, Branch Office, and Representative Office. Each of these structures carries distinct ownership, liability, and operational parameters that this article examines in full.

An Overview of Business Structures in Saudi Arabia

Saudi Arabia's company law framework provides six principal entity types available to local and foreign investors. The primary legislation governing these structures is the Companies Law issued by Royal Decree No. M/3 dated 1437H (2015), subsequently amended in 2022 to introduce reforms on capital requirements and governance standards. Each entity type is structured to serve a distinct commercial purpose, from full foreign ownership vehicles to locally integrated firms.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (JSC) | Corporate entity | Limited to shares | Taxed | Yes | 2 shareholders | Ministry of Commerce | Companies Law 2015 (amended 2022) |

| Limited Liability Company (LLC) | Corporate entity | Limited to capital | Taxed | Yes | 1–50 shareholders | Ministry of Commerce | Companies Law 2015 (amended 2022) |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | Min. 2 partners | Ministry of Commerce | Companies Law 2015 |

| Limited Partnership | Hybrid entity | Mixed liability | Taxed | Yes | Min. 2 partners | Ministry of Commerce | Companies Law 2015 |

| Simple Commandite Company | Hybrid entity | Mixed liability | Taxed | Yes | Min. 2 partners | Ministry of Commerce | Companies Law 2015 |

| Branch Office | Extension of parent | Parent liable | Taxed | Yes | N/A | MISA | Foreign Investment Law |

| Representative Office | Non-trading entity | Parent liable | Exempt from CIT | No | N/A | MISA | Foreign Investment Law |

| Single-Person Company (SPC) | Corporate entity | Limited to capital | Taxed | Yes | 1 shareholder | Ministry of Commerce | Companies Law 2015 (amended 2022) |

Each of these structures is examined in full in the sections below.

