Key Takeaways

- The Private Company Limited by Shares (Pvt Ltd) is the most commonly formed entity in Zimbabwe, governed by the Companies and Other Business Entities Act [Chapter 24:31] and registered through COBERA.

- Foreign businesses can operate in Zimbabwe without incorporating a separate local entity by registering as an External Company, Branch Office, or Representative Office.

- Companies Limited by Guarantee are structurally suited to non-profit or membership-based organisations rather than commercial, profit-driven operations.

- Zimbabwe's tax administration falls under the Zimbabwe Revenue Authority (ZIMRA), which operates a residence-based tax system that applies differently depending on the chosen business structure.

Introduction to Entity Types in Zimbabwe

Zimbabwe is a landlocked country in southern Africa, bordered by Zambia, Mozambique, South Africa, and Botswana. It is an independent republic, and business registration falls under the authority of the Companies and Other Business Entities Registry (COBERA), which administers the Companies and Other Business Entities Act [Chapter 24:31] — the primary legislation governing corporate formation and compliance.

The country operates a residence-based tax system, with the Zimbabwe Revenue Authority (ZIMRA) responsible for tax administration.

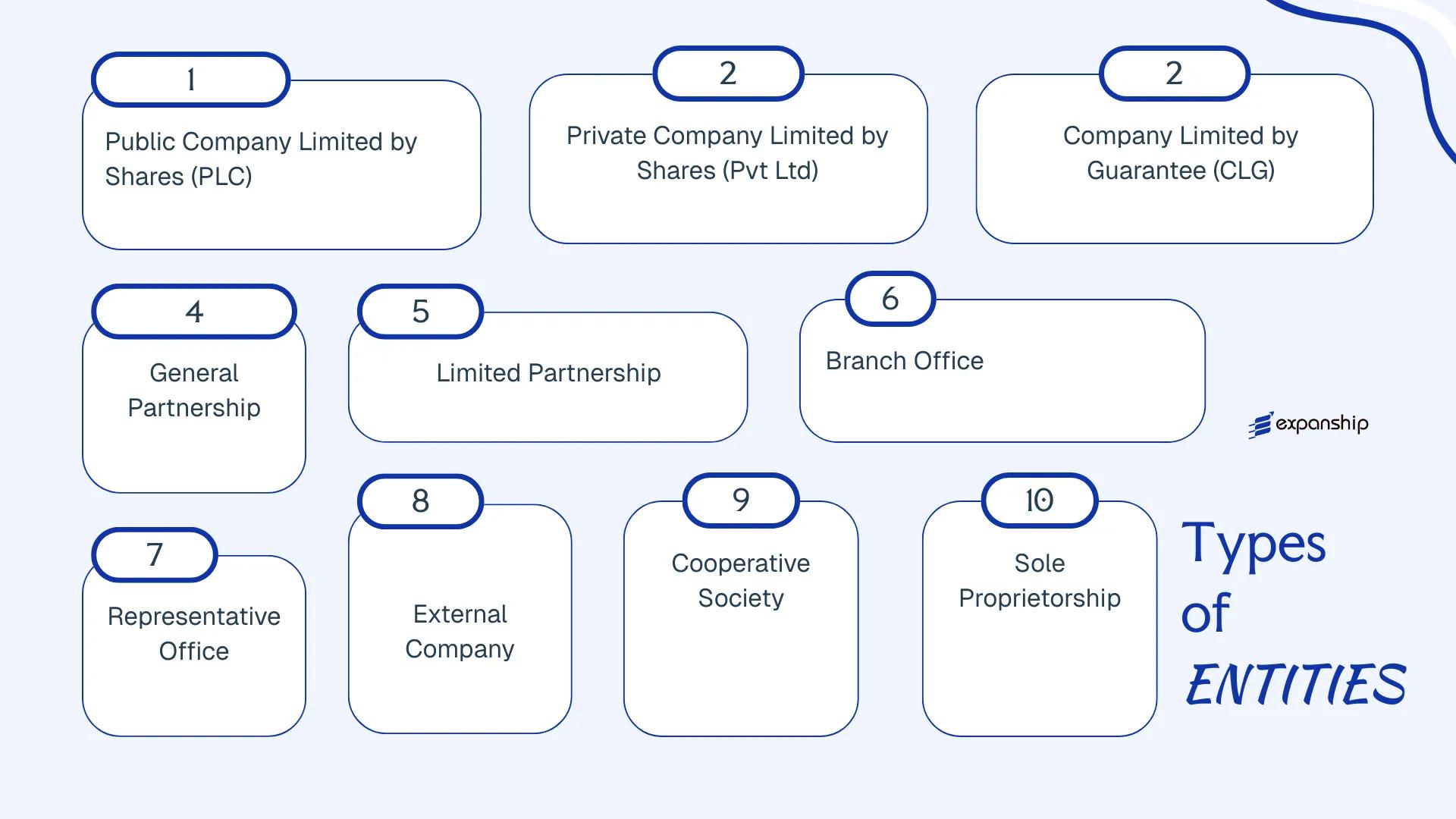

Selecting among the available types of business entities in Zimbabwe requires a clear understanding of each structure's legal standing, liability implications, and operational requirements. The entities available under Zimbabwean law include the Private Company Limited by Shares, Public Company Limited by Shares, Company Limited by Guarantee, General Partnership, Limited Partnership, External Company, Branch Office, Representative Office, Cooperative Society, and Sole Proprietorship.

Each structure carries distinct registration procedures, governance obligations, and compliance requirements. This article examines every available option in detail to help you determine which legal form suits your business objectives.

