Key Takeaways

- The GmbH is Germany's most widely registered entity, offering limited liability without the capital intensity or governance requirements of an AG.

- Entity registration in Germany is processed through the Handelsregister, maintained by local courts (Amtsgerichte) under state (Land) authority, with additional registration often required at the Finanzamt or Gewerbeamt depending on legal form.

- Governed by the Handelsgesetzbuch (HGB) and form-specific statutes, Germany's legal entity options span capital companies (AG, GmbH, UG, KGaA), partnerships (OHG, KG, GbR, PartG), foreign establishment forms, and sole proprietorships.

- Partnership structures such as the OHG, KG, and GbR carry personal liability implications that restrict their suitability to closely held professional or trading arrangements rather than ventures requiring broader investor participation.

Introduction to Entity Types in Germany

Germany is a federal republic in Central Europe, bordered by nine countries including France, Poland, and the Netherlands. As one of the largest economies in the European Union, it operates a territorial-based tax system with an extensive network of double tax treaties.

Company registration is handled through the Handelsregister, the official commercial register maintained by local courts (Amtsgerichte) under the oversight of the respective state (Land) authorities. Depending on the legal form, your business may also need to register with the tax office (Finanzamt) and, in some cases, the trade office (Gewerbeamt).

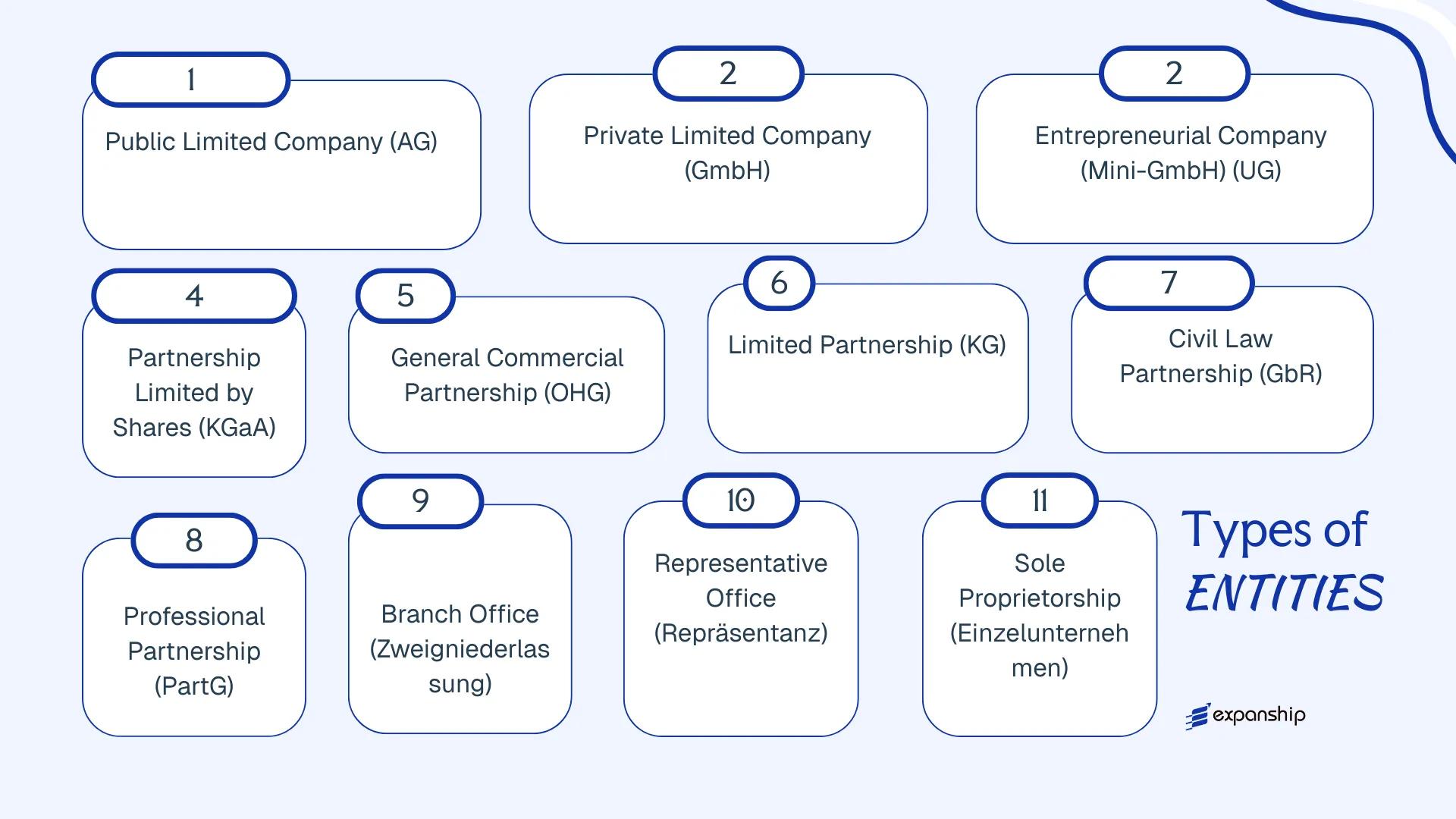

The types of business entities in Germany span a range of corporate structures — from capital companies to partnerships and foreign establishment forms. Available legal entity types include the AG, GmbH, UG, KGaA, OHG, KG, GbR, PartG, Einzelunternehmen, Zweigniederlassung, and Repräsentanz.

Each form carries distinct requirements around minimum capital, liability, governance, and registration procedure. This article covers each one in detail.

