Key Takeaways

- Bolivia's commercial registry is administered by FUNDEMPRESA under the Ministry of Productive Development and Plural Economy, with all business structures required to register in the Registro de Comercio.

- The Sociedad de Responsabilidad Limitada (S.R.L.) is the most commonly registered entity for small and medium-sized businesses in Bolivia due to its simplified governance and capped partner structure.

- Foreign companies seeking a direct commercial presence in Bolivia can establish a Branch Office without creating a separate legal entity, though the parent company retains full liability for its operations.

- Bolivia applies a territorial tax system administered by the Servicio de Impuestos Nacionales (SIN), under which only domestic-source income is subject to corporate taxation.

Introduction to Entity Types in Bolivia

Bolivia is a landlocked country in central South America, bordered by Brazil, Paraguay, Argentina, Chile, and Peru. It is an independent republic governed under the 2009 Political Constitution of the State (Constitución Política del Estado). Company registration and commercial activity fall under the regulatory authority of the Fundación para el Desarrollo Empresarial (FUNDEMPRESA), which operates under the oversight of the Ministry of Productive Development and Plural Economy and maintains the Bolivian Commercial Registry (Registro de Comercio).

Bolivia applies a territorial tax system, meaning domestic-source income is subject to corporate taxation while foreign-source income is generally outside its scope.

