Key Takeaways

- The Ley General de Sociedades Mercantiles (LGSM) governs most commercial entity types in Mexico, with formal incorporation processed through the Registro Público de Comercio under the Secretaría de Economía.

- The Sociedad Anónima (SA) remains the most widely registered entity in Mexico, making it the default choice for mid-to-large businesses requiring a share-based capital structure.

- Mexico's Sociedad por Acciones Simplificada (SAS) is the only entity type offering a fully digital registration process, designed for low-capital ventures with a single founder.

- Regulatory trends in Mexico are moving toward stricter beneficial ownership reporting, with both the SAT and IMSS tightening anti-money laundering compliance requirements.

Introduction to Entity Types in Mexico

Mexico is a federal republic in North America, bordered by the United States to the north and Guatemala and Belize to the southeast. Selecting among the available types of business entities in Mexico requires an understanding of how each structure is governed under the Ley General de Sociedades Mercantiles (LGSM) — the General Law of Mercantile Corporations — which establishes the legal framework for most commercial entities operating in the country.

Company registration falls under the oversight of the Secretaría de Economía (Ministry of Economy), with the Registro Público de Comercio handling the formal incorporation process at the federal level. The country operates a residence-based tax system, with additional obligations governed by the Servicio de Administración Tributaria (SAT).

Mexican legal entity types available to both domestic and foreign investors include the Sociedad Anónima (SA), Sociedad Anónima Bursátil (SAB), Sociedad de Responsabilidad Limitada (SRL), Sociedad por Acciones Simplificada (SAS), various partnership structures, cooperative societies, foreign branch and representative offices, and the sole proprietorship format known as Persona Física con Actividad Empresarial.

Each structure carries distinct implications for liability, ownership, taxation, and regulatory compliance — all of which this article addresses in turn.

An Overview of Business Structures in Mexico

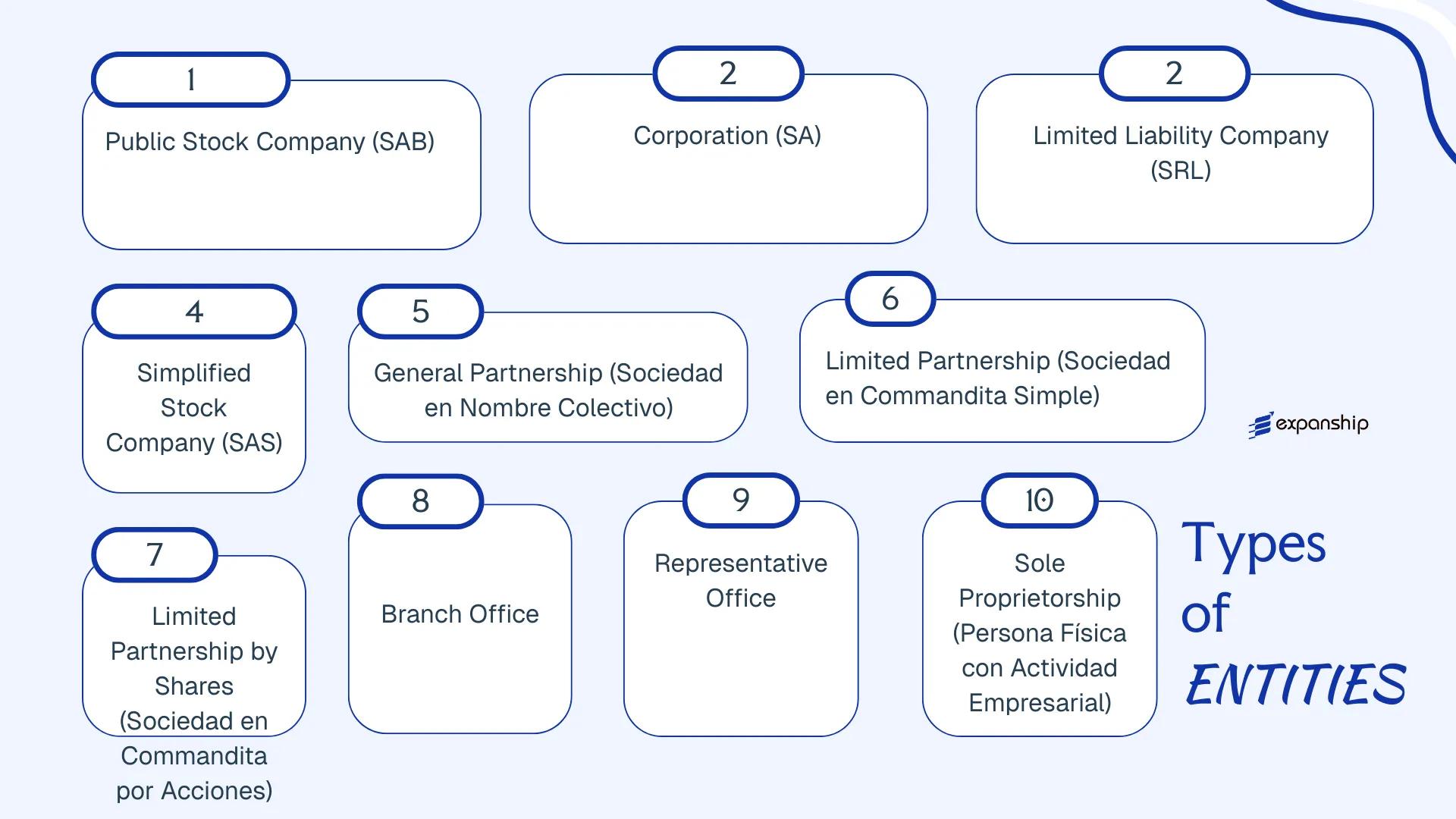

Mexico's company law framework offers eight principal business structures, each governed primarily by the Ley General de Sociedades Mercantiles (LGSM) of 1934, with the Sociedad por Acciones Simplificada introduced later under a 2016 amendment to that same statute. Foreign investors and domestic entrepreneurs alike work within this framework, which also draws on the Código de Comercio and sector-specific regulations administered by the Secretaría de Economía. Each structure carries distinct implications for liability, governance, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima Bursátil (SAB) | Public corporation | Limited to shares | Taxable | Permitted | 2 shareholders | CNBV / Secretaría de Economía | LGSM / Ley del Mercado de Valores |

| Sociedad Anónima (SA) | Private corporation | Limited to shares | Taxable | Permitted | 2 shareholders | Secretaría de Economía | LGSM |

| Sociedad de Responsabilidad Limitada (SRL) | LLC | Limited to contributions | Taxable | Permitted | 2 partners (max 50) | Secretaría de Economía | LGSM |

| Sociedad por Acciones Simplificada (SAS) | Simplified corporation | Limited to shares | Taxable | Permitted | 1 shareholder | Secretaría de Economía | LGSM (2016 amendment) |

| Sociedad en Nombre Colectivo | General partnership | Unlimited | Taxable | Permitted | 2 partners | Secretaría de Economía | LGSM |

| Sociedad en Commandita Simple | Limited partnership | Mixed | Taxable | Permitted | 2 partners | Secretaría de Economía | LGSM |

