Key Takeaways

- The Faroe Islands operates its own corporate legal and fiscal framework independently from Denmark, with company registration administered by the Skráseting Føroya (Faroese Business Authority).

- Among all recognized Faroese business structures, the Einkafelag (Sp/F) is the most commonly registered form for private ventures due to its defined liability boundaries and manageable governance requirements.

- Faroese law recognizes distinct entity types for specific commercial purposes, including the Samvinnufelag for member-driven cooperative arrangements and the Kommandittfelag (K/F) for limited partnership structures where personal liability exposure varies by partner role.

- Foreign businesses can establish a presence in the Faroe Islands without forming a separate legal entity by registering either a branch office or a representative office under Faroese commercial law.

Introduction to Entity Types in Faroe Islands

Located in the North Atlantic between Norway and Iceland, the Faroe Islands is an archipelago of 18 islands with a distinct political status: a self-governing territory within the Kingdom of Denmark. While Danish foreign policy and defense matters apply, the islands operate their own legal and fiscal systems, giving them considerable autonomy over corporate regulation.

Company registration falls under the jurisdiction of the Faroese Business Authority (Skráseting Føroya), which maintains the official business registry and oversees compliance requirements for all registered entities.

The tax regime is territorial in orientation, with corporate tax rates that differ from Denmark's — though specific rates vary by entity type and activity, and certain sectors face distinct treatment.

