Key Takeaways

- The private company limited by shares is the most widely used entity under the Companies Ordinance (Cap. 622) and accommodates the broadest range of commercial purposes in Hong Kong.

- Hong Kong's Companies Registry administers all corporate registrations, while the Inland Revenue Department applies taxation on a territorial basis, meaning only Hong Kong-sourced profits are taxable.

- Branch offices expose the foreign parent entity to direct legal liability, whereas representative offices are legally prohibited from generating revenue.

- General partnerships and limited partnerships differ fundamentally in liability exposure, with limited partnerships providing statutory liability protection unavailable under a general partnership structure.

Introduction to Entity Types in Hong Kong

Hong Kong is a Special Administrative Region (SAR) of China, situated on the southeastern coast of the Pearl River Delta, bordered by Guangdong Province to the north and the South China Sea to the south. Under the "one country, two systems" framework, it maintains a distinct legal system based on English common law, separate from mainland China's legal order.

Company registration and ongoing compliance fall under the jurisdiction of the Companies Registry, which administers the Companies Ordinance (Cap. 622) — the primary legislation governing corporate entities. The Inland Revenue Department administers taxation under a territorial basis, meaning only profits sourced within the SAR are subject to tax.

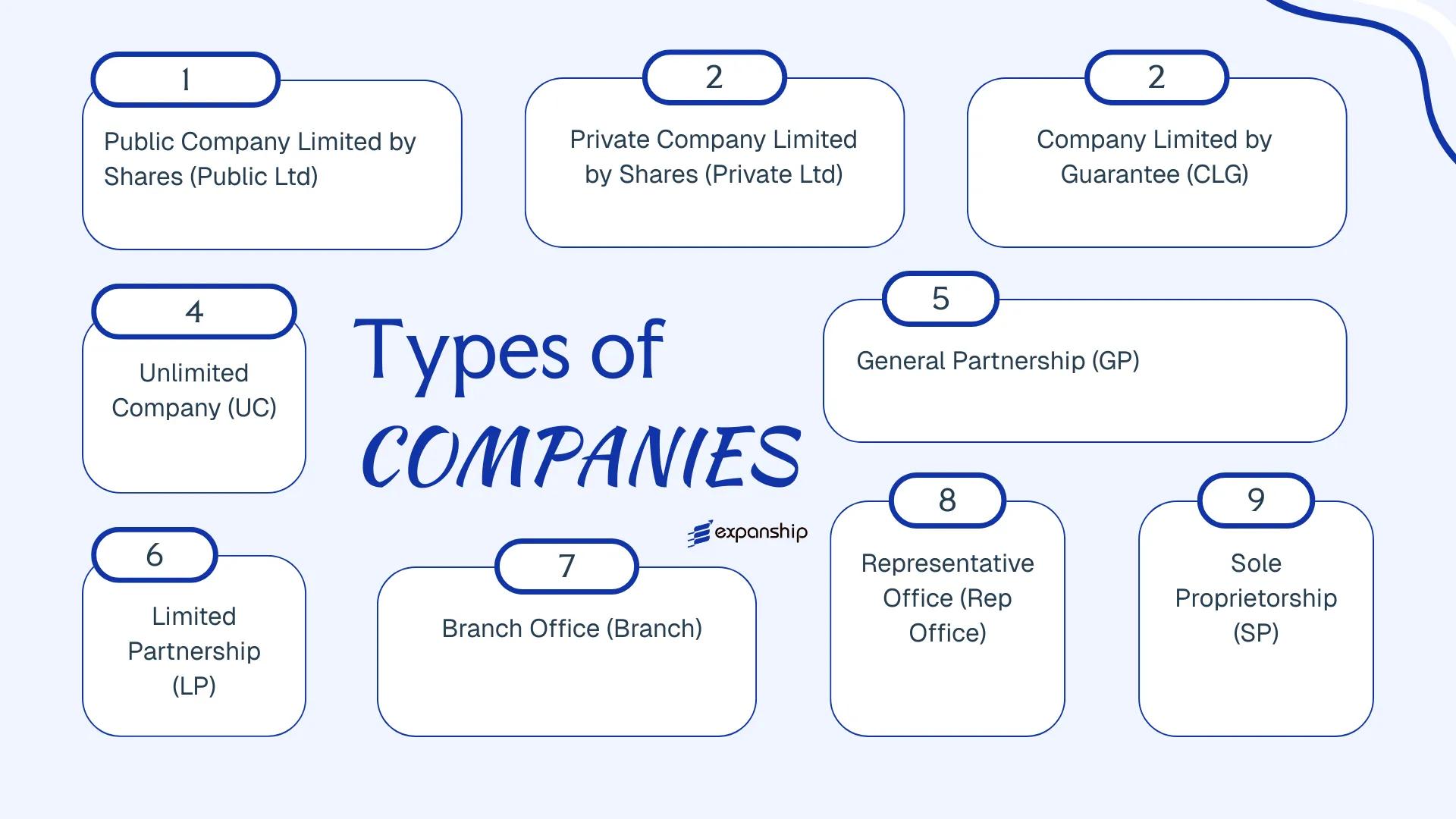

Several types of business entities in Hong Kong are available to both residents and foreign founders. These include the Private Company Limited by Shares, Public Company Limited by Shares, Company Limited by Guarantee, Unlimited Company, General Partnership, Limited Partnership, Branch Office, Representative Office, and Sole Proprietorship.

Each structure carries distinct implications for liability, governance, and tax treatment. This article examines each option across those dimensions to help you determine which Hong Kong legal entity structure suits your business objectives.

