Key Takeaways

- The USVI Division of Corporations and Trademarks, operating under the Office of the Lieutenant Governor, serves as the central registry for all entity formations and ongoing compliance filings in the territory.

- Corporations accessing the USVI Economic Development Commission program can qualify for significant territorial tax reductions under the territory's mirror tax system administered by the USVI Bureau of Internal Revenue.

- The LLC is the most commonly registered entity type in the U.S. Virgin Islands, valued for its flexible member agreements and pass-through tax treatment.

- Sole proprietorships carry no formal registration requirement under USVI law but expose the owner to unlimited personal liability.

Introduction to Entity Types in U.S. Virgin Islands (VI)

Located in the northeastern Caribbean Sea, the U.S. Virgin Islands is an unincorporated territory of the United States, situated approximately 40 miles east of Puerto Rico. As a U.S. territory, it operates under a hybrid legal framework that draws from federal U.S. law while maintaining its own territorial statutes governing commerce and corporate affairs.

Company registration falls under the jurisdiction of the USVI Division of Corporations and Trademarks, which operates within the Office of the Lieutenant Governor. This body processes entity formations, maintains the business registry, and oversees ongoing compliance filings for entities organized under territorial law.

The tax posture is a defining feature for businesses registered here. The territory administers its own mirror tax system under the USVI Bureau of Internal Revenue, and qualifying companies may access significant reductions through the Economic Development Commission program.