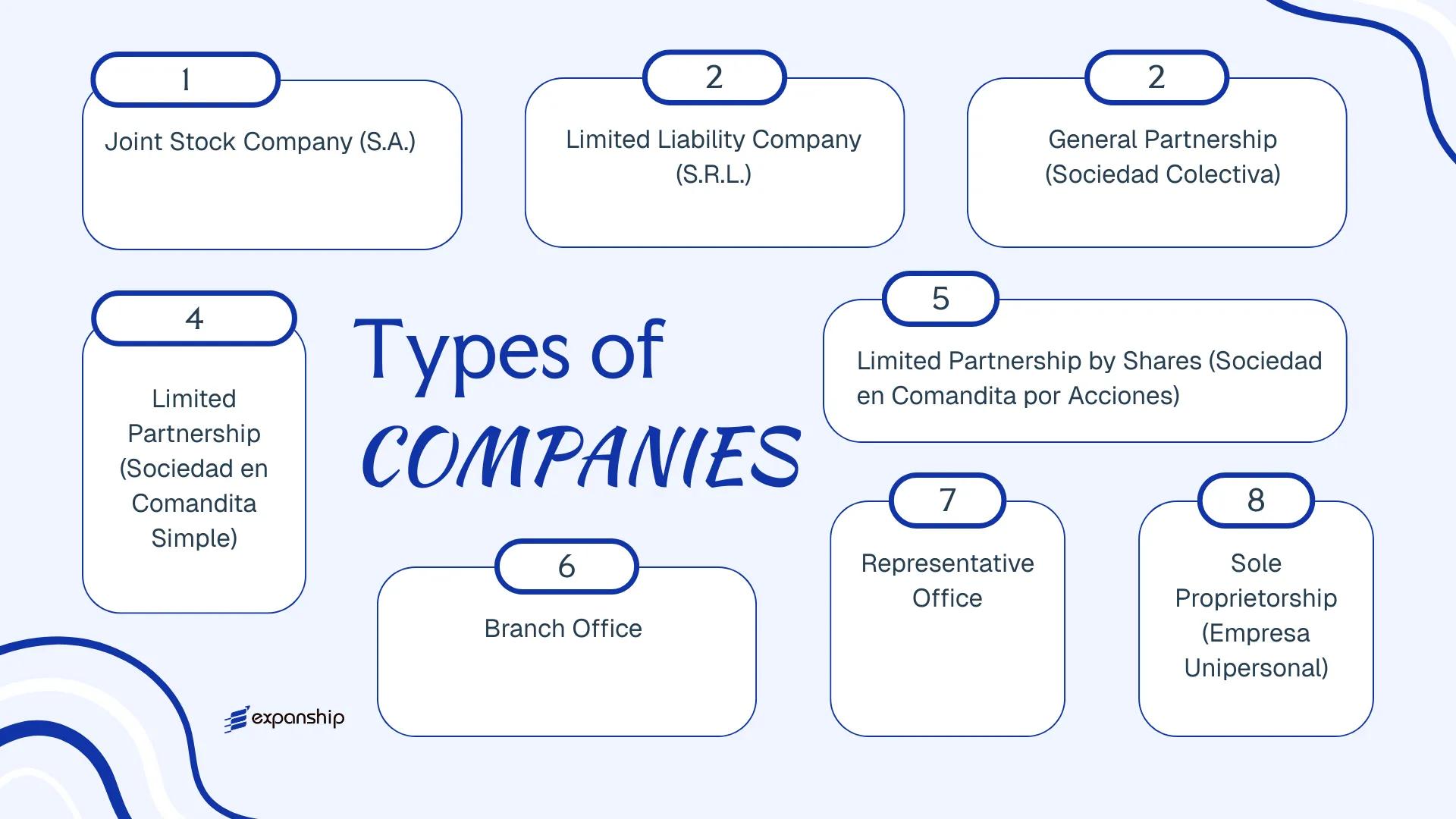

Businesses operating in the country can be established through several legal forms: Sociedad Anónima (S.A.), Sociedad de Responsabilidad Limitada (S.R.L.), Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and Empresa Unipersonal. Each of these structures carries distinct implications for liability, governance, capital requirements, and foreign ownership — all of which this article examines in detail.

An Overview of Business Structures in Bolivia

Bolivia's commercial legal framework, governed primarily by the Código de Comercio (Commercial Code, Decree Law No. 14379 of 1977) and supplemented by regulations from SEPREC (Servicio Plurinacional de Registro de Comercio), recognizes several distinct entity types for the overview of business structures in Bolivia. Each structure carries different implications for liability, governance, and capital requirements. The sections that follow examine each type in full detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Joint Stock Company | Limited to shares | Taxable | Permitted | 3 shareholders | SEPREC | Código de Comercio |

| Sociedad de Responsabilidad Limitada (S.R.L.) | Limited Liability Company | Limited to quota | Taxable | Permitted | 2 members | SEPREC | Código de Comercio |

| Sociedad Colectiva | General Partnership | Unlimited, joint | Taxable | Permitted | 2 partners | SEPREC | Código de Comercio |

| Sociedad en Comandita Simple | Limited Partnership | Mixed liability | Taxable | Permitted | 2 partners | SEPREC | Código de Comercio |

| Sociedad en Comandita por Acciones | Share-based Partnership | Mixed liability | Taxable | Permitted | 2 partners | SEPREC | Código de Comercio |

| Branch Office | Foreign entity extension | Parent liable | Taxable | Permitted | 1 (parent entity) | SEPREC | Código de Comercio |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | 1 (parent entity) | SEPREC | Código de Comercio |

| Empresa Unipersonal | Sole Proprietorship | Unlimited | Taxable | Permitted | 1 owner | SEPREC | Código de Comercio |

Each of these structures is examined in full in the sections below.

