Key Takeaways

- The Proprietary Limited Company (Pty Ltd) is the most registered entity type in Australia, governed by the Corporations Act 2001 and administered by ASIC.

- No Liability Companies (NL) are restricted exclusively to mining ventures, making them one of the most narrowly scoped corporate forms available under Australian law.

- Foreign businesses entering Australia can register through ASIC as a foreign company or establish a branch, each carrying distinct compliance obligations under the Corporations Act 2001.

- Companies Limited by Guarantee serve non-profit and membership-based organizations, distinguishing them structurally from share-based corporate forms available in Australia.

Introduction to Entity Types in Australia

Australia is a sovereign federal nation in the Asia-Pacific region, bordered by the Indian and Pacific Oceans and situated southeast of Southeast Asia. Under the Corporations Act 2001, the primary federal legislation governing company formation, the Australian Securities and Investments Commission (ASIC) administers company registration and ongoing compliance at the national level.

Australia operates a standard corporate tax regime — resident companies are taxed on worldwide income, with rates that vary based on company size and turnover.

Selecting among the types of business entities in Australia depends on factors including liability exposure, ownership structure, and intended operational scale. The corporate structures available in Australia span a range of legal forms suited to different commercial purposes.

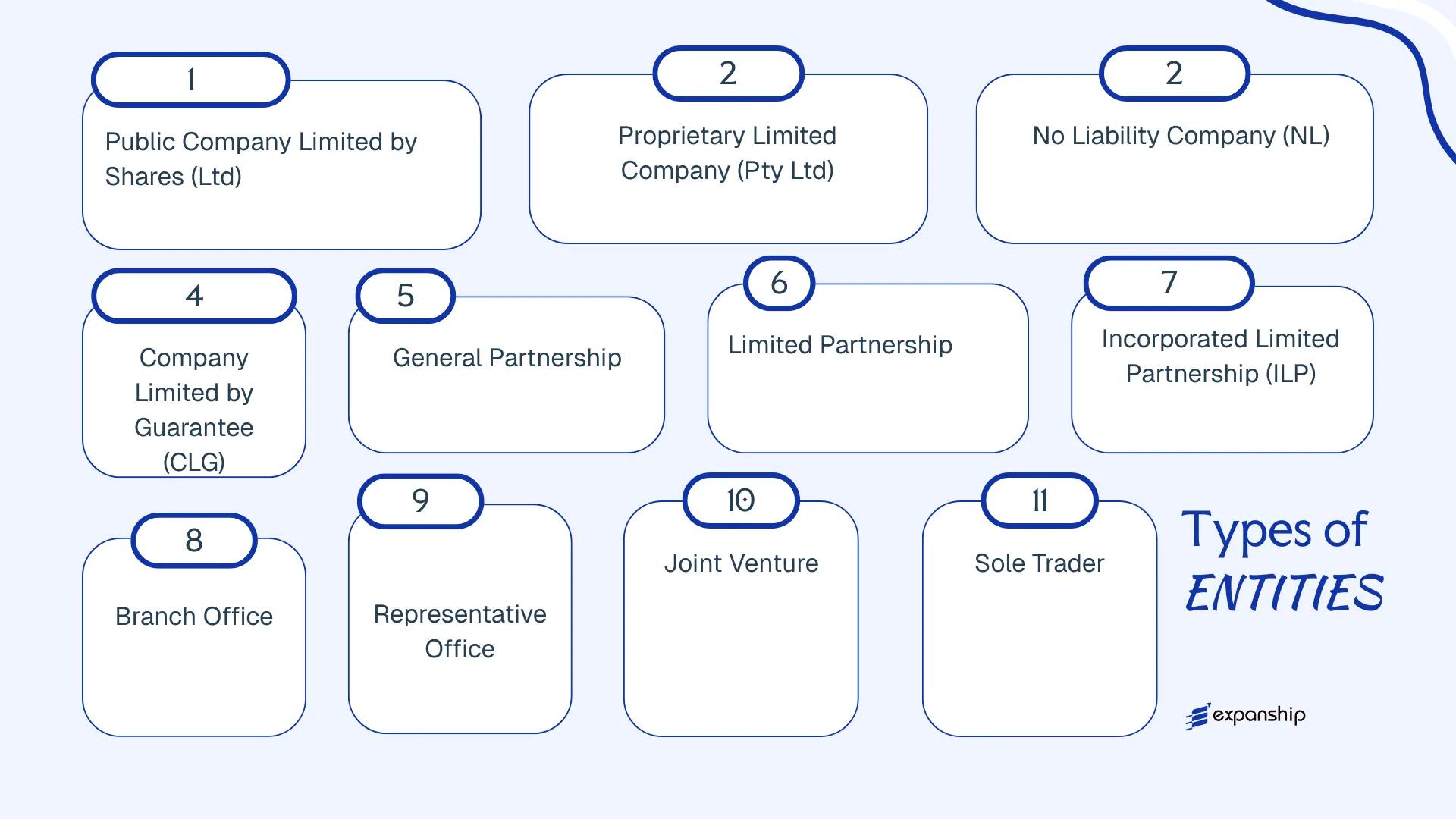

Entities available under Australian law include:

- Proprietary Limited Company (Pty Ltd)

- Public Company Limited by Shares (Ltd)

- No Liability Company (NL)

- Company Limited by Guarantee

- General Partnership

- Limited Partnership

- Incorporated Limited Partnership

- Branch Office

- Representative Office

- Sole Trader

Each of these business entity types in Australia carries distinct formation requirements, governance obligations, and liability implications, all of which are examined in detail throughout this article.