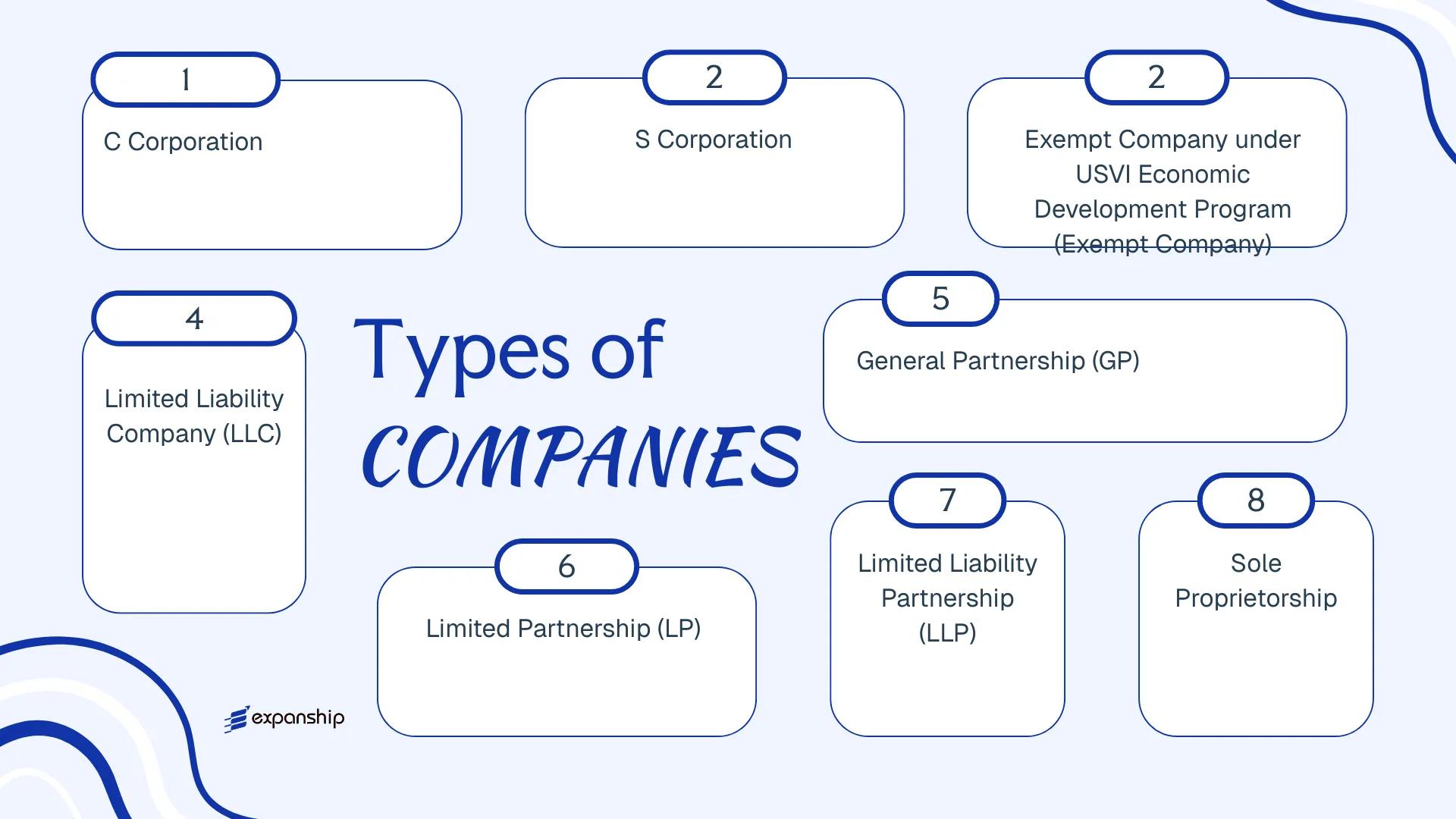

Businesses forming in the territory may choose from the following entity types:

- Corporation (including C Corporation, S Corporation, and Exempt Company under the USVI Economic Development Program)

- Limited Liability Company (LLC)

- General Partnership

- Limited Partnership

- Limited Liability Partnership (LLP)

- Foreign Business Entity (Foreign Corporation, Foreign LLC, Foreign Partnership)

- Sole Proprietorship

Each structure carries distinct implications for ownership, liability, taxation, and compliance — all of which are examined in the sections that follow.

An Overview of Business Structures in U.S. Virgin Islands (VI)

The overview of business structures USVI founders and foreign investors need begins with the Virgin Islands Code, Title 13, which serves as the primary legislative framework governing company formation and registration in the territory. Several distinct entity types are available, each designed to serve a different commercial purpose, ownership structure, or liability profile.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| C Corporation | Separate legal entity | Limited to investment | Taxable (federal/USVI rates) | Permitted | 1 shareholder | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| S Corporation | Separate legal entity | Limited to investment | Pass-through (federal rules apply) | Permitted | 1–100 shareholders | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| Exempt Company (EDP) | Separate legal entity | Limited to investment | EDC tax benefits apply | Restricted | 1 shareholder | USVI Economic Development Authority | Title 29, VI Code |

| LLC | Hybrid entity | Limited to contribution | Pass-through default | Permitted | 1 member | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| General Partnership | Unincorporated association | Unlimited personal | Pass-through | Permitted | 2 partners | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| Limited Partnership | Hybrid structure | Mixed (general/limited) | Pass-through | Permitted | 1 GP, 1 LP | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| LLP | Registered partnership | Limited for partners | Pass-through | Permitted | 2 partners | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| Sole Proprietorship | Unincorporated individual | Unlimited personal | Personal income tax | Permitted | 1 individual | Department of Licensing and Consumer Affairs | General business law |

| Foreign Corporation | Registered foreign entity | Limited to investment | Subject to home jurisdiction | Permitted (registered) | Per home jurisdiction | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| Foreign LLC | Registered foreign entity | Limited to contribution | Subject to home jurisdiction | Permitted (registered) | Per home jurisdiction | USVI Division of Corporations and Trademarks | Title 13, VI Code |

| Foreign Partnership | Registered foreign entity | Per partnership type | Subject to home jurisdiction | Permitted (registered) | Per home jurisdiction | USVI Division of Corporations and Trademarks | Title 13, VI Code |

Each of these structures is examined in full in the sections below.

Corporation (C Corporation, S Corporation, Exempt Company under USVI Economic Development Program)

Corporations in the U.S. Virgin Islands are governed primarily by the Virgin Islands Business Corporation Act (Title 13, V.I. Code), which establishes the legal framework for formation, governance, and dissolution. USVI corporation formation — whether C Corp or S Corp — creates a separate legal entity, meaning shareholders bear no personal liability for corporate debts beyond their capital contribution.