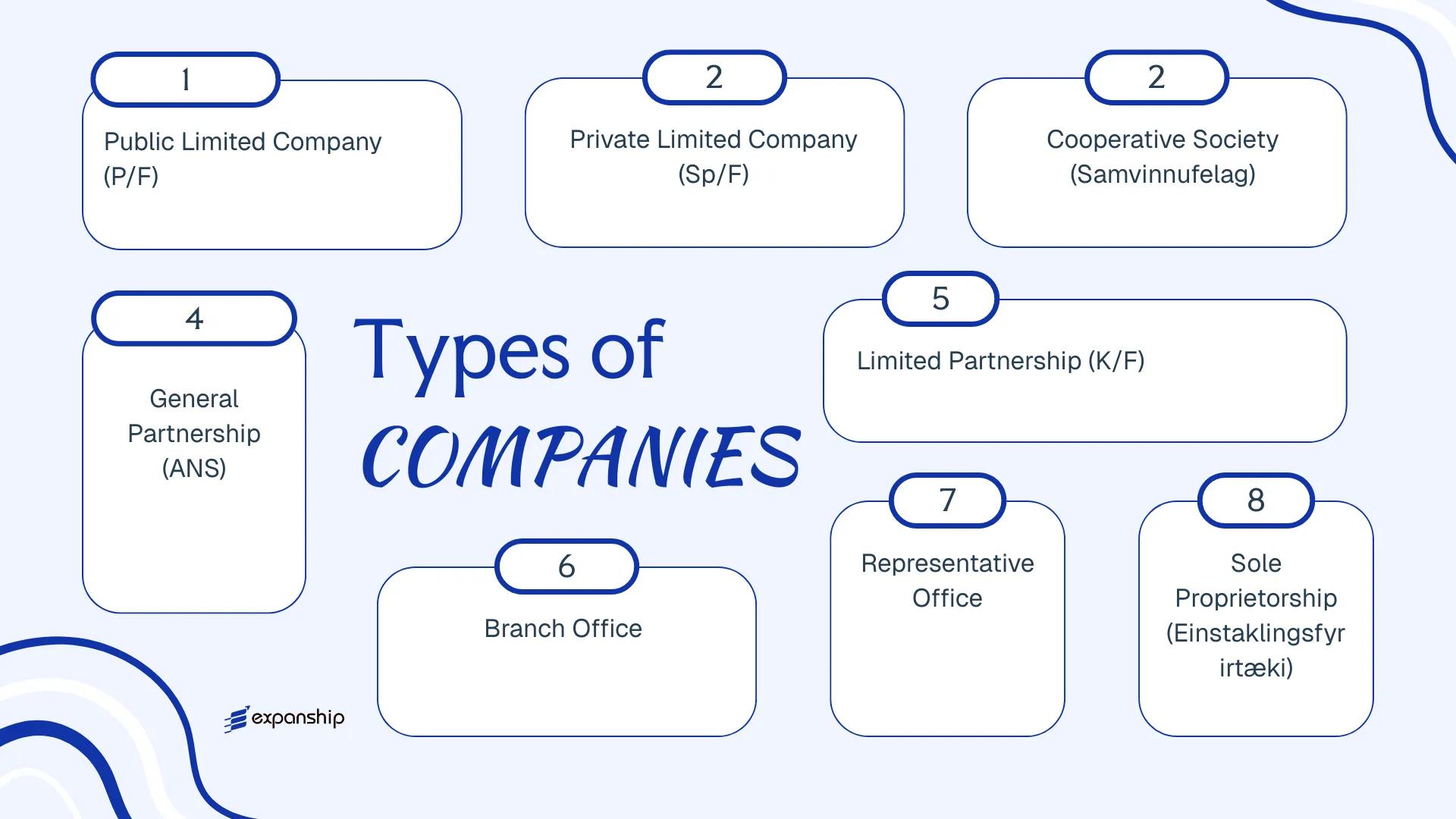

Several business entity types Faroese law recognizes include the Samlagsfelag (P/F), Einkafelag (Sp/F), Samvinnufelag, Ansvarligt Felag (ANS), Kommandittfelag (K/F), Branch Office, Representative Office, and Einstaklingsfyrirtæki. Each structure carries its own liability, governance, and registration requirements.

This article examines each of these Faroese company structures in turn — covering formation requirements, liability rules, and the circumstances under which each form is typically used.

An Overview of Business Structures in Faroe Islands

Faroese company law provides several distinct legal forms for doing business, primarily governed by the Løgtingslóg nr. 65 fra 10. mai 1995 um virksomhedsformer (the Faroese Companies Act) and related legislation administered through the Faroese Commerce and Companies Agency (Skráseting Føroya). Each structure carries different implications for liability, governance, and tax treatment.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Samlagsfelag (P/F) | Public Limited Company | Limited | Taxed | Yes | 1 shareholder | Skráseting Føroya | Companies Act |

| Einkafelag (Sp/F) | Private Limited Company | Limited | Taxed | Yes | 1 shareholder | Skráseting Føroya | Companies Act |

| Samvinnufelag | Cooperative Society | Limited | Taxed | Yes | Minimum members required | Skráseting Føroya | Cooperative legislation |

| Ansvarligt Felag (ANS) | General Partnership | Unlimited | Taxed | Yes | 2 partners | Skráseting Føroya | Partnership rules |

| Kommandittfelag (K/F) | Limited Partnership | Mixed | Taxed | Yes | 1 general + 1 limited | Skráseting Føroya | Partnership rules |

| Branch Office | Foreign branch | Head office liable | Taxed on local income | Yes | N/A | Skráseting Føroya | Companies Act |

| Representative Office | Non-trading presence | Head office liable | Generally exempt | No | N/A | Skráseting Føroya | General rules |

| Einstaklingsfyrirtæki | Sole Proprietorship | Unlimited | Taxed | Yes | 1 individual | Skráseting Føroya | General rules |

Each of these structures is examined in full in the sections below.