Joint Stock Company (JSC) / شركة المساهمة

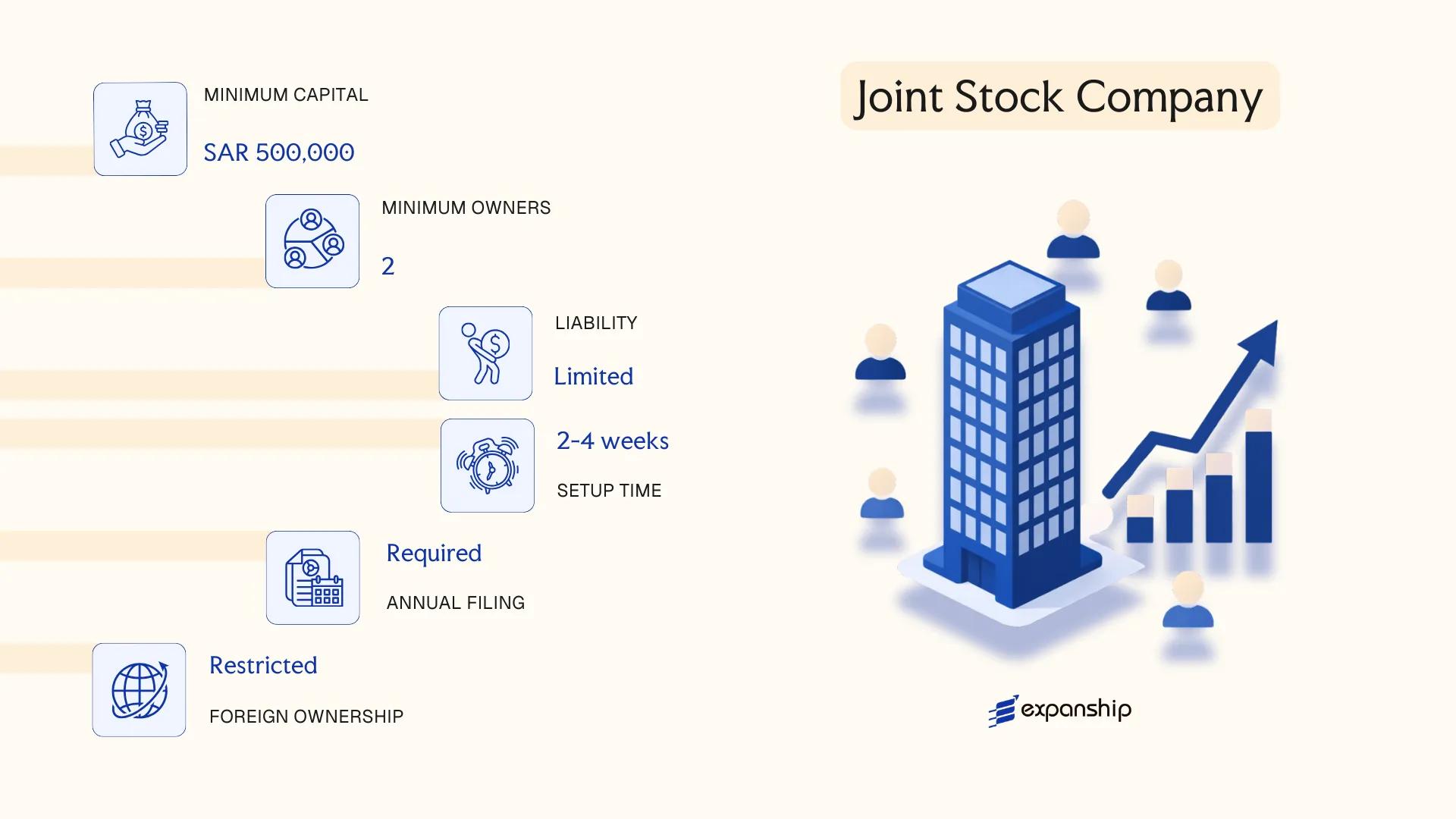

A Joint Stock Company Saudi Arabia JSC is governed by the Companies Law issued under Royal Decree No. M/3 of 1437H (2015G), as amended, and administered by the Ministry of Commerce. The entity carries a separate legal personality, with shareholder liability capped at the value of their subscribed shares.

Capital is divided into equal-value tradeable shares, which distinguishes this structure from other commercial forms. Depending on whether shares are listed or privately held, the entity operates either as a public or closed joint stock company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (JSC) / شركة المساهمة | Separate legal personality; shareholders not liable beyond share subscriptions |

| Members | Shareholders; minimum 2 for closed JSC, minimum 200 for public listing | Board of Directors (minimum 3 members) manages operations |

| Local Presence | Registered office in Saudi Arabia required | A licensed company secretary or registered address must be maintained |

| Capital | SAR 500,000 minimum for closed JSC; SAR 10,000,000 for publicly listed | Must be fully subscribed at incorporation; capital denominated in SAR |

| Privacy | Shareholder register maintained internally; public companies subject to CMA disclosure | Closed JSCs have comparatively higher confidentiality |

Focus Points

- Taxation: Subject to 20% corporate income tax on non-GCC foreign shareholder profits; zakat applies to Saudi/GCC national shareholders at 2.5%; VAT at 15% applies to taxable supplies; withholding tax applies to certain cross-border payments at rates between 5–20%.

- Annual Compliance: Audited financial statements required annually; General Assembly meetings must be held within six months of the fiscal year end; filings submitted to the Ministry of Commerce.

- Regulatory Oversight: Public JSCs fall under the Capital Market Authority (CMA); closed JSCs are regulated by the Ministry of Commerce.

- Conversion: A closed JSC may convert to a public company upon meeting CMA listing requirements, including minimum capital and shareholder thresholds.

- Foreign Ownership: Foreign investors may hold shares, subject to MISA (Ministry of Investment) licensing and sector-specific restrictions under the Negative List.

Sub-Types

Public Joint Stock Company

Shares are listed on the Saudi Exchange (Tadawul) and offered to the public. This sub-type is subject to CMA regulations, mandatory prospectus disclosure, and ongoing reporting obligations beyond those required of a closed entity.

Closed Joint Stock Company (Saudi Arabia)

Shares are privately held and not publicly traded. The شركة المساهمة السعودية in closed form is commonly used for large family-owned businesses, joint ventures, and investment holding structures where public capital markets access is not required.

Closing

The JSC suits large-scale commercial operations, holding structures, and businesses planning an eventual public listing, though the comparatively high minimum capital requirement and administrative burden of board governance make it less practical for smaller ventures.

This structure is most appropriate for large enterprises, institutional joint ventures, or businesses with long-term capital market ambitions.

Company Incorporation in Saudi Arabia

Incorporate a Joint Stock Company or other entity type in Saudi Arabia with end-to-end support from Expanship.