An Overview of Business Structures in Australia

Australia's corporate law framework provides several distinct entity types, each governed primarily by the Corporations Act 2001 (Cth), administered by the Australian Securities and Investments Commission (ASIC). Specific structures such as partnerships and sole traders fall under state and territory legislation rather than federal law. Each entity type carries different implications for liability, taxation, membership requirements, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (Ltd) | Incorporated body | Limited by shares | Taxed | Yes | 1 shareholder | ASIC | Corporations Act 2001 |

| Proprietary Company (Pty Ltd) | Incorporated body | Limited by shares | Taxed | Yes | 1 shareholder | ASIC | Corporations Act 2001 |

| No Liability Company (NL) | Incorporated body | No personal liability | Taxed | Mining only | 1 shareholder | ASIC | Corporations Act 2001 |

| Company Limited by Guarantee | Incorporated body | Limited by guarantee | Taxed / exempt | Yes | 1 member | ASIC | Corporations Act 2001 |

| General Partnership | Unincorporated | Unlimited | Pass-through | Yes | 2 partners | State/Territory | State Partnership Acts |

| Limited Partnership | Unincorporated | Mixed | Pass-through | Yes | 2 partners | State/Territory | State Partnership Acts |

| Incorporated Limited Partnership | Incorporated body | Mixed | Pass-through | Yes | 2 partners | State/Territory | State ILP legislation |

| Branch Office | Foreign structure | Parent liable | Taxed | Yes | N/A | ASIC | Corporations Act 2001 |

| Representative Office | Foreign structure | Parent liable | Generally exempt | No | N/A | ASIC / State | Varies |

| Sole Trader | Unincorporated | Unlimited | Pass-through | Yes | 1 individual | State/Territory | State legislation |

Each of these structures is examined in full in the sections below.

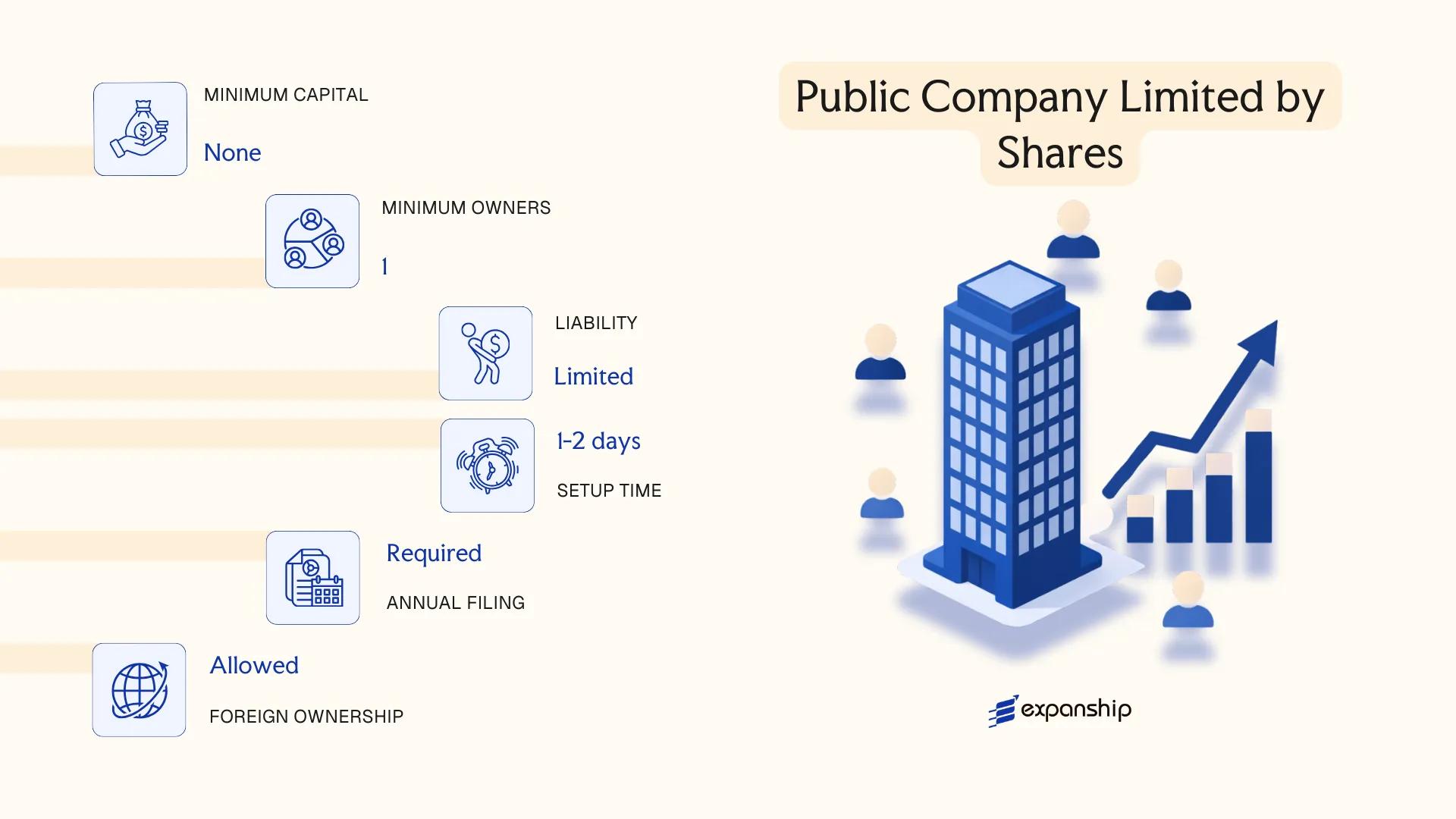

Public Company Limited by Shares (Ltd)

Governed by the Corporations Act 2001 (Cth) and regulated by the Australian Securities and Investments Commission (ASIC), an Australian public company limited by shares is a distinct legal entity with perpetual succession and the capacity to sue and be sued in its own name. Shareholder liability is capped at the unpaid amount on their shares, separating personal assets from corporate obligations.

Unlike a proprietary company, a public Ltd can offer shares to the general public and may apply for listing on the Australian Securities Exchange (ASX), though listing is not mandatory. This structure suits large-scale capital raising, institutional investors, and businesses anticipating broad public ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality; perpetual succession |

| Members | Shareholders; minimum 1 director (ordinarily resident in Australia), minimum 3 directors overall; minimum 1 company secretary | No maximum shareholder limit; at least 1 director must ordinarily reside in Australia |

| Minimum Members (Shareholders) | 1 shareholder (no maximum) | Shares can be publicly offered |

| Local Presence | Registered office in Australia; at least 1 Australian-resident director | Registered office must be open and accessible during business hours |

| Share Capital | AUD; no statutory minimum paid-up capital | Capital can be raised from the public via prospectus under Ch. 6D of the Corporations Act |

| Privacy | Director names and shareholder register are publicly accessible via ASIC | Financial reports must be lodged and are publicly available |

Focus Points

- Taxation: Subject to the standard corporate tax rate (currently 30%); GST applies at 10% on taxable supplies; dividends may carry franking credits; withholding tax applies to unfranked dividends, interest, and royalties paid to non-residents; stamp duty on share transfers varies by state.

