Key Takeaways

- Estonia's Commercial Code (Äriseadustik) governs all primary business structures, including the Aktsiaselts (AS), Osaühing (OÜ), Täisühing (TÜ), Usaldusühing (UÜ), Tulundusühistu, and Füüsilisest isikust ettevõtja (FIE), each carrying distinct liability, capital, and governance requirements.

- The Osaühing (OÜ) represents the majority of registered entities in Estonia, driven in part by its low capital threshold, single-member eligibility, and compatibility with the e-Residency program for non-resident founders.

- Retained profits are not taxed at the corporate level under Estonia's deferred corporate tax system — the tax liability arises only upon distribution of profits.

- Formation and ongoing statutory filings for all entity types are administered through the Estonian Business Register (Äriregister), managed by the Centre of Registers and Information Systems (RIK), and conducted almost entirely online.

Introduction to Entity Types in Estonia

Estonia is a Northern European sovereign state bordering Latvia to the south and Russia to the east, with a coastline along the Baltic Sea. Understanding the types of business entities in Estonia begins with the Estonian Business Register (Äriregister), administered by the Centre of Registers and Information Systems (RIK), which serves as the central authority for company formation and ongoing statutory filings.

Estonia operates a deferred corporate tax system — retained profits are not taxed at the corporate level, only distributed profits.