An Overview of Business Structures in Zimbabwe

Governed primarily by the Companies and Other Business Entities Act [Chapter 24:31] (COBE Act), enacted in 2019, Zimbabwe's legal framework recognises several distinct entity types available to both resident and foreign operators. The Zimbabwe Revenue Authority (ZIMRA) and the Companies and Intellectual Property Commission (CIPC) — known locally as the Companies Registry — each play a defined role in the registration and ongoing compliance of these entities. Each structure carries different implications for liability, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (PLC) | Incorporated company | Limited to shares | Taxed | Yes | 2 shareholders | Companies Registry | COBE Act |

| Private Company (Pvt Ltd) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Companies Registry | COBE Act |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed / Exempt | Yes | 1 member | Companies Registry | COBE Act |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | ZIMRA | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | ZIMRA | Partnership Act |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Yes | N/A | Companies Registry | COBE Act |

| Representative Office | Foreign entity extension | Parent liable | Generally exempt | Restricted | N/A | Companies Registry | COBE Act |

| External Company | Registered foreign company | Parent liable | Taxed | Yes | N/A | Companies Registry | COBE Act |

| Cooperative Society | Incorporated body | Limited | Taxed | Yes | 10 members | Registrar of Co-ops | Co-operative Societies Act |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | ZIMRA / Local Authority | Various |

Each of these structures is examined in full in the sections below.

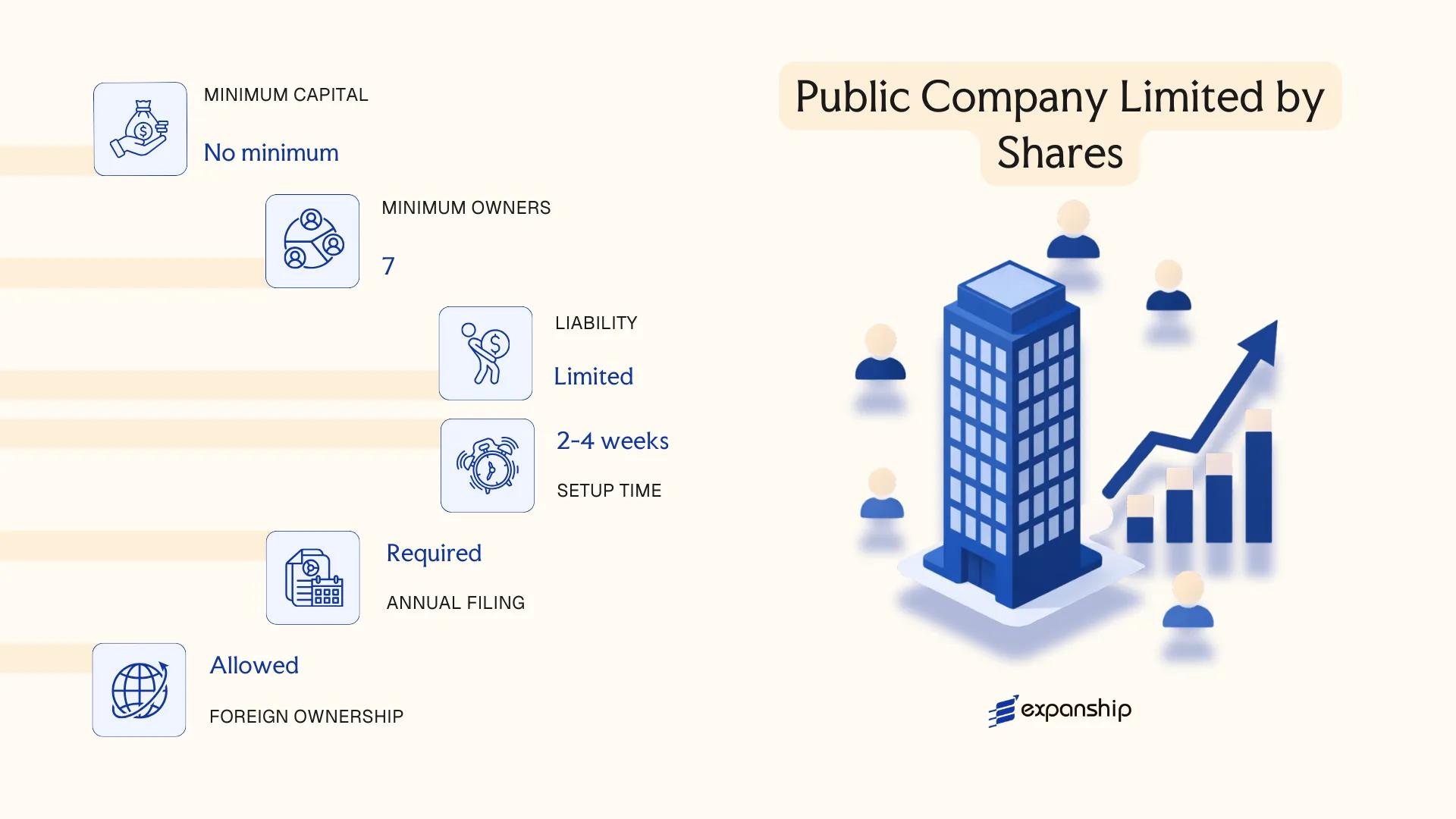

Public Company Limited by Shares (PLC)

A Zimbabwe public company limited by shares is governed by the Companies and Other Business Entities Act [Chapter 24:31], enacted in 2019 to replace the former Companies Act. Under this legislation, the entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Shareholder liability is confined to the amount unpaid on their shares. Unlike a private company, a PLC may offer its shares to the general public and, subject to meeting the Zimbabwe Stock Exchange's listing requirements, may seek admission to trading on a recognised exchange.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under COBE Act [Chapter 24:31] |

| Designated Parties | Shareholders (members), Directors, Company Secretary | Minimum 2 directors; a company secretary is mandatory |

| Members | Minimum 2 shareholders; no upper limit | Shares may be offered to the public |

| Local Presence | Registered office in Zimbabwe required | Must maintain a physical registered address, not a PO Box |

| Share Capital | Denominated in ZiG (Zimbabwe Gold) or USD | No statutory minimum capital prescribed under COBE Act |

| Privacy | Shareholder register is publicly accessible | Financial statements must be filed and are available for inspection |

Focus Points

- Taxation: Subject to corporate income tax at 25%, VAT at 15% on taxable supplies, withholding taxes on dividends and interest, and capital gains tax on disposals of specified assets; listed companies may attract a reduced corporate rate.

