Key Takeaways

- Vietnam's business entity framework is governed primarily by the Law on Enterprises No. 59/2020/QH14 and the Law on Investment No. 61/2020/QH14, which together define structures ranging from Joint Stock Companies to Business Cooperation Contracts.

- All enterprises must register through the National Business Registration Portal administered by the Department of Business Registration under the Ministry of Planning and Investment and obtain an Enterprise Registration Certificate before commencing operations.

- Foreign investors entering Vietnam most commonly use the wholly foreign-owned enterprise structure, while joint ventures remain the appropriate vehicle where local partnership is strategically or legally required.

- The Joint Stock Company (Công ty Cổ phần) is the designated structure for businesses intending to raise capital from multiple shareholders or pursue a future public listing under Vietnamese law.

Introduction to Entity Types in Vietnam

Located in Southeast Asia, Vietnam shares land borders with China, Laos, and Cambodia, and sits along the South China Sea. It is a unified socialist republic governed by the Communist Party of Vietnam, which directly shapes the legal framework within which businesses operate.

Company registration falls under the authority of the National Business Registration Portal, administered by the Department of Business Registration under the Ministry of Planning and Investment. Enterprises must register through this portal and obtain an Enterprise Registration Certificate before commencing operations. Vietnam applies a standard corporate income tax regime, with specific rates and incentives varying by industry, location, and investment scale.

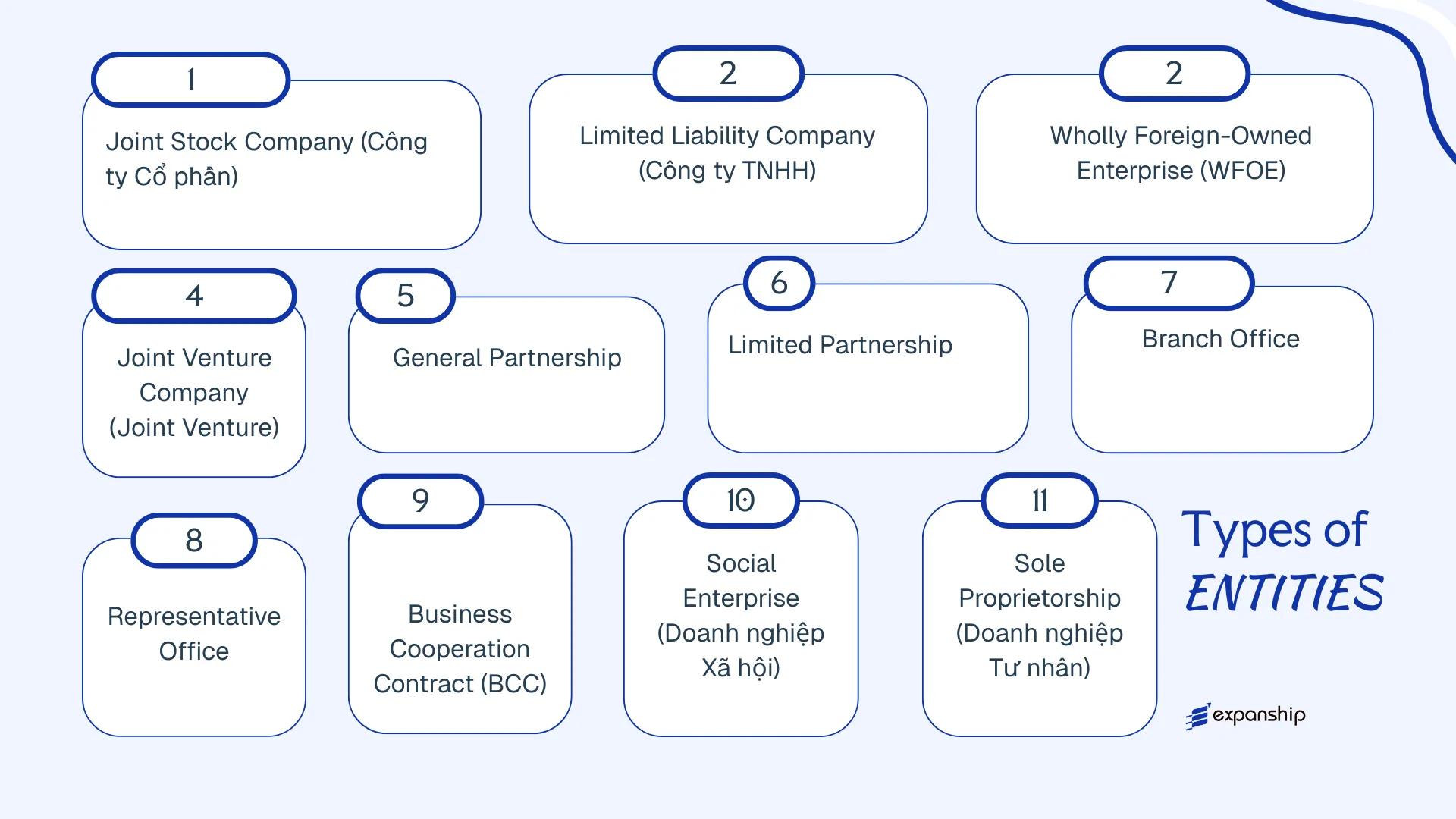

The types of business entities in Vietnam are defined primarily under the Law on Enterprises No. 59/2020/QH14 and the Law on Investment No. 61/2020/QH14. Available Vietnamese legal entity structures include the Joint Stock Company, Limited Liability Company (single-member and multi-member), General Partnership, Limited Partnership, Sole Proprietorship, State-Owned Enterprise, Social Enterprise, Wholly Foreign-Owned Enterprise, Joint Venture Company, Branch Office, Representative Office, and Business Cooperation Contract.

Each structure carries distinct requirements around ownership, liability, capital, and governance. This article examines each entity in detail.