Limited Liability Company (LLC) / شركة ذات مسؤولية محدودة

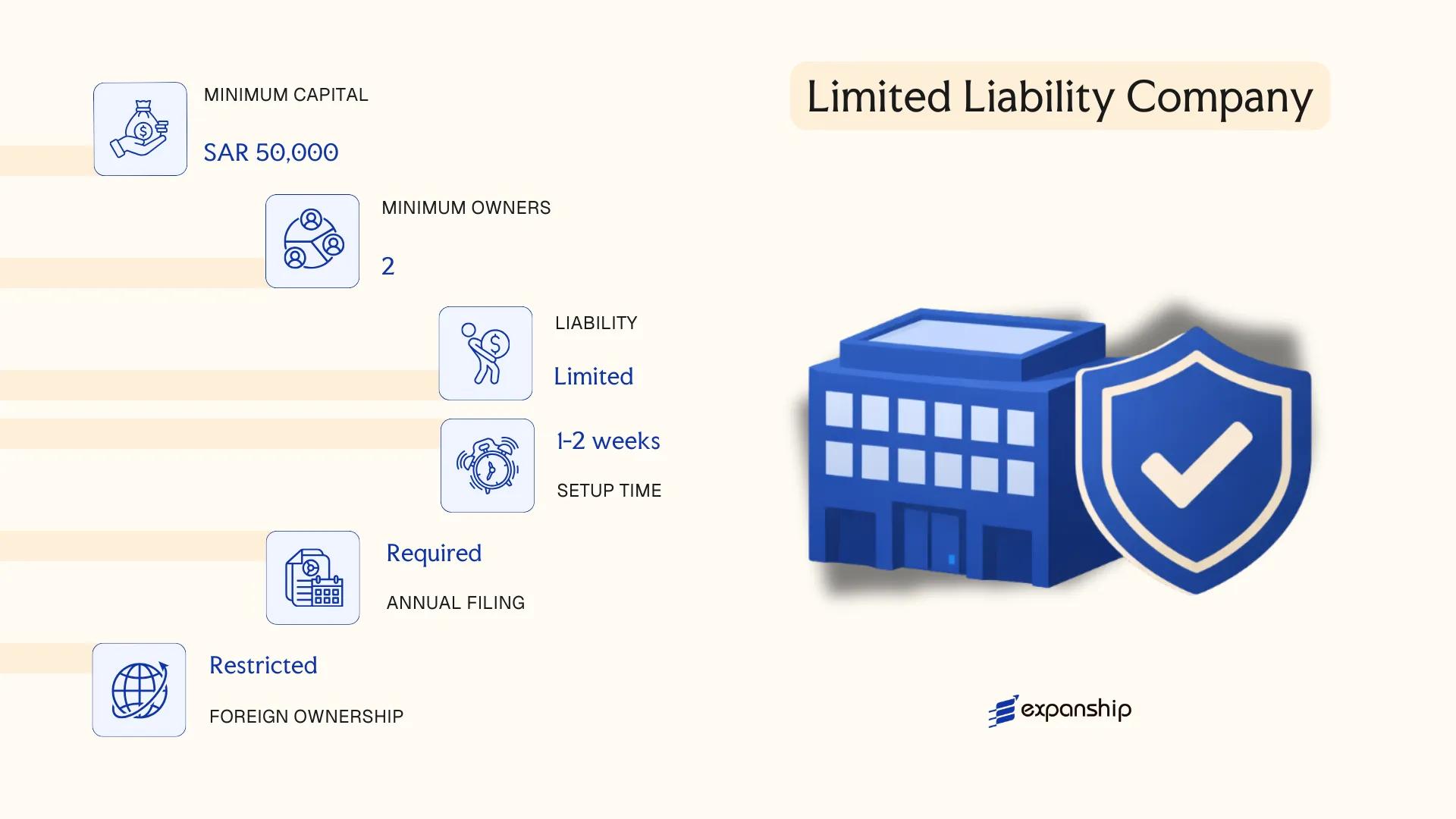

Governed by the Companies Law issued under Royal Decree No. M/3 of 1437H (2015G) and its subsequent amendments, the Limited Liability Company Saudi Arabia LLC structure is the most commonly registered commercial form for both domestic and foreign investors. The entity holds a separate legal personality, meaning it can own assets, enter contracts, and bear obligations independently of its members.

Liability is capped at each member's contribution to the capital. This hybrid structure combines the operational flexibility of a partnership with the liability protection of a corporate form, making it a practical vehicle for a wide range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Registered with the Ministry of Commerce (MoC) |

| Members | Min. 1, Max. 50 | Members hold "quotas" (not shares); referred to as partners |

| Foreign Ownership | Up to 100% in most sectors | Subject to SAGIA/Invest Saudi licensing; restricted sectors apply |

| Minimum Capital | No statutory minimum for most activities | Certain regulated activities (e.g., insurance, finance) impose sector-specific minimums |

| Local Presence | Registered office address in KSA required | Virtual offices generally not accepted; physical address needed |

| Privacy | Member names disclosed in commercial register | Articles of association are publicly filed with MoC |

Focus Points

- Taxation: Subject to 20% corporate income tax on foreign-owned profit share; Saudi/GCC national-owned shares subject to Zakat at 2.5%; VAT applies at 15%; withholding tax applies to certain cross-border payments (rates vary by payment type and treaty status).

