Key Takeaways

- Romania's micro-enterprise regime taxes qualifying SRLs at 1% or 3% of gross turnover rather than net profit, making it structurally more advantageous than standard corporate tax for early-stage businesses with high margins or low expenses.

- As an EU member state since 2007, a Romanian entity provides legal access to the EU single market under the Treaty on the Functioning of the European Union, eliminating the regulatory barriers that non-EU structures face when trading across member state borders.

- With double taxation treaties covering 90+ countries, a Romanian company materially reduces withholding tax exposure and cross-border profit repatriation costs in ways that jurisdictions with narrower treaty networks cannot match.

- Compliance obligations administered by ANAF and the Oficiul Național al Registrului Comerțului are governed by frameworks aligned with EU standards, meaning foreign investors operate within a predictable legal environment rather than an opaque or discretionary one.

Romania is an EU member state situated in southeastern Europe, bordering the Black Sea and sharing land borders with Hungary, Bulgaria, Ukraine, Moldova, and Serbia. This geographic position, combined with its status as a full European Union member since 2007, makes it a studied choice for foreign investors seeking a regulated continental base. Company registration is administered by the Registrul Comerțului, the national trade register operating under the authority of the Ministry of Justice. Foreign businesses most commonly establish a Societate cu Răspundere Limitată when entering the market.

From a tax standpoint, the country operates a low-tax regime anchored by a flat corporate rate, supplemented by a turnover-based micro-enterprise option for qualifying entities. Foreign ownership of Romanian companies faces no general statutory restrictions, and the legal framework reflects EU standards on capital movement and investor protections under the Treaty on the Functioning of the European Union.

This article examines the concrete advantages that a Romanian business entity offers to internationally operating firms and foreign entrepreneurs.