- Annual Compliance: Must hold an AGM within five months of financial year-end; lodge audited financial statements with ASIC annually; continuous disclosure obligations apply if listed on ASX under the ASX Listing Rules.

- Treaty Access: As an Australian tax resident entity, the company can access Australia's broad double tax agreement network covering over 40 countries.

- Conversion: A proprietary company can convert to a public company by passing a special resolution and notifying ASIC; the reverse conversion requires meeting proprietary company eligibility criteria.

- Restrictions: Cannot have fewer than three directors; must comply with prospectus requirements under Chapter 6D when making public share offers.

Closing

A public Ltd company is used for large trading operations, ASX-listed ventures, and businesses requiring access to public equity markets. The principal advantage is unrestricted capital raising from the public; the main drawback is substantial ongoing compliance, including mandatory audits, AGM requirements, and, if listed, continuous disclosure obligations.

Best suited for large enterprises, companies seeking ASX listing, or businesses requiring broad public investment — not practical for small or closely held operations given the compliance burden.

Company Incorporation in Australia

Incorporate a public or proprietary company in Australia with end-to-end support from ASIC registration to post-incorporation compliance.

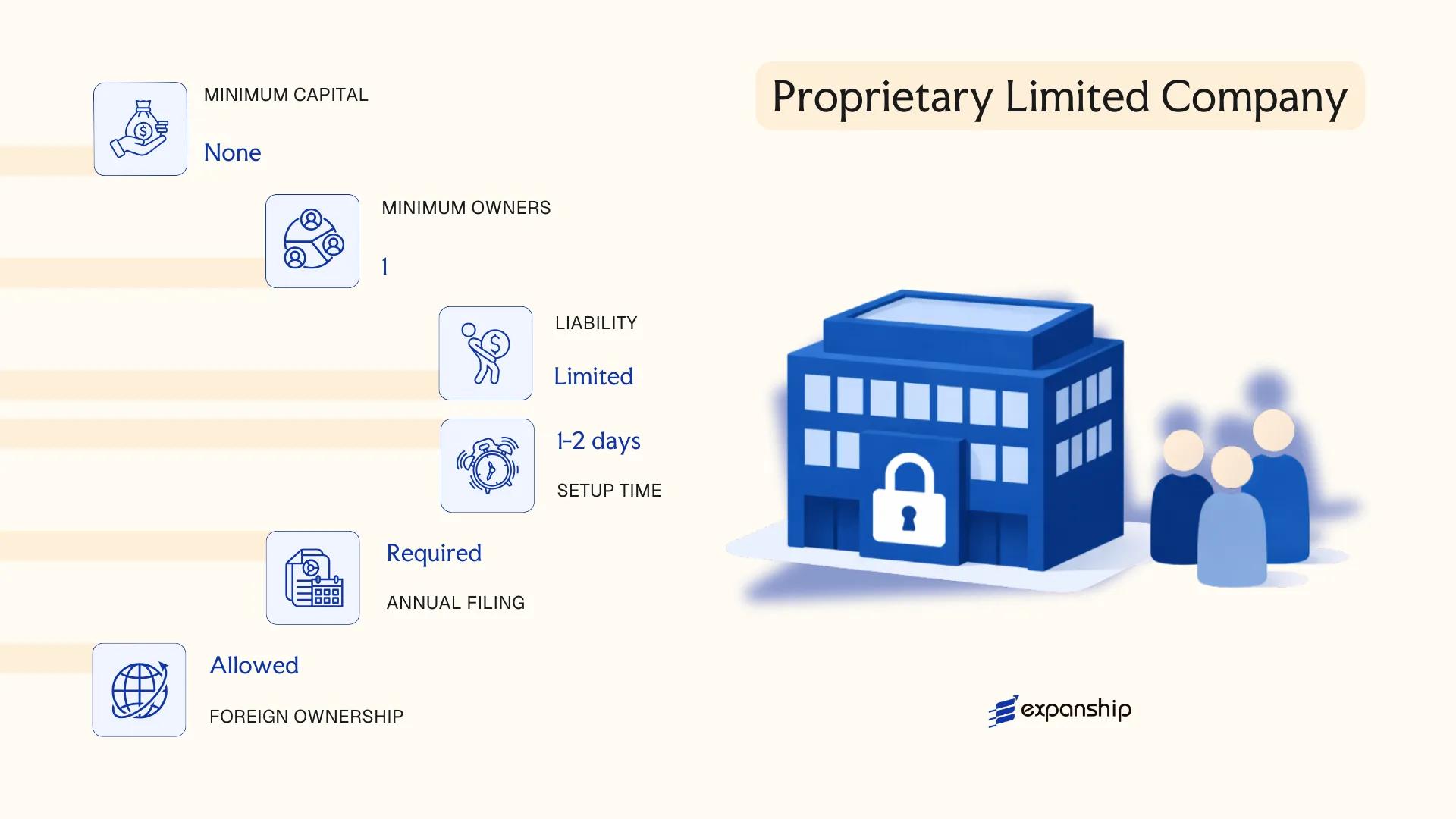

Proprietary Limited Company (Pty Ltd)

The proprietary limited company Australia Pty Ltd structure is governed by the Corporations Act 2001 (Cth), administered by the Australian Securities and Investments Commission (ASIC). It exists as a separate legal entity, meaning the company holds assets, incurs liabilities, and enters contracts in its own name.

Liability of shareholders is limited to the amount unpaid on their shares. This structure sits between a sole trader and a public company, making it the dominant vehicle for closely held businesses operating in Australia.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Separate legal personality; distinct from its owners |

| Members | Shareholders (min. 1, max. 50 non-employee shareholders) | Employee shareholders are excluded from the 50-person cap |

| Directors | Min. 1 director; must ordinarily reside in Australia | At least one director must be an Australian resident |

| Local Presence | Registered office address in Australia (cannot be a PO Box) | ASIC requires a physical or registered address for service |

| Capital | No minimum share capital; denominated in AUD | Shares can be issued at any agreed value |

| Privacy | Financial statements are generally not publicly disclosed for small proprietary companies | Large proprietary companies have additional reporting obligations |

Focus Points

- Taxation: Subject to corporate income tax at 25% (base rate entities with turnover under AUD 50 million) or 30%; GST registration required if annual turnover exceeds AUD 75,000; dividend withholding tax of 30% (reduced under applicable tax treaties); payroll tax applies at state level.