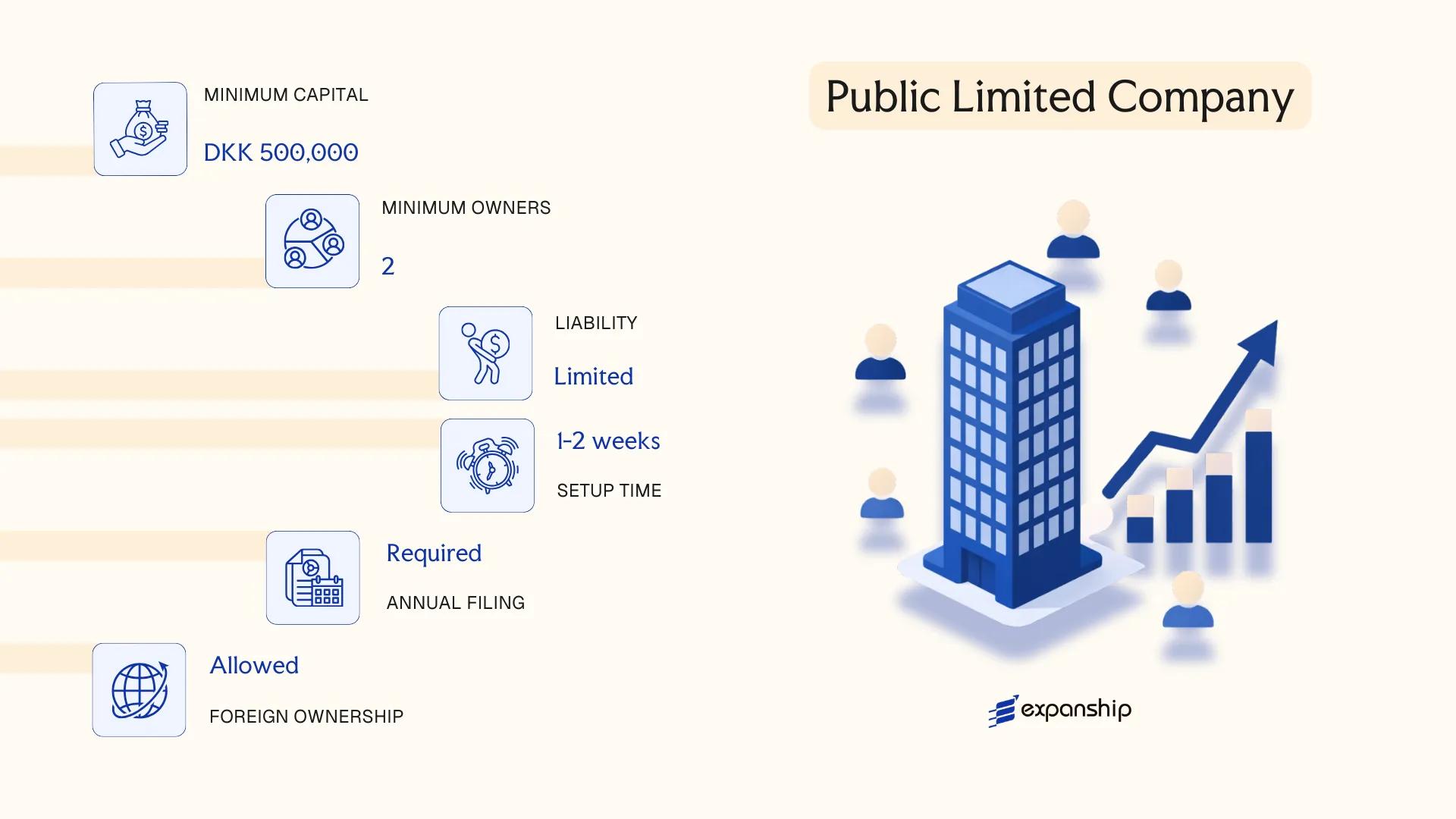

Samlagsfelag (P/F) – Public Limited Company

The Samlagsfelag (P/F) is the primary vehicle for large-scale commercial activity and public capital raising in the Faroe Islands. Governed by the Faroese Companies Act, this structure carries separate legal personality, meaning the entity holds rights and obligations independently of its shareholders.

Shareholders bear no personal liability beyond their subscribed capital. This makes the P/F structurally comparable to the Danish aktieselskab (A/S), reflecting the historical legislative alignment between the two jurisdictions.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Separate legal personality; limited liability |

| Members | Shareholders; Board of Directors required | No maximum on shareholders; minimum one shareholder permitted |

| Local Presence | Registered office in the Faroe Islands | Registered agent not mandated by statute, but a local address is required |

| Share Capital | DKK 500,000 minimum | Must be fully subscribed at incorporation; shares may be publicly traded |

| Privacy | Shareholder register is generally accessible | Directors and company details filed with the Faroese Commerce and Companies Agency |

Focus Points

- Taxation: Subject to corporate income tax administered by TAKS (the Faroese Tax Authority); VAT applies to taxable supplies; dividend withholding tax may apply to non-resident shareholders depending on applicable agreements.

- Annual Compliance: Audited financial statements required; annual accounts must be filed with the Faroese Commerce and Companies Agency.

- Economic Substance: No formalised substance regime equivalent to certain offshore jurisdictions, but physical or operational presence may be expected for treaty and tax purposes.

- Treaty Access: The Faroe Islands maintain independent tax agreements with several Nordic countries; access depends on residency and structure.

- Conversion: A P/F may be converted to a private limited company (Sp/F) subject to meeting the relevant statutory conditions.

Closing

The P/F suits businesses requiring access to public capital markets, large joint ventures, or structures where credibility with institutional counterparties matters. The mandatory minimum capital of DKK 500,000 and the auditing requirement represent meaningful compliance commitments that may outweigh the benefits for smaller operations.

The P/F is best suited for established businesses or groups seeking to raise capital publicly or structure significant commercial operations under a recognised, regulated corporate form.

Company Incorporation in the Faroe Islands

Incorporate a Samlagsfelag (P/F) or other entity type in the Faroe Islands with end-to-end support from Expanship.

Einkafelag (Sp/F) – Private Limited Company

The Einkafelag (Sp/F) private limited company in the Faroe Islands is the most commonly used corporate structure for closely held businesses. Governed by Faroese company law, it carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders. Liability is confined to each member's capital contribution.