Registered with the USVI Division of Corporations and Trademarks, a corporation requires Articles of Incorporation and must maintain a registered agent with a physical address in the territory.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (stock-based entity) | Separate legal personality; limited liability for shareholders |

| Members | Shareholders (owners), Directors (governance), Officers (management) | No maximum on shareholders; minimum 1 director |

| Local Presence | Registered Agent + Registered Office in USVI | Registered agent must have a physical USVI address |

| Capital | USD; no statutory minimum paid-up capital | Authorized share capital stated in Articles of Incorporation |

| Privacy | Officer and director names filed publicly | Beneficial ownership not on public record by default |

Focus Points

- Taxation: USVI corporations are subject to a mirrored federal tax system — federal tax rules apply locally; the statutory corporate rate mirrors U.S. federal rates, though EDA-qualified companies may receive significant reductions; no separate USVI VAT applies, but gross receipts tax applies to local business activity.

- Annual Compliance: Annual report filing and franchise tax payment required to the Division of Corporations and Trademarks; failure to file results in administrative dissolution.

- Economic Substance: EDA-exempt companies must demonstrate genuine operational presence, including physical office space, qualified employees, and minimum investment thresholds, to maintain their benefits.

- Treaty Access: As a U.S. territory, the USVI does not independently access U.S. tax treaties; treaty benefits depend on the entity's U.S. tax classification and residency determination.

- Conversion: A USVI corporation may convert to an LLC under Title 13 provisions, subject to creditor protection requirements.

Sub-Types

C Corporation

A standard USVI corporation taxed under the mirrored federal system, with corporate-level tax on profits and potential dividend taxation at the shareholder level. Commonly used for operating businesses, holding structures, and entities seeking EDA benefits.

S Corporation

An S Corp election under IRC Subchapter S allows pass-through taxation, eliminating corporate-level tax — profits and losses flow directly to shareholders' personal returns. Eligibility requires no more than 100 shareholders, all of whom must be U.S. citizens or resident aliens, and only one class of stock is permitted.

Exempt Company under USVI Economic Development Program

Businesses approved by the USVI Economic Development Authority (EDA) under the Economic Development Commission (EDC) program may qualify for a 90% reduction in corporate income tax, a 90% reduction in personal income tax on business income, and exemptions from certain gross receipts and excise taxes. Qualification requires a minimum capital investment, local employment, and maintaining genuine operations within the territory for the duration of the benefit period (typically 10–30 years).

Closing

Corporations suit trading operations, IP holding structures, and businesses targeting EDA incentives, though the compliance burden — particularly for EDA-exempt companies maintaining economic substance — is meaningfully higher than for simpler entity forms.

USVI corporations are most appropriate for U.S.-connected businesses seeking territorial tax advantages through EDA qualification while retaining a familiar corporate governance structure.

Company Incorporation in U.S. Virgin Islands

Register a corporation in the USVI through the Division of Corporations and Trademarks with full compliance support.