- Annual Compliance: Must hold an Annual General Meeting, file audited financial statements with the Registrar of Companies, and submit annual returns; listed entities face additional continuous disclosure obligations under ZSE rules.

- Audit Requirement: Statutory audit by a registered public auditor is mandatory, regardless of size.

- Conversion: May be converted to a private company by special resolution, subject to Registrar approval and compliance with COBE Act procedures.

- Treaty Access: Zimbabwe has a limited network of double taxation agreements; treaty benefits depend on the specific counterparty jurisdiction.

Recommendations

A PLC suits businesses seeking broad capital access through public subscription or eventual stock exchange listing, with the key advantage being unrestricted transferability of shares. The primary drawback is the significant ongoing compliance burden, including mandatory audits, public disclosure, and AGM requirements.

Large-scale enterprises or growth-stage businesses planning to raise public capital or pursue a Zimbabwe Stock Exchange listing.

Company Incorporation in Zimbabwe

Incorporate a public or private company in Zimbabwe with expert guidance on COBE Act compliance and registration requirements.

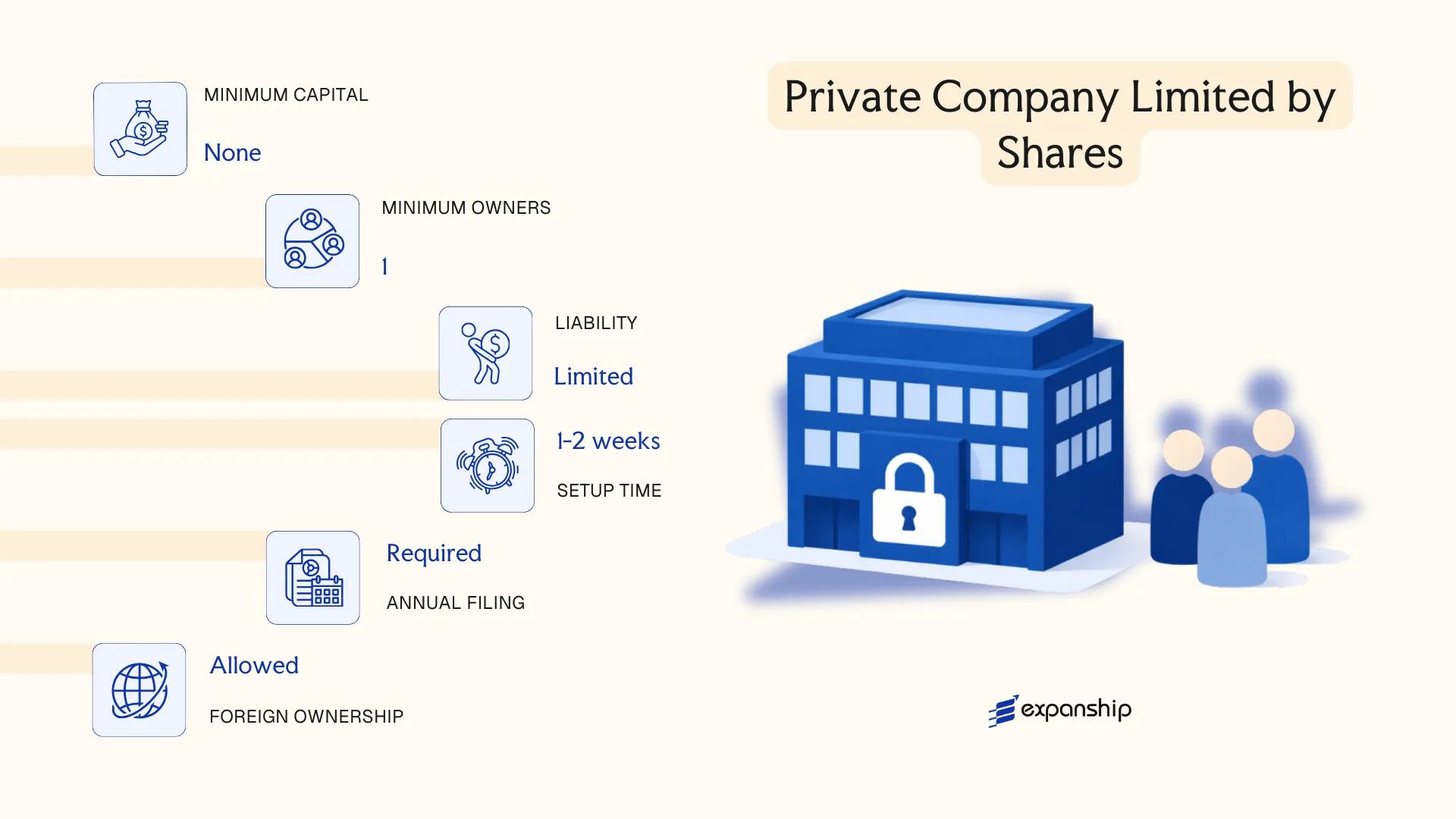

Private Company Limited by Shares (Pvt Ltd)

The Zimbabwe private company limited by shares (Pvt Ltd) is governed by the Companies and Other Business Entities Act (COBE Act), Chapter 24:31, which came into force in 2020, replacing the longstanding Companies Act. Under this legislation, the entity holds separate legal personality, meaning it can own property, enter contracts, and incur liabilities in its own name. Shareholder liability is confined to the amount unpaid on their shares.

