Key Takeaways

- Vanuatu's zero-tax environment — with no income tax, capital gains tax, or withholding tax — makes the International Company its most registered formation, particularly among non-resident entrepreneurs seeking offshore holding structures.

- All business entities in Vanuatu, from International Companies to sole proprietorships, are registered and overseen by the Vanuatu Financial Services Commission (VFSC) under the Companies Act and related legislation.

- The jurisdiction's legal framework draws from both English common law and French civil law traditions, a direct consequence of the Anglo-French Condominium that governed the territory prior to independence in 1980.

- Entity selection in Vanuatu is increasingly shaped by the VFSC's trajectory toward greater transparency and alignment with international compliance standards, beyond formation costs or tax position alone.

Introduction to Entity Types in Vanuatu

Vanuatu is an archipelago nation in the South Pacific, situated northeast of Australia and east of New Caledonia, comprising roughly 80 islands. It is an independent republic and a member of the United Nations, with a legal system that draws from both English common law and French civil law traditions — a legacy of the Anglo-French Condominium that preceded independence in 1980.

Company registration and oversight fall under the Vanuatu Financial Services Commission (VFSC), which serves as the central regulatory authority for business entity types in Vanuatu. The VFSC administers the Companies Act and related legislation governing the formation and maintenance of corporate structures.

From a tax perspective, Vanuatu operates with no income tax, no capital gains tax, and no withholding tax, making it a zero-tax jurisdiction for most business activities.

