Key Takeaways

- Saint Martin (French side) operates under French commercial law via the Code de commerce, with company registration handled by the Greffe du Tribunal Mixte de Commerce de Basse-Terre.

- The SAS has become the most widely registered entity in Saint Martin MF due to its contractual flexibility and minimal shareholder requirements.

- Despite alignment with French regulatory standards, Saint Martin sits outside the EU's fiscal territory and maintains its own VAT regime, creating distinct tax compliance obligations.

- Partnerships such as the Société en Nom Collectif (SNC) expose partners to unlimited personal liability, making them suitable only for specific professional or family arrangements rather than general commercial use.

Introduction to Entity Types in Saint Martin (MF)

Saint Martin (French side) is a French collectivity located in the northeastern Caribbean, sharing the island of Saint Martin with the Dutch territory of Sint Maarten. Governed under the Collectivité de Saint-Martin, the territory operates as an overseas collectivity of France following its separation from Guadeloupe in 2007. Business entity types Saint Martin MF fall under French commercial law, primarily the Code de commerce, with company registration administered through the Greffe du Tribunal Mixte de Commerce de Basse-Terre, which handles filings for entities operating in the collectivity.

The territory has a distinct tax status — it sits outside the European Union's fiscal territory and maintains its own VAT regime, making it structurally different from metropolitan France for tax purposes.