An Overview of Business Structures in Vietnam

Vietnam business structures overview begins with a clear legislative foundation. The Law on Enterprises (Luật Doanh nghiệp), most recently consolidated under Law No. 59/2020/QH14, defines the primary corporate forms available to domestic and foreign investors alike. Each structure carries distinct rules on liability, ownership, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company | Separate legal entity | Limited to shares | Taxable | Permitted | 3 shareholders | Department of Planning & Investment | Law on Enterprises 2020 |

| LLC (Two-Member+) | Separate legal entity | Limited to capital | Taxable | Permitted | 2 members | Department of Planning & Investment | Law on Enterprises 2020 |

| LLC (Single-Member) | Separate legal entity | Limited to capital | Taxable | Permitted | 1 member/owner | Department of Planning & Investment | Law on Enterprises 2020 |

| Wholly Foreign-Owned Enterprise | Separate legal entity | Limited to capital | Taxable | Permitted | 1 foreign investor | Department of Planning & Investment | Law on Investment 2020 |

| Joint Venture Company | Separate legal entity | Limited to capital | Taxable | Permitted | 2+ parties | Department of Planning & Investment | Law on Investment 2020 |

| General Partnership | Separate legal entity | Unlimited (general partners) | Taxable | Permitted | 2 general partners | Department of Planning & Investment | Law on Enterprises 2020 |

| Limited Partnership | Separate legal entity | Mixed | Taxable | Permitted | 2+ partners | Department of Planning & Investment | Law on Enterprises 2020 |

| Branch Office | Not a legal entity | Parent liable | Taxable | Restricted | N/A | Ministry of Industry & Trade | Law on Commerce 2005 |

| Representative Office | Not a legal entity | Parent liable | Exempt (no revenue) | Not permitted | N/A | Ministry of Industry & Trade | Law on Commerce 2005 |

| Business Cooperation Contract | Contractual arrangement | Per contract terms | Taxable | Permitted | 2+ parties | Department of Planning & Investment | Law on Investment 2020 |

| State-Owned Enterprise | Separate legal entity | State-backed | Taxable | Permitted | State as owner | Commission for State Capital | Law on Enterprises 2020 |

| Social Enterprise | Separate legal entity | Limited | Taxable | Permitted | Varies by form | Department of Planning & Investment | Law on Enterprises 2020 |

| Sole Proprietorship | Not a separate legal entity | Unlimited | Taxable | Permitted | 1 individual | Department of Planning & Investment | Law on Enterprises 2020 |

Each of these structures is examined in full in the sections below.

Joint Stock Company (Công ty Cổ phần) Under the Law on Enterprises

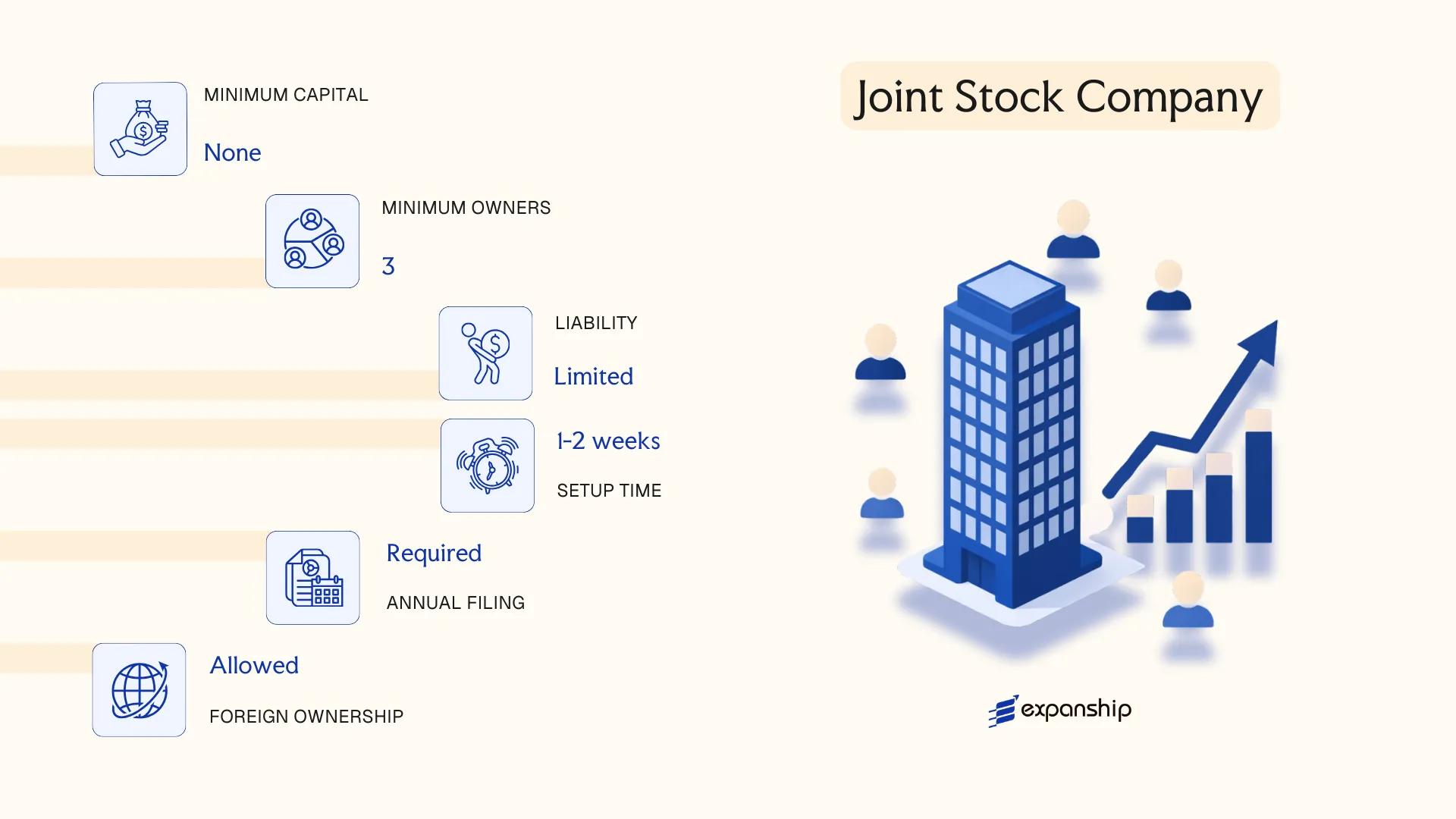

Governed by the Law on Enterprises No. 59/2020/QH14, a Joint Stock Company Vietnam (Công ty Cổ phần) is a separate legal entity distinct from its shareholders, who bear liability only to the extent of their contributed capital. This structure combines corporate flexibility with capital-raising capacity, making it the only Vietnamese business form permitted to issue shares to the public.

Minimum founding requires three shareholders, with no upper limit on total shareholder count. Shares may be freely transferred unless restricted by the company's charter during the initial three years following incorporation, or by agreement among shareholders thereafter.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity (juridical person) | Governed by Law on Enterprises No. 59/2020/QH14 |

| Members | Shareholders; minimum 3, no maximum | Members of the Board of Directors serve as directors; at least 20% of the Board must be independent members in public companies |

| Local Presence | Registered address in Vietnam required | A legal representative (resident in Vietnam) must be designated; no statutory registered agent requirement |

| Capital | No statutory minimum for most sectors; denominated in VND | Regulated industries (banking, insurance, securities) impose sector-specific minimums set by relevant licensing authorities |

| Share Transfer | Freely transferable after initial lock-up period | Founding shareholders restricted from transferring shares for 3 years post-incorporation without shareholder approval |

| Privacy | Shareholder register maintained internally; public companies subject to State Securities Commission disclosure rules | Non-public JSCs have limited public disclosure obligations |

Focus Points

- Taxation: Subject to Corporate Income Tax at the standard rate of 20%; VAT applies to taxable goods and services; withholding tax applies to dividend distributions and cross-border payments to foreign parties; no stamp duty on share transfers, though a 0.1% securities transfer tax applies.