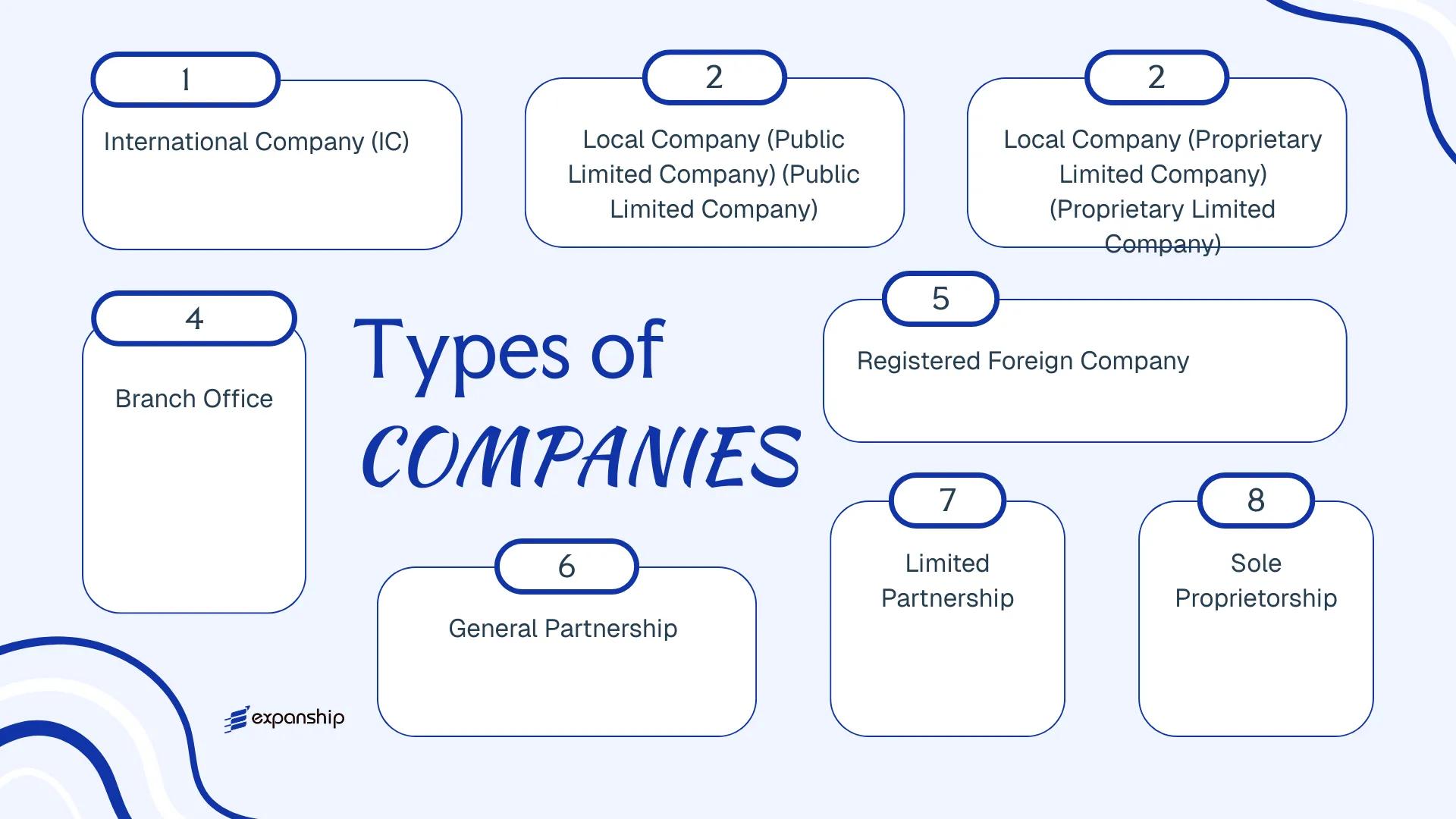

The types of companies in Vanuatu available for registration include:

- International Company (IC)

- Local Company — Public Limited

- Local Company — Proprietary Limited

- Registered Foreign Company (Branch)

- General Partnership

- Limited Partnership

- Sole Proprietorship

Each structure differs in ownership requirements, liability treatment, permitted activities, and reporting obligations. This article examines each option in detail to help you determine which formation best fits your operational and compliance requirements.

An Overview of Business Structures in Vanuatu

Vanuatu's company law framework accommodates several distinct entity types, each governed primarily by the Companies Act [CAP 191] and, for internationally-focused structures, the International Companies Act [CAP 222]. Administered through the Vanuatu Financial Services Commission (VFSC), these structures range from locally-trading proprietary companies to tax-exempt international companies and registered foreign branches. Each form carries a different liability profile, tax treatment, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| International Company (IC) | Incorporated company | Limited | Exempt | No | 1 shareholder | VFSC | International Companies Act [CAP 222] |

| Public Limited Company | Incorporated company | Limited | Taxed | Yes | 2 shareholders | VFSC | Companies Act [CAP 191] |

| Proprietary Limited Company | Incorporated company | Limited | Taxed | Yes | 1 shareholder | VFSC | Companies Act [CAP 191] |

| Branch Office | Foreign body corporate | Parent liable | Taxed | Yes | N/A | VFSC | Companies Act [CAP 191] |

| Registered Foreign Company | Foreign body corporate | Parent liable | Taxed | Yes | N/A | VFSC | Companies Act [CAP 191] |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | N/A | Partnership Act [CAP 212] |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | N/A | Partnership Act [CAP 212] |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed | Yes | 1 owner | N/A | Business Names Act |

Each of these structures is examined in full in the sections below.

International Company (IC)

Vanuatu International Company IC registration is governed by the International Companies Act \[CAP 222\], which consolidates the legal framework for offshore entities incorporated under this structure. An IC holds a separate legal personality distinct from its members, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholders bear no personal liability beyond their contributed capital.

Administered by the Vanuatu Financial Services Commission (VFSC), the IC is the principal vehicle for cross-border commercial activity, asset holding, and international trade structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | International Company (IC) | Incorporated under the International Companies Act \[CAP 222\] |

| Members | Shareholders: minimum 1, no maximum | Corporate shareholders permitted; bearer shares are prohibited |

| Management | Directors: minimum 1, no maximum | No residency requirement for directors; corporate directors permitted |

| Local Presence | Registered Agent required; no registered office obligation beyond agent's address | Agent must be VFSC-licensed |

| Capital | No minimum share capital; any currency permitted | Shares may be issued with or without par value |

| Privacy | Beneficial ownership recorded with VFSC but not on public register | Director and shareholder details are not publicly disclosed |

Focus Points

- Taxation: ICs are exempt from all domestic taxes, including corporate income tax, withholding tax, VAT, and stamp duty, provided they conduct no business with Vanuatu residents.

- Economic Substance: No economic substance requirements currently apply to ICs incorporated in Vanuatu.

- Annual Compliance: Annual renewal fees are payable to the VFSC; no audited financial statements are required, though basic records must be maintained.

- Treaty Access: Vanuatu has a limited tax treaty network; ICs generally cannot access treaty benefits, which may affect structures involving treaty-dependent income flows.

- Restrictions: ICs are prohibited from conducting banking, insurance, or trust business without additional licensing, and cannot trade directly with Vanuatu residents.

Closing

The IC suits non-resident investors using Vanuatu as a holding, trading, or IP ownership vehicle where offshore tax exemption and structural confidentiality are priorities. Its primary limitation is restricted treaty access, which narrows its utility for income flows subject to foreign withholding taxes.

