Key Takeaways

- Canada's dual legislative framework means businesses can incorporate either federally under the Canada Business Corporations Act administered by Corporations Canada, or provincially under statutes such as the Ontario Business Corporations Act or Alberta Business Corporations Act.

- The Unlimited Liability Corporation is available only in Alberta, British Columbia, and Nova Scotia, and exists primarily to serve U.S. parent companies seeking flow-through tax treatment under cross-border structures.

- Federal corporations offer national name protection and interprovincial mobility, making them the most commonly registered entity type across Canada.

- Partnerships and sole proprietorships remain unincorporated forms that carry pass-through taxation but expose owners to greater personal liability than incorporated structures.

Introduction to Entity Types in Canada

Canada sits in the northern half of North America, sharing its southern border with the United States and spanning ten provinces and three territories. It is an independent federal state and a member of the G7, operating under a dual legislative framework where both federal and provincial governments hold authority over business registration and corporate law.

Depending on the jurisdiction of incorporation, company registration falls under either federal oversight through Corporations Canada, which administers the Canada Business Corporations Act (CBCA), or under the relevant provincial registry. Canada applies a residence-based tax system, meaning corporations are taxed on worldwide income, though an extensive network of tax treaties modifies that obligation for foreign-owned structures.

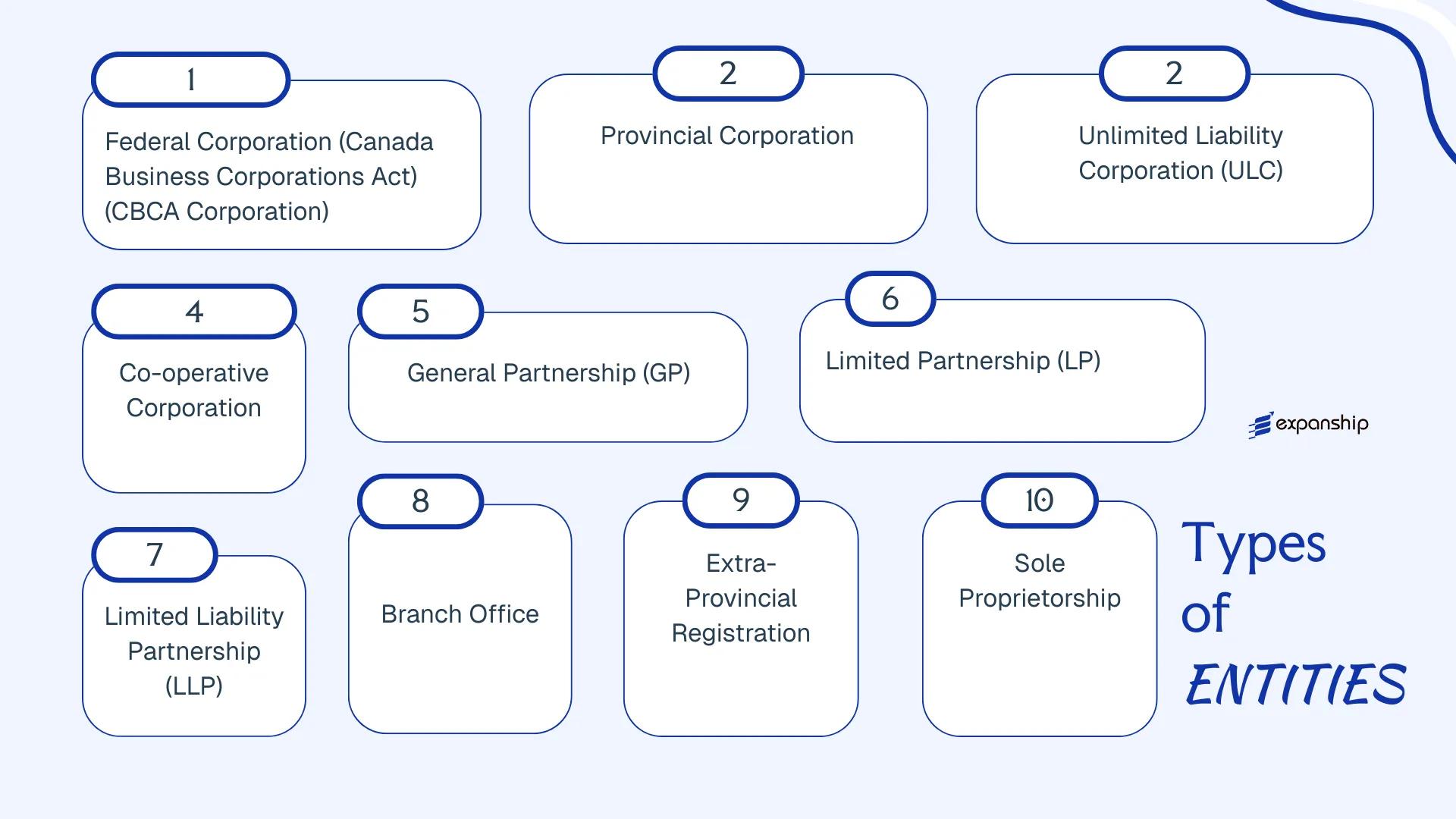

The types of business entities in Canada span both incorporated and unincorporated forms. Available structures include the Federal Corporation, Provincial Corporation, Unlimited Liability Corporation, Co-operative Corporation, General Partnership, Limited Partnership, Limited Liability Partnership, Branch Office, Extra-Provincial Registration, and Sole Proprietorship.