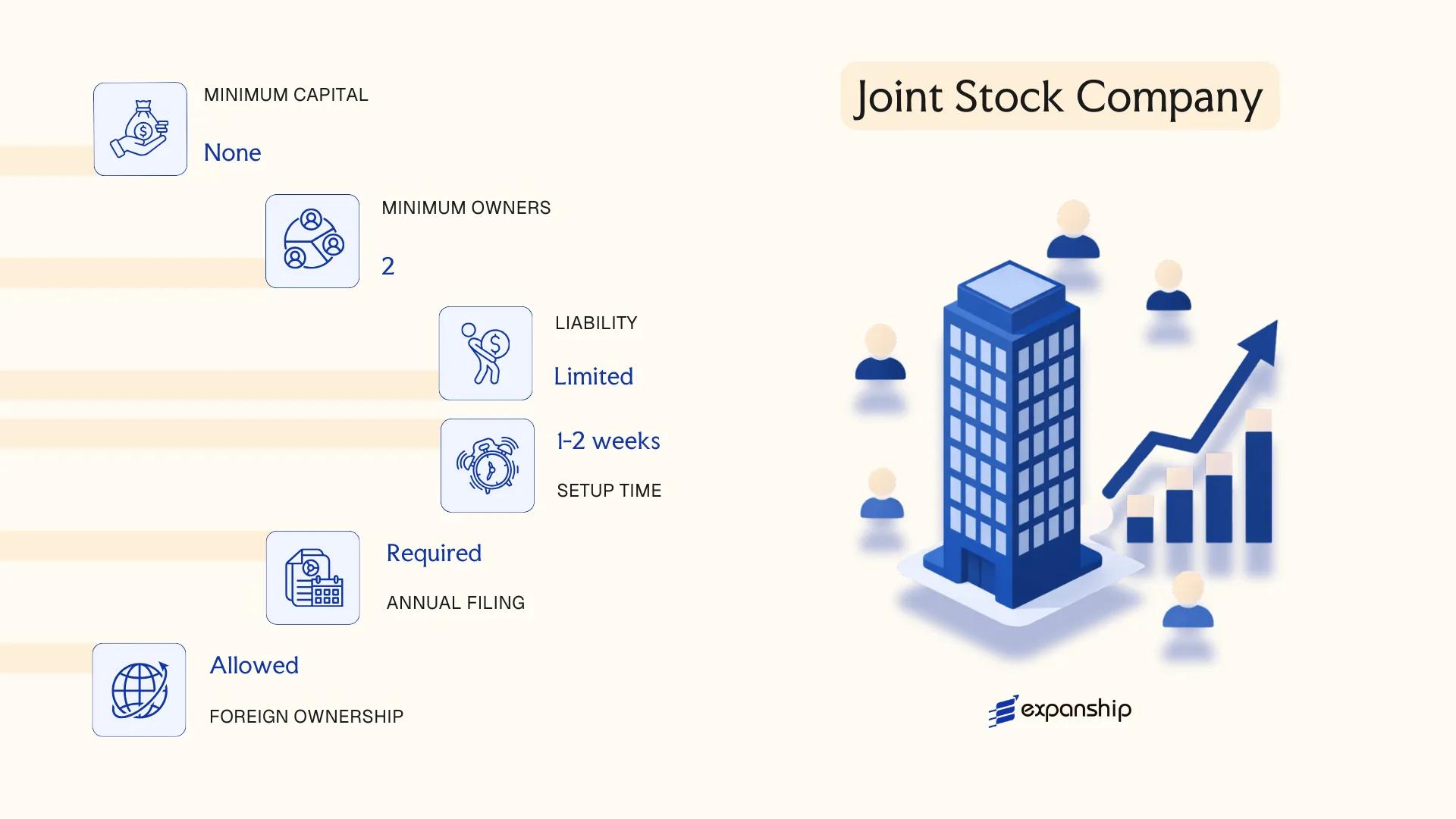

Sociedad Anónima (S.A.) — Joint Stock Company

Governed by the Código de Comercio de Bolivia (Commercial Code, Decree-Law No. 14379 of 1977), the Sociedad Anónima is the primary vehicle for large-scale commercial activity requiring public or institutional capital. Sociedad Anónima Bolivia S.A. formation results in an entity with full separate legal personality, meaning the company holds rights and obligations independently of its shareholders.

Shares are freely transferable by default, which distinguishes this structure from closed membership entities. Shareholder liability is capped at the value of subscribed capital, and the firm is registered with and supervised by SEPREC (Servicio Plurinacional de Registro de Comercio).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Separate legal personality; governed by Código de Comercio |

| Members | Shareholders (Accionistas) | Minimum 3 shareholders; no statutory maximum |

| Governing Body | Board of Directors (Directorio) | Minimum 3 directors; at least one must be resident in Bolivia |

| Local Presence | Registered address in Bolivia required | No mandatory registered agent; physical domicile is registered with SEPREC |

| Share Capital | Denominated in Bolivianos (BOB); minimum BOB 1,000 | 25% must be paid-up at incorporation; remainder within 2 years |

| Privacy | Shareholder names appear in public registry | Share registers are maintained but not always fully public |

Focus Points

- Taxation: Corporate income tax (IUE) is levied at 25% on net profits; VAT (IVA) applies at 13%; dividend distributions to non-residents attract a withholding tax of 12.5%; no stamp duty on share transfers under general provisions.

- Annual Compliance: Annual financial statements must be filed with SEPREC; audited accounts are required when capital or turnover exceeds statutory thresholds.

- Economic Substance: No formal economic substance legislation exists, though the physical domicile and local director requirements provide de facto operational presence obligations.

- Treaty Access: Bolivia has a limited double taxation treaty network; S.A. entities can access treaties within the Andean Community (Decision 578) framework.

- Conversion: An S.A. may be converted into an S.R.L. or another commercial form through a notarised shareholders' resolution and re-registration with SEPREC.

Closing

The S.A. suits businesses planning to raise external investment, operate at scale, or pursue eventual public listing, though the three-director minimum and mandatory local directorship add administrative overhead compared to simpler structures. One clear limitation is that the public nature of shareholder registration reduces ownership privacy.

The S.A. is most appropriate for medium-to-large enterprises, joint ventures with institutional partners, or businesses intending to issue shares to multiple investors.

Company Incorporation in Bolivia

Incorporate a Sociedad Anónima or other business entity in Bolivia with end-to-end support from SEPREC registration through to post-incorporation compliance.

