Key Takeaways

- The Registrar of Joint Stock Companies and Firms (RJSC), operating under Bangladesh's Ministry of Commerce, is the central authority governing company formation, dissolution, and statutory filings across all entity types.

- Bangladesh's Private Limited Company remains the most widely registered structure in the country, offering liability protection and accessibility to both resident founders and foreign investors under the Companies Act 1994.

- Foreign businesses entering the Bangladeshi market without committing to a local subsidiary can operate through a Branch Office, Liaison Office, or Representative Office, each carrying distinct regulatory obligations.

- Solo founders in Bangladesh have a dedicated structure available to them in the form of the One Person Company, which provides limited liability without requiring multiple shareholders or partners.

Introduction to Entity Types in Bangladesh

Bangladesh sits in South Asia, bordered by India on three sides and Myanmar to the southeast, with the Bay of Bengal forming its southern coastline. It is an independent sovereign republic. Businesses registering in the country fall under the authority of the Registrar of Joint Stock Companies and Firms (RJSC), which operates under the Ministry of Commerce and administers company formation, dissolution, and ongoing statutory filings.

The country operates a residence-based tax system with corporate income tax applicable to locally registered entities, and rates vary by sector and listing status.

Several distinct corporate structures are available under Bangladeshi law. These include the Public Limited Company, Private Limited Company, One Person Company, General Partnership, Limited Partnership, Branch Office, Liaison Office, Representative Office, and Sole Proprietorship. Each structure carries different requirements around ownership, liability, and regulatory obligations.

This article examines each of these types of business entities in Bangladesh — covering formation requirements, ownership rules, liability exposure, and the regulatory framework that applies to each.

An Overview of Business Structures in Bangladesh

Under the Companies Act 1994 and its subsequent amendments, six primary corporate structures are available to investors and entrepreneurs operating within the country. The Registrar of Joint Stock Companies and Firms (RJSC&F) serves as the central registration authority for most of these entities. Each structure carries distinct rules on liability, membership, governance, and permitted activities.

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Incorporated company | Limited | Taxed | Permitted | 7 shareholders | RJSC&F | Companies Act 1994 |

| Private Limited Company | Incorporated company | Limited | Taxed | Permitted | 2 shareholders | RJSC&F | Companies Act 1994 |

| One Person Company | Incorporated company | Limited | Taxed | Permitted | 1 shareholder | RJSC&F | Companies Act 1994 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Permitted | 2 partners | RJSC&F | Partnership Act 1932 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Permitted | 2 partners | RJSC&F | Partnership Act 1932 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Restricted | N/A | BIDA / Bangladesh Bank | Foreign Private Investment Act 1980 |

| Liaison Office | Foreign entity extension | Parent liable | Exempt | Not permitted | N/A | BIDA / Bangladesh Bank | Foreign Private Investment Act 1980 |

| Representative Office | Foreign entity extension | Parent liable | Exempt | Not permitted | N/A | BIDA / Bangladesh Bank | Foreign Private Investment Act 1980 |

| Sole Proprietorship | Unregistered / registered | Unlimited | Taxed | Permitted | 1 owner | Local authority / trade body | No single governing act |

Each of these structures is examined in full in the sections below.