An Overview of Business Structures in Germany

German company law provides several distinct entity types, each governed primarily by the Handelsgesetzbuch (HGB), the GmbH-Gesetz, the Aktiengesetz (AktG), and the Partnerschaftsgesellschaftsgesetz (PartGG). Each form carries a different liability profile, capital requirement, and governance structure suited to a specific commercial purpose.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| AG | Public limited company | Limited to share capital | Taxable | Yes | 1 shareholder | Handelsregister | Aktiengesetz |

| GmbH | Private limited company | Limited to share capital | Taxable | Yes | 1 shareholder | Handelsregister | GmbH-Gesetz |

| UG | Mini private limited company | Limited to share capital | Taxable | Yes | 1 shareholder | Handelsregister | GmbH-Gesetz |

| KGaA | Partnership limited by shares | Mixed: general/limited | Taxable | Yes | 1 general partner | Handelsregister | Aktiengesetz |

| OHG | General commercial partnership | Unlimited, joint | Taxable | Yes | 2 partners | Handelsregister | HGB |

| KG | Limited partnership | Mixed: general/limited | Taxable | Yes | 2 partners | Handelsregister | HGB |

| GbR | Civil law partnership | Unlimited, joint | Taxable | Yes | 2 partners | None (unregistered) | BGB |

| PartG | Professional partnership | Unlimited or limited | Taxable | Yes | 2 partners | Partnerschaftsregister | PartGG |

| Branch Office | Zweigniederlassung | Parent bears liability | Taxable | Yes | Parent company | Handelsregister | HGB |

| Representative Office | Repräsentanz | Parent bears liability | Limited tax nexus | Restricted | Parent company | Local trade office | HGB |

| Einzelunternehmen | Sole proprietorship | Unlimited, personal | Taxable | Yes | 1 individual | Handelsregister / Gewerbeamt | HGB |

Each of these structures is examined in full in the sections below.

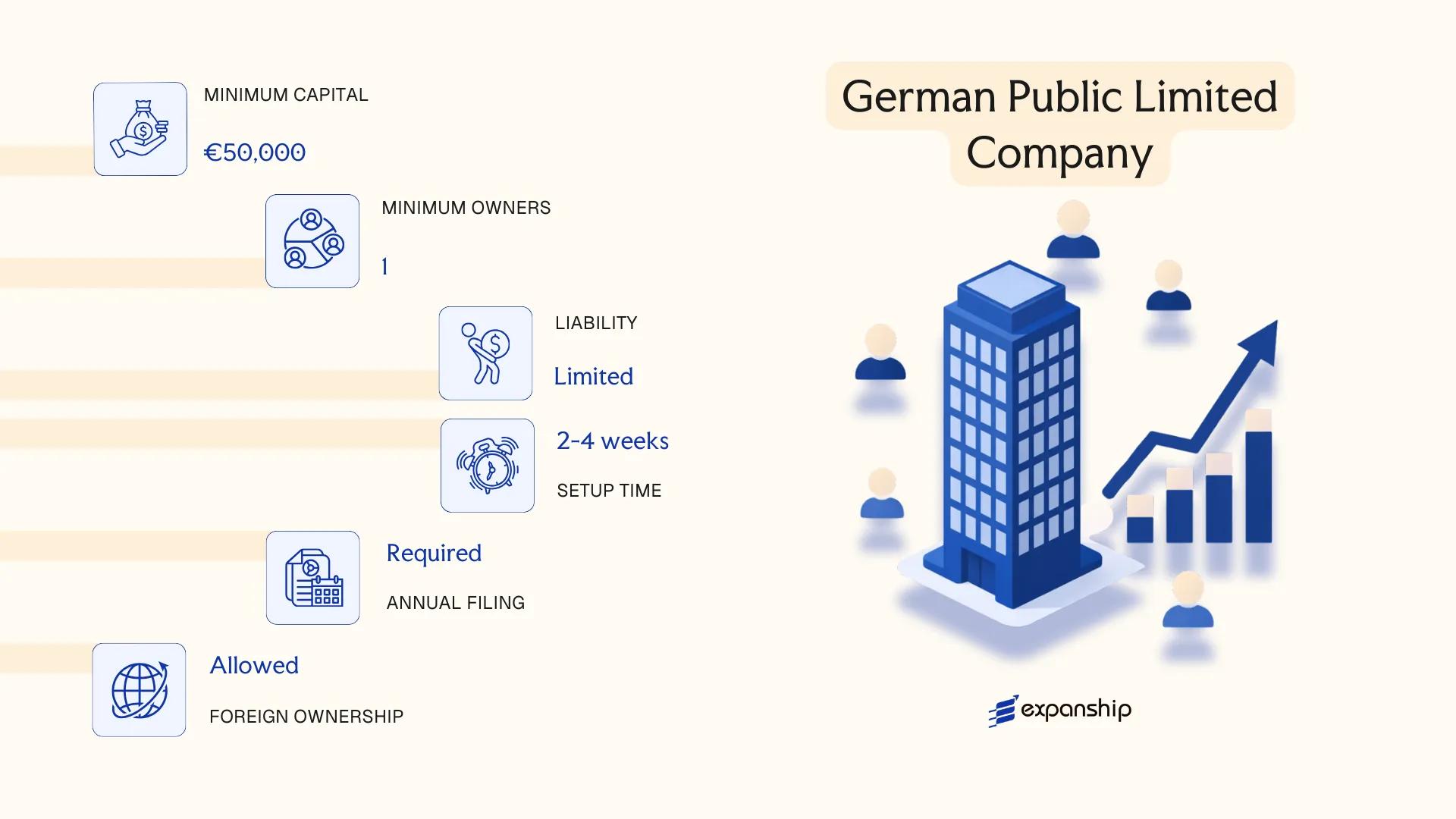

Aktiengesellschaft (AG) – German Public Limited Company

Governed by the Aktiengesetz (AktG) of 1965, the Aktiengesellschaft is a separate legal entity in which shareholders bear no personal liability beyond their capital contribution. Aktiengesellschaft AG Germany formation suits businesses seeking access to public capital markets or requiring a structure recognisable to institutional investors.

Share capital is divided into transferable shares, and ownership is entirely distinct from management. The supervisory board (Aufsichtsrat) oversees the management board (Vorstand), creating a mandatory two-tier governance structure under the AktG.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Aktiengesellschaft (AG) | Separate legal personality; limited liability for shareholders |

| Members | Shareholders (Aktionäre): minimum 1; no maximum. Management Board (Vorstand): min. 1 member. Supervisory Board (Aufsichtsrat): min. 3 members | Supervisory Board mandatory; employee co-determination may apply in larger firms |

| Local Presence | Registered office (Sitz) in Germany required; no mandatory resident director, but Vorstand must be operationally accountable | Registered address must appear in commercial register (Handelsregister) |

| Share Capital | EUR 50,000 minimum; at least 25% paid up at incorporation | Capital divided into named-value (Nennbetragsaktien) or no-par shares (Stückaktien) |

| Privacy | Shareholder names not publicly disclosed; Vorstand members listed in Handelsregister | Beneficial ownership reported to Transparenzregister |

Focus Points

- Taxation: Subject to corporate income tax at 15% plus solidarity surcharge (5.5% thereof), trade tax (Gewerbesteuer) varying by municipality, and 19% standard VAT; dividend distributions attract 25% withholding tax (reduced under applicable tax treaties or the EU Parent-Subsidiary Directive).

