Key Takeaways

- Foreign investors can hold 100% equity in a Bangladesh private limited company across most sectors, with oversight managed through the Bangladesh Investment Development Authority (BIDA) rather than mandatory local partnership requirements.

- Companies listed on a Bangladeshi stock exchange benefit from a reduced corporate tax rate of 20% under the National Board of Revenue (NBR) framework, creating a meaningful cost differential for businesses with longer-term structuring flexibility.

- The Companies Act 1994, administered by the Registrar of Joint Stock Companies and Firms (RJSC), governs an online registration process that consolidates incorporation steps into a single portal, reducing the administrative friction typical of comparable South Asian jurisdictions.

- Export-oriented manufacturers gain access to dedicated infrastructure and fiscal incentives through Export Processing Zones regulated by the Bangladesh Export Processing Zones Authority (BEPZA), an operational advantage that is structurally embedded rather than dependent on discretionary approvals.

Bangladesh is an independent republic in South Asia, bordered by India on three sides and Myanmar to the southeast, with direct access to the Bay of Bengal. The benefits of incorporating in Bangladesh draw attention from foreign investors across manufacturing, technology, and services sectors, supported by a regulatory environment that has progressively opened to overseas capital. Company registration is administered by the RJSC, the Registrar of Joint Stock Companies and Firms, which operates under the Ministry of Commerce.

Foreign businesses typically establish a presence through a private limited company. The country operates a territorial tax system with treaty-based components, meaning locally sourced income is taxed domestically while double taxation agreements govern cross-border obligations with select trade partners.

Bangladesh maintains a generally open posture toward foreign direct investment, permitting full overseas ownership across a wide range of sectors with limited restrictions. This article examines the principal advantages that make Bangladesh company formation a substantive option for businesses seeking a presence in South Asia.