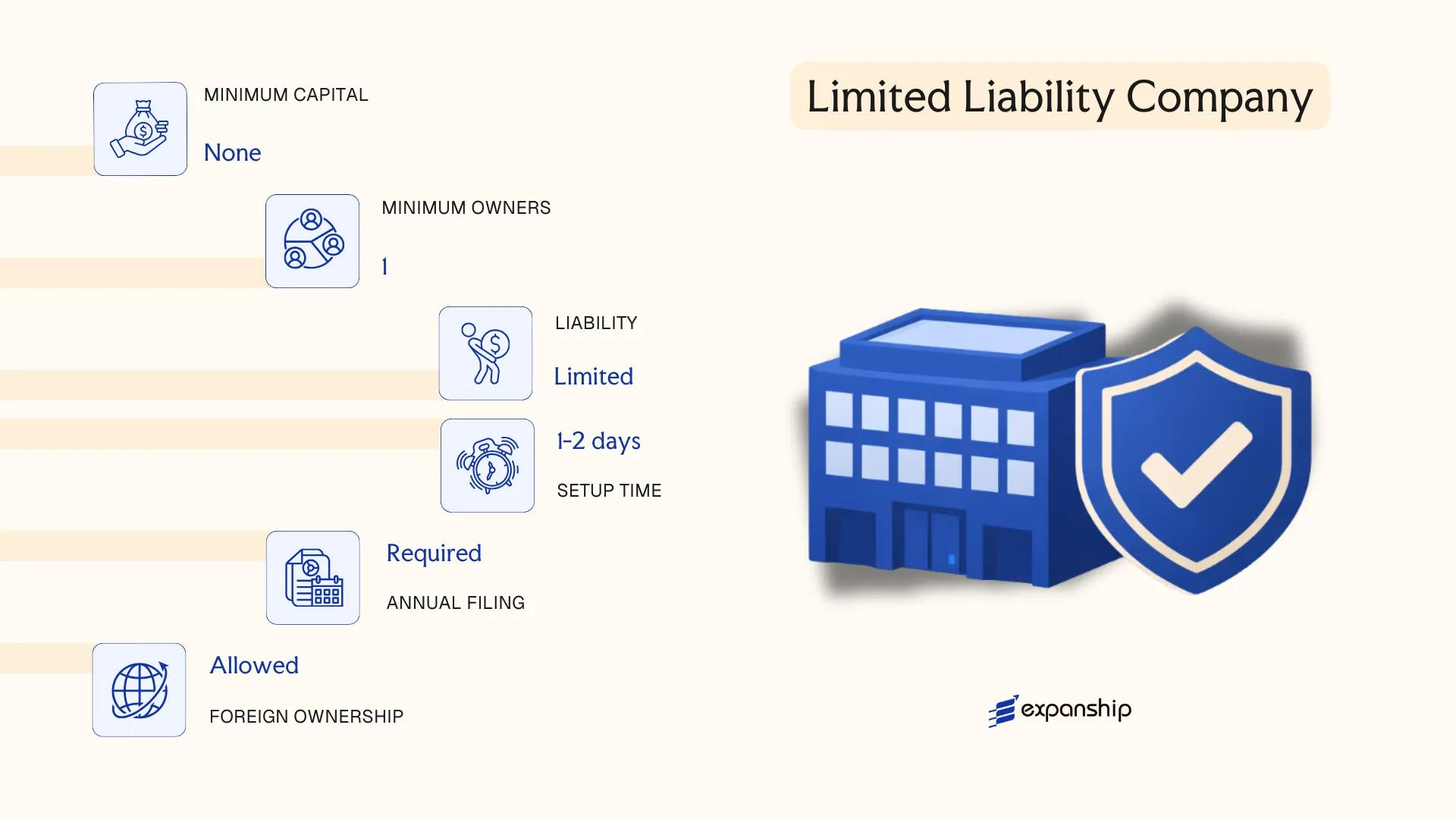

Limited Liability Company (LLC)

US Virgin Islands LLC formation is governed by the Virgin Islands Limited Liability Company Act (Title 13, Chapter 11 of the Virgin Islands Code). An LLC is a separate legal entity, meaning it can own property, enter contracts, and incur liabilities in its own name. Members' personal liability is confined to their capital contribution, and the structure functions as a hybrid between a corporation and a partnership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; governed by Title 13, Chapter 11 |

| Members | Referred to as Members | Minimum 1; no maximum; may be individuals or legal entities of any nationality |

| Management | Member-managed or Manager-managed | Managers need not be members; structure is defined in the operating agreement |

| Local Presence | Registered Agent required | Agent must maintain a physical address in the territory |

| Capital | USD; no statutory minimum | Contributions may be cash, property, or services |

| Privacy | Members not publicly disclosed | Operating agreement and membership details are not filed with the Division of Corporations and Trademarks |

Focus Points

- Taxation: LLCs are pass-through entities by default; members report income on personal returns under the USVI mirror tax system, which largely mirrors the U.S. Internal Revenue Code, though USVI-sourced income may qualify for reduced rates under the Economic Development Program.

- Operating Agreement: No statutory requirement to file the operating agreement publicly, but USVI LLC operating agreement requirements mandate that one exists in writing to govern member rights, profit allocation, and management authority.

- Annual Compliance: Annual report filing and franchise fee payment are required with the Division of Corporations and Trademarks; failure to file can result in administrative dissolution.

- Economic Substance: LLCs engaged in certain activities may be subject to economic substance requirements aligned with U.S. federal reporting obligations.

- Conversion: An existing corporation or partnership may convert into an LLC under the Virgin Islands Code, subject to filing a certificate of conversion.