- Annual Compliance: Must hold an Annual General Meeting of Shareholders; file audited financial statements with the Business Registration Authority; large enterprises and public companies are subject to mandatory independent audit requirements.

- Economic Substance: No specific economic substance legislation modelled on offshore regimes; however, tax residency and permanent establishment rules under domestic law and applicable tax treaties are relevant for foreign-controlled structures.

- Treaty Access: As a Vietnamese-resident entity, a JSC is eligible to access Vietnam's network of Double Taxation Agreements, subject to meeting beneficial ownership and anti-abuse conditions.

- Conversion: May be converted to a Limited Liability Company or another enterprise form under procedures set out in the Law on Enterprises, subject to approval by the Business Registration Office.

Closing

A Công ty Cổ phần suits trading operations, large-scale investment projects, and businesses anticipating equity fundraising or eventual public listing; its primary advantage is unrestricted share issuance, while the mandatory three-shareholder minimum and comparatively heavier governance requirements represent practical constraints for smaller operations.

Businesses planning to raise external equity, onboard multiple investors, or pursue a future public offering on the Ho Chi Minh Stock Exchange or Hanoi Stock Exchange.

Company Incorporation in Vietnam

Incorporate a Joint Stock Company or other business entity in Vietnam with end-to-end support from registration through to post-incorporation compliance.

Limited Liability Company (Công ty TNHH) Under the Law on Enterprises

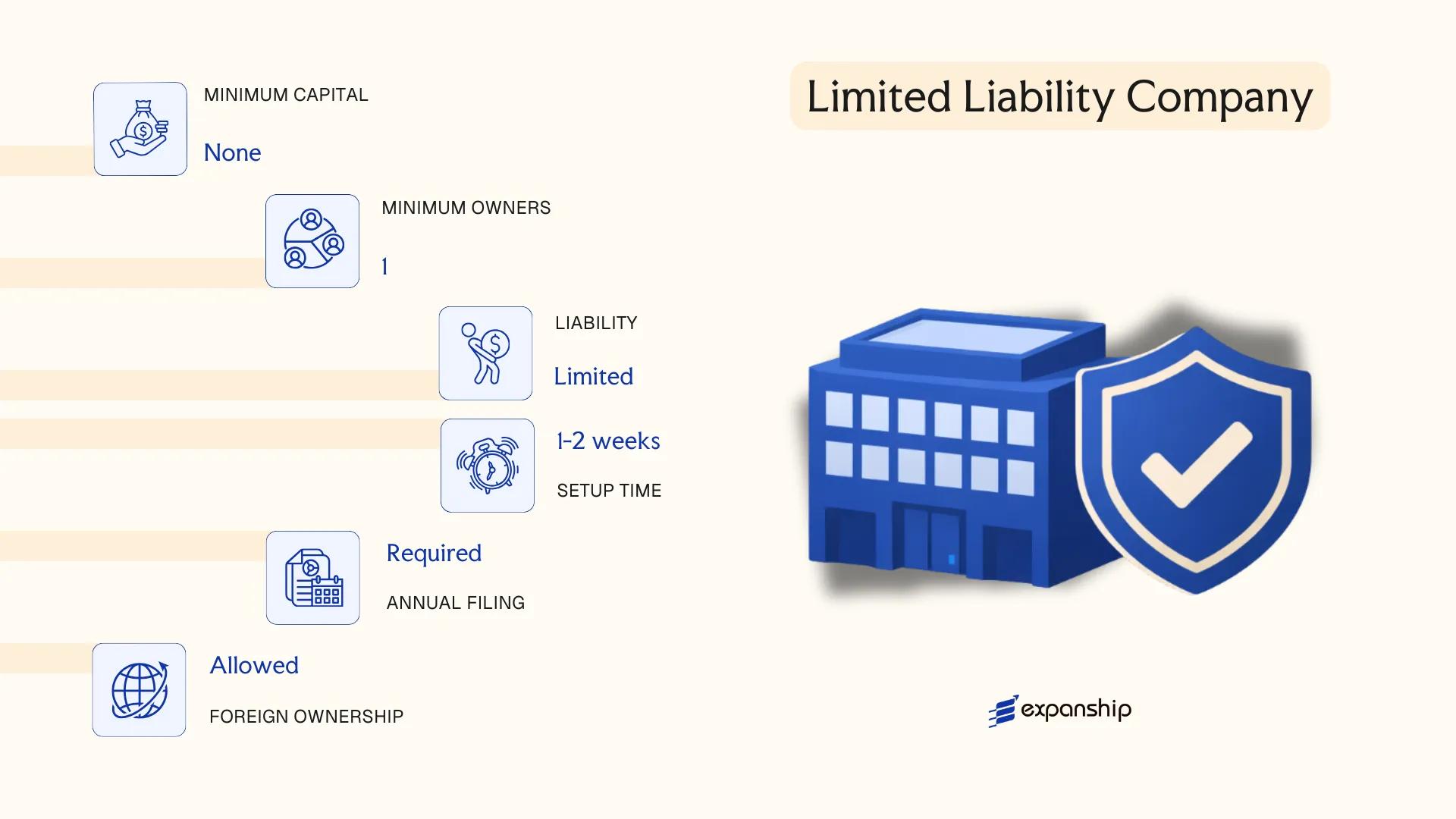

Governed by the Law on Enterprises No. 59/2020/QH14, the Limited Liability Company Vietnam Công ty TNHH is the most widely used business structure for foreign and domestic investors. It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its members, who bear liability only to the extent of their contributed capital.