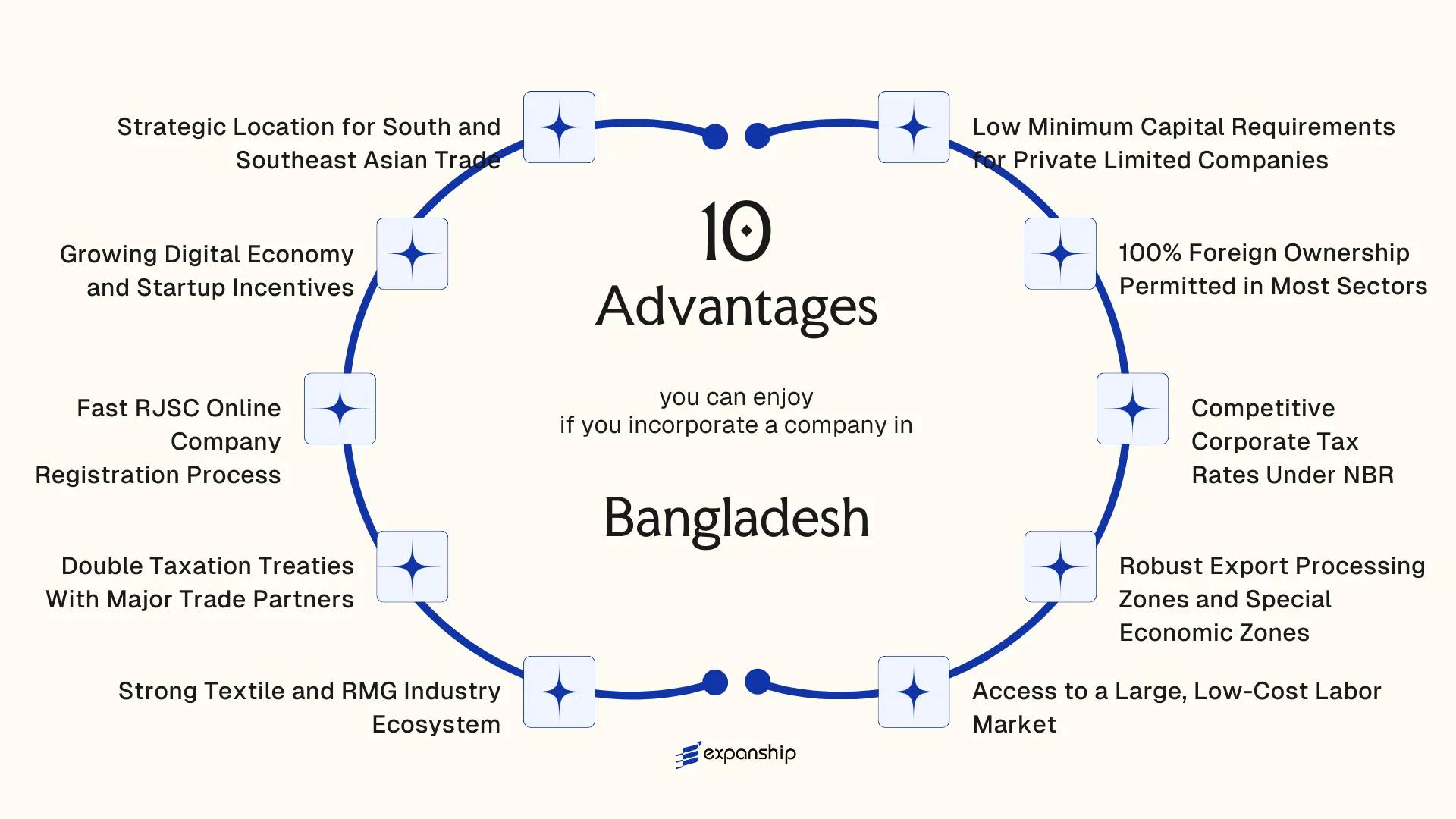

Low Minimum Capital Requirements for Private Limited Companies

Bangladesh private limited company low capital requirement rules are among the most accessible in South Asia. Under the Companies Act 1994, there is no statutory minimum paid-up capital prescribed for private limited companies.

What the Rules Actually Allow

Your business can be incorporated with a nominal paid-up capital, such as BDT 1, though most firms register with a modest authorized capital to allow future share issuance flexibility. The Registrar of Joint Stock Companies and Firms (RJSC) does not impose a capital threshold that would otherwise force early-stage investors to lock up significant funds before operations begin.

Why This Matters Structurally

For foreign investors, the absence of a mandatory minimum paid-up capital requirement under the Companies Act 1994 means startup costs are determined by your operational plan, not by a regulatory floor. Capital that would otherwise sit idle in a corporate account can instead be deployed directly into business activity from the outset.

You can incorporate a private limited company through RJSC without meeting a minimum capital threshold, keeping your initial financial commitment aligned with actual business needs.

100% Foreign Ownership Permitted in Most Sectors

100% foreign ownership Bangladesh company is permitted across most sectors under the Bangladesh Investment Development Authority (BIDA), which governs foreign direct investment entry rules. This means your business can be wholly owned by non-resident shareholders without requiring a local partner or co-investor, a structural freedom that significantly reduces negotiation complexity and preserves full decision-making authority.

The legal basis for this stems from the Foreign Private Investment (Promotion and Protection) Act, 1980, which guarantees equal treatment of foreign and domestic capital. Under this framework, repatriation of profits and invested capital is also protected, giving foreign owners a degree of financial control that is directly tied to ownership rights.

A small number of sectors remain restricted or reserved for local ownership, including arms manufacturing, forest plantation in reserved areas, and certain security printing activities. Outside these carve-outs, your entity can hold 100% of shares regardless of the investor's nationality or country of residence.

Practical advantages of full foreign ownership in this structure include:

- No obligation to share profits with a mandatory local partner

- Full control over internal governance, shareholder agreements, and equity transfers

- No dilution risk arising from government-imposed ownership caps

- Flexibility to restructure the share register without local consent requirements

Incorporate a Company in Bangladesh

Set up a wholly foreign-owned private limited company in Bangladesh with full BIDA compliance.

Competitive Corporate Tax Rates Under NBR

Bangladesh corporate tax rate advantages NBR make the jurisdiction's fiscal structure worth examining closely for any foreign investor evaluating South Asia. Under the Income Tax Act 2023, the National Board of Revenue administers corporate income tax, and the standard rate for non-listed companies sits at 27.5%. Listed companies that meet stock exchange disclosure requirements pay a reduced rate of 22.5%, creating a direct financial incentive for firms considering a public listing.