| Sociedad en Commandita por Acciones | Share-based limited partnership | Mixed | Taxable | Permitted | 2 partners | Secretaría de Economía | LGSM |

| Sociedad Cooperativa de Producción | Production cooperative | Limited | Tax-exempt (conditions apply) | Permitted | 5 members | Secretaría del Trabajo | Ley General de Sociedades Cooperativas |

| Sociedad Cooperativa de Consumo | Consumer cooperative | Limited | Tax-exempt (conditions apply) | Permitted | 5 members | Secretaría del Trabajo | Ley General de Sociedades Cooperativas |

| Branch Office | Foreign branch | Parent liable | Taxable | Permitted | N/A | Secretaría de Economía | Ley de Inversión Extranjera |

| Representative Office | Liaison office | Parent liable | Generally non-taxable | Not permitted | N/A | Secretaría de Economía | Ley de Inversión Extranjera |

| Persona Física con Actividad Empresarial | Sole proprietorship | Unlimited personal | Taxable | Permitted | 1 individual | SAT | Código Fiscal de la Federación |

Each of these structures is examined in full in the sections below.

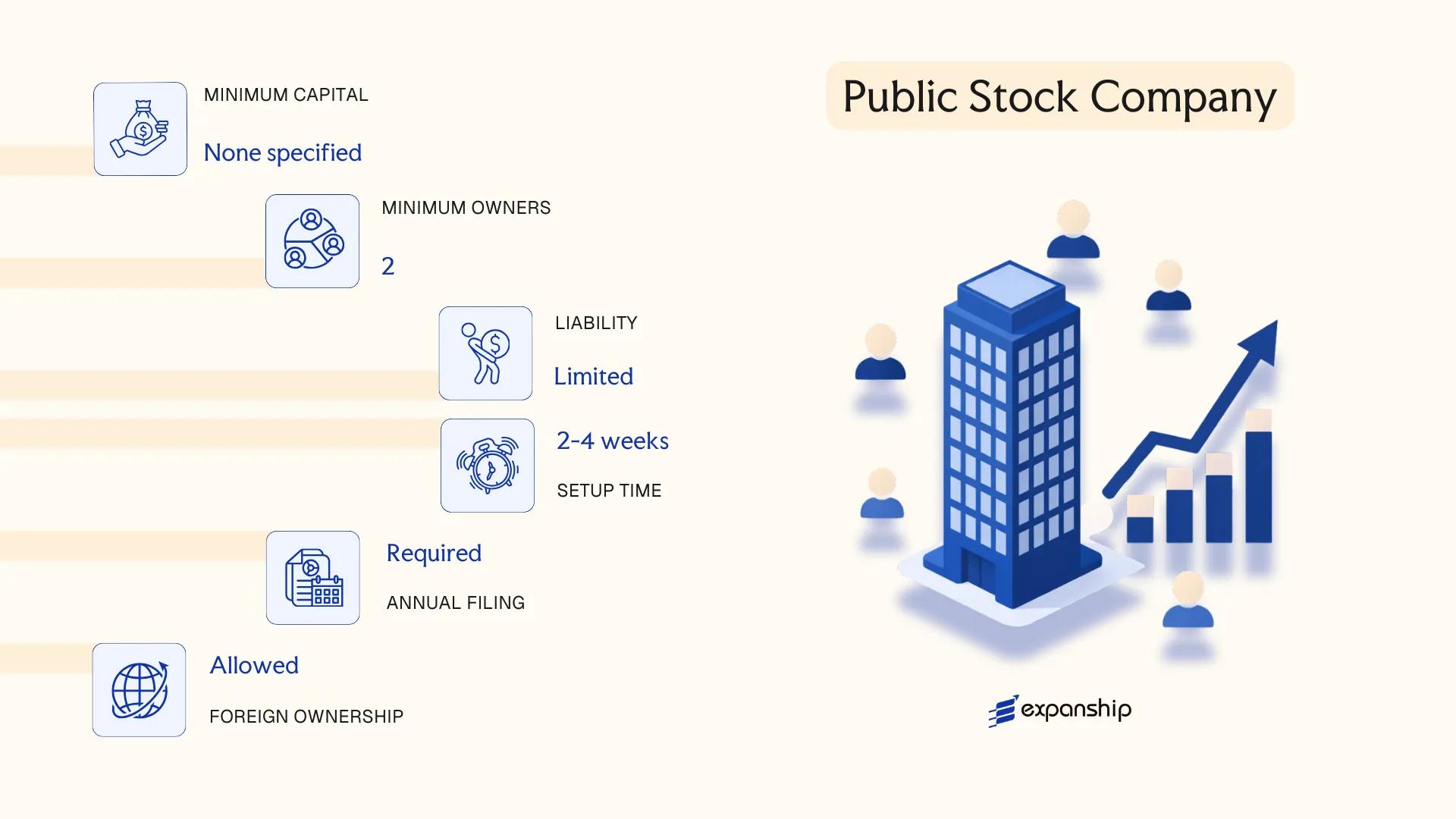

Sociedad Anónima Bursátil (SAB) — Public Stock Company

The Sociedad Anónima Bursátil Mexico SAB is governed by the Ley del Mercado de Valores (LMV) of 2005, which established this entity as a distinct corporate form separate from the standard SA. It carries full legal personality and limited liability for its shareholders, but unlike a private corporation, its shares are registered and traded on the Bolsa Mexicana de Valores (BMV) or another recognized securities exchange.

This structure functions as a hybrid — retaining the foundational corporate mechanics of an SA while layering in mandatory public disclosure, minority shareholder protections, and oversight by the Comisión Nacional Bancaria y de Valores (CNBV). Governance requirements are substantially more demanding than those of a private entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima Bursátil | Governed by LMV 2005 |

| Members | Shareholders (Accionistas) | Minimum 2; no statutory maximum; public float required |

| Local Presence | Registered office in Mexico; CNBV-registered | Exchange listing mandatory |

| Capital | MXN; no fixed statutory minimum, but listing rules apply | BMV sets minimum float and capitalization thresholds |

| Privacy | Low | Full public disclosure of financials and ownership |

| Governance | Board of Directors required; independent directors mandatory | Minimum 25% of board must be independent under LMV |

Focus Points

- Taxation: Subject to 30% corporate income tax (ISR); 16% VAT on applicable transactions; dividend withholding at 10% for individuals; SAT administers federal tax obligations.

- Annual Compliance: Audited financial statements, quarterly and annual reports filed with CNBV; continuous disclosure obligations under LMV.

- Economic Substance: Must maintain genuine operational and governance presence given exchange listing and regulatory scrutiny.

- Treaty Access: Qualifies for benefits under Mexico's tax treaties as a resident entity, subject to limitation-on-benefits provisions.

- Conversion: An SA may convert to SAB status upon satisfying CNBV registration and BMV listing requirements; conversion requires shareholder approval and public deed amendment.