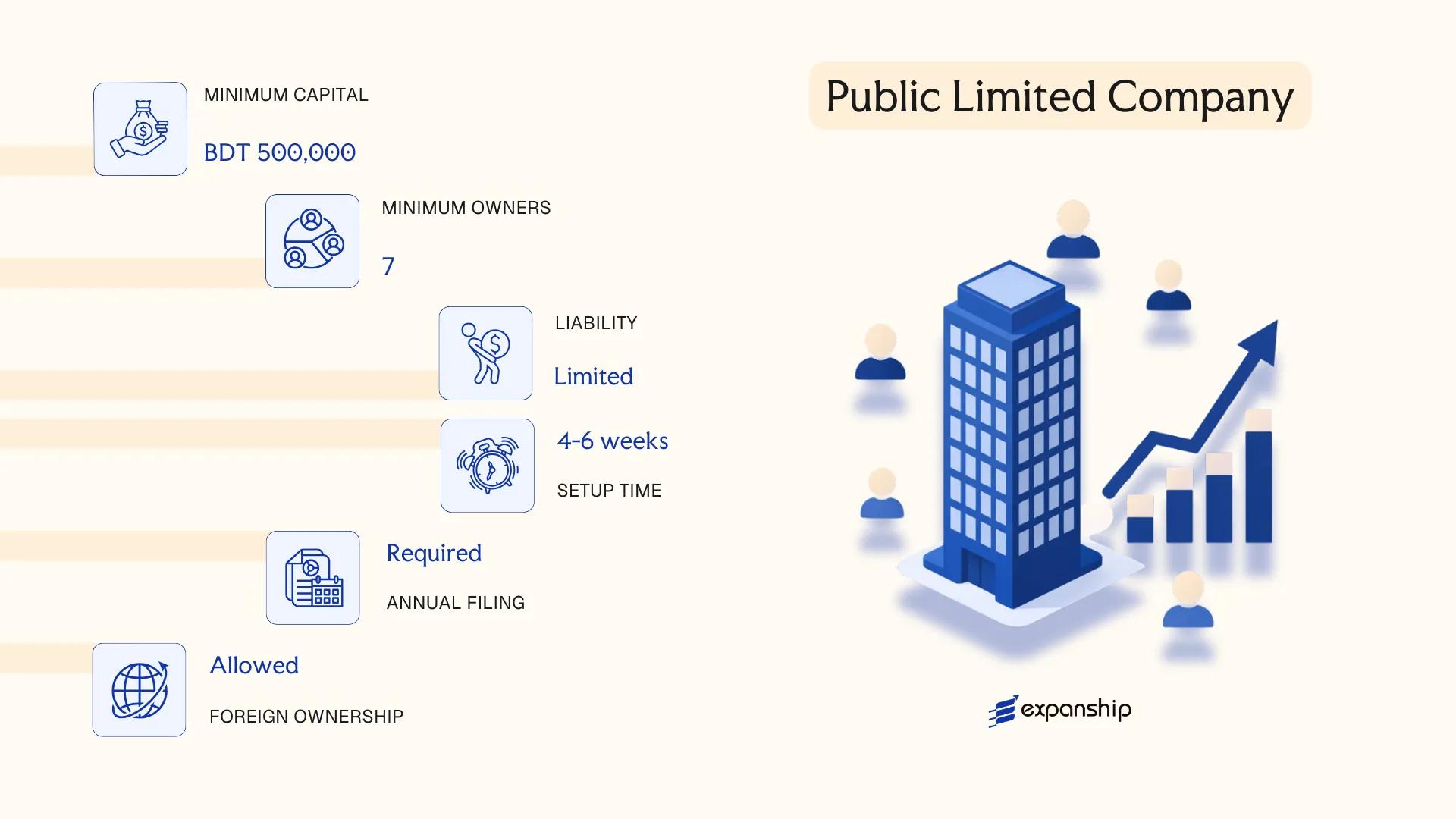

Public Limited Company (PLC)

A public limited company Bangladesh PLC is governed by the Companies Act 1994, administered by the Registrar of Joint Stock Companies and Firms (RJSC). The entity carries a separate legal personality, meaning its obligations are distinct from those of its shareholders, and liability is capped at the amount unpaid on shares held.

Shares in a PLC may be offered to the general public, and the entity may apply for listing on the Dhaka Stock Exchange (DSE) or Chittagong Stock Exchange (CSE). Listing is regulated by the Bangladesh Securities and Exchange Commission (BSEC) under the Securities and Exchange Ordinance 1969 and subsequent rules.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under the Companies Act 1994 |

| Members | Min. 7 shareholders; no maximum | Directors: min. 3; at least one must be a resident director |

| Local Presence | Registered office in Bangladesh required | RJSC filing address; cannot be a PO Box |

| Share Capital | BDT denominated; no statutory minimum for incorporation | Listed companies must meet BSEC's minimum paid-up capital thresholds |

| Share Transferability | Shares freely transferable | Restrictions on transfer are not permitted as in a private company |

| Privacy | Shareholder and director details filed publicly with RJSC | Financial statements publicly accessible once listed |

Focus Points

- Taxation: Corporate income tax applies at 20% for listed companies and 27.5% for non-listed PLCs; VAT at 15% on applicable supplies; withholding tax obligations apply on dividends, service payments, and contracts; stamp duty payable on share transfers — full guidance available via the National Board of Revenue (NBR).

- Annual Compliance: Mandatory annual general meeting (AGM), audited financial statements, and annual returns filed with RJSC; listed entities face additional continuous disclosure obligations under BSEC rules.

- Conversion: A private limited company may convert to a PLC by passing a special resolution and satisfying RJSC and, where applicable, BSEC requirements.

- Foreign Ownership: No general restriction on foreign shareholding; sector-specific caps may apply in areas such as banking, insurance, and media.

- Treaty Access: Bangladesh has a network of double taxation agreements (DTAs); a locally incorporated PLC qualifies as a tax resident entity for treaty purposes.

Closing

A PLC suits businesses seeking public capital markets access, large-scale operations, or broad institutional investment. The ability to list on the DSE or CSE is a structural advantage unavailable to private entities, though the compliance burden — particularly under BSEC's continuous disclosure and corporate governance requirements — is substantially higher than for closely held structures.

A PLC is most appropriate for large enterprises, joint ventures targeting public fundraising, or businesses with a clear roadmap toward a stock exchange listing in Bangladesh.

Company Incorporation in Bangladesh

Expanship assists with RJSC registration, document preparation, and post-incorporation compliance for companies incorporating in Bangladesh.