Each of these structures carries distinct implications for liability, taxation, governance, and foreign ownership eligibility. This article examines each one in detail.

An Overview of Business Structures in Canada

Canada's company law framework accommodates several distinct business structures, governed primarily by the Canada Business Corporations Act (CBCA) at the federal level and by parallel provincial statutes such as the Alberta Business Corporations Act and the Ontario Business Corporations Act. Each structure carries a different legal form, liability profile, and tax treatment suited to specific commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Federal Corporation | Separate legal entity | Limited | Taxed | Yes | 1 director | Corporations Canada | CBCA |

| Provincial Corporation | Separate legal entity | Limited | Taxed | Yes | 1 director (varies) | Provincial registrar | Provincial BCA |

| Unlimited Liability Corporation (ULC) | Separate legal entity | Unlimited | Taxed | Yes | 1 shareholder | Provincial registrar | ABCA / NSCA / BCBCA |

| Co-operative Corporation | Separate legal entity | Limited | Taxed / exempt | Yes | Varies by province | Provincial registrar | Co-operative Acts |

| General Partnership | Not separate | Unlimited | Pass-through | Yes | 2 partners | Provincial registry | Provincial Partnership Act |

| Limited Partnership | Partial separation | Mixed | Pass-through | Yes | 1 GP + 1 LP | Provincial registry | Provincial LP Act |

| Limited Liability Partnership | Partial separation | Partial | Pass-through | Restricted | 2 partners | Provincial registry | Provincial LLP Act |

| Branch Office | Not separate | Unlimited | Taxed | Yes | N/A | Provincial registrar | Extra-Provincial Acts |

| Sole Proprietorship | Not separate | Unlimited | Pass-through | Yes | 1 person | Provincial registry | Provincial registration rules |

Each of these structures is examined in full in the sections below.

Federal Corporation (Canada Business Corporations Act, CBCA)