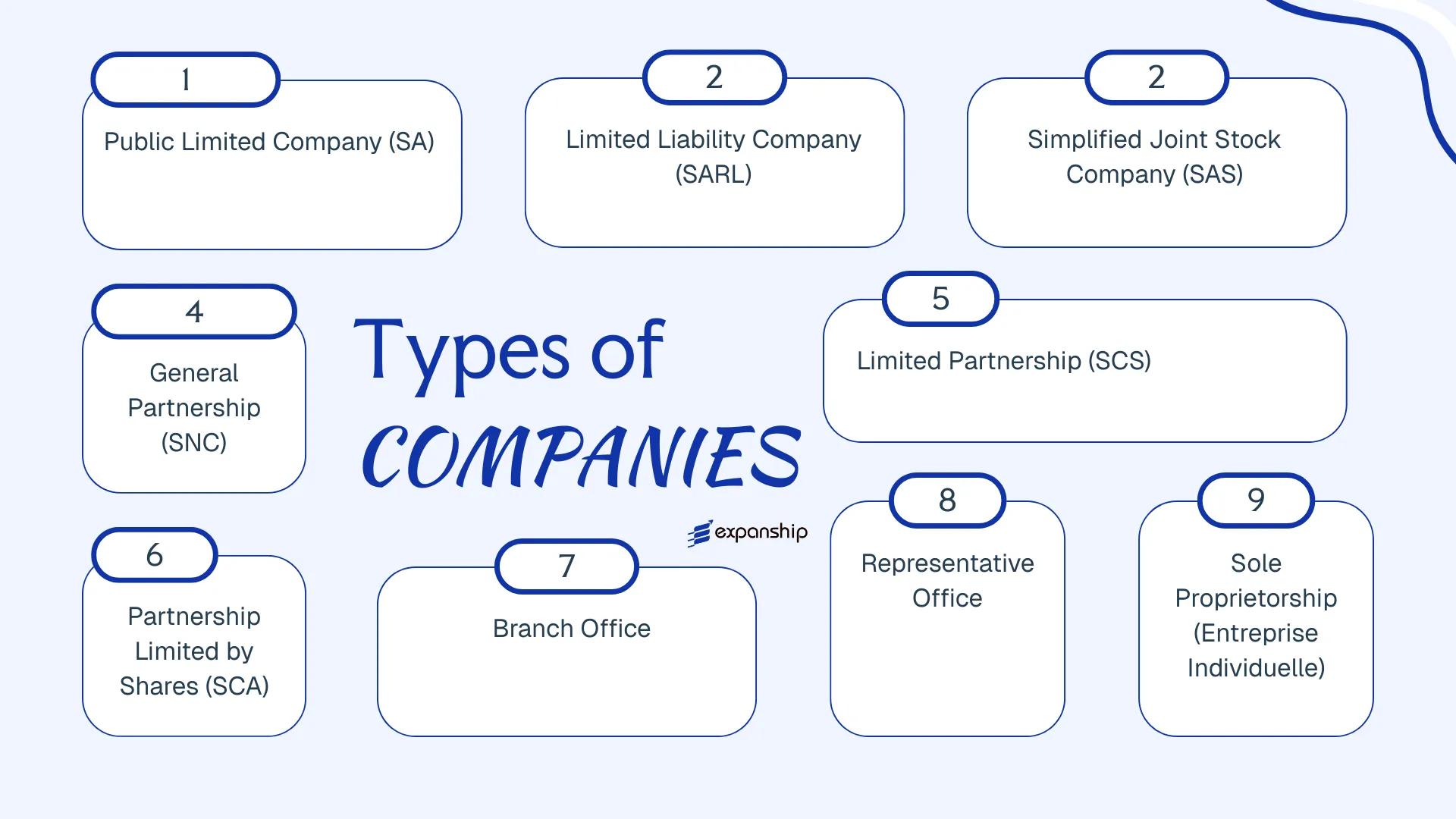

Businesses establishing a presence here may choose from several corporate forms: the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société par Actions Simplifiée (SAS), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, and the Entreprise Individuelle. Each structure carries distinct implications for liability, governance, and taxation, all of which are examined in the sections that follow.

An Overview of Business Structures in Saint Martin (MF)

Saint Martin (French side) recognises several distinct business structures under the French legal framework that applies to the collectivity. As a territorial collectivity of France, the jurisdiction follows the French Commercial Code (Code de Commerce) as its primary governing legislation, supplemented by applicable French company law statutes. Each structure carries different implications for liability, governance, and taxation, and suits different operational profiles.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Corporation | Limited | Taxable | Yes | 2 shareholders | Greffe du Tribunal | Code de Commerce |

| SARL | LLC equivalent | Limited | Taxable (IS/IR) | Yes | 1 member | Greffe du Tribunal | Code de Commerce |

| SAS | Simplified corp. | Limited | Taxable (IS) | Yes | 1 shareholder | Greffe du Tribunal | Code de Commerce |

| SNC | General partnership | Unlimited | Transparent (IR) | Yes | 2 partners | Greffe du Tribunal | Code de Commerce |

| SCS | Limited partnership | Mixed | Transparent (IR) | Yes | 2 partners | Greffe du Tribunal | Code de Commerce |

| SCA | Partnership/shares | Mixed | Taxable (IS) | Yes | 4 partners | Greffe du Tribunal | Code de Commerce |

| Branch Office | Non-legal entity | Parent liable | Taxable | Yes | N/A | Greffe du Tribunal | Code de Commerce |

| Representative Office | Non-legal entity | Parent liable | Generally exempt | Restricted | N/A | Greffe du Tribunal | Code de Commerce |

| Entreprise Individuelle | Sole proprietorship | Unlimited* | Taxable (IR) | Yes | 1 person | Greffe du Tribunal | Code de Commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme (SA) in Saint Martin MF operates under French commercial law — specifically the provisions of the Code de commerce — as the territory applies French metropolitan legislation by default. It carries full separate legal personality, meaning the entity holds rights and obligations independently of its shareholders, whose liability is confined to their capital contributions.

Structured as a joint stock company, the SA divides its capital into freely transferable shares, making it suited to entities that anticipate external investment or eventual public listing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Joint stock company with separate legal personality |

| Members | Shareholders (minimum 2, no maximum for private SA) | Directors: minimum 3, maximum 18 (Board of Directors model) |

| Capital | EUR 37,000 minimum; at least 50% paid up at incorporation | Remainder due within 5 years |

| Local Presence | Registered office required in Saint Martin (MF) | No mandatory local director under French law |

| Transferability | Shares freely transferable by default | Articles may impose restrictions |

| Privacy | Shareholder details filed with the registrar | Beneficial ownership disclosed under EU AML directives applied locally |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard rate; VAT applies under French rules; withholding taxes on dividends follow French domestic rates, subject to applicable tax treaties.

- Annual Compliance: Statutory auditor (commissaire aux comptes) mandatory; annual accounts must be filed with the Registre du Commerce et des Sociétés (RCS).

- Economic Substance: No separate OECD-style substance regime distinct from French metropolitan obligations applies, though operational reality may affect tax residency determinations.

- Treaty Access: As a French collectivity, treaty access depends on the scope of individual conventions; France's broad tax treaty network may extend, but treaty applicability to Saint Martin requires case-by-case verification.

- Conversion: An SA may be converted into an SAS or SARL by shareholder resolution, subject to meeting the target form's requirements.

Closing

The SA suits larger commercial operations, holding structures with multiple institutional investors, or businesses planning a capital-raising path. Its principal advantage is unrestricted share transferability; the principal constraint is governance formality — mandatory board composition rules and a statutory auditor requirement impose ongoing administrative cost.

Best suited for businesses with multiple institutional shareholders, significant capitalisation needs, or a mid-to-long-term path toward structured investment rounds.

Company Incorporation in Saint Martin (MF)

Incorporate an SA or other entity type in Saint Martin (MF) with Expanship's end-to-end corporate services.