- Annual Compliance: Mandatory annual financial statements prepared under HGB or IFRS (for listed entities), filed with the Bundesanzeiger; annual general meeting (Hauptversammlung) required each fiscal year.

- Treaty Access: Qualifies as a resident company under German tax law, granting full access to Germany's extensive double tax treaty network (90+ treaties).

- Conversion: Can be converted into a GmbH or KGaA under the Umwandlungsgesetz (UmwG) without liquidation.

- Public Listing: Shares may be listed on regulated markets such as the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse); listing triggers additional BaFin (Federal Financial Supervisory Authority) disclosure obligations.

Closing

The AG is used primarily for large trading companies, holding structures, and businesses intending to raise equity from external investors or pursue a public listing. The ability to issue freely transferable shares to an unlimited number of investors is a structural advantage, though the mandatory two-tier board and minimum capital threshold of EUR 50,000 make it disproportionate for small or early-stage operations.

The AG is most appropriate for established businesses planning public capital raising, institutional investment, or cross-border expansion requiring a recognised, credible corporate form.

Company Incorporation in Germany

Set up your German Aktiengesellschaft or other entity with end-to-end support from Expanship's corporate specialists.

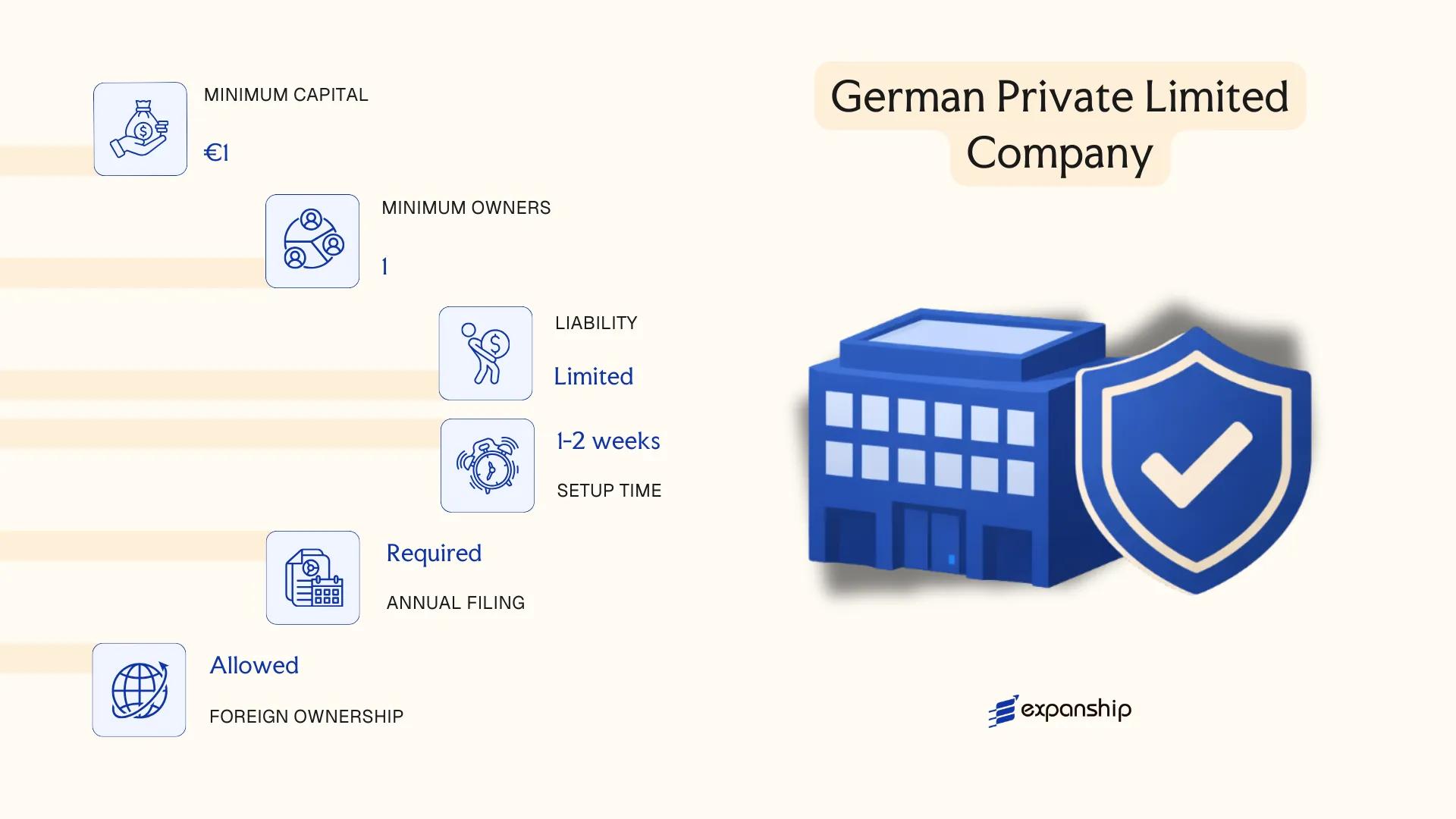

Gesellschaft mit beschränkter Haftung (GmbH) – German Private Limited Company

Governed by the Gesetz betreffend die Gesellschaften mit beschränkter Haftung (GmbHG) of 1892, the GmbH is the most widely used corporate form in Germany. Meeting GmbH Germany registration requirements grants the entity full separate legal personality, meaning the company holds assets, enters contracts, and incurs liabilities in its own name.

Shareholders bear no personal liability beyond their capital contributions. This hybrid nature — combining corporate limited liability with relatively flexible internal governance — makes the structure suitable across a broad range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Gesellschaft mit beschränkter Haftung (GmbH) | Private limited company; not publicly traded |

| Members | Shareholders (Gesellschafter); min. 1, no statutory maximum | Single-shareholder GmbH is permitted |

| Management | Managing Director (Geschäftsführer); min. 1, no maximum | Need not be a German resident or national |

| Local Presence | Registered office (Sitz) required within Germany | Must be registered with the local Handelsregister (commercial register) |

| Share Capital | EUR 25,000 minimum; at least 50% paid up at formation | Gesellschaft mit beschränkter Haftung formation requires notarial deed |

| Privacy | Shareholder names filed with Handelsregister; publicly searchable | Beneficial ownership reported to Transparenzregister |

Focus Points

- Taxation: Subject to corporate income tax (15%), solidarity surcharge (5.5% thereof), and trade tax (Gewerbesteuer, rate varies by municipality); VAT registration required for taxable supplies; withholding tax applies to dividend distributions to foreign shareholders, subject to EU Parent-Subsidiary Directive or applicable tax treaty reduction.