Private Limited Company (Ltd.)

A private limited company Bangladesh Ltd structure is governed by the Companies Act 1994, administered by the Registrar of Joint Stock Companies and Firms (RJSC). The entity carries a distinct legal personality, meaning it exists separately from its shareholders, and liability is confined to each member's unpaid share capital.

Registration with RJSC requires filing a Memorandum and Articles of Association, along with prescribed forms and fees. Once incorporated, the firm can hold assets, enter contracts, and sue or be sued in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Separate legal entity under Companies Act 1994 |

| Members | Min. 2 shareholders, Max. 50 | Directors: Min. 2; at least one must be a natural person |

| Local Presence | Registered office address in Bangladesh | Must be a physical address; P.O. Box not accepted |

| Capital | BDT; no statutory minimum paid-up capital for most sectors | Some regulated sectors impose sector-specific minimums |

| Share Transfer | Restricted by Articles | Shares cannot be offered to the general public |

| Privacy | Financials filed with RJSC; publicly searchable | Beneficial ownership disclosure required |

Focus Points

- Taxation: Subject to corporate income tax (currently 27.5% for non-listed companies), 15% VAT on applicable supplies, withholding tax obligations on payments to contractors and employees, and stamp duty on share transfers and instruments.

- Annual Compliance: Must file audited financial statements and annual returns with RJSC; AGM required within 18 months of incorporation and annually thereafter.

- Treaty Access: Eligible for Bangladesh's tax treaty network, covering double taxation relief on dividends, royalties, and capital gains with treaty partner countries.

- Foreign Ownership: Up to 100% foreign equity permitted in most sectors; restricted or prohibited in certain sectors under the Bangladesh Investment Development Authority (BIDA) framework.

- Conversion: Can convert to a public limited company subject to RJSC approval and compliance with minimum membership requirements under the Companies Act 1994.

Closing

This structure suits trading operations, foreign subsidiaries, joint ventures, and holding arrangements where liability protection and operational permanence are priorities. The defined shareholder cap and transfer restrictions, however, limit equity fundraising from the public.

Foreign investors and local entrepreneurs establishing an operational or subsidiary entity in Bangladesh who require limited liability without public capital-raising obligations.