The IC is most appropriate for internationally mobile entrepreneurs and non-resident investors seeking a tax-neutral, low-compliance offshore entity with no substance obligations.

Company Incorporation in Vanuatu

Incorporate an International Company (IC) or other entity type in Vanuatu through Expanship's end-to-end incorporation service.

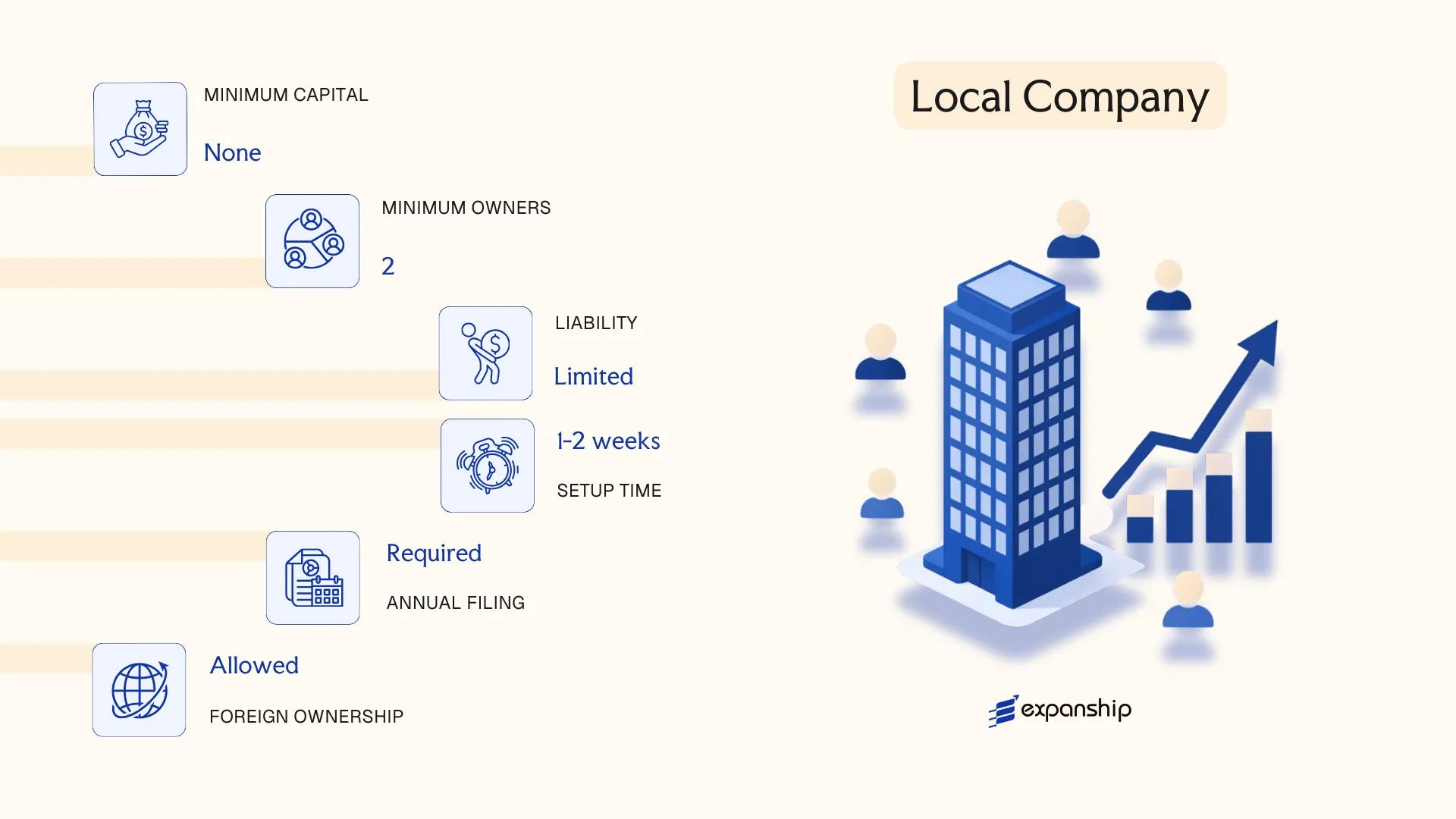

Local Company (Public Limited Company)

Vanuatu public limited company registration is governed by the Companies Act \[CAP 191\], which provides for a locally incorporated entity with separate legal personality and limited liability for its shareholders. This structure is designed primarily for businesses that intend to raise capital from the public through the issuance of shares to an unrestricted pool of investors.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under Companies Act \[CAP 191\] |

| Members | Shareholders; minimum 2, no maximum | Directors: minimum 2; no residency requirement |

| Local Presence | Registered office in Vanuatu required | Must maintain a registered address at all times |

| Capital | Denominated in VUV or foreign currency; no statutory minimum | Shares may be offered to the general public |

| Privacy | Shareholder and director details filed with VFSC | Records are accessible to the public |

Focus Points

- Taxation: No corporate income tax, no withholding tax, no VAT, and no capital gains tax apply to local public companies; stamp duty may apply to certain transactions.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Vanuatu Financial Services Commission (VFSC).