- Annual Compliance: Annual financial statements must be prepared under HGB (Handelsgesetzbuch) and filed with the Bundesanzeiger; audit requirements apply once two of three size thresholds are exceeded.

- Conversion: A GmbH can be converted into an AG or UG under the Umwandlungsgesetz (UmwG) without dissolving the entity.

- Treaty Access: As a resident entity, the GmbH accesses Germany's extensive double tax treaty network and EU directives.

- Share Transfer: Transfers of GmbH shares require notarial certification; no free transferability as with publicly listed shares.

Closing

The GmbH suits trading operations, holding structures, and IP ownership vehicles where limited liability and operational control are both required. Its main constraint is the EUR 25,000 minimum capital requirement, which creates an upfront financial commitment not present in all comparable European private company forms.

The GmbH is well suited to foreign investors and established businesses seeking a fully recognized, liability-protected operating entity in Germany.

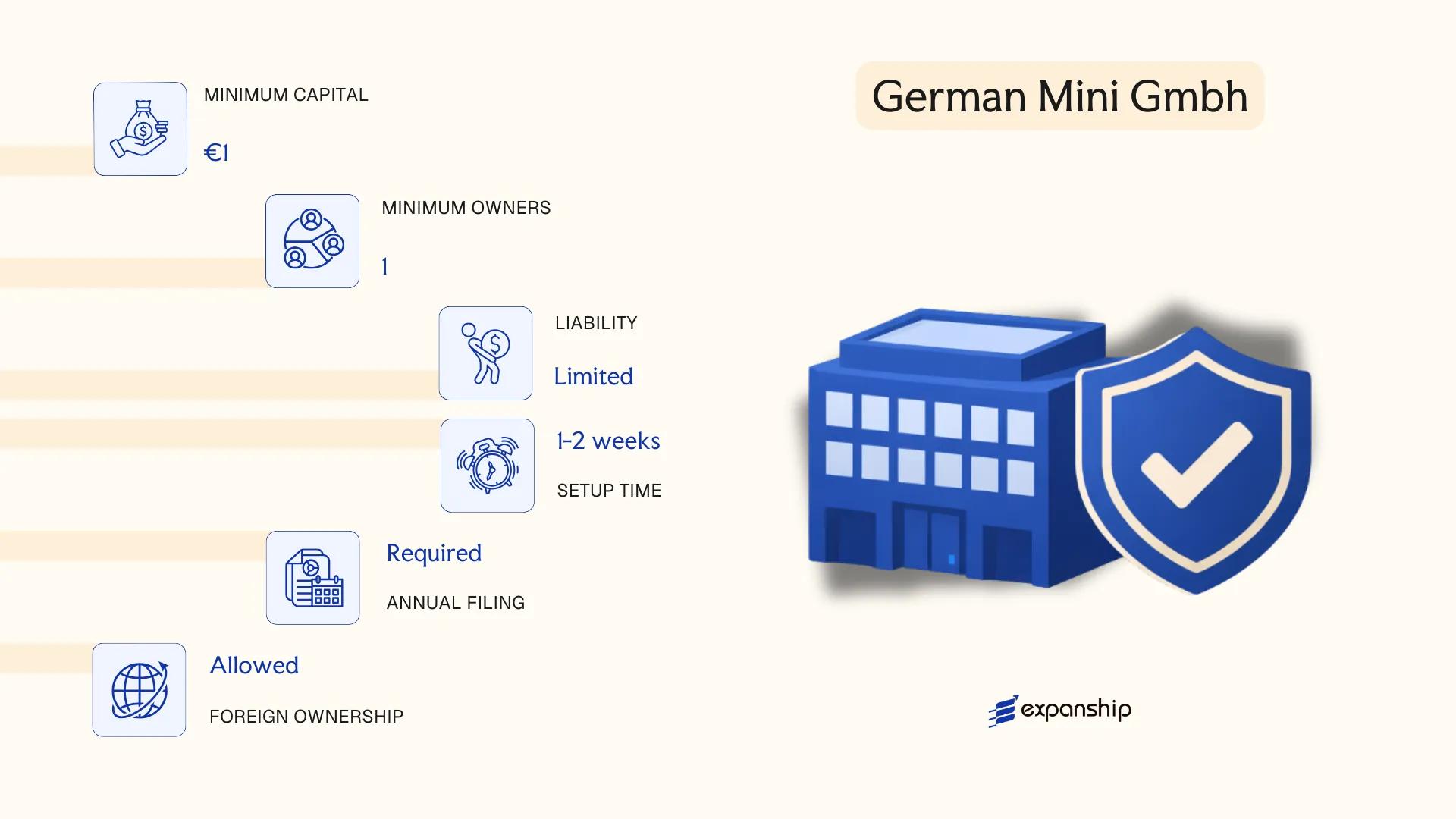

Unternehmergesellschaft (UG) – German Mini-GmbH

Introduced through the MoMiG reform of 2008 as an amendment to the GmbH-Gesetz (GmbHG), the Unternehmergesellschaft haftungsbeschränkt is a capital company with full separate legal personality and limited liability for its shareholders. It was designed specifically to lower the barrier for UG Unternehmergesellschaft Germany setup by allowing formation with a minimum share capital of just €1.

Structurally, the UG operates under the same GmbHG framework as the GmbH, making it a variant rather than a distinct legal form. One defining statutory obligation is the mandatory reserve accumulation: the entity must retain 25% of its annual net profit until the share capital reaches €25,000, at which point conversion to a full GmbH becomes possible under §5a GmbHG.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Kapitalgesellschaft (capital company) | Variant of GmbH under §5a GmbHG |

| Members | Shareholders (Gesellschafter) | Minimum 1, no maximum; managed by at least 1 Geschäftsführer (managing director) |

| Capital | Minimum €1; currency EUR | Must accumulate 25% of annual net profit as statutory reserve until €25,000 is reached |

| Local Presence | Registered office (Sitz) in Germany required | No mandatory resident director, but a German business address is required for registration |

| Privacy | Shareholder and director details filed with Handelsregister | Publicly accessible via the commercial register |

Focus Points

- Taxation: Subject to corporate income tax (Körperschaftsteuer) at 15% plus solidarity surcharge, trade tax (Gewerbesteuer) at varying municipal rates, and VAT (Umsatzsteuer) at the standard 19% rate; withholding tax applies to dividend distributions.