An Overview of Business Structures in Hong Kong

Under the Companies Ordinance (Cap. 622), which came into force in March 2014, six distinct entity types are available to those forming a company in the territory. Beyond incorporated entities, the legal framework also accommodates partnerships and foreign business presence structures, giving businesses a total of nine formation options across different regulatory regimes. Each structure carries different implications for liability, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Private Company Limited by Shares | Incorporated | Limited to shares | Taxed | Permitted | 1 shareholder | Companies Registry | Companies Ordinance (Cap. 622) |

| Public Company Limited by Shares | Incorporated | Limited to shares | Taxed | Permitted | 1 shareholder | Companies Registry / SFC | Companies Ordinance (Cap. 622) |

| Company Limited by Guarantee | Incorporated | Limited to guarantee | Taxed / Exempt | Restricted | 1 member | Companies Registry | Companies Ordinance (Cap. 622) |

| Unlimited Company | Incorporated | Unlimited | Taxed | Permitted | 1 shareholder | Companies Registry | Companies Ordinance (Cap. 622) |

| General Partnership | Unincorporated | Unlimited | Taxed | Permitted | 2 partners | Business Registration Office | Partnership Ordinance (Cap. 38) |

| Limited Partnership | Unincorporated | Mixed | Taxed | Permitted | 2 partners | Companies Registry | Limited Partnerships Ordinance (Cap. 37) |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Permitted | N/A | Companies Registry | Companies Ordinance (Cap. 622) |

| Representative Office | Foreign entity extension | Parent liable | Generally exempt | Not permitted | N/A | InvestHK / IRD | No dedicated ordinance |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Permitted | 1 owner | Business Registration Office | Business Registration Ordinance (Cap. 310) |

Each of these structures is examined in full in the sections below.

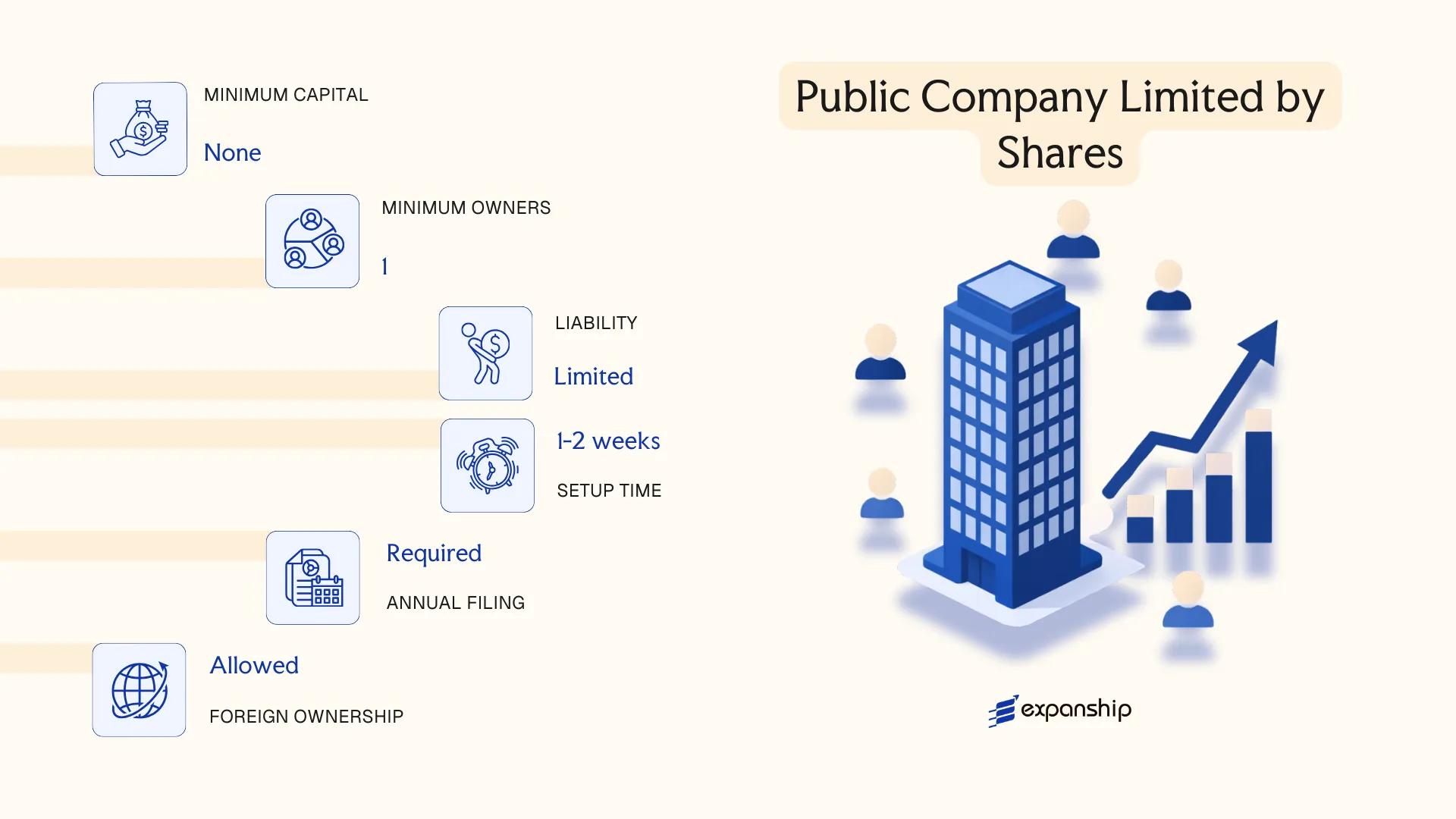

Public Company Limited by Shares

A Hong Kong public company limited by shares is governed by the Companies Ordinance (Cap. 622), which came into force in March 2014. Under this legislation, the entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the unpaid amount on their shares.

Unlike a private company, a public company may offer its shares to the general public. This structure is a prerequisite for listing on the Hong Kong Stock Exchange (HKEX), making it the standard vehicle for businesses seeking access to public capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public company limited by shares | Separate legal personality; liability capped at unpaid share value |

| Members | Shareholders; no maximum limit; minimum 1 shareholder | Shares may be offered to the public |

| Directors | Minimum 2 directors; at least 1 must be a natural person | No statutory requirement for a Hong Kong-resident director |

| Local Presence | Registered office in Hong Kong; company secretary required (individual must be HK resident or body corporate with registered office in HK) | Registered office address must be maintained at all times |

| Share Capital | Denominated in any currency; no statutory minimum paid-up capital | Share capital structure must be defined in the articles of association |

| Privacy | Director and shareholder details filed with the Companies Registry and publicly accessible | Beneficial ownership information held in a significant controllers register |

Focus Points

- Taxation: Corporate profits tax applies at 16.5% on assessable profits (8.25% on the first HKD 2 million under the two-tiered regime); no VAT, no withholding tax on dividends, and stamp duty applies to share transfers at 0.2% of consideration.