Certain sectors attract even lower rates. Textile manufacturers, for instance, have historically received preferential treatment through reduced applicable rates, and companies operating in designated export-oriented categories can access further concessions under specific NBR provisions.

| Company Type | Applicable Tax Rate |

|---|---|

| Non-listed private company | 27.5% |

| Stock exchange-listed company | 22.5% |

| One Person Company (OPC) | 22.5% |

| Mobile financial services company | 37.5% |

For a foreign-owned private limited company incorporated through RJSC, the 27.5% rate applies by default. That figure sits below the global average corporate rate, which the Tax Foundation has tracked at approximately 23% unweighted but closer to 26% on a GDP-weighted basis, placing Bangladesh within a broadly competitive range for emerging markets.

Tax holidays of up to ten years are available for qualifying investments in priority sectors, administered through the Bangladesh Investment Development Authority in coordination with NBR. Eligibility depends on sector classification, investment threshold, and location, so the benefit is structured rather than universal.

Robust Export Processing Zones and Special Economic Zones

Bangladesh Export Processing Zone business benefits are administered primarily through the Bangladesh Export Processing Zones Authority (BEPZA), a statutory body established under the Bangladesh Export Processing Zones Authority Act, 1980. BEPZA oversees eight operational EPZs, including those in Dhaka, Chittagong, and Comilla, creating geographically distributed access to export-oriented infrastructure.

Companies operating within EPZs receive a ten-year corporate income tax exemption from the date of commercial production, with a reduced rate applicable for the following period. This structure significantly lowers your effective tax burden during the early operational years when capital recovery is most critical.

The Bangladesh Economic Zones Authority (BEZA) governs Special Economic Zones under the Bangladesh Economic Zones Act, 2010. Unlike EPZs, SEZs accommodate domestic-market-oriented industries alongside export operations, which gives your business greater flexibility in revenue sourcing.

Keep these points in mind:

- Foreign firms in EPZs must export 100% of production

- BEPZA offers one-stop service for permits, utilities, and customs clearance within zones

- SEZ investors may qualify for duty-free import of capital machinery under BEZA gazette notifications

- Land lease terms in SEZs are generally long-duration, reducing relocation risk

- EPZ tax holidays apply from the date of commercial production, not incorporation

Foreign companies operating inside EPZs are exempt from complying with certain provisions of local labor laws, including restrictions that would otherwise limit night-shift work for women.

Access to a Large, Low-Cost Labor Market

Bangladesh's low-cost labor market advantage is among the most structurally significant reasons foreign manufacturers and service firms establish a local presence. With a population exceeding 170 million and a median age below 28, the working-age population is large, growing, and concentrated in urban industrial centers like Dhaka, Chittagong, and Gazipur.

What the Cost Structure Means for Your Business

The national minimum wage in Bangladesh is set sectorally by the Minimum Wage Board under the Wages and Employment Act. For the garment sector, the minimum wage was revised to BDT 12,500 per month in late 2023 — a figure that remains substantially below comparable rates in Vietnam, Indonesia, or India. For labor-intensive operations, this differential directly compresses your per-unit production cost.

Outside the garment sector, wages across manufacturing, back-office processing, and light assembly remain competitive. Your fixed payroll obligations are lower at comparable output volumes than in most regional peers.

Workforce Scale and Skill Availability

Bangladesh produces over 300,000 university graduates annually, with technical and vocational training institutions operating under the Bangladesh Technical Education Board (BTEB). This creates a measurable supply of mid-level technical staff and supervisory workers without the premium typical of tighter labor markets.

For firms hiring workforce in Bangladesh to support export-oriented production or services, the combination of volume and cost structure reduces the break-even threshold on new operations considerably.

Plan Your Entry Into Bangladesh's Labor Market

Speak with Expanship's corporate specialists to understand how to structure your Bangladesh entity and workforce setup in compliance with local labor and employment regulations.

Strong Textile and RMG Industry Ecosystem

The Bangladesh RMG industry ecosystem benefits any foreign firm entering the garment or textile sector, because the surrounding infrastructure, supplier base, and policy environment have been built specifically around export-oriented manufacturing.