- Annual Compliance: Must file financial statements with the Bundesanzeiger and submit annual tax returns; small entities qualify for simplified disclosure under HGB size thresholds.

- Reserve Obligation: Statutory profit retention of 25% annually is mandatory until share capital reaches €25,000, restricting full profit distribution in early years.

- Conversion: May convert to a full GmbH once capital reaches €25,000, through a notarised amendment to the articles of association (Gesellschaftsvertrag).

- Treaty Access: As a German tax-resident entity, the UG qualifies for Germany's extensive double tax treaty network, provided substance requirements are met.

Closing

The UG suits early-stage ventures, freelancers, and small businesses that require limited liability without the capital commitment of a GmbH. The minimal entry capital is a clear advantage; the mandatory reserve accumulation limits dividend flexibility until the €25,000 threshold is met.

Founders and early-stage entrepreneurs seeking limited liability at minimal upfront capital cost, with a clear path to upgrading to a full GmbH.

Kommanditgesellschaft auf Aktien (KGaA) – Partnership Limited by Shares

The KGaA partnership limited by shares Germany is a hybrid corporate form regulated under Sections 278–290 of the Aktiengesetz (AktG) 1965, supplemented where applicable by general partnership provisions under the Handelsgesetzbuch (HGB). It carries separate legal personality and combines two distinct member classes: at least one general partner (Komplementär) with unlimited personal liability, and shareholders (Kommanditaktionäre) whose exposure is capped at their share capital contribution.

Structurally, the entity issues registered shares and must appoint a supervisory board (Aufsichtsrat), yet management authority rests solely with the general partner rather than a conventionally elected board of directors. This arrangement gives the controlling partner operational autonomy that an AG structure would not permit.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Hybrid – corporation and partnership | Governed by AktG §§278–290 and HGB partnership rules |

| Members | Min. 1 Komplementär (general partner, unlimited liability) + min. 1 Kommanditaktionär (shareholder) | No statutory maximum on shareholders; Komplementär may be a legal entity |

| Management | Komplementär manages exclusively | Shareholders cannot override management decisions |

| Local Presence | Registered office (Sitz) in Germany required | No mandatory local director, but Komplementär must be identifiable |

| Share Capital | Minimum €50,000; divided into shares | Same threshold as the AG; at least 25% paid up on registration |

| Privacy | Komplementär disclosed in Handelsregister | Shareholder register is not fully public for non-listed KGaAs |

Focus Points

- Taxation: Subject to corporate income tax (15%), solidarity surcharge (5.5% thereof), and trade tax (Gewerbesteuer) at municipal rates; VAT obligations apply at the standard 19% rate; dividends distributed to non-resident shareholders may attract withholding tax, reducible under applicable double tax treaties.

- Annual Compliance: Annual financial statements must be prepared under HGB; listed KGaAs apply IFRS; filing with the Bundesanzeiger (Federal Gazette) is mandatory.

- Economic Substance: The Komplementär must exercise genuine management functions from the registered seat to sustain the structural integrity of the form.

- Conversion: Conversion to an AG or GmbH is possible under the Umwandlungsgesetz (UmwG), subject to shareholder resolution and court registration.

- Restrictions: Foreign nationals may act as Komplementär, but if the general partner is a GmbH or AG, that entity's own registration requirements apply in parallel.

Closing

The KGaA suits family-controlled or founder-led businesses that require access to public capital markets while preserving concentrated management authority in the hands of one controlling partner. The primary limitation is structural complexity: maintaining dual governance layers and a supervisory board increases administrative overhead relative to most other German entity forms.

The KGaA is most appropriate for established businesses or dynastic family groups seeking exchange-listed capital-raising capacity without diluting operational control.

Partnerships in Germany [Offene Handelsgesellschaft (OHG), Kommanditgesellschaft (KG), Gesellschaft bürgerlichen Rechts (GbR), Partnerschaftsgesellschaft (PartG)]

German partnership types OHG KG GbR are each governed by distinct provisions within the Handelsgesetzbuch (HGB) of 1897 and the Bürgerliches Gesetzbuch (BGB) of 1896. Unlike capital companies, most partnerships lack separate legal personality in the full corporate sense, though the GbR gained partial legal capacity recognition through the Personengesellschaftsrechtsmodernisierungsgesetz (MoPeG) reform effective January 2024.

Liability exposure varies significantly across these structures. The OHG and GbR impose unlimited joint and several liability on all partners, while the KG splits partners into two distinct classes with differing liability profiles. The Partnerschaftsgesellschaft (PartG), regulated under the Partnerschaftsgesellschaftsgesetz (PartGG) of 1994, is reserved exclusively for members of recognised liberal professions.

Key Characteristics

| Requirement | OHG | KG | GbR | PartG |

|---|---|---|---|---|

| Legal Form | Commercial partnership | Limited partnership | Civil law partnership | Professional partnership |

| Members Referred As | Partners (Gesellschafter) | General partner (Komplementär) + limited partner (Kommanditist) | Partners (Gesellschafter) | Partners (Partner) |

| Minimum Members | 2 partners | 1 general + 1 limited partner | 2 partners | 2 partners (licensed professionals only) |

| Liability | All partners: unlimited | General partner: unlimited; Limited partner: capped at registered contribution | All partners: unlimited (joint and several) | Partners: unlimited; PartGmbB variant limits professional liability |

| Registration | Handelsregister (HGB §106) | Handelsregister (HGB §162) | Gesellschaftsregister (post-MoPeG 2024) | Partnerschaftsregister |

| Minimum Capital | None | None | None | None |

Focus Points

- Taxation: Partnerships are tax-transparent; profits flow through to individual partners and are subject to personal income tax (Einkommensteuer) or corporate tax depending on partner type; trade tax (Gewerbesteuer) applies at entity level; VAT registration required when thresholds are met; no withholding tax on profit distributions as such.