- Annual Compliance: Mandatory annual return filing with the Companies Registry, audited financial statements, and an AGM each calendar year.

- Listing Obligations: If listed on HKEX, the entity is subject to the Listing Rules administered by the Securities and Futures Commission (SFC) and HKEX, including continuous disclosure requirements.

- Conversion: A public company may be re-registered as a private company under Cap. 622, subject to shareholder approval and Companies Registry filing.

- Economic Substance: No general economic substance regime applies, though listed entities face enhanced governance expectations under SFC regulations.

Closing

This structure suits large enterprises, institutional investors, and businesses planning an IPO or requiring access to equity capital markets. The ability to raise funds publicly is a defining advantage; however, the associated regulatory burden — including SFC oversight, mandatory audits, and continuous disclosure — makes it a disproportionately complex structure for businesses not actively pursuing a public listing.

Enterprises seeking public capital through an HKEX listing or those structuring a holding vehicle with broad institutional shareholding.

Company Incorporation in Hong Kong

Incorporate a public or private company in Hong Kong with end-to-end support from Expanship.

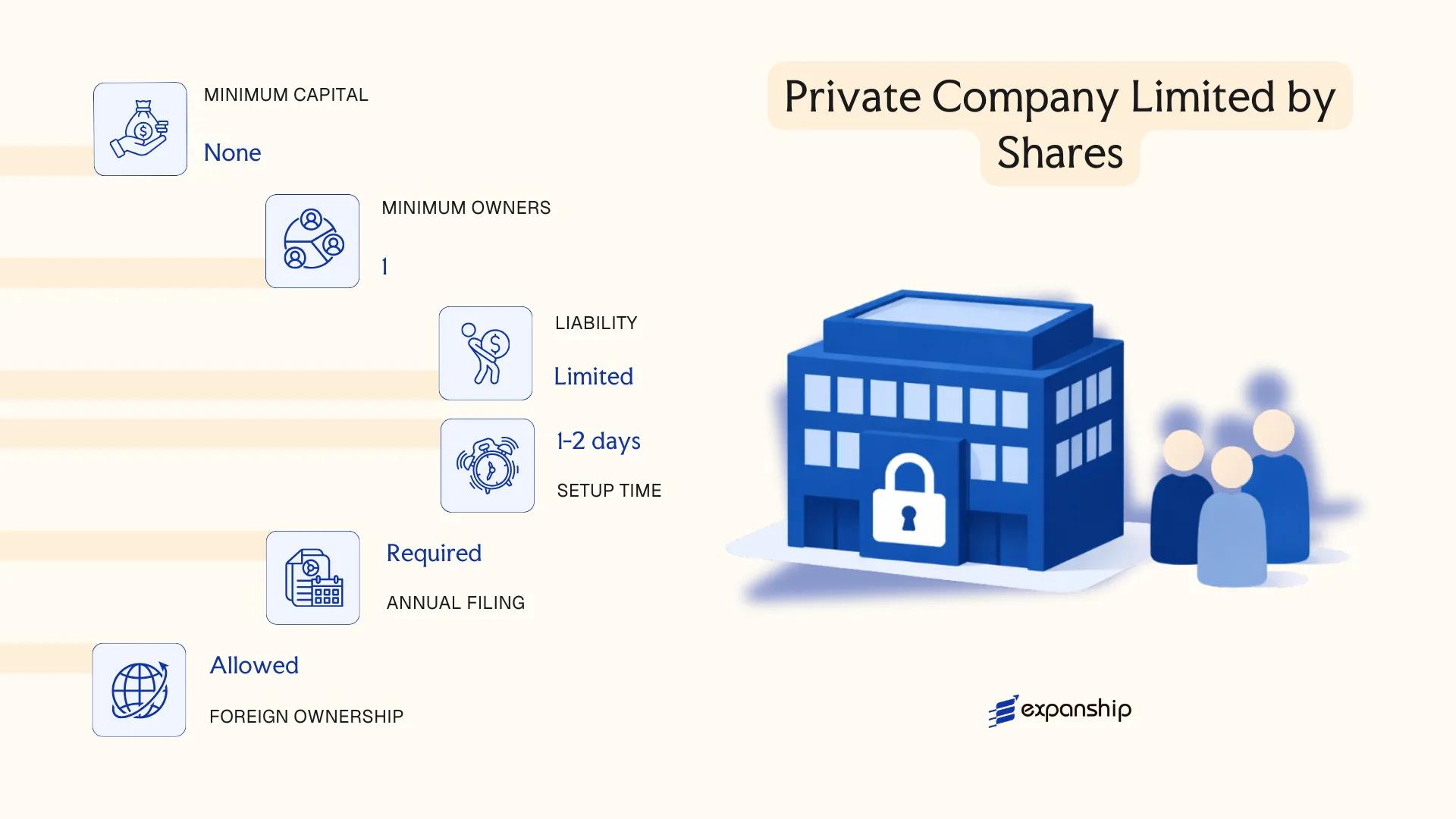

Private Company Limited by Shares

A Hong Kong private company limited by shares is the most widely used corporate structure in the territory, governed by the Companies Ordinance (Cap. 622), which came into effect in March 2014. The entity holds a separate legal personality distinct from its shareholders, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Liability exposure for shareholders is confined to the amount unpaid on their shares. This structure makes it a practical vehicle for both local operations and cross-border holding arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under Companies Ordinance (Cap. 622) |

| Members | Shareholders: min. 1, max. 50 | Excludes employees who are shareholders |

| Directors | Min. 1 natural person director | No residency requirement; corporate directors permitted alongside at least one natural person |

| Local Presence | Registered office address in Hong Kong required | Must be a physical address; P.O. Box not accepted |

| Share Capital | No minimum paid-up capital; default currency is HKD | Shares may be issued in foreign currencies |

| Privacy | Shareholder and director details filed with Companies Registry | Beneficial ownership recorded in internal register; not publicly searchable |

Focus Points

- Taxation: Profits tax applies at 8.25% on the first HKD 2 million of assessable profits and 16.5% thereafter; no VAT or GST; dividends are not subject to withholding tax; stamp duty applies on share transfers at 0.26% of consideration or value (0.13% per party).