- Annual Compliance: Must lodge an annual ASIC review fee and maintain a register of members, directors, and secretaries; large proprietary companies must prepare and lodge audited financial statements.

- Franking Credits: Dividends paid from after-tax profits may carry franking credits, reducing effective tax burden on resident shareholders.

- Restrictions: Cannot offer shares to the public; limited to 50 non-employee shareholders.

- Conversion: Can be converted to a public company by passing a special resolution and meeting ASIC requirements under the Corporations Act 2001.

Closing

A Pty Ltd suits trading operations, holding structures, and IP ownership where owners want limited liability within a private, closely held framework. The primary limitation is the shareholder cap and the prohibition on public fundraising.

This structure is most appropriate for foreign investors and domestic operators seeking a private, limited liability vehicle for ongoing commercial activity in Australia without the compliance burden of a public company.

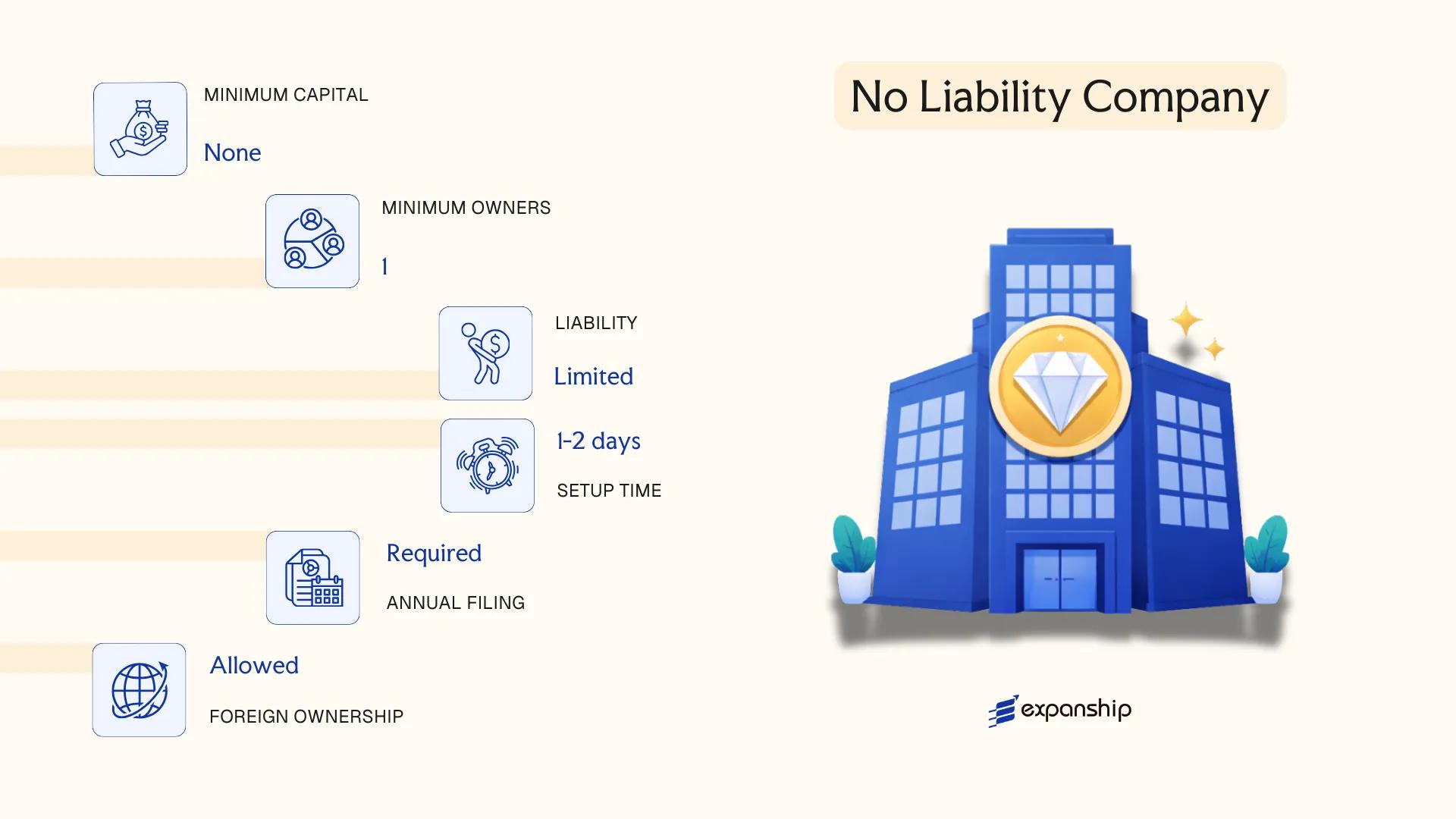

No Liability Company (NL)

A no liability company Australia NL is a corporate structure governed by the Corporations Act 2001 (Cth). It carries separate legal personality, meaning the entity itself — not its shareholders — bears legal and financial responsibility for its obligations.

What distinguishes this structure is its defining liability rule: shareholders have no obligation to pay calls on unpaid shares. If a shareholder declines to meet a call, the company may forfeit the shares but cannot pursue the member for the outstanding amount.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company under Corporations Act 2001 (Cth) | Separate legal personality |

| Members | Shareholders; no minimum shareholder count specified beyond general company rules; no maximum | No liability attaches to unpaid share calls |

| Directors | Minimum 1 director ordinarily resident in Australia | At least one director must reside domestically |

| Registered Office | Required within Australia | Must be a physical address, not a PO Box |

| Capital | AUD; no statutory minimum paid-up capital | Shares may be partly paid; calls are unenforceable against members |

| Permitted Activities | Mining purposes only | Restricted by statute to mining operations |

Focus Points

- Taxation: Subject to the standard corporate tax rate (25% for base-rate entities, 30% otherwise); GST applies where turnover thresholds are met; dividend withholding tax applies to non-resident shareholders; stamp duty obligations vary by state.