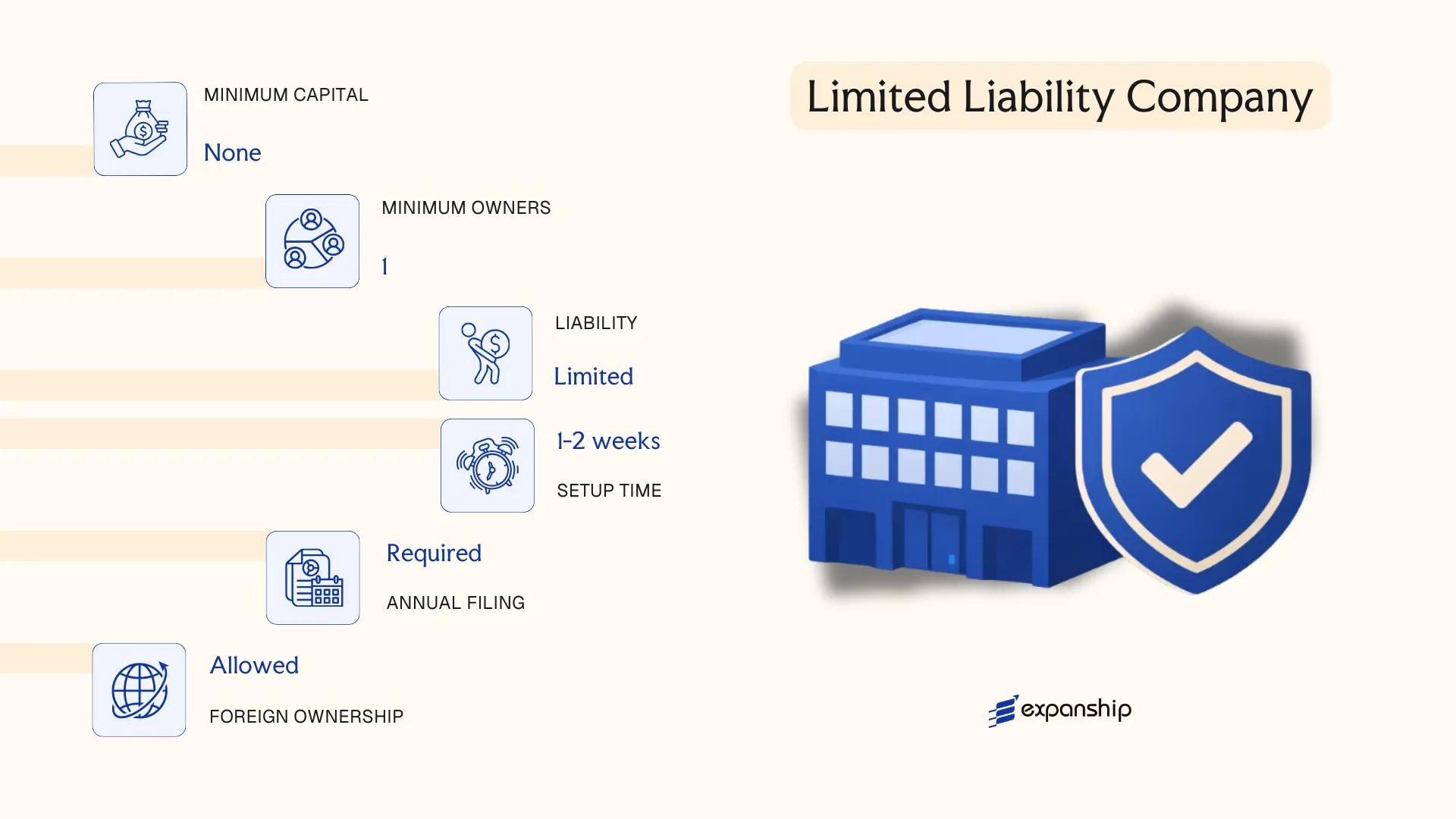

Sociedad de Responsabilidad Limitada (S.R.L.) — Limited Liability Company

The Sociedad de Responsabilidad Limitada Bolivia framework is governed by the Bolivian Commercial Code (Código de Comercio, Decree-Law No. 14379 of 1977), which remains the primary legislative instrument regulating commercial entities in the country.

Structured as a hybrid between a corporation and a partnership, the S.R.L. carries separate legal personality and limits each member's liability to their capital contribution. Ownership is divided into cuotas (quotas) rather than shares, which restricts free transferability and makes this structure more closely held by nature.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada | Separate legal entity; governed by Código de Comercio |

| Members | Referred to as socios (partners/members); minimum 2, maximum 25 | Exceeding 25 socios triggers mandatory conversion |

| Management | Managed by one or more gerentes (managers) | Managers may be socios or third parties |

| Local Presence | Registered address in Bolivia required | A legal domicile must be maintained with the relevant departmental registry |

| Capital | No statutory minimum; denominated in Bolivianos (BOB) | Capital divided into cuotas; paid-up requirements apply at registration |

| Privacy | Socios and gerentes recorded in the Commercial Registry (SEPREC) | Ownership information is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax (IUE) at 25%; VAT at 13% applies to commercial transactions; withholding taxes apply to dividend remittances and cross-border payments to non-residents.