- Annual Compliance: Must file an annual return with the Companies Registry and hold an Annual General Meeting (AGM), though private companies may dispense with the AGM by unanimous written resolution.

- Economic Substance: No standalone economic substance legislation equivalent to some offshore jurisdictions, but tax residency and the territorial source principle require genuine nexus for profits tax exemption claims on offshore income.

- Treaty Access: Eligible for Hong Kong's network of Comprehensive Double Taxation Agreements (CDTAs), subject to beneficial ownership and substance conditions.

- Conversion: A private company may re-register as a public company under Cap. 622 by special resolution and by meeting the relevant requirements for public companies.

Closing

Private companies limited by shares are commonly used for trading, regional holding structures, IP ownership, and family business operations, with the territorial tax system serving as a key structural advantage. The restriction to a maximum of 50 shareholders, however, limits scalability for businesses that may eventually require broader equity participation or public capital-raising.

This structure suits entrepreneurs, SMEs, and multinational subsidiaries seeking a straightforward incorporated presence with liability protection and access to Hong Kong's tax treaty network.

Company Limited by Guarantee

A company limited by guarantee Hong Kong structures differs from share-based entities in that it has no share capital and no shareholders. Governed by the Companies Ordinance (Cap. 622), the entity carries separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name. Members are not shareholders; instead, each member undertakes to contribute a defined sum to the entity's assets if it is wound up.

This structure is the standard vehicle for non-profit organisations, trade associations, professional bodies, and charities operating in the jurisdiction. Because it cannot distribute profits to members, it is not suited to commercial ventures seeking a return on investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated body with separate legal personality | Registered under Companies Ordinance (Cap. 622) |

| Members | Minimum 1; no statutory maximum | Members are guarantors, not shareholders |

| Guarantee Amount | Defined in the articles; typically HKD 1 per member | Payable only upon winding up |

| Local Presence | Registered office address in Hong Kong required | Must be a physical address, not a PO Box |

| Share Capital | None | Profits, if any, must be retained and applied to the entity's objects |

| Privacy | Directors and members listed on public register at Companies Registry | Beneficial ownership disclosure obligations apply |

Focus Points

- Taxation: Exempt from profits tax if registered as a charity under the Inland Revenue Ordinance (s.88); otherwise, surplus income derived from trade may be taxable at the standard corporate rate of 16.5%.

- Annual Compliance: Annual return filing with the Companies Registry and audited accounts are required; charities must also satisfy the Inland Revenue Department of ongoing qualifying activities.

- Economic Substance: No substance requirements apply, as this structure does not generate passive income in the conventional sense.

- Conversion: A CLG registration in Hong Kong cannot be converted to a company limited by shares under Cap. 622 without dissolution and re-incorporation.

- Restrictions: Distribution of profits or assets to members during the entity's lifetime is prohibited by statute.

Closing

The guarantee company Hong Kong framework is used almost exclusively for non-commercial purposes: registered charities, industry associations, educational bodies, and social enterprises. The principal advantage is potential profits tax exemption under s.88; the primary limitation is the absolute prohibition on profit distribution, which makes the structure unsuitable for any income-generating business with investors expecting returns.

This entity type is best suited for non-profit organisations, charities, and membership associations that require legal personality but have no intention of distributing profits.