Forming an LLC in US Virgin Islands suits businesses seeking operational flexibility without the formality of a corporation, particularly for holding structures, real estate ownership, or joint ventures. The pass-through default avoids entity-level taxation, though members who are U.S. persons remain subject to federal tax obligations regardless of USVI residency.

USVI LLCs are well-suited for U.S.-connected investors seeking territorial tax benefits through the Economic Development Program while maintaining a flexible, lightly governed ownership structure.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership (LLP)]

Partnership structures in the U.S. Virgin Islands are governed by the Uniform Partnership Act and related statutes adopted under USVI law, which distinguish between general partnerships, limited partnerships, and limited liability partnerships. Each form carries different liability profiles and operational requirements.

USVI limited partnership registration requires filing a Certificate of Limited Partnership with the USVI Division of Corporations and Trademarks. General partnerships, by contrast, can form by agreement without mandatory registration, though filing is advisable for record purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual business association | LP and LLP have separate legal status upon registration; GP does not require filing |

| Members Referred To As | Partners (General Partners / Limited Partners) | GP: all partners bear joint liability; LP: at least one GP and one LP required |

| Membership | Minimum 2 partners; no statutory maximum | LLP requires at least 2 partners |

| Local Presence | Registered Agent with a USVI address required for LP and LLP | GP has no mandatory registered agent requirement |

| Capital | No minimum capital requirement; USD denomination | Contributions defined by partnership agreement |

| Privacy | Partner names disclosed in formation filings for LP and LLP | GP agreements are private if unregistered |

Focus Points

- Taxation: Partnerships are generally pass-through entities for USVI income tax purposes; partners report income individually under the USVI mirrored Internal Revenue Code, with no entity-level income tax, capital gains tax, or VAT.

- Annual Compliance: Registered LPs and LLPs must maintain a registered agent and file periodic reports with the Division of Corporations and Trademarks; GPs have minimal statutory compliance obligations.

- Economic Substance: Partnership structures engaged in relevant activities may be subject to USVI economic substance requirements depending on the nature of operations.

- Conversion: USVI statutes generally permit conversion of a partnership to an LLC or corporation through a formal conversion filing.

- Treaty Access: The USVI is a U.S. territory, not an independent treaty jurisdiction; access to U.S. tax treaties depends on the partners' individual residency status.

Sub-Types

General Partnership (GP)

A GP arises automatically when two or more persons carry on business for profit without forming a separate legal entity. All partners bear unlimited joint and several liability for partnership obligations.

Limited Partnership (LP)

An LP separates management from passive investment: general partners manage and bear unlimited liability, while limited partners contribute capital and have liability capped at their investment. This structure suits investment vehicles and real estate holding arrangements.

Limited Liability Partnership (LLP)

The USVI LLP shields partners from personal liability arising from the wrongful acts of other partners, while still requiring registration with the Division of Corporations and Trademarks. It is commonly used by professional service firms.

Closing

Partnership structures suit joint ventures, professional practices, and investment holding arrangements where pass-through taxation is preferred. The key advantage is fiscal transparency; the primary limitation is that general partners in a GP or LP retain unlimited personal liability.

USVI partnerships are best suited for professional firms, co-investors, and joint venture parties seeking pass-through tax treatment with clearly defined capital contribution arrangements.

