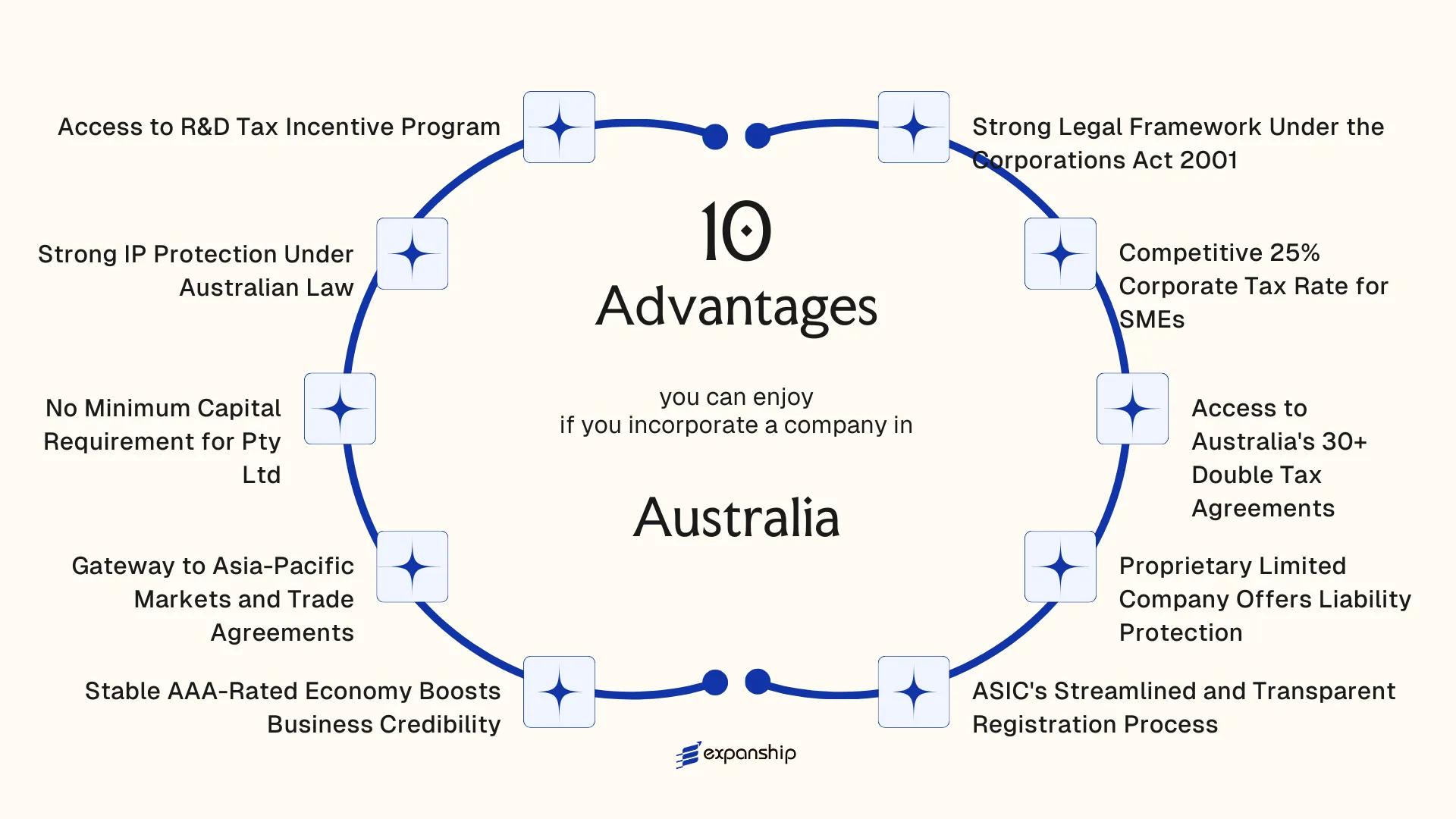

Key Takeaways

- Australia's base rate entities benefit from a reduced 25% corporate tax rate, giving qualifying SMEs a meaningful cost advantage over jurisdictions with flat higher-rate regimes.

- The Corporations Act 2001 provides Proprietary Limited company shareholders with statutory liability protection that insulates personal assets from business obligations without requiring complex legal structuring.