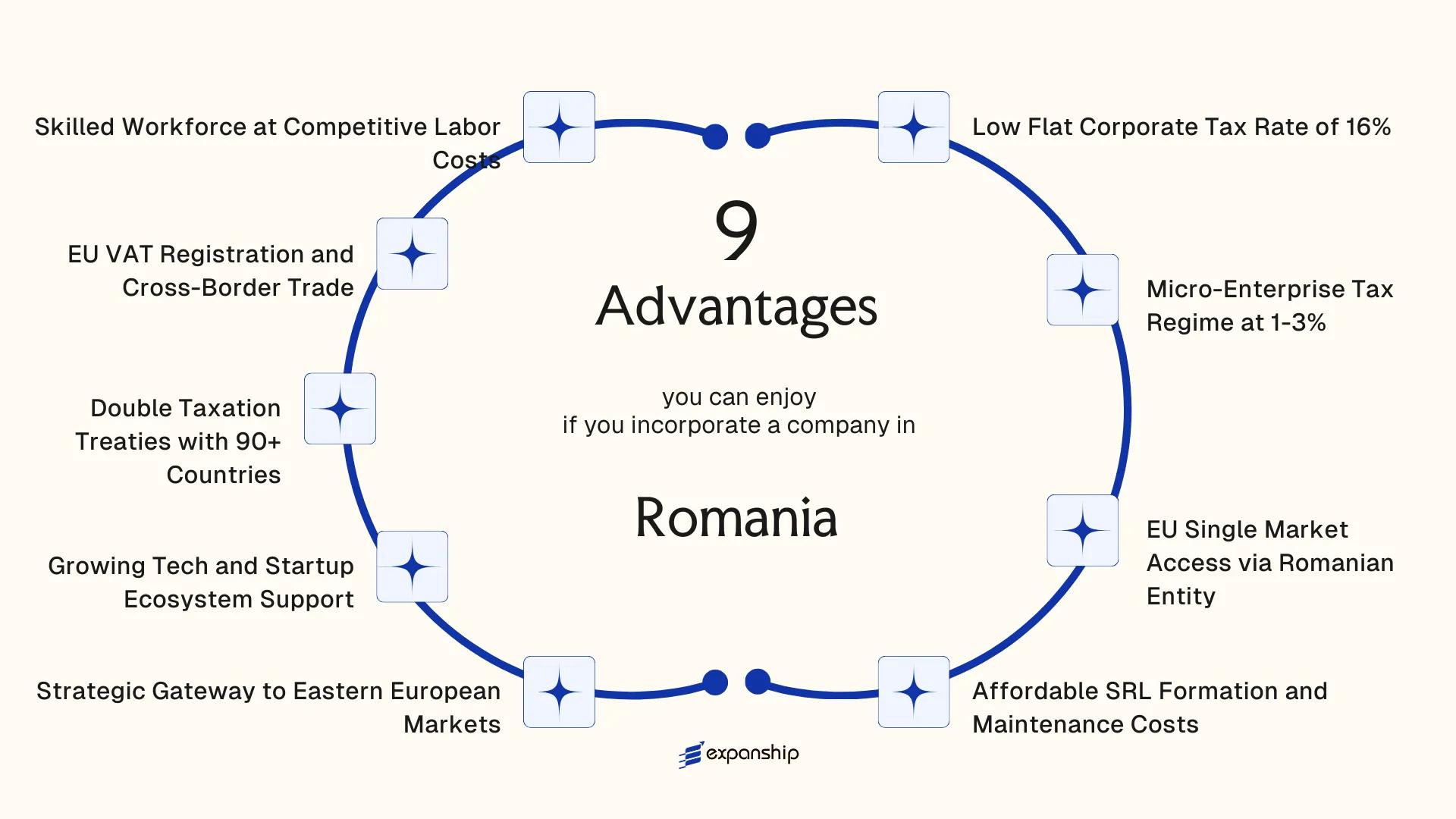

Low Flat Corporate Tax Rate of 16%

Romania's 16% flat corporate tax rate applies uniformly to net profit, with no graduated thresholds or sector-based variations for standard companies. The Romania 16% flat corporate tax advantage is governed under the Fiscal Code (Codul Fiscal), which establishes this rate as the baseline for all resident entities, including the Societate cu Răspundere Limitată (SRL).

Predictability as a Financial Planning Tool

A flat rate eliminates the tax bracket uncertainty that affects profit reinvestment decisions in progressive systems. For a foreign investor structuring earnings through a Romanian SRL, this means projected after-tax returns remain consistent regardless of annual profit fluctuations.

How the Rate Compares Within the EU

The EU average corporate tax rate sits above 21%, making Romania's rate one of the lower flat rates among member states. Your firm retains a structurally higher share of taxable profits compared to entities incorporated in Germany, France, or Italy.

Corporate tax is calculated on net profit after allowable deductions under the Fiscal Code, so tax-deductible operating expenses reduce the actual effective rate further.

Your Romanian entity's tax liability scales only with profit, never with revenue brackets or arbitrary thresholds.

Micro-Enterprise Tax Regime at 1-3%

Romania's micro-enterprise tax regime is one of the more structurally distinctive low-tax options available within the EU, applying a revenue-based tax rate of 1% or 3% in place of the standard 16% corporate profit tax. This rate applies to qualifying SRLs with annual revenues below €500,000, calculated on gross turnover rather than taxable profit. For foreign-owned businesses in early or growth stages, taxing revenue instead of profit removes much of the complexity and exposure tied to profit calculation and cost deduction rules.

The 1% rate applies when your company has at least one full-time employee. Without an employee, the rate rises to 3%. Both figures sit well below the EU average corporate tax rate, which typically exceeds 20% across major economies.

Eligibility conditions are defined under Romanian Fiscal Code provisions governing microîntreprinderi, with oversight from ANAF, the national tax authority. The regime is opted into at registration or at the start of a fiscal year.

Several structural features make the eligibility conditions favourable rather than restrictive:

- The revenue ceiling of €500,000 covers most early-stage and mid-size consulting, services, or digital businesses comfortably

- The employee requirement is a single full-time position, a low threshold for a functioning entity

- Revenue is assessed annually, giving your firm a full operating year before re-evaluation

Incorporate Your Company in Romania

Set up a compliant Romanian SRL and access the micro-enterprise tax regime from day one.