Closing

The SAB suits large enterprises seeking access to public capital markets, institutional investors, or a listing pathway for an existing private corporation. The primary advantage is unrestricted access to equity capital through public share issuance; the principal drawback is the continuous and costly regulatory burden imposed by CNBV oversight and exchange listing rules.

Large, established businesses with significant capital requirements and the operational capacity to meet ongoing public disclosure and corporate governance obligations.

Company Incorporation in Mexico

Incorporate your business entity in Mexico with end-to-end support across entity types, registration, and compliance.

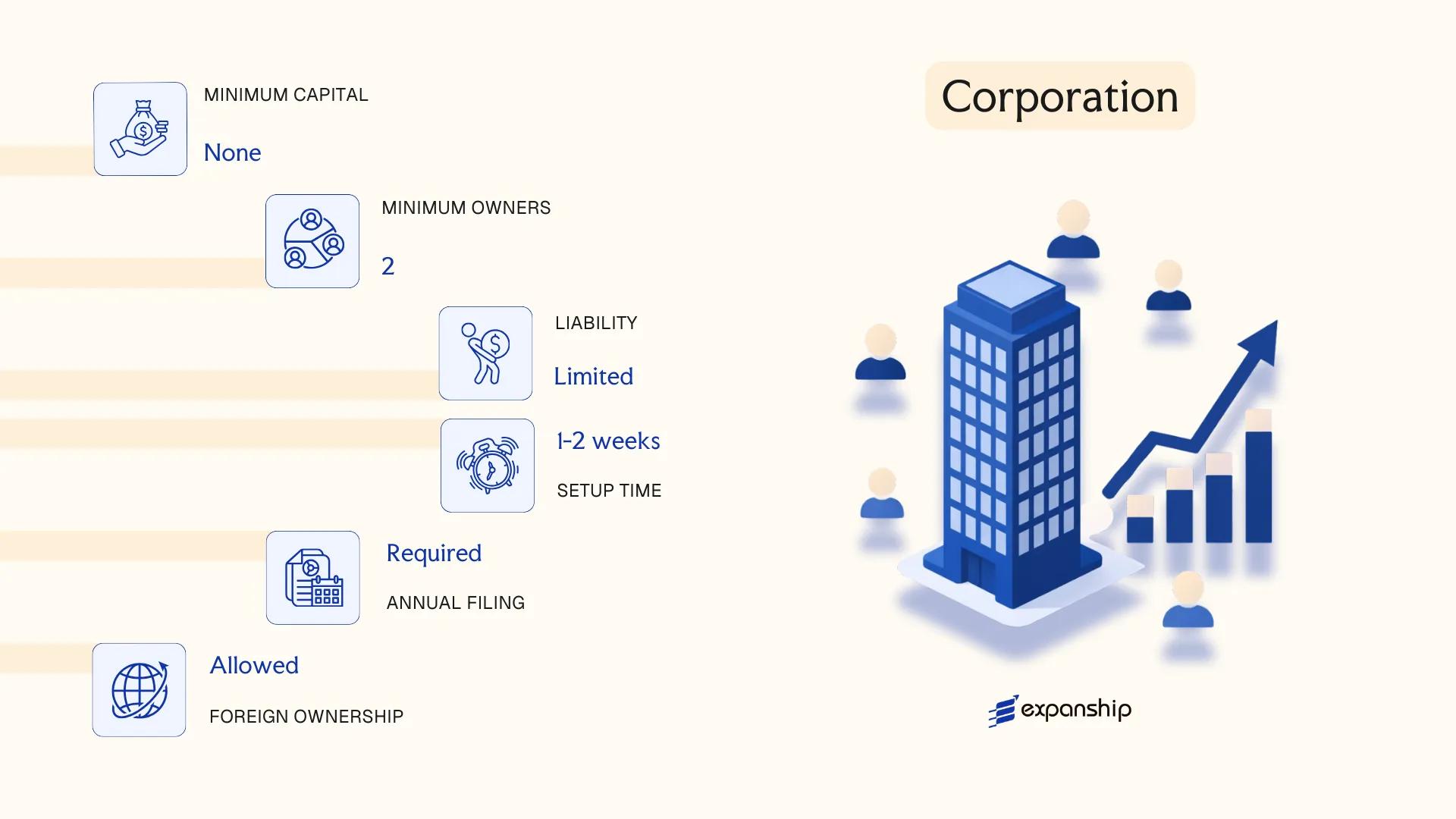

Sociedad Anónima (SA) — Corporation

Governed by the Ley General de Sociedades Mercantiles (LGSM) of 1934, the Sociedad Anónima is the standard corporate structure for medium to large private businesses. A Sociedad Anónima Mexico corporation setup confers full separate legal personality upon incorporation, meaning the entity holds rights and obligations independently of its shareholders.

Liability is capped at each shareholder's subscribed capital contribution. Capital is divided into shares, which may be transferred subject to any restrictions set out in the corporate bylaws (estatutos sociales).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (SA) or SA de CV | "de CV" (de Capital Variable) denotes variable capital |

| Members | Minimum 2 shareholders; no statutory maximum | Shareholders hold shares (acciones); no public listing |

| Management | Board of Directors or sole administrator (administrador único) | At least one Comisario (statutory auditor) required |

| Local Presence | Registered address in Mexico required | A notario público must formalize incorporation |

| Capital | Minimum MXN 50,000; at least 20% paid-in at incorporation | Denominated in Mexican pesos |

| Privacy | Shareholder names appear in public registry (RPC) | Beneficial ownership disclosed to SAT under AML rules |

Focus Points

- Taxation: Subject to 30% corporate income tax (ISR); 16% VAT (IVA) on applicable transactions; 10% withholding tax on dividends distributed to non-residents; no stamp duty on share transfers.

- Annual Compliance: Annual shareholders' meeting required; audited financial statements mandatory above certain revenue thresholds set by SAT.

- Treaty Access: Qualifies for benefits under Mexico's tax treaty network, provided substance and beneficial ownership requirements are met.

- Conversion: May convert to SA de CV by amending bylaws to introduce variable capital provisions, without dissolving the entity.

- Foreign Ownership: 100% foreign ownership is permitted in most sectors; restricted or regulated industries require prior authorization from the Comisión Nacional de Inversiones Extranjeras (CNIE).

Sub-Types

SA de CV (Sociedad Anónima de Capital Variable)

The SA de CV Mexico formation adds a variable capital regime, allowing the company to increase or reduce its capital without requiring a full notarial amendment each time. This structure is the most widely used variant for both domestic and foreign-owned operating companies.

Recommendations

The SA suits foreign investors establishing operating subsidiaries, holding structures, or joint ventures where scalability and treaty access are priorities. Its main constraint is administrative overhead: ongoing notarial requirements, mandatory statutory auditors, and public registry disclosure make it more burdensome than lighter structures.

Foreign companies and investors seeking a recognized, scalable corporate vehicle with access to Mexico's tax treaty network and the ability to support multiple shareholders or future equity restructuring.