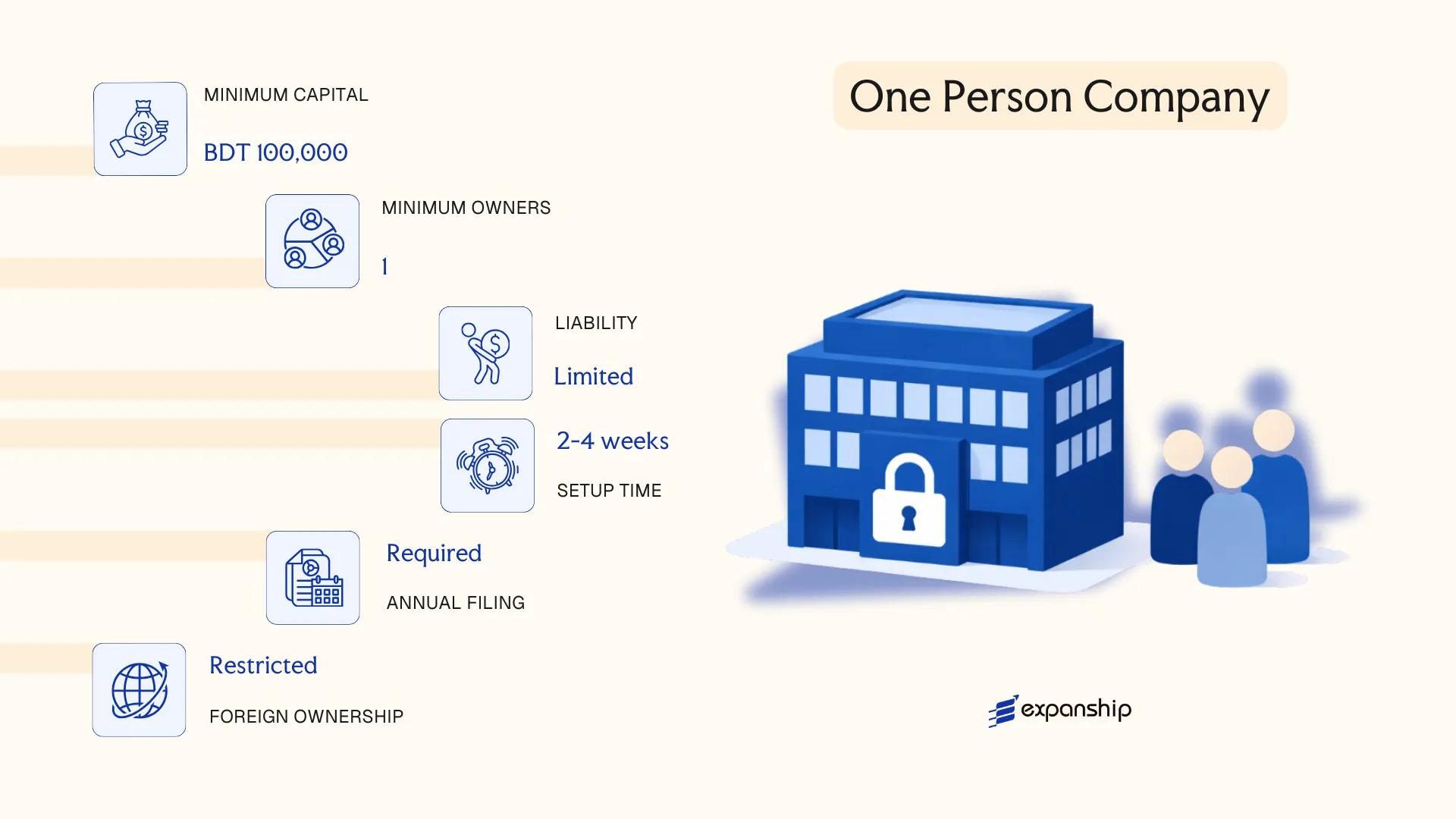

One Person Company (OPC)

Introduced under the Companies Act 1994 (as amended by the Companies (Amendment) Act 2020), the one person company Bangladesh framework allows a single individual to form a legally distinct corporate entity. The OPC carries separate legal personality, meaning the company's liabilities do not extend to the owner's personal assets beyond their subscribed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company with single ownership | Governed under the Companies Act 1994; registered with the Registrar of Joint Stock Companies and Firms (RJSC) |

| Members | 1 shareholder (minimum and maximum); 1 nominee required | The nominee assumes ownership if the sole member dies or becomes incapacitated |

| Directors | Minimum 1 director | The sole shareholder may also serve as the sole director |

| Local Presence | Registered office address in Bangladesh required | A physical or registered address must be maintained for official correspondence |

| Capital | BDT; no statutory minimum paid-up capital specified | Authorised capital determines stamp duty payable at incorporation |

| Privacy | Shareholder details filed with RJSC | Records are accessible through the RJSC public registry |

Focus Points

- Taxation: Subject to standard corporate income tax (currently 27.5% for non-listed companies), VAT obligations under the VAT and Supplementary Duty Act 2012, and applicable withholding tax on payments such as rent, service fees, and dividends.

- Annual Compliance: Annual general meetings, audited financial statements, and annual returns must be filed with the RJSC.

- Conversion: An OPC must convert to a private or public limited company if paid-up capital exceeds BDT 50 million or annual turnover crosses prescribed thresholds.

- Restrictions: The sole member must be a natural person; corporate entities cannot form an OPC. The member must also be a Bangladeshi national or resident, which effectively closes this structure to foreign investors.

- Treaty Access: As a domestic company, an OPC may access Bangladesh's double taxation agreements, subject to meeting substance and residency conditions.

Closing

An OPC suits Bangladeshi nationals operating small-to-medium enterprises who require limited liability without the administrative complexity of a multi-shareholder structure. The single-ownership model simplifies governance, though the nationality restriction on membership is a firm barrier for foreign entrepreneurs.

Bangladeshi resident individuals seeking limited liability protection for a sole-owned business without bringing in additional shareholders.