- Annual Compliance: Audited financial statements required annually; financial year-end and auditor appointment must be registered with MoC.

- Treaty Access: Saudi Arabia maintains a network of double taxation treaties; LLC entities are generally eligible, subject to beneficial ownership and substance requirements.

- Conversion: An LLC may be converted to a Joint Stock Company under the Companies Law, subject to MoC approval and minimum capital thresholds.

- Restrictions: Certain sectors (banking, insurance, media) restrict or prohibit foreign LLC ownership; activities require corresponding licenses from sector regulators.

Closing

The LLC suits trading operations, regional subsidiaries, joint ventures, and holding structures where full foreign ownership is required but a public listing is not. One clear limitation is the 50-member cap on partners, which restricts equity-raising capacity compared to a Joint Stock Company.

Best suited for foreign investors and SMEs seeking a controlled operational presence in KSA without the regulatory burden of a publicly listed structure.

Partnerships [General Partnership, Limited Partnership, Simple Commandite Company]

Governed by the Companies Law issued under Royal Decree No. M/3 of 1437H (2015G) and its subsequent amendments, partnership company types in Saudi Arabia share a common characteristic: partners bear personal liability for the firm's obligations, either in full or in part depending on the structure chosen. Unlike a Limited Liability Company or Joint Stock Company, these entities do not universally confer limited liability on all participants.

Partnerships must be registered with the Ministry of Commerce and have their contracts authenticated accordingly. They are less commonly used for large commercial ventures but remain relevant for professional services, family businesses, and arrangements where personal accountability between partners is commercially acceptable.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (General, Limited, or Simple Commandite) | Governed by the 2015 Companies Law |

| Members | Referred to as Partners; minimum 2 for all types | No statutory maximum for general partnerships; limited partnerships require at least one general and one limited partner |

| Local Presence | Registered office address in Saudi Arabia required | Must be maintained throughout the entity's life |

| Capital | No statutory minimum; denominated in SAR | Capital contributions defined in the partnership agreement |

| Liability | General partners: unlimited personal liability; limited partners: liability capped at capital contribution | Varies by partner class |

| Privacy | Partnership contracts filed with the Ministry of Commerce | Agreements become part of the commercial register |

Focus Points

- Taxation: Partnerships are fiscally transparent for Saudi national partners; foreign partners' shares are subject to corporate income tax at 20%, with Zakat applicable to Saudi partners' shares. VAT registration is required if turnover exceeds the mandatory threshold (SAR 375,000 annually).

- Annual Compliance: Partners must file financial statements and maintain updated commercial registration with the Ministry of Commerce each year.

- Treaty Access: Access to Saudi Arabia's tax treaty network depends on the residency status of the individual partners, not the partnership itself.

- Restrictions: Foreign nationals cannot act as general partners in a general partnership without satisfying the foreign investment requirements set by the Ministry of Investment (MISA).

- Conversion: A partnership may be converted to another corporate form, such as an LLC, subject to the procedures outlined in the Companies Law and approval from relevant authorities.

Sub-Types

General Partnership (شركة التضامن)

All partners carry unlimited joint and several liability for the firm's debts. This structure is typically used where partners have an established relationship of trust and where the business operates at a scale where personal liability is a manageable risk.

Limited Partnership (شركة التوصية البسيطة)

At least one general partner retains unlimited liability while one or more limited partners contribute capital without taking on management responsibilities. The limited partners' exposure is restricted to their agreed capital contribution, making Saudi Arabia limited partnership formation suitable where passive investors wish to participate financially without operational involvement.

Simple Commandite Company (شركة التوصية بالأسهم)

The simple commandite company Saudi Arabia recognises divides capital into transferable shares held by limited partners, while general partners retain unlimited liability and management authority. This hybrid form bridges the partnership and corporate worlds, though it remains uncommonly used in practice.

Recommendations

Partnerships are most appropriate for professional services firms, family-controlled trading operations, or arrangements between a small number of known counterparties where the partners are comfortable with the liability exposure the structure carries. The principal limitation is that general partners face unlimited personal liability, which significantly increases the financial risk compared to corporate structures.