- Annual Compliance: Must lodge annual financial reports and returns with ASIC; mining-purpose restriction must remain satisfied.

- Conversion: An NL company may convert to another company type under Part 2B.7 of the Corporations Act 2001, subject to ASIC approval and member consent.

- Restrictions: Statutorilylimited to mining purposes; the company name must end with "No Liability" or "NL."

- Treaty Access: As an Australian tax resident entity, it may access Australia's double tax agreement network, subject to meeting residency and beneficial ownership conditions.

Closing

The NL company structure suits Australian mining company no liability arrangements where capital is raised through partly paid shares and investor exposure needs to be capped at the share subscription price. The primary advantage is the statutory bar on pursuing shareholders for unpaid calls; the key drawback is that its use is legally confined to mining activities, making it unsuitable for any other commercial purpose.

This structure is best suited for mineral exploration and mining ventures seeking to raise capital from investors who require a hard limit on their financial exposure.

Company Limited by Guarantee

A company limited by guarantee Australia operates under the Corporations Act 2001 (Cth), administered by the Australian Securities and Investments Commission (ASIC). It is a separate legal entity, meaning it can hold property, enter contracts, and sue or be sued in its own name.

Liability of each member is limited to the amount they have guaranteed to contribute upon winding up — typically a nominal sum. This structure makes it the standard vehicle for not-for-profit organisations, charities, associations, and community bodies that require corporate status without share capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated body corporate | Governed by the Corporations Act 2001 (Cth) |

| Members | Referred to as members; minimum 1 member, no statutory maximum | No shareholders; members hold no equity interest |

| Directors | Minimum 1 director; must ordinarily reside in Australia | At least one Australian-resident director required |

| Local Presence | Registered office in Australia; registered agent not mandatory | ASIC-registered office address required |

| Capital | No share capital; members provide a guarantee amount (often AUD 10–50) | Guarantee is contingent liability only, triggered on winding up |

| Privacy | Director names and registered office are publicly disclosed via ASIC register | Financial reports may be required depending on size tier |

Focus Points

- Taxation: Generally exempt from income tax if registered as a charity with the Australian Charities and Not-for-profits Commission (ACNC); GST registration thresholds and fringe benefits tax concessions may apply separately.

- Annual Compliance: Must lodge an annual statement with ASIC and, if ACNC-registered, submit an Annual Information Statement; larger entities face full financial reporting obligations.

- Restrictions: Cannot distribute profits or assets to members; all surplus must be applied toward the entity's stated objects.

- Conversion: Can convert to another company type under the Corporations Act 2001, though ASIC approval is required and restrictions apply if charitable status is held.

- Treaty Access: No access to double tax treaty benefits, as the entity does not pay income tax in the conventional corporate sense.

Used primarily for charities, sporting clubs, industry associations, and community organisations, this structure provides corporate legal personality without the complexity of share capital. The key limitation is the absolute prohibition on profit distribution, which makes it unsuitable for any commercially oriented venture.

Best suited for non-profit organisations, charities, and membership-based associations seeking corporate status with limited member liability under Australian law.

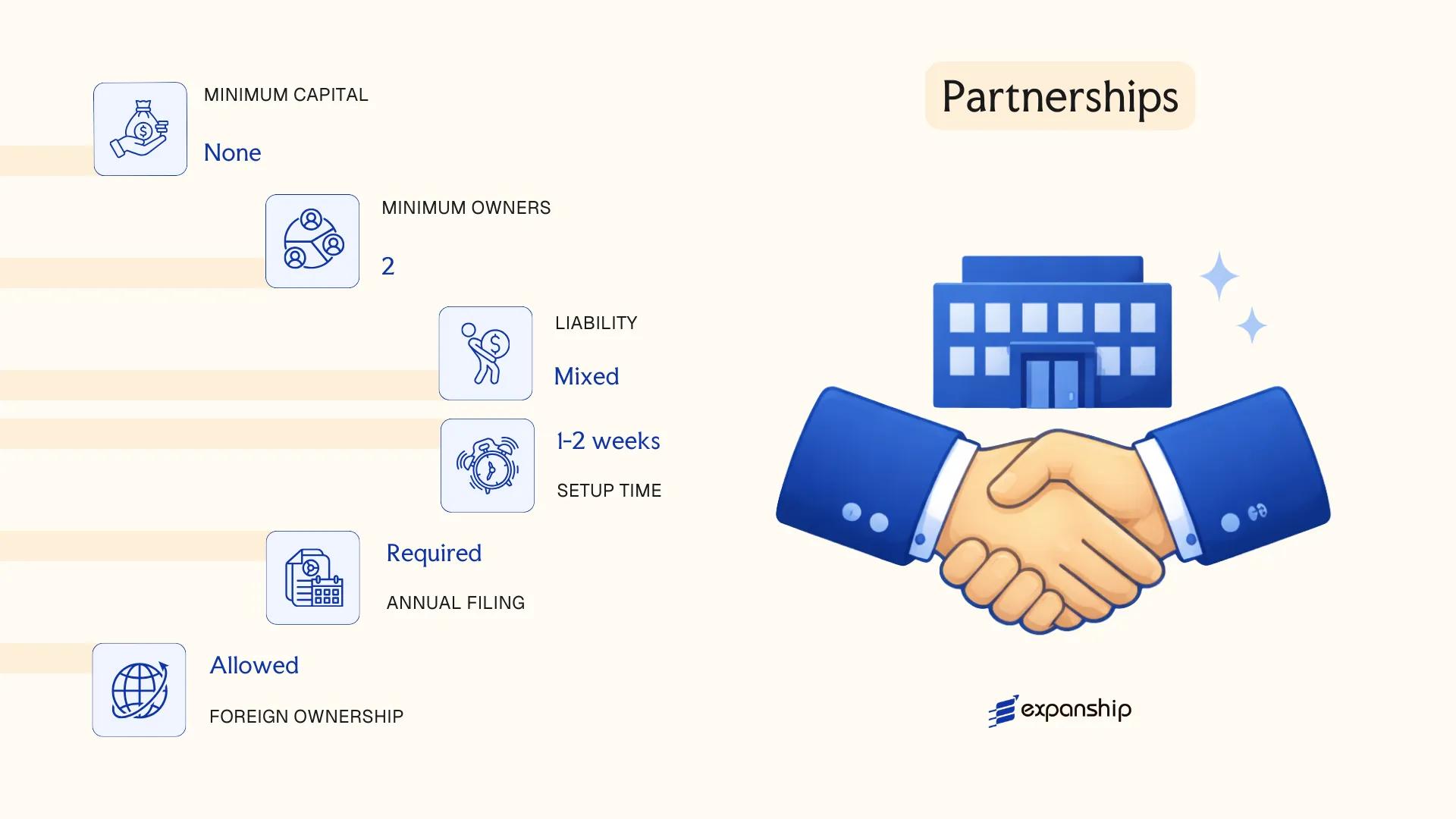

Partnerships (General Partnership, Limited Partnership, Incorporated Limited Partnership)