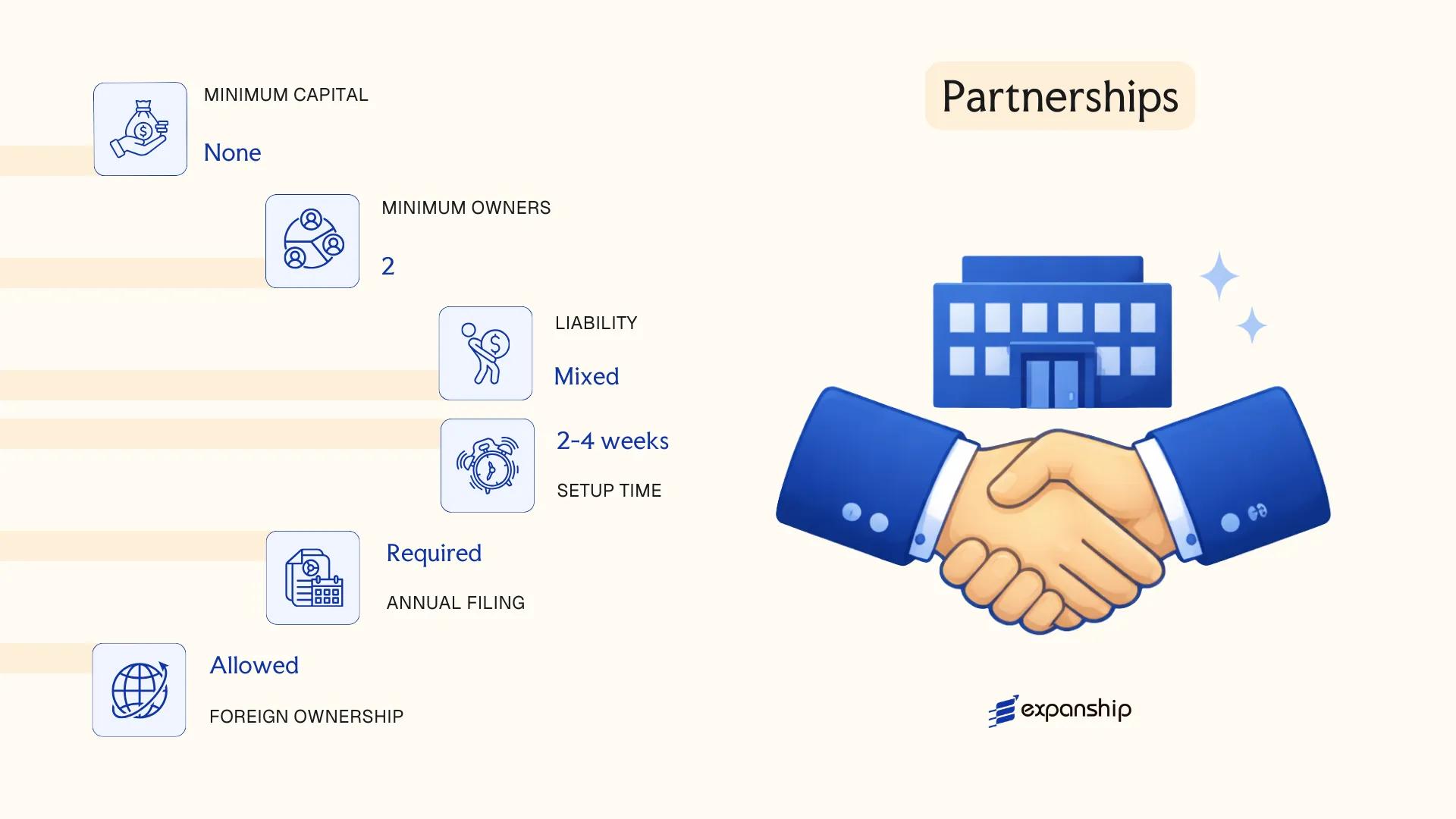

Partnerships [General Partnership, Limited Partnership]

Governed by the Partnership Act 1932, partnerships in Bangladesh do not possess a separate legal personality distinct from their partners. This means partners bear personal liability for the firm's obligations, though the structure offers operational simplicity compared to incorporated entities. Partnership business registration Bangladesh falls under the jurisdiction of the Registrar of Joint Stock Companies and Firms (RJSC&F), and while registration is not mandatory under the Act, an unregistered firm loses the right to sue third parties or enforce contractual claims in court.

Two recognised forms exist: the general partnership and the limited partnership. Both share the same governing statute, but differ significantly in how liability is allocated among members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated firm | No separate legal personality; partners are the business |

| Members | Partners; minimum 2, maximum 20 (general); 20 for banking firms capped at 10 | Limits set under the Partnership Act 1932 and Companies Act 1994 |

| Liability | Unlimited (general partners); limited to capital contribution (limited partners) | Limited partners cannot participate in management |

| Local Presence | Registered office address required at RJSC&F | Physical address within Bangladesh mandatory for filing |

| Capital | BDT; no statutory minimum | Defined by the partnership deed |

| Privacy | Partnership deed is filed but not widely publicised | Moderate privacy; deed details accessible via RJSC&F |

Focus Points

- Taxation: Firms are taxed as separate assessable entities under the Income Tax Act 2023 at applicable rates; partners are then taxed on distributed profits, creating a degree of double taxation. VAT registration obligations apply based on annual turnover thresholds.

- Annual Compliance: Filing of income tax returns with the National Board of Revenue (NBR) is required annually; no annual return filing mandated at RJSC&F post-registration, though deed amendments must be notified.

- Treaty Access: Partnerships generally do not qualify as residents for double tax treaty purposes, limiting access to Bangladesh's tax treaty network.

- Conversion: A partnership may convert to a private limited company under the Companies Act 1994, though the process requires fresh incorporation rather than a statutory conversion mechanism.

- Restrictions: Foreign nationals face significant restrictions on forming or joining partnerships, as RJSC&F registration and foreign ownership in partnerships are subject to regulatory scrutiny under investment laws.

Sub-Types

General Partnership

All partners carry unlimited joint and several liability for the firm's debts. General partnership Bangladesh formation suits small domestic businesses and professional service firms where all partners actively participate in management and decision-making.