- Public Offering: Share issuance to the public requires compliance with applicable securities regulations administered by the VFSC.

- Conversion: A public company may be re-registered as a proprietary limited company subject to meeting the relevant conditions under the Act.

A public limited company suits larger commercial operations or businesses seeking to raise equity from external investors, with the key advantage of unrestricted share transferability. The primary drawback is the higher compliance burden, including mandatory audits and public disclosure of corporate records.

This structure is most appropriate for businesses seeking public investment or planning a future listing on a recognised exchange.

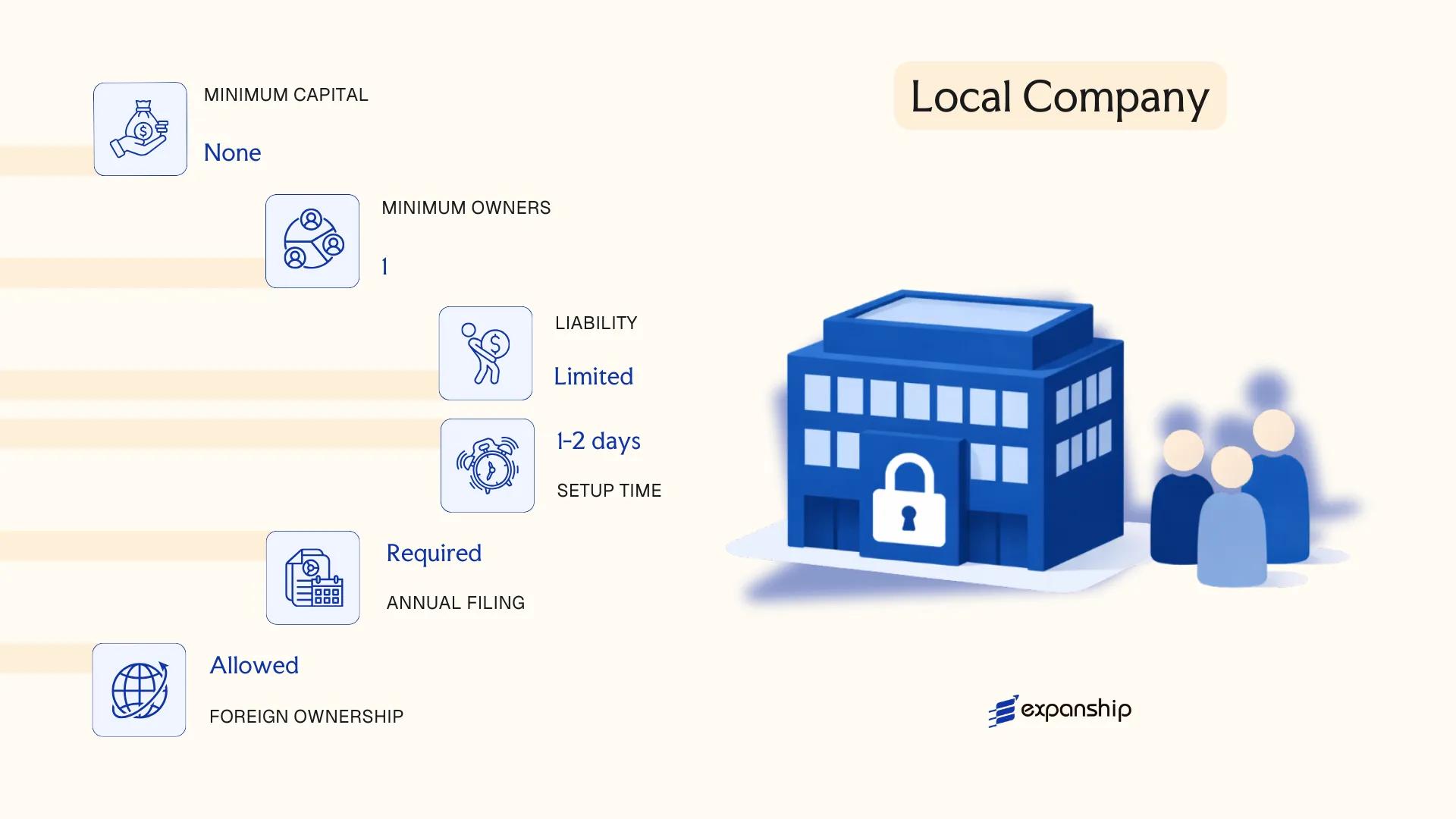

Local Company (Proprietary Limited Company)