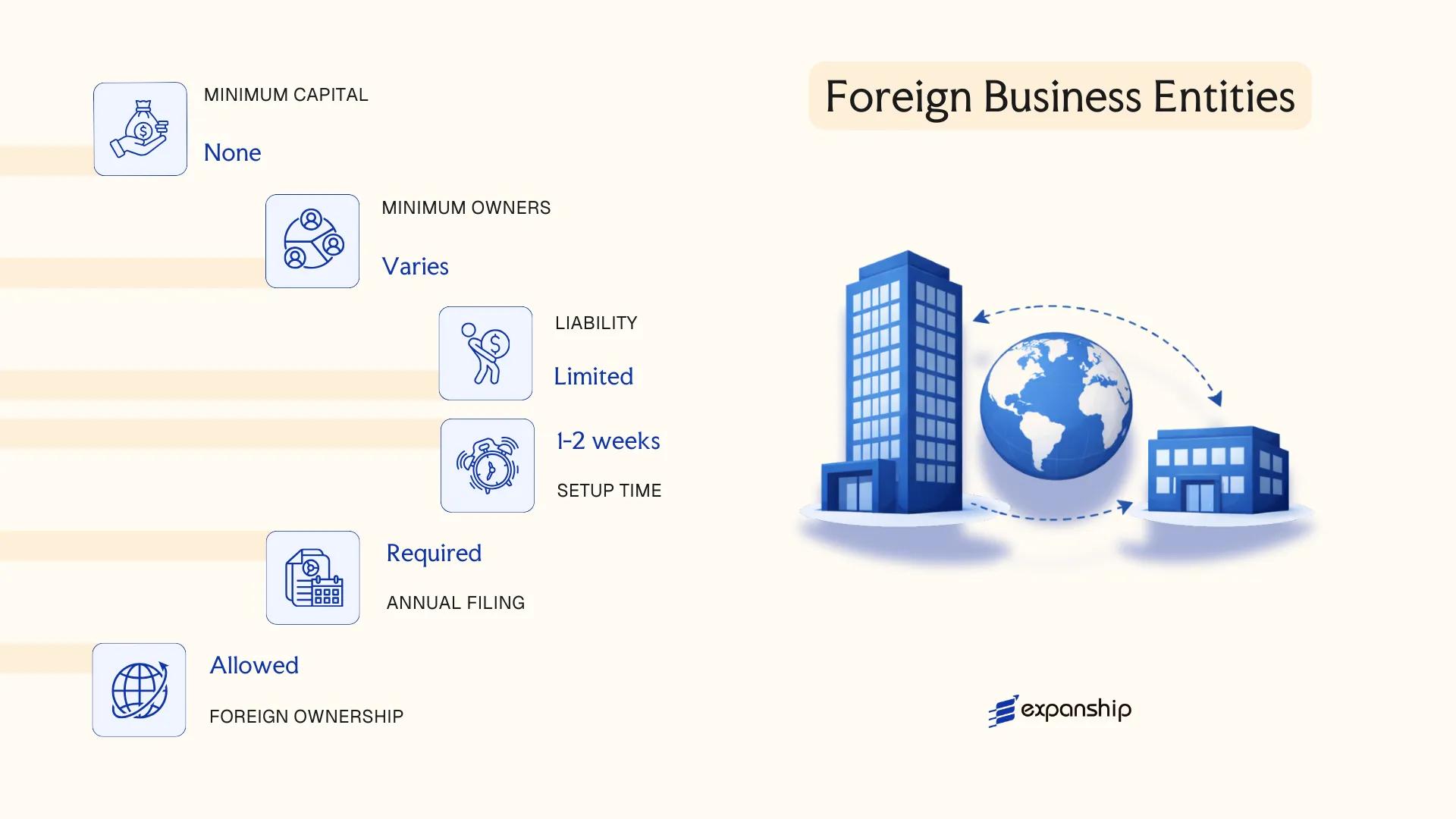

Foreign Business Entities [Foreign Corporation, Foreign LLC, Foreign Partnership, Registered Foreign Entity under USVI Division of Corporations and Trademarks]

Foreign corporations, LLCs, and partnerships formed outside the U.S. Virgin Islands must register with the USVI Division of Corporations and Trademarks before conducting business locally. Foreign corporation registration in US Virgin Islands is governed under Title 13 of the Virgin Islands Code, which sets out the qualification requirements for out-of-territory entities. Registration does not create a new legal entity — the foreign firm retains the legal form, liability structure, and governance rules of its home jurisdiction.

Qualification is required when a business is "transacting business" within the territory, a threshold defined by statute with specific exclusions for activities such as maintaining bank accounts or holding board meetings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Retains home jurisdiction form (corp, LLC, partnership) | No new entity is created upon registration |

| Registered Agent | Mandatory; must be a resident agent in USVI | Required for service of process |

| Registered Office | Local address in USVI required | P.O. Box typically not accepted |

| Filing Authority | USVI Division of Corporations and Trademarks | Certificate of Authority must be obtained |

| Home Jurisdiction Docs | Certified certificate of existence/good standing required | Must be current at time of filing |

| Privacy | Officers/managers disclosed in filings | No anonymous registration available |

Focus Points

- Taxation: Foreign entities operating in USVI are subject to the mirror tax system, which replicates the U.S. Internal Revenue Code; no separate VAT or general sales tax applies at the territory level, though gross receipts tax may apply depending on the nature of business activity.