Partnerships in Saudi Arabia are best suited for Saudi national professionals or family groups forming a closely held business where personal trust between partners substitutes for structural liability protection.

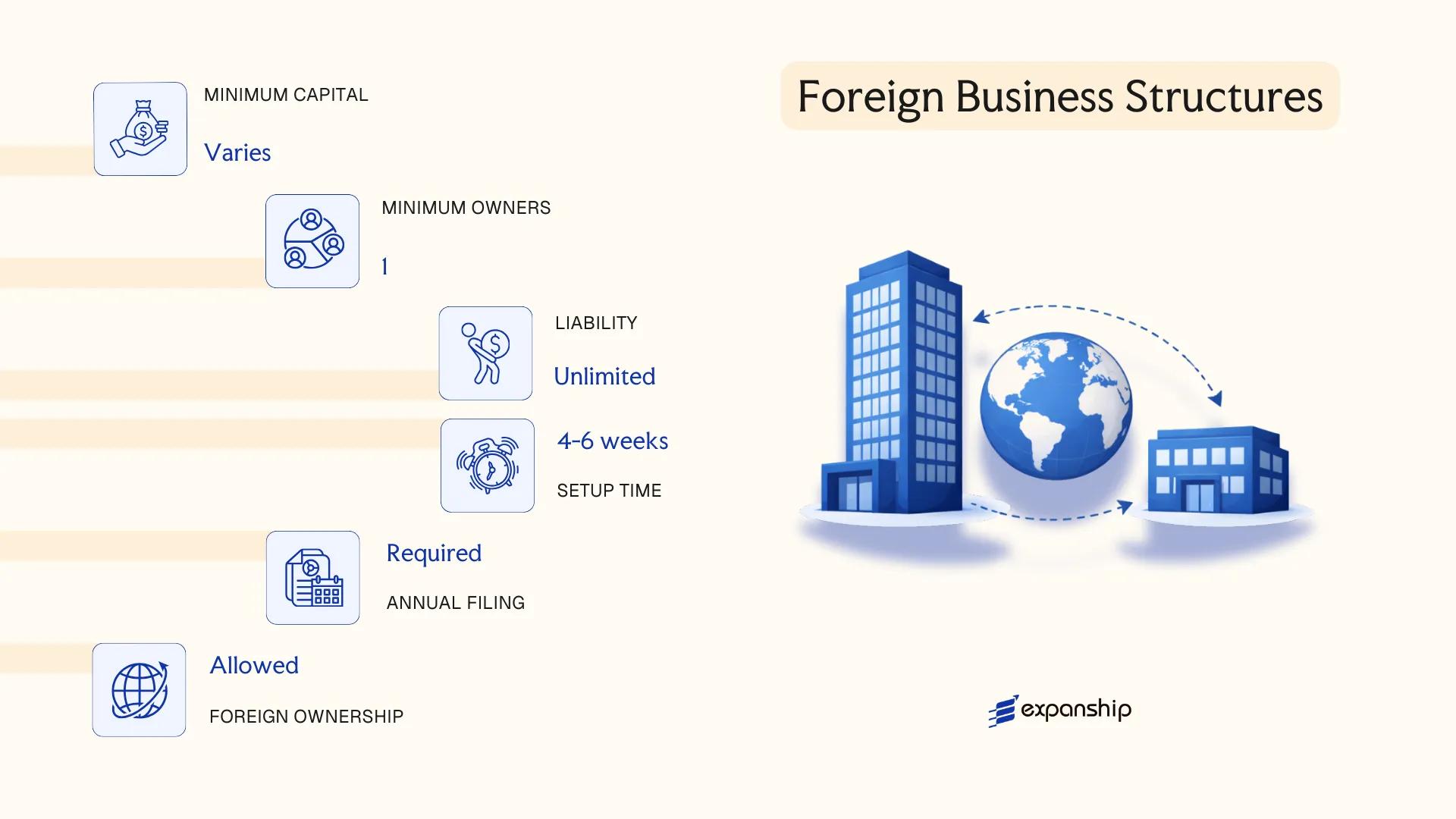

Foreign Business Structures [Branch Office, Representative Office]

Registering a foreign company branch office in Saudi Arabia is governed by the Companies Law (Royal Decree No. M/3, 2022) alongside the Foreign Investment Law (Royal Decree No. M/1, 2000) and its implementing regulations. Neither structure constitutes a separate legal entity — both remain legally and financially continuous with the parent company abroad.

