Key Takeaways

- Federal incorporation under the Canada Business Corporations Act gives a foreign-owned company a single legal identity recognised across all provinces, removing the need to re-register separately in each territory where the business operates.

- Canada's SR&ED program converts qualifying research and development expenditure into refundable federal tax credits, meaning eligible companies recover cash regardless of whether they owe corporate tax in a given year.

- Registering a corporation in Canada provides automatic preferential market access to both the United States and Mexico under CUSMA, a trade framework that most comparable incorporation jurisdictions cannot replicate within a single agreement.

- The federal corporate tax rate structure, combined with provincial variation and the small business deduction available to qualifying Canadian-controlled private corporations, creates a layered tax environment that rewards structured planning for foreign investors.

Incorporating a business in Canada gives foreign investors access to a G7 economy governed by stable federal institutions and a transparent legal environment. Canada is an independent sovereign nation and a federal state, with company registration administered at both the federal and provincial levels. At the federal level, businesses are registered through Corporations Canada, the federal body responsible for incorporating and maintaining companies under the Canada Business Corporations Act. The federal corporation — specifically the structure available under that Act — is the most common vehicle through which foreign businesses establish a presence nationally.

The country operates a territorial-leaning, treaty-based tax system with progressive corporate rates that vary by business size and province. Foreign ownership restrictions are minimal across most sectors, and foreign direct investment is generally permitted without prior government approval outside of industries subject to the Investment Canada Act.

This article examines the concrete advantages that make Canadian incorporation an option worth serious consideration for internationally operating businesses.