- Annual Compliance: OHG and KG must file annual financial statements with the Handelsregister; GbR obligations depend on whether it is registered; PartG filing requirements align with HGB provisions.

- Treaty Access: Partnerships themselves generally do not access double tax treaties directly; treaty benefits depend on the residence and status of the individual partners.

- Conversion: A GbR conducting commercial activity must convert to an OHG or KG once it meets the threshold for commercial operations under HGB §1.

- Restrictions: PartG membership is restricted to natural persons holding a recognised professional qualification; corporate partners are not permitted.

Sub-Types

Kommanditgesellschaft auf Aktien (KGaA)

Covered separately in this guide as a hybrid capital structure; not a pure partnership form.

GmbH & Co. KG

A widely used structural variant of the KG where a GmbH serves as the sole general partner. This arrangement limits the unlimited liability exposure that would otherwise attach to a natural person acting as Komplementär, making it common for family businesses and mid-sized commercial operations.

Partnerschaftsgesellschaft mit beschränkter Berufshaftung (PartGmbB)

Introduced by amendment to the PartGG in 2013, this variant caps professional liability to the firm's assets when adequate professional indemnity insurance is maintained, distinguishing it from the standard PartG where partners remain personally exposed.

Partnerships suit structures where pass-through taxation is preferred and where partners are willing to accept personal liability, as in family-run trading or professional services operations. The primary advantage is the absence of minimum capital requirements; the main limitation is the unlimited personal liability carried by at least one partner in every form except the PartGmbB.

Partnerships in Germany are most appropriate for closely held commercial ventures, family businesses, and licensed professionals seeking a flexible structure without the administrative overhead of a capital company.

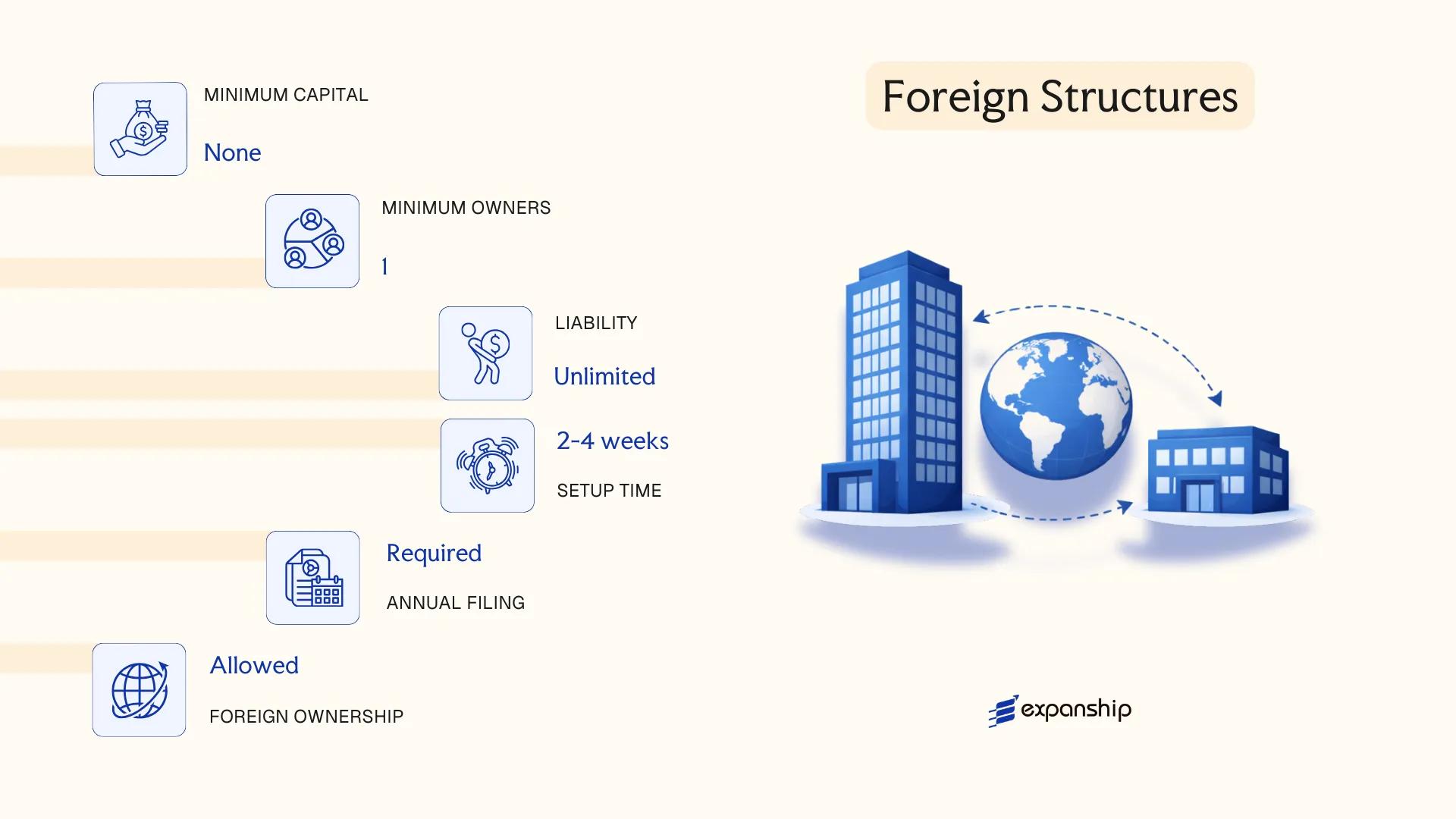

Foreign Structures in Germany [Branch Office (Zweigniederlassung), Representative Office (Repräsentanz)]

Foreign companies seeking a presence without incorporating a new legal entity have two primary options: the foreign branch office Germany (Zweigniederlassung) and the representative office (Repräsentanz). A Zweigniederlassung is not a separate legal entity — it remains an extension of the parent company, which bears full liability for its activities.

Registration of a Zweigniederlassung is governed by the Handelsgesetzbuch (HGB) and requires filing with the local Handelsregister (Commercial Register). The Repräsentanz, by contrast, operates informally with no statutory registration framework, restricting it to liaison and promotional functions only.