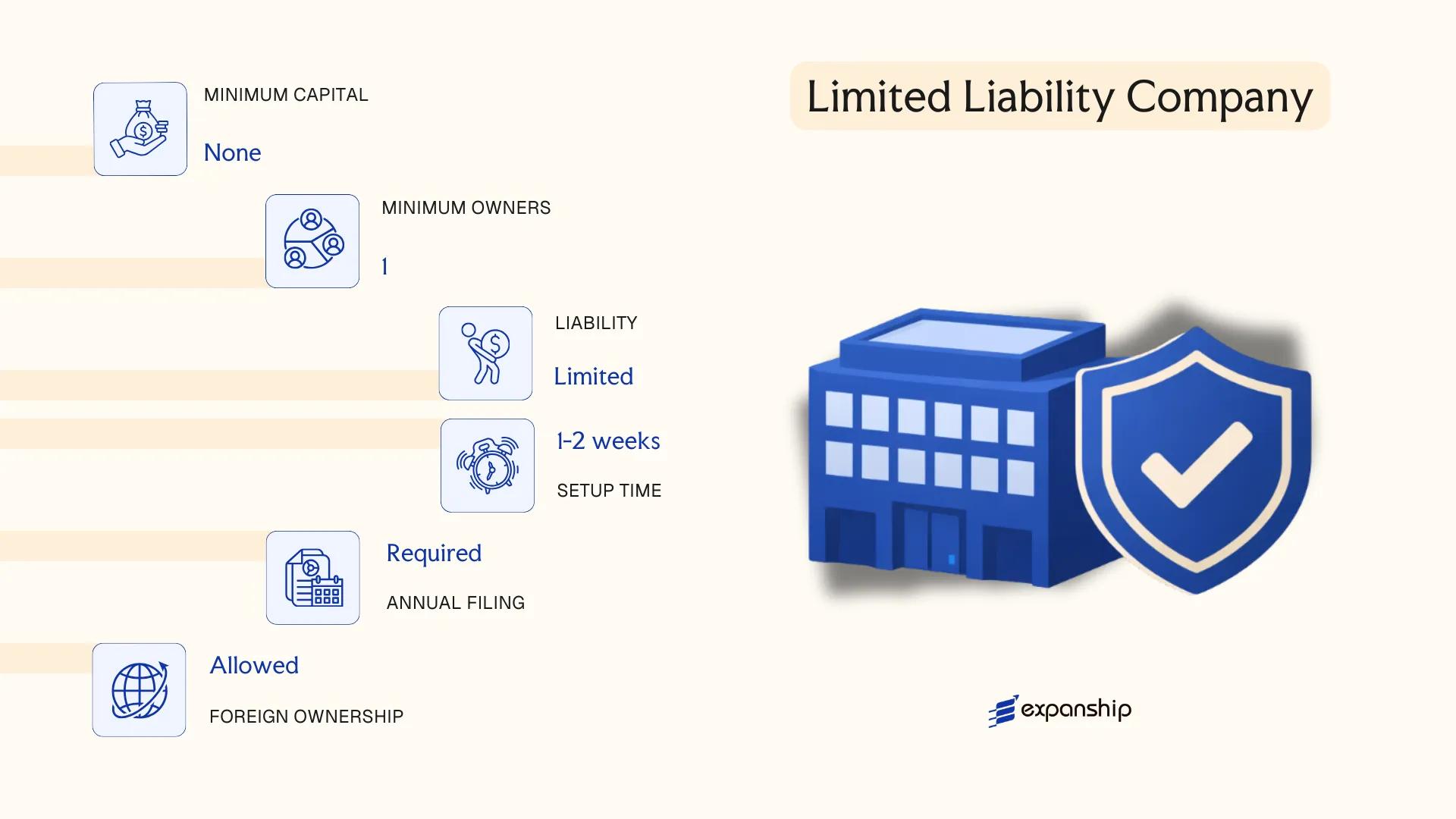

Sociedad de Responsabilidad Limitada (SRL) — Limited Liability Company

The Sociedad de Responsabilidad Limitada Mexico SRL is governed by the Ley General de Sociedades Mercantiles (LGSM), originally enacted in 1934 and amended periodically since. It carries separate legal personality from its members, meaning the entity can hold assets, enter contracts, and incur obligations in its own name.

Liability is capped at each member's capital contribution. This hybrid character — combining the liability protection of a corporation with a more flexible internal governance structure — makes the SRL a recognized equivalent to an LLC in other jurisdictions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada | Governed by LGSM; separate legal personality |

| Members | 2 minimum, 50 maximum | Members (socios) hold participaciones (quotas), not shares |

| Management | One or more gerentes (managers) | Can be members or third parties; no board requirement |

| Local Presence | Registered address in Mexico required | Registered agent not mandated by statute, but a fiscal domicile is required for SAT registration |

| Capital | No statutory minimum under current LGSM | Capital divided into quotas; contributions recorded in the public deed |

| Privacy | Member names appear in the public deed registered with the Public Registry of Commerce | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to 30% corporate income tax (ISR); VAT at 16% on taxable supplies; dividend distributions to foreign members attract a 10% withholding tax; no stamp duty on incorporation.

- Annual Compliance: Annual financial statements required; tax filings with the Servicio de Administración Tributaria (SAT); monthly VAT and ISR provisional declarations.

- Treaty Access: Qualifies for benefits under Mexico's tax treaty network, subject to beneficial ownership and anti-abuse provisions.

- Conversion: Can be converted to an SA or other mercantile form under LGSM procedures, requiring notarial deed and re-registration.

- Restrictions: The 50-member cap is a hard statutory limit; exceeding it requires conversion to an SA.

Closing

The SRL suits small-to-mid-size trading operations, joint ventures, and holding structures where a limited number of known participants want defined governance without the formalities of a public company. The quota-based ownership structure allows flexible profit allocation, though the 50-member ceiling restricts scalability for larger capital-raising exercises.

The SRL is most appropriate for closely held businesses, bilateral joint ventures, or foreign subsidiaries where ownership is concentrated and public share issuance is not required.