- Over 4,500 active garment factories operate across the country, meaning your business can source cut-and-make capacity, fabric, accessories, and finishing services from within a single geographic cluster rather than managing cross-border supply chains.

- The Bangladesh Garment Manufacturers and Exporters Association (BGMEA) and the Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA) function as structured industry bodies that facilitate buyer-supplier connections and provide sector-level compliance data, reducing your onboarding research burden.

- Under the Export Policy Order issued by the Ministry of Commerce, RMG exporters qualify for back-to-back letters of credit, allowing fabric and input procurement on deferred payment terms without tying up working capital.

- Textile and garment exporters benefit from a reduced corporate tax rate of 12% under the National Board of Revenue (NBR) framework, compared to the standard 27.5% rate applicable to non-publicly traded companies.

- The concentration of spinning, weaving, dyeing, and finishing mills in areas like Gazipur and Narayanganj shortens your supplier lead times and reduces logistics costs between raw material sourcing and finished goods export.

Double Taxation Treaties With Major Trade Partners

Bangladesh double taxation treaty advantages are most visible when you examine the actual withholding tax reductions that apply to cross-border income flows. Under agreements administered through the National Board of Revenue (NBR), reduced rates on dividends, royalties, and interest replace the standard domestic withholding rates, directly reducing the tax cost of repatriating profits or licensing intellectual property from a Bangladeshi entity.

The country maintains DTTs with over 30 jurisdictions, including the United States, United Kingdom, Germany, Canada, India, China, Japan, and Singapore. Each treaty defines specific reduced rates by income category, so the applicable benefit depends on both the treaty partner and the nature of the payment.

For foreign investors, the practical gain is the elimination of dual taxation on the same income stream. Without treaty protection, income earned in Bangladesh and remitted abroad could face taxation in both jurisdictions. A treaty overrides that outcome by establishing which state holds primary taxing rights.

A Singaporean parent company receiving dividends from its Bangladeshi subsidiary may qualify for a reduced withholding rate under the Bangladesh-Singapore DTAA, rather than the standard domestic rate under the Income Tax Act 1984, preserving a measurable margin on each distribution.

Treaty eligibility generally requires the recipient entity to meet the residency conditions specified in the relevant agreement.

Fast RJSC Online Company Registration Process

The Bangladesh RJSC online registration advantages are primarily structural: the Registrar of Joint Stock Companies and Firms (RJSC) operates a dedicated e-registration portal that allows applicants to submit incorporation documents, pay government fees, and obtain a Certificate of Incorporation without attending in-person. For a foreign investor managing the process remotely, this removes the need to be physically present in Dhaka during the initial setup phase.

Name clearance, document submission, and fee payment are all handled through the RJSC portal in a sequential digital workflow. Processing timelines for a private limited company under this system can fall within a matter of days once documentation is complete. That speed directly reduces the gap between a business decision and legal entity formation.

Key practical advantages of the RJSC e-registration system include:

- Digital name clearance reduces back-and-forth communication delays

- Incorporation fees are paid online, eliminating the need for local bank visits at the registration stage

- The Certificate of Incorporation is issued electronically, allowing post-incorporation steps to begin promptly

Foreign shareholders must still obtain an Encashment Certificate from a scheduled bank confirming inward remittance of paid-up capital before the RJSC will finalize incorporation of a foreign-invested company.

Growing Digital Economy and Startup Incentives

Bangladesh's digital economy startup incentives are anchored in formal policy, not aspiration. The government's Digital Bangladesh initiative, formalized under the ICT Act and extended through successive national budgets, has produced a suite of tax and regulatory advantages specifically targeting technology-driven businesses.

Tax Exemptions for IT-Enabled Services

Under the Income Tax Ordinance, software development firms, IT-enabled service companies, and certain digital businesses registered with the Bangladesh Hi-Tech Park Authority (BHTPA) qualify for a tax exemption on income, with the benefit extending through 2024 and subject to periodic renewal by the National Board of Revenue (NBR). For a foreign-owned tech firm, this means operating during early growth years without the drag of corporate income tax.