Key Characteristics

| Requirement | Zweigniederlassung (Branch) | Repräsentanz (Rep. Office) |

|---|---|---|

| Legal Personality | None – extension of parent | None – extension of parent |

| Liability | Parent bears full liability | Parent bears full liability |

| Registration | Mandatory – Handelsregister | Not required |

| Local Representative | Authorised signatory required | No formal requirement |

| Business Activity | Permitted | Not permitted – liaison only |

| Privacy | Directors/signatories disclosed publicly | No public disclosure |

Focus Points

- Taxation: A Zweigniederlassung is subject to German corporate income tax (15% plus solidarity surcharge) and trade tax (Gewerbesteuer) on locally attributable profits; VAT registration is required if taxable supplies are made. The Repräsentanz generally creates no taxable presence if confined to preparatory activities.

- Permanent Establishment Risk: A Repräsentanz may inadvertently constitute a permanent establishment under German tax law or applicable double tax treaties if it exceeds permitted activities.

- Annual Compliance: The Zweigniederlassung must file annual accounts of the parent with the Handelsregister and maintain German-language documentation.

- Treaty Access: Branch profits may be subject to withholding tax on remittances depending on the applicable double taxation agreement between Germany and the parent's home jurisdiction.

- Conversion: A Zweigniederlassung can be converted into a fully incorporated entity such as a GmbH, though this requires a separate incorporation process rather than a direct statutory conversion.

Closing

A Zweigniederlassung suits foreign companies testing the German market or executing specific contracts, while a Repräsentanz serves only pre-commercial purposes such as market research. The branch avoids full incorporation costs but exposes the parent to unlimited liability for all German operations.

Best suited for established foreign businesses requiring a transitional or limited operational footprint before committing to full local incorporation.

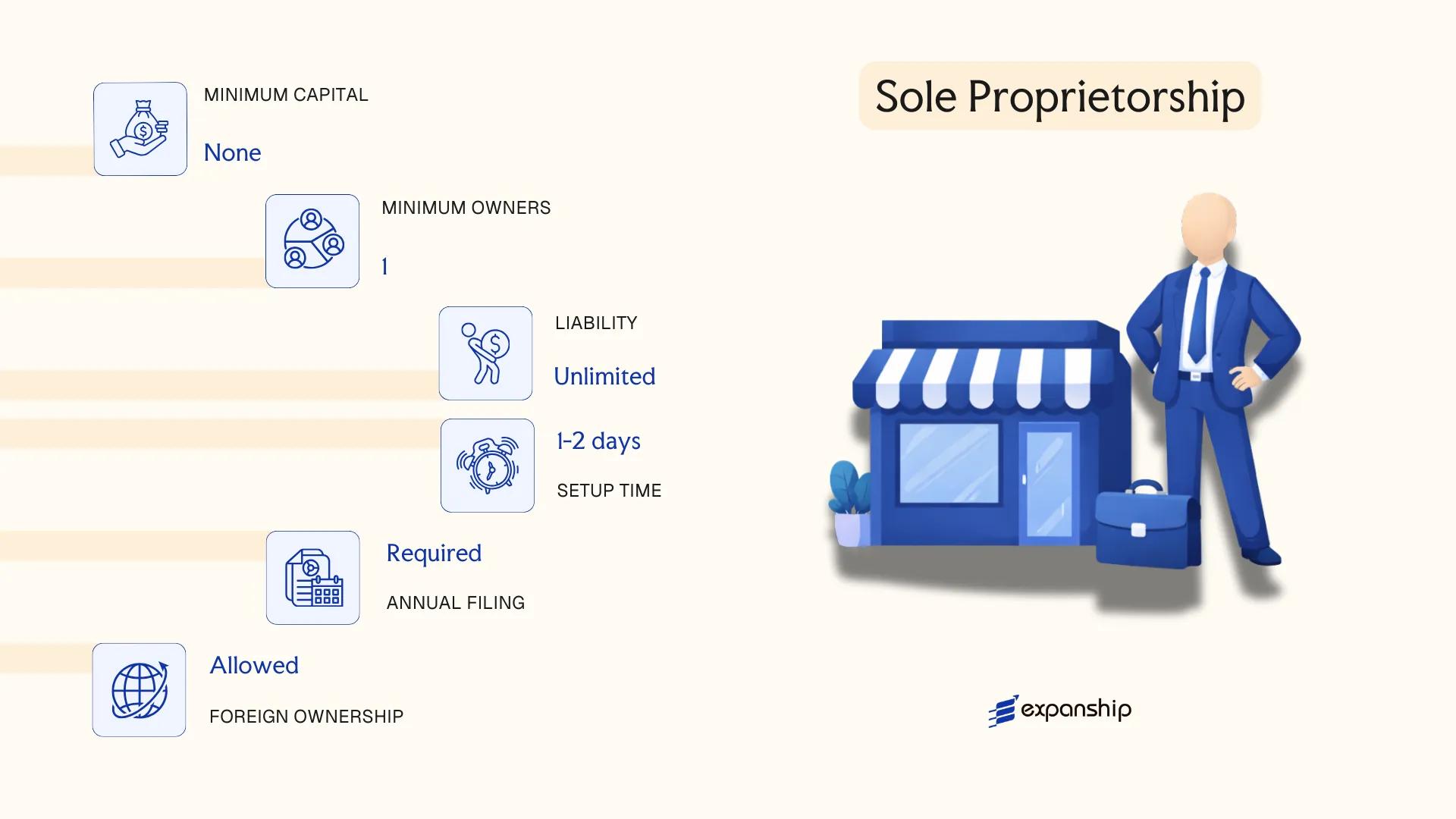

Einzelunternehmen – Sole Proprietorship

The Einzelunternehmen sole proprietorship Germany represents the simplest business structure available under German commercial law. No separate founding act governs its formation exclusively; instead, registration obligations arise under the Handelsgesetzbuch (HGB) for commercial traders and the Gewerbeordnung (GewO) for trade registration.

Unlike a GmbH or AG, the Einzelunternehmen carries no separate legal personality. The proprietor and the business are legally identical, meaning personal assets are fully exposed to business liabilities without any protective barrier.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Einzelunternehmen) | No separate legal personality |

| Proprietor | Single individual only | Referred to as Inhaber (owner) |

| Liability | Unlimited personal liability | All personal assets at risk |

| Registration | Gewerbeanmeldung with local Gewerbeamt; HGB entry if commercial | Freiberufler register with Finanzamt only |

| Capital | No minimum capital required | Funds contributed informally |

| Local Presence | Registered business address in Germany required | No resident agent requirement |

Focus Points

- Taxation: Subject to income tax (Einkommensteuer) at progressive rates up to 45%; trade tax (Gewerbesteuer) applies if commercially registered; VAT registration required once turnover exceeds the Kleinunternehmerregelung threshold under §19 UStG.