Pvt Ltd registration Zimbabwe makes this structure the most widely used vehicle for domestic and foreign-owned businesses. The firm cannot offer its shares to the general public, and any transfer of shares is subject to restrictions set out in the articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality under COBE Act, Chapter 24:31 |

| Members | Shareholders (1–50) and at least 1 Director | Director and shareholder may be the same person; 50-shareholder cap excludes employees holding shares |

| Local Presence | Registered office address required in Zimbabwe | Must be a physical address; registered with ZIMRA and the Companies Registry |

| Share Capital | ZWL or USD; no statutory minimum | USD-denominated share capital is permissible for foreign-owned entities |

| Privacy | Shareholder details filed and publicly accessible via Companies Registry | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to 25% corporate income tax; VAT registration mandatory above the prescribed threshold; dividends withholding tax applies at 10% for non-resident shareholders; 15% withholding tax on royalties and fees paid to non-residents.

- Annual Compliance: Annual returns must be filed with the Companies Registry; audited financial statements required unless exempt.

- Economic Substance: No formal substance legislation equivalent to offshore regimes, but ZIMRA scrutinises transfer pricing and thin capitalisation for related-party transactions.

- Conversion: A Pvt Ltd may convert to a public company by special resolution and satisfying the requirements under the COBE Act.

- Restrictions: Share transfers require board or shareholder approval per the articles; public share offerings are prohibited.

Across trading, holding, and service operations, the Pvt Ltd remains the default structure for Zimbabwe private company incorporation due to its straightforward governance and limited liability protection. Its primary constraint is the 50-shareholder ceiling, which limits capital-raising capacity without restructuring.

Small to mid-sized businesses, foreign investors establishing a local operating entity, and entrepreneurs seeking a formal, liability-protected structure without public disclosure obligations for share transfers.

Company Limited by Guarantee

A company limited by guarantee Zimbabwe falls under the Companies and Other Business Entities Act (Chapter 24:31), enacted in 2019. Unlike a share-based entity, members contribute a guaranteed amount to cover debts upon winding up rather than purchasing equity. The structure carries separate legal personality and limited liability, making it functionally distinct from an unincorporated association.

Registration is handled through the Companies and Intellectual Property Commission (CIPC Zimbabwe), formerly the Registrar of Companies. This entity form is used primarily by non-profit organisations, professional associations, charities, and statutory bodies where profit distribution among members is neither intended nor permitted.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality; not share-based |

| Members | Guarantors (minimum 2, no maximum) | No shareholders; members provide a guarantee amount rather than share capital |

| Local Presence | Registered office in Zimbabwe | Must maintain a physical address within the country |

| Capital | No share capital; guarantee amount specified in Memorandum | Guarantee is typically a nominal sum (e.g., USD 1–100 per member) |

| Profit Distribution | Prohibited | Surpluses must be applied toward the entity's stated objects |

| Privacy | Directors and members listed in public register | Minimal financial disclosure for non-commercial entities |

Focus Points

- Taxation: Exempt from corporate income tax if registered as a Public Benefit Organisation (PBO) with ZIMRA; VAT registration required if turnover exceeds the prescribed threshold; withholding tax applies on payments to non-residents.

- Annual Compliance: Must file annual returns with CIPC Zimbabwe and maintain audited financial statements; failure to file triggers penalties and potential deregistration.

- Economic Substance: No formal economic substance regime applies to guarantee companies; activity must remain consistent with stated non-commercial objects.

- Conversion: Can be converted to a private company limited by shares under Chapter 24:31, subject to CIPC approval and constitutional amendment.

- Restrictions: Cannot distribute income or assets to members during operation or upon dissolution; residual assets must transfer to a similar entity or designated beneficiary.

Closing Paragraph

A guarantee company suits non-profit entities, trade associations, and professional bodies that require formal corporate standing without profit-sharing structures. The key advantage is that members bear no financial exposure beyond their stated guarantee. The primary limitation is the absolute prohibition on income distribution, which eliminates this structure for any commercial or investment purpose.

This entity type is best suited for charities, industry associations, and civil society organisations seeking legal personality and liability protection without a shareholding framework.