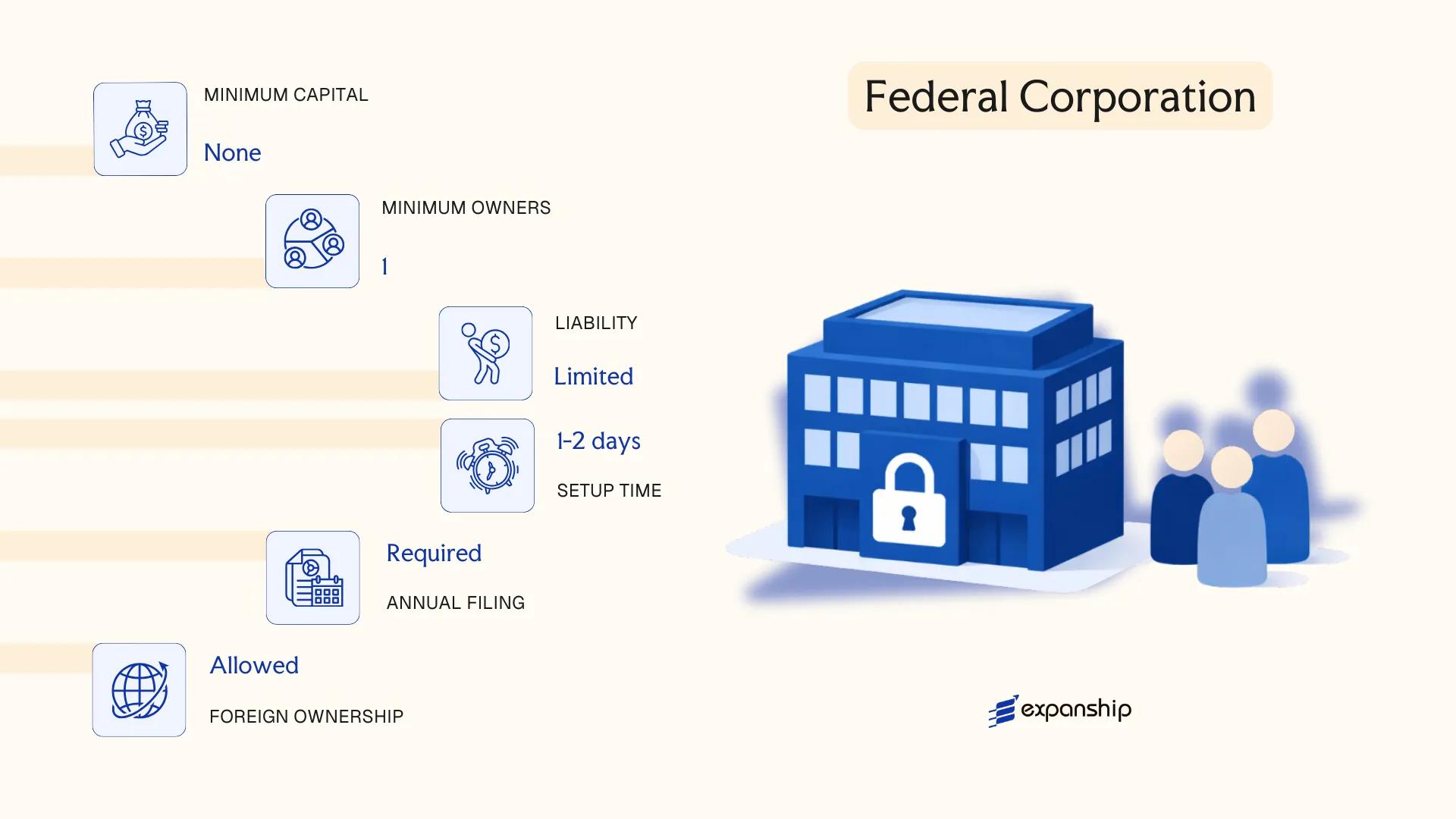

Enacted in 1975, the Canada Business Corporations Act (CBCA) governs federal corporation Canada CBCA registration and creates a corporation as a distinct legal entity, separate from its shareholders. This separation confers limited liability on shareholders and allows the company to own property, enter contracts, and sue or be sued in its own name.

Incorporated federally under Corporations Canada, a CBCA entity can operate under its corporate name in every province and territory, subject to extra-provincial registration requirements in jurisdictions where it actively carries on business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Business corporation | Governed by the CBCA; separate legal personality |

| Members | Directors (min. 1), Shareholders (min. 1); no maximum for either | At least 25% of directors must be Canadian residents (or 1 of 3, whichever is greater); exemptions apply for certain industries |

| Local Presence | Registered office must be in Canada; address on public record | A physical Canadian address is required; virtual offices are generally accepted |

| Share Capital | No minimum capital requirement; shares issued in CAD | Par-value shares are not permitted under the CBCA |

| Privacy | Director and shareholder details filed with Corporations Canada | Beneficial ownership register requirements are expanding under federal amendments |

Focus Points

- Taxation: Federal corporate income tax applies at 15% (general rate) or 9% (small business rate) after abatements; provincial tax layers on top; GST/HST registration required if annual taxable supplies exceed CAD 30,000; withholding tax on dividends paid to non-residents is generally 25%, reducible under tax treaties.

- Annual Compliance: Annual return filed with Corporations Canada; financial statements and director/shareholder registers maintained internally; AGM required unless all shareholders waive it in writing.

- Treaty Access: As a Canadian-resident corporation, access to Canada's extensive tax treaty network (90+ treaties) is available, subject to residency and beneficial ownership conditions.

- Director Residency: The Canadian-resident director requirement has been a structuring consideration for foreign investors; it was removed for certain federal corporate categories under ongoing legislative amendments — confirm current status at time of incorporation.

- Conversion: A provincial corporation may be converted to a federal entity through a continuance process under CBCA s. 187 without dissolving and re-incorporating.

Closing

A CBCA corporation suits businesses intending to operate across multiple provinces, hold intellectual property nationally, or signal pan-Canadian presence to counterparties. The primary structural advantage is unrestricted interprovincial name protection; the key limitation is the Canadian-resident director requirement, which adds a layer of structuring complexity for fully foreign-owned businesses.

Foreign investors and domestic operators who require a nationally recognised corporate vehicle with cross-provincial mobility and access to Canada's full tax treaty network.

Company Incorporation in Canada

Incorporate a federal corporation under the CBCA with registered office support and compliance setup.

Provincial Corporation (Alberta Business Corporations Act, Ontario Business Corporations Act, etc.)

Incorporating at the provincial level means your company exists as a distinct legal entity under the legislation of a specific province. Each province maintains its own statute: Alberta operates under the Alberta Business Corporations Act (ABCA, RSA 2000), while Ontario companies are governed by the Ontario Business Corporations Act (OBCA, RSO 1990). Both follow a corporate model with separate legal personality and limited shareholder liability.