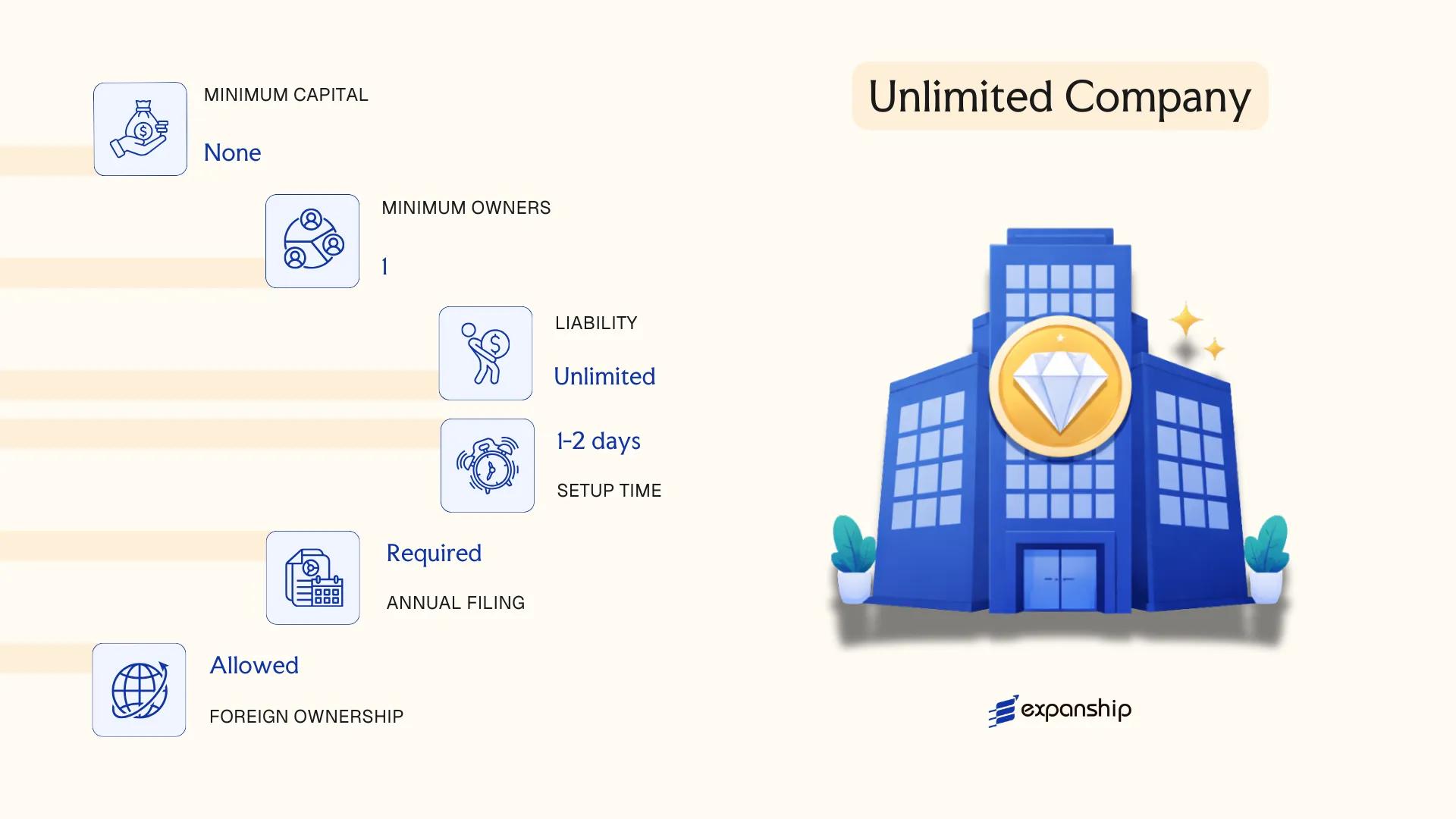

Unlimited Company

Unlimited company Hong Kong registration is governed by the Companies Ordinance (Cap. 622), the same legislation that regulates other locally incorporated entities. Unlike a company limited by shares or by guarantee, an unlimited company carries no ceiling on member liability — shareholders are personally liable for all debts and obligations of the firm if it is wound up with insufficient assets.

Separate legal personality still applies, meaning the entity exists as a distinct legal person capable of entering contracts, holding property, and suing in its own name. The absence of limited liability is therefore not a structural defect but a deliberate feature that makes this structure rare in commercial practice, typically chosen only where confidentiality over filed accounts carries more weight than liability protection.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company (private or public) | Incorporated under Companies Ordinance (Cap. 622) |

| Members | Shareholders; minimum 1, no statutory maximum | Private unlimited companies require at least 1 shareholder |

| Directors | Minimum 1 natural person; no residency requirement | Corporate directors permitted alongside natural persons |

| Local Presence | Registered office address in Hong Kong required | Must be a physical address; P.O. Box not accepted |

| Capital | No minimum share capital; HKD is standard | Shares can be denominated in any currency |

| Financial Disclosure | Exempt from filing annual financial statements with the Companies Registry | This is the primary reason firms choose this structure |

Focus Points

- Taxation: Subject to Hong Kong's territorial profits tax at 8.25% on the first HKD 2 million of assessable profits and 16.5% thereafter; no VAT, no capital gains tax, and withholding tax applies only to royalties paid to non-residents at up to 16.5%.

- Annual Compliance: Must file an annual return with the Companies Registry and hold an annual general meeting; audit requirements apply, though financial statements are not publicly filed.

- Conversion: An unlimited company may be re-registered as a company limited by shares under Cap. 622, allowing businesses to adopt limited liability if circumstances change.

- Treaty Access: Qualifies as a Hong Kong resident entity and may access Hong Kong's network of over 45 comprehensive double tax agreements, subject to substance requirements.

- Restrictions: No public offering of shares is permitted for private unlimited companies; the structure is unsuitable for businesses requiring investor confidence tied to capped liability.

Closing Paragraph

Unlimited companies are most commonly used by professional firms or subsidiaries of foreign groups where the parent accepts unlimited exposure and values the exemption from public financial disclosure. The filing exemption is the single clearest advantage; the absence of liability protection remains the structural drawback that limits adoption.

This structure suits wholly-owned subsidiaries of foreign corporations seeking confidentiality over financial accounts, where the parent entity is prepared to bear unlimited liability exposure.

Partnerships [General Partnership, Limited Partnership]

Partnerships in Hong Kong are governed by two separate statutes: the Partnership Ordinance (Cap. 38) for general partnerships, and the Limited Partnerships Ordinance (Cap. 37) for limited partnerships. Neither structure carries separate legal personality, meaning partners bear direct exposure to the firm's obligations. Hong Kong limited partnership registration is handled through the Inland Revenue Department, while general partnerships operate without mandatory registration, though Business Registration under the Business Registration Ordinance (Cap. 310) remains obligatory for both.

A limited partnership must have at least one general partner with unlimited liability and at least one limited partner whose liability is capped at their capital contribution. Unlike a general partnership, the limited structure requires formal filing with the Registrar of Companies to take legal effect.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Personality | None | None |

| Members | Partners (min. 2, max. 20 for most businesses) | General partners (min. 1) + Limited partners (min. 1); max. 20 total |

| Liability | Unlimited for all partners | Unlimited for general partners; capped for limited partners |

| Registration | Business Registration only (IRD) | Filed with Registrar of Companies + Business Registration |

| Local Presence | Registered address in Hong Kong required | Registered address in Hong Kong required |

| Capital | No statutory minimum; HKD contributions | No statutory minimum; limited partner's liability capped at contribution |

Focus Points

- Taxation: Partnerships are taxed at the partner level under profits tax (currently 15% for individuals); no corporate profits tax applies at the entity level, and there is no VAT or GST in Hong Kong.

- Annual Compliance: Business Registration renewal is required annually; limited partnerships must notify the Registrar of any changes to partners or capital contributions.

- Treaty Access: Partnerships generally do not access Hong Kong's double tax agreements, as treaty benefits typically require corporate residency status.

- Restrictions: General partners in a limited partnership cannot restrict their own liability; limited partners who participate in management risk losing their liability cap under Cap. 37.

- Conversion: No direct statutory conversion pathway exists from a partnership to a limited company; restructuring requires dissolution and fresh incorporation.