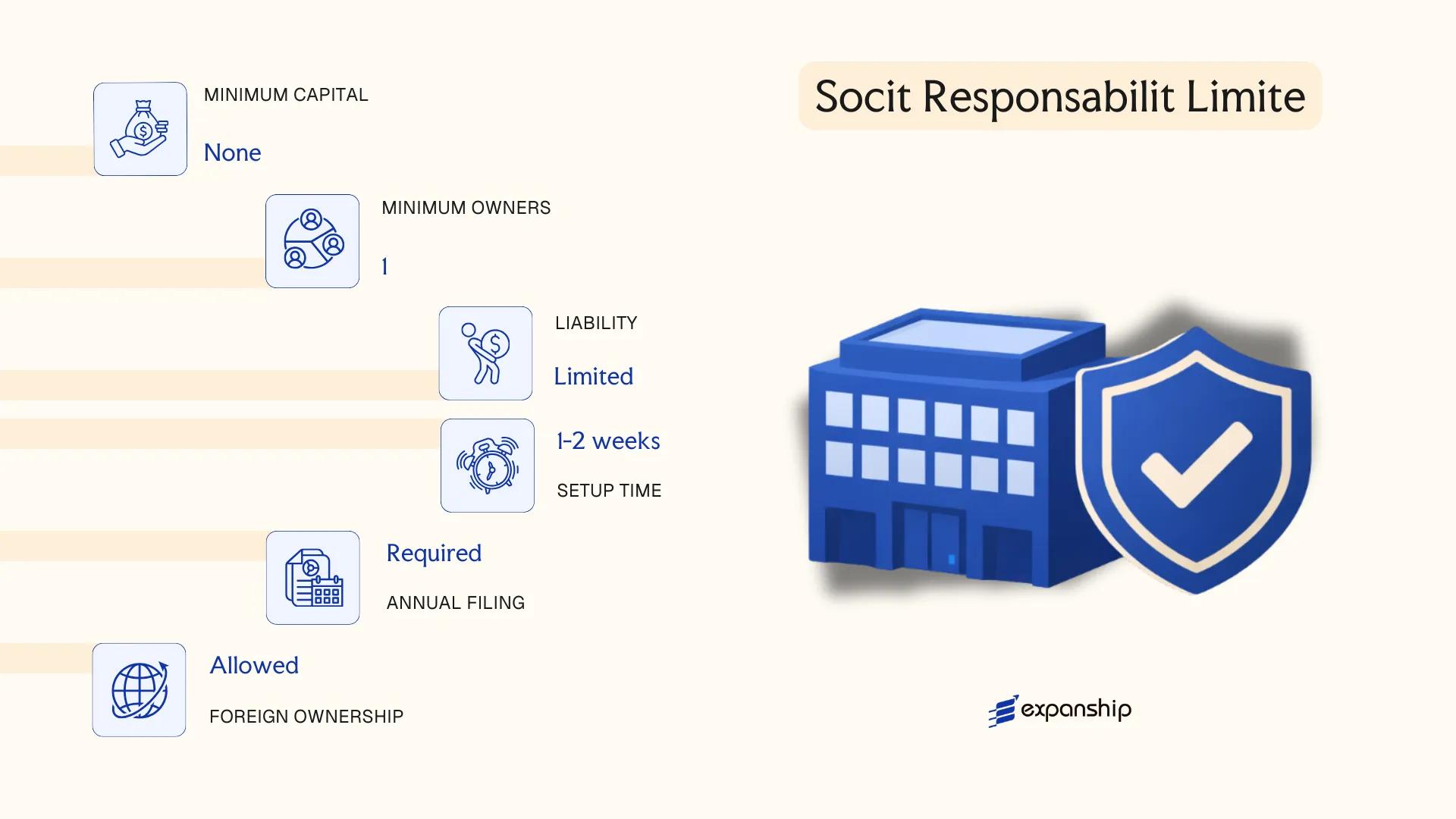

Société à Responsabilité Limitée (SARL)

SARL registration Saint Martin MF follows the French commercial code framework, specifically the provisions of the Code de Commerce, as adapted and applied in Saint Martin's French collectivity. The SARL carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its members.

Liability is capped at each member's capital contribution. This structure sits between a sole proprietorship and a full public company, making it a common choice for closely held businesses with a defined ownership group.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée | Separate legal personality; members' liability limited to contributions |

| Members | 1–100 associés (shareholders) | A single-member SARL is called an EURL |

| Management | One or more gérants (managers) | Need not be a member; individuals only, not corporate managers |

| Registered Office | Physical address in Saint Martin (French side) required | Must be maintained throughout the company's life |

| Share Capital | No statutory minimum under current French law | Capital must be adequate for the stated business activity |

| Privacy | Shareholder details filed with the registrar | Beneficial ownership disclosed under French anti-money laundering rules |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at standard rates; VAT applies to taxable supplies; no separate withholding tax regime specific to the collectivity beyond French national rules.