Limited Partnership

Under the Partnership Act 1932, a limited partnership includes at least one general partner with unlimited liability alongside one or more limited partners whose exposure is confined to their agreed capital contribution. Limited partnership Bangladesh law restricts limited partners from taking part in day-to-day management; doing so forfeits their limited liability protection.

Closing

A partnership structure in Bangladesh is suited to small-scale domestic trading, professional services, or family-run businesses seeking a low-cost entry structure, with the key advantage of straightforward formation. The principal drawback is unlimited personal liability for general partners, which poses meaningful financial risk as the business scales.

Partnerships are best suited for small domestic businesses or professional practitioners seeking a simple, low-cost operating structure without the compliance burden of incorporation.

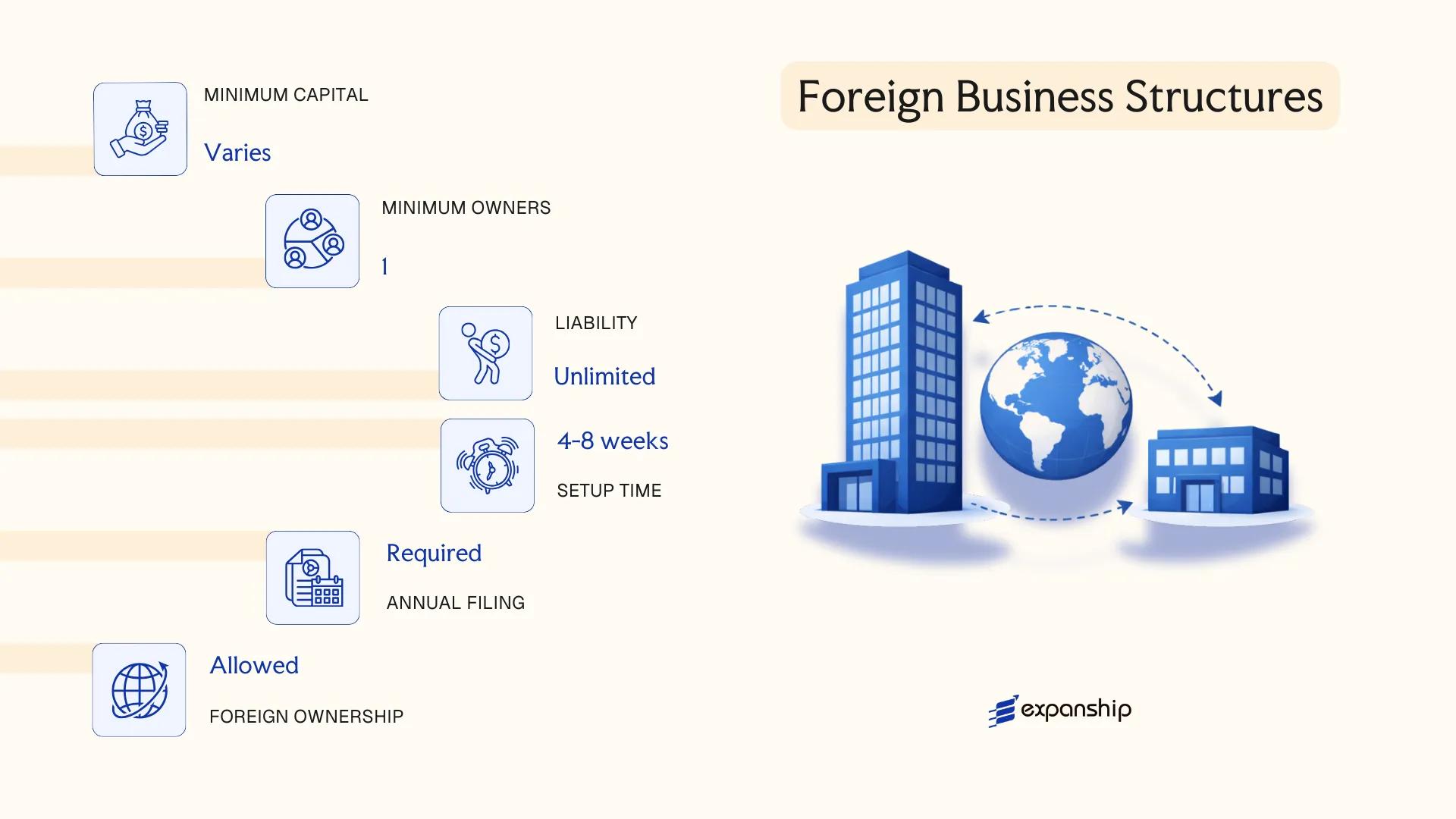

Foreign Business Structures [Branch Office, Liaison Office, Representative Office]

Foreign companies seeking a presence in Bangladesh without incorporating a separate local entity operate under the Foreign Private Investment (Promotion and Protection) Act, 1980, alongside the Companies Act, 1994. Crucially, none of these structures constitute a separate legal entity — the parent company retains full legal and financial responsibility for all activities conducted in Bangladesh.