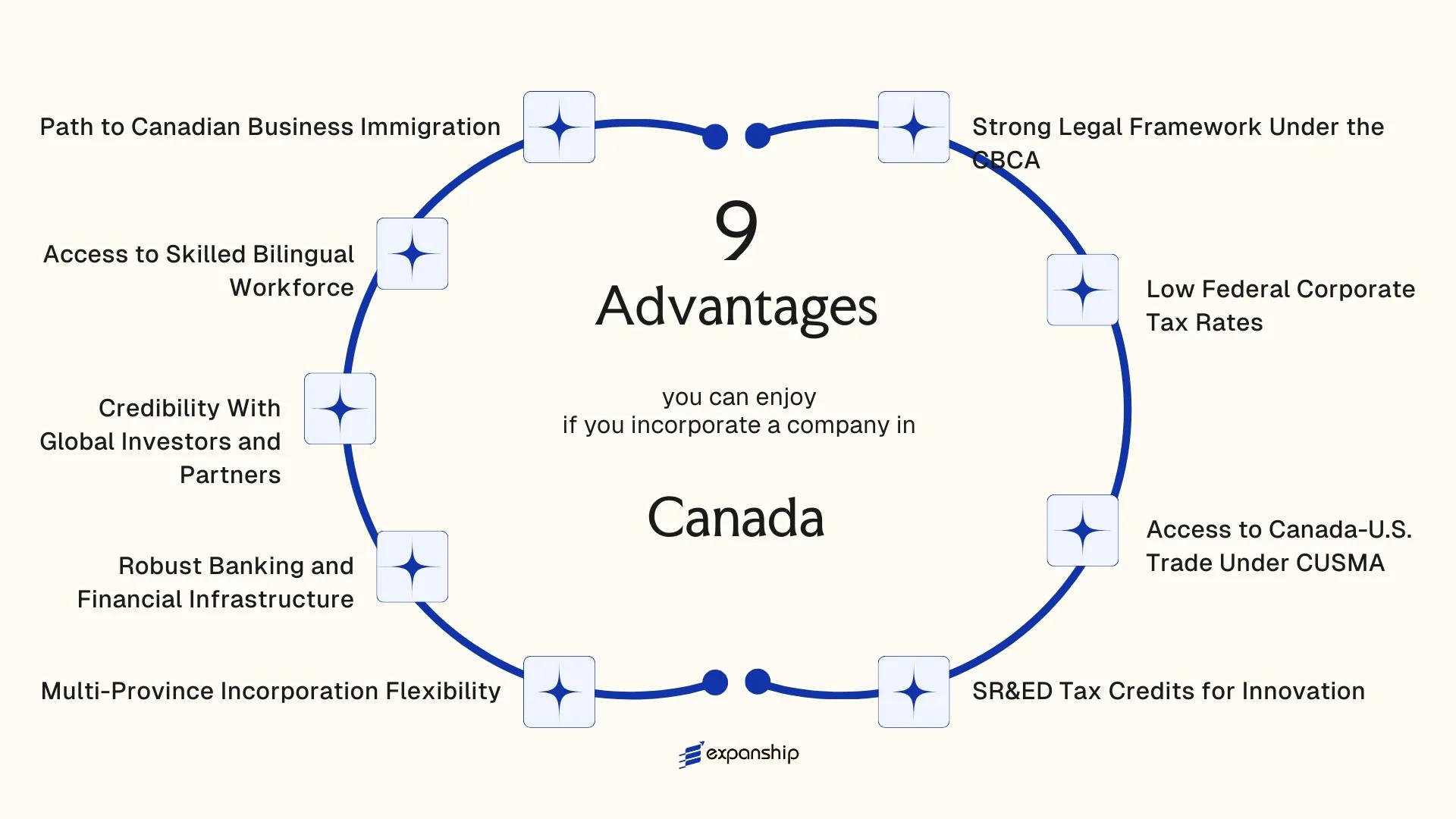

Strong Legal Framework Under the CBCA

The CBCA legal framework benefits for businesses extend well beyond basic registration formalities. Federal incorporation under the Canada Business Corporations Act creates a legal identity that carries weight across all provinces and internationally recognized jurisdictions.

Predictability Through Codified Shareholder Protections

The CBCA establishes specific statutory rights for minority shareholders, including dissent and appraisal rights under Section 190, which allow shareholders to demand fair value for their shares in certain corporate transactions. For foreign investors holding minority stakes, this codified protection reduces exposure to governance risk in ways that depend on contractual arrangements alone in less structured regimes.

Directors owe fiduciary duties under Section 122 of the CBCA, with personal liability exposure that reinforces accountability at the board level. That accountability structure gives external investors and institutional partners a clearer basis for due diligence.

Federal Jurisdiction Removes Provincial Uncertainty

A corporation formed under the CBCA holds its legal status at the federal level, meaning its constitutional validity does not shift when your business operates across provincial boundaries. Oversight falls under Corporations Canada, which administers federal filings, annual returns, and compliance requirements through a single regulatory point of contact.

Federal incorporation under the CBCA gives your entity a single, nationally recognized legal status administered by Corporations Canada, eliminating the need to re-establish corporate standing in each province where you operate.

Low Federal Corporate Tax Rates

Canada's federal corporate tax rate sits at 15% for general corporations, a figure that compares favorably against the United States federal rate of 21%. For Canadian-Controlled Private Corporations (CCPCs) earning active business income below the $500,000 small business deduction threshold, the federal rate drops to 9%. That gap carries real consequences for retained earnings, reinvestment capacity, and after-tax cash flow.

The small business deduction, governed under Section 125 of the Income Tax Act, applies to qualifying active business income and is available to corporations that meet specific residency and ownership conditions. Foreign-owned entities generally fall outside CCPC status, but the standard 15% federal rate remains globally competitive for international firms.

Provincial corporate tax applies separately and varies by province, yet the federal rate functions as a fixed, predictable floor for your tax planning. That predictability reduces fiscal uncertainty when structuring cross-border operations or forecasting multi-year returns.

Structurally, the federal tax framework offers several features that reduce your effective burden:

- No federal capital gains tax on the sale of qualifying small business corporation shares under the lifetime capital gains exemption

- Scientific research expenditures receive deductions at the federal level independently of provincial treatment

- Foreign tax credits under the Income Tax Act help offset double taxation on income earned abroad

- The general tax rate reduction under Section 123.4 applies broadly, without industry carve-outs that could complicate your eligibility

Incorporate Your Company in Canada

Set up a federally or provincially incorporated company in Canada with full compliance support from Expanship.