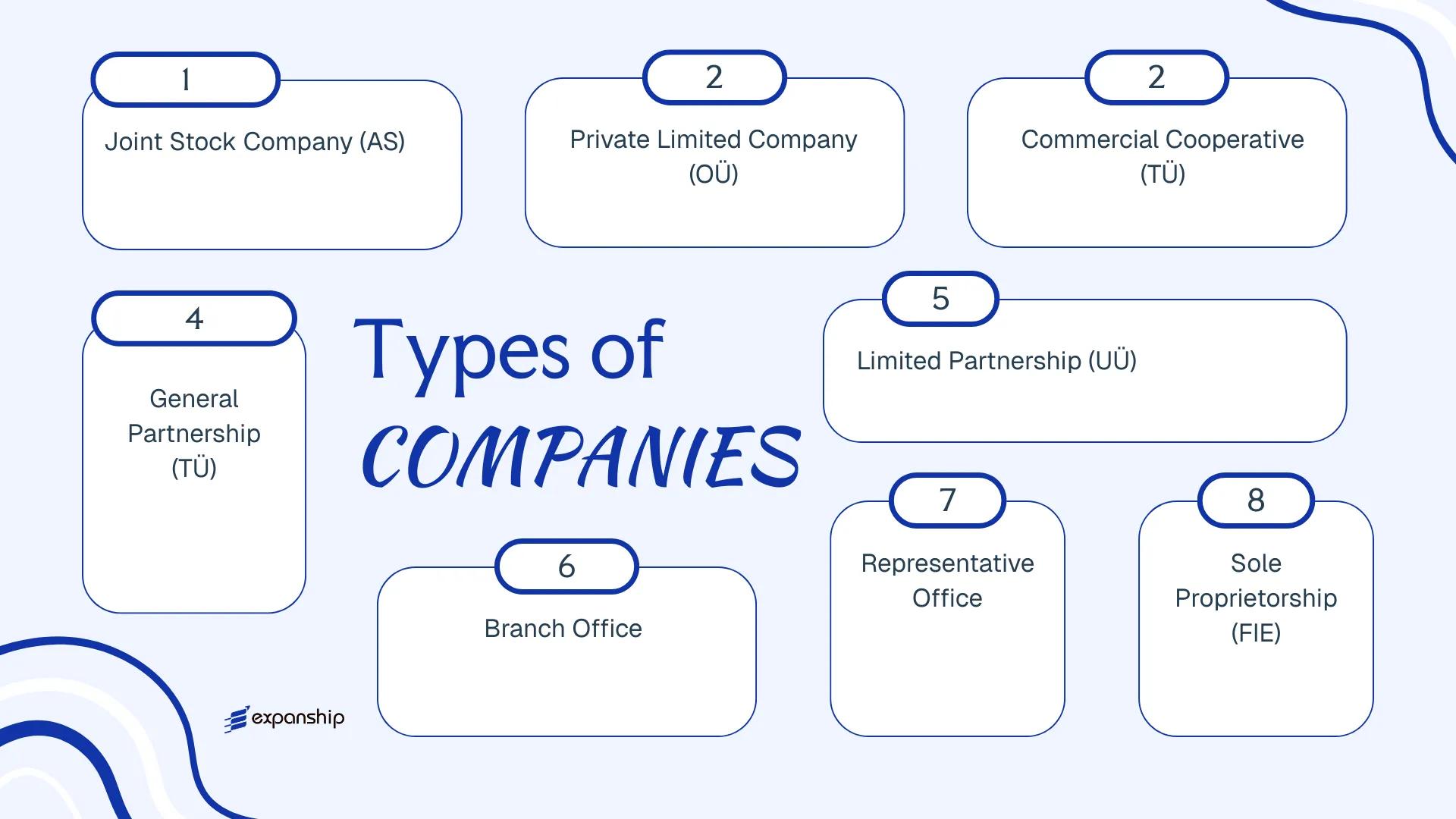

Businesses operating under Estonian law can choose from several legal structures: Aktsiaselts (AS), Osaühing (OÜ), Täisühing (TÜ), Usaldusühing (UÜ), Tulundusühistu, a branch office, a representative office, or a sole proprietorship registered as a Füüsilisest isikust ettevõtja (FIE). Each carries distinct liability rules, capital requirements, and governance obligations under the Commercial Code (Äriseadustik).

This article examines each structure in detail — covering formation requirements, governance, liability exposure, and practical use cases to help your business select the appropriate legal form.

An Overview of Business Structures in Estonia

Under the Äriseadustik (Commercial Code), Estonian company law recognises six primary legal entity types available to resident and non-resident founders. Each form carries distinct rules on liability, governance, and capital requirements. The sections that follow examine each structure individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aktsiaselts (AS) | Joint Stock Company | Limited to shares | Taxed | Yes | 1 shareholder | Estonian Business Register | Äriseadustik |

| Osaühing (OÜ) | Private Limited Company | Limited to capital | Taxed | Yes | 1 shareholder | Estonian Business Register | Äriseadustik |

| Tulundusühistu | Commercial Cooperative | Limited | Taxed | Yes | 3 members | Estonian Business Register | Äriseadustik |

| Täisühing (TÜ) | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Estonian Business Register | Äriseadustik |

| Usaldusühing (UÜ) | Limited Partnership | Mixed liability | Taxed | Yes | 2 partners | Estonian Business Register | Äriseadustik |

| Branch Office | Foreign branch | Parent liable | Taxed | Yes | 1 (parent entity) | Estonian Business Register | Äriseadustik |

| Representative Office | Non-trading presence | Parent liable | Exempt | No | 1 (parent entity) | Estonian Business Register | Äriseadustik |

| FIE | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 individual | Estonian Business Register | Äriseadustik |

Each of these structures is examined in full in the sections below.