Startup Registration and Institutional Support

The Startup Bangladesh Company Limited, a government-backed venture fund operating under the ICT Division, provides seed financing and co-investment to qualifying early-stage firms. Foreign companies establishing subsidiary entities in Bangladesh can participate in this ecosystem provided they meet local registration requirements under the RJSC.

Incentives Under Hi-Tech Parks

Businesses operating within BHTPA-designated Hi-Tech Parks access additional benefits:

- Exemption from value-added tax on certain services

- Reduced utility tariffs within park boundaries

- Dedicated one-stop service units for faster regulatory clearance

- Access to technology infrastructure maintained under a single authority

Your business benefits from a policy environment where the statutory incentives are tied to defined industrial classifications, reducing ambiguity when structuring for tax purposes.

Strategic Location for South and Southeast Asian Trade

Bangladesh's strategic location South Asia trade position places it at a junction that few countries in the region can replicate. Sitting at the northeastern edge of the Indian subcontinent, the country shares land borders with India on three sides and Myanmar to the southeast, while its southern coastline opens directly into the Bay of Bengal. That geography translates into overland connectivity to a consumer market exceeding 1.4 billion people in India alone, alongside maritime access to Southeast Asian ports.

The Chittagong Port handles the majority of the country's seaborne trade and connects to key shipping lanes running between South Asia, Southeast Asia, and East Asia. For manufacturers or distributors, proximity to these lanes reduces transit times compared to landlocked production bases elsewhere in South Asia. Mongla Port, the secondary deep-sea facility, provides an additional outlet particularly relevant for goods moving toward the western Indian states.

From a practical standpoint, your firm benefits from several geographically-driven advantages:

- Overland access to India's northeastern states through the Benapole and Akhaura land ports, which are among the busiest bilateral trade crossings in the region

- Proximity to Myanmar's border crossings, offering a staging point for trade into ASEAN markets

- Bay of Bengal positioning that connects to major transshipment hubs including Colombo, Singapore, and Port Klang without requiring passage through congested straits

- Alignment with the proposed Bangladesh-China-India-Myanmar (BCIM) Economic Corridor, which would formalize multimodal trade routes across the subregion

For businesses oriented toward South or Southeast Asian distribution, the geographic footprint reduces both logistics cost and supply chain exposure tied to single-route dependency.

Why Bangladesh Stands Out Against Regional Alternatives

Investors evaluating Bangladesh against regional alternatives typically weigh it against India, Vietnam, and Myanmar, three markets that attract similar types of export-oriented and manufacturing foreign investment. The Bangladesh vs regional alternatives business advantages become clearer when examined across specific, structural parameters rather than broad economic comparisons.

What the comparison reveals is a consistent pattern: Bangladesh holds measurable advantages in labor cost positioning, preferential market access, and sectoral fiscal incentives, particularly for firms in manufacturing and export-driven industries. Vietnam offers a developed SEZ infrastructure, but its minimum wage levels have risen steadily. India presents a far larger consumer market, yet its corporate tax compliance burden and federal-state regulatory layers add operational friction that smaller foreign entities often underestimate.

| Parameter | Bangladesh | India | Vietnam | Myanmar |

|---|---|---|---|---|

| Standard Corporate Tax Rate | 27.5% (listed); 30% (non-listed) | 25.17% (with surcharge) | 20% | 22% |

| Minimum Paid-Up Capital (Private Ltd) | No statutory minimum | No statutory minimum | ~VND 1 (no minimum for most sectors) | MMK equivalent varies by sector |

| 100% Foreign Equity Permitted | Yes, in most sectors | Sector-specific FDI caps apply | Yes, with sector exceptions | Yes, with sector-specific restrictions |

| LDC GSP Trade Preferences | Yes (EU, UK, Canada, others) | No | No | Partially suspended |

| Export Processing Zone Availability | Yes, under BEPZA | Yes, under SEBI/SEZ framework | Yes, under MPI | Limited, underdeveloped |

| Labor Cost (Garment Sector) | Among the lowest regionally | Higher | Rising significantly | Comparable, but political risk is elevated |

Compliance Services for Companies in Bangladesh

Ongoing corporate compliance in Bangladesh involves filings with the RJSC, annual returns, and NBR tax obligations. Expanship manages these requirements to keep your entity in good standing.