- With more than 30 double tax agreements in force, cross-border income flows — including dividends, royalties, and interest — can be structured to reduce withholding tax exposure across Australia's key trading partner jurisdictions.

- Businesses investing in qualifying research and development activity gain access to the R&D Tax Incentive program, a refundable or non-refundable tax offset that directly reduces the net cost of innovation expenditure.

Situated in the Asia-Pacific region, Australia is an independent sovereign nation and a member of the G20, operating under a stable federal system of government. Company registration is administered by the Australian Securities and Investments Commission, a statutory body established under the Australian Securities and Investments Commission Act 2001. Foreign businesses looking to establish a local presence most commonly do so through a Proprietary Limited company. The country operates a residence-based tax system, with treaty obligations forming a significant part of how cross-border income is treated.

Foreign ownership is broadly permitted across most sectors, with Australia maintaining an open foreign direct investment policy subject to review thresholds under the Foreign Acquisitions and Takeovers Act 1975. Certain sensitive industries require clearance from the Foreign Investment Review Board, but the general framework is permissive by international standards.

Understanding the benefits of incorporating in Australia requires looking across several regulatory, financial, and commercial dimensions. This article examines those advantages in detail.

Strong Legal Framework Under the Corporations Act 2001

The Corporations Act 2001 (Cth) establishes a single, nationally uniform legal framework governing company formation, director duties, shareholder rights, and disclosure obligations across all states and territories. For a foreign business owner, operating under one federal statute rather than a patchwork of state-level regimes significantly reduces legal complexity.

Defined Shareholder and Director Protections

The Act codifies specific duties owed by directors to the company, including the duty to act in good faith and the duty to prevent insolvent trading under sections 180 to 184. These provisions give investors and co-owners a legally enforceable basis for holding management accountable, which is not always available in jurisdictions where such duties remain at common law or are loosely defined.

Predictable Dispute Resolution and Disclosure Standards

Part 2F.1 of the Act grants shareholders formal rights to bring oppression claims before the courts. Australian corporate law protections for investors are therefore statutory, not discretionary. ASIC, the corporate regulator, enforces ongoing compliance obligations, meaning the counterparties your business deals with are held to the same binding standards.

Statutory protections under the Corporations Act 2001 give your investors and directors a clear, court-enforceable legal footing from the day your entity is registered.

Competitive 25% Corporate Tax Rate for SMEs

Australia's corporate tax framework splits rates between two categories of companies. The standard rate sits at 30%, but base rate entities — broadly, companies with an aggregated turnover below AUD 50 million that derive no more than 80% of their income from passive sources — qualify for the reduced Australia 25% corporate tax rate SMEs benefit from under the Income Tax Rates Act 1986. For a foreign-owned proprietary limited company structured around active business operations, that 25% rate is the operative figure from day one of trading.

That gap of five percentage points against the standard rate has direct consequences for retained earnings. Profits that remain in the company and fund reinvestment or expansion are taxed at a materially lower cost than those of larger corporate peers.

The passive income threshold is particularly relevant for foreign investors. Your structure qualifies so long as the business generates its revenue through active operations rather than dividends, interest, or royalties — precisely the profile of a trading or services entity.

Why the threshold conditions work in your favour:

- The AUD 50 million turnover ceiling covers the vast majority of foreign-owned subsidiaries and startups entering the market

- The 80% active income test aligns naturally with operating businesses rather than holding structures

- Eligibility is assessed annually, so a growing company retains the rate for each year it qualifies

Incorporate a Company in Australia

Set up a proprietary limited company in Australia and position your business to access the 25% base rate entity tax from the start of operations.

Access to Australia's 30+ Double Tax Agreements

Australia's network of double tax agreements (DTAs) covers more than 30 countries, including major trading partners such as the United States, United Kingdom, Japan, Singapore, and Germany. For a foreign business owner, this network directly reduces the risk of the same income being taxed twice — once by Australia and once by your home jurisdiction.