Partnership structures in Australia are governed primarily by state and territory legislation rather than a single federal act — each jurisdiction maintains its own Partnership Act (for example, the Partnership Act 1958 in Victoria or the Partnership Act 1892 in New South Wales). A general partnership does not create a separate legal entity; the partners are personally liable for the firm's obligations. Limited partnerships and incorporated limited partnerships (ILPs) offer structural variations that address liability and investor separation.

Registration requirements differ by structure. An ILP must be registered under the relevant state legislation — in Victoria, under the Partnership Act 1958 as amended — and is commonly used for venture capital and private equity funds, partly due to Venture Capital Limited Partnership (VCLP) and Early Stage Venture Capital Limited Partnership (ESVCLP) concession regimes administered by the ATO and the AFSA.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | General Partnership: not a separate legal entity; Limited Partnership: not separate; ILP: separate legal entity | Only the ILP achieves legal separation from its partners |

| Members | Partners (general and/or limited) | GP: min. 2, no federal cap; LP/ILP: at least 1 general partner + 1 limited partner |

| Local Presence | Registered office in the relevant state or territory | ILP must maintain a registered address in the state of registration |

| Capital | No prescribed minimum; AUD-denominated | Limited partners' liability is capped at their capital contribution |

| Privacy | Partner details generally on public record at state level for ILPs; GP arrangements less formally disclosed | VCLP/ESVCLP registration with AFSA adds a layer of regulatory visibility |

Focus Points

- Taxation: Partnerships are generally flow-through vehicles — income is assessed at the partner level; ILPs structured as VCLPs may access capital gains tax concessions and withholding tax exemptions for eligible foreign investors; GST registration applies where turnover thresholds are met.

- Annual Compliance: State-level registration renewals apply; ILPs registered as VCLPs must report annually to the AFSA and meet ongoing investment mandate conditions.

- Treaty Access: Partners that are foreign entities may access Australia's tax treaty network depending on their own residence and the partnership's characterisation in the relevant treaty jurisdiction.

- Restrictions: General partners in an LP or ILP bear unlimited liability; limited partners who participate in management risk losing their liability protection under state legislation.

Sub-Types

General Partnership

Partners share management and bear joint and several unlimited liability. Typically used by professional services firms or small co-owned businesses operating without a formal corporate shell.

Limited Partnership (LP)

Separates passive limited partners (capped liability) from at least one managing general partner (unlimited liability). Commonly used for investment vehicles and property syndicates but does not constitute a separate legal entity.

Incorporated Limited Partnership (ILP)

The ILP is a distinct legal entity, allowing it to contract, hold assets, and sue in its own name. This structure is the standard vehicle for venture capital and private equity fund formation under Australian law, and supports VCLP and ESVCLP registration with AFSA.

Closing

Partnerships suit investment fund structures, professional service arrangements, and co-investment vehicles where flow-through tax treatment is a priority; the ILP's separate legal personality and eligibility for concessional tax treatment under VCLP and ESVCLP regimes represent its primary advantage, while the general partner's unlimited liability remains a structural constraint across all partnership forms.

ILPs registered as VCLPs or ESVCLPs are best suited to venture capital fund managers and institutional investors seeking flow-through tax treatment with a degree of structural formality.