- Annual Compliance: Annual financial statements must be filed with SEPREC; tax declarations submitted to the Servicio de Impuestos Nacionales (SIN).

- Quota Transfer Restrictions: Transfer of cuotas to third parties requires consent of members holding at least 75% of capital, as stipulated in the Commercial Code.

- Treaty Access: Bolivia has a limited double tax treaty network; confirm treaty eligibility before structuring cross-border operations.

- Conversion: An S.R.L. exceeding 25 socios must convert to a Sociedad Anónima under Article 195 of the Commercial Code.

Closing

The S.R.L. suits closely held trading operations, family businesses, and mid-market ventures where ownership control and administrative simplicity are priorities; the 25-member cap, however, makes it unsuitable for businesses anticipating broad investor participation.

Small to mid-sized businesses with a defined, stable group of owners seeking limited liability without the governance complexity of a Sociedad Anónima.

Partnerships in Bolivia [Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Bolivia's Commercial Code (Código de Comercio, Decree Law No. 14379 of 1977) governs all partnership structures, including the partnerships Bolivia Sociedad Colectiva framework and its variants. Unlike corporations, general partnerships do not provide limited liability to all partners, making the choice of structure a consequential one.

Three distinct partnership forms exist under Bolivian law, each defined by how liability is allocated among partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnerships (Sociedad Colectiva / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones) | Registered with SEPREC (Registro de Comercio) |

| Members | Partners (socios or accionistas depending on form); minimum 2, no statutory maximum | Sociedad Colectiva: all partners are general; Comandita forms split general and limited partners |

| Liability | General partners: unlimited personal liability; limited partners (comandita only): capped at capital contribution | Sociedad Colectiva has no limited partners |

| Local Presence | Registered legal address in Bolivia required | No statutory requirement for a local resident manager, but a registered agent is standard practice |

| Capital | Denominated in Bolivianos (BOB); no statutory minimum for Sociedad Colectiva or Sociedad en Comandita Simple | Sociedad en Comandita por Acciones issues shares; capital divided accordingly |

| Privacy | Partner names appear in the public commercial registry | No beneficial ownership confidentiality |

Focus Points

- Taxation: Partnerships are generally subject to corporate income tax (IUE) at 25%, VAT (IVA) at 13%, and transaction tax (IT) at 3%; profit distributions to foreign partners may attract withholding tax under domestic rules or applicable tax treaties.

- Annual Compliance: Annual financial statements must be filed with SEPREC; accounting records must be maintained in accordance with Bolivian accounting standards.

- Treaty Access: Bolivia has a limited tax treaty network; treaty benefits for partnership income depend on the partner's residency and the treaty's treatment of transparent entities.

- Conversion: Partnerships may be converted into other commercial forms (e.g., S.R.L. or S.A.) through a formal amendment process before SEPREC, subject to partner consent.

- Restrictions: General partners in all three forms cannot transfer their interest without unanimous consent of the remaining partners, unless the partnership agreement provides otherwise.

Sub-Types

Sociedad Colectiva

All partners carry unlimited joint and several liability for the firm's obligations. This structure is rarely used in practice and is generally unsuitable where personal asset protection is a priority.

Sociedad en Comandita Simple

This form introduces two partner classes: general partners (socios gestores) with unlimited liability who manage the business, and limited partners (socios comanditarios) whose liability is restricted to their capital contribution. It is used where passive investors want defined exposure without taking management responsibility.

Sociedad en Comandita por Acciones

The Bolivia Sociedad en Comandita por Acciones follows the same dual-partner model as the simple comandita but divides the limited partners' capital into transferable shares, which introduces equity-like features without full corporate structure. It suits ventures requiring capital from multiple passive investors while retaining centralized control with general partners.

Closing

Partnership structures in Bolivia are primarily used by family businesses or professional service groups where partners are willing to accept personal liability in exchange for simpler governance. The main limitation across all three forms is the unlimited exposure of general partners, which significantly narrows the commercial profile of entities suited to these structures.

Bolivian partnership structures are best suited for closely held family businesses or professional firms where all active partners have aligned interests and personal liability is an accepted operating condition.