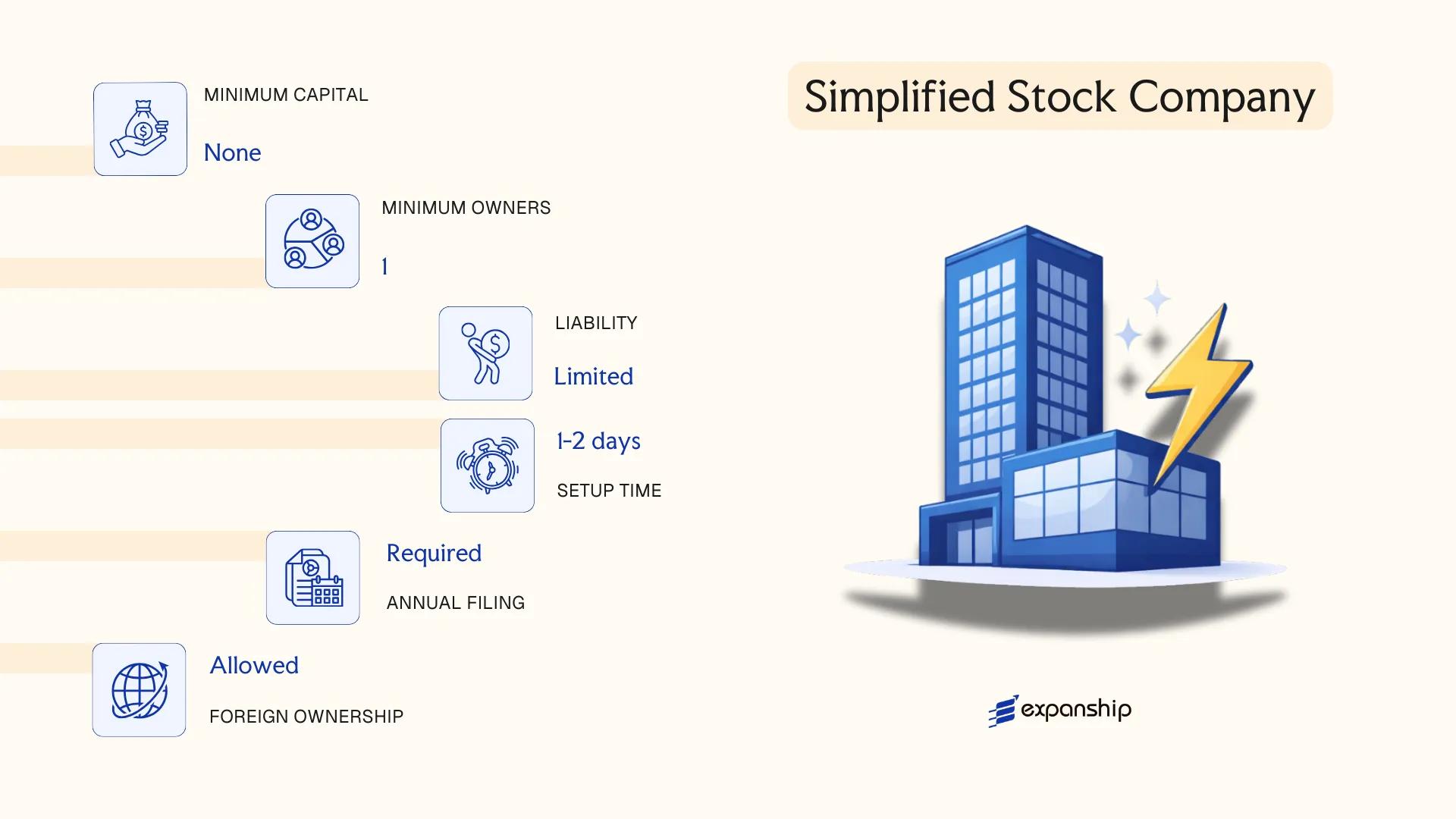

Sociedad por Acciones Simplificada (SAS) — Simplified Stock Company

Introduced under the Ley para Regular las Instituciones de Tecnología Financiera and subsequently governed by amendments to the Ley General de Sociedades Mercantiles (LGSM) in 2016, the Sociedad por Acciones Simplificada Mexico SAS is a simplified corporate form designed to reduce administrative barriers for small businesses and startups. It carries separate legal personality and grants shareholders limited liability up to the value of their contributed capital.

Registration is conducted entirely online through the Secretaría de Economía's Sistema de Apertura Rápida de Empresas (SARE) platform, without requiring a notarial deed. This distinguishes the SAS from most other Mexican corporate forms and significantly reduces formation costs.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad por Acciones Simplificada | Governed by LGSM, Chapter XIV |

| Members | Shareholders; 1–50 natural persons only | Legal entities cannot be shareholders |

| Management | Sole Administrator or Board | Appointed by shareholders |

| Local Presence | Registered address in Mexico required | No mandatory local director |

| Capital | No statutory minimum; MXN-denominated | Capital divided into shares |

| Revenue Cap | Annual income must not exceed MXN 5 million | Exceeding this threshold requires conversion |

| Privacy | Shareholder data filed with Secretaría de Economía | Limited public privacy |

Focus Points

- Taxation: Subject to corporate income tax (ISR) at 30%, VAT (IVA) at 16%, and applicable withholding taxes on dividends and royalties; no special tax regime applies by default.

- Annual Compliance: Financial statements must be filed electronically; no notarial intervention required for routine filings.

- Restrictions: Shareholders must be natural persons only; foreign individuals may participate, but the revenue cap and shareholder limit constrain scalability.

- Conversion: Upon exceeding the MXN 5 million annual revenue threshold, the entity must convert to a Sociedad Anónima or another qualifying form under the LGSM.

- Treaty Access: As a Mexican-resident entity, the SAS can access Mexico's tax treaty network, subject to beneficial ownership and substance requirements.

Closing

The SAS suits early-stage domestic ventures and sole founders testing a business model, with online formation at minimal cost being its principal practical advantage. Its hard cap of 50 natural-person shareholders and the MXN 5 million revenue ceiling make it unsuitable for scaling businesses or those seeking external equity investment.

The SAS is best suited for Mexican-resident entrepreneurs and small founding teams launching low-revenue, early-stage ventures who want a formal legal structure without notarial formation costs.

Partnerships [Sociedad en Nombre Colectivo, Sociedad en Commandita Simple, Sociedad en Commandita por Acciones]

Partnership structures in Mexico business law are governed by the Ley General de Sociedades Mercantiles (LGSM) of 1934, which remains the primary federal statute regulating commercial entities. All three partnership forms carry separate legal personality upon registration with the Registro Público de Comercio, distinguishing them from informal arrangements.

Each structure allocates liability differently across partner classes. Two forms apply unlimited joint liability to at least one category of partner, while the share-based variant introduces capital divided into shares, creating a hybrid between a partnership and a corporation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad en Nombre Colectivo / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones | All three are mercantile entities under the LGSM |

| Members | Partners (socios); general (gestores) and limited (comanditarios) where applicable | Minimum 2 partners; no statutory maximum |

| Liability | Unlimited for general partners; limited to capital contribution for comanditarios | SNC partners bear unlimited joint liability across all members |

| Local Presence | Registered domicile in Mexico; notarised deed required | No mandatory resident director requirement under LGSM |

| Capital | No statutory minimum; SCA divides capital into shares | SCS divides capital into parts (partes sociales), not shares |

| Privacy | Partner names appear in the public registry and, for SNC, in the firm name itself | Low privacy by structure |

Focus Points

- Taxation: Subject to corporate income tax (ISR) at 30%, VAT (IVA) at 16% on applicable transactions, and withholding taxes on profit distributions to foreign partners; no separate stamp duty regime applies.

- Annual Compliance: Filing of annual tax return with the Servicio de Administración Tributaria (SAT); financial statements required; changes to partnership deed require notarial intervention and registry update.

- Treaty Access: Entities qualify as Mexican residents for purposes of tax treaty access, subject to SAT residency certification.

- Restrictions: Foreign ownership is permitted but subject to sector-specific restrictions under the Ley de Inversión Extranjera; certain activities require prior authorisation from the Comisión Nacional de Inversiones Extranjeras.

- Conversion: LGSM permits transformation into other entity types through a formal deed process and creditor notification period.