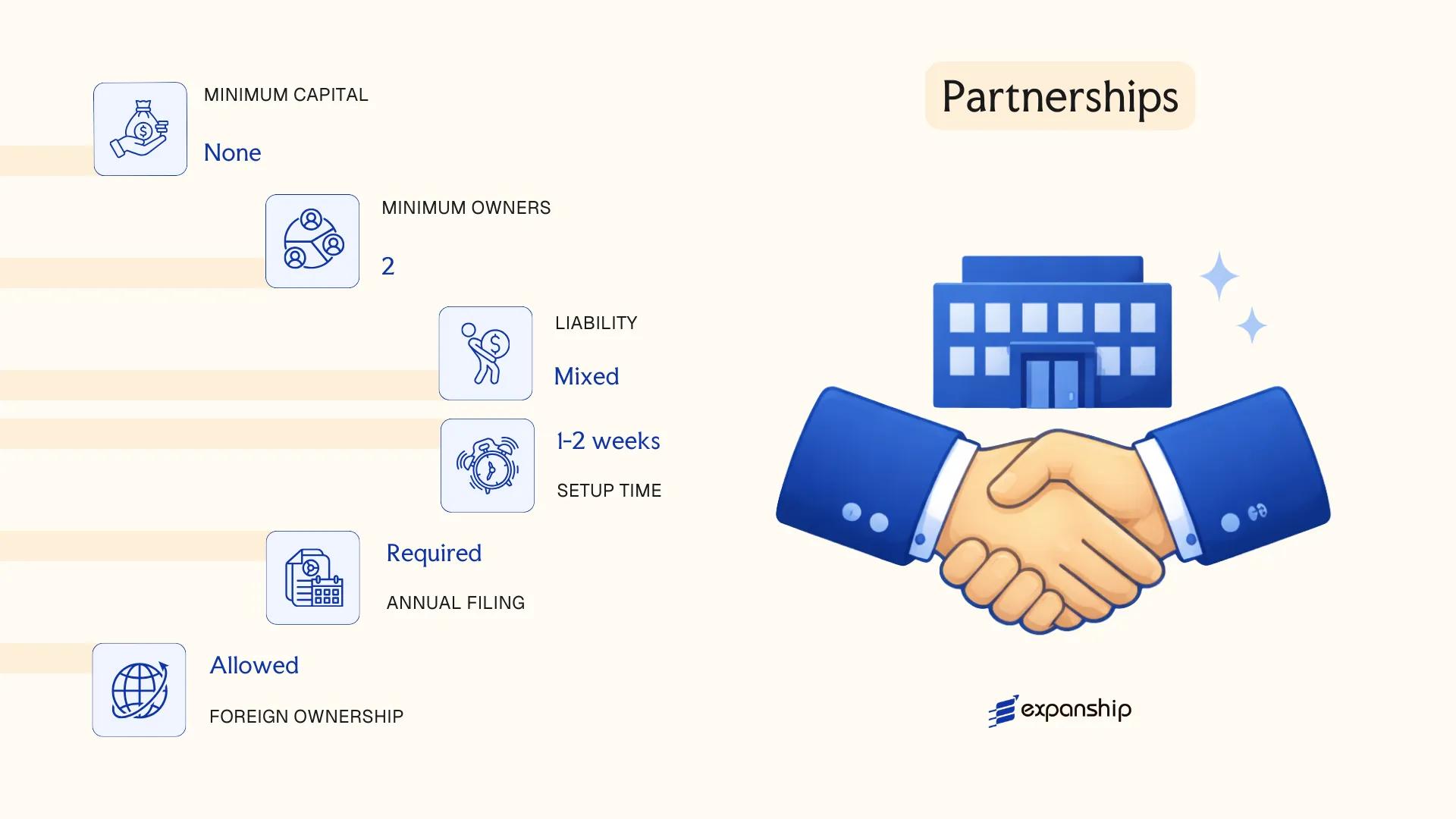

Partnerships (General Partnership, Limited Partnership)

Partnership registration in Zimbabwe is governed primarily by the Partnership Act [Chapter 24:12], which draws on common law principles inherited from Roman-Dutch law. Partnerships do not possess separate legal personality under Zimbabwean law, meaning partners bear personal liability for the firm's obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality; firm's debts are partners' debts |

| Members | Partners; minimum 2, maximum 20 (general); limited partnerships require at least 1 general and 1 limited partner | Exceeding 20 members triggers obligation to incorporate |

| Local Presence | Registered business address in Zimbabwe | No statutory registered agent requirement, but a local address is mandatory |

| Capital | Zimbabwe Gold (ZiG); no statutory minimum | Partners' contributions defined by partnership agreement |

| Privacy | Partnership agreements are not filed publicly | Partner identities may be disclosed during tax registration with ZIMRA |

| Liability | General partners: unlimited personal liability; limited partners: liability capped at capital contribution | Limited partners must not participate in management |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits taxed in partners' hands at individual or corporate income tax rates, currently up to 24%; VAT registration required if annual turnover exceeds the prescribed threshold; withholding tax applies to payments made to foreign partners.

- Annual Compliance: No annual return filed with CIPA; income tax returns filed with ZIMRA annually.

- Restrictions: Limited partners lose liability protection if they participate in day-to-day management decisions.

- Conversion: A partnership may convert to a private company by incorporating under the Companies and Other Business Entities Act [Chapter 24:31].

Sub-Types

General Partnership

All partners carry unlimited joint and several liability for the firm's debts. This structure is commonly used by professional service providers such as legal or accounting firms.

Limited Partnership

At least one general partner assumes unlimited liability while one or more limited partners contribute capital with liability restricted to that contribution. Formation requires a written partnership agreement, though Zimbabwe does not maintain a dedicated public limited partnership register comparable to some other jurisdictions.

Closing

Partnerships suit smaller professional practices or joint ventures where two or more parties wish to pool resources without the administrative burden of full incorporation. The absence of a minimum capital requirement is a practical advantage, though unlimited liability for general partners represents a significant exposure.

Partnerships in Zimbabwe are most appropriate for professional service firms or small-scale joint ventures where the partners have an established relationship and a clear, written partnership agreement is in place.