- Annual Compliance: Annual accounts must be filed with the Registre du Commerce et des Sociétés (RCS); statutory audit required only above certain size thresholds.

- Economic Substance: No distinct substance regime separate from French national requirements applies at the collectivity level.

- Conversion: An SARL may be converted into an SAS or SA by shareholder resolution, subject to Code de Commerce procedures.

- Transfer Restrictions: Share transfers to non-members require approval from members holding a majority of the share capital.

Closing

The SARL suits trading operations, service businesses, and family-owned ventures seeking straightforward governance without the formalities of a public company. Its transfer restrictions on shares, while providing ownership stability, can limit liquidity for investors seeking an exit.

The SARL is best suited for small to medium-sized businesses with a limited, stable group of shareholders who intend to manage the company directly.

Société par Actions Simplifiée (SAS)

Governed by French commercial law as adapted and applied within the Saint-Martin collectivity, the SAS company Saint Martin MF operates under the same foundational framework as its metropolitan French counterpart, principally structured under the provisions of the Code de Commerce. The entity holds a distinct legal personality, separate from its shareholders, with liability confined to the amount of capital contributed.

Flexibility is the defining characteristic of this structure. An SAS incorporation Saint Martin collectivity allows founders to draft bylaws that tailor governance, share transfer conditions, and decision-making procedures to the specific operational requirements of the business, making it a common choice for joint ventures and investor-backed entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Separate legal personality; limited liability |

| Members | Shareholders (associés) | Minimum 1 (SASU variant); no statutory maximum |

| Governance | President (Président) mandatory | Additional management bodies are optional and defined by bylaws |

| Local Presence | Registered office in Saint-Martin | No statutory requirement for a local director |

| Share Capital | No minimum capital requirement | Must be stated in the articles; contributions can be in cash or kind |

| Privacy | Shareholder identity disclosed at registration | Beneficial ownership subject to French transparency rules |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at standard rates; VAT applies under French rules; no separate local corporate tax regime; dividends may attract withholding tax depending on recipient jurisdiction.

- Annual Compliance: Annual accounts must be filed; statutory audit required once the entity exceeds two of three statutory thresholds (turnover, balance sheet, headcount).

- Economic Substance: No specific economic substance regime distinct from French law obligations applies; standard French rules on tax residency and management control govern.

- Treaty Access: Access to France's extensive tax treaty network, which covers over 120 jurisdictions, is available where treaty conditions are satisfied.

- Conversion: Can be converted into an SA or SARL by shareholder resolution, subject to Code de Commerce procedures.

Sub-Types

Société par Actions Simplifiée Unipersonnelle (SASU)

The SASU is a single-shareholder variant of the SAS, structurally identical but permitting sole ownership without requiring additional associates. It is commonly used by individual entrepreneurs or parent companies establishing a wholly owned subsidiary.

Closing

The simplified joint stock company Saint Martin MF suits holding structures, joint ventures, and technology or IP-holding entities where governance flexibility and investor-friendly share transfer provisions carry practical weight. The absence of a minimum capital requirement lowers the initial formation barrier, though the obligation to maintain formal accounts and comply with French statutory audit thresholds adds an ongoing administrative burden.

The SAS is most appropriate for multi-investor ventures and structured holdings where bespoke shareholder arrangements and scalable governance are a priority.

Partnerships in Saint Martin (MF) [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Partnerships in Saint Martin (MF) — covering the SNC, SCS, and SCA structures — are governed by French commercial law as extended to the collectivity, principally through the French Code de Commerce. Each form carries distinct liability profiles: the Société en Nom Collectif assigns unlimited joint and several liability to all partners, while the commandite structures introduce a separation between general and limited partners.

Registration is handled through the Centre de Formalités des Entreprises (CFE), and these entities acquire separate legal personality upon registration in the Registre du Commerce et des Sociétés (RCS).

Key Characteristics

| Requirement | SNC | SCS / SCA | Notes |

|---|---|---|---|

| Legal Form | General partnership | Limited partnerships | SCA combines partnership and share-based structure |

| Members | Associés (partners) | Gérants (general) + Commanditaires (limited) | SNC: min. 2 partners, no maximum; SCS: min. 1 of each class; SCA: min. 1 general + 3 limited |

| Liability | Unlimited for all | Unlimited (general); limited to contribution (limited) | SNC partners bear personal liability for company debts |

| Capital | No statutory minimum (EUR) | SCA: EUR 37,000 minimum | SCS has no minimum capital requirement |

| Local Presence | Registered office in Saint Martin required | Same | No mandatory local director requirement under current rules |

| Privacy | Partners listed in RCS | General partners listed; limited partners may have reduced disclosure | RCS filings are publicly accessible |

Focus Points

- Taxation: Partnerships are generally fiscally transparent under French tax principles; profits flow through to partners and are taxed at the individual or corporate level depending on partner status, with no separate corporate income tax at entity level unless an election is made; VAT, local business tax (cotisation foncière des entreprises), and applicable withholding taxes on distributions to non-resident partners apply.