A Vanuatu proprietary limited company setup is governed by the Companies Act \[CAP 191\], the same legislation that covers public companies. The proprietary limited company is a private entity with separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares.

Designed for closely held ownership, this structure restricts the public offering of shares and limits the transferability of interests. It suits resident-owned businesses, joint ventures, and family-held commercial operations where external capital raising is not required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Separate legal personality; cannot offer shares to the public |

| Members | Shareholders: min. 1, max. 50 | Directors: min. 1; no nationality requirement specified under general provisions |

| Local Presence | Registered office in Vanuatu required | Must maintain a local registered address; a registered agent is advisable |

| Capital | No statutory minimum share capital; VUV or foreign currency permitted | Shares must be fully or partly paid on issue |

| Privacy | Register of members is not fully public | Beneficial ownership details held internally; VFSC maintains company records |

Focus Points

- Taxation: No corporate income tax, no capital gains tax, no VAT, and no withholding tax on dividends; stamp duty may apply to certain instruments.

- Annual Compliance: Annual returns must be filed with the Vanuatu Financial Services Commission (VFSC); financial records must be maintained.

- Economic Substance: Domestic trading companies do not face the same substance requirements applied to International Companies.

- Restrictions: Share transfers require compliance with the articles of association; public share offerings are prohibited.

- Conversion: A proprietary company may convert to a public company by amending its constitution and meeting VFSC requirements.

Closing

This structure suits small-to-medium domestic businesses, family enterprises, and joint ventures requiring limited liability without the compliance burden of a public company. Its principal limitation is the cap on shareholders and the prohibition on public fundraising.

Local entrepreneurs and resident investors seeking a straightforward private trading or holding structure with capped liability and no public disclosure obligations.