Sub-Types

Sociedad en Nombre Colectivo (SNC)

All partners carry unlimited, joint, and subsidiary liability for firm obligations. The firm name must include a partner's surname, making partner identity publicly visible by law.

Sociedad en Comandita Simple (SCS)

Two partner classes coexist: general partners with unlimited liability who manage the firm, and limited partners (comanditarios) whose liability is capped at their capital contribution. Limited partners cannot participate in management without losing their liability protection.

Sociedad en Comandita por Acciones (SCA)

Capital is divided into shares rather than participations, applying the comandita structure to a share-based framework. This makes the SCA closer in capital mechanics to the SA while retaining dual partner-class liability rules.

Closing

These structures suit family-owned trading operations or professional firms where partners accept personal liability in exchange for operational simplicity, though the unlimited liability exposure of general partners makes them unsuitable for high-risk commercial ventures.

These partnership forms are best suited for closely held, low-risk businesses where founding partners are willing to accept personal liability and do not anticipate external investment.

Cooperative [Sociedad Cooperativa de Producción, Sociedad Cooperativa de Consumo]

Sociedad Cooperativa Mexico formation requirements are governed by the Ley General de Sociedades Cooperativas (LGSC), enacted in 1994 and last significantly amended in 2009. A Sociedad Cooperativa holds separate legal personality upon registration and operates on the principle of limited liability for its members.

Unlike capital-driven entities, this structure is worker- or consumer-oriented by design. Profits are distributed as surplus returns rather than dividends, and voting rights follow a one-member-one-vote rule regardless of capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Cooperativa (SC) | Governed by the LGSC 1994 |

| Members | Referred to as socios; minimum 5, no statutory maximum | All members hold equal voting rights |

| Local Presence | Registered address in Mexico required | No registered agent requirement under LGSC |

| Capital | Variable capital (capital variable); no fixed minimum | Contributions recorded via certificates (certificados de aportación) |

| Privacy | Member register maintained internally; not fully public | Filed with Registro Público de Comercio |

Focus Points

- Taxation: Subject to Income Tax (ISR) at the entity level; surplus distributions to members may receive preferential treatment; VAT obligations apply to commercial activities; no stamp duty on cooperative formations.

- Annual Compliance: Annual general assembly required; audited financial statements mandatory above certain thresholds; surplus distribution resolutions must be documented.

- Restrictions: Foreign participation is permitted but subject to foreign investment rules under the Ley de Inversión Extranjera; certain sectors may restrict cooperative ownership.

- Conversion: A cooperative may convert to a mercantile society under Mexican law, though the process requires unanimous member approval and notarial intervention.

Sub-Types

Sociedad Cooperativa de Producción

This variant organises workers who contribute labour directly to the cooperative's productive activity. It is the standard structure for worker cooperatives in manufacturing, services, or agriculture.

Sociedad Cooperativa de Consumo

Composed of consumers rather than workers, this sub-type pools purchasing power to supply goods or services to its own members. It is commonly used by credit unions, housing cooperatives, and consumer supply groups.

Who Uses This Structure

The Sociedad Cooperativa suits worker-owned enterprises and member-service organisations rather than conventional commercial ventures. Its primary advantage is democratic governance combined with favourable surplus distribution treatment; its principal limitation is that raising external investment capital is structurally difficult, since ownership cannot be transferred through shares in the conventional sense.

Best suited for worker collectives, artisan groups, or consumer associations where shared ownership and equal governance are structural priorities rather than incidental features.

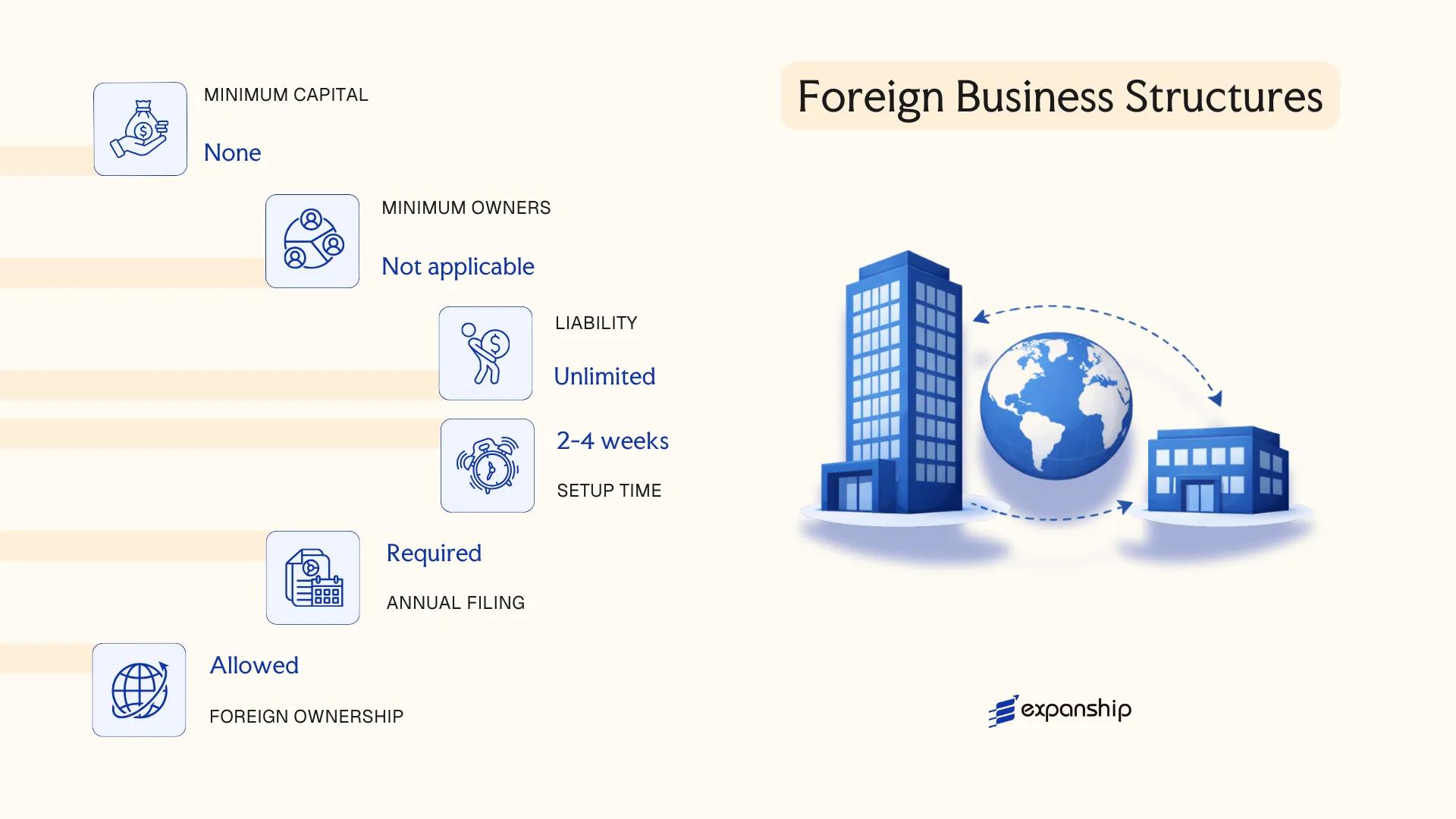

Foreign Business Structures [Branch Office, Representative Office]

Foreign companies seeking a presence in Mexico without incorporating a new local entity may operate through either a branch office or a representative office. A foreign company branch office Mexico setup is governed by the Ley General de Sociedades Mercantiles (LGSM) and requires registration with the Registro Público de Comercio. Unlike a locally incorporated entity, a branch (Sucursal) has no separate legal personality — the parent company bears full liability for its Mexican operations.