Aktsiaselts (AS) – Joint Stock Company

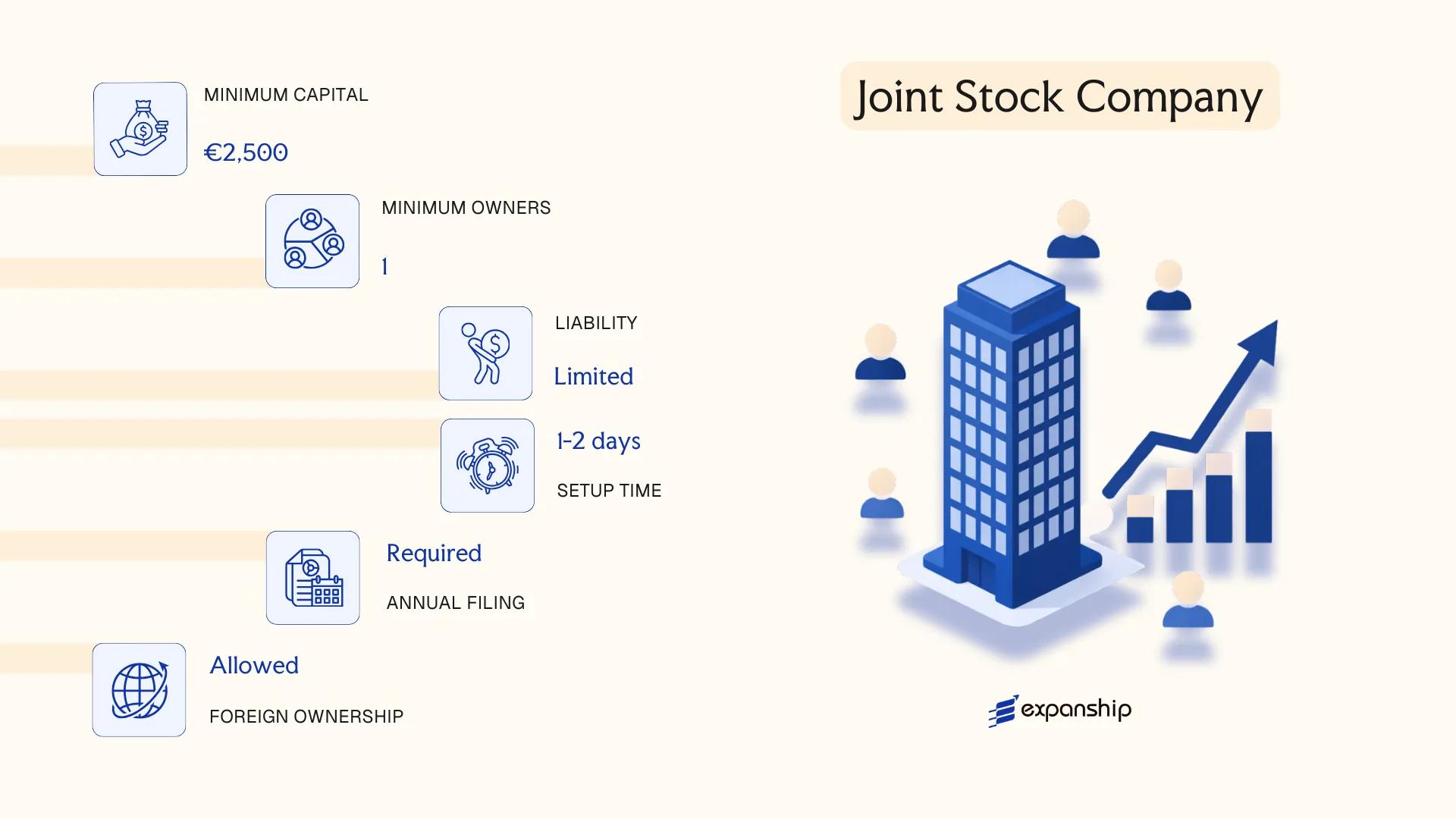

The Aktsiaselts, commonly abbreviated as AS, is Estonia's joint stock company structure and is governed by the Commercial Code (Äriseadustik), which came into force in 1995. It carries full legal personality, meaning the entity exists independently of its shareholders, who bear liability only to the extent of their capital contributions.

Shares in an AS are freely transferable and may be listed on a regulated stock exchange, which distinguishes this structure from Estonia's private limited company. It is used predominantly by larger enterprises, financial institutions, and businesses seeking access to public capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Aktsiaselts / AS) | Separate legal personality; shareholder liability limited to subscribed capital |

| Members | Shareholders (aktsionärid); minimum 1 shareholder, no maximum | Shareholders may be natural persons or legal entities, resident or non-resident |

| Governing Bodies | Supervisory Board (nõukogu) + Management Board (juhatus) | Supervisory Board is mandatory; minimum 3 members on Supervisory Board |

| Local Presence | Registered address in Estonia required | A local registered agent is not mandated by law, but a local address is obligatory |

| Share Capital | Minimum €25,000; must be fully paid before registration | Shares may be registered or bearer shares are not permitted; par value or no-par-value shares allowed |

| Privacy | Shareholders and board members are publicly listed in the Estonian Business Register | No nominee shareholding rules exist, but beneficial ownership is reported to the register |

Focus Points

- Taxation: Corporate income tax applies at 0% on retained earnings; 20% on profit distributions, with a reduced 14% rate on regularly paid dividends; standard VAT rate is 22%; withholding tax of 7% may apply on dividends paid to individuals under the reduced rate mechanism; no stamp duty on share transfers.

- Annual Compliance: Annual report must be filed with the Business Register within six months of the financial year-end; auditor appointment is mandatory if the entity meets two of three statutory thresholds (revenue, assets, headcount).

- Economic Substance: No formal substance test, but Estonian tax residency is determined by place of registration; management and control exercised abroad may trigger foreign tax residency issues.

- Treaty Access: Estonia's tax treaty network covers 60+ jurisdictions; AS entities qualify as residents for treaty purposes under standard residency provisions.

- Conversion: An AS may be converted into an OÜ or another permitted entity type under the Commercial Code's transformation (ümberkujundamine) provisions.