Oversight falls under the Ministry of Investment of Saudi Arabia (MISA), which issues the required foreign investment licence before any commercial registration can proceed with the Ministry of Commerce.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | Extension of parent; no separate legal personality | Extension of parent; no separate legal personality |

| Permitted Activities | Full commercial and operational activities within licensed scope | Non-revenue activities only (market research, liaison, promotion) |

| Members / Management | Appointed General Manager (must be resident in KSA) | Appointed Representative Manager |

| Capital Requirement | No statutory minimum; parent bears full financial liability | No statutory minimum |

| Local Presence | Registered office address in KSA required | Registered office address in KSA required |

| Licensing Body | MISA licence + Ministry of Commerce registration | MISA licence + Ministry of Commerce registration |

Focus Points

- Taxation: Branch profits are subject to 20% corporate income tax; Zakat does not apply to foreign-owned branches. VAT at 15% applies to taxable supplies. Withholding tax applies on payments to non-residents at rates between 5% and 20% depending on payment type.

- Economic Substance: No specific economic substance regime mirrors the offshore model, but MISA licences carry activity and operational continuity conditions that must be maintained annually.

- Annual Compliance: Audited financial statements must be filed annually; the MISA licence requires periodic renewal and demonstration of ongoing activity.

- Treaty Access: The parent company's tax residency determines access to Saudi Arabia's double taxation treaties; branch structures can generally access applicable treaties.

- Restrictions: Representative offices cannot invoice clients, generate revenue, or sign commercial contracts in their own capacity.

Sub-Types

Branch Office

A branch office is licensed to conduct revenue-generating operations within the scope defined by its MISA licence, making it the standard structure for foreign firms seeking active market participation without incorporating a separate Saudi entity.

Representative Office

A representative office is restricted to promotional, liaison, and market research functions only. It cannot conclude contracts or earn income, and is typically used by firms testing the market or maintaining a presence to support overseas operations.

Closing

Both structures suit foreign businesses seeking a defined, time-limited presence without establishing a locally incorporated entity, though the absence of separate legal personality means the parent company bears unlimited liability for all obligations. The representative office's activity restrictions make it unsuitable for any revenue-generating operations.

A branch office suits established foreign companies with a specific licensed activity; a representative office suits those in a pre-commercial or exploratory phase.