Structured as a hybrid between a fully public company and a partnership, the Sp/F suits businesses that require formal corporate standing without the disclosure burdens associated with publicly listed entities. Sp/F company formation in the Faroe Islands is administered through the Faroese Commerce and Companies Agency (Fyrirtækjaskráin).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Einkafelag) | Separate legal personality; limited liability |

| Members | Shareholders: minimum 1, no maximum | Shareholders may be natural persons or legal entities of any nationality |

| Governing Body | Board of Directors or Managing Director | Smaller Sp/F entities may operate with a single managing director |

| Local Presence | Registered office required in the Faroe Islands | No statutory requirement for a local resident director, though a registered address is mandatory |

| Share Capital | Minimum DKK 50,000 | Must be fully subscribed at incorporation; denominated in Danish Krone |

| Privacy | Shareholder register is not fully public | Basic company information is accessible via the commercial registry |

Focus Points

- Taxation: Subject to Faroese corporate income tax; VAT obligations apply to taxable supplies; no separate withholding tax regime specific to dividends has been publicly codified under standard Faroese rules, though Danish tax treaty frameworks may have relevance given the constitutional relationship.

- Annual Compliance: Annual financial statements must be filed with Fyrirtækjaskráin; audit requirements depend on the size thresholds of the entity.

- Economic Substance: No formal substance legislation mirroring offshore regimes; standard operational presence is expected.

- Conversion: An Sp/F may be converted to a public Samlagsfelag (P/F) subject to meeting the applicable capital and procedural requirements under Faroese company law.

- Restrictions: Shares in an Sp/F cannot be offered to the general public or listed on a securities exchange.

Closing

The Sp/F is well suited for trading operations, holding structures, and family-owned businesses seeking formal limited liability without public reporting obligations. Its straightforward governance structure reduces administrative overhead, though the minimum capital requirement and mandatory registered office add baseline setup costs that sole proprietors or small operators should account for.

The Sp/F is best suited for entrepreneurs, SMEs, and foreign investors seeking a private, limited liability vehicle with a manageable compliance burden for operating or holding activities in the Faroe Islands.

Samvinnufelag – Cooperative Society

A Samvinnufelag cooperative society in the Faroe Islands is governed primarily by Faroese cooperative legislation, operating as a distinct legal entity with separate legal personality from its members. The structure carries limited liability and functions as a hybrid between a commercial company and a membership association, making it distinct from standard capital-based entities.

Ownership and economic benefit are distributed among members based on participation rather than capital contribution. This principle, common to cooperative structures across Nordic jurisdictions, means profit allocation follows transactional activity with the cooperative rather than shareholding.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society (Samvinnufelag) | Separate legal personality; limited liability for members |

| Members | Referred to as members; no fixed statutory maximum; minimum typically 5 | Membership open-entry principle generally applies |

| Management | Board of Directors elected by members | General assembly holds supreme authority |

| Local Presence | Registered office required in Faroe Islands | No statutory requirement for a resident agent |

| Capital | No fixed minimum share capital; member contributions define funding | Contributions may be equal or variable per member |

| Privacy | Member register maintained; not always publicly disclosed in full | Board details generally on public record |

Focus Points

- Taxation: Subject to Faroese corporate income tax on net profits; VAT obligations apply to taxable supplies; no specific cooperative tax exemption exists as a general rule.

- Annual Compliance: Annual accounts must be prepared and submitted; general assembly must be held yearly.

- Treaty Access: Limited access to double tax treaty benefits compared to capital-based companies; treaty eligibility depends on residency and structure.

- Restrictions: Primarily suited for member-serving activities; use as a pure holding or speculative investment vehicle is structurally inconsistent with cooperative principles.

- Conversion: Conversion to a limited liability company is possible but requires member approval and regulatory re-registration.

Closing

Samvinnufelags are used in sectors such as fishing, agriculture, retail, and consumer services, where collective member benefit drives the business model. The structure supports democratic governance and equitable profit distribution, though it is less suited to external investor participation or capital-intensive ventures requiring clear equity tiers.

Best suited for member-driven industries such as fishing cooperatives, agricultural collectives, or consumer-owned retail businesses where profit distribution by participation outweighs the need for external investment.

Partnerships [Ansvarligt Felag (ANS) – General Partnership, Kommandittfelag (K/F) – Limited Partnership]

Both ANS K/F partnership structures in the Faroe Islands are governed by Faroese commercial law, with regulatory oversight handled through the Faroese Business Authority (Skráseting Føroya). Partnerships are recognized as separate legal entities for registration purposes, though personal liability exposure varies significantly between the two forms.