Closing

The AS structure is suited to businesses seeking to raise public capital, operate in regulated financial sectors, or establish a large-scale holding or trading operation where formal governance and share transferability are priorities. The mandatory Supervisory Board adds a layer of administrative overhead that makes this structure disproportionate for most small or mid-sized businesses.

The AS is most appropriate for large enterprises, regulated financial institutions, or businesses planning a public offering or institutional investment round.

Company Incorporation in Estonia

Incorporate an Aktsiaselts or any other Estonian entity type with end-to-end support from registration through compliance.

Osaühing (OÜ) – Private Limited Company

The Osaühing, or OÜ, is the most widely registered business structure in Estonia, governed by the Commercial Code (Äriseadustik), which came into force in 1995. As a separate legal entity, the OÜ carries its own rights and obligations distinct from those of its shareholders, and liability is confined to the company's assets.

Shares in an OÜ are not publicly tradable, which distinguishes it from the joint stock form. Ownership is represented by registered participations (osad) rather than freely transferable shares, and any transfer is subject to the conditions set out in the articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Osaühing) | Separate legal personality; limited liability |

| Members | Shareholders (osanikud): min. 1, no maximum; Directors (juhatuse liige): min. 1 | Shareholders and directors may be the same person; no nationality restrictions |

| Local Presence | Registered address in Estonia required | Must maintain a physical or virtual registered address; a local contact person may be required for service of process |

| Capital | Min. €0.01 (or €2,500 for standard formation); EUR-denominated | Since 2023 amendments, formation without a minimum capital contribution is permitted under simplified procedure |

| Privacy | Shareholders and directors are listed in the public Business Register (Äriregister) | Beneficial ownership must be disclosed to the register |

Focus Points

- Taxation: Subject to Estonia's deferred corporate tax model — retained profits are not taxed; a 22% income tax applies upon distribution; standard VAT rate is 22%; no withholding tax on dividends paid to corporate shareholders in most cases under the Income Tax Act.

- Annual Compliance: Annual report must be filed with the Business Register within six months of the financial year end; failure triggers penalty notices and potential deletion from the register.

- Economic Substance: No formal substance requirements under domestic law, though EU anti-avoidance directives (ATAD) apply; tax residency is determined by place of registration.

- Treaty Access: Estonia has concluded over 60 double tax treaties; OÜ entities qualify as residents for treaty purposes under standard residency criteria.

- Conversion: An OÜ may be converted into an AS, cooperative, or other permitted form under the Commercial Code transformation provisions without dissolution.

Closing

The OÜ suits trading operations, holding structures, and digital service businesses, particularly those using Estonia's e-Residency programme for EU market access. Its simplified capital requirement lowers the formation threshold, though the public disclosure of all shareholders and directors offers limited privacy.

Best suited for entrepreneurs, small-to-medium enterprises, and e-residents seeking an EU-based entity with straightforward formation and a favourable profit-reinvestment tax model.