EU Single Market Access via Romanian Entity

EU single market access via Romania company formation gives your business automatic standing within a trading bloc of over 440 million consumers. A Romanian Societate cu Răspundere Limitată (SRL) or Societate pe Acțiuni (SA) is incorporated under Romanian law and registered with the Oficiul Național al Registrului Comerțului (ONRC), which confers full EU legal personhood from the date of registration.

That status is consequential. Under the Treaty on the Functioning of the European Union (TFEU), your entity gains the four fundamental freedoms: free movement of goods, services, capital, and persons across all 27 member states. No separate market-entry applications, no bilateral trade negotiations, and no customs duties on intra-EU transactions.

| Freedom | Practical Scope |

|---|---|

| Goods | Tariff-free trade across all EU member states |

| Services | Cross-border provision without local re-incorporation |

| Capital | Unrestricted transfer of funds within the EU |

| Persons | Ability to employ EU nationals without work permit obligations |

For businesses outside the EU, establishing through a Romanian firm means those market access rights apply immediately upon incorporation, rather than through a foreign subsidiary arrangement that may face additional regulatory scrutiny. Passporting rights available in regulated sectors, such as financial services under EU directives, also flow from an EU-domiciled entity, making the firm's legal base in Romania directly relevant to how widely it can operate.

Affordable SRL Formation and Maintenance Costs

Among the affordable Romanian SRL formation advantages, the state registration fee stands out immediately. Filing through the Trade Register (Oficiul Național al Registrului Comerțului, or ONRC) costs well under 200 EUR in most cases, and the minimum share capital requirement for an SRL is just 1 RON (approximately 0.20 EUR). For a foreign investor, this means capital is not locked away at the point of incorporation.

Annual compliance costs also remain modest. An SRL with straightforward operations can maintain legal standing through relatively low statutory accounting fees, annual confirmations, and general assembly filings. These obligations exist, but they do not carry the overhead typical of incorporation in Western EU states.

Keep these points in mind:

- The 1 RON minimum share capital must be deposited before registration is complete

- ONRC handles both incorporation and ongoing structural changes (director updates, address changes)

- Accounting services are a recurring cost; engage a locally licensed accountant from day one

- Failure to file annual financial statements with the Ministry of Finance can trigger suspension of the firm

The Romania low company maintenance costs benefits foreign entrepreneurs who want an EU-registered entity without committing significant capital to administration. Compared to jurisdictions where minimum share capital starts at EUR 10,000 or more, the SRL structure keeps entry costs contained and ongoing obligations proportionate to the business's actual scale.

An SRL in Romania can be founded by a single associate and a single administrator, meaning one person can legally own and manage the entire entity without requiring a co-founder or a local director.

Strategic Gateway to Eastern European Markets

Romania's geographic position places your business within a few hours' road or rail distance of Bulgaria, Hungary, Moldova, Ukraine, and Serbia. As a Romania gateway to Eastern European markets, a company registered here can distribute goods or services across the broader region without establishing separate legal presences in each neighboring country.

Centrality Within the Regional Supply Chain

Bucharest sits at a convergence point of the Trans-European Transport Network (TEN-T) corridors, which connect Western Europe to the Black Sea. Physical proximity to the Port of Constanta, one of the largest ports on the Black Sea, gives goods-based businesses a direct maritime route into Central Asian and Middle Eastern markets that landlocked EU jurisdictions cannot replicate as efficiently.

Romania's membership in the EU Customs Union means a single customs declaration covers transit through the country toward other member states. Your entity registered under Romanian law operates under EU regulatory frameworks while maintaining commercial access to non-EU neighbors like Moldova and Ukraine through bilateral trade agreements, expanding your addressable market beyond the bloc's borders.