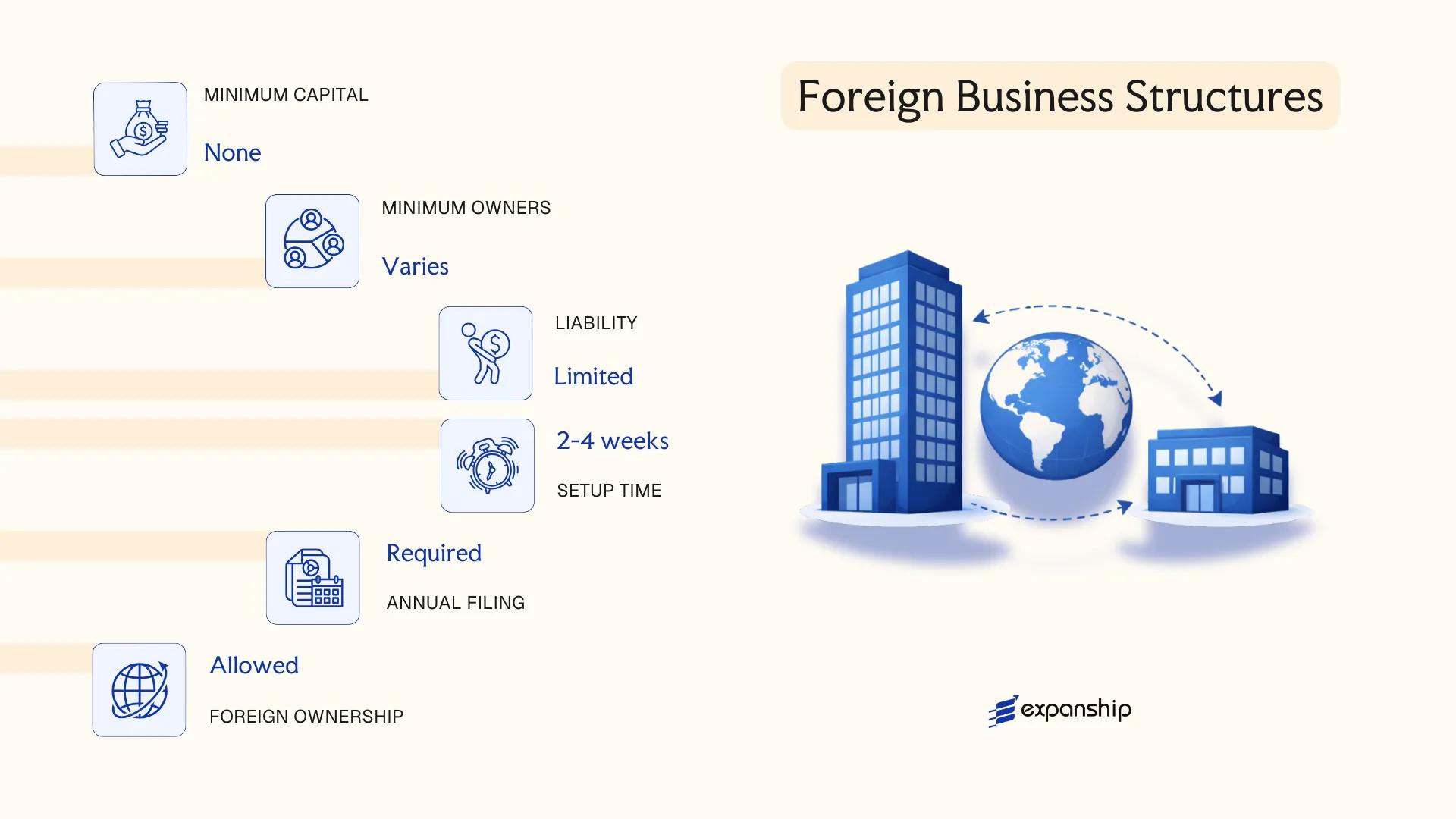

Foreign Business Structures (Branch Office, Representative Office, Foreign Company Registration)

Foreign companies seeking to operate in Australia must register with the Australian Securities and Investments Commission (ASIC) under Part 5B.2 of the Corporations Act 2001 (Cth). Unlike incorporating a new local entity, foreign company registration in Australia allows the overseas parent to conduct business directly without creating a separate legal entity.

A registered foreign company is not legally distinct from its parent. The parent bears full liability for the Australian operations, which distinguishes this structure from a locally incorporated subsidiary.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign company registered under Part 5B.2 of the Corporations Act 2001 | Not a separate legal entity; an extension of the overseas parent |

| Representatives | Local agent (individual or company resident in Australia) | Mandatory appointment; personally liable for certain compliance obligations |

| Local Presence | Registered office address in Australia | Must be a physical address; cannot be a PO Box |

| Capital | No minimum capital requirement | Parent's financials govern overall liability exposure |

| Disclosure | Financial statements of the foreign company may require lodgement with ASIC | Dependent on whether the entity meets the definition of a "disclosing entity" |

| Privacy | Director and local agent details are publicly searchable on the ASIC register | Less privacy than some offshore structures |

Focus Points

- Taxation: The Australian branch profits are subject to corporate income tax at 30% (or 25% for base rate entities); no separate dividend withholding tax applies on branch remittances, though royalty and interest payments to the foreign parent attract withholding tax; GST registration is required if annual turnover meets the threshold.

- Transfer pricing: Transactions between the Australian branch and its foreign head office must comply with the ATO's transfer pricing rules under Subdivision 815-B of the Income Tax Assessment Act 1997.

- Annual compliance: Annual review fees and lodgement of financial accounts with ASIC are required; any changes to the parent company's structure, name, or constitution must be notified within prescribed timeframes.

- Treaty access: As an extension of the parent, treaty benefits depend on the parent's country of residence and applicable double tax agreements Australia holds with that jurisdiction.

- Conversion: A registered foreign company can transition to a locally incorporated entity (e.g., a Pty Ltd), though the process involves a fresh incorporation rather than a structural conversion.

Sub-Types

Branch Office

A branch office conducts active commercial operations in Australia under the parent company's name. It generates taxable income locally and must maintain accounting records sufficient to satisfy ATO and ASIC requirements. This structure suits foreign firms that need a direct trading presence without establishing a separate corporate entity.

Representative Office

A representative office is used for liaison, market research, or promotional activities and does not engage in revenue-generating transactions. ASIC foreign company registration is still required if the office constitutes "carrying on business" under the Corporations Act 2001; however, limited-activity offices that fall below this threshold may operate without full registration. Legal advice is typically needed to assess whether a specific activity triggers the registration obligation.

Closing

Registered foreign company structures are most commonly used for short-to-medium-term market entry, project-based work, or where the parent prefers consolidated global reporting. The absence of a minimum capital requirement simplifies setup, but the unlimited liability exposure of the parent and mandatory public disclosure obligations are material drawbacks for many businesses.

This structure suits established foreign companies testing the Australian market or executing defined contracts, where forming a local subsidiary is not yet commercially justified.

Sole Trader

A sole trader structure in Australia is the simplest form of business operation available to individuals. Unlike a company, it carries no separate legal personality — you and the business are the same legal entity, meaning personal assets are exposed to business liabilities without limitation.

Registration does not involve ASIC. Instead, you apply for an Australian Business Number (ABN) through the Australian Business Register (ABR), operated by the Australian Taxation Office. If you trade under a name other than your own, that name must also be registered as a business name with ASIC under the Business Names Registration Act 2011.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business structure | No separate legal entity from the owner |

| Proprietor | Sole proprietor (one individual only) | Cannot have co-owners; no members, directors, or shareholders |

| Local Presence | ABN registration; business name registration if trading under a non-personal name | Registered through ABR and ASIC respectively |

| Capital | No minimum capital requirement; AUD-denominated | Funding drawn from personal finances or loans |

| Privacy | Business name and ABN are publicly searchable | No financial statements required to be lodged publicly |

Focus Points

- Taxation: Sole traders are taxed at individual marginal income tax rates (up to 45%), not the corporate tax rate; GST registration is required if annual turnover exceeds AUD 75,000; no separate entity-level tax applies.

- Annual Compliance: No annual review fee or ASIC lodgement obligation beyond maintaining an active ABN and current business name registration.

- Conversion: Converting to a Pty Ltd requires establishing a new company, transferring assets, and potentially triggering CGT and stamp duty obligations.

- Restrictions: Cannot raise equity capital from investors; unsuitable for structures requiring multiple owners or limited liability protection.