Under an Ansvarligt Felag general partnership in the Faroe Islands, all partners bear unlimited joint and several liability for the firm's obligations. The Kommandittfelag limited partnership introduces a two-tier structure: at least one general partner retains unlimited liability, while limited partners are liable only to the extent of their contributed capital.

Key Characteristics

| Requirement | ANS (General Partnership) | K/F (Limited Partnership) |

|---|---|---|

| Legal Form | Separate registered entity; unlimited liability for all partners | Separate registered entity; mixed liability structure |

| Members | Minimum 2 general partners; no statutory maximum | Minimum 1 general partner (unlimited liability) + 1 limited partner; no statutory maximum |

| Local Presence | Registered address in the Faroe Islands required | Registered address in the Faroe Islands required |

| Capital | No statutory minimum; contributions defined in partnership agreement | No statutory minimum; limited partner's liability capped at contributed capital |

| Privacy | Partner names filed with Skráseting Føroya; publicly accessible | General and limited partner names disclosed in the public register |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent; profits flow through to partners and are taxed at the individual or corporate level depending on partner type; VAT registration applies where turnover thresholds are met.

- Annual Compliance: Annual accounts must be submitted to Skráseting Føroya; filing obligations vary based on the size and activity of the firm.

- Economic Substance: No formal economic substance regime comparable to some offshore jurisdictions; standard Faroese commercial presence requirements apply.

- Restrictions: Limited partners in a K/F must not participate in active management, or they risk losing liability protection under Faroese partnership law.

- Conversion: Conversion to a capital company structure such as a Sp/F is possible but requires formal re-registration and partner consent.

Closing

Faroese partnerships suit joint ventures, professional services arrangements, and investment vehicles where flexibility in profit-sharing is a priority. The key advantage is structural simplicity with no minimum capital requirement; the principal drawback is the unlimited personal liability carried by general partners in both entity forms.

These structures are best suited for two or more parties, including professionals or investors, seeking a low-formality vehicle with flexible governance and no mandatory share capital.