Sub-Types

General Partnership

All partners share equal management rights and unlimited joint liability for the firm's debts unless a partnership agreement specifies otherwise. This structure suits small professional practices or co-founded businesses where partners operate actively.

Limited Partnership

One or more general partners manage operations and bear unlimited liability, while limited partners contribute capital passively. This structure is frequently used for private equity funds and investment vehicles where investor liability must be defined and contained.

Recommendations

Partnerships suit professional service firms, joint ventures with a defined partner group, or investment funds requiring a pass-through tax structure without corporate formalities. The absence of separate legal personality is a meaningful operational constraint, particularly for entering contracts or holding property.

General partnerships fit small professional practices; limited partnerships are suited to fund structures and capital ventures requiring defined investor liability.

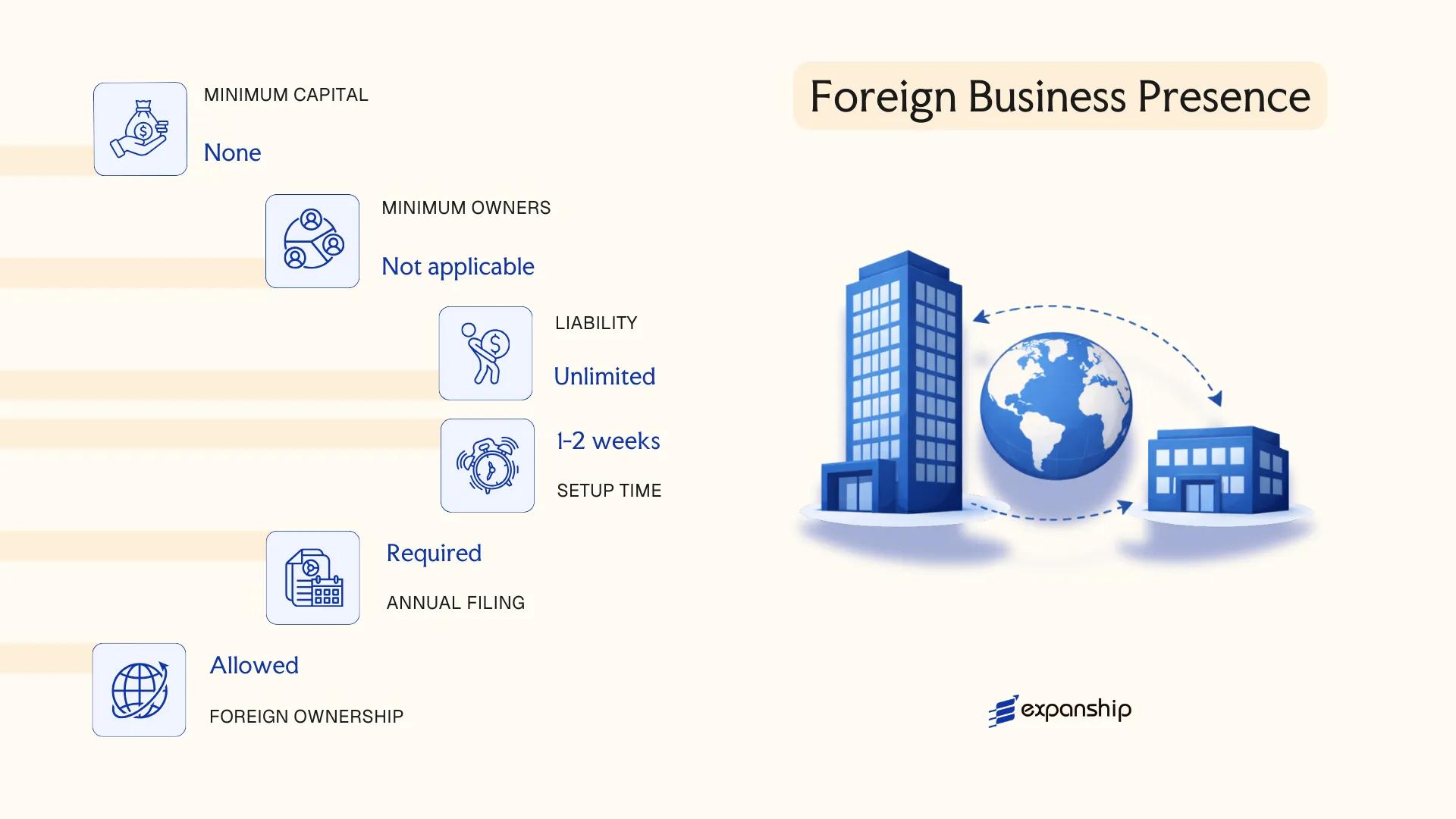

Foreign Business Presence [Branch Office, Representative Office]

Foreign companies seeking a presence in Hong Kong without forming a locally incorporated entity have two primary options: registering a branch office or establishing a representative office. The distinction between a Hong Kong branch office vs representative office is significant, particularly regarding legal liability and permitted activities, and the choice directly affects how your business operates within the territory.

A branch office is not a separate legal entity. The parent company bears full legal liability for the branch's obligations. Registration is governed by Part 16 of the Companies Ordinance (Cap. 622), which requires overseas companies to register with the Companies Registry within one month of establishing a place of business.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of the foreign parent; no separate legal personality | Informal presence; no statutory registration framework under Cap. 622 |

| Governing Law | Companies Ordinance (Cap. 622), Part 16 | No dedicated legislation; operationally constrained by business activity scope |

| Local Presence | Registered address in Hong Kong; authorised representative required | Physical office address; no formal registration required |

| Permitted Activities | Full commercial activities on behalf of the parent | Liaison, market research, promotional activities only; cannot generate revenue |

| Capital Requirement | None stipulated locally; parent's capital structure applies | Not applicable |

| Privacy | Parent company's constitutional documents filed publicly with Companies Registry | No public filing obligation |

Focus Points

- Taxation: Branch profits are subject to Hong Kong's Profits Tax at 16.5% (standard rate) on assessable profits sourced in Hong Kong; no separate VAT applies, though stamp duty is payable on applicable instruments.