- Economic Substance: No specific economic substance regime applies distinct from standard French collectivity rules; however, genuine activity must support the entity's registered purpose.

- Annual Compliance: Annual accounts must be filed with the RCS; SCA entities face additional obligations aligned with société anonyme reporting requirements given their share-based capital structure.

- Conversion: An SNC may be converted to an SARL or SAS subject to unanimous partner consent and compliance with the applicable capital and governance requirements of the target form.

- Restrictions: SNC partners cannot transfer their interests without unanimous consent of all other partners, making exit or ownership restructuring operationally constrained.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is the base general partnership form, in which every associé holds unlimited personal liability. It is used primarily for family-owned businesses or professional firms where partners prefer pass-through taxation and accept shared liability.

Société en Commandite Simple (SCS)

The SCS introduces a two-class partner structure without issuing transferable shares. Limited partners contribute capital and bear risk only to the extent of their contribution, while general partners manage and assume unlimited liability.

Société en Commandite par Actions (SCA)

The SCA issues shares to limited partners, enabling broader capital-raising capacity. General partners retain management control, making this structure suited to investment vehicles or family holding groups where founders wish to maintain control while accepting outside equity investors.

Partnerships suit closely held trading or holding arrangements where the partners prefer fiscal transparency over the administrative burden of a share-based structure. The pass-through tax treatment is a functional advantage; the unlimited liability exposure of general partners remains the principal structural constraint.

SNC and SCS structures are best suited to small groups of known partners operating a defined business activity together, where personal accountability among founders is commercially acceptable.