Structurally, the Công ty TNHH sits between a sole proprietorship and a joint stock company. Capital is divided into contributed portions rather than tradeable shares, and ownership transfer is subject to restrictions, making it a closer structure to a private limited company under common law systems.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Công ty TNHH) | Separate legal personality; not publicly listed |

| Members | 1 (single-member) or 2–50 (multi-member) | Members contribute capital; no shares issued |

| Management | Owner's Council or Members' Council; Director/General Director | Single-member firms may be managed directly by the owner |

| Local Presence | Registered head office address in Vietnam required | No registered agent requirement; a physical or virtual office suffices |

| Capital | Denominated in VND; no statutory minimum for most sectors | Sector-specific minimum capital (charter capital) applies in regulated industries |

| Transfer of Interest | Members' capital transfer restricted; existing members have right of first refusal | Transfer to third parties requires approval per charter and law |

| Privacy | Member details filed with the National Business Registration Portal (NBRP) and publicly accessible | No bearer interests permitted |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 20%; VAT applies to taxable supplies; withholding tax applies to profit remittances, royalties, and service fees paid to foreign parties under the Foreign Contractor Tax regime.

- Annual Compliance: Must file audited financial statements, submit annual tax returns to the General Department of Taxation, and maintain statutory records at the registered office.

- Treaty Access: Eligible for benefits under Vietnam's double tax agreements, subject to meeting beneficial ownership and substance conditions.

- Conversion: Can be converted into a joint stock company or other permitted entity type under Article 202 of the Law on Enterprises, subject to regulatory approval.

- Restrictions: Cannot issue shares or raise public capital; member count capped at 50, limiting scalability for larger investor groups.

Sub-Types

Single-Member LLC (Công ty TNHH Một Thành Viên)

Owned by a single individual or organisation, this variant concentrates control entirely in one owner, who also bears sole responsibility for contributing the full charter capital. It is commonly used by foreign investors establishing a wholly owned operating entity or holding structure.

Two-or-More Member LLC (Công ty TNHH Hai Thành Viên Trở Lên)

This variant accommodates between two and fifty members and requires a Members' Council as the highest governance body. Two member LLC Vietnam requirements include that capital contributions and ownership proportions be documented in the company charter, with profit and loss allocated accordingly.

Closing

The Công ty TNHH suits trading, services, holding, and light manufacturing operations where public fundraising is not required and ownership is intended to remain closely held. The capped membership and restrictions on capital transfer, however, limit this structure for businesses anticipating significant equity expansion or eventual public listing.

The TNHH structure is best suited for foreign investors and domestic entrepreneurs seeking a straightforward, privately held operating or holding entity with defined liability and without the governance overhead of a joint stock company.

Foreign-Invested Entities in Vietnam [Wholly Foreign-Owned Enterprise, Joint Venture Company]

Completing a wholly foreign-owned enterprise Vietnam setup requires registration under the Law on Investment 2020 (Law No. 61/2020/QH14) alongside the Law on Enterprises 2020 (Law No. 59/2020/QH14). These two laws together govern how foreign capital enters and operates within the country. A foreign-invested enterprise (FIE) is defined by the Law on Investment as any entity where foreign investors hold 1% or more of its charter capital.

Both principal FIE structures — the Wholly Foreign-Owned Enterprise (WFOE) and the Joint Venture Company — carry separate legal personality and confer limited liability on their investors. Structurally, either may be established as a limited liability company or a joint stock company under the Law on Enterprises, making the FIE classification an ownership-based designation rather than a standalone legal form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | LLC or JSC (foreign-owned) | FIE is an ownership classification, not a distinct legal form |

| Members | Shareholders or members depending on form | LLC: 1–50 members; JSC: minimum 3 shareholders; no upper cap for JSC |

| Local Presence | Registered office address in Vietnam required | A physical or virtual address in the jurisdiction is mandatory for registration |

| Capital | VND; no statutory minimum for most sectors | Specific sectors (banking, insurance, securities) carry prescribed minimums set by sectoral regulators |

| Licensing | Investment Registration Certificate (IRC) + Enterprise Registration Certificate (ERC) | IRC issued by the Department of Planning and Investment (DPI) or relevant Economic Zone Authority |

| Privacy | Shareholder data filed with state registers | Beneficial ownership disclosures required; registers are not fully public but accessible to authorities |

Focus Points

- Taxation: Corporate income tax at 20% standard rate; VAT at 10% (or 5%/0% for specified goods and services); withholding tax applies to dividends, royalties, and service fees paid to foreign parties at rates of 5%–10% depending on income type.

- Conditional market access: Foreign ownership in restricted sectors is capped under Vietnam's Schedule of Commitments to the WTO and bilateral trade agreements; exceeding these thresholds requires prior approval from the Ministry of Planning and Investment (MPI).

- Annual compliance: Audited financial statements must be filed annually; statutory audit by a licensed Vietnamese audit firm is mandatory for FIEs regardless of size.

- Tax treaty access: Vietnam maintains double taxation agreements (DTAs) with over 80 countries; treaty benefits require a tax residency certificate and satisfaction of beneficial ownership conditions.

- Conversion: An FIE established as an LLC may convert to a JSC through a resolution of its members' council and re-registration with the Business Registration Office, subject to meeting JSC formation thresholds.

Sub-Types

Wholly Foreign-Owned Enterprise (WFOE)

A WFOE holds 100% foreign ownership with no mandatory Vietnamese partner. This structure is used when the target business activity is open to full foreign ownership under Vietnamese law and applicable trade commitments, giving the investor direct operational control without profit-sharing obligations to a local party.

Joint Venture Company

A Joint Venture (JV) involves at least one foreign investor and one Vietnamese party, with ownership proportions agreed contractually and reflected in the charter. JVs are commonly used to access sectors where full foreign ownership is restricted, or where a local partner provides regulatory relationships, market access, or land-use rights that an entirely foreign-owned entity cannot independently obtain.

Closing

Foreign-invested enterprises are most commonly used for manufacturing, technology, trading, and service operations where the investor requires full operational presence rather than a liaison function. Direct ownership of assets and the ability to repatriate profits are clear structural advantages, though sector-specific ownership caps and the dual-registration process through the DPI add regulatory steps absent in domestic entity formation.

Foreign investors seeking operational control and direct market participation in Vietnam, particularly in manufacturing, technology, or services sectors open to full or majority foreign ownership.

Partnerships in Vietnam [General Partnership, Limited Partnership]

Governed by the 2020 Law on Enterprises (Law No. 59/2020/QH14), a partnership company Vietnam general limited structure — known locally as công ty hợp danh — is one of the less commonly used forms of business organisation. Unlike most other entity types under the same legislation, a partnership is required to have at least two general partners who bear unlimited joint liability for the firm's obligations.

A partnership does possess separate legal personality under Vietnamese law, which distinguishes it from a sole proprietorship. This means the entity can enter contracts, hold assets, and sue or be sued in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (Công ty Hợp Danh) | Recognised under the 2020 Law on Enterprises |

| Members | At least 2 general partners; limited partners permitted | General partners bear unlimited personal liability; limited partners are liable only to the extent of their contributed capital |

| Registered Office | Physical address in Vietnam required | Must be a valid, locatable business address |

| Capital | No statutory minimum; denominated in VND | Capital contributions recorded in the partnership charter |

| Privacy | Member details filed with the Business Registration Office | Information is part of the public business registration record |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 20%; VAT applies to taxable supplies; no specific partnership-level withholding tax exemption exists.