- Annual Compliance: Registered branches must file an annual return with the Companies Registry and maintain a local authorised representative at all times.

- Treaty Access: Hong Kong has a network of Comprehensive Avoidance of Double Taxation Agreements (CDTAs); branch eligibility for treaty benefits depends on the parent entity's jurisdiction of incorporation.

- Activity Restrictions: A representative office cannot enter into contracts, issue invoices, or conduct revenue-generating operations — any deviation risks reclassification as a taxable entity.

- Conversion: A branch can be converted into a locally incorporated subsidiary, though this requires a separate incorporation process under the Companies Ordinance rather than a direct structural conversion.

Sub-Types

Branch Office

Registered under Part 16 of the Companies Ordinance (Cap. 622), a branch office allows the foreign parent to conduct full commercial operations in Hong Kong. All liabilities incurred by the branch remain the direct responsibility of the parent company.

Representative Office

No statutory registration is required, but the office's activities must remain strictly non-commercial. It is typically used for market research, maintaining client relationships, or coordinating regional communications without triggering a tax liability.

A branch office suits foreign companies that need to conduct active business operations without incorporating a new local entity, though the absence of liability separation exposes the parent to direct legal risk. A representative office carries no such risk but is structurally limited to non-revenue activities.

A branch office is best suited for established foreign corporations that require a revenue-generating presence but prefer to avoid the administrative overhead of a separately incorporated subsidiary.

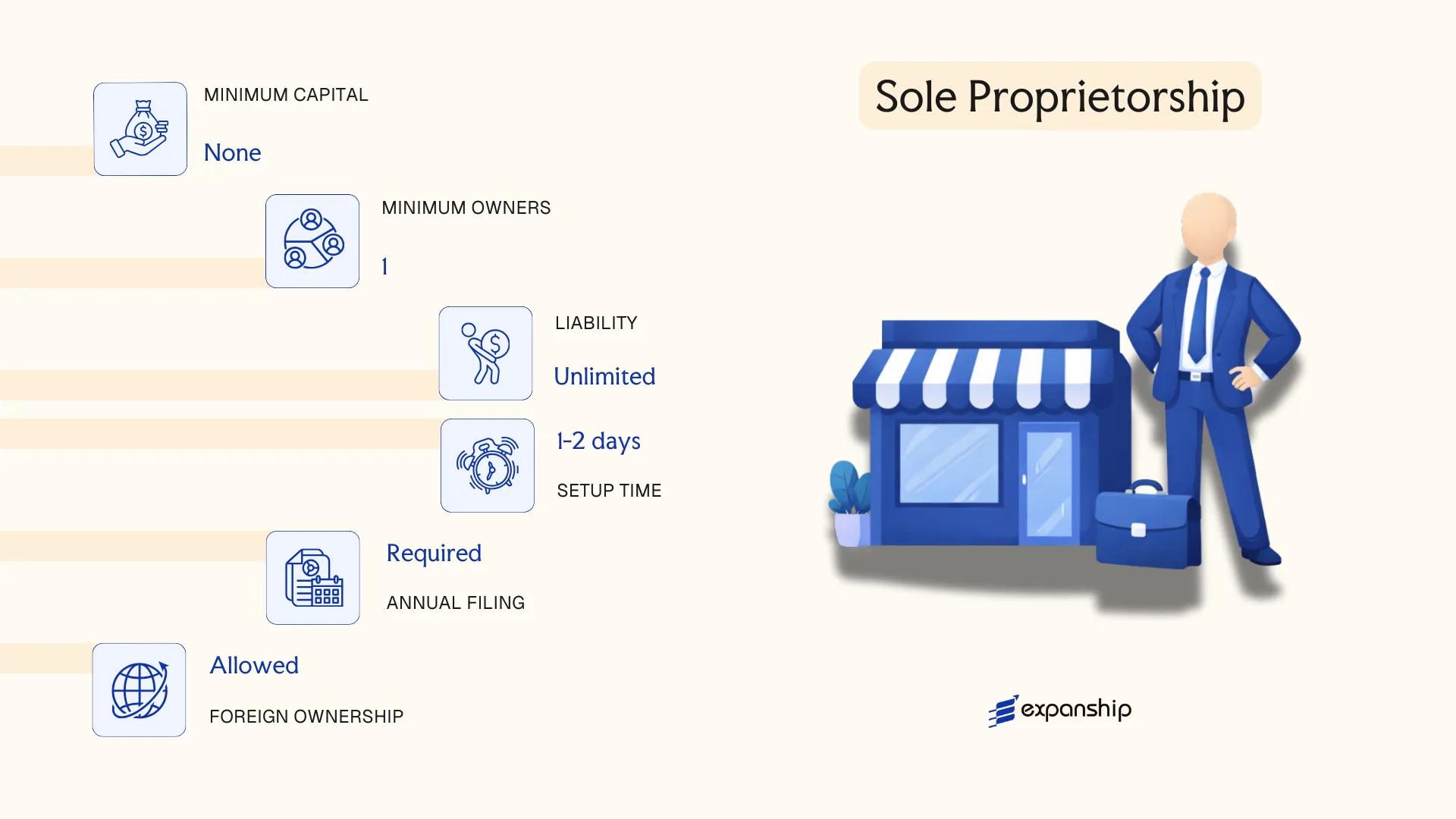

Sole Proprietorship

Sole proprietorship registration in Hong Kong is governed by the Business Registration Ordinance (Cap. 310), administered by the Inland Revenue Department (IRD). Unlike the corporate structures discussed earlier in this guide, a sole proprietorship carries no separate legal personality — the business and its owner are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration must be completed within one month of commencing business. The Business Registration Certificate, renewed annually or every three years, is the primary compliance document required to operate legally.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Sole proprietor | Single individual only; no partners or shareholders |

| Membership | 1 proprietor (minimum and maximum) | Cannot have co-owners; use a partnership structure instead |

| Local Presence | Registered business address in Hong Kong | IRD-registered address required for correspondence |

| Capital | No minimum capital requirement | No statutory paid-up capital obligation |

| Privacy | Owner's name may appear on public business registration records | Limited privacy compared to corporate structures |

Focus Points

- Taxation: Subject to profits tax on Hong Kong-sourced income at 15% (unincorporated); the two-tier regime does not apply; no VAT or GST; standard stamp duty applies to property transactions.