Registration and approvals are handled through the Bangladesh Investment Development Authority (BIDA), with additional sector-specific clearances sometimes required from the Bangladesh Bank or relevant ministries.

Key Characteristics

| Requirement | Branch Office | Liaison Office | Representative Office |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Commercial operations, revenue generation | Promotion, coordination, market research only | Limited promotion; no commercial activity |

| Registered with | BIDA + RJSC | BIDA | BIDA |

| Local Office | Mandatory physical office required | Mandatory physical office required | Mandatory physical office required |

| Capital Requirement | Inward remittance of working capital required (minimum amount set by BIDA at time of approval) | No minimum capital; funded by parent via remittance | No minimum capital; funded by parent via remittance |

| Revenue Generation | Permitted | Not permitted | Not permitted |

Focus Points

- Taxation: Branch offices are subject to corporate income tax at 37.5% on Bangladesh-sourced income; liaison and representative offices generate no local income and are generally not subject to corporate tax, though VAT registration may be required for branch offices engaged in taxable supplies.

- Repatriation: Profits remitted abroad by a branch office are subject to a branch profits remittance tax of 20% under the Income Tax Act, 2023.

- Annual Compliance: All three structures must renew their BIDA registration periodically and submit audited accounts or activity reports to BIDA; branch offices have additional filing obligations with the RJSC.

- Restrictions: Liaison and representative offices cannot generate local revenue, sign commercial contracts, or invoice clients; any income-earning activity requires conversion to a branch office or incorporated entity.

- Conversion: Converting a branch office to a locally incorporated private limited company is possible but requires fresh incorporation with the RJSC and does not constitute a legal merger of entities.

Sub-Types

Branch Office

A foreign company registration as a branch office in Bangladesh allows revenue-generating commercial activity, making it the only structure among the three that can execute contracts and bill local clients directly.

Liaison Office

A liaison office Bangladesh registration restricts the entity strictly to non-commercial functions — market research, promoting the parent's products, and coordinating between the parent and local counterparts — with all operational costs funded by the parent abroad.

Representative Office

Representative office Bangladesh setup functions similarly to a liaison office but is typically used by foreign firms in financial services or specific regulated sectors, subject to additional approvals from the Bangladesh Bank where applicable.

A foreign company branch office in Bangladesh suits firms that need operational capability without incorporating locally, though the absence of limited liability means the parent bears all legal exposure. Liaison and representative offices serve companies in early-market or relationship-management phases where revenue generation is not yet the objective.

Foreign firms testing the Bangladesh market or coordinating regional operations without committing to full local incorporation.

Sole Proprietorship

A sole proprietorship is the simplest form of business registration in Bangladesh, operating without a dedicated corporate statute. Unlike companies formed under the Companies Act 1994, this structure has no separate legal personality — the owner and the business are treated as one entity in law, meaning personal assets remain exposed to business liabilities. Sole proprietorship registration in Bangladesh is primarily governed at the local government level through trade license issuance rather than through a central company registry.

The trade license, issued by the relevant City Corporation, Pourashava, or Union Parishad depending on location, is the foundational requirement for operating as a sole trader. The National Board of Revenue (NBR) handles tax registration, and a TIN (Taxpayer Identification Number) is required for most commercial activities. There is no minimum capital requirement, and the setup process is relatively straightforward compared to incorporated structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality; owner bears full personal liability |

| Member Type | Proprietor | Single individual only; no partners or shareholders |

| Members | Minimum: 1 / Maximum: 1 | Cannot have co-owners; adding a partner requires dissolving and restructuring |

| Local Presence | Trade License address required | Must correspond to an actual place of business within the issuing municipality |

| Capital | BDT; no statutory minimum | Capital is entirely at the proprietor's discretion |

| Privacy | No public registry filing | Business details are not centrally published, though trade license records are held locally |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act 2023 at applicable individual slab rates; VAT registration required if annual turnover exceeds the threshold set by NBR; no separate corporate tax applies.

- Annual Compliance: Trade license must be renewed annually with the issuing local authority; TIN-based income tax returns must be filed with NBR each year.

- Treaty Access: As an unincorporated entity, a sole proprietorship does not qualify as a "resident" company for the purposes of Bangladesh's tax treaties, limiting access to reduced withholding tax rates.

- Conversion: Conversion to a Private Limited Company requires fresh incorporation under the Companies Act 1994 and transfer of assets; there is no automatic conversion mechanism.

- Foreign Ownership: Foreign nationals face significant restrictions and, in practice, cannot operate a sole proprietorship in Bangladesh without residency and relevant permits.

Closing Paragraph

A sole proprietorship suits domestic individual traders, freelancers, and small-scale service providers who operate locally and require a low-cost, minimal-compliance structure. The primary advantage is ease of setup; the material drawback is unlimited personal liability, which makes this structure unsuitable for any business carrying meaningful financial or legal risk.