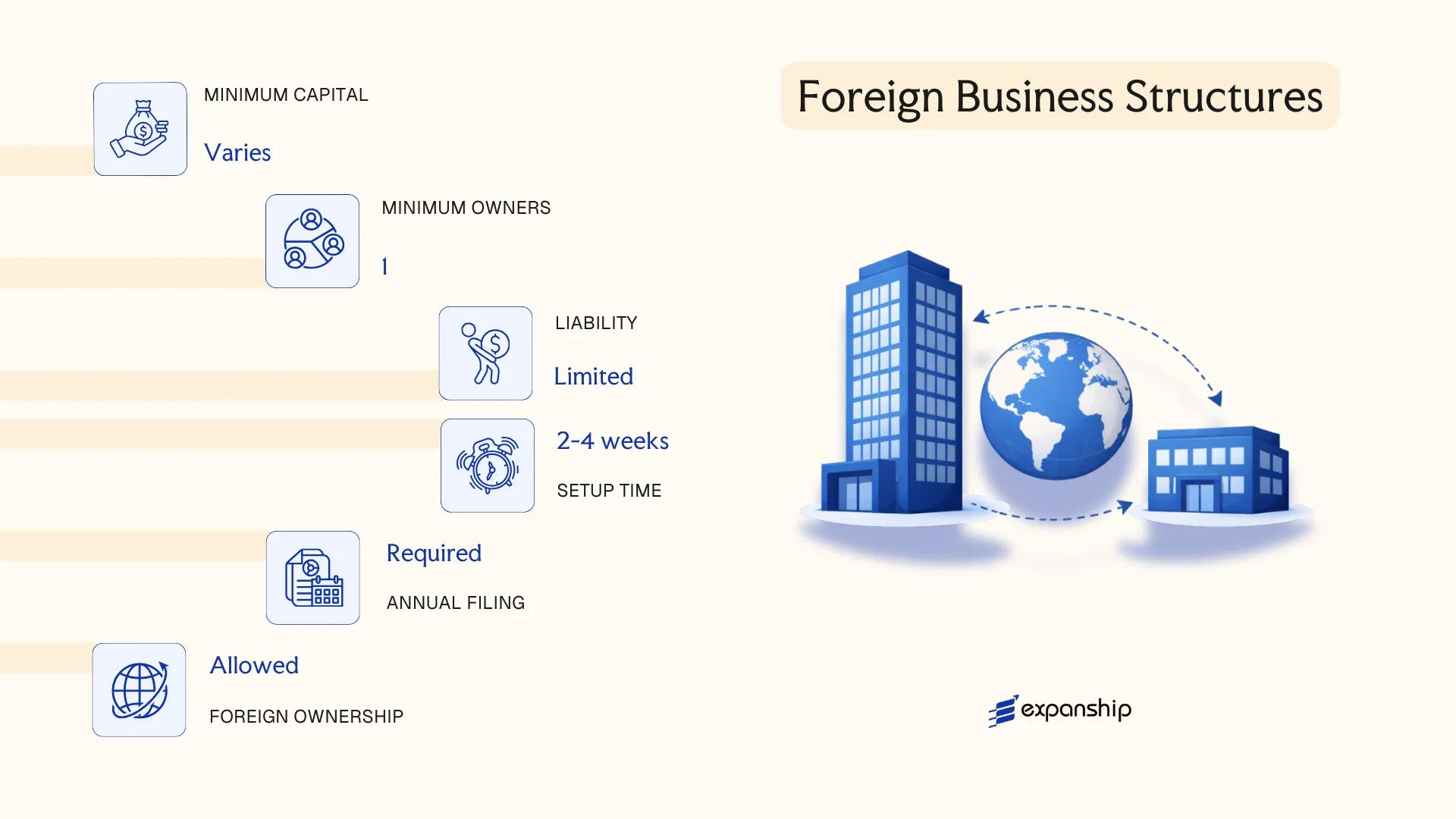

Foreign Business Structures (Branch Office, Representative Office, External Company)

Foreign entities seeking to operate in Zimbabwe must register under the Companies and Other Business Entities Act (COBE Act), Chapter 24:31, which came into force in 2020. A foreign company branch office Zimbabwe registration does not create a new legal entity — the parent company retains full liability for the branch's obligations. Under the COBE Act, foreign firms operating locally are classified as external companies and must register with the Zimbabwe Revenue Authority (ZIMRA) and the Companies and Intellectual Property Office (CIPO).

Registration requires filing prescribed forms with CIPO, submitting certified copies of the parent company's constitutional documents, and appointing a local representative. The external company must maintain a registered office address within the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | External Company / Branch | No separate legal personality; parent bears all liability |

| Representative | Local appointed agent | Must be a resident individual or locally registered entity |

| Local Presence | Registered office address required | Physical address, not a PO Box |

| Capital | No prescribed minimum | Parent company's capital structure applies |

| Disclosure | Parent's financials may be required | CIPO may require audited accounts of the parent |

| Governing Law | COBE Act, Chapter 24:31 | Administered by CIPO |

Focus Points

- Taxation: Subject to corporate income tax at 25% on Zimbabwe-sourced income; VAT registration required if turnover exceeds the threshold; withholding taxes apply on remitted profits.

- Annual Compliance: Must file annual returns with CIPO and maintain local accounting records reflecting local operations.

- Treaty Access: Zimbabwe's double taxation agreements may apply, depending on the parent's jurisdiction of incorporation.

- Restrictions: Cannot engage in activities beyond the parent company's stated objects; certain sectors require additional regulatory approvals.

- Conversion: An external company can subsequently incorporate a locally registered private company if permanent establishment is intended.

Sub-Types

Branch Office

A branch operates as a direct extension of the foreign parent, conducting revenue-generating activities under the parent's name. It is typically used by firms providing services or executing contracts within the country.

Representative Office

A representative office is restricted to liaison, marketing, and promotional activities — it cannot generate local revenue or enter into commercial contracts on its own account. This structure suits firms testing market conditions before committing to full registration.

Recommendations

Registering as an external company suits foreign businesses with defined project timelines or contractual engagements, offering a faster entry path than incorporating a new entity, though the parent's unlimited exposure to local liabilities is a material drawback for risk-sensitive structures.

Foreign companies with short- to medium-term operational commitments or those conducting pre-market research before establishing a locally incorporated subsidiary.

Cooperative Society

Cooperative society registration Zimbabwe falls under the Cooperative Societies Act [Chapter 24:05], administered by the Registrar of Co-operative Societies within the Ministry responsible for co-operative development. A registered cooperative acquires separate legal personality upon registration, meaning it can own property, enter contracts, and sue or be sued in its own name. Liability of members is generally limited to the extent of their shareholding or contribution, though the precise terms depend on the society's constitution.

Cooperatives are member-driven entities organised around a common economic purpose — agricultural marketing, savings and credit, consumer supply, or housing, among others. Each member holds an equal vote regardless of the number of shares held, which distinguishes this structure from a conventional share company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Registered under the Cooperative Societies Act [Chapter 24:05] |

| Members | Referred to as members; minimum 10, no statutory maximum | All members carry equal voting rights (one member, one vote) |

| Governing Body | Committee of Management (elected by members) | Functions similarly to a board of directors |

| Registered Office | Must maintain a registered office within Zimbabwe | Address filed with the Registrar of Co-operative Societies |

| Share Capital | Denominated in ZiG (Zimbabwe Gold); no prescribed statutory minimum | Shares are typically of low nominal value; transferability is restricted |

| Privacy | Officer and member details held on the cooperative register | Register is accessible to the public on application |

Focus Points

- Taxation: Cooperatives are subject to corporate income tax at the standard rate; agricultural cooperatives may qualify for sector-specific exemptions. VAT registration is required once turnover thresholds are met. Withholding tax applies to dividends and certain payments as under general Zimbabwean tax law.

- Annual Compliance: Societies must hold an Annual General Meeting, submit audited financial statements, and file an annual return with the Registrar of Co-operative Societies.