Each treaty allocates taxing rights between the two countries, typically reducing or eliminating withholding tax on dividends, interest, and royalties paid across borders. The specific rates vary by treaty, but many agreements cap withholding tax on dividends at 15% or lower for qualifying recipients, which is a direct cost reduction on profit repatriation compared to the default domestic rate of 30%.

| Treaty Partner | Standard Rate | Reduced DTA Rate (Qualifying) |

|---|---|---|

| United States | 30% | 15% |

| United Kingdom | 30% | 15% |

| Japan | 30% | 10% |

| Singapore | 30% | 15% |

| Germany | 30% | 15% |

DTAs also provide certainty on permanent establishment rules, which determines when your entity's activities in a foreign country create a taxable presence there. That clarity matters when structuring cross-border operations, since ambiguity on this point can expose a firm to unexpected tax obligations in multiple countries simultaneously.

Australia's treaties are administered under the International Tax Agreements Act 1953, which incorporates each DTA into domestic law. Eligibility for treaty benefits generally requires that your entity qualifies as a tax resident under the relevant agreement's residency provisions.

Proprietary Limited Company Offers Liability Protection

Proprietary limited company liability protection Australia is one of the more tangible structural advantages the Pty Ltd form provides to foreign investors. Under the Corporations Act 2001, shareholders of a proprietary limited company bear liability only to the extent of any unpaid amount on their shares. Personal assets sit outside the reach of creditors pursuing the company.

This separation between personal and corporate liability is not merely contractual. It is a statutory construct. If your Australian entity incurs debt or faces litigation, your exposure as a foreign shareholder is confined to your equity contribution. That boundary holds regardless of where you are incorporated or tax-resident.

The Pty Ltd liability shield advantages become particularly relevant when entering unfamiliar regulatory territory. Operating through a locally registered entity means Australian counterparties, suppliers, and lenders interact with a structure they recognise, one that carries defined legal obligations and a clear liability boundary.

Keep these points in mind:

- Liability is capped at the unpaid value on issued shares, not total company debt

- Directors may face personal liability under Corporations Act 2001 for insolvent trading under section 588G, which is separate from shareholder liability

- A shareholder guarantee, if voluntarily provided to a lender, overrides the statutory shield for that specific obligation

- The entity must remain solvent and compliant with ASIC reporting obligations to preserve its legal standing

A Pty Ltd can be incorporated with a single shareholder and a single director who is the same person, meaning a sole foreign individual can establish a fully compliant Australian company without a local co-owner.

ASIC's Streamlined and Transparent Registration Process

One of the clearer ASIC company registration advantages Australia offers foreign investors is the speed and predictability of the incorporation process itself. The Australian Securities and Investments Commission operates a centralised online portal through which a proprietary limited company can be registered, often within one business day once documentation is in order. For an overseas founder working across time zones, that timeline eliminates weeks of uncertainty that are common in jurisdictions requiring notarised paper submissions or multi-agency approvals.

A Single Point of Entry for Company Formation

ASIC's Business Registration Service consolidates company registration with related obligations, including the Australian Business Number (ABN) and Goods and Services Tax (GST) registration, into one digital process. Rather than coordinating between separate government bodies, your business can complete foundational registration requirements through a single interaction, reducing both administrative load and the risk of procedural gaps.

Transparency as an Operational Asset

All registered companies are recorded on ASIC's publicly searchable register, which documents officeholder details, registered addresses, and company status. That public record creates a verifiable corporate identity from day one. For a foreign firm entering new commercial relationships in the Asia-Pacific region, a confirmed ASIC registration provides counterparties, banks, and government agencies with immediate, independent confirmation of your entity's legal standing, without requiring additional authentication steps.

Incorporate in Australia and Claim Every Advantage

Our team helps foreign businesses complete ASIC registration correctly and efficiently, with full guidance on post-incorporation compliance obligations.

Stable AAA-Rated Economy Boosts Business Credibility

Australia holds one of the few remaining AAA credit ratings from all three major agencies: Moody's, S&P, and Fitch. This trifecta signals fiscal discipline and institutional stability to counterparties, banks, and investors worldwide, which translates directly into lower perceived risk when your business operates under an Australian-registered entity.

For foreign founders, that credibility has concrete commercial value. Banking relationships open more readily, supplier credit terms tend to be more favorable, and institutional clients in regulated industries are more willing to engage a firm incorporated in a jurisdiction with this rating profile. The Australian Prudential Regulation Authority and the Reserve Bank of Australia maintain oversight frameworks that reinforce this stability at the financial system level.