Tulundusühistu (TÜ) – Commercial Cooperative

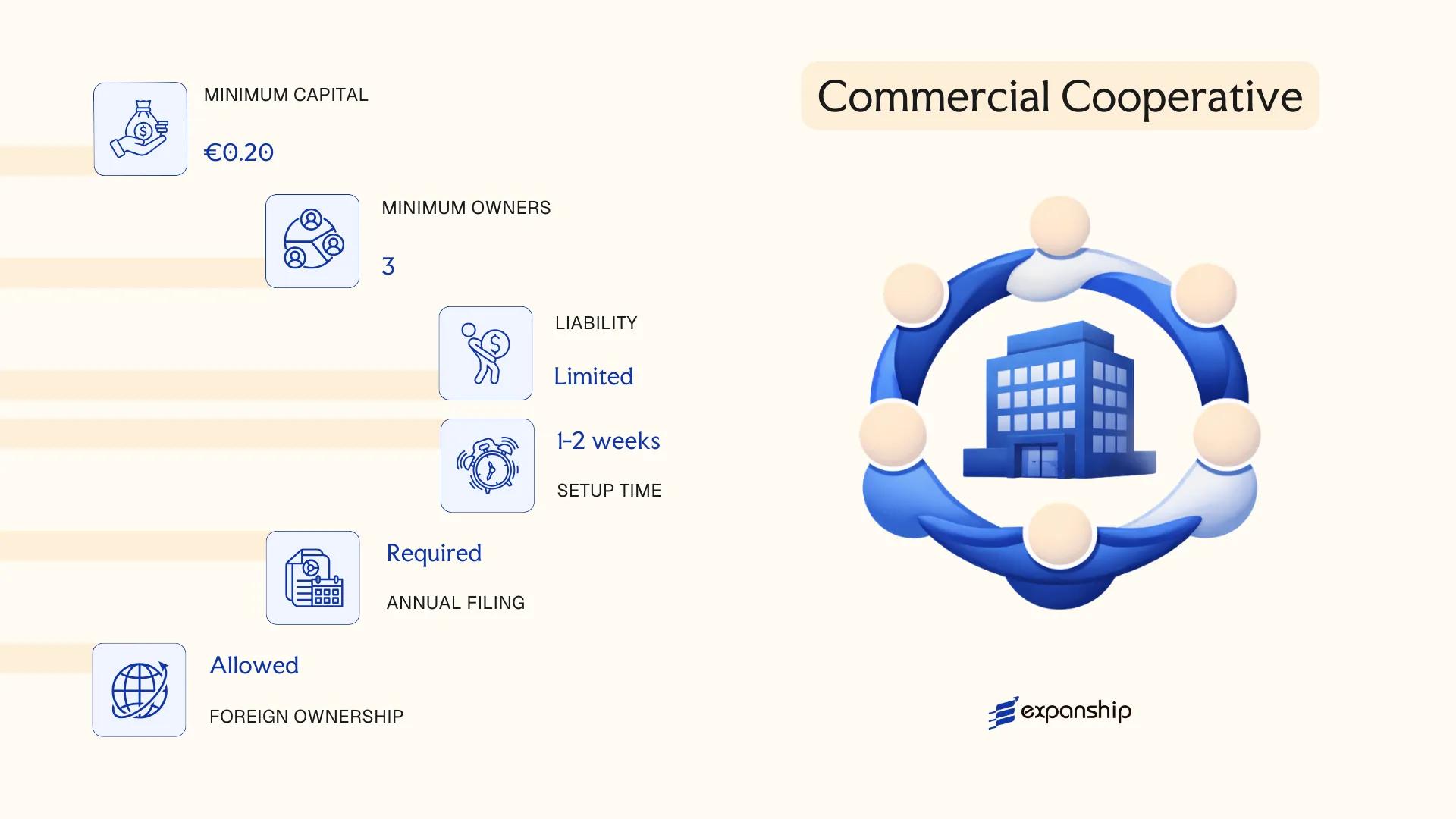

Governed by the Commercial Associations Act (Tulundusühistuseadus), enacted in 2002, the Tulundusühistu commercial cooperative Estonia is a member-owned legal entity designed to serve the economic interests of its members rather than generate profit for external shareholders. It holds separate legal personality, meaning it can enter contracts, own assets, and incur liabilities in its own name.

Liability is limited to members' contributions, though the articles of association may provide for supplementary liability. This hybrid nature — sitting between a capital-based company and an association — makes it structurally distinct from either a private or public limited company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Commercial Cooperative | Separate legal personality; governed by the Commercial Associations Act 2002 |

| Members | Referred to as liikmed (members); minimum 5 natural or legal persons | No statutory maximum; membership is open unless articles restrict it |

| Governing Bodies | Management Board (juhatus) and General Meeting (üldkoosolek); Supervisory Board required if over 200 members | Each member holds one vote regardless of contribution size |

| Local Presence | Registered address in Estonia required | Must be registered with the Estonian Commercial Register (Äriregister) |

| Capital | No statutory minimum share capital; members pay entry fees and membership contributions as defined in articles | Capital structure determined internally |

| Privacy | Directors and members are recorded in the Commercial Register and are publicly accessible | No nominee member arrangements recognised |

Focus Points

- Taxation: Subject to standard Estonian corporate income tax rules; distributed profits taxed at 20/80 rate; VAT registration required if turnover exceeds the statutory threshold; no separate cooperative-specific tax regime applies.

- Annual Compliance: Must file annual reports with the Äriregister; general meeting required at least once per year to approve financial statements.

- Economic Substance: No specific substance test beyond standard registration requirements, but genuine member activity is expected given the cooperative's purpose-driven structure.

- Treaty Access: Qualifies as a resident entity under Estonian law and can access Estonia's tax treaty network, subject to beneficial ownership requirements.

- Restrictions: Cannot issue publicly traded shares; membership rights are generally non-transferable without board or general meeting approval.