- Restrictions: Membership is limited to persons sharing the defined common bond; cooperative shares cannot be freely transferred to outside parties.

- Treaty Access: No preferential double tax treaty treatment specific to cooperatives; standard treaty provisions apply based on residency.

- Conversion: Conversion to a company structure is not a straightforward statutory process and would generally require dissolution and re-incorporation.

Sub-Types

Savings and Credit Cooperative Society (SACCO)

A SACCO operates exclusively around financial services — member savings mobilisation and lending — and is subject to additional oversight from the Reserve Bank of Zimbabwe under certain thresholds, distinguishing it from purely trading or agricultural cooperatives.

Agricultural Cooperative

Organised around the collective marketing, processing, or procurement of agricultural inputs and produce. This sub-type may access sector-specific government support programmes not available to general cooperatives.

A cooperative society suits member-owned businesses where collective economic activity, particularly in agriculture, housing, or savings, is the primary objective. The one-member-one-vote governance model supports equitable decision-making, though it can limit the ability to attract external investment since shareholding does not confer proportionate control.

Best suited for groups of individuals with a shared economic interest — such as farmers, artisans, or community savings groups — who require a formal legal structure with collective governance rather than investor-driven ownership.

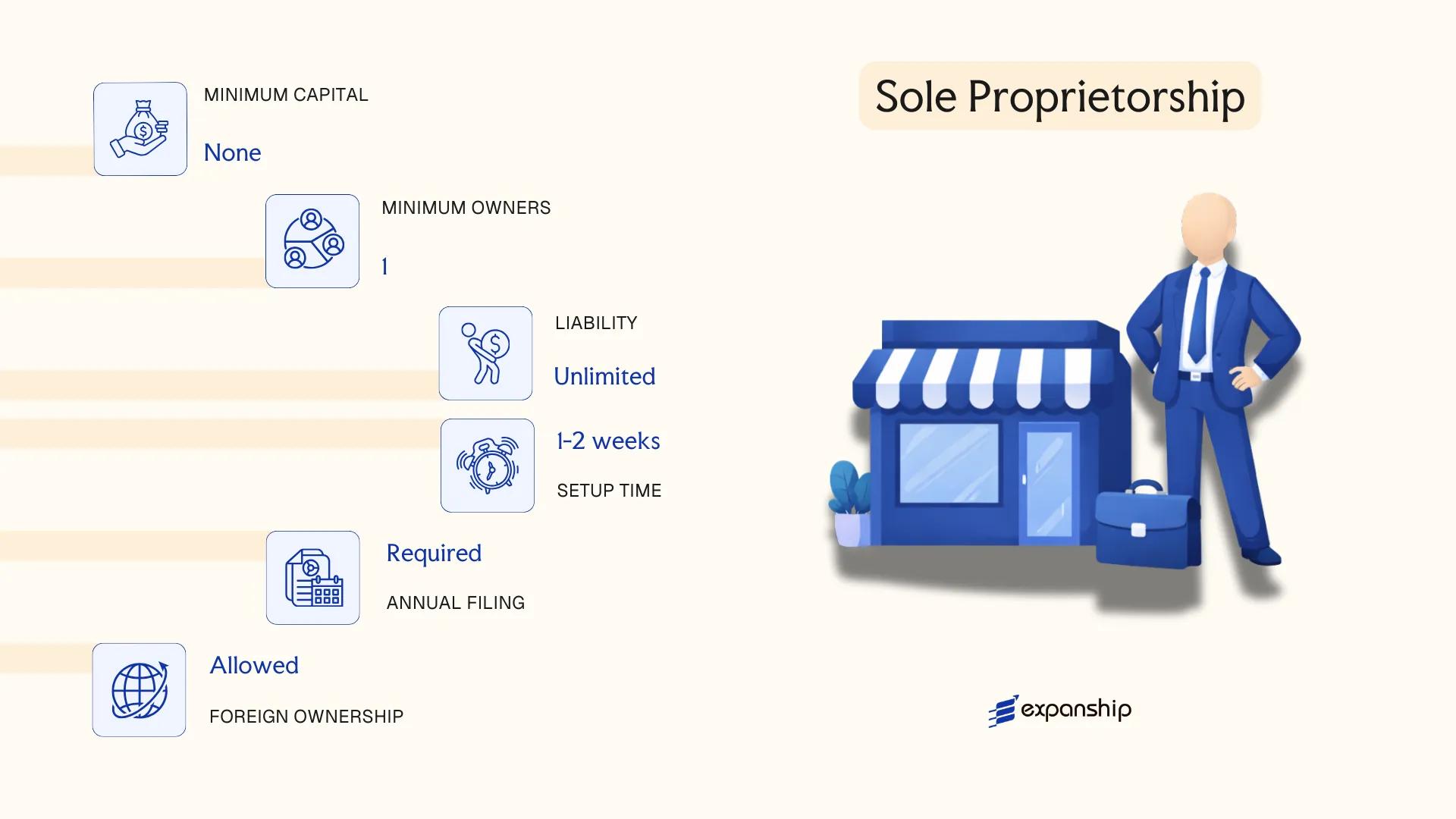

Sole Proprietorship

Sole proprietorship Zimbabwe registration does not follow a dedicated incorporation statute in the way that companies do. This structure is governed loosely under general business law principles, with registration requirements administered at the local authority level and, where applicable, through the Zimbabwe Revenue Authority (ZIMRA) for tax purposes. There is no separate legal personality — the business and its owner are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Operating as a sole trader is the most direct way to conduct business in Zimbabwe. No memorandum of incorporation is required, and setup costs are minimal. That said, the absence of limited liability makes this structure unsuitable for activities carrying significant financial or legal risk.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | One individual proprietor | No minimum capital or shareholding structure |

| Local Presence | Physical trading address required | Local authority registration applies per municipality |

| Capital | ZWG; no statutory minimum | Owner contributes personal funds directly |

| Privacy | No public registry filing | Trading name registration may be required locally |

| Liability | Unlimited personal liability | Personal assets at risk for all business debts |

Focus Points

- Taxation: Subject to personal income tax under ZIMRA; VAT registration is mandatory once turnover exceeds the prescribed threshold; no corporate tax applies.