Access to Canada-U.S. Trade Under CUSMA

Signed in 2018 and implemented in 2020, the Canada-United States-Mexico Agreement (CUSMA) replaced NAFTA as the governing trade framework across North America. For a foreign business incorporated in Canada, this treaty creates direct, preferential access to a combined market of roughly 500 million consumers. That access is not incidental — it is a structural benefit tied specifically to where your company is registered.

Under CUSMA, goods that meet the agreement's Rules of Origin requirements move across the U.S.-Canada border with zero or reduced tariffs. For a foreign investor using a Canadian entity as their North American operating base, this means manufactured or processed goods can reach U.S. buyers without the duty burden that applies to imports from outside the agreement's territory.

| Trade Area | CUSMA Provision | Relevance to Incorporated Business |

|---|---|---|

| Goods Trade | Tariff elimination on qualifying goods | Reduces export costs to U.S. and Mexican markets |

| Rules of Origin | Regional Value Content thresholds | Determines tariff eligibility for your products |

| Services | Cross-border services provisions | Supports service-based firms operating across borders |

| Investment | National Treatment for investors | Protects foreign-owned Canadian entities in U.S. market |

Canada CUSMA trade agreement benefits for businesses extend beyond goods. The treaty includes provisions covering cross-border services, intellectual property, and digital trade, giving service-based firms incorporated here a defined legal framework when contracting with U.S. clients. National Treatment obligations under CUSMA also mean your Canadian-registered company must be treated no less favorably than a U.S. domestic entity when operating within that market.

SR&ED Tax Credits for Innovation

One of the most quantifiable SR&ED tax credits benefits for Canadian corporations is the ability to recover a significant portion of eligible research and development expenditures directly through the tax system. Administered under the federal Income Tax Act, the SR&ED program allows incorporated businesses to claim investment tax credits (ITCs) on qualifying wages, materials, and contractor costs tied to experimental development or applied research.

Federal ITCs for most corporations sit at 15% of eligible spending. Canadian-controlled private corporations (CCPCs) qualify for an enhanced 35% credit on the first $3 million of qualified expenditures annually, with unused credits refundable at 40%. For a foreign-owned entity that incorporates locally and meets CCPC criteria, this translates into direct cash recovery, not just a deduction against taxable income.

Provinces including Ontario, Quebec, and British Columbia administer their own supplemental R&D credits, which stack on top of the federal program. Quebec's credit rate, for instance, reaches up to 30% for eligible SMEs. This layering effect materially reduces the net cost of sustained innovation activity.

Keep the following in mind when accessing this benefit:

- Your business must file a T661 form with the Canada Revenue Agency alongside the corporate return

- CCPC status requires that Canadians hold more than 50% of voting shares

- Both current and capital expenditures may qualify, subject to CRA guidelines

- Claims are subject to technical and financial review; documentation standards are strict

SR&ED credits can be claimed retroactively for up to 18 months after a corporation's fiscal year-end, giving newly incorporated firms time to identify qualifying work already completed.

Multi-Province Incorporation Flexibility

Multi-province incorporation flexibility in Canada gives foreign businesses a structural choice that few federal systems offer at comparable cost or speed. You can incorporate either federally under the Canada Business Corporations Act (CBCA) or provincially under the legislation of any individual province or territory, and the right choice depends entirely on where you intend to operate and how broadly.

Federal vs. Provincial: What the Choice Actually Means

A federal incorporation under the CBCA grants your company the right to carry on business under its registered name in all provinces and territories, making it suitable for firms with pan-Canadian operations. Provincial incorporation, by contrast, restricts name protection and operational rights to the incorporating province unless the company separately registers as an extra-provincial entity in each additional province where it conducts business.

This distinction matters practically. Alberta's Business Corporations Act and British Columbia's Business Corporations Act each offer their own residency requirements for directors that differ from the CBCA's current rules, and some provinces have eliminated director residency requirements entirely, which can simplify governance for foreign-owned firms with no Canadian-resident principals.