- Annual Compliance: Annual reports must be filed with the Division of Corporations and Trademarks; failure to file can result in revocation of the Certificate of Authority.

- Economic Development Program: Foreign entities do not automatically qualify for the USVI Economic Development Authority (EDA) tax benefits; a separate application and physical presence requirement apply.

- Conversion: A registered foreign entity cannot convert directly into a domestic USVI entity through the registration process; a separate formation and dissolution procedure is required.

- Restrictions: Certain regulated industries — including banking, insurance, and telecommunications — require additional licensing beyond standard qualification.

Closing

Registered foreign entities are typically used by U.S. mainland businesses or international firms that need a physical operational presence in USVI without dissolving or restructuring their existing corporate form. The primary advantage is operational continuity under the home jurisdiction's legal structure; the key limitation is that registration alone does not confer access to USVI tax incentive programs.

U.S. mainland corporations and LLCs expanding into USVI operations without restructuring their existing entity, particularly those in retail, professional services, or logistics.

Sole Proprietorship

A sole proprietorship in the US Virgin Islands is the simplest business structure available, operating without a separate legal personality from its owner. No dedicated sole proprietorship statute governs this form; it exists by default under general territorial law, meaning the owner bears unlimited personal liability for all business debts and obligations.

Registration requirements are minimal compared to incorporated entities. If you operate under a name other than your own legal name, you must file a fictitious business name — commonly called a "doing business as" (DBA) — with the USVI Division of Corporations and Trademarks under the Lieutenant Governor's Office.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated, no separate legal entity | Owner and business are legally the same person |

| Members | Single individual proprietor; no maximum or minimum beyond one | No shareholders, directors, or members |

| Local Presence | DBA filing with USVI Division of Corporations and Trademarks if trading under a fictitious name | No registered agent requirement for sole proprietors |

| Capital | No minimum capital requirement; USD is the operating currency | Capital is the owner's personal funds |

| Privacy | Owner's name is publicly associated with the business | DBA filings are public records |

Focus Points

- Taxation: Subject to USVI personal income tax on business profits; the territory mirrors the U.S. Internal Revenue Code, so federal income tax rules apply through the "mirror tax" system — no separate corporate tax, no VAT, no withholding tax on the proprietor's own drawings.

- Annual Compliance: Business license renewal is required annually through the USVI Department of Licensing and Consumer Affairs (DLCA); no annual report is filed with the Division of Corporations and Trademarks.

- Economic Substance: No economic substance obligations apply to sole proprietorships.

- Conversion: Converting to an LLC or corporation requires forming a new entity separately; there is no statutory conversion mechanism for sole proprietorships.

- Restrictions: Foreign nationals must verify eligibility to operate a business under applicable immigration and licensing rules before starting a sole proprietorship in USVI.

Closing

A sole proprietorship suits early-stage local service businesses, freelancers, and individuals testing a market concept with low overhead. The primary limitation is unlimited personal liability — all business debts expose the owner's personal assets directly.

Local residents and small-scale operators conducting low-risk, single-owner activities who do not require liability separation or external investment.

How to Choose the Right Entity Type in U.S. Virgin Islands (VI)

Choosing the right business entity USVI entrepreneurs and foreign investors register often determines far more than tax liability — it shapes your compliance obligations, liability exposure, and operational flexibility for years ahead.

Why Your Entity Choice Matters

The structure you form on day one carries consequences that compound over time. Selecting the wrong type is not a minor administrative inconvenience; it can produce the following concrete outcomes:

- Registering as a foreign entity when your business operates locally — employing staff or serving USVI residents — places you in breach of the Virgin Islands Uniform Business Organizations Code (Title 13 V.I.C.), which can result in penalties or administrative dissolution.

- Forming a company under the Economic Development Program for its tax benefits while also needing access to U.S. tax treaty provisions may create a conflict, as program beneficiaries operate under a separate tax incentive framework that does not interact predictably with standard treaty mechanisms.

- Selecting a structure that triggers USVI substance expectations — such as maintaining a bona fide business presence under EDC requirements — without the capacity to staff an office or conduct management locally exposes you to benefit clawback and compliance failures.