- Annual Compliance: Must file annual financial statements and maintain updated records with the Department of Planning and Investment.

- Restrictions: General partners cannot be members of another partnership or operate as a sole proprietor concurrently without consent from the remaining partners.

- Conversion: A partnership may convert to a limited liability company or joint stock company subject to member approval and re-registration procedures.

Sub-Types

General Partnership

All members hold general partner status, carrying unlimited personal liability for the entity's debts. This structure is typically used by professional service providers such as law firms or auditing practices where personal accountability is a regulatory or reputational expectation.

Limited Partnership

Includes both general partners (with unlimited liability) and limited partners (liable only up to their capital contribution). Limited partners cannot participate in management decisions, which restricts their operational role to that of passive investors.

Partnerships suit small professional service firms or ventures where two or more individuals intend to operate under a shared legal identity with defined capital contributions. The separate legal personality offers a degree of structural formality, but the unlimited liability of general partners remains a significant exposure that most foreign investors prefer to avoid.

This structure is most appropriate for Vietnamese professionals in regulated fields, such as law or accounting, where partnership formation aligns with licensing requirements.

Foreign Business Presence in Vietnam [Branch Office, Representative Office, Business Cooperation Contract]

Establishing a foreign company branch office Vietnam does not require incorporating a new legal entity. Under the Law on Enterprises 2020 and sector-specific regulations, foreign firms may operate through a branch office, a representative office, or a business cooperation contract — each serving distinct operational purposes and carrying different levels of commercial authority.

A branch office can conduct direct commercial activities and generate revenue, while a representative office is restricted to liaison, market research, and promotional functions without revenue-generating capacity. A business cooperation contract (BCC) under the Law on Investment 2020 allows a foreign party to cooperate with a Vietnamese partner on a contractual basis, without forming a separate legal entity.

Key Characteristics

| Requirement | Branch Office | Representative Office | BCC |

|---|---|---|---|

| Legal Form | Non-legal entity extension of parent | Non-legal entity liaison office | Contractual arrangement, no separate entity |

| Legal Authority | Can sign contracts, conduct business | Cannot conduct revenue-generating activities | Rights and obligations defined by contract terms |

| Licensing Body | Ministry of Industry and Trade (MOIT) or relevant sector ministry | MOIT or relevant sector ministry | Investment Registration Certificate from provincial DPI |

| Local Presence | Must maintain a physical address in Vietnam | Must maintain a registered office address | No physical office requirement |

| Liability | Parent company bears full liability | Parent company bears full liability | Each party liable per contractual obligations |

| Permitted Duration | Subject to licence renewal (typically 5-year terms) | Subject to licence renewal (typically 5-year terms) | Defined by contract duration |

Focus Points

- Taxation: Branch office profits subject to Corporate Income Tax (CIT) at the standard 20% rate; VAT applies to taxable supplies; withholding tax applies to remittances to the parent; representative offices are generally not CIT-liable as they generate no revenue; BCC income taxed at the applicable rate for each contracting party separately.

- Annual Compliance: Branch offices must file annual financial statements and tax returns; representative offices must renew operating licences and file annual activity reports with the licensing authority.

- Treaty Access: Branch offices and BCCs may access Vietnam's double tax treaties through the parent entity's residency status, subject to treaty provisions and substance requirements.

- Restrictions: Representative offices cannot issue invoices, collect payments, or sign commercial contracts in their own name; certain sectors restrict or prohibit branch office operations entirely.

- Conversion: Neither a branch nor a representative office can be converted directly into a locally incorporated entity — a separate incorporation process is required.

Sub-Types

Branch Office

A licensed branch operates as a dependent unit of the foreign parent, authorised to conduct business activities within the scope defined by its licence. Permitted sectors are regulated — banking, legal services, and certain other industries have separate licensing regimes under their own sector laws.

Representative Office

This structure is used solely for non-commercial purposes such as market research, supplier liaison, and promoting the parent company's products or services. It cannot enter into contracts for commercial gain or act as an importer of record.

Business Cooperation Contract (BCC)

A BCC allows a foreign investor to collaborate with a Vietnamese counterpart by sharing revenues or products rather than forming a joint entity. It is commonly used in sectors such as telecommunications and oil and gas, where equity joint ventures face regulatory restrictions.

A branch office suits firms requiring direct commercial activity without committing to full local incorporation, though the parent's unlimited liability exposure is a material consideration. A representative office is appropriate for preliminary market-entry activities only, and a BCC works where contractual revenue-sharing is operationally sufficient.

Foreign firms testing the Vietnamese market or operating under sector-specific restrictions that limit equity-based structures.

State-Owned Enterprise (Doanh nghiệp Nhà nước)