Provincial corporation registration Canada falls under the authority of provincial registrars rather than Corporations Canada. In Alberta, this is the Corporate Registry; in Ontario, the Ontario Business Registry. The entity structure mirrors the federal CBCA model but confines the company's name protection and certain regulatory recognition to the incorporating province.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private or public share capital corporation | Separate legal personality; shareholders not liable for corporate debts |

| Members | Directors (min. 1); Shareholders (min. 1, no maximum) | Alberta: 25% of directors must be Canadian residents; Ontario: 25% residency requirement also applies |

| Local Presence | Registered office within the incorporating province | Must maintain a physical address on record with the provincial registrar |

| Share Capital | No minimum paid-up capital; shares in CAD | Par-value and no-par-value shares permitted |

| Privacy | Shareholder names are not on public record in most provinces | Director names are publicly registered |

Focus Points

- Taxation: Subject to federal corporate income tax (general rate 15%) plus provincial corporate tax (e.g., Alberta 8%, Ontario 11.5% general rate); HST/GST applies to taxable supplies; withholding tax on dividends paid to non-residents at 25% (reducible under tax treaties).

- Annual Compliance: Annual returns must be filed with the provincial registrar; financial statements and shareholder meetings required per the applicable statute.

- Extra-Provincial Registration: Operating outside the incorporating province requires extra-provincial registration in each additional jurisdiction.

- Treaty Access: Provincial corporations qualify as Canadian residents for tax treaty purposes, provided central management and control is exercised in Canada.

- Conversion: An ABCA or OBCA corporation may apply to continue federally under the CBCA, and vice versa, through a statutory continuance process.

Closing

Provincial corporations are used for businesses whose operations are concentrated within one province, as well as for holding structures, real estate ownership, and operating companies where provincial-level incorporation suffices. The main advantage over federal incorporation is lower initial registration cost and simpler filing requirements; the limitation is that name protection does not extend beyond the incorporating province without separate extra-provincial registrations.

A provincial corporation suits entrepreneurs and SMEs whose commercial activity, client base, and operational footprint are concentrated within a single Canadian province.

Unlimited Liability Corporation (ULC)

An unlimited liability corporation Canada ULC is a distinct corporate form available in three provinces: Nova Scotia, Alberta, and British Columbia, governed respectively by the Nova Scotia Companies Act (1989), the Alberta Business Corporations Act (2000), and the Business Corporations Act (British Columbia) (2002). Unlike standard Canadian corporations, a ULC carries separate legal personality but imposes unlimited personal liability on shareholders if the company is wound up while insolvent.

This structure has no practical domestic use case for Canadian residents, given the personal liability exposure. Its primary application is cross-border tax planning, particularly for US-based investors, because the IRS treats a ULC as a flow-through entity (partnership or disregarded entity) under US tax rules while Canadian law recognises it as a corporation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation with unlimited shareholder liability | Liability triggers only on insolvent winding-up |

| Members | Shareholders; minimum 1, no maximum | Directors: minimum 1; no residency requirement in BC and AB; Nova Scotia requires at least 1 director |

| Local Presence | Registered office in province of incorporation | No resident agent requirement in most provinces |

| Capital | No minimum share capital; CAD currency | Shares can be issued for any consideration |

| Privacy | Shareholder register not publicly searchable in all provinces | Alberta and BC offer relatively stronger privacy |

Focus Points

- Taxation: No separate Canadian federal tax treaty benefit as a ULC; subject to enhanced 25% withholding tax on dividends paid to US shareholders under Article IV(7) of the Canada-US Tax Convention unless structured correctly.

- Annual Compliance: Annual return filing required with the relevant provincial registrar; financial statements not mandated to be filed publicly.

- Conversion: A standard provincial corporation can be converted to a ULC through a formal amendment process in Alberta and BC; Nova Scotia permits continuation from foreign jurisdictions.

- Restrictions: Cannot issue shares to the public; not suitable for Canadian resident shareholders due to personal liability exposure on insolvency.

Sub-Types

Nova Scotia Unlimited Liability Company (NS ULC)

The Nova Scotia unlimited liability company was historically the most commonly used ULC variant for US tax structuring, largely because Nova Scotia permitted single-member companies before other provinces. It remains a recognised vehicle under the Nova Scotia Companies Act but has lost ground to Alberta and BC structures due to procedural differences.

Alberta ULC

The Alberta ULC structure for foreign investors offers a more modern statutory framework under the ABCA and is frequently chosen for its straightforward incorporation process and no public disclosure of shareholder information at the provincial registry level.

Closing

A ULC is used almost exclusively as a holding or financing entity within US-Canada corporate groups, where the hybrid tax treatment creates a structural advantage. The core limitation is direct: Canadian-resident shareholders bear personal liability for corporate debts upon insolvency, making this form unsuitable outside a controlled cross-border ownership structure.

US-based parent companies or investors establishing a Canadian subsidiary where flow-through treatment under US tax rules is required.

Co-operative Corporation

Co-operative corporation registration Canada is governed at the federal level by the Canada Cooperatives Act (1998), administered by Corporations Canada. Most provinces also maintain their own co-operative legislation — Ontario's Co-operative Corporations Act, for example, or Alberta's Co-operatives Act — allowing incorporation at either level depending on your operational scope.