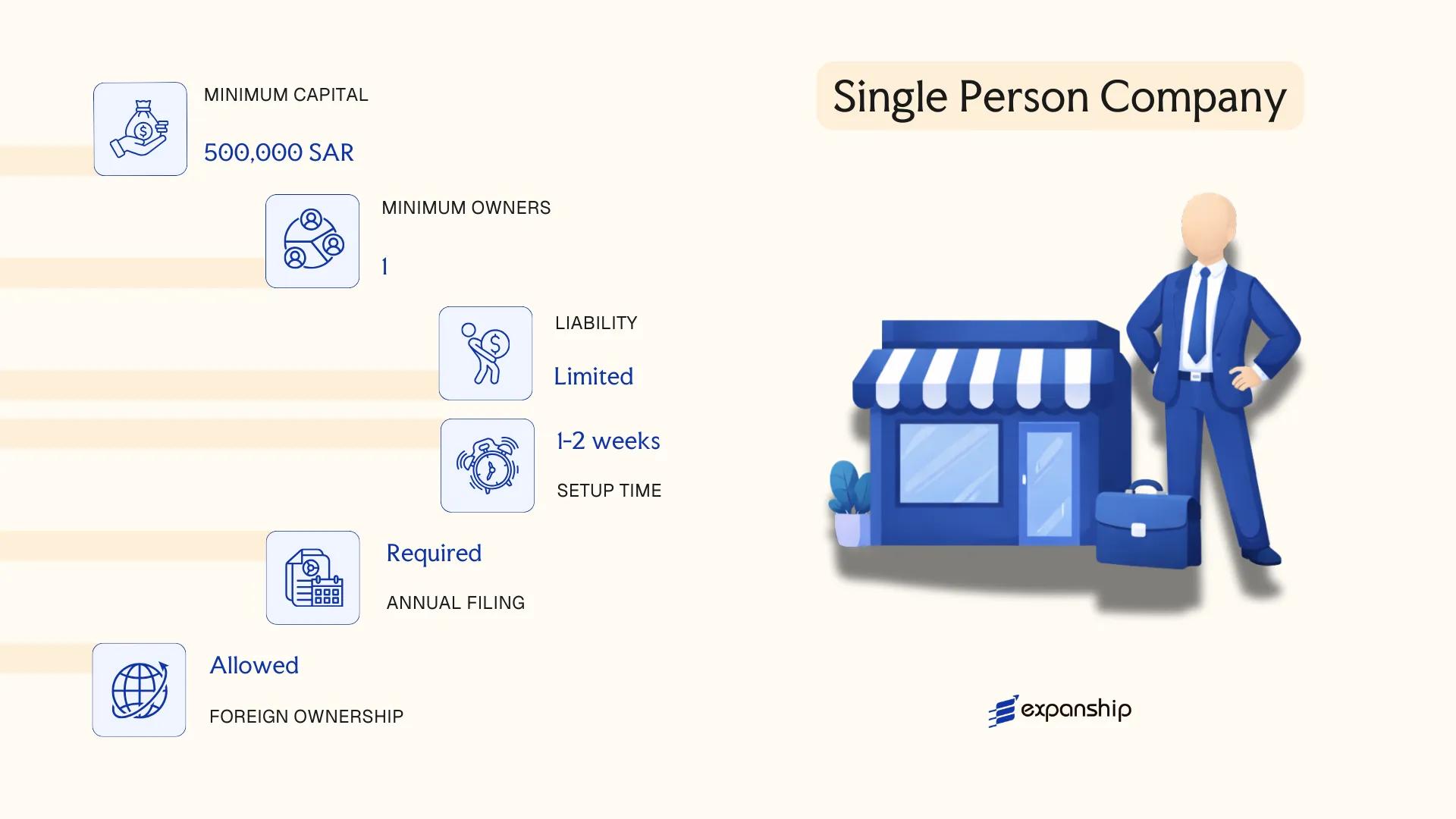

Single-Person Company (SPC) / شركة الشخص الواحد

A Single Person Company Saudi Arabia SPC is a distinct legal form introduced under the Companies Law issued by Royal Decree No. M/3 dated 1437H (2015), with further refinements through subsequent ministerial regulations. The entity carries full legal personality separate from its sole founder, meaning the founder's personal assets are shielded from the company's liabilities.

Structurally, the SPC functions as a hybrid: it combines the single-ownership simplicity of a sole proprietorship with the limited liability protection associated with a multi-member LLC. Registration and ongoing oversight fall under the Ministry of Commerce.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-Person Company (SPC) | Separate legal personality; limited liability |

| Member Designation | Sole Owner / Manager | One person holds both ownership and management roles unless a separate manager is appointed |

| Membership | 1 founder (individual or legal entity) | No maximum; structure is inherently single-owner |

| Local Presence | Registered office address in Saudi Arabia | Physical or serviced address accepted |

| Capital | SAR denominated; no statutory minimum for most activities | Certain licensed activities may impose sector-specific minimums |

| Privacy | Owner details filed with Ministry of Commerce | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to 20% corporate income tax for foreign-owned SPCs; Saudi/GCC national-owned SPCs fall under Zakat at 2.5%; VAT applies at 15% if turnover exceeds the registration threshold; withholding tax applies on cross-border payments.

- Annual Compliance: Financial statements must be filed annually; an auditor appointment is required regardless of revenue size.

- Conversion: An SPC can be converted to an LLC or other structure under the Companies Law if ownership expands.

- Restrictions: Cannot issue shares to the public or list on a stock exchange in its current form.

- Economic Substance: Activities subject to Saudi Arabia's substance requirements must demonstrate genuine operational presence.

Closing

An SPC suits founders who need a formally structured, liability-protected entity for holding assets, IP ownership, or operating a single-owner trading business without the administrative overhead of a multi-member structure. The primary limitation is its inability to admit additional investors without conversion.

An SPC is most appropriate for solo entrepreneurs and foreign investors establishing a wholly owned subsidiary who require legal separation between personal and business assets.

How to Choose the Right Entity Type in Saudi Arabia

Why Your Entity Choice Matters

Selecting the wrong structure under Saudi Arabia's Companies Law (Royal Decree No. M/132 of 2022) produces legal and financial consequences that are difficult to reverse post-registration.

- Registering a Representative Office when your operations involve direct sales or revenue generation violates its permitted scope, exposing the business to penalties and potential cancellation by the Ministry of Commerce.

- Choosing a structure incompatible with SAGIA/MISA licensing requirements for your specific sector — such as restricted or partially restricted activities — can result in the rejection of your foreign investment licence or its subsequent revocation.

- Forming a Joint Stock Company when a single-person consultancy is all that is required imposes mandatory audited financial statements and a supervisory board, adding compliance costs that an SPC would not carry.