Access to Non-EU Neighboring Economies

Moldova and Ukraine, both outside the EU, have Association Agreements with the European Union that include Deep and Comprehensive Free Trade Area (DCFTA) provisions. A Romanian-registered firm benefits from these frameworks when conducting cross-border commercial activity, since transactions flow through an EU-domiciled entity rather than requiring you to establish operations in markets with less predictable regulatory environments.

Plan Your Romanian Market Entry Strategy

Speak with Expanship's corporate advisors to understand how a Romanian entity can support your regional expansion goals.

Growing Tech and Startup Ecosystem Support

Romania's startup ecosystem has matured considerably over the past decade, making the country's Romania startup ecosystem advantages for investors increasingly concrete rather than aspirational. Cluj-Napoca, Bucharest, and Iași host active tech communities, university-linked incubators, and accelerator programs that give foreign firms direct access to local talent networks and co-development opportunities.

- The Romanian Startup Act (Law no. 209/2022) introduced a formal legal framework recognizing innovative startups, allowing qualifying companies to access fiscal facilities, including deferred payment of certain tax obligations during early-stage operations.

- Under this legislation, eligible startups can benefit from exemptions on profit tax for up to three years, giving early-stage foreign-owned entities meaningful runway to reinvest capital.

- Romania participates in EU-funded programs, including Horizon Europe and structural funds channeled through the Ministry of Research, Innovation and Digitalization, which foreign firms incorporated locally can access.

- The country's high university enrollment in computer science and engineering disciplines means your business can recruit technical talent without relying solely on imported labor.

- The Romanian tech industry benefits for foreign companies are reinforced by a growing base of mid-market software firms, creating viable acquisition targets, partnership structures, and B2B client pipelines for companies entering the region.

Double Taxation Treaties with 90+ Countries

Romania's double taxation treaty network benefits foreign business owners by eliminating one of the most significant friction points in cross-border profit flows: paying tax twice on the same income. With treaties in force covering over 90 countries, including major trading partners across the EU, Asia, and North America, a Romanian entity gives you legal grounds to reduce or eliminate withholding taxes on dividends, royalties, and interest paid across borders.

Treaty rates on dividends paid from a Romanian company to a foreign parent are frequently reduced to 5% or 10%, depending on the specific agreement. Without treaty protection, the standard domestic withholding rate applies, which makes the treaty network a direct cost variable for holding structures and profit repatriation strategies.

These treaties are governed under bilateral agreements ratified through Romanian domestic law and generally follow the OECD Model Tax Convention framework. Eligibility for reduced rates typically requires the recipient to be a tax resident in the treaty country and to meet any ownership thresholds specified in the relevant agreement.

A foreign investor receiving €500,000 in annual dividends from a Romanian SRL, where the applicable treaty reduces withholding tax from 16% to 5%, retains €55,000 more per year compared to a non-treaty scenario, before any additional domestic tax credits applied in the investor's home country.

EU VAT Registration and Cross-Border Trade

Registering a Romanian SRL for EU VAT gives your business direct access to the intra-Community trade framework governed by EU VAT Directive 2006/112/EC, as transposed into Romanian law through the Fiscal Code (Legea nr. 227/2015). This means zero-rated supplies between VAT-registered entities across member states, which reduces cash flow friction on cross-border transactions.

Once your firm holds a valid Romanian VAT number (prefixed RO), it appears in the VIES database, allowing counterparties across all 27 member states to verify and apply the reverse charge mechanism. Suppliers in Germany, France, or elsewhere can invoice your entity without charging local VAT, and your business handles the accounting adjustment domestically.

Romania EU VAT registration benefits for businesses extend to the One Stop Shop (OSS) scheme. If your entity sells digital services or goods to EU consumers, OSS registration through the Romanian Tax Authority (ANAF) allows you to report and remit VAT obligations across multiple member states through a single quarterly filing, rather than registering separately in each country.

- Intra-EU B2B supplies: zero-rated when both parties are VAT-registered

- OSS filing: consolidated reporting for B2C cross-border sales

- VIES verification: confirms your entity's standing to EU trade partners

OSS is available only for businesses without a fixed establishment in the member states where their customers are located; if your firm has a permanent establishment elsewhere in the EU, different VAT rules apply.