- An AAA-rated sovereign signals that contractual and financial obligations in this jurisdiction are backed by a stable institutional environment, reducing counterparty hesitation in cross-border dealings.

- Foreign firms incorporated locally can reference Australia's sovereign rating in investor documentation, which adds verifiable weight to funding applications or partnership proposals.

- The country's uninterrupted GDP growth record of over 28 years prior to the COVID-19 pandemic established a long-term track record that rating agencies continue to factor into their assessments.

- Regulatory bodies such as ASIC operate under legislative mandates that reinforce transparency, giving your registered entity a credibility baseline that is difficult to replicate in lower-rated jurisdictions.

Gateway to Asia-Pacific Markets and Trade Agreements

Australia's geographic position and treaty network make it a practical base for businesses seeking structured access to Asia-Pacific markets. As an Australia gateway Asia-Pacific market access point, a locally incorporated entity can trade under preferential tariff schedules that are unavailable to firms operating from outside the region.

Australia is a signatory to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which covers 11 member economies including Japan, Canada, Mexico, and Vietnam. For a foreign-owned Australian company, CPTPP advantages include reduced or eliminated tariffs on goods exported to these markets, along with provisions covering investment protection and cross-border services trade.

Beyond the CPTPP, Australia maintains bilateral free trade agreements with China (ChAFTA), South Korea (KAFTA), Japan (JAEPA), India (ECTA), and the ASEAN-Australia-New Zealand FTA. Each agreement carries specific rules of origin, so goods produced or substantially transformed in Australia may qualify for preferential rates that a foreign firm could not access by shipping directly from its home country.

A business exporting eligible goods to Japan under JAEPA may face 0% tariffs on qualifying product categories, compared to the standard MFN rate that would otherwise apply to non-FTA trading partners.

No Minimum Capital Requirement for Pty Ltd

Under the Corporations Act 2001, there is no minimum capital requirement for Australia Pty Ltd companies. A proprietary limited company can be incorporated with a single share issued at any nominal value, including one cent. This directly reduces the financial barrier to entry for foreign founders who want a legal presence without committing significant capital at formation.

Capital can be contributed progressively as the business generates revenue or secures investment. For early-stage ventures or holding structures, this means the entity can be legally active and contract-capable before substantial funds are deployed.

The zero share capital requirement also benefits flexible capital structures. Shareholders and directors can agree on share classes, issue prices, and contribution schedules that reflect the firm's actual funding timeline, rather than satisfying an arbitrary statutory threshold.

- A Pty Ltd can be formed with one share at a nominal value

- No paid-up capital minimum applies at registration or post-incorporation

- Share capital can be increased at any point through a resolution of shareholders

- Different share classes with varying rights can be issued under the company's constitution

While no minimum capital applies, your company's constitution and any shareholder agreement may impose internal capital requirements that override the statutory default.

Strong IP Protection Under Australian Law

Australia intellectual property protection benefits are grounded in a well-developed statutory framework that gives foreign business owners enforceable rights from the moment they register or establish qualifying use.

Dedicated Legislation by IP Type

Each category of intellectual property is governed by its own statute. Patents fall under the Patents Act 1990, trademarks under the Trade Marks Act 1995, copyright under the Copyright Act 1968, and designs under the Designs Act 2003. This separation means protections are precisely defined, reducing ambiguity in enforcement.

IP Australia as the Registering Authority

IP Australia administers trademark, patent, and design registrations. A registered trademark grants the holder exclusive rights nationally for an initial ten-year period, renewable indefinitely. For a foreign firm, this creates a durable territorial right that is enforceable in Federal Court without reliance on common law use alone.

Alignment With International Treaties

The country is a signatory to the Madrid Protocol, the Patent Cooperation Treaty, and the Berne Convention. This means an existing international trademark or patent application can be extended into the jurisdiction through established multilateral channels, reducing the administrative burden of building a local IP portfolio from scratch.

Practical Enforcement Value

IP rights registered here are enforceable against infringers through the Federal Court of Australia, which has dedicated intellectual property jurisdiction. Remedies available include injunctions, damages, and account of profits. For foreign investors holding brand or technology assets, this judicial enforceability converts registration into a commercially protective instrument rather than a procedural formality.