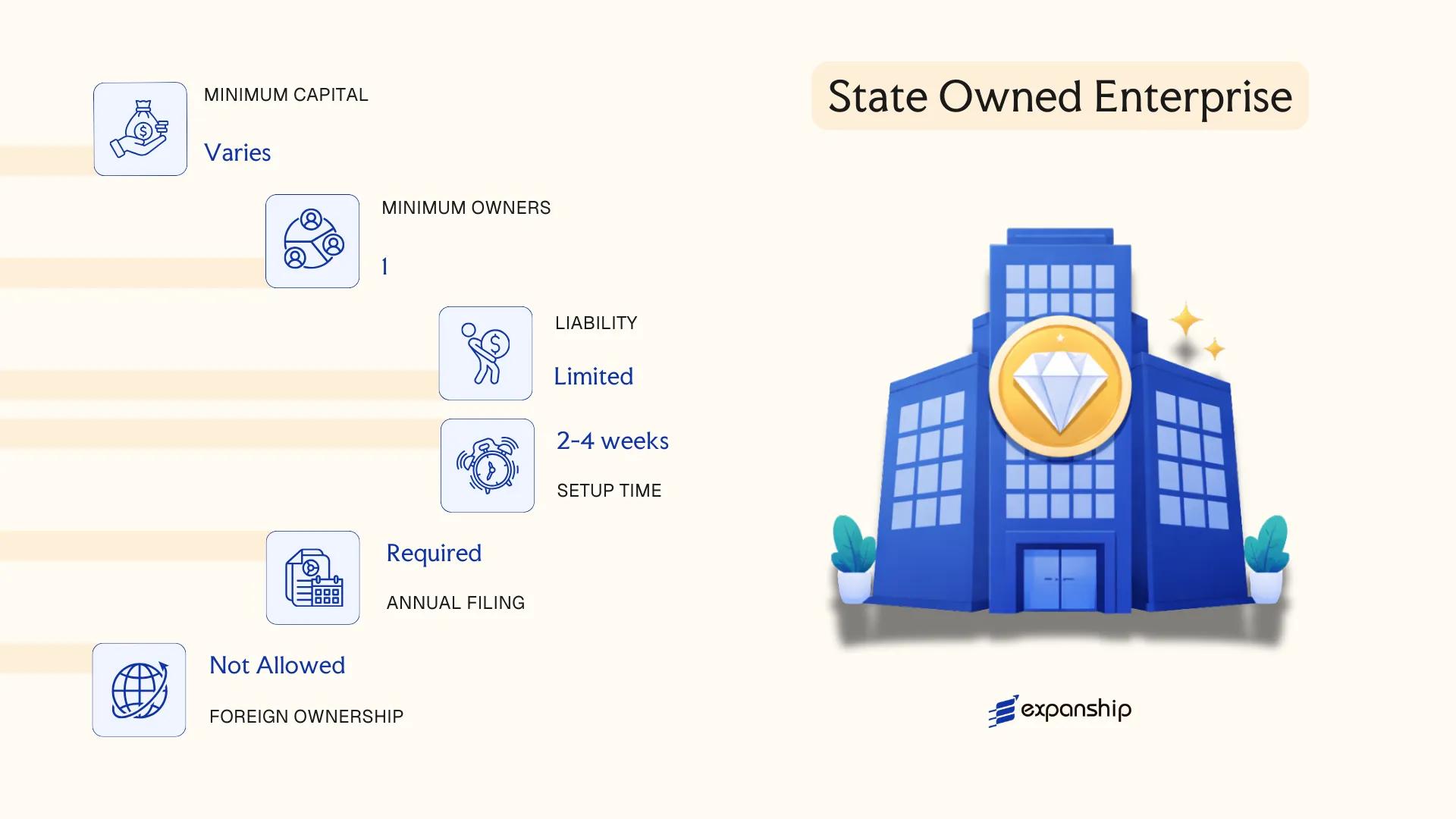

A state-owned enterprise Vietnam (Doanh nghiep Nha nuoc) is governed primarily by the Law on Enterprises No. 59/2020/QH14, which defines this entity as any enterprise in which the state holds more than 50% of charter capital or total voting shares. Supplementary regulations under Decree No. 47/2021/ND-CP further specify governance obligations and internal management structures.

These entities carry separate legal personality and limited liability relative to state capital contributions, though their hybrid nature means commercial operations remain subject to direct state ownership influence and public policy mandates.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | State-Owned Enterprise (Doanh nghiep Nha nuoc) | Operates as a JSC or LLC in which the state holds >50% capital |

| Members | State as majority shareholder or capital contributor | The state exercises rights through authorised representative agencies |

| Local Presence | Registered office required within Vietnam | Must maintain a physical headquarters; representative bodies common in multiple provinces |

| Charter Capital | No universal statutory minimum; sector-specific thresholds apply | State capital is tracked separately under Decree 47/2021 |

| Governance | Board of Members or Board of Directors plus a General Director | Supervisory Board mandatory for enterprises wholly owned by the state |

| Privacy | Ownership and financials subject to public disclosure | Annual financial reports filed with the Ministry of Finance and relevant line ministry |

Focus Points

- Taxation: Subject to standard Corporate Income Tax at 20%; VAT applies to taxable supplies; withholding tax obligations mirror those of private enterprises; state dividends remitted to the state budget rather than private shareholders.

- Profit distribution: Retained earnings and dividend allocation are regulated under Law on Management and Use of State Capital No. 69/2014/QH13.

- Annual compliance: Mandatory audited financial statements, performance reports to the owner representative agency, and disclosure filings with the Ministry of Finance.

- Restrictions: Certain sectors restrict or prohibit private or foreign participation, reserving activity exclusively for state-owned entities; conversion to private ownership requires government approval.

- Equitisation: The state may reduce its stake through an equitisation process (co phan hoa), converting the enterprise into a joint-stock company with partial private or foreign shareholding.

Sub-Types

Wholly State-Owned Enterprise (100% State Capital)

The state holds the entire charter capital, and no private shareholders participate. These entities operate in strategic sectors such as national defence, electricity transmission, and postal services where market liberalisation is restricted by law.

Majority State-Owned Enterprise (50%–99% State Capital)

The state retains a controlling stake while private or foreign investors hold minority positions. This structure is common in post-equitisation entities or mixed-capital enterprises operating in competitive commercial sectors.

State-owned enterprises are the primary vehicle for government participation in strategic industries, infrastructure, and public utilities, with the key structural advantage being direct access to state capital and policy support. The primary limitation is constrained operational autonomy, as major decisions require approval from owner representative agencies such as the Committee for Management of State Capital at Enterprises (CMSC).

This structure is suited to government bodies or state agencies seeking a regulated commercial vehicle to operate in strategically controlled or public-interest sectors.