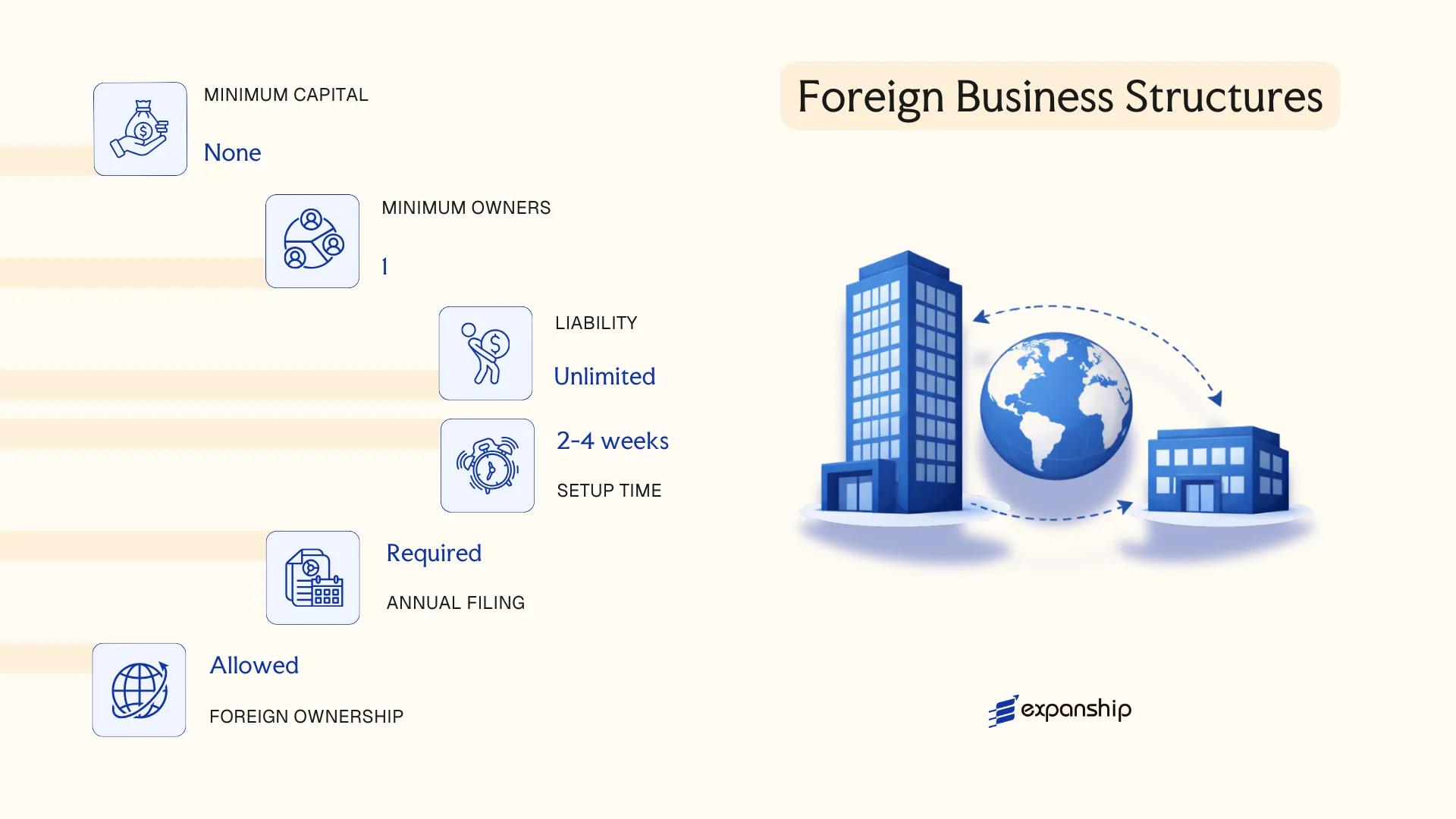

Foreign Business Structures in Bolivia [Branch Office, Representative Office]

Foreign companies seeking a formal presence without incorporating a separate entity can pursue a foreign branch office Bolivia registration under Bolivia's Commercial Code (Código de Comercio, Decree Law 14379 of 1977). Both the branch office and the representative office are recognised structures, though they differ significantly in operational scope and legal treatment.

Neither structure constitutes a separate legal person from the parent company. The parent entity remains directly liable for all obligations incurred by its Bolivian presence, and both structures must be registered with SEPREC (Servicio Plurinacional de Registro de Comercio).

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Authorised Representative | Locally appointed legal representative (apoderado) mandatory | Locally appointed legal representative mandatory |

| Permitted Activity | Full commercial and trading operations | Non-commercial activities only (market research, liaison, promotion) |

| Local Office | Physical address in Bolivia required | Physical address required |

| Capital | No statutory minimum; parent bears financial responsibility | No statutory minimum |

| Privacy | Parent company details disclosed in SEPREC registration | Parent company details disclosed |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax (IUE) at 25%; VAT at 13% applies to commercial transactions; a remittance tax (IUE-BE) of 12.5% applies to profits transferred to the foreign parent.