A representative office (Oficina de Representación) serves a more limited function. It may conduct market research and promotional activities but cannot engage in revenue-generating commercial transactions. Both structures require a legal representative domiciled in Mexico who holds a notarized power of attorney.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Prohibited |

| Local Representative | Required (notarized power of attorney) | Required (notarized power of attorney) |

| Registered Address | Required in Mexico | Required in Mexico |

| SAT Registration | Mandatory (RFC number) | Required if employees present |

| Minimum Capital | None prescribed by law | None |

| Privacy | Parent company details publicly registered | Parent company details publicly registered |

Focus Points

- Taxation: Branch profits are subject to 30% corporate income tax (ISR); VAT at 16% applies to taxable supplies; a 10% profit remittance tax applies when distributing earnings to the foreign parent; no separate stamp duty regime exists.

- Treaty Access: Mexico's tax treaty network may reduce withholding on remittances, depending on the parent's jurisdiction of residence.

- Annual Compliance: Branches must file annual ISR returns with the Servicio de Administración Tributaria (SAT) and maintain Mexican-standard accounting records.

- Commercial Restrictions: A representative office cannot invoice clients, sign commercial contracts, or generate local revenue.

- Conversion: A branch may not be converted directly into a Mexican corporation; a new entity must be incorporated separately.

Sub-Types

Sucursal (Branch Office)

A Sucursal is a fully operational extension of the foreign parent, permitted to enter contracts, generate revenue, and employ staff in Mexico. It is commonly used by foreign firms testing the market before committing to full local incorporation.

Oficina de Representación (Representative Office)

An Oficina de Representación is restricted to liaison, promotional, and preparatory activities. It suits firms whose Mexican presence is limited to supporting overseas sales or coordinating with local partners, with no intention of direct commercial engagement.

Closing

Both structures suit foreign companies seeking a transitional or limited operational footprint without the administrative burden of forming a new legal entity. The primary constraint is the absence of limited liability — the parent remains fully exposed to obligations incurred in Mexico.

Foreign companies conducting pre-market research or managing limited in-country operations while maintaining centralized control under the parent entity.

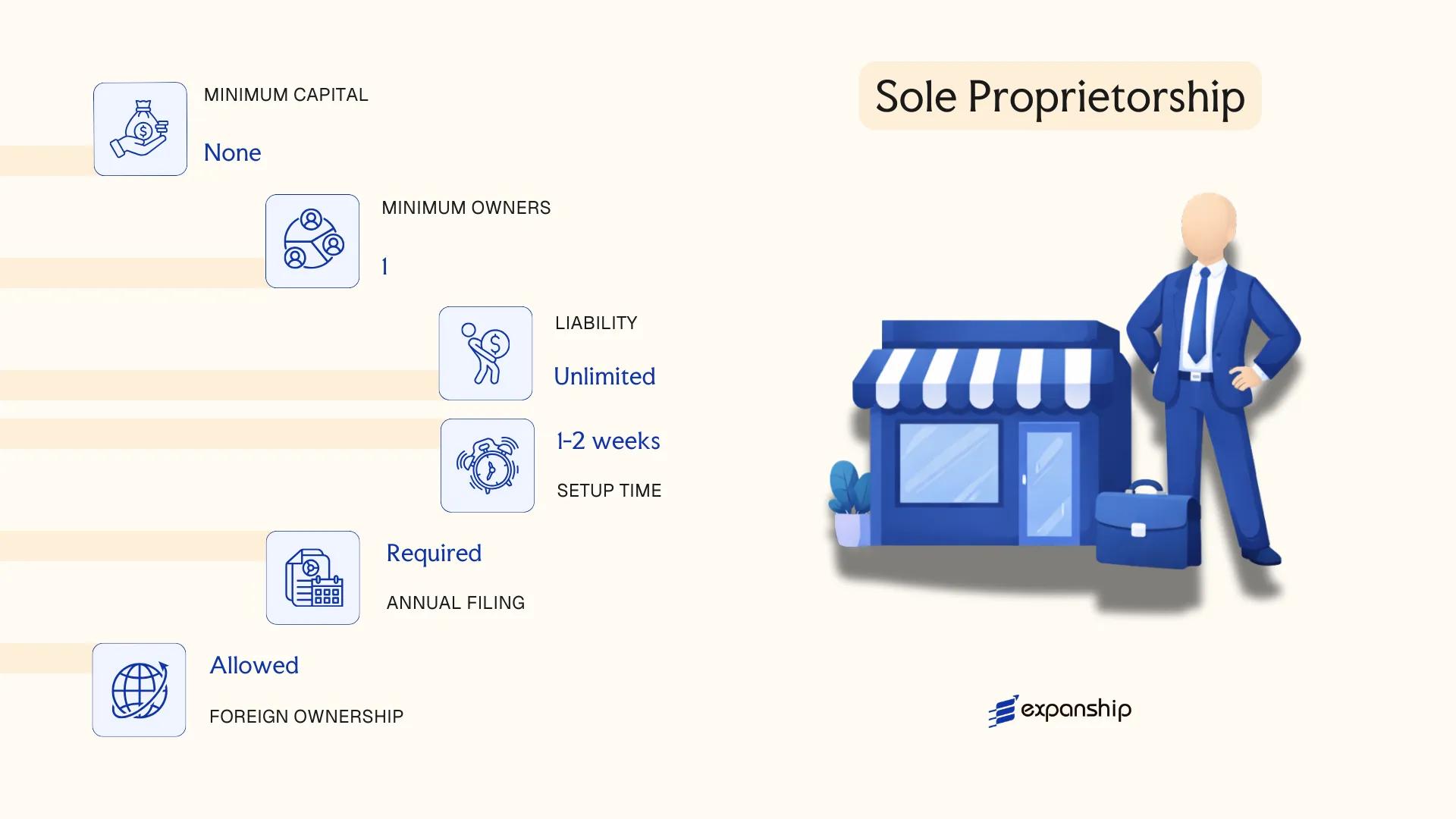

Sole Proprietorship [Persona Física con Actividad Empresarial]

Operating as a Persona Física con Actividad Empresarial Mexico means conducting business as an individual rather than through a separate legal entity. This structure is governed by the Ley del Impuesto sobre la Renta (LISR) and regulated at the federal level by the Servicio de Administración Tributaria (SAT), which oversees registration, tax filing, and compliance obligations.