Closing

A sole trader arrangement suits freelancers, contractors, and early-stage operators testing a concept before committing to a formal corporate structure. The absence of incorporation costs and ongoing ASIC fees reduces administrative overhead, but unlimited personal liability remains a material risk as business activity scales.

Individuals operating independently with low liability exposure, minimal startup capital, and no requirement for outside equity investment.

How to Choose the Right Entity Type in Australia

Selecting the wrong structure has tangible legal and financial consequences — understanding how to choose a business structure in Australia before you register prevents costly corrections later.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations, tax position, and legal exposure from day one. Choosing incorrectly produces concrete outcomes:

- A foreign company that conducts business locally without registering under the Corporations Act 2001 faces penalties and potential deregistration by ASIC.

- Selecting a Company Limited by Guarantee when your business requires access to Australia's tax treaty network may disqualify you from withholding tax reductions in counterpart jurisdictions.

- Forming a proprietary company when a trust structure would better serve asset protection locks your business into annual director obligations, shareholder reporting requirements, and ASIC fees that do not apply to trusts.

- Registering a No Liability company outside the mining sector — its legally permitted scope — exposes the entity to structural invalidity challenges.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or managed investment schemes each point to a distinct structure under the Corporations Act 2001.

- Ownership and Management: Single-director proprietary companies suit sole operators, while multi-party ventures may require a partnership agreement or a company constitution governing board decisions.

- Tax Objectives: Your need for treaty access, franking credit eligibility, or flow-through taxation should determine whether a company, trust, or partnership is appropriate.

- Substance Capacity: If your firm cannot maintain genuine decision-making and operational presence locally, structures with lighter compliance thresholds — such as a partnership — may be more defensible.

- Privacy Requirements: Director and shareholder details for proprietary and public companies appear on the ASIC public register; nominee arrangements can address this where permitted.

- Exit Strategy: Not all Australian entities support redomiciliation or conversion; confirm whether your chosen structure permits winding up, transfer of registration, or restructuring before committing.

The full text of the [Corporations Act 2001](https://www.legislation.gov.au/Details/C2022C00149) is available on the Federal Register of Legislation.

Compliance Services for Companies in Australia

Ongoing compliance support for Australian entities, including ASIC filings, annual reviews, and statutory record maintenance.

Conclusion

Selecting the right structure is one of the first binding decisions you make when incorporating a business in Australia, and each option under the Corporations Act 2001 serves a distinct purpose. The Proprietary Limited Company (Pty Ltd) is the most registered entity type in Australia, favored by private businesses for its liability protection and relatively low administrative burden. Public Limited Companies suit firms seeking capital from external investors through ASX or other markets. No Liability Companies are confined to mining ventures, while Companies Limited by Guarantee serve non-profit and membership-based organizations. Partnerships offer operational flexibility without a separate legal personality, and foreign entities can enter through a registered foreign company or branch under ASIC's oversight.

Regulatory settings administered by ASIC and the ATO continue to evolve, with ongoing updates to disclosure obligations and Australia's expanding tax treaty network reflecting a maturing compliance environment. Expanship's team works directly within these frameworks to support your registration process.

How Expanship Can Assist You

Expanship's corporate services in Australia cover the full registration journey, from selecting the correct entity type to meeting your ongoing obligations under the Corporations Act 2001. Whether you are incorporating a Proprietary Limited Company (Pty Ltd), registering a foreign company, or establishing a No Liability Company for mining operations, every structure requires precise engagement with the Australian Securities and Investments Commission (ASIC).

Expanship's Australia company incorporation services include:

- Preparation and legalization of all incorporation documents

- Registered agent and registered office provision

- ASIC filing and ongoing registrar liaison

- Post-incorporation compliance management, including annual review obligations

- Business name registration and ABN/ACN applications

- Banking introduction assistance

Get in touch with Expanship Australia to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Proprietary Limited Company (Pty Ltd) is the most frequently registered structure, primarily because it limits shareholder liability, imposes fewer disclosure obligations than a public company, and suits businesses of almost any scale. ASIC registers Pty Ltd companies in far greater numbers than any other corporate form each year.

A Pty Ltd restricts share transfers and cannot offer securities to the public, while a Ltd can list on the ASX and raise capital from external investors. Both are taxed as corporate entities under the Income Tax Assessment Act 1997, but a Ltd carries significantly heavier ongoing compliance obligations, including mandatory audits and continuous disclosure requirements under Chapter 6CA of the Corporations Act 2001.

A Proprietary Limited Company provides the most privacy among Australian structures. Shareholder details are not published on the ASIC public register; only director information appears. Nominee director and shareholder arrangements are legally permissible, subject to disclosure obligations under the beneficial ownership regime.

A sole trader requires only one individual by definition, and a Pty Ltd can be formed with a single director and shareholder who is also an Australian resident. Partnerships, by contrast, require at least two partners, and an Incorporated Limited Partnership under state legislation similarly requires a general partner and at least one limited partner.

Foreigners can register a Pty Ltd, establish a branch under a Foreign Company Registration with ASIC under Part 5B.2 of the Corporations Act 2001, or operate through a representative office. A Pty Ltd requires at least one director ordinarily resident in Australia, so foreign founders typically appoint a local director to satisfy that requirement.

Conversion between certain structures is permitted. A Pty Ltd can be converted to a public company, or vice versa, by passing a special resolution and notifying ASIC. Converting a company into a partnership or sole trader arrangement is not a direct legal conversion — it requires winding up the existing entity and establishing the new structure separately.

Companies incorporated under the Corporations Act 2001 — including Pty Ltd, Ltd, No Liability, and Company Limited by Guarantee — hold separate legal personality distinct from their members. General partnerships and sole traders do not; in both cases, the individual owners bear personal liability for business obligations without the protection of a corporate veil.

A sole trader carries the lightest compliance burden, with no ASIC registration, no annual review fee, and no corporate reporting obligations. A general partnership is similarly light, though it requires an ABN and tax registration. Both structures sacrifice liability protection in exchange for that administrative simplicity.

Determining the right structure depends on factors including residency, liability exposure, capital-raising intentions, and long-term operational plans. Expanship's corporate services team works through each of these variables systematically to identify the most appropriate formation path for your specific circumstances.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.