A co-operative is a distinct legal entity with separate legal personality and limited liability for its members. Unlike a standard share corporation, its structure is member-controlled: each member holds one vote regardless of capital contribution, and surplus earnings are distributed as patronage returns rather than dividends proportional to ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Co-operative Corporation | Separate legal personality; limited liability for members |

| Members | Referred to as "members"; minimum 3 (federal); provincially varies | No statutory maximum; membership classes may exist |

| Governance | Board of directors elected by members | One member, one vote principle applies |

| Local Presence | Registered office required in the incorporating jurisdiction | No separate registered agent requirement federally |

| Capital | No prescribed minimum; membership shares and investment shares permitted | Investment shares may carry limited voting rights |

| Privacy | Director and officer information filed publicly with Corporations Canada or provincial registry | Beneficial ownership rules apply where legislated |

Focus Points

- Taxation: Subject to standard federal and provincial corporate income tax rates; co-operatives may deduct patronage allocations paid to members, reducing taxable income — HST/GST obligations apply to taxable supplies as with any corporation.

- Annual Compliance: Annual returns filed with Corporations Canada or the relevant provincial registry; audited financial statements may be required depending on revenue thresholds.

- Restrictions: Federal co-operatives must operate consistently with co-operative principles; certain activities (e.g., purely investment-holding functions) are structurally incompatible with the model.

- Conversion: A co-operative may convert to a standard share corporation under applicable legislation, though member approval and regulatory consent are required.

Sub-Types

Worker Co-operative

Membership is restricted to individuals employed by the co-operative. This structure is used primarily by employee-owned service businesses and supports internal equity arrangements through member loans or shares.

Consumer Co-operative

Members are the end-users or customers of the co-operative's goods or services. Retail grocery co-operatives and financial co-operatives (credit unions) commonly adopt this form.

Producer Co-operative

Membership consists of producers — typically agricultural — who collectively market or process their output. This sub-type frequently operates under sector-specific provincial legislation.

Multi-Stakeholder Co-operative

Recognised under several provincial frameworks, this variant allows more than one class of members (workers, consumers, and supporting members) within a single entity. It is not available under the federal Canada Cooperatives Act.

Who Should Consider This Structure

Co-operative corporations are well-suited to collectively owned enterprises where member participation and equitable governance take priority over investment return. The patronage deduction mechanism offers a tax-efficient distribution structure unavailable to conventional corporations. The primary drawback is structural rigidity — the one-member-one-vote rule and restrictions on profit distribution can limit the entity's attractiveness to outside investors.

Co-operative corporations are best suited for member-driven ventures — worker collectives, agricultural producers, or community retail operations — where democratic control outweighs the need for external capital investment.

Partnerships (General Partnership, Limited Partnership, Limited Liability Partnership)

Partnership structures in Canada LP LLP arrangements are governed primarily at the provincial level, with each province enacting its own legislation. Ontario's Partnerships Act (R.S.O. 1990, c. P.5) and Limited Partnerships Act (R.S.O. 1990, c. L.16) are representative examples, while Alberta operates under the Partnership Act (R.S.A. 2000, c. P-3).

Unlike corporations, a general partnership does not constitute a separate legal entity in most provinces. Partners bear joint and several liability for the firm's obligations, making the choice of partnership type a structurally significant decision.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual arrangement (GP); registered entity (LP, LLP) | GP has no separate legal personality in most provinces |

| Members | General Partners and/or Limited Partners; no statutory maximum | LP requires at least one general partner and one limited partner |

| Local Presence | Registered office in the province of formation required | LP must file a declaration with the provincial registrar |

| Capital | No minimum capital requirement; contributions defined by partnership agreement | Denominated in CAD; no prescribed minimum |

| Privacy | Partner names disclosed in registration filings | LP declarations are public record in most provinces |

Focus Points

- Taxation: Partnerships are flow-through entities; income is allocated to partners and taxed at their applicable rate. No entity-level corporate tax applies, though withholding tax may apply to distributions to non-resident partners.

- Annual Compliance: LPs must maintain a current declaration of limited partnership; changes to partners or addresses require amended filings with the provincial registrar.

- Treaty Access: Non-resident partners may access Canada's tax treaty network depending on their own residency status; the partnership itself does not access treaties directly.

- LLP Restrictions: LLP status is generally restricted to regulated professions such as law, accounting, and medicine under provincial legislation.

- Conversion: Provincial statutes in Ontario and Alberta permit conversion of a general partnership to a limited partnership, subject to filing requirements.

Sub-Types

General Partnership (GP)

All partners share management responsibilities and carry unlimited personal liability for partnership debts. GPs are commonly used for small professional firms or joint ventures where liability exposure is acceptable to all parties.