Why the Provincial Route Has Its Own Merits

Quebec, operating under civil law rather than common law, follows the Business Corporations Act (LSAQ) and suits businesses whose primary market is francophone Canada. Ontario's provincial framework under the Business Corporations Act (Ontario) is widely recognized by financial institutions and counterparties, which can ease banking and contracting processes for Ontario-focused operations.

Choosing the right incorporating jurisdiction is not merely administrative. It directly affects director composition requirements, name protection scope, and the cost of subsequent provincial registrations as your business expands.

Plan Your Canadian Incorporation Structure

Understand which incorporating jurisdiction fits your business structure, director profile, and operational footprint before you file.

Robust Banking and Financial Infrastructure

Canada banking infrastructure benefits for corporations extend well beyond simple account access. The country's financial system is regulated by the Office of the Superintendent of Financial Institutions (OSFI) under the Bank Act, creating a regulatory environment that foreign firms can rely on for predictability and institutional stability.

- Incorporated businesses gain access to major Schedule I banks, including RBC, TD, Scotiabank, BMO, and CIBC, all of which offer dedicated commercial banking divisions with multi-currency accounts, trade finance facilities, and cross-border wire capabilities, reducing friction for businesses operating across North American and international markets.

- Canada maintains a domestic payment system through Payments Canada, which oversees the Large Value Transfer System (LVTS) and the Automated Clearing Settlement System (ACSS). For your business, this means access to same-day and next-day settlement infrastructure that supports high-volume commercial transactions.

- Canadian chartered banks are recognized counterparties in international correspondent banking networks. A firm incorporated here carries institutional credibility that can ease the process of opening accounts or establishing credit relationships in other jurisdictions.

- Foreign-owned corporations incorporated under the Canada Business Corporations Act (CBCA) are generally eligible for the same commercial banking products as domestically owned firms, subject to standard due diligence and beneficial ownership disclosure requirements under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act.

Credibility With Global Investors and Partners

Canadian incorporation credibility for global investors is grounded in a legal and institutional foundation that foreign partners can independently verify. Corporations formed under the Canada Business Corporations Act (CBCA) are registered through Corporations Canada, a federal registry that is publicly accessible and internationally recognized. That transparency gives counterparties, banks, and institutional investors a clear, auditable record of your entity's existence and structure.

Membership in the Financial Action Task Force (FATF) means Canadian-registered businesses operate under anti-money laundering and beneficial ownership disclosure standards that satisfy due diligence requirements in most major financial markets. For a foreign founder raising capital or negotiating supply agreements, this reduces friction during investor KYC processes.

The OECD ranks Canada consistently among the top economies for regulatory quality and rule of law, two factors that institutional funds use when evaluating jurisdictions for portfolio companies.

"Canada ranks 14th globally on the World Bank's Rule of Law index, placing it above the majority of G20 economies." — World Bank Worldwide Governance Indicators, 2023.

Your firm's address in a CBCA-incorporated entity also signals proximity to U.S. markets without the compliance complexity of a U.S. domestic entity, a distinction that resonates with European and Asian investors evaluating North American market entry.

Access to Skilled Bilingual Workforce

Canada's bilingual skilled workforce advantages for businesses are built into the country's legal and institutional structure. Under the Official Languages Act, English and French hold equal status federally, producing a labour pool that is formally trained in both languages from the primary level onward.

For a foreign-incorporated entity, this has direct operational implications:

- Firms targeting both anglophone and francophone North American markets can hire domestically without building separate regional teams.

- Provinces like Quebec, New Brunswick, and Ontario each maintain distinct bilingual labour concentrations, allowing your hiring strategy to align with where your business incorporates or operates.

- Canada's immigration pathways, including the Federal Skilled Worker Program under the Immigration and Refugee Protection Act, bring internationally trained professionals into this workforce annually, expanding the technical talent base.

Post-secondary institutions such as McGill University, the University of Ottawa, and HEC Montréal produce graduates across engineering, finance, law, and technology who are operationally fluent in both official languages. For a firm serving international clients or managing cross-border regulatory filings, this reduces the need for external translation infrastructure.

Bilingual hiring requirements vary by province; businesses incorporated in Quebec and operating there must comply with the Charter of the French Language (Bill 101), which imposes specific obligations on workplace language use.