- Social Security: The proprietor is generally responsible for arranging their own health and pension contributions independently.

- Conversion: Can be converted into a GmbH or other capital company, though asset transfer procedures apply.

- Annual Compliance: No mandatory statutory audit; accounting obligations depend on whether the business qualifies as a Kaufmann under the HGB.

Closing

The Einzelunternehmen suits freelancers, sole traders, and small-scale operators who prioritise low administrative overhead over liability protection. Its primary limitation is unrestricted personal liability, which makes it unsuitable for businesses carrying significant financial or operational risk.

Freelancers (Freiberufler) and small sole traders seeking minimal setup costs and straightforward administration, with no immediate need for liability protection.

How to Choose the Right Entity Type in Germany

Choosing the right company type in Germany is not a formality — the structure you register determines your tax exposure, liability, regulatory obligations, and operational capacity from day one.

Why Your Entity Choice Matters

Forming the wrong entity type produces concrete, often costly outcomes:

- Selecting a UG when you need to raise external equity capital forces a costly conversion process under the GmbHG before institutional investors will participate.

- Choosing a GbR for commercial trading activity means unlimited personal liability for all partners, with no liability cap available until you convert to a registered commercial partnership or capital company.

- Registering a branch (Zweigniederlassung) when full legal independence is required means the parent entity remains directly liable for the branch's obligations — there is no liability separation.

- Forming an AG when your business has fewer than a handful of shareholders adds a mandatory supervisory board (Aufsichtsrat) and annual audit obligations that do not apply to a GmbH.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct legal structures under German law.

- Liability Exposure: Your tolerance for personal liability determines whether a capital company or a partnership structure is appropriate.

- Ownership Structure: Multi-investor businesses requiring transferable shares point toward an AG, while closely held operations suit a GmbH.

- Minimum Capital: Available startup capital is a threshold variable — the AG requires €50,000, the GmbH €25,000, and the UG as little as €1.

- Substance Capacity: If you cannot maintain genuine management presence in Germany, structures with lighter operational requirements may carry lower compliance risk.

- Exit and Conversion: Not all entity types permit straightforward redomiciliation or conversion; a GmbH can be converted to an AG under the Umwandlungsgesetz, but the process involves notarial and court procedures.

The governing legislation for most capital companies is the Gesetz betreffend die Gesellschaften mit beschränkter Haftung (GmbHG), available in full on Germany's official legal database.

Compliance Services for Companies in Germany

Ongoing compliance support for German entities, including annual filings, reporting obligations, and regulatory monitoring.

Conclusion

Germany's company incorporation landscape offers a structured range of legal forms, each governed by the Handelsgesetzbuch (HGB) or the specific statutes that define them. The GmbH remains the most widely registered entity, preferred by founders who want limited liability without the capital and governance requirements of an AG. The UG serves those starting with minimal capital, functioning as a stepping stone toward full GmbH status. An AG suits larger enterprises requiring access to capital markets, while the KGaA fits hybrid ownership models combining shareholder and partnership interests. The OHG, KG, and GbR carry personal liability implications that make them more appropriate for closely held professional or trading arrangements.

Registered with the Handelsregister and supervised under frameworks including BaFin oversight for regulated activities, German entity formation follows clearly codified procedures. Setting up a company in Germany continues to attract international business given ongoing treaty network development and the jurisdiction's position within EU regulatory frameworks. Expanship's team works directly within these structures to support your registration process from the ground up.

How Expanship Can Assist You

Expanship Germany company formation services cover the full process of establishing a legal presence under German commercial law, from selecting between a GmbH, UG, or AG to completing registration with the Handelsregister (Commercial Register) through the relevant Amtsgericht (local court). Your choice of entity directly shapes your liability exposure, capital requirements, and ongoing reporting duties — and getting that foundation right matters from day one.

Expanship can assist you across each stage of the process:

- Document preparation, notarisation, and apostille or legalisation

- Registered address and resident agent provision in Germany

- Filing coordination with the Amtsgericht and Handelsregister

- Post-incorporation compliance management, including annual filings and shareholder obligations

- Liaison with the Finanzamt for tax registration

- Banking introduction support for your new German entity

To discuss your specific situation, reach out to Expanship Germany directly.

Frequently Asked Questions (FAQ)

The GmbH (Gesellschaft mit beschränkter Haftung) is the most frequently incorporated entity in Germany, largely because it combines limited liability with comparatively straightforward governance requirements. A minimum share capital of €25,000 and registration with the Handelsregister make it accessible to a broad range of businesses.

Both structures offer limited liability, but an AG requires €50,000 in share capital and is subject to more extensive supervisory obligations under the Aktiengesetz, including a mandatory Aufsichtsrat once certain employee thresholds are met. A GmbH operates under the GmbHG and is generally subject to lighter ongoing disclosure and governance requirements, making it the more common choice for closely held firms.

The GbR (Gesellschaft bürgerlichen Rechts) does not require entry in the Handelsregister, meaning member details are not routinely subject to public commercial registration disclosure. However, nominee arrangements vary in enforceability under German law, and professional advice should be sought before relying on any privacy-oriented structuring.

A GmbH and AG can each be formed by a single shareholder under German law. Partnerships such as the OHG and KG require at least two partners by definition, and a GbR similarly requires a minimum of two participants to constitute a civil-law society.

Non-residents face no statutory nationality restrictions when incorporating a GmbH or AG. The managing director (Geschäftsführer) of a GmbH does not need to be a German resident, though practical considerations around notarial authentication of documents and a registered business address in Germany apply.

The Umwandlungsgesetz (UmwG) governs structural changes including conversion, merger, and spin-off. A UG can be converted into a GmbH once its reserves reach €25,000, and a GmbH can be transformed into an AG through a statutory conversion process.

The GmbH, AG, UG, and KGaA each hold full legal personality as juristische Personen. A GbR traditionally lacked separate legal personality, though the Personengesellschaftsrechtsmodernisierungsgesetz (MoPeG), effective January 2024, now grants registered GbRs legal capacity comparable to other commercial partnerships.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.