Limited Partnership (LP)

Limited partners contribute capital and receive profit allocations but are restricted from participating in management to retain liability protection. This structure is widely used in real estate investment, private equity funds, and venture capital arrangements; limited partnership registration in Canada typically requires filing a declaration with the relevant provincial registry.

Limited Liability Partnership (LLP)

A limited liability partnership in Canada shields partners from personal liability arising from the negligence of other partners, while preserving joint and several liability for one's own acts. Provincial eligibility is restricted to designated professional groups.

Closing

Partnerships suit joint ventures, fund structures, and professional practices where flow-through taxation and flexible profit allocation are priorities; the absence of a minimum capital requirement is a practical advantage, though unlimited liability in a general partnership remains a significant exposure for individual partners.

LP and LLP structures are best suited to fund managers, real estate syndicates, and regulated professionals seeking tax transparency with defined liability boundaries.

Foreign Business Structures (Branch Office, Extra-Provincial Registration)

A foreign company branch office Canada registration does not create a separate legal entity. The parent company remains fully liable for all obligations incurred through the branch, meaning creditors can pursue the parent's global assets. This structure is governed at the federal level by the Canada Business Corporations Act (CBCA) and provincially by statutes such as the Business Corporations Act (Ontario) or the Business Corporations Act (British Columbia).

Extra-provincial registration Canada requirements apply when a foreign corporation carries on business in a province other than where it was first registered domestically, or when a non-Canadian firm establishes operations in any Canadian province. Each province administers its own registration regime independently.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign corporation | Not a separate legal person; parent bears full liability |

| Local Representative | Attorney for Service required in most provinces | Must be a Canadian resident; receives legal notices on behalf of the foreign entity |

| Registered Office | Provincial registered address mandatory | Cannot be a P.O. box; must be a physical address in the registering province |

| Capital Requirements | None specified | No minimum capital deposit required to register |

| Privacy | Parent company details filed publicly | Registered agent details appear on provincial registry records |

| Annual Compliance | Annual return filing with provincial registrar | Requirements and fees vary by province |

Focus Points

- Taxation: Branch profits are subject to federal and provincial corporate income tax; a federal Branch Profits Tax of 25% (reducible under tax treaties) applies to after-tax earnings remitted to the foreign parent, in lieu of dividend withholding tax.

- Treaty Access: Treaty benefits depend on the parent's residency; the branch itself is not a treaty resident and does not independently qualify.

- Economic Substance: No separate substance regime applies to branches, but the foreign parent's activities in the province determine permanent establishment status under the Income Tax Act.

- Conversion: A branch can be converted into a subsidiary corporation, but this is treated as a taxable disposition of assets absent specific rollover provisions under the Income Tax Act.

- Restrictions: Certain regulated industries — including banking, insurance, and telecommunications — impose additional federal licensing requirements beyond provincial registration.

Closing

A branch structure suits foreign corporations testing a market or managing short-term project work, where administrative simplicity outweighs the risk of unlimited parental liability. The absence of a separate legal entity keeps setup costs low, but full exposure of the parent's balance sheet to local claims is a material drawback.

Foreign corporations with limited, time-bound operations in Canada that do not require liability separation from the parent entity.