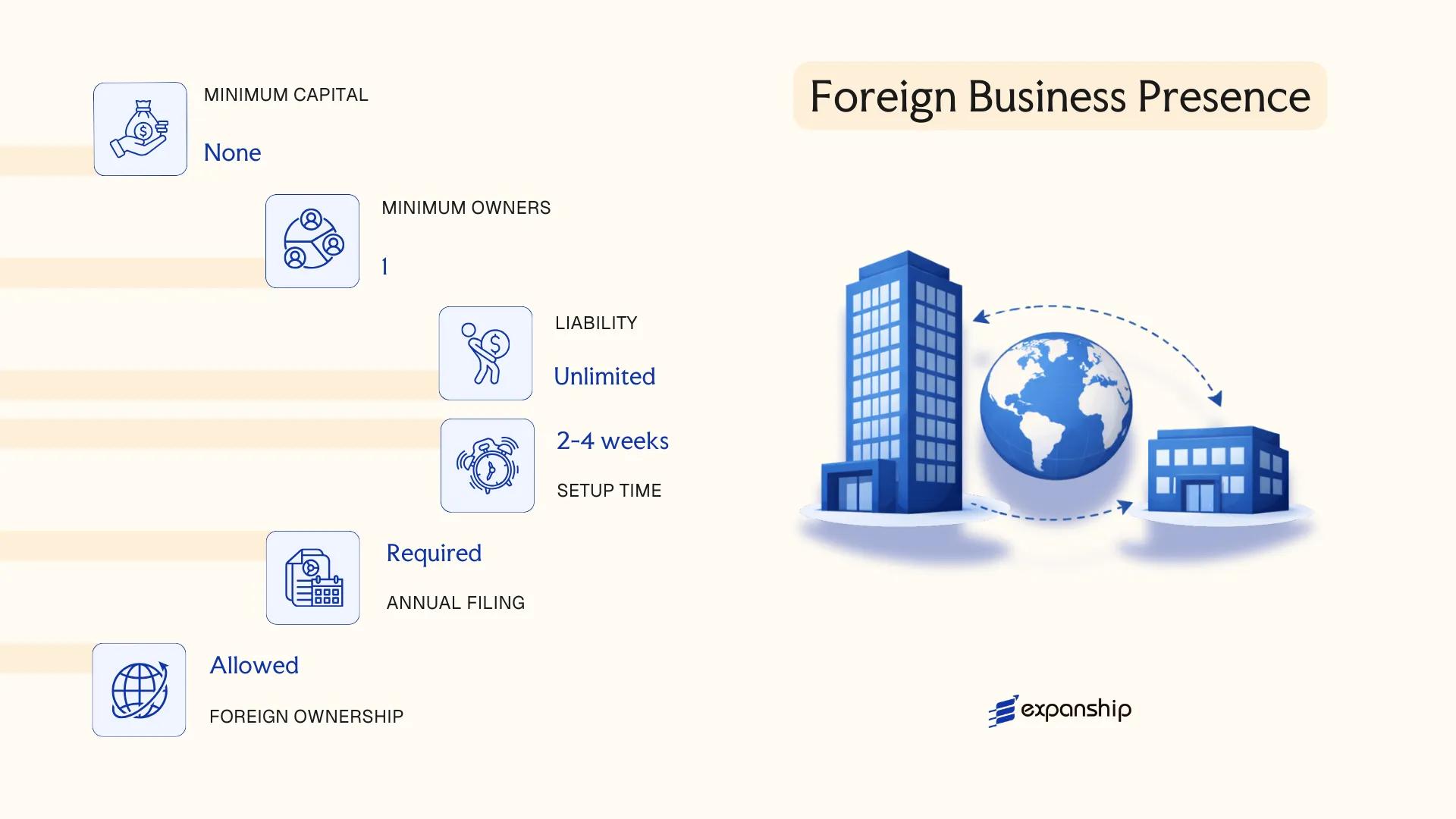

Foreign Business Presence [Branch Office, Representative Office]

A foreign company branch office in the Faroe Islands operates as an extension of its parent entity rather than a separate legal person. The branch remains fully integrated with the foreign parent, which bears unlimited liability for its obligations. Registration is governed by the Faroese Companies Act (Felagslógin), administered through the Faroese Commerce and Companies Agency (Skráseting Føroya).

Unlike a branch, a representative office carries no authority to generate revenue or enter binding contracts on behalf of the parent. Its permitted activities are limited to market research, liaison functions, and promotional work.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Liability | Parent bears full liability | Parent bears full liability |

| Revenue Generation | Permitted | Not permitted |

| Local Representative | Mandatory — must be resident in the Faroe Islands | Required |

| Registered Address | Required locally | Required locally |

| Capital Requirement | No separate minimum capital | No separate minimum capital |

Focus Points

- Taxation: Branch profits are subject to Faroese corporate income tax; VAT registration is required if taxable turnover thresholds are met; withholding tax may apply to profit remittances depending on applicable treaties.

- Economic Substance: No formal economic substance regime applies to branches, but a local representative is mandatory.

- Annual Compliance: Annual accounts filed at Skráseting Føroya; parent company financial statements may be required to accompany the filing.

- Treaty Access: The Faroe Islands maintain their own tax treaty network, separate from Denmark's; treaty access for branches depends on the parent entity's jurisdiction of incorporation.

- Restrictions: Representative offices cannot invoice clients, hold inventory for sale, or sign commercial contracts.

Closing

A branch structure suits foreign firms testing the Faroese market or executing specific contracts without committing to a locally incorporated entity, though the absence of liability separation between the branch and its parent is a material commercial risk.

Foreign companies with existing operations seeking a direct commercial presence or a preliminary market entry point before committing to full incorporation.