Closing

The cooperative structure suits agricultural producers, consumer groups, housing associations, and sector-specific member organisations where collective economic activity is the primary purpose. One clear advantage is the one-member-one-vote governance model, which prevents capital concentration from overriding member interests. The principal limitation is restricted capital-raising capacity, as the entity cannot issue shares to outside investors.

The Tulundusühistu is best suited for groups of five or more individuals or entities seeking to organise shared economic activity under a democratic governance model, rather than for investment-driven or profit-distribution purposes.

Partnerships in Estonia [Täisühing (TÜ) – General Partnership, Usaldusühing (UÜ) – Limited Partnership]

Both the Täisühing (TÜ) and the Usaldusühing (UÜ) are governed by the Commercial Code (Äriseadustik), which came into force in 1995. Unlike capital companies, these structures are built on personal relationships between partners rather than contributed capital.

Each form holds separate legal personality under Estonian law, meaning the partnership itself can own assets, enter contracts, and bear obligations. The distinction between them lies in liability: the Täisühing general partnership exposes all partners to unlimited joint and several liability, while the Usaldusühing UÜ limited partnership introduces a tiered structure with at least one general partner bearing unlimited liability alongside one or more limited partners whose exposure is capped at their contribution. Estonia general and limited partnership registration is processed through the e-Business Register maintained by the Centre of Registers and Information Systems (RIK).

Key Characteristics

| Requirement | Täisühing (TÜ) | Usaldusühing (UÜ) |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership |

| Members | Partners (minimum 2, no statutory maximum); all hold general partner status | Minimum 1 general partner + 1 limited partner; no statutory maximum |

| Liability | Unlimited, joint and several for all partners | General partners: unlimited; limited partners: capped at registered contribution |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered address in Estonia required; no mandatory local director | Registered address in Estonia required; no mandatory local director |

| Management | All general partners entitled to manage and represent by default | Only general partners manage; limited partners excluded from management by default |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits are attributed directly to partners and taxed at their level; the 0% corporate tax on retained earnings does not apply at entity level, and VAT registration is required once taxable turnover exceeds the statutory threshold (currently €40,000 annually).

- Annual Compliance: Partners must file an annual report with RIK; the partnership is subject to the same accounting obligations as capital companies under the Accounting Act (Raamatupidamise seadus).

- Treaty Access: As flow-through entities, treaty benefits depend on the tax residency of the individual partners, not the partnership itself.

- Restrictions: A general partner in either structure cannot, without consent of all partners, conduct competing business activities in the same field.

- Conversion: Both forms may be converted into a capital company (OÜ or AS) through the transformation procedure under the Commercial Code.

Sub-Types

Täisühing (TÜ) – General Partnership

Every partner participates in management and bears full personal liability for the firm's obligations. This structure is used primarily by professional services operators or family-run businesses where all participants take an active role.

Usaldusühing (UÜ) – Limited Partnership

The UÜ separates active management from passive investment. Limited partners contribute capital and share in profits but are legally barred from acting on behalf of the business; if a limited partner acts publicly as a representative, they risk losing limited liability status under the Commercial Code.

Who Uses These Structures

Partnership forms are suited to closely held professional practices or small-scale ventures where the participants know each other and intend to manage the business directly. The absence of a minimum capital requirement lowers the entry threshold, though unlimited liability for general partners remains a material exposure that restricts their appeal for higher-risk commercial activity.

These structures are most appropriate for two or more individuals operating a small professional practice or trade business who are prepared to accept personal liability in exchange for a simple, low-cost legal form.

Foreign Business Presence in Estonia [Branch Office, Representative Office]

A foreign company branch office Estonia is governed primarily by the Commercial Code (Äriseadustik), which sets out registration requirements and operating conditions for non-resident entities. Under this framework, two structures are available: the branch office (filiaal) and the representative office (esindus).

Neither form constitutes a separate legal entity. Both remain extensions of the parent company, which retains full legal responsibility for their activities.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Full commercial operations | Promotional and liaison activities only; no revenue generation |

| Registration | Mandatory with the Estonian Commercial Register | No formal registration requirement |

| Local Contact Person | Required; must be a resident of Estonia or an EEA state | Recommended but not legally mandated |

| Registered Address | Required in Estonia | Required in Estonia |

| Capital Requirement | None | None |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to Estonia's corporate income tax model — tax applies upon profit distribution, not accrual; VAT registration is required if taxable turnover exceeds the €40,000 threshold; withholding tax obligations follow those of the parent jurisdiction.