- Selecting an LLC with multiple shareholders when the activity requires full foreign ownership clarity may create governance complications if the ownership structure conflicts with applicable foreign investment ratios.

Key Factors to Consider

- Business Activity: Regulated sectors such as insurance, banking, and capital markets mandate specific structures approved by the relevant sectoral regulator, not simply the Ministry of Commerce.

- Ownership Structure: A sole operator points toward an SPC, while multi-party ventures require an LLC or JSC depending on scale and governance needs.

- Foreign Ownership: MISA-licensed entities face sector-specific foreign equity caps that directly constrain which structures are permissible.

- Liability Exposure: Activities carrying significant third-party risk warrant structures with clearly defined limited liability rather than general partnerships.

- Capital Requirements: JSC formation requires a minimum share capital that an LLC or SPC does not, affecting which structure is financially viable at incorporation.

- Exit and Transferability: Share transferability rules differ materially between an LLC and a JSC, and your anticipated exit route should inform the choice from the outset.

Review the full text of the Companies Law on the Bureau of Experts at the Council of Ministers official portal before proceeding.

Compliance Services for Companies in Saudi Arabia

Ongoing compliance support for Saudi-registered entities, including annual filings, licence renewals, and regulatory reporting with MISA and the Ministry of Commerce.

Conclusion

Selecting the right structure is one of the most consequential decisions in incorporating a company in Saudi Arabia guide terms, as each entity type carries distinct implications for liability, ownership, and operational scope. The LLC remains the most widely registered form, favored by both domestic entrepreneurs and foreign investors for its flexibility on capital and shareholding. Joint Stock Companies suit larger enterprises seeking access to capital markets or institutional investment. Partnerships serve closely held, professionally managed operations. Branch and Representative Offices apply specifically to foreign firms extending an existing legal presence. The Single-Person Company accommodates sole proprietors requiring formal legal separation.

Saudi Arabia's regulatory direction, shaped by ongoing Vision 2030 reforms and the Ministry of Investment's continued liberalization of foreign ownership rules, points toward a more accessible registration environment. The Companies Law, last substantially revised in 2022, continues to be updated in ways that affect entity governance and compliance obligations.

How Expanship Can Assist You

Selecting the right entity type is only the first step. From corporate services company formation in Saudi Arabia to maintaining post-incorporation obligations, Expanship works directly with the Ministry of Commerce (MoC) and the Ministry of Investment (MISA) processes that govern registration for every structure covered in this blog.

From your initial filings through to ongoing compliance, our support covers:

- Document preparation, attestation, and legalization

- Registered agent and registered office provision

- Government filing and liaison with MISA and the MoC

- Post-incorporation compliance management

- Corporate bank account introduction assistance

Every jurisdiction has its own pace and procedural requirements. Saudi Arabia is no different, and knowing which authority handles your specific entity type saves considerable time.

Reach out to Expanship Saudi Arabia to discuss your business setup requirements with our team.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently registered structure, governed under the Companies Law issued by Royal Decree M/3. Its combination of capped shareholder liability, relatively straightforward incorporation through the Ministry of Commerce, and flexibility in ownership percentages makes it the default choice for both domestic entrepreneurs and foreign investors entering the market.

No. The Single-Person Company (SPC) is specifically designed for sole ownership and permits formation by a single natural or legal person. General and limited partnerships require a minimum of two partners, while a JSC requires a minimum of two shareholders — meaning not all structures are accessible to a solo founder.

Foreign investors may establish an LLC, JSC, Branch Office, or Representative Office, subject to obtaining a foreign investment licence from the Ministry of Investment (MISA) under the Foreign Investment Law. Certain sectors remain restricted or require a Saudi partner, so the applicable MISA activity classification determines which structure is permissible for your specific business activity.

Conversion is permitted under the Saudi Companies Law. An LLC may convert to a JSC, and other structural transformations are allowed provided the converting entity meets the legal requirements of the target form. The process requires shareholder approval, creditor notification, and registration of the conversion with the Ministry of Commerce.

The SPC and LLC generally carry lighter ongoing requirements compared to a JSC, which is subject to more stringent disclosure, auditing, and governance obligations under the Companies Law. A Representative Office has no profit-generating mandate and therefore avoids corporate tax filings, though it remains subject to annual reporting to MISA.

The LLC, JSC, SPC, and Limited Partnership all hold separate legal personality under Saudi law, meaning their rights and liabilities are distinct from those of their owners. A General Partnership does not confer the same liability shield — partners remain jointly and severally liable for the firm's obligations, without the corporate veil available to shareholders of an LLC or JSC.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.