Skilled Workforce at Competitive Labor Costs

Romania's skilled workforce cost advantages make it one of the more financially efficient EU locations for labor-intensive operations. Average gross wages remain significantly below the Western European mean, yet the country produces a consistent output of technically trained graduates, particularly in engineering, computer science, and applied mathematics.

Wage Levels and Employer Contributions

The national gross minimum wage is set by government decision and adjusted periodically, sitting well below comparable floors in Germany, France, or the Netherlands. Beyond base wages, employer social contribution obligations are relatively contained. Under Romanian law, the primary social security burden falls on the employee side, which reduces your firm's total payroll cost per hire compared to jurisdictions where employer-side contributions are substantially higher.

Technical and University Graduate Supply

Romania's university system produces tens of thousands of graduates annually across STEM disciplines. Cities such as Cluj-Napoca, Iași, Timișoara, and Bucharest host established technical universities with strong industry ties. For a foreign business establishing a Romanian subsidiary, this means access to mid-level technical staff without the recruitment premiums common in Western EU markets.

English Proficiency and Multilingual Capacity

English proficiency among younger professionals is high. A significant share of the working-age population also holds functional competency in French, German, or Italian, which reduces onboarding friction for multinationals operating across multiple European markets.

- Engineering and IT salaries remain below the EU average while skill levels are internationally competitive

- Employer social contributions are structured to minimize the employer-side payroll burden

- Major university cities provide a distributed talent base, not concentrated in a single metro area

Why Romania Stands Out Among EU Incorporation Destinations

Evaluated against jurisdictions that foreign investors most commonly weigh alongside a Romanian entity, the relevant comparators are Bulgaria, Hungary, and Poland. All three share EU membership, target similar investor profiles, and are geographically proximate. The comparison is instructive because it shifts the question from absolute rates to structural fit: tax regime flexibility, treaty network depth, and formation cost combine to shape the real cost of operating a compliant EU entity.

Where Romania distinguishes itself is not in any single metric but in the combination of a tiered income-based tax structure alongside a mature treaty network. The micro-enterprise regime under the Fiscal Code allows qualifying SRLs to pay 1% or 3% on turnover rather than the standard 16% corporate rate, a structural feature that has no direct equivalent in Hungary or Poland. For a business generating modest early-stage revenue, this design compresses the effective tax burden without requiring offshore structuring.

| Parameter | Romania | Bulgaria | Hungary | Poland |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 16% | 10% | 9% | 19% (9% for small taxpayers) |

| Micro/SME Preferential Regime | Yes (1–3% on turnover) | No direct equivalent | No | Limited |

| Double Tax Treaties | 90+ | 70+ | 80+ | 80+ |

| Minimum Share Capital (Standard LLC) | RON 200 (~EUR 40) | BGN 2 (~EUR 1) | HUF 3,000,000 (~EUR 8,000) | PLN 5,000 (~EUR 1,150) |

| EU VAT Registration Access | Yes | Yes | Yes | Yes |

| Annual Compliance Filing Body | ANAF / Trade Register | NRA / Commercial Register | NAV / Company Court | KAS / KRS |

Compliance Services for Romanian Companies

Ongoing compliance support for SRLs and other Romanian entities, covering annual filings, ANAF reporting obligations, and Trade Register requirements.

Conclusion

Romania's position as an EU member state with one of the bloc's lower corporate tax rates makes a compelling structural case for foreign incorporation. The micro-enterprise regime, which caps tax liability at 1% or 3% of turnover rather than net profit, directly reduces the tax burden for early-stage businesses in ways that standard corporate tax structures in comparable EU jurisdictions do not. Combined with treaty coverage across 90+ countries, your entity gains a network of double taxation protections that directly affects cross-border profit repatriation and withholding obligations.