- Treaty Access: Access to Estonia's tax treaties is generally available through the parent company's residence, not through the branch itself.

- Annual Compliance: Branch offices must submit annual accounts to the Commercial Register; the representative office has no equivalent filing obligation.

- Restrictions: A representative office cannot enter into commercial contracts or generate revenue; any transition to trading activity requires establishing a branch or a locally incorporated entity.

- Conversion: A branch can be converted into a locally incorporated entity, though this requires a new registration process rather than a straightforward reclassification.

Closing

A branch office suits foreign firms testing or expanding into the Estonian market without committing to a locally incorporated structure, though the parent's unlimited liability exposure is a material drawback. The representative office is appropriate only for strictly non-commercial functions such as market research or liaison.

A branch office is best suited for established foreign companies that need operational presence without local incorporation, provided the parent is willing to assume direct legal and financial liability.

Füüsilisest isikust ettevõtja (FIE) – Sole Proprietorship

A FIE sole proprietorship Estonia is the simplest form of business registration available to individuals. Governed by the Commercial Code (Äriseadustik, 1995), the FIE carries no separate legal personality — the proprietor and the business are legally one and the same.

Because there is no separation between personal and business assets, all debts and obligations fall directly on the individual. Registration is handled through the Estonian Commercial Register (Äriregister), administered by the Centre of Registers and Information Systems (RIK).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality from the owner |

| Members | Single natural person (proprietor) | Must be a natural person; legal entities cannot register as FIE |

| Local Presence | Estonian address required | Must maintain a registered address in Estonia |

| Capital | No minimum capital requirement | No share capital; personal assets are directly at risk |

| Privacy | Name and address publicly listed in Äriregister | Limited privacy; full personal details are accessible |

| Liability | Unlimited personal liability | Proprietor's private assets are exposed to business creditors |

Focus Points

- Taxation: Subject to income tax at the standard rate on business income; VAT registration is mandatory once taxable turnover exceeds the statutory threshold; social tax (sotsiaalmaks) applies at 33% on declared business income, with an additional unemployment insurance contribution.

- Annual Compliance: Must submit an annual income tax return to the Estonian Tax and Customs Board (Maksu- ja Tolliamet); no separate annual report is required unlike capital-based entities.

- Economic Substance: The proprietor must conduct activity personally; the FIE status cannot be used as a passive holding structure.

- Conversion: A FIE can convert into an OÜ or other commercial entity under the Commercial Code, though this requires a formal transformation procedure through the Commercial Register.

- Restrictions: A FIE cannot issue shares, bring in equity partners, or transfer the business registration itself — only the assets can be sold.

Closing

The FIE structure suits freelancers, sole traders, and individuals testing a business concept with low initial overhead, though the absence of liability protection makes it unsuitable for activities carrying meaningful financial or legal risk.

Resident individuals conducting small-scale, low-risk self-employed activity who do not require liability separation or external investment.

How to Choose the Right Entity Type in Estonia

Selecting the correct structure from the outset shapes your tax position, liability exposure, and administrative burden for the life of your business. Knowing how to choose the right company type in Estonia requires examining several concrete variables before filing anything with the Äriregister (Estonian Commercial Register).

Why Your Entity Choice Matters

Misalignment between your chosen structure and your actual operations produces specific, avoidable consequences:

- Choosing an OÜ or AS when your operations generate no Estonian-source income but require local transaction capacity may expose you to unnecessary corporate compliance obligations under the Commercial Code (äriseadustik).

- Selecting an entity without access to Estonia's tax treaty network — such as certain cooperative structures — means withholding tax reductions available under bilateral agreements cannot be claimed by your business.

- Forming a general partnership (täisühing) when limited liability is operationally necessary leaves partners with unlimited personal exposure to business debts.

- Registering as a FIE when your revenue exceeds the thresholds that trigger mandatory social tax and income tax obligations creates a disproportionate personal tax burden compared to operating through an OÜ.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward a different structure — an AS is required for financial sector licensing, while an OÜ suits most commercial operations.

- Ownership and Management: A sole founder with no plans for external investors can operate efficiently as an OÜ with a single-member board, whereas multi-investor arrangements may warrant the shareholder governance framework of an AS.

- Tax Objectives: Estonia's 0% corporate tax on retained earnings applies to both OÜ and AS, but your need for treaty access, VAT registration, or eligibility under specific regimes should determine which entity fits.