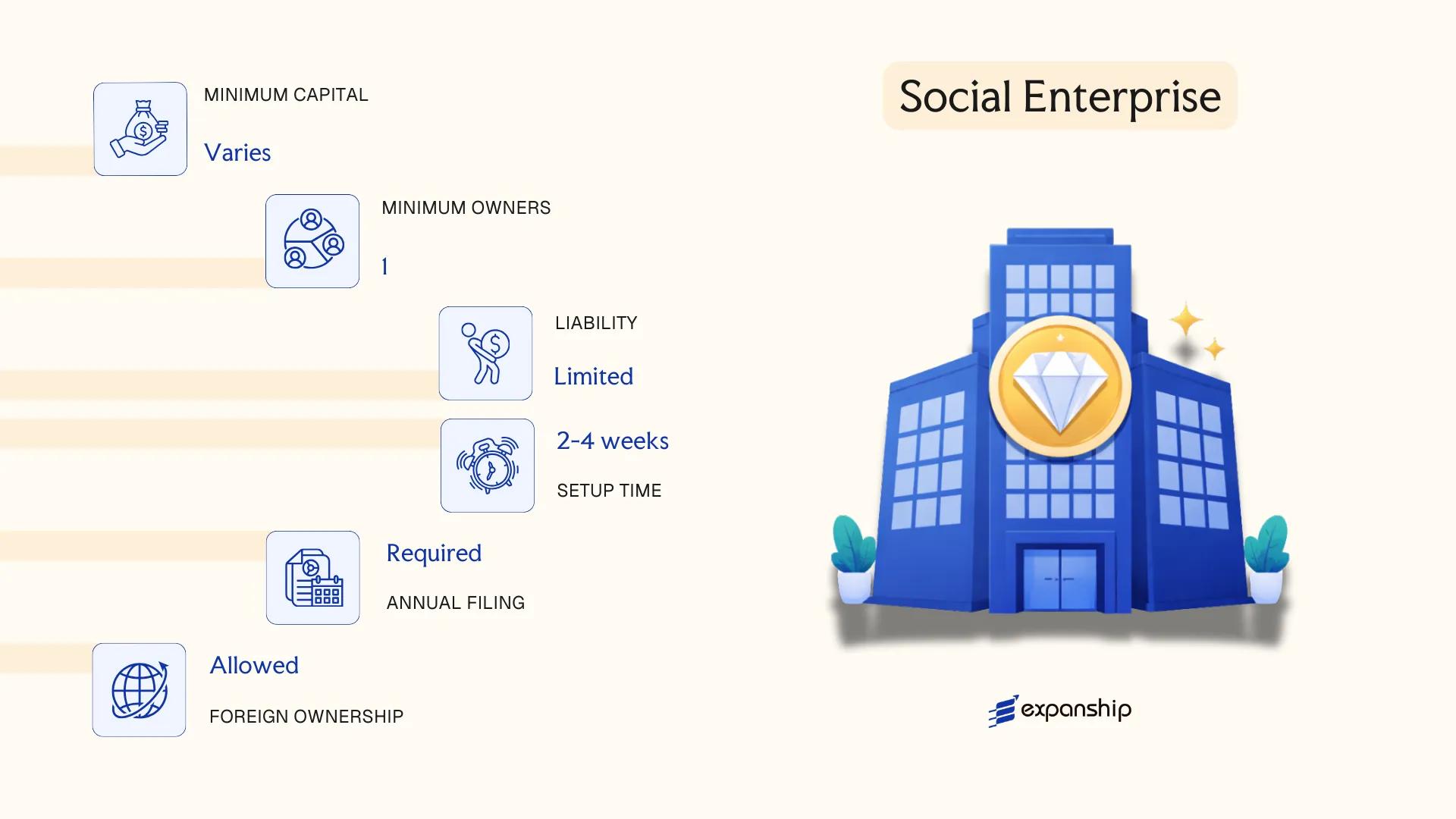

Social Enterprise (Doanh nghiệp Xã hội)

A social enterprise Vietnam (Doanh nghiep Xa hoi) framework is established under the Law on Enterprises No. 59/2020/QH14, which came into effect on 1 January 2021. This form of business carries separate legal personality and limited liability, but operates under a hybrid mandate: it must pursue profit while committing at least 51% of annual after-tax profit to reinvestment in its stated social or environmental objectives.

Structurally, a social enterprise can be established as a limited liability company, joint stock company, or partnership — meaning it does not constitute an entirely distinct corporate form but rather a designation layered onto an existing legal structure registered with the Department of Planning and Investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Overlaid on LLC, JSC, or Partnership | Not a standalone entity class; base structure governs governance rules |

| Members / Shareholders | Directors, members, or shareholders depending on base structure | Minimums and maximums follow the underlying entity type chosen |

| Local Presence | Registered office address required in Vietnam | Must maintain a physical registered address |

| Capital | VND; no statutory minimum specific to social enterprises | Minimum capital rules of the chosen base entity type apply |

| Profit Commitment | Minimum 51% of after-tax profit reinvested | Documented annually; deviation triggers loss of designation |

Focus Points

- Taxation: Subject to standard Corporate Income Tax at 20%; VAT obligations, withholding tax, and other levies follow the underlying entity type with no blanket exemptions granted solely by virtue of the social enterprise designation.

- Annual Compliance: Must submit annual financial statements and a report demonstrating fulfilment of the 51% profit reinvestment commitment to the business registration authority.

- Restrictions: Prohibited from using assets or profits for purposes other than the registered social or environmental mission during the designation period; cannot distribute surplus profit to owners in excess of the permitted threshold.

- Conversion: The social enterprise designation can be renounced, but the enterprise must notify the Department of Planning and Investment and settle any obligations tied to preferential treatment received.

- Incentives: May be eligible for state support mechanisms including preferential access to certain public procurement and grant programmes, though these are not automatic and depend on sector-specific regulations.

Closing

This structure suits organisations seeking a commercially sustainable vehicle to address social or environmental objectives while retaining formal business status. The primary advantage is access to state support channels unavailable to purely commercial firms; the key limitation is the legally binding profit reinvestment obligation, which restricts owner distributions and requires ongoing documentary proof.

Best suited for founders or organisations whose core mission is social or environmental impact and who can demonstrate a commercially viable revenue model to sustain the mandatory reinvestment commitment.

Sole Proprietorship (Doanh nghiệp Tư nhân)

A sole proprietorship Vietnam — Doanh nghiep Tu nhan — is governed by the Law on Enterprises 2020 (Law No. 59/2020/QH14). Unlike a limited liability company or joint stock company, this structure does not confer separate legal personality; the business and its owner are treated as a single legal entity.

Ownership is restricted to one individual, who bears unlimited personal liability for all obligations of the business. This means the proprietor's personal assets are fully exposed to business debts, with no protective boundary between personal and commercial finances.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole entity | No separate legal personality; owner and business are legally inseparable |

| Members | Single individual proprietor only | No shareholders or co-owners permitted; one proprietor maximum |

| Local Presence | Registered office address in Vietnam required | Must maintain a principal place of business within the jurisdiction |

| Capital | No statutory minimum; owner declares contributed capital | Declared capital sets the ceiling for the proprietor's personal financial liability disclosure |

| Liability | Unlimited personal liability | All personal assets of the proprietor are exposed to business debts |

| Privacy | Proprietor's name and declared capital are publicly registered | Information is recorded with the Business Registration Authority under the Department of Planning and Investment |

Focus Points

- Taxation: Subject to personal income tax on business profits rather than corporate income tax; VAT registration applies where turnover thresholds are met under the Law on Value Added Tax.

- Annual Compliance: Must submit annual financial disclosures and declared capital figures to the Business Registration Office; accounting records are maintained under Vietnamese Accounting Standards.

- Conversion: May be converted into a limited liability company or joint stock company under Article 205 of the Law on Enterprises 2020, subject to registration requirements.

- Restrictions: Cannot issue shares or bonds; prohibited from contributing capital to or acquiring stakes in partnerships or other companies.

- Treaty Access: As an unincorporated entity without separate legal personality, access to Vietnam's double tax treaty network is limited compared to incorporated structures.