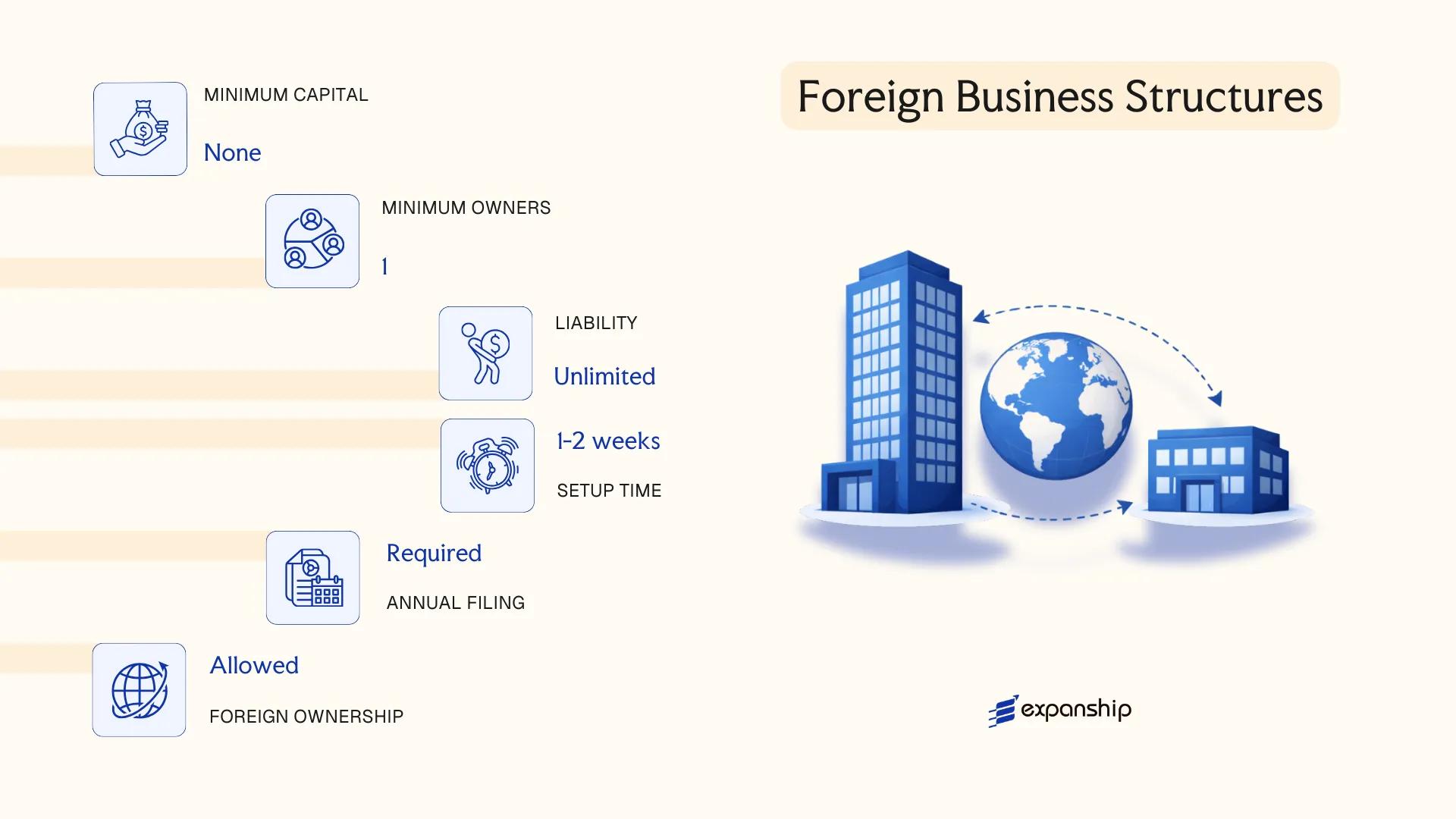

Foreign Business Structures in Saint Martin (MF) [Branch Office, Representative Office]

Establishing a foreign branch office in Saint Martin MF is governed by French commercial law, specifically the Code de Commerce, which applies through the collectivity's legal framework as a French overseas territory. A branch office (succursale) has no separate legal personality — it remains an extension of the parent company, which bears full liability for the branch's obligations.

A representative office (bureau de représentation) operates under similar principles but with a narrower commercial scope. Neither structure constitutes an independent legal entity, which distinguishes them from locally incorporated forms such as the SARL or SAS.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted; limited to liaison, market research |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Local Registration | Required with the Registre du Commerce et des Sociétés (RCS) | Required; lighter formalities than branch |

| Local Presence | Registered address required | Registered address required |

| Capital Requirement | None specific; parent's capital governs | None |

Focus Points

- Taxation: Branch profits are subject to French corporate tax rules applicable in the collectivity; VAT obligations depend on the nature of transactions conducted.

- Economic Substance: No separate substance regime applies; the parent entity's home jurisdiction obligations remain relevant.

- Annual Compliance: Annual accounts of the parent must be filed with local commercial registry authorities.

- Treaty Access: Access to France's tax treaty network may be available depending on the parent's residence and structure.

- Restrictions: A representative office cannot generate revenue or enter commercial contracts directly.

Sub-Types

Branch Office (Succursale)

A succursale can conduct full trading operations and enter binding contracts on behalf of the parent, making it suitable for businesses seeking operational presence without local incorporation.

Representative Office (Bureau de Représentation)

This structure is limited to non-commercial functions such as promotional activities or coordination. It cannot invoice clients or conclude sales agreements independently.

Both structures suit foreign companies testing the local market or managing regional operations without establishing a standalone entity. The key advantage is speed and simplicity of setup; the principal limitation is the parent's unlimited exposure to liabilities incurred locally.

Foreign branch office registration in Saint Martin MF is best suited for established companies with an existing legal entity abroad that require a controlled, operational presence without the administrative overhead of full local incorporation.