Unlike corporate forms, this structure carries no separate legal personality. The proprietor and the business are the same legal subject, meaning personal assets are fully exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual with business activity | Not a corporate entity; no separate legal personality |

| Referred To As | Proprietor / Contribuyente | Registered individually before the SAT |

| Members | 1 individual only | No partners or shareholders permitted |

| Local Presence | RFC registration; domicilio fiscal required | Must maintain a registered tax address in Mexico |

| Capital | No minimum capital requirement | Personal assets and business assets are not legally separated |

| Privacy | RFC and tax data held by SAT | Business records are not publicly filed in a commercial registry |

Focus Points

- Taxation: Subject to personal income tax (ISR) at progressive rates up to 35%; VAT obligations apply if activity is taxable; eligible for the RIF regime replacement under the RESICO-PF simplified regime introduced in 2022 for qualifying small contributors.

- Annual Compliance: Must file monthly provisional ISR and VAT declarations, plus an annual tax return (declaración anual) before April 30.

- Economic Substance: No formal substance test, but the SAT may audit business activity to confirm the declared domicilio fiscal reflects actual operations.

- Conversion: Can incorporate into an SA or SRL at any time, though asset transfer may trigger tax consequences.

- Restrictions: Cannot issue shares, admit partners, or access certain B2B contracts that require a corporate counterparty.

Closing

This structure suits freelancers, sole traders, and small operators who need a low-cost, low-complexity entry point for conducting commercial activity without forming a company. The primary advantage is minimal setup cost and administrative simplicity; the principal drawback is unlimited personal liability for all business obligations.

Best suited for individual entrepreneurs or self-employed professionals in Mexico with low revenue, limited counterparty risk, and no plans to take on partners or outside investment.

How to Choose the Right Entity Type in Mexico

Selecting how to choose the right business entity in Mexico requires more than comparing registration fees — the structure you form shapes your tax position, liability exposure, and operational capacity for years.

Why Your Entity Choice Matters

- Registering a foreign entity as a representative office while conducting commercial transactions locally violates the Ley General de Sociedades Mercantiles and can result in forced dissolution or administrative penalties.

- Choosing an SAS when your business later requires external investment triggers mandatory conversion, since the SAS structure prohibits listing shares or admitting institutional shareholders.

- Selecting a structure without proper tax residency substance when the SAT applies economic substance scrutiny can result in income reclassification and surcharges on unpaid contributions.

- Forming an SA when a single-person consultancy is your model adds statutory audit thresholds and annual shareholders' meeting obligations that do not apply to a sole proprietorship regime.

Key Factors to Consider

- Business Activity: Active commercial trading, passive asset holding, and regulated sectors each point to a different statutory structure under Mexican mercantile law.

- Ownership Structure: A single founder generally suits an SAS or sole proprietorship, while multiple investors or foreign co-owners require an SA or SRL.

- Tax Objectives: Your eligibility for Mexico's tax treaty network and applicable ISR rate depends on entity classification and residency status.

- Liability Requirements: If personal asset protection is a priority, structures with unlimited partner liability — such as the Sociedad en Nombre Colectivo — are unsuitable.

- Exit Strategy: Not all Mexican entities permit redomiciliation or conversion without dissolution; confirm this before formation.

- Substance Capacity: If you cannot maintain a local office or payroll, confirm that your chosen structure does not trigger SAT permanent establishment rules.

Compliance Services for Companies in Mexico

Ongoing compliance support for Mexican entities, including SAT filings, annual meeting obligations, and statutory recordkeeping.

Conclusion

Selecting the right structure is one of the most consequential decisions in any starting a business in Mexico legal guide, and the choice ultimately depends on ownership composition, liability exposure, and intended activity. The Sociedad Anónima remains the most widely registered entity, favored by mid-to-large operators requiring share-based capital structures. The SRL suits smaller, closely held operations with a fixed pool of partners. The SAS addresses low-capital, single-founder ventures through a fully digital registration process under the Secretaría de Economía. Partnerships carry unlimited liability and are uncommon in commercial practice. The SAB applies exclusively to publicly listed companies under CNBV oversight. Foreign firms typically enter through a branch or representative office before committing to full incorporation.

Regulatory reform has trended toward digitization and anti-money laundering compliance, with the SAT and IMSS tightening beneficial ownership reporting requirements. Expanship assists clients in aligning their Mexico company formation summary with both current statute and projected compliance obligations.

How Expanship Can Assist You

Expanship's company incorporation services Mexico covers the full formation process, from selecting the right entity under the Ley General de Sociedades Mercantiles to registering with the Registro Público de Comercio and obtaining your RFC through the Servicio de Administración Tributaria (SAT). Whether you're forming an SA, an SRL, or the newer SAS structure, our team handles the regulatory steps specific to each.

Expanship's Mexico business setup assistance extends well beyond the initial filing:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Government filing and liaison with the Registro Público de Comercio

- Post-incorporation compliance management, including annual obligations

- Corporate tax registration with the SAT

- Banking introduction assistance for corporate account opening

Ready to move forward? Reach out to Expanship Mexico to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (SA) is the most frequently incorporated structure, largely because it accommodates a wide range of business activities, permits foreign shareholding, and is recognized across financial institutions and commercial counterparties. Its regulatory framework under the Ley General de Sociedades Mercantiles (LGSM) is well-established, which reduces legal uncertainty during setup and operation.

Both structures offer limited liability and separate legal personality, but they differ substantially in scale and compliance requirements. An SAS is restricted to annual revenues below 5 million pesos and cannot be used by entities with existing commercial obligations, whereas an SA carries no revenue ceiling. Tax treatment under the SAT follows the same general corporate income tax regime for both, but the SAS involves lighter formation formalities.

The SRL provides a degree of ownership discretion, as partner information is recorded in the public commerce registry (Registro Público de Comercio) but receives less public scrutiny than shareholder registers in larger SA structures. Nominee arrangements are not formally prohibited under Mexican law, though their practical use is limited by beneficial ownership disclosure obligations introduced through anti-money laundering regulations.

No. The SA and SRL each require a minimum of two shareholders or partners respectively under the LGSM. The SAS is the only structure explicitly designed for sole incorporation, permitting a single natural person to act as both founder and sole shareholder.

Foreign nationals may form an SA, SRL, SAS, or SAB, subject to foreign investment restrictions under the Ley de Inversión Extranjera. Certain sectors require majority Mexican ownership or prior authorization from the Comisión Nacional de Inversiones Extranjeras. A Branch Office or Representative Office offers an alternative for firms preferring not to incorporate a separate legal entity.

Conversion between entity types is permitted under the LGSM, provided shareholders approve the transformation by the required majority and the entity meets the legal requirements of the target structure. An SA can convert to an SRL and vice versa. The process involves amending the articles of incorporation and updating the registration with the Registro Público de Comercio.

Not uniformly. The SA, SRL, SAS, SAB, and cooperatives each hold separate legal personality from their members. General partnerships (Sociedad en Nombre Colectivo) also have legal personality under the LGSM, but partners retain unlimited joint liability for the firm's obligations, which materially changes the risk profile compared to capital-based structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.