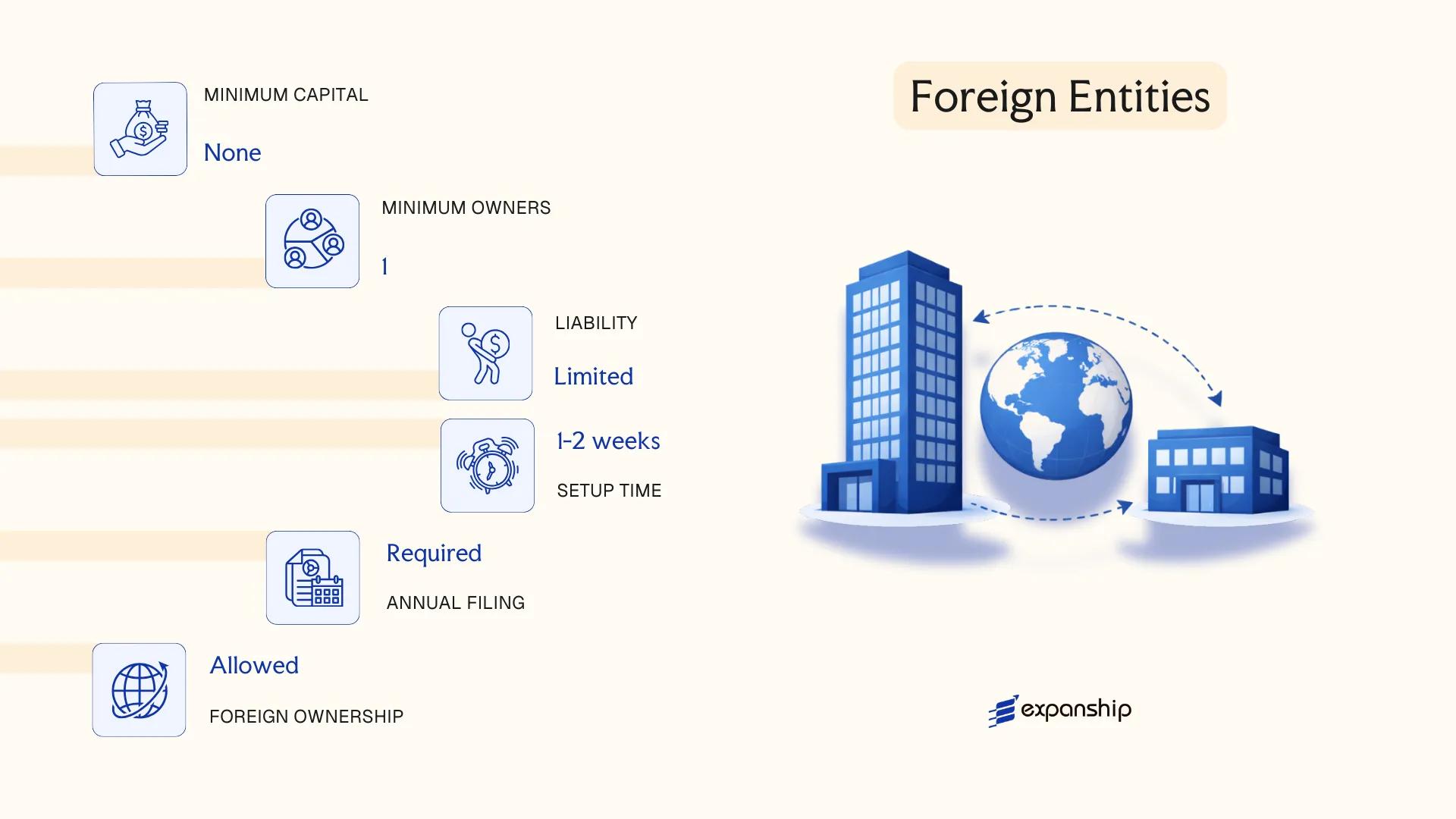

Foreign Entities in Vanuatu [Branch Office, Registered Foreign Company]

Registering a foreign company in Vanuatu is governed by the Companies Act \[CAP 191\], which requires any overseas entity carrying on business locally to register as a foreign company with the Vanuatu Financial Services Commission (VFSC). A registered foreign company does not constitute a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations.

Foreign entities do not incorporate a new legal person under Vanuatu law. Instead, they obtain recognition to operate locally while remaining subject to the laws of their home jurisdiction for matters of internal governance and constitution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Registered Foreign Company | Not a separate legal entity; parent bears full liability |

| Members | Directors of the parent company; local agent required | No separate shareholder structure created locally |

| Local Presence | Registered agent and a physical place of business in Vanuatu | VFSC requires a local address for service of documents |

| Capital | No prescribed minimum capital for registration | Parent company's capital structure applies |

| Privacy | Parent company's constitutional documents filed with VFSC | These become public record upon registration |

Focus Points

- Taxation: No corporate income tax, no withholding tax, and no VAT applies to business income; customs duties may apply to goods imported for local operations.

- Annual Compliance: Annual returns and financial statements of the parent must be filed with the VFSC; failure to file attracts penalties under CAP 191.

- Economic Substance: Trading activities conducted locally may attract substance considerations depending on the nature of income earned.

- Treaty Access: Vanuatu's limited tax treaty network means the foreign parent generally cannot rely on treaty protections through the branch.

- Restrictions: Certain regulated sectors — banking, insurance, and financial services — require additional licensing regardless of the registration status.

Sub-Types

Branch Office

A branch office is the standard operational form for a foreign entity conducting active trade or service delivery within Vanuatu. It carries no liability ring-fencing; any claims against the branch can be pursued against the parent company's global assets.

Registered Foreign Company (Non-Trading)

Some foreign entities register solely to hold property, enter contracts, or maintain a legal presence without conducting active commerce. The registration process under CAP 191 is the same, but the scope of permitted activity is narrower.

Closing

A registered foreign company suits businesses that need a direct operational presence without the administrative overhead of incorporating a separate subsidiary, though the absence of liability separation between parent and branch is a material commercial risk to consider.

This structure is most appropriate for established foreign businesses expanding into Vanuatu for a defined operational purpose where consolidating branch results into the parent's accounts is a deliberate accounting preference.

Partnerships in Vanuatu [General Partnership, Limited Partnership]

Vanuatu partnerships are governed by the Partnership Act [Cap 152], which applies to both general and limited partnership structures. A general partnership does not carry separate legal personality — partners bear joint and unlimited liability for the firm's obligations. Vanuatu limited partnership registration introduces a two-tier membership model, separating liability between general and limited partners.