Access to R&D Tax Incentive Program

Administered jointly by the Australian Taxation Office (ATO) and AusIndustry, the R&D Tax Incentive program is one of the more structurally significant reasons a foreign business might choose to incorporate locally rather than operate through a branch or representative office. Access to Australia R&D tax incentive program benefits is limited to incorporated entities that are registered as Australian resident companies or foreign companies incorporated here, which means the choice of legal structure has a direct effect on eligibility.

The program operates on a tax offset model rather than a deduction, which produces a more predictable financial outcome. Eligible entities with an aggregated annual turnover below AUD 20 million receive a refundable tax offset of 18.5 percentage points above the company tax rate, while larger entities receive a non-refundable offset of 8.5 or 16.5 percentage points depending on R&D intensity. For a foreign-owned subsidiary conducting qualifying research activity in Australia, this translates into real cash flow support, particularly during early-stage operations when the entity may not yet be profitable.

Qualifying expenditure must relate to experimental activities conducted under a systematic program aimed at generating new knowledge, as defined under the Industry Research and Development Act 1986. Activities must be registered annually with AusIndustry before the program deadline.

Foreign companies that establish an Australian subsidiary specifically to conduct R&D can structure their operations to concentrate eligible expenditure within the local entity, thereby maximising access to offsets that would not be available through other structures. The practical benefits include:

- Refundable offsets functioning as a cash payment for loss-making early-stage companies

- R&D expenditure thresholds that accommodate firms at varying scales

- The ability to include certain expenditure on overseas R&D activities if the work cannot be conducted domestically

Why Australia Stands Out Among Business Destinations

Comparing Australia against its most relevant regional alternatives reveals where its regulatory and structural profile holds distinct advantages. Foreign investors evaluating incorporation in the Asia-Pacific corridor most commonly weigh Singapore and Hong Kong as direct competitors, given their similar common law foundations, regional trade positioning, and appeal to internationally mobile businesses. New Zealand is also a practical reference point due to its geographic proximity, shared legal heritage under English common law, and comparable SME-oriented entity structures.

What the comparison below makes visible is that why Australia is best for business incorporation is not a single factor but a convergence of several simultaneously: treaty network depth, R&D fiscal incentives, IP legal infrastructure, and a creditor-grade sovereign economy. Singapore and Hong Kong each offer lower headline tax rates, but neither provides an equivalent R&D tax offset program or the same breadth of double tax agreements administered through the Australian Taxation Office. New Zealand lacks the volume of DTAs and the AAA-rated economic standing that directly supports business credibility with international counterparties.

| Parameter | Australia | Singapore | Hong Kong | New Zealand |

|---|---|---|---|---|

| Corporate Tax Rate (SMEs) | 25% (base rate entities) | 17% (standard) | 16.5% (standard) | 28% (standard) |

| Double Tax Agreements | 40+ treaties | 90+ treaties | 45+ treaties | 40+ treaties |

| R&D Tax Incentive | Yes (up to 43.5% offset) | Yes (limited schemes) | No direct equivalent | Yes (limited) |

| Minimum Share Capital | None (Pty Ltd) | S$1 nominal | HK$1 nominal | NZ$1 nominal |

| Sovereign Credit Rating | AAA (S&P) | AAA (S&P) | AA+ (S&P) | AA+ (S&P) |

| IP Legal Framework | Patents Act 1990 + strong enforcement | Strong, TRIPS-compliant | Strong, TRIPS-compliant | Patents Act 2013 |

| APAC Trade Agreement Access | Yes (CPTPP, AUSFTA, etc.) | Yes (CSFTA, EUSFTA, etc.) | Limited (CEPA with China) | Yes (CPTPP, etc.) |

| Primary Regulatory Body | ASIC | ACRA | Companies Registry | Companies Office |

Compliance Services for Companies in Australia

Maintaining a registered Australian company requires meeting ongoing obligations under the Corporations Act 2001, including annual reviews, statutory filings with ASIC, and director duty compliance. Expanship supports businesses at every stage of their compliance lifecycle.

Conclusion

Incorporating in Australia offers a combination of structural, fiscal, and legal advantages that are difficult to replicate in a single jurisdiction. The 25% corporate tax rate for base rate entities, access to over 30 double tax agreements, and the R&D Tax Incentive program together form a fiscally coherent case for establishing a Proprietary Limited company here.