- Annual Compliance: Business Registration Certificate must be renewed; no annual return or audited accounts required by statute.

- Treaty Access: No access to Hong Kong's tax treaty network, as treaties apply to corporate entities.

- Conversion: Can be converted to a private limited company, though assets and contracts must be formally transferred.

- Restrictions: Cannot issue shares, raise equity capital, or operate in regulated industries that require corporate licensing.

Closing Paragraph

A sole proprietorship suits freelancers, consultants, and small-scale local traders who operate with minimal overhead and do not require liability protection or external investment. The absence of audit requirements reduces ongoing costs, but unlimited personal liability remains a significant structural risk.

Local individual operators running low-risk, single-person businesses who prioritise simplicity over liability protection.

How to Choose the Right Entity Type in Hong Kong

Why Your Entity Choice Matters

Selecting the wrong structure at registration has concrete, lasting consequences under the Companies Ordinance (Cap. 622).

- Registering a foreign branch when you intend to conduct substantive local trade can result in regulatory non-compliance under the Companies Ordinance, exposing the business to striking off or financial penalties.

- Choosing a structure that lacks access to Hong Kong's network of double taxation agreements means you cannot claim reduced withholding tax rates in counterpart jurisdictions.

- Forming a private company limited by shares for a single-person consultancy with no audit exemption triggers mandatory audit costs that a sole proprietorship registered under the Business Registration Ordinance (Cap. 310) would not incur.

- Selecting a company structure when a trust would better serve asset protection or succession planning locks your business into annual shareholder obligations and statutory filing requirements that do not apply to trust arrangements.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or fund management each require a distinct structure under Hong Kong law.

- Ownership and Management: A single-owner operation and a multi-party joint venture have different requirements for governance, liability separation, and profit distribution.

- Tax Objectives: Your eligibility for the two-tiered profits tax regime or offshore income exemption depends on which entity type you register and how it operates.

- Substance Capacity: If your firm cannot maintain a genuine local presence, consider whether the chosen structure will satisfy the Inland Revenue Department's requirements for tax claims.

- Exit Strategy: Not all structures permit redomiciliation or conversion; confirm in advance whether your chosen entity type supports the exit route you anticipate.

Compliance Services for Companies in Hong Kong

Ongoing compliance support for Hong Kong-registered entities, including annual return filing, statutory obligations, and regulatory reporting.

Conclusion

Selecting the right structure is one of the most consequential decisions in this Hong Kong company formation summary guide. The private company limited by shares dominates registrations under the Companies Ordinance (Cap. 622) and suits the broadest range of commercial purposes. Public companies serve businesses seeking capital from external investors, while companies limited by guarantee are reserved for non-profit and membership organisations. Unlimited companies carry unrestricted liability and are rarely used. General partnerships offer simplicity at the cost of personal exposure; limited partnerships suit investment vehicles where liability must be defined by statute. Branch offices bind the foreign parent directly, whereas representative offices cannot generate revenue. Sole proprietorships remain the most straightforward structure for individual traders.

Hong Kong continues to expand its network of comprehensive avoidance of double taxation agreements, reinforcing its position as a preferred holding and regional headquarters jurisdiction. Expanship's team works directly with the Companies Registry and relevant authorities to guide your registration from structure selection through to full compliance.

How Expanship Can Assist You

Expanship's Hong Kong company incorporation services cover the full process of forming and maintaining a legal entity under the Companies Ordinance (Cap. 622). From private companies limited by shares to companies limited by guarantee, every structure discussed in this guide falls within our service scope — including filings lodged directly with the Companies Registry.

Our team handles the administrative and compliance work so your business can focus elsewhere. Specifically, we assist with:

- Document preparation, notarization, and legalization

- Registered office and registered agent provision

- Government filing and Companies Registry liaison

- Post-incorporation compliance management

- Business registration renewal with the Inland Revenue Department

- Banking introduction assistance

Reach out to Expanship Hong Kong to discuss which structure suits your business objectives.

Frequently Asked Questions (FAQ)

The private company limited by shares is by far the most frequently incorporated structure. Its appeal rests on capped shareholder liability, a single-member minimum, and eligibility for the territory's two-tier profits tax regime.

A branch is a registered extension of its foreign parent under the Companies Ordinance, carries no separate legal personality, and exposes the parent entity to local liabilities. A private limited company is an independent legal person, files its own profits tax return with the Inland Revenue Department, and ring-fences the parent from Hong Kong-sourced obligations.

A private company limited by shares permits the appointment of nominee directors and shareholders, whose details appear on the Companies Registry public register in place of the beneficial owner's. Beneficial ownership information is held separately and disclosed only to designated authorities under the statutory beneficial ownership regime.

A sole proprietorship and a private company limited by shares can each be formed by one individual. General and limited partnerships require a minimum of two partners, and a company limited by guarantee requires at least one member but is structurally unsuited to single commercial operators.

All principal entity types, including private companies limited by shares, unlimited companies, and companies limited by guarantee, are accessible to non-residents without any local ownership requirement. Foreign individuals may act as sole directors and sole shareholders of a private limited company; however, every locally registered business must maintain a registered address in the territory.

The Companies Ordinance provides a re-registration mechanism that allows a private company limited by shares to convert to an unlimited company, and vice versa. Conversion between fundamentally different structures, such as from a partnership to a limited company, generally requires dissolution of the original entity and fresh incorporation rather than a direct re-registration.

Private and public companies limited by shares, companies limited by guarantee, and unlimited companies all possess distinct legal personality under the Companies Ordinance. Partnerships, sole proprietorships, and representative offices do not; in each case, the individual partners or proprietor remain personally exposed to business obligations.

A sole proprietorship has no annual return filing requirement with the Companies Registry and no statutory audit obligation. That said, the proprietor remains personally liable for all debts and must still register with the Business Registration Office and file annual profits tax returns with the Inland Revenue Department.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.