Under a limited partnership, at least one general partner retains unlimited liability and manages the business, while limited partners contribute capital and enjoy liability capped at their investment. This structure is sometimes used by investment vehicles and fund structures where passive investor protection matters.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Personality | None | None |

| Members | Partners (min. 2, max. 20) | Min. 1 general partner + 1 limited partner |

| Management | All partners | General partner(s) only |

| Liability | Unlimited for all partners | Unlimited for general partner; capped for limited partners |

| Local Presence | Registered address required | Registered address required |

| Capital | No statutory minimum; no prescribed currency | No statutory minimum |

| Privacy | Partner names on public record | General partner names on public record |

Focus Points

- Taxation: Vanuatu levies no corporate income tax, no withholding tax, and no VAT on partnerships; partners are generally taxed in their own jurisdictions on distributed income.

- Annual Compliance: Partnerships must maintain a registered address and file any changes in partnership composition with the Vanuatu Financial Services Commission (VFSC).

- Treaty Access: Vanuatu has a limited tax treaty network; partnerships typically cannot access treaty benefits on behalf of partners.

- Restrictions: Partnerships may not be used for regulated financial services activities without the appropriate licence from the VFSC.

- Conversion: Converting a partnership to a company structure is possible but requires a fresh incorporation process rather than a statutory conversion mechanism.

Sub-Types

General Partnership

All partners participate in management and carry unlimited personal liability. This structure suits small trading operations or professional practices where co-owners actively run the business.

Limited Partnership

The Vanuatu LP vs general partnership distinction turns on liability and control: limited partners sacrifice management rights in exchange for capped exposure. This format is more common in investment holding or collective arrangements where passive capital participation is the objective.

General partnerships suit closely held trading or professional arrangements with active co-owners; limited partnerships are more appropriate where passive investor participation and capital protection are required. The absence of income tax is a material advantage, though the lack of separate legal personality means creditors can pursue partners personally.

Limited partnerships are best suited for passive investment structures or fund arrangements where at least one experienced operator can act as the managing general partner.

Sole Proprietorship

Operating as a sole proprietorship in Vanuatu is the simplest form of business structure available to individuals. There is no dedicated sole trader statute — this structure operates under general business licensing requirements administered by the Vanuatu Financial Services Commission (VFSC) and relevant municipal or provincial authorities.

Unlike incorporated entities, a sole proprietorship carries no separate legal personality. The individual owner and the business are legally the same, meaning personal assets are fully exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital required; no shareholders or directors |

| Local Presence | Business licence required | Issued by VFSC or local authority depending on activity |

| Capital | No statutory minimum | Owner funds the business directly |

| Privacy | Name registered under individual's legal name | Trading name registration available |

Focus Points

- Taxation: No corporate income tax, capital gains tax, withholding tax, or VAT in Vanuatu; the proprietor may be subject to business licence fees based on turnover.

- Annual Compliance: Business licence renewal required annually; no formal annual return filing to VFSC.

- Treaty Access: No access to double tax treaty benefits as an unincorporated individual business.

- Conversion: Can convert to a proprietary limited company by incorporating a new entity and transferring business assets.

- Restrictions: Foreign nationals face restrictions on operating sole proprietorships in sectors reserved for Vanuatu citizens under the Foreign Investment Act.

Closing

A sole proprietorship suits freelancers, local traders, and individuals testing a small-scale operation, with minimal setup cost as its primary advantage — though unlimited personal liability remains a significant structural risk.

Local residents or citizens running small, low-risk businesses who want the lowest possible administrative overhead.

How to Choose the Right Entity Type in Vanuatu

Choosing the right company structure in Vanuatu is a decision with direct legal and financial consequences — not a preference to be revisited easily after registration.

Why Your Entity Choice Matters

The structure you register shapes your obligations, your tax position, and your exposure to regulatory risk from day one. Selecting the wrong entity type produces concrete outcomes:

- Registering an International Company and then trading locally with Vanuatu residents puts you in breach of the [International Companies Act \[CAP 222\]](https://www.vanuatulaw.com), which can result in striking off or financial penalties.

- Choosing a tax-exempt offshore entity when you need access to double tax agreements means you cannot claim withholding tax reductions in counterpart jurisdictions, as exempt entities are typically excluded from treaty benefits.

- Selecting a structure that requires audited financial statements when your operation is a single-person consultancy introduces unnecessary annual compliance costs that a simpler entity would avoid.

- Forming a company when a trust or foundation would serve your asset protection objectives locks you into annual shareholder and directorship obligations that those alternative structures do not carry.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated sectors such as funds or insurance each point toward a distinct structure under Vanuatu law.

- Local vs. Offshore Operations: If your firm intends to transact with Vanuatu residents or employ local staff, an International Company is prohibited from doing so and a local proprietary or public limited company is required instead.