- Substance Capacity: If you cannot maintain a physical presence, designated decision-making, or resident management, structures requiring demonstrated local substance will create reporting risk.

- Exit Strategy: Not all entity types permit redomiciliation or conversion under the äriseadustik — confirm your chosen structure supports your intended exit mechanism before registration.

- Privacy Requirements: Director and shareholder details are publicly accessible through the Äriregister, so assess whether nominee arrangements are necessary for your situation.

Compliance Services for Companies in Estonia

Maintain your Estonian entity's good standing with ongoing compliance support, including annual reporting, statutory filings, and regulatory obligations.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a company in Estonia guide. Each entity type serves a distinct purpose: the Osaühing suits most small to mid-sized ventures due to its low capital threshold and single-member eligibility; the Aktsiaselts addresses larger firms requiring public share issuance or institutional investment; partnerships accommodate businesses built around personal liability arrangements; cooperatives serve member-driven commercial activity; and the FIE remains the simplest entry point for individual traders operating under personal liability.

The OÜ accounts for the clear majority of registered entities, a pattern consistent with Estonia's e-Residency program attracting non-resident founders. Regulatory direction has continued toward digital-first administration, with the Commercial Register and the e-Business Register maintaining Estonia's position as a jurisdiction where formation and ongoing compliance are managed almost entirely online. Expanship's team works directly within these systems on behalf of clients.

How Expanship Can Assist You

Expanship's company incorporation services in Estonia cover the full process, from selecting the right entity under the Commercial Code (Äriseadustik) to registering your business with the Estonian Commercial Register (Äriregister). Whether you are forming an Osaühing, an Aktsiaselts, or establishing a branch of a foreign entity, our team works with the specific requirements each structure carries.

From initial document preparation through to ongoing compliance, our Estonia corporate services include:

- Document preparation and notarization for Commercial Register filings

- Registered address and contact person provision

- Liaison with the Äriregister and other relevant authorities

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance for both resident and e-Resident shareholders

Get in touch with Expanship Estonia to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Osaühing (OÜ) is by far the most frequently registered business structure, largely because it requires a minimum share capital of just €2,500 and permits a single shareholder to act simultaneously as the sole director. Its registration through the e-Business Register can be completed within one business day when using Estonia's e-Residency infrastructure.

Both structures carry separate legal personality and limited liability under the Commercial Code (äriseadustik), but the AS requires a minimum share capital of €25,000 and is subject to more stringent disclosure and governance requirements, including a mandatory supervisory board in certain configurations. An OÜ is generally suited to smaller, closely held operations, while an AS is typically used for larger enterprises or those seeking public investment.

Among registered entities, the OÜ imposes fewer mandatory disclosure requirements compared to the AS, though beneficial ownership information must still be submitted to the Estonian commercial register under anti-money laundering obligations. Nominee shareholder arrangements are legally permissible, but nominee directors are less standard in practice. The AS requires broader public disclosure of financial statements.

A sole individual can establish an OÜ, AS, or register as a FIE (sole proprietor). A Täisühing (general partnership) and Usaldusühing (limited partnership) each require at least two partners by statutory definition under the Commercial Code. The Tulundusühistu (commercial cooperative) requires a minimum of two founding members.

All major entity types, including the OÜ and AS, are open to non-resident founders without a requirement for local shareholding or a resident director. Estonia's e-Residency programme allows foreign nationals to establish and manage an OÜ entirely remotely using a government-issued digital identity. Registration is handled through the e-Business Register, administered by the Centre of Registers and Information Systems (RIK).

The Commercial Code permits the transformation (ümberkujundamine) of one entity type into another, including conversion of an OÜ to an AS or vice versa, without dissolving the original entity. The process requires a transformation plan, shareholder resolution, and re-registration with the commercial register. Not all conversions are available in every direction; partnership-to-capital-company transformations are subject to additional procedural requirements.

The OÜ, AS, and Tulundusühistu each hold separate legal personality distinct from their members. General partnerships (Täisühing) and limited partnerships (Usaldusühing) also have legal personality under Estonian law, though general partners in a Täisühing bear unlimited personal liability for the entity's obligations. The FIE has no separate legal personality; the individual and the business are legally the same person.

The FIE has the lightest administrative burden, with no annual report filed to the commercial register and no requirement to maintain a separate legal structure. That said, a FIE provides no liability protection, which makes it unsuitable for activities carrying significant financial or legal risk. Among capital companies, the OÜ generally involves fewer governance formalities than the AS.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.