The benefits of incorporating in Romania are not uniform across all business types. A technology firm staffed by locally hired engineers benefits differently from a trading company using a Romanian SRL purely for EU market access. Your industry, revenue model, and shareholder structure each affect which aspects of the framework apply and to what degree.

For businesses that do qualify under the relevant thresholds and conditions, the combination of EU single market access, a treaty-backed tax framework, and a skilled workforce available at labor costs below the Western European average represents a materially significant structural advantage. Formalising that advantage requires accurate entity setup, correct registration with the Oficiul National al Registrului Comertului, and ongoing compliance with ANAF's reporting obligations. Getting those steps right from the outset determines whether the theoretical benefits translate into operational ones.

Start Your Romanian Company Formation With Expanship Today

Expanship supports foreign investors through each stage of Romanian company formation, from initial name reservation at the Oficiul Național al Registrului Comerțului (ONRC) through to post-incorporation compliance under Romanian law. The blog sections above have covered the SRL structure, applicable tax regimes, workforce considerations, and treaty access — the services described below are built around those same operational and regulatory requirements.

Expanship's scope for Romania business incorporation covers the following:

- Preparation and legalization of founding documents, including the constitutive act required under Law No. 31/1990

- Registered agent and registered office provision in Romania, as required for ONRC registration

- Government filing and direct liaison with the ONRC and, where applicable, ANAF for tax registration

- Post-incorporation compliance management, including annual reporting and statutory obligations

- Corporate maintenance services covering share transfers, director changes, and capital amendments

- Banking introduction assistance to support account opening with Romanian financial institutions

Reach out to Expanship Romania to discuss your company setup requirements.

Frequently Asked Questions (FAQ)

Standard registration through the ONRC typically takes between three and five business days once all documentation is submitted in the correct form. Delays most commonly arise from incomplete notarized documents, discrepancies in the articles of association, or pending apostille certifications on foreign-issued identity documents. Expedited processing is available for an additional fee, which can reduce the timeline to one business day.

Since the amendment introduced through Law No. 223/2020, the minimum share capital requirement for an SRL was reduced to 1 Romanian leu. The capital does not need to be deposited in a blocked escrow account prior to registration, which removes a procedural step that previously added time and cost to the formation process.

Under the Romanian Fiscal Code, companies with annual turnover below 500,000 euros may qualify for the micro-enterprise regime, paying 1% tax on revenue if they have at least one full-time employee, or 3% if they do not. Certain activity types are excluded, including banking, insurance, gambling, and petroleum exploration. A company that exceeds the turnover threshold during the fiscal year transitions to the standard 16% corporate income tax rate from the quarter in which the limit was breached.

A Romanian company can apply for a Romanian VAT number through the National Agency for Fiscal Administration (ANAF), which grants access to the EU VAT system, including intra-community acquisitions and supplies. Registration is not automatic upon incorporation; it must be applied for separately, either voluntarily or once the domestic VAT threshold of 300,000 Romanian lei is exceeded. Once registered, the entity can engage in VAT-exempt intra-community transactions and use the EU's OSS (One Stop Shop) scheme for cross-border digital and e-commerce services.

The majority of treaties concluded by Romania follow the OECD Model Tax Convention framework, covering income categories such as dividends, interest, royalties, capital gains, and employment income. The specific withholding tax rates for dividends and royalties vary by treaty, and the applicable rate depends on the tax residency of the beneficial owner. The treaties are administered in conjunction with domestic rules under the Romanian Fiscal Code, and treaty benefits must generally be claimed by presenting a certificate of fiscal residency issued by the counterpart jurisdiction's tax authority.

If a company registered under the micro-enterprise regime loses its qualifying employee during the fiscal year and does not hire a replacement within 30 days, the applicable tax rate increases from 1% to 3% on revenue. Continued non-compliance with the employee condition beyond the stipulated period can result in reclassification to the standard corporate income tax regime. ANAF monitors compliance through mandatory payroll reporting obligations, and retroactive adjustments to tax liability may apply for the affected fiscal quarters.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.