- Annual Compliance: No statutory annual returns to the Companies and Other Business Entities Registry (COBE); local authority licence renewal is typically required annually.

- Treaty Access: No access to double taxation agreements as a non-corporate entity; income flows directly to the individual.

- Conversion: Can be converted into a private company under the Companies and Other Business Entities Act (Chapter 24:31), though assets and contracts must be formally transferred.

- Restrictions: Cannot raise equity capital or issue shares; growth financing is limited to personal funds or debt.

Closing Paragraph

A sole proprietorship suits low-risk, owner-operated trading or service activities where administrative simplicity is a priority. The key advantage is minimal setup and compliance burden; the primary limitation is unlimited personal liability, which removes any financial protection between the owner and the business.

Local traders, freelancers, and micro-enterprises operating informally or in early-stage business activity with limited liability exposure.

How to Choose the Right Entity Type in Zimbabwe

Selecting the wrong structure from the outset creates regulatory and financial consequences that are difficult to unwind. Here is what the decision actually turns on.

Why Your Entity Choice Matters

The [Companies and Other Business Entities Act \[Chapter 24:31\]](https://www.parlzim.gov.zw/acts-list/companies-and-other-business-entities-act-24-31) governs most formation decisions, and its requirements attach to the entity type, not your intentions.

- An external company that begins trading locally without registering with the Zimbabwe Registrar of Companies operates in breach of the Act and risks deregistration or financial penalties.

- Registering a tax-exempt entity when you need access to Zimbabwe's double taxation agreements means the entity cannot claim treaty-based withholding tax reductions in counterpart jurisdictions.

- Forming a private company when a trust or estate planning vehicle would suffice locks your business into annual shareholder obligations, statutory meetings, and filing requirements that do not apply to those alternatives.

- Selecting a structure that triggers mandatory audit requirements for a single-person consultancy adds recurring compliance costs that serve no proportionate purpose for that business model.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point to a distinct structure under Zimbabwean law.

- Local vs. Cross-Border Operations: If your firm will transact with Zimbabwean residents, it must be registered locally; an external company registration applies only in specific circumstances.

- Ownership and Management: Single-owner operations and multi-party arrangements carry different governance requirements, particularly regarding board composition and member liability.

- Tax Objectives: Your need for full exemption, treaty access, or eligibility under a specific tax regime should narrow the viable entity options before other factors are considered.

- Substance Capacity: If you cannot maintain staff or decision-making functions in-country, some structures will create reporting obligations your business cannot realistically satisfy.

- Exit Strategy: Redomiciliation, conversion, and voluntary winding-up procedures differ across entity types, and some structures offer fewer options than others when circumstances change.

Compliance Services for Companies in Zimbabwe

Maintain statutory obligations, annual filings, and regulatory requirements for your Zimbabwean entity.

Conclusion

A Zimbabwe company incorporation summary across all available structures reveals a spectrum suited to different ownership profiles and operational scales. The Private Company (Pvt Ltd), registered under the Companies and Other Business Entities Act [Chapter 24:31], remains the most commonly formed entity, preferred for its liability protection and operational flexibility. Public companies serve larger enterprises requiring capital market access, while companies limited by guarantee suit non-profit or membership-based organisations. Partnerships carry unlimited liability but require no formal registration with ZIMRA or CIPRO. External companies and branch offices allow foreign firms to operate without incorporating a separate local entity.

Regulatory oversight continues to consolidate under CIPRO, with ongoing efforts to digitise filing processes. Your choice of structure has direct implications for tax treatment, ownership restrictions, and reporting obligations under Zimbabwean law.

How Expanship Can Assist You

Expanship company registration Zimbabwe services are built around the specific structures and requirements discussed throughout this guide. From registering a Private Company Limited by Shares to filing the necessary documentation with the Zimbabwe Companies and Intellectual Property Commission (CIPC), every step involves local regulatory nuance that requires accurate, jurisdiction-specific handling.

Across each stage of formation and ongoing compliance, Expanship supports your business directly:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Zimbabwe

- Filing and liaison with the Companies and Intellectual Property Commission

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for corporate account setup

Our corporate services Zimbabwe clients receive end-to-end coordination, so nothing falls through the gaps between your home jurisdiction and Zimbabwean regulatory requirements.

Ready to move forward? Reach out through Expanship Zimbabwe to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Private Company Limited by Shares (Pvt Ltd) is the most frequently incorporated structure, registered with the Companies and Intellectual Property Commission (CIPC). Its liability protection, relatively straightforward formation requirements, and suitability for both small and medium-sized operations account for its consistent popularity.

A Pvt Ltd, Public Company, and Company Limited by Guarantee each carry separate legal personality under the COBE Act. General Partnerships and Sole Proprietorships do not — owners in those structures remain personally liable for business obligations without the legal separation that incorporation provides.

Among registered entities, a Private Company discloses less publicly than a Public Company, which is subject to broader reporting obligations. Nominee directorship arrangements are available, though beneficial ownership disclosure requirements under the country's anti-money laundering framework still apply.

A Pvt Ltd can be formed by a single shareholder and one director. General Partnerships require a minimum of two partners, making sole formation impossible. A Sole Proprietorship, by definition, involves one natural person operating without co-owners.

Foreign individuals and corporate bodies may register a Pvt Ltd, incorporate as an External Company, or establish a Branch Office. Certain sectors remain subject to indigenisation and local ownership thresholds, so the applicable investment regulations must be reviewed before selecting a structure.

The COBE Act allows for re-registration between certain categories — for example, a Private Company may convert to a Public Company by meeting the relevant share and governance thresholds. Conversion from a company to a partnership is not a recognised continuation process under the Act; a new entity would need to be formed.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.