Two factors stand out above the rest. First, the liability separation available through the Pty Ltd structure, governed by the Corporations Act 2001, means your personal assets remain insulated from business obligations without complex legal engineering. Second, the DTAs Australia holds with major economies reduce the friction of cross-border profit repatriation, a practical concern for any foreign investor operating across multiple markets.

That said, the benefits of incorporating in Australia align most directly with businesses targeting Asia-Pacific expansion, those investing in qualifying R&D activity, or firms that benefit from treaty-protected income flows. A holding company with no regional operations may not extract the same value from these structures as an active trading entity would.

For businesses where the fit is strong, the regulatory foundation managed by ASIC, combined with the country's AAA sovereign credit rating, provides a stable and credible platform for long-term operations. The next step is matching your specific business model and ownership structure to the correct entity type and compliance pathway.

Start Your Australian Company Formation With Expanship

Expanship supports foreign entrepreneurs and businesses through every stage of forming a Proprietary Limited company in Australia, from initial name reservation with the Australian Securities and Investments Commission to post-incorporation compliance under the Corporations Act 2001. Starting your Australia company formation with Expanship means working with a team familiar with ASIC's registry requirements, the obligations imposed on foreign directors, and the specific documentation standards that apply to non-resident shareholders.

Expanship's services for Australian entity formation cover the following:

- Preparation and legalization of incorporation documents, including the company constitution and consent-to-act forms for directors

- Registered office and local agent provision to satisfy ASIC's requirement for an Australian address

- Government filing and direct liaison with ASIC throughout the registration process

- Post-incorporation compliance management, including annual review fee obligations and ASIC notification requirements

- Corporate secretarial support to maintain statutory registers and minute books under the Corporations Act 2001

- Banking introduction assistance to support your business in opening an Australian corporate account

Reach out to Expanship Australia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

A base rate entity — broadly, a company with an aggregated annual turnover below AUD 50 million that derives no more than 80% of its income from passive sources — is taxed at 25%. The standard corporate tax rate of 30% applies to larger companies that fall outside these thresholds. Both rates apply to Australian-sourced taxable income, and the applicable rate is assessed each income year based on the entity's circumstances at that time.

Administered jointly by AusIndustry and the Australian Taxation Office, the R&D Tax Incentive provides a tax offset for eligible research and development expenditure. Companies with an aggregated turnover below AUD 20 million may access a refundable 43.5% tax offset, while larger entities are entitled to a non-refundable 38.5% offset. Expenditure must relate to activities registered under the Industry Research and Development Act 1986, and registration must be completed after the end of the relevant income year.

Australia's Double Tax Agreements, of which there are more than 40 in force, generally allocate taxing rights between Australia and the treaty partner country to prevent the same income from being fully taxed in both jurisdictions. The specific relief available — whether through exemption, a reduced withholding tax rate, or a foreign tax credit mechanism — depends on the terms of the individual agreement and the type of income involved. The ATO publishes the full text of each treaty, and the applicable provisions differ materially between agreements.

ASIC imposes annual review fees on registered companies, and failure to pay within the prescribed period results in late payment penalties. If a company remains non-compliant for an extended period, ASIC has the authority under the Corporations Act 2001 to deregister the entity, which extinguishes its legal existence and can expose directors to personal liability for debts incurred after deregistration. Directors also face potential disqualification if they are found to have managed a company while insolvent.

No minimum share capital is prescribed under the Corporations Act 2001 for a Proprietary Limited company. A Pty Ltd can be incorporated with a single share issued at any nominal value, including AUD 1. While this provides structural flexibility, the amount of capital contributed can have practical implications for banking relationships and the firm's ability to meet its financial obligations.

Intellectual property rights in Australia are governed by a suite of federal statutes, including the Patents Act 1990, the Trade Marks Act 1995, and the Copyright Act 1968. An Australian-incorporated entity can register patents and trade marks with IP Australia, the government body responsible for administering these rights, and enforcement is available through the Federal Court of Australia. Rights registered in Australia do not automatically extend to other jurisdictions, so separate protection in each relevant market must be obtained independently.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.