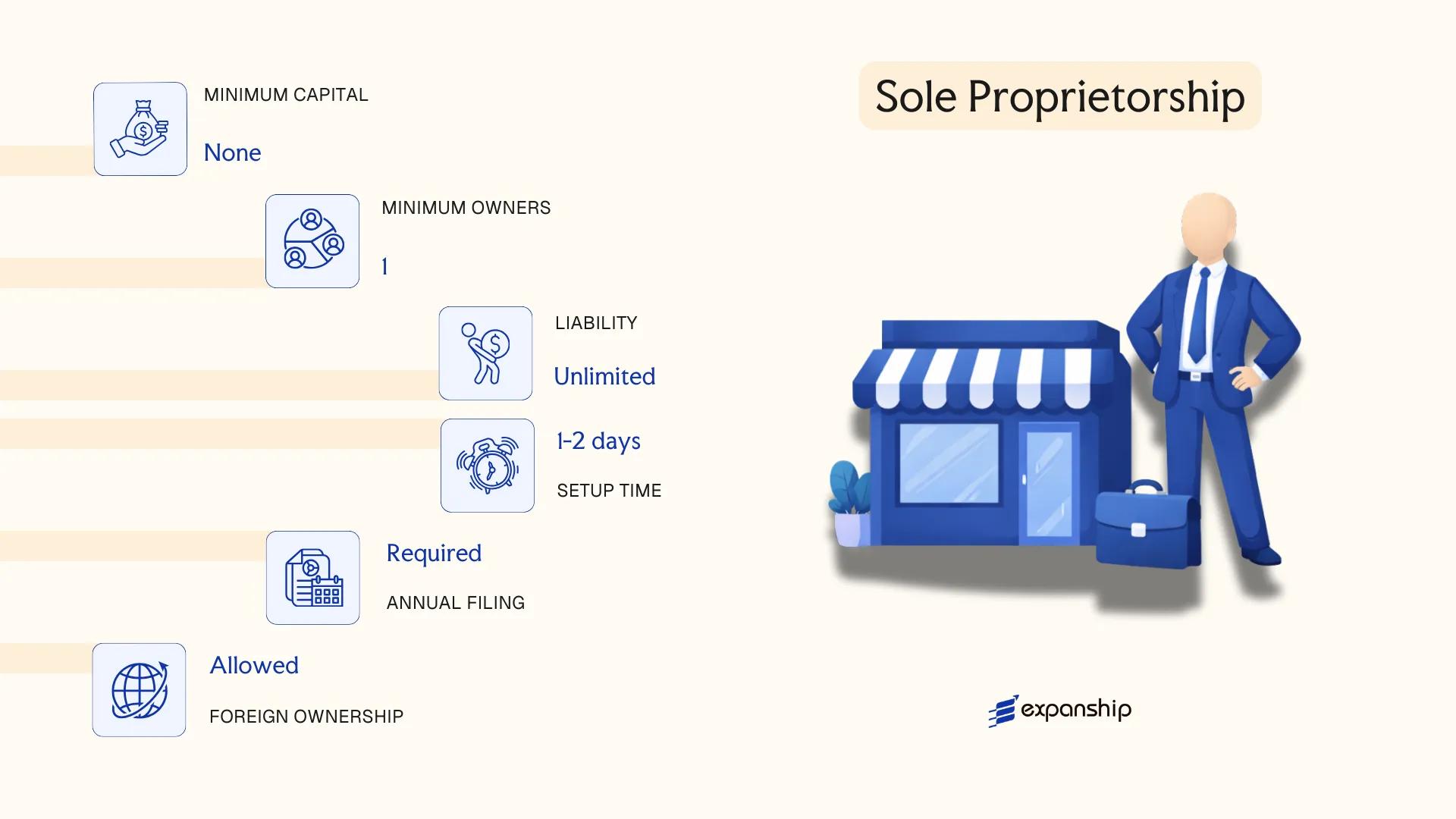

Sole Proprietorship

Sole proprietorship registration Canada follows no single federal statute. Unlike corporations, sole proprietorships are governed by provincial and territorial legislation, primarily through business names registration acts in each province. There is no separate legal personality — the business and the owner are the same legal entity.

Because the owner bears unlimited personal liability for all debts and obligations of the business, this structure carries meaningful financial exposure. Registration requirements vary by province: in Ontario, the Business Names Act requires registration within 60 days of commencing business under a name other than the owner's legal name; British Columbia operates under the Partnership Act, which covers sole proprietor name registrations; Alberta uses the Partnership Act (RSA 2000) for similar purposes. Operating under your own full legal name may not require registration in some provinces, though tax registration with the Canada Revenue Agency (CRA) is still necessary once income thresholds are met.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Members | Single proprietor | One individual only; no minimum share capital |

| Local Presence | Business address required | Provincial registration office varies by province |

| Capital | No minimum | No prescribed capital requirement under any provincial act |

| Privacy | Owner's name may appear on public registry | Varies by province; business name filings are generally public |

| Liability | Unlimited personal liability | Personal assets exposed to business creditors |

Focus Points

- Taxation: Business income reported on the owner's personal T1 return; no corporate tax applies; GST/HST registration required once annual taxable supplies exceed CAD 30,000; no withholding tax on business income distributions since no dividends are issued.

- Annual Compliance: No annual returns to a corporate registry; provincial business name registrations must be renewed periodically (typically every 5 years in Ontario).

- Treaty Access: No access to Canada's tax treaty network for reduced withholding rates, as treaties apply to corporate entities or individuals in specific capacities.

- Conversion: Can be converted to a corporation through asset transfer or business incorporation, triggering potential tax implications under the Income Tax Act.

- Restrictions: Cannot issue shares, raise equity capital, or operate across provinces under a single registration — separate registrations are required in each province.

Closing

A sole proprietorship suits self-employed individuals, freelancers, and single-operator service businesses where administrative simplicity outweighs the need for liability protection or external investment. The primary advantage is minimal setup cost and administrative burden; the clear limitation is unlimited personal liability, which makes this structure unsuitable for businesses carrying significant financial or legal risk.

Independent contractors, consultants, and sole traders testing a business concept before committing to incorporation.

How to Choose the Right Entity Type in Canada

Selecting the correct entity structure at incorporation affects tax treatment, liability exposure, and regulatory obligations for the entire life of your business. Understanding how to choose a business structure in Canada requires examining concrete consequences, not just general preferences.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences that are difficult to reverse.