Conclusion

The benefits of incorporating in Bangladesh converge around a set of structural conditions that are difficult to replicate elsewhere in South Asia: a statutory corporate tax rate that drops to 20% for listed entities, unrestricted foreign equity ownership across most sectors, and export-oriented infrastructure through EPZs administered by BEPZA. Together, these features form a coherent framework for foreign capital, not an isolated incentive here or there.

That said, the fit between your business and this jurisdiction depends on sector, scale, and structure. A manufacturing firm targeting EU or US apparel buyers operates in a fundamentally different environment than a digital startup seeking NBR's reduced tax treatment for registered IT companies. The rules under the Bangladesh Investment Development Authority (BIDA) and the Companies Act 1994 apply consistently, but their practical value shifts depending on what you are building and how you intend to operate.

For foreign investors who have assessed those variables, the path forward involves engaging the Registrar of Joint Stock Companies and Firms (RJSC) process, satisfying any applicable BIDA registration requirements, and structuring the entity correctly from the outset. Decisions made at incorporation, particularly around share structure, repatriation planning, and sector classification, have long-term compliance and tax implications that are far easier to address before registration than after.

Start Your Bangladesh Company Formation With Expanship

Engaging Expanship for Bangladesh company formation with Expanship connects your business to a firm that handles the full registration process under the Registrar of Joint Stock Companies and Firms (RJSC), alongside ongoing compliance obligations imposed by the Bangladesh Investment Development Authority (BIDA) and the National Board of Revenue (NBR). The entity types covered in this blog, including private limited companies and entities operating within Export Processing Zones, each carry distinct filing requirements that Expanship manages directly.

Expanship's service scope covers the complete incorporation and maintenance cycle for your entity:

- Document preparation, notarization, and legalization for foreign directors and shareholders

- Registered agent and registered office provision within Bangladesh

- Government filing and direct liaison with the RJSC, BIDA, and relevant sector regulators

- Post-incorporation compliance management, including annual return filings and statutory updates

- Corporate bank account introduction assistance with locally licensed banks

- Work permit and expatriate quota support where applicable under BIDA guidelines

Reach out to Expanship Bangladesh to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

There is no statutory minimum paid-up capital requirement for a private limited company under the Companies Act 1994. In practice, BIDA recommends a minimum foreign investment threshold for entities seeking a work permit or investor visa, and specific sector regulators may impose their own capital floors, so the applicable figure varies by industry and intended activities.

The Registrar of Joint Stock Companies and Firms (RJSC) online portal has reduced the name clearance and incorporation filing process to a matter of days for straightforward applications. Full registration, including obtaining a Trade License and Tax Identification Number (TIN), generally takes between one and three weeks depending on document completeness and the applicant's sector.

Bangladesh has signed double taxation avoidance agreements (DTAAs) with a number of major trade and investment partners, including the United Kingdom, China, India, and several other countries. These treaties allocate taxing rights between jurisdictions and typically reduce withholding tax rates on dividends, interest, and royalties paid from Bangladesh to treaty-country residents. The National Board of Revenue (NBR) administers treaty application in practice.

The standard corporate tax rate for non-publicly traded companies in Bangladesh is set by the Finance Act, which the NBR updates annually. As of recent Finance Act provisions, the general rate for non-listed companies has been 27.5%, though listed companies and entities in specific sectors such as export-oriented industries or Special Economic Zones may qualify for reduced rates or tax holidays. Confirming the current rate against the applicable Finance Act for the relevant income year is advisable.

Companies established within Export Processing Zones (EPZs) administered by the Bangladesh Export Processing Zones Authority (BEPZA) receive a distinct regulatory and fiscal framework that differs from mainland registration. Benefits typically include tax holidays for a defined initial period, duty-free import of machinery and raw materials, and exemptions from certain local taxes. These concessions are governed by the BEPZA Act and are conditional on meeting export performance requirements.

There is no universal statutory minimum for local employment applicable to all sectors, but work permit regulations administered by BIDA effectively limit the ratio of foreign employees a company may hire relative to its local workforce. BIDA guidelines generally require companies to demonstrate that local talent is unavailable before approving expatriate positions, which in practice creates an incentive to hire locally from the country's labor market.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.