Closing

This structure suits micro-scale or informal trading operations where simplicity of registration is prioritised over liability protection. The absence of a minimum capital requirement lowers the barrier to entry, but unlimited personal liability makes it unsuitable for businesses carrying significant financial risk.

Individual traders or sole operators running low-risk, small-scale businesses who require minimal regulatory complexity and do not anticipate external investment or significant commercial liabilities.

How to Choose the Right Entity Type in Vietnam

Selecting how to choose a business structure in Vietnam is not a purely administrative decision — the entity type you register determines your tax exposure, your liability, and what activities you are legally permitted to conduct.

Why Your Entity Choice Matters

The structure you form shapes every compliance obligation that follows. Getting it wrong has concrete consequences:

- A representative office cannot sign commercial contracts or generate revenue; using one to conduct active trading violates the Law on Enterprises and the Investment Law, and can result in forced closure or administrative penalties.

- A foreign-invested entity operating in a conditional business sector without the correct Investment Registration Certificate (IRC) triggers suspension of operations under Decree 31/2021/ND-CP.

- Selecting a structure without legal entity status — such as a Business Cooperation Contract — means you cannot own assets, open a bank account in the entity's name, or independently enforce contracts.

- Registering as a Single-Member LLC when your business later requires equity investment from multiple parties forces a full conversion process under the Law on Enterprises, incurring additional regulatory filings and timeline delays.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct entity structures under Vietnamese law.

- Ownership Structure: A single foreign investor points toward a Wholly Foreign-Owned Enterprise, while multi-party arrangements require a Joint Venture or Joint Stock Company.

- Sector Restrictions: Vietnam's market access commitments under the WTO and bilateral trade agreements cap foreign ownership percentages in specific industries, which narrows your structural options before other factors apply.

- Tax Position: Your eligibility for corporate income tax incentives under the Law on Tax Administration depends partly on entity classification and the location of your registered business.

- Substance Capacity: If you cannot maintain a physical office and staff in-country, structures requiring demonstrable operational presence will expose you to compliance failures.

- Exit Flexibility: Dissolution, conversion between entity types, or equity transfer procedures differ significantly across structures, and the Law on Enterprises sets distinct timelines and approval requirements for each.

The full text of the Law on Enterprises 2020 (Law No. 59/2020/QH14) is available on the official Vietnamese Government Portal.

Corporate Compliance Services in Vietnam

Ongoing compliance support for foreign-invested entities and locally registered companies operating under Vietnamese law.

Conclusion

Vietnam's enterprise law framework, governed primarily by the Law on Enterprises 2020 and the Law on Investment 2020, defines a range of structures suited to different ownership profiles and commercial objectives. As a Vietnam company formation summary guide, this overview has addressed each entity type on its own terms.

The Joint Stock Company suits businesses planning to raise capital from multiple shareholders or pursue a future public listing. A single-member LLC fits sole foreign investors seeking straightforward ownership and limited liability. The two-member or more LLC serves small-to-medium partnerships without the governance overhead of a JSC. Among foreign-invested entities, the wholly foreign-owned enterprise remains the most registered structure for inbound investment. Joint ventures apply where local partnership is strategically or legally required. Representative offices and branch offices serve foreign firms testing the market or executing limited commercial activities without full incorporation.

Regulatory reforms and continued expansion of Vietnam's bilateral investment treaty network suggest a trajectory toward greater foreign investment accessibility in the medium term. Expanship's team operates directly within this framework.

How Expanship Can Assist You

Expanship provides corporate services Vietnam company incorporation clients need across the full setup process — from selecting the right entity under the 2020 Law on Enterprises to registering with the Department of Planning and Investment (DPI) or the relevant provincial authority. The entity types covered in this blog each carry distinct registration requirements, capital rules, and ongoing compliance obligations that your business will need to meet from day one.

Our Vietnam incorporation service covers the end-to-end process:

- Document preparation, notarization, and legalization

- Registered address and local registered agent provision

- DPI filings and business registration certificate management

- Post-incorporation compliance, including annual reporting and license renewals

- Corporate bank account introduction support

Expanship's team works directly with the relevant Vietnamese authorities on your behalf, reducing back-and-forth and keeping your timeline on track.

Ready to move forward? Contact Expanship Vietnam to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Limited Liability Company (Công ty TNHH) is the most frequently established entity, primarily because it combines capped liability with a relatively straightforward compliance structure. Both single-member and two-or-more-member variants are available, making it accessible to a wide range of ownership configurations.

A Wholly Foreign-Owned Enterprise (WFOE) is not a separate legal category under the Law on Enterprises 2020 — it refers to an LLC or Joint Stock Company structured with 100% foreign ownership. The distinction that matters operationally is the Investment Registration Certificate (IRC) requirement for foreign-owned firms, which adds a layer of regulatory approval absent for domestically owned entities. Both structures are subject to the standard 20% corporate income tax rate, but foreign-owned entities may face additional sector-specific licensing obligations.

No Vietnamese enterprise type provides strong confidentiality by default, as the National Business Registration Portal publicly discloses ownership and management information. The use of nominee directors or shareholders is not formally regulated and carries legal risk under Vietnamese law. A Single-Member LLC technically minimises the number of disclosed individuals, but this does not constitute meaningful privacy protection.

A Single-Member LLC requires only one owner, and a Joint Stock Company requires a minimum of three shareholders. General Partnerships require at least two general partners, while a Sole Proprietorship is by definition owned by one individual but carries unlimited personal liability. Not all structures are available to a single founder, and the JSC minimum shareholder threshold is a common constraint.

Foreigners may establish a wholly foreign-owned LLC or Joint Stock Company after obtaining an IRC from the provincial Department of Planning and Investment. Participation in a Joint Venture Company is also available, provided the applicable sector does not impose foreign ownership caps under Vietnam's WTO commitments or the Law on Investment 2020. Sole Proprietorships and General Partnerships are generally restricted to Vietnamese individuals or carry conditions that make them impractical for most foreign investors.

The Law on Enterprises 2020 explicitly permits conversion between certain entity types, including from a Single-Member LLC to a Multi-Member LLC, from an LLC to a Joint Stock Company, and from a JSC back to an LLC. The conversion requires updating the Enterprise Registration Certificate through the Business Registration Office. Not all conversions are available in both directions, and foreign-owned entities must also update their IRC when ownership structure changes.

LLCs, Joint Stock Companies, and Limited Partnerships possess separate legal personality under the Law on Enterprises 2020, meaning they can own assets, enter contracts, and bear liabilities independently. A Sole Proprietorship does not have legal personality separate from its owner, which exposes the individual to unlimited liability. Representative Offices and Business Cooperation Contracts also lack independent legal personality, as they operate as extensions of or arrangements between existing legal entities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.