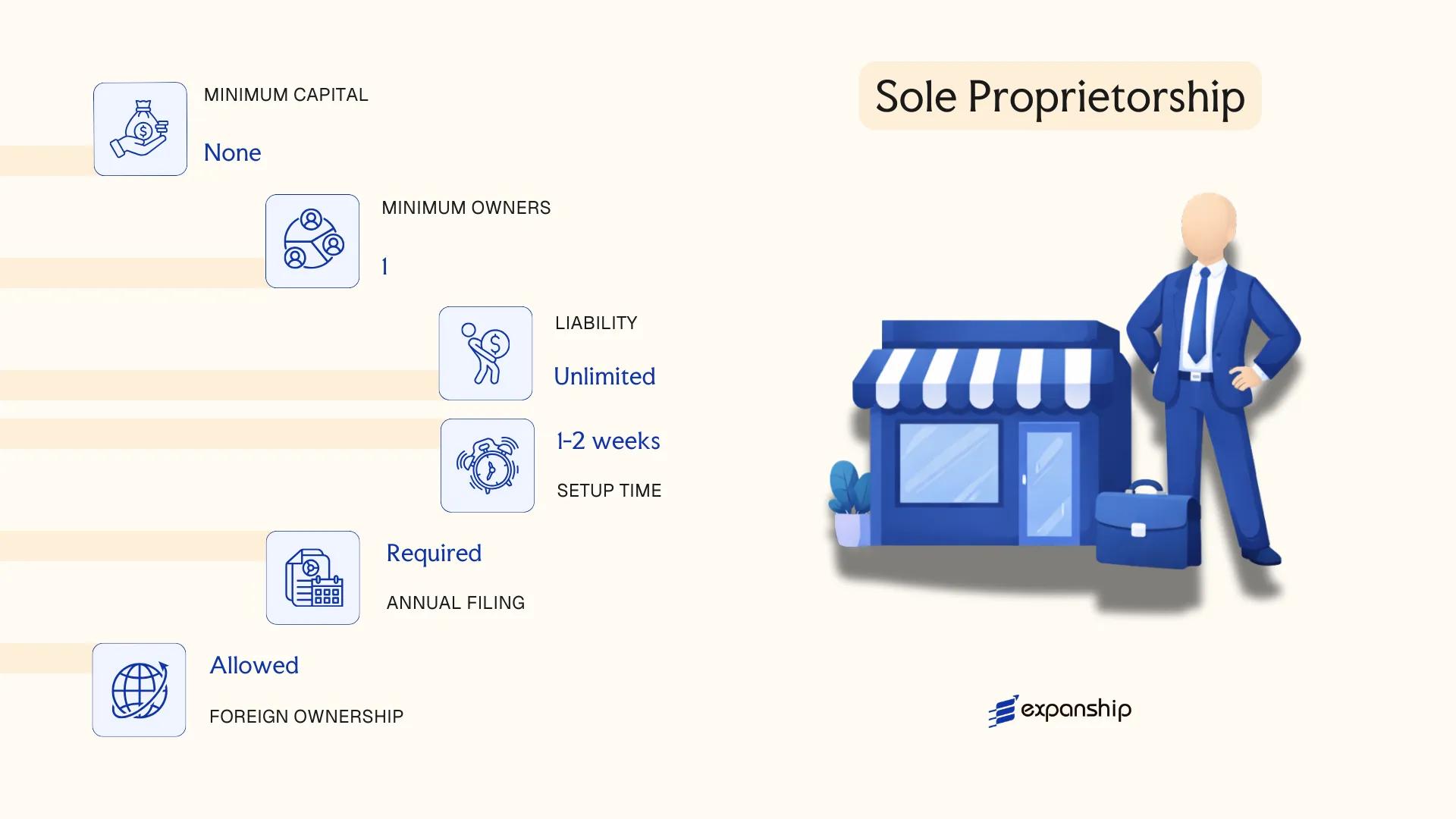

Einstaklingsfyrirtæki – Sole Proprietorship

The Einstaklingsfyrirtæki is the simplest form of self-employed business in the Faroe Islands, governed under the general commercial registration framework administered by Skráseting Føroya, the Faroese Register of Companies. Registration is mandatory before commencing trading activity.

There is no separation between the proprietor and the business — the owner bears full personal liability for all debts and obligations. This legal structure carries no independent legal personality, meaning the firm cannot hold assets, enter contracts, or sue in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality from the owner |

| Members | Single proprietor only | One individual; no minimum capital threshold |

| Local Presence | Registered address in the Faroe Islands required | Must be a physical address, not a PO box |

| Capital | No statutory minimum | Proprietor's personal assets back all liabilities |

| Privacy | Owner's name is publicly registered | Minimal privacy; details filed with Skráseting Føroya |

Focus Points

- Taxation: Subject to personal income tax rather than corporate tax; VAT registration required once turnover exceeds the statutory threshold; no withholding tax obligations as a separate entity.

- Annual Compliance: Annual accounts must be filed; obligations are lighter than for limited companies but financial records must be maintained.

- Treaty Access: No access to double tax treaties as a separate legal person; tax position flows through to the individual proprietor.

- Conversion: Can be converted into a limited liability entity such as an Sp/F, though formal re-registration with Skráseting Føroya is required.

- Restrictions: Foreign nationals may face residency or permit requirements before registering as a sole trader.

Closing

This structure suits freelancers, artisans, and small-scale traders operating with low overhead and limited third-party risk exposure. The primary drawback is unlimited personal liability, which creates direct exposure of the proprietor's personal assets to business creditors.

Best suited for Faroese residents or individuals with the right to work in the territory who are launching a low-risk, owner-operated business with no immediate plans to scale or bring on external capital.

How to Choose the Right Entity Type in Faroe Islands

Choosing the right company structure in the Faroe Islands is a decision with direct legal and financial consequences — not an administrative formality.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations from day one. Specific outcomes to be aware of:

- Registering a foreign branch to conduct local trade while omitting registration with the Faroese Tax Administration (TAKS) and the Faroese Business Authority can result in penalties or forced deregistration.

- Selecting a tax-exempt cooperative when your counterparties require treaty access means you cannot claim withholding tax reductions under applicable double taxation agreements.