- Ownership and Management: Single-owner operations have different governance needs than multi-party arrangements, and the degree of management flexibility varies significantly between company and partnership structures.

- Tax Objectives: Vanuatu imposes no corporate income tax, but your home jurisdiction's controlled foreign corporation rules or substance requirements may still affect which entity type is viable.

- Privacy Requirements: The public register maintained by the Vanuatu Financial Services Commission discloses certain company information; your tolerance for that disclosure should inform whether nominee arrangements are necessary.

- Exit Strategy: Not all entity types in Vanuatu permit redomiciliation or conversion; confirm at formation whether the structure supports your intended exit or restructuring path.

Compliance Services for Companies in Vanuatu

Ongoing compliance support for Vanuatu-registered entities, including annual returns, registered agent obligations, and regulatory filings with the Vanuatu Financial Services Commission.

Conclusion

This Vanuatu company incorporation summary reflects a jurisdiction that offers structurally distinct options across its primary entity categories. The International Company remains the most registered formation, favoured by non-resident entrepreneurs seeking a tax-neutral offshore holding structure under the International Companies Act. Local Proprietary Limited Companies suit resident-operated businesses with restricted shareholding, while Public Limited Companies apply where broader capital raising is required. Registered foreign companies and branch offices serve multinationals extending existing operations into the market. General and limited partnerships fit smaller ventures or professional arrangements, and sole proprietorships remain the simplest entry point for individual traders.

Vanuatu's regulatory framework, overseen by the Vanuatu Financial Services Commission, has trended toward greater transparency and compliance alignment with international standards. Your choice of entity will increasingly be shaped by that trajectory as much as by formation costs or tax position.

How Expanship Can Assist You

Expanship's Vanuatu company registration services cover the full process — from selecting the right structure under the Companies Act to filing with the Vanuatu Financial Services Commission (VFSC). Whether you are forming an International Company for offshore asset holding or registering a local Proprietary Limited Company for operations on the ground, your setup is handled with jurisdiction-specific knowledge, not generic templates.

From initial documentation through to ongoing compliance, here is what Expanship provides:

- Document preparation and notarization

- Registered agent and registered office provision

- Government filing and VFSC liaison

- Post-incorporation compliance management

- Banking introduction assistance

As a corporate services provider in Vanuatu, Expanship works directly with the relevant authorities on your behalf, so nothing falls through the cracks after incorporation.

Get in touch with Expanship Vanuatu to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The International Company (IC) is by far the most registered structure, primarily because it is exempt from local income tax and imposes no requirements on shareholders to reside in-country. Its straightforward incorporation process under the International Companies Act makes it the default choice for non-resident entrepreneurs.

An IC is prohibited from trading with Vanuatu residents and holds no local tax obligations, whereas a Proprietary Limited Company can transact domestically and is subject to local regulatory oversight. Compliance obligations for a domestic Proprietary Limited Company are considerably more extensive, including requirements under the Companies Act [CAP 191].

The International Company provides the highest degree of confidentiality; beneficial ownership details and shareholder registers are not part of the public record. Nominee director and shareholder arrangements are permissible, adding a further layer of separation between the beneficial owner and the registered entity.

An IC requires only one director and one shareholder, and a Proprietary Limited Company can also be formed by a sole individual. Partnerships, whether general or limited, require a minimum of two partners by legal definition, making sole formation impossible for those structures.

Foreign nationals may incorporate an International Company without restriction, and may also register a Proprietary Limited Company or a Public Limited Company under the Companies Act [CAP 191]. Establishing a branch office requires registration as a foreign company with the Vanuatu Financial Services Commission, which involves submitting certified constitutional documents from the home jurisdiction.

The Companies Act [CAP 191] provides mechanisms for re-registration between certain domestic company types, such as converting a Proprietary Limited Company to a Public Limited Company. Conversion between an International Company and a domestic entity involves a more involved process and generally requires engaging the Vanuatu Financial Services Commission directly.

International Companies, Proprietary Limited Companies, and Public Limited Companies all hold separate legal personality distinct from their members. General partnerships do not; partners bear personal liability for obligations of the firm. Limited partnerships occupy a middle position — the limited partner's liability is capped, but the general partner remains personally exposed.

The International Company imposes the lightest compliance burden: there are no annual financial reporting requirements to a public registry and no local audit obligations under current regulations. By contrast, domestic companies registered under the Companies Act [CAP 191] must meet filing and record-keeping standards administered by the Vanuatu Financial Services Commission.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.