- Economic Substance: The branch must maintain genuine operational activity in Bolivia; a dormant or inactive registration risks administrative cancellation by SEPREC.

- Annual Compliance: Annual financial statements and renewal of the SEPREC registration are required; the appointed legal representative must hold valid, notarised powers of attorney.

- Restrictions: Representative offices cannot generate local revenue, sign commercial contracts, or invoice clients; any revenue-generating activity requires a branch or locally incorporated entity.

- Treaty Access: Bolivia has a limited tax treaty network; access to double taxation agreements depends on the parent company's jurisdiction of incorporation.

Sub-Types

Branch Office (Sucursal)

Operationally equivalent to the parent company within Bolivia, a sucursal can sign contracts, issue invoices, and conduct full trading activity. This structure is suited to foreign firms committing to active commercial operations rather than preliminary market entry.

Representative Office (Oficina de Representación)

Restricted to promotional and liaison functions, this structure cannot generate revenue or execute binding commercial agreements on behalf of the parent. It is typically used for Bolivia representative office setup during an exploratory phase before committing to full incorporation or a branch structure.

Closing

Both structures serve foreign businesses that require a regulated presence without the administrative burden of establishing a separate Bolivian legal entity; the key constraint is that the parent company bears unlimited liability for all local obligations.

Foreign companies already operating in Latin America that need a defined Bolivian presence for either active trading (branch) or non-commercial market entry (representative office), and whose parent entity can absorb direct legal and financial exposure.

Sole Proprietorship (Empresa Unipersonal)

The Empresa Unipersonal Bolivia sole proprietorship structure is governed primarily by the Bolivian Commercial Code (Código de Comercio, Decree-Law No. 14379 of 1977) and supplemented by subsequent regulatory provisions. Unlike partnership-based forms, this structure vests all ownership and management in a single individual.

Treated as a distinct legal entity upon registration, the Empresa Unipersonal separates the proprietor's business assets from personal patrimony to a degree, though liability protections are more limited than those afforded to an S.R.L. or S.A. Registration is processed through SEPREC (Servicio Plurinacional de Registro con Personalidad Jurídica), the national registry authority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresa Unipersonal) | Registered legal entity; not a mere informal trade name |

| Members | Single proprietor only | No minimum capital partner; one natural person exclusively |

| Local Presence | Registered business address required | Must maintain a physical commercial domicile within Bolivia |

| Capital | No statutory minimum; denominated in BOB | Capital declared at registration; reflects actual business activity |

| Privacy | Proprietor's name linked publicly to the entity | SEPREC records are accessible; limited confidentiality |

| Liability | Unlimited personal liability in practice | Asset separation is partial; courts may pierce the veil |

Focus Points

- Taxation: Subject to income tax under Impuesto sobre las Utilidades de las Empresas (IUE) at 25%; VAT (IVA) at 13% applies to transactions; no separate withholding tax regime distinct from general rules.

- Annual Compliance: Annual financial statements must be submitted to SEPREC and tax filings to the Servicio de Impuestos Nacionales (SIN).

- Treaty Access: Access to Bolivia's limited double tax treaty network is uncertain for sole proprietors; treaty relief is generally more reliably available to incorporated entities.

- Conversion: The structure can be converted into an S.R.L. or S.A. through a formal transformation process before SEPREC, though this requires full re-registration.

- Restrictions: Foreign nationals may face additional requirements to establish an Empresa Unipersonal, including proof of legal residency.

Closing Paragraph

This structure suits resident individuals conducting small-scale trading, consulting, or service activities where administrative simplicity outweighs the need for robust liability protection. The principal limitation is the absence of meaningful liability separation, which exposes the proprietor's personal assets to business creditors.

Bolivian resident individuals operating low-risk, single-owner businesses who prioritise minimal administrative overhead over liability protection.

How to Choose the Right Entity Type in Bolivia

Selecting how to structure your business presence is a legal and financial decision with binding consequences under Bolivian commercial law.

Why Your Entity Choice Matters

The wrong structure can create concrete operational and legal problems:

- Registering a foreign branch without meeting the local authorization requirements under the Código de Comercio exposes the entity to penalties and potential forced deregistration by SEPREC.

- Choosing a structure that falls outside Bolivia's tax treaty eligibility criteria means you cannot claim reduced withholding rates in counterpart jurisdictions.

- Forming an S.A. when a single-person consultancy is the intended activity adds mandatory audit and corporate governance obligations that an Empresa Unipersonal would not require.

- Selecting a partnership structure when liability exposure is a concern locks partners into unlimited personal liability for company debts.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each correspond to different permissible structures under Bolivian commercial law.