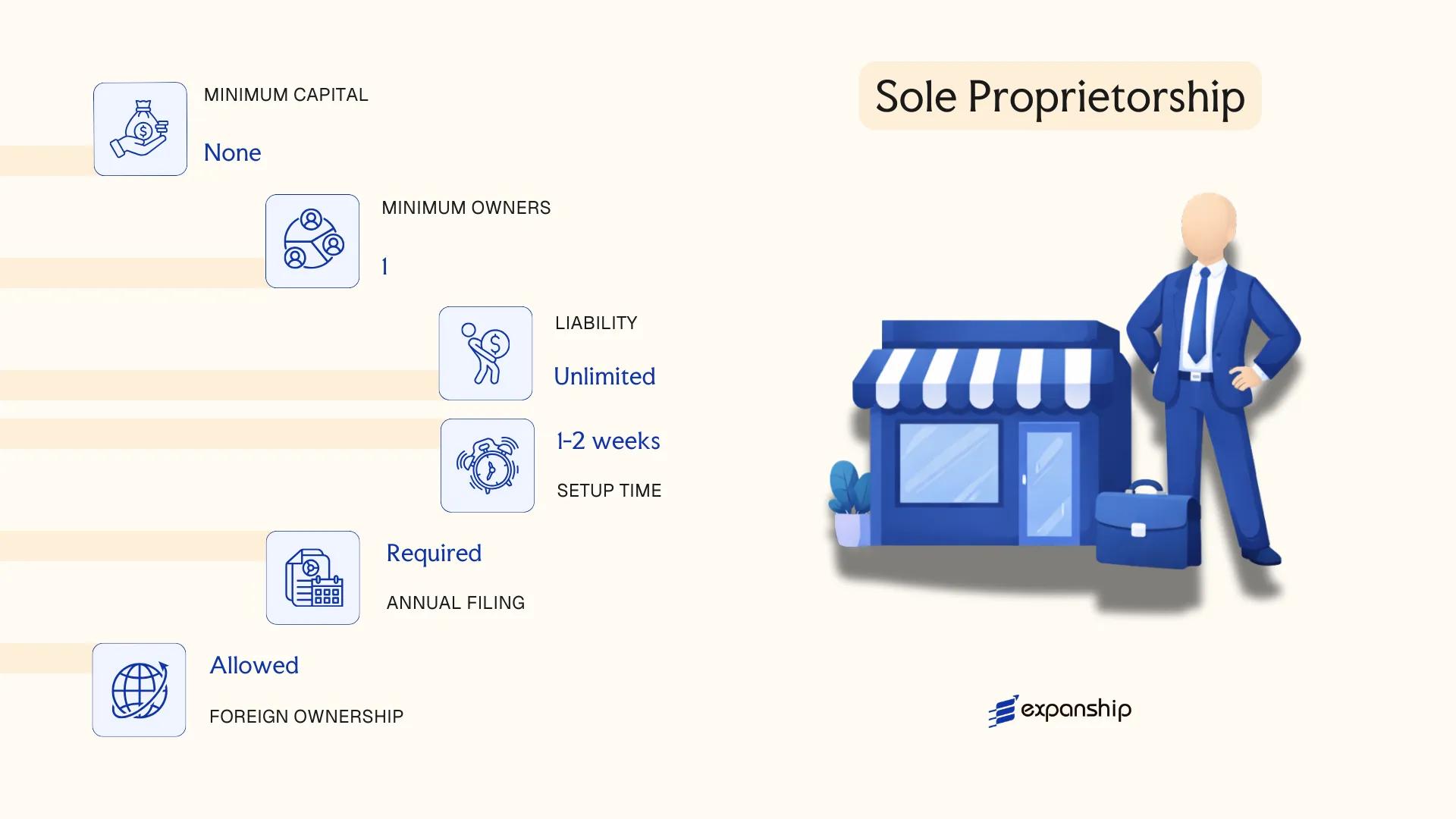

Sole Proprietorship (Entreprise Individuelle)

The Entreprise Individuelle Saint Martin MF is the simplest legal form available for individual operators. Governed by French commercial law as applied in the collectivity, it carries no separate legal personality — the proprietor and the business are legally one and the same.

Because the individual and the enterprise are legally indistinct, the proprietor bears unlimited personal liability for all business debts. Registration is handled through the Centre de Formalités des Entreprises (CFE), which routes filings to the relevant registries including the Registre du Commerce et des Sociétés (RCS) for commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship; no separate legal personality | Proprietor and business are legally unified |

| Members | Single proprietor | No shareholders, directors, or partners; one individual only |

| Local Presence | Registered business address required | Must correspond to the principal place of activity |

| Capital | No minimum capital requirement | No paid-up capital formality at incorporation |

| Liability | Unlimited personal liability | Personal assets exposed to business creditors |

| Privacy | Proprietor's name publicly associated with the firm | No separation between personal and business identity in records |

Focus Points

- Taxation: Subject to French income tax (impôt sur le revenu) on business profits; VAT registration required once turnover thresholds are exceeded; no corporate tax applies at this level.

- Social contributions: The proprietor pays social security contributions (cotisations sociales) as a self-employed individual, calculated on net professional income.

- Annual compliance: Annual income declaration required; no separate corporate accounts filing, though accounting records must be maintained.

- Conversion: Can be converted into a corporate form such as an EURL or SASU without dissolving operations, subject to standard French procedural requirements.

- Restrictions: Certain regulated professions are excluded from this form and require specific professional registration or licensing.

Closing

The Entreprise Individuelle suits freelancers, tradespeople, and small-scale service operators who require minimal administrative overhead. Its primary advantage is the absence of capital requirements and simplified registration; the corresponding drawback is full personal exposure to business liabilities.

Best suited for resident individuals conducting low-risk, single-person commercial or artisanal activities with limited third-party financial exposure.

How to Choose the Right Entity Type in Saint Martin (MF)

Choosing the right company structure in Saint Martin MF is not a procedural formality — the structure you register determines your tax exposure, liability framework, reporting obligations, and operational capacity from day one.