Path to Canadian Business Immigration

Incorporating a business in Canada creates a direct structural link to several federal and provincial immigration programs. The Canada business immigration pathway through incorporation is not incidental — it is explicitly built into program eligibility criteria administered by Immigration, Refugees and Citizenship Canada (IRCC).

The Start-Up Visa Program

Under the Start-Up Visa (SUV) Program, foreign nationals who secure a commitment from a designated organization — a venture capital fund, angel investor group, or business incubator — can apply for permanent residence. The incorporated entity must be actively managed from within the country, and the applicant must hold a minimum percentage of voting shares alongside the designated organization. This structure means your corporation is not just a legal formality; it is the qualifying instrument for your immigration application.

Owner-Operator LMIA Pathway

Foreign entrepreneurs who own and control a Canadian corporation can apply for a work permit through the Owner-Operator Labour Market Impact Assessment (LMIA) stream. Unlike standard LMIA applications, this pathway accounts for the applicant's role as both employer and employee within their own firm. Holding majority shares in an incorporated business directly supports the evidentiary requirements for this permit.

Provincial Nominee Programs

Several provinces, including Ontario, British Columbia, and Alberta, operate Entrepreneur streams under their Provincial Nominee Programs (PNPs). Eligibility under these streams typically requires:

- Incorporation or intent to incorporate a qualifying business

- Minimum net worth and investment thresholds set by each province

- Active management and ownership stake requirements

- A performance agreement with the provincial authority

Meeting the incorporation threshold is often the first condition assessed.

Why Canada Stands Out Among Top Incorporation Destinations

Among the top incorporation destination advantages that foreign investors evaluate, three factors tend to dominate: tax efficiency, treaty access, and the predictability of the legal system. Compared to jurisdictions like the United Kingdom, Singapore, and Delaware (USA), Canada holds a measurable position across each of these dimensions. Those three were selected because they represent the most realistic alternatives a foreign business owner would weigh when choosing a North American or common-law base for their operations.

What the comparison reveals is less about any single metric and more about the combination. The federal corporate tax rate of 15%, the Canada-United States-Mexico Agreement providing preferential market access, and the Scientific Research and Experimental Development program together form a package that few comparable jurisdictions replicate in full. Singapore offers low tax rates but no equivalent CUSMA access. The UK provides treaty depth but a higher headline corporate rate of 25%. Delaware offers structural flexibility but no federal SR&ED equivalent and no preferential trade rights into Canada.

| Parameter | Canada | United Kingdom | Singapore | Delaware (USA) |

|---|---|---|---|---|

| Federal Corporate Tax Rate | 15% | 25% | 17% | N/A (state-level entity; federal rate applies) |

| R&D Tax Incentive | SR&ED (up to 35% refundable) | R&D tax relief (varies by company size) | R&D tax deduction (up to 250%) | Federal R&D credit only; no state equivalent |

| Preferential Trade Access to U.S. Market | Yes, via CUSMA | No (post-Brexit; no U.S. FTA) | No direct U.S. FTA | Domestic access only |

| Common Law Legal System | Yes (except Quebec) | Yes | Yes (based on English common law) | Yes |

| Federal Incorporation Statute | Canada Business Corporations Act | Companies Act 2006 | Companies Act 1967 | Delaware General Corporation Law |

| Privacy of Directors (public registry) | Limited disclosure required | Publicly registered | Publicly registered | Minimal disclosure required |

| Bilingual Official Language Advantage | Yes (English and French) | No | No (English primary) | No |

Compliance Services for Companies in Canada

Maintain your Canadian entity in good standing with annual filings, registered agent services, and regulatory reporting under the CBCA and provincial statutes.

Conclusion

The benefits of incorporating in Canada rest on a combination of structural and practical factors that hold up under scrutiny. Federal incorporation under the Canada Business Corporations Act gives your company a single, nationally recognised legal identity. The SR&ED program turns eligible R&D expenditure into refundable tax credits, reducing after-tax costs in ways that directly affect cash flow. Access to the United States and Mexican markets through CUSMA, without separate trade arrangements, gives a Canadian-registered entity a commercial reach that most comparable jurisdictions cannot replicate through one agreement alone.