- Ownership Structure: An S.R.L. suits small, closed ownership groups with up to 25 quota-holders, while an S.A. accommodates larger or publicly tradeable capital structures.

- Tax Objectives: Your eligibility for Bolivia's tax regimes — including the RC-IVA or IUE — depends on the entity type and its registration classification with the SIN.

- Liability Exposure: Partnerships offer no liability shield; quota-based or share-based entities limit member exposure to their contribution.

- Substance Capacity: If you cannot maintain a physical presence and local decision-making, certain entity types will face heightened scrutiny from tax authorities.

- Exit and Conversion: Not all Bolivian structures permit straightforward conversion or redomiciliation; confirm this with SEPREC before incorporating.

Compliance Services for Companies in Bolivia

Ongoing compliance support for Bolivian entities, including annual filings, director obligations, and regulatory reporting with SEPREC and the SIN.

Conclusion

Incorporating a company in Bolivia requires matching your operational goals to the structural and regulatory realities of each available entity form. The Sociedad Anónima suits larger enterprises requiring transferable shareholding and capital market access, while the Sociedad de Responsabilidad Limitada remains the most commonly registered vehicle for small and medium-sized businesses due to its simplified governance and capped partner structure. Partnership forms serve closely held operations where personal liability is accepted by design. Branch offices give foreign firms a direct commercial presence without creating a separate legal entity, and the Empresa Unipersonal remains the entry point for individual operators.

Oversight from SEPREC and tax administration through the SIN continue to evolve, with Bolivia gradually refining its commercial registry processes. Your choice of structure will determine filing obligations, liability exposure, and how your business interacts with Bolivian counterparties for years ahead.

How Expanship Can Assist You

Expanship's Bolivia company incorporation services cover the full process of establishing and maintaining a legal presence in the country. From registering a Sociedad Anónima or Sociedad de Responsabilidad Limitada with FUNDEMPRESA — Bolivia's commercial registry — to fulfilling ongoing obligations with the Servicio de Impuestos Nacionales, your business gets hands-on support at every stage.

Our corporate services team in Bolivia handles the documentation, filings, and regulatory liaison your structure requires:

- Preparation and legalization of incorporation documents

- Registered agent and local office provision

- Filing coordination with FUNDEMPRESA and relevant municipal authorities

- Post-incorporation compliance management, including annual renewals

- Banking introduction assistance for corporate account opening

Reach out to Expanship Bolivia to discuss the right structure for your business.

Frequently Asked Questions (FAQ)

The Sociedad de Responsabilidad Limitada (S.R.L.) is the most frequently registered entity in Bolivia. Its combination of limited liability protection and relatively straightforward administration under the Bolivian Commercial Code makes it the default choice for small and medium-sized businesses.

A Branch Office is not a separate legal entity; it remains an extension of its foreign parent and carries no independent liability shield. An S.R.L., by contrast, holds its own legal personality under Bolivian law, meaning the parent company's exposure is contained. Compliance obligations for both structures are administered through FUNDEMPRESA, but the S.R.L. requires locally appointed management and a distinct capital structure.

Among registered business structures, the S.R.L. offers comparatively limited public disclosure, as quota ownership details are recorded in founding documents rather than a broadly searchable public registry. Nominee arrangements are not a formal feature of Bolivian corporate law, though legal representation structures can be used. Disclosure requirements are ultimately governed by the Commercial Code and applicable tax regulations administered by the Servicio de Impuestos Nacionales (SIN).

Not all structures are available to a sole individual. An S.R.L. requires a minimum of two and a maximum of twenty-five quota-holders, so a single person cannot form one alone. The Empresa Unipersonal is the designated structure for single-person business activity, while partnerships by definition require at least two participants.

Foreign nationals can incorporate an S.R.L. or S.A., and may also establish a Branch Office of a foreign entity. Registration requires obtaining a tax identification number (NIT) from the SIN and completing the FUNDEMPRESA registration process. There are no nationality restrictions on ownership, though certain regulated sectors may impose additional requirements.

Conversion between entity types is permitted under the Bolivian Commercial Code, which allows transformation from one corporate form to another subject to shareholder approval and regulatory re-registration. An S.R.L. can be converted to an S.A. when the business grows and requires an expanded shareholder base or capital structure. The process involves amending the constitutive documents and updating records with FUNDEMPRESA.

Not all do. The S.A., S.R.L., Sociedad en Comandita por Acciones, and Empresa Unipersonal each hold separate legal personality distinct from their owners. General partnerships (Sociedad Colectiva) and simple limited partnerships (Sociedad en Comandita Simple) also acquire legal personality upon registration, but partners in a Sociedad Colectiva retain unlimited personal liability regardless.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.