- Forming a Samlagsfelag (P/F) when your operation is a single-person consultancy subjects your business to statutory audit requirements and annual general meeting obligations that would not apply under a sole proprietorship.

- Choosing a general partnership structure when asset protection or estate planning is the primary objective creates joint and unlimited personal liability that no shareholder agreement can fully offset.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward a distinct structure under Faroese company law.

- Ownership and Management: A sole owner with no co-investors may find that an Einkafelag (Sp/F) offers adequate structure without the governance overhead of a public company.

- Tax Objectives: Your need for full exemption, specific regime eligibility, or treaty access should be confirmed before selecting an entity, as not all structures qualify equally.

- Substance Capacity: If you cannot maintain staff or decision-making functions locally, verify whether your chosen entity type carries substance thresholds that trigger reporting obligations.

- Privacy Requirements: The Faroese Business Authority maintains a public register; understanding what is disclosed — and what nominee arrangements are permissible — should factor into your decision.

- Exit Strategy: Redomiciliation and conversion options vary by entity type; confirm whether your preferred structure permits these before registering.

Compliance Services for Companies in the Faroe Islands

Maintain good standing with Faroese regulatory requirements, including annual filings, tax registration, and reporting obligations.

Conclusion

Each entity structure available under Faroese commercial law serves a distinct purpose. The Samlagsfelag (P/F) suits larger enterprises requiring public capital access, while the Einkafelag (Sp/F) remains the most commonly registered form for private ventures, valued for its defined liability boundaries and comparatively straightforward governance. Partnerships — both ANS and K/F — fit closely held arrangements where partners accept greater personal exposure. The Samvinnufelag applies specifically to member-driven economic cooperation. Branch offices and representative offices allow foreign firms to establish a presence without creating a separate legal entity.

Incorporating a company in the Faroe Islands guide materials consistently point toward the Einkafelag as the default choice for most incoming businesses. Governed under Faroese corporate legislation administered through the Skráseting Føroya, the business registry, the framework continues to mature as the territory expands its administrative capacity. Professional guidance on entity selection and registration procedures becomes relevant when local regulatory requirements intersect with your home jurisdiction's rules.

How Expanship Can Assist You

Expanship company formation services Faroe Islands cover the full process, from selecting between a Samlagsfelag (P/F) and an Einkafelag (Sp/F) to meeting the registration requirements set by the Faroese Commercial and Companies Authority (Skráseting Føroya). Your obligations do not end at incorporation — annual reporting, directorship requirements, and ongoing regulatory filings all demand attention.

From document preparation to post-incorporation compliance, our team manages every stage on your behalf:

- Document preparation and notarization

- Registered agent and registered office provision

- Filing with Skráseting Føroya and related government bodies

- Post-incorporation compliance management

- Banking introduction assistance

Ready to move forward? Contact Expanship Faroe Islands to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Einkafelag (Sp/F), or private limited company, is the most frequently registered structure. Its relatively low minimum share capital requirement and liability protection make it the default choice for small to medium-sized businesses operating locally.

Both entities offer limited liability, but the Samlagsfelag (P/F) is structured for public share issuance and carries heavier disclosure and governance obligations under Faroese company law. An Einkafelag (Sp/F) restricts share transfers and has lighter ongoing compliance requirements, making it more practical for closely held businesses.

Among available structures, the Einkafelag (Sp/F) generally discloses less publicly than the Samlagsfelag (P/F), since it is not subject to public share listing requirements. Director and shareholder information is registered with Skráseting Føroya, the Faroese Business Register, though nominee arrangements may be available under local practice.

Not all structures permit single-person formation. An Einkafelag (Sp/F) can be formed by a sole shareholder, whereas an Ansvarligt Felag (ANS) and Kommandittfelag (K/F) each require a minimum of two partners by their nature as partnership structures.

Foreign individuals and companies may register an Einkafelag (Sp/F) or Samlagsfelag (P/F) without a residency requirement, though in practice certain director or management appointments may need to satisfy local administrative conditions. A branch office registered under a foreign parent company offers an alternative without creating a separate legal entity.

Conversion between entity types is generally permissible under Faroese corporate law, most commonly from an Einkafelag (Sp/F) to a Samlagsfelag (P/F) as a business scales. The process involves re-registration with Skráseting Føroya and compliance with the capital and governance requirements of the target structure.

The Einkafelag (Sp/F), Samlagsfelag (P/F), and Samvinnufelag each hold separate legal personality distinct from their members. Partnerships such as the Ansvarligt Felag (ANS) and the Kommandittfelag (K/F) do not carry full separate legal personality in the same sense, and general partners remain personally liable for the entity's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.