- Registering a foreign entity under extra-provincial registration while conducting business that qualifies as a federal undertaking may place you in breach of the Canada Business Corporations Act, exposing the company to administrative dissolution.

- Choosing an Unlimited Liability Corporation without confirming your home jurisdiction recognises the pass-through treatment eliminates the tax efficiency the structure was designed to produce.

- Selecting a general partnership when your activity triggers securities regulation means your partners may carry personal liability for regulatory penalties, with no statutory cap.

- Forming a corporation when a limited partnership would serve a fund structure means imposing shareholder meetings, director filings, and annual returns that are structurally unnecessary for that purpose.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each require a different statutory framework.

- Ownership Structure: Multi-party ventures involving foreign investors may require share classes or partnership units that not all provincial acts accommodate equally.

- Tax Objectives: Access to Canada's tax treaty network generally requires a resident corporation, not a branch or transparent entity.

- Liability Exposure: Personal liability for debts is unlimited in a general partnership and sole proprietorship, which is material when your contracts carry significant financial risk.

- Substance Capacity: If you cannot maintain a genuine operating presence, structures requiring a resident director or registered office demand ongoing third-party appointments.

- Exit and Redomiciliation: The CBCA permits continuance in and out of the federal jurisdiction; not all provincial acts offer equivalent provisions.

Corporate Compliance Services for Companies in Canada

Maintain annual filings, registered office requirements, and director obligations under federal and provincial corporate legislation.

Conclusion

Selecting the right structure is the foundation of any Canada business incorporation summary guide. Federal corporations under the CBCA suit businesses seeking national name protection and interprovincial mobility. Provincial corporations work well for firms operating within a single province under statutes such as the OBCA or ABCA. The Unlimited Liability Corporation remains specific to Alberta, British Columbia, and Nova Scotia, primarily serving U.S. parent companies seeking flow-through tax treatment. Co-operatives fit member-owned enterprises with democratic governance requirements. Partnerships offer pass-through taxation without separate legal personality, while sole proprietorships carry the fewest formation requirements and the greatest personal exposure.

Federal corporations represent the most commonly registered entity type nationally. Regulatory oversight from Corporations Canada continues to modernize through digital filing systems and expanded online registry access, signaling a trajectory toward greater administrative efficiency. Your specific tax position, liability tolerance, and operational geography will ultimately determine which structure aligns with your business objectives.

How Expanship Can Assist You

Expanship Canada company incorporation services cover the full range of entities discussed in this blog — from federal CBCA corporations and provincial structures under acts like the OBCA or ABCA, to limited partnerships and ULCs. Your filing goes through Corporations Canada at the federal level, or the relevant provincial registrar, depending on the structure you select. Expanship's team handles both routes.

Getting the right entity registered is only part of the process. Ongoing obligations, registered office requirements, and director residency rules all require attention after incorporation.

Here is what Expanship provides:

- Government filing and registrar liaison (federal and provincial)

- Registered agent and registered office provision

- Document preparation and legalization

- Extra-provincial registration across Canadian provinces

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Canada to discuss which structure fits your business objectives.

Frequently Asked Questions (FAQ)

The private corporation incorporated under either the Canada Business Corporations Act (CBCA) or a provincial equivalent is the most frequently chosen structure. It offers shareholders limited liability, flexible share structures, and access to the small business deduction under the Income Tax Act.

A CBCA corporation holds automatic rights to use its name and conduct business across all provinces, whereas a provincially incorporated company must file extra-provincial registrations in each additional jurisdiction where it operates. Tax treatment under the Income Tax Act is identical for both; the distinction lies in administrative reach and name protection.

The Unlimited Liability Corporation (ULC), available in Alberta, British Columbia, and Nova Scotia, does not require public disclosure of shareholder information beyond what appears in the articles. Director information is generally on public record, but beneficial ownership details are subject to ongoing legislative reform at the federal level.

A sole proprietorship and a single-member corporation are both available to one individual. Partnerships, by definition, require at least two parties, and co-operative corporations under provincial co-operatives legislation require a minimum number of founding members, which varies by province.

Most structures are accessible to non-residents. Under the CBCA, however, at least 25 percent of directors must be Canadian residents, a requirement that does not apply to corporations incorporated in British Columbia or Nova Scotia. Foreign investors frequently use those two provinces, or opt for a limited partnership, to avoid the residency constraint.

Conversion between corporate forms is permitted through a process of continuance under section 187 of the CBCA, which allows a corporation to migrate into or out of federal jurisdiction. A general partnership cannot convert directly into a corporation without forming a new entity and transferring assets, as no statutory amalgamation route exists between unincorporated and incorporated structures.

Corporations incorporated under the CBCA or provincial statutes hold full legal personality, separate from their shareholders. General partnerships and sole proprietorships do not; liability flows directly to the individual partners or owner. Limited partnerships occupy a middle position: the limited partnership itself can hold assets, but the general partner remains personally exposed.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.