Local individual entrepreneurs and small traders conducting low-risk, domestic commercial activity who do not require external investment or liability protection.

How to Choose the Right Entity Type in Bangladesh

Choosing the right company structure in Bangladesh is a legal and operational decision with measurable consequences — not simply an administrative formality.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations, tax treatment, and operational permissions under Bangladeshi law. Selecting the wrong form carries concrete risks:

- Registering a liaison office but conducting direct commercial transactions violates its permitted scope under BIDA regulations, exposing the entity to cancellation and financial penalties.

- Choosing a structure without access to Bangladesh's tax treaty network means you cannot claim withholding tax reductions available under treaties with counterpart jurisdictions.

- Forming a private limited company for a single-person consultancy introduces mandatory audit requirements under the Companies Act 1994, adding recurring costs that an OPC structure might avoid.

- Selecting an entity without the capacity to demonstrate local substance can trigger compliance failures under BIDA registration conditions.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each require distinct entity forms under Bangladeshi law.

- Ownership Structure: A sole founder points toward an OPC, while multi-party ventures require a private or public limited company.

- Tax Objectives: Your need for treaty access, sector-specific tax exemptions, or standard corporate tax treatment will narrow the available options.

- Operational Scope: Foreign entities intending only market research or liaison functions cannot conduct revenue-generating activities through a representative or liaison office.

- Compliance Capacity: Audited financials, annual returns, and board requirements vary significantly across structures — assess what your business can realistically sustain.

- Exit and Conversion: Not all entity types permit straightforward conversion or redomiciliation; verify your intended exit path before registering.

Compliance Services for Companies in Bangladesh

Ongoing compliance support for Bangladeshi entities, including annual filings, RJSC submissions, and regulatory reporting.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a company in Bangladesh guide. The Private Limited Company is the most registered entity type in the country, favored by both resident founders and foreign investors for its liability protection and relatively straightforward registration through the Registrar of Joint Stock Companies and Firms (RJSC). The One Person Company suits solo founders operating without partners, while the Public Limited Company is reserved for businesses seeking public capital. Branch and liaison offices serve foreign firms testing the market before committing to a local subsidiary.

Regulatory direction under the Companies Act 1994 has been gradually modernizing, with RJSC expanding its digital filing infrastructure. Bangladesh's growing bilateral investment treaty network signals increased attention to foreign investor protections. Understanding these structures and the frameworks governing them positions your business to make a registration decision grounded in operational and legal reality.

How Expanship Can Assist You

Expanship Bangladesh company incorporation services cover the full range of entity types discussed in this blog, from a Private Limited Company registered under the Companies Act 1994 to a Branch Office approved by the Bangladesh Investment Development Authority (BIDA). Whichever structure fits your business model, our team works directly within the local regulatory framework to keep your formation on track.

From initial document preparation through to post-incorporation obligations, our service scope includes:

- Document preparation and notarization/legalization

- Registered agent and registered office provision

- Filing with the Registrar of Joint Stock Companies and Firms (RJSC)

- BIDA registration and related government liaison

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Bangladesh to discuss which entity structure suits your business objectives.

Frequently Asked Questions (FAQ)

The Private Limited Company is the most frequently incorporated entity, registered under the Companies Act 1994 through the Registrar of Joint Stock Companies and Firms (RJSC). Its combination of limited liability, flexible shareholding, and suitability for both domestic operations and foreign investment accounts for its widespread use.

A Branch Office cannot issue shares or retain profits locally and is treated as an extension of its foreign parent for tax purposes, while a Private Limited Company is a separate legal entity subject to corporate income tax in Bangladesh. The Private Limited Company holds unrestricted local trading rights; a Branch Office operates under conditions set by the Bangladesh Investment Development Authority (BIDA) approval.

Among registered structures, the One Person Company discloses only one shareholder publicly, limiting the visibility of ownership to a single individual. Nominee arrangements are not a formal feature under the Companies Act 1994, so privacy is structural rather than nominee-based.

A One Person Company requires exactly one shareholder and one director by statute. General Partnerships and Limited Partnerships both require a minimum of two partners, making sole formation legally impossible for those structures.

Foreigners may incorporate a Private Limited Company, establish a Branch Office, or register a Liaison Office or Representative Office through BIDA. Foreign ownership of up to 100% is permitted in a Private Limited Company across most sectors, subject to the relevant sectoral policy under the Foreign Private Investment (Promotion and Protection) Act 1980.

Conversion from a Private Limited Company to a Public Limited Company is expressly recognised under the Companies Act 1994. Conversion between fundamentally different structures, such as from a partnership to a limited company, generally requires dissolution of the original entity and fresh incorporation rather than a statutory continuation process.

Private Limited Companies, Public Limited Companies, and One Person Companies hold separate legal personality under the Companies Act 1994. Sole proprietorships and general partnerships do not; in those structures, the owner or partners remain personally liable for all obligations of the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.