Why Your Entity Choice Matters

- Registering a structure intended for passive holding and then conducting active local trade can constitute a breach of applicable French commercial law, exposing the business to administrative penalties or involuntary dissolution.

- Selecting an entity that falls outside France's tax treaty network means your business cannot claim withholding tax reductions on dividends, royalties, or interest paid to counterpart jurisdictions.

- Forming a multi-shareholder company when your activity is a single-person consultancy imposes ongoing general meeting, minutes, and potential audit obligations that do not apply to an Entreprise Individuelle.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structures under French commercial law as extended to the collectivity.

- Ownership and Management: A sole operator has no practical need for a board structure, while multi-party ventures with investor relationships require the governance mechanisms of an SA or SAS.

- Tax Objectives: Your eligibility for specific French fiscal regimes — including the micro-entreprise threshold or standard corporate tax — depends directly on which legal form you register.

- Liability Exposure: Unlimited personal liability under an SNC or Entreprise Individuelle is structurally incompatible with high-risk commercial activity.

- Substance Capacity: If you cannot maintain genuine local decision-making, certain structures will attract greater regulatory scrutiny under French anti-avoidance provisions.

- Exit Strategy: Not all structures permit redomiciliation or conversion without dissolution; confirm this before formation.

The full text of the French Code de Commerce, which governs the commercial entities available in Saint Martin MF, is published on Légifrance.

Compliance Services for Companies in Saint Martin (MF)

Maintain your entity's good standing with ongoing compliance support tailored to French commercial law requirements applicable in Saint Martin.

Conclusion

Saint Martin MF company incorporation summary points to a jurisdiction governed by French commercial law, where the choice of entity shapes tax exposure, liability, and operational structure in substantive ways. The SAS has emerged as the most commonly registered vehicle, favored for its contractual flexibility and minimal shareholder requirements. The SA suits larger enterprises requiring formal governance boards, while the SARL remains practical for closely held businesses with defined ownership. Partnerships such as the SNC carry unlimited liability and serve specific professional or family arrangements. Branch and representative offices give foreign firms a controlled presence without establishing a separate legal person.

As a French collectivity, Saint Martin continues to align with mainland French regulatory standards, and its position within the EU VAT and customs framework shapes the compliance obligations your business will carry from the outset. Expanship's team works directly within this regulatory environment.

How Expanship Can Assist You

Expanship company formation Saint Martin MF services are built around the specific legal framework that governs this French collectivity — from registering an SARL or SAS with the Greffe du Tribunal Mixte de Commerce to meeting post-incorporation obligations under French corporate law as applied locally. Each engagement is handled with the regulatory structure of the collectivity in mind, not treated as a generic French territory filing.

Across the full incorporation and compliance cycle, our team supports your business at every stage:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision in Saint Martin

- Government filing and liaison with the Greffe du Tribunal Mixte de Commerce

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for newly incorporated entities

Get in touch with Expanship Saint Martin to discuss the right structure for your business.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered structure on the French side. Its combination of limited liability, a single-member option, and relatively straightforward compliance requirements makes it practical for small to medium-sized businesses.

An SA requires a minimum of seven shareholders and a higher share capital threshold, whereas a SARL can be formed by a single associé. For ongoing compliance, the SA carries heavier disclosure and governance obligations, including mandatory statutory auditors once certain thresholds are met.

The Société par Actions Simplifiée (SAS) affords comparatively more flexibility in governance documentation, though French-side transparency rules still require beneficial ownership registration. Nominee arrangements are available in principle but do not exempt a business from declarations under French anti-money laundering directives applicable in the collectivity.

A SARL and an EURL (single-member SARL variant) can be established by one person. Partnerships such as the Société en Nom Collectif require at least two associés, and the Société en Commandite par Actions mandates both general and limited partners, making sole formation structurally impossible for those forms.

Non-residents may form a SARL, SAS, or SA on the French side without nationality restrictions under applicable French commercial law. A foreign firm may also establish a branch (succursale) registered with the relevant Registre du Commerce et des Sociétés, though the parent company retains full legal liability for that branch's obligations.

French commercial law, which governs Saint Martin's French collectivity, permits transformation between certain entity forms, including SARL to SAS, subject to shareholder approval and notarial procedures. Not all conversions are available in every direction; transformation into an SA, for example, requires meeting applicable capital and shareholder minimums before the change takes effect.

The SA, SARL, and SAS each hold distinct legal personality separate from their shareholders. General partnerships under a Société en Nom Collectif also possess legal personality, but partners bear joint and unlimited liability for the firm's debts, which is a substantive distinction from the capital-based structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.