Not every business will draw equal value from these features. A firm with no R&D activity gains little from SR&ED, and a company focused entirely on domestic sales may not need CUSMA access at all. The advantages of Canadian incorporation for foreign investors are genuine, but the weight they carry depends on your industry, ownership structure, and the markets you intend to serve.

Understanding which benefits apply to your specific situation is the necessary first step before any filing with Corporations Canada or a provincial registry. Getting that analysis right shapes everything from your entity type to your provincial jurisdiction of incorporation.

Let Expanship Handle Your Canadian Incorporation

Incorporating a federal business entity under the Canada Business Corporations Act, registering with the Canada Revenue Agency, and meeting provincial compliance obligations involves procedural steps that carry real consequences if handled incorrectly. Expanship's Canadian incorporation services benefits foreign investors by providing structured support across each of these stages, from pre-incorporation planning through ongoing statutory maintenance.

Expanship's service scope for Canadian entities includes:

- Preparation and notarization of incorporation documents, including Articles of Incorporation and the corporate by-laws

- Provision of a registered office address and resident Canadian director service where required under the CBCA

- Filing with Corporations Canada and liaising with provincial registrars as applicable

- Post-incorporation compliance management, including annual return filings and minute book maintenance

- CRA business number and HST/GST registration assistance

- Banking introduction support to facilitate the opening of a Canadian corporate account

To get started, contact Expanship Canada directly.

Frequently Asked Questions (FAQ)

The general federal corporate income tax rate is 15%, but Canadian-Controlled Private Corporations (CCPCs) qualifying for the Small Business Deduction pay a reduced federal rate of 9% on the first CAD 500,000 of active business income. Provincial corporate tax rates apply on top of the federal rate and vary by province. Total combined rates depend on the province of operation and whether the corporation qualifies as a CCPC.

A corporation incorporated in Canada can use the Canada-United States-Mexico Agreement (CUSMA) to access preferential tariff treatment on qualifying goods traded across the Canada-U.S. border. This is particularly relevant for manufacturers and goods exporters, as eligible products may enter the U.S. market at reduced or zero tariff rates. The preferential access is contingent on meeting the rules of origin requirements specified under CUSMA.

The Scientific Research and Experimental Development (SR&ED) program is administered by the Canada Revenue Agency (CRA) and provides tax incentives for corporations conducting eligible research and development work in Canada. To qualify, the work must involve systematic investigation or experimentation in a scientific or technological field aimed at advancing knowledge or resolving technological uncertainty. CCPCs can claim a refundable investment tax credit of up to 35% on the first CAD 3 million of eligible expenditures, while other corporations receive a non-refundable 15% credit.

Federal incorporation under the CBCA grants the corporation the right to carry on business under its corporate name throughout Canada, but extra-provincial registration is still required in each province or territory where the business maintains a physical presence or conducts operations. This registration process is governed by each province's own legislation. The federal structure does not replace provincial licensing or registration obligations.

Failure to file the annual return required under the CBCA can result in the corporation being dissolved by Corporations Canada through an administrative process. Directors may face personal liability for corporate obligations incurred after dissolution, depending on the circumstances. A dissolved corporation can apply for revival under the CBCA, but the process requires filing outstanding returns and paying any applicable fees.

No minimum share capital is required to incorporate under the CBCA. A federal corporation can be incorporated with a single share issued at a nominal value. The CBCA does require that a corporation maintain stated capital accounts and comply with solvency tests before making distributions to shareholders.

A Canadian corporation can sponsor foreign skilled workers through pathways such as the Temporary Foreign Worker Program or the International Mobility Program, both administered by Employment and Social Development Canada (ESDC) and Immigration, Refugees and Citizenship Canada (IRCC). Eligibility to recruit under certain streams requires the employer to meet criteria related to business legitimacy, including proof of active operations. The corporation itself does not need a specific incorporation structure to access these programs, but it must be in good standing and able to demonstrate genuine employment needs.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.