- Forming a corporation when a single-member LLC would suffice imposes annual board formalities, shareholder meeting requirements, and potentially audited financials that are disproportionate for a solo consultancy.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point toward a distinct legal structure under USVI law.

- Local vs. External Operations: Businesses serving USVI residents must register with the Division of Corporations and Trademarks and meet local licensing requirements, whereas entities operating entirely outside the territory face a different compliance profile.

- Ownership and Management: A single owner typically benefits from the LLC's flexible operating agreement structure, while multi-investor arrangements may require the governance formality of a corporation.

- Tax Objectives: Your eligibility for the Economic Development Authority's benefits, standard USVI income tax treatment, or pass-through taxation each correspond to different entity types.

- Substance Capacity: If you cannot realistically place employees or management decisions within the territory, you must account for this before selecting a structure that requires demonstrable local presence.

- Exit Strategy: Not all USVI entities support redomiciliation or statutory conversion; confirm whether your chosen structure permits these mechanisms before formation.

Compliance Services for Companies in the U.S. Virgin Islands

Maintain good standing and meet ongoing regulatory obligations under USVI law.

Conclusion

Selecting the right structure is the first binding decision in any US Virgin Islands company formation process. Corporations suit businesses seeking access to the Economic Development Program's tax benefits, while C and S corporations differ primarily in their ownership and distribution rules. The LLC remains the most commonly registered entity type in the territory, favored for its flexibility in member agreements and pass-through taxation. Partnerships serve joint ventures and professional firms, with the LLP offering partners a degree of liability separation. Sole proprietorships carry no formal registration burden but leave the owner fully exposed.

USVI's regulatory framework, administered through the Division of Corporations and Trademarks, continues to align with federal U.S. standards, which supports the territory's credibility with international counterparties. For businesses requiring professional guidance through this incorporating in US Virgin Islands guide, Expanship offers jurisdiction-specific advisory across all recognized entity types.

How Expanship Can Assist You

Expanship USVI company registration services are built around the specific structural options and compliance obligations covered in this guide — from forming a domestic LLC or corporation under Title 13 of the Virgin Islands Code to registering a foreign entity with the USVI Division of Corporations and Trademarks.

From initial document preparation through to post-incorporation maintenance, our corporate services in the US Virgin Islands cover the full scope of what your business needs to stay compliant:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in St. Thomas or St. Croix

- Filing and liaison with the USVI Division of Corporations and Trademarks

- Annual report filing and ongoing compliance management

- Support with Economic Development Commission (EDC) program documentation

- Banking introduction assistance for newly formed entities

Reach out to Expanship US Virgin Islands to discuss your entity formation requirements.

Frequently Asked Questions (FAQ)

The LLC is the most frequently formed business structure in the territory. Its combination of pass-through taxation, limited liability, and relatively minimal statutory formalities under Title 13 of the Virgin Islands Code makes it the default choice for both resident and non-resident operators.

An LLC formed under standard USVI rules is taxed under the mirror tax system and can trade locally without restriction. An Exempt Company under the Economic Development Authority program receives substantial reductions on income tax, gross receipts tax, and excise tax, but must meet ongoing employment, capital investment, and local presence requirements to retain those benefits.

An LLC offers the most privacy among standard USVI entities. Member names are not required on the publicly filed Articles of Organization, and nominee arrangements are legally permissible, though beneficial ownership information may still be reportable under federal requirements.

A sole proprietorship, LLC, and corporation can each be formed by one individual. General partnerships and limited partnerships require at least two partners by definition, so a single person cannot form those structures alone.

Non-U.S. nationals may form an LLC or corporation in the territory without restriction on foreign ownership. Foreigners seeking tax benefits under the Economic Development Authority program must, however, satisfy residency and physical presence conditions that make remote ownership of an EDA-certified entity structurally difficult.

Title 13 of the Virgin Islands Code permits statutory conversion between certain entity types, including conversion of a partnership to an LLC or a corporation. The process requires filing a Certificate of Conversion with the Division of Corporations and Trademarks, and the converted entity retains the rights and obligations of its predecessor.

Corporations and LLCs possess distinct legal personality separate from their owners. General partnerships do not have separate legal personality under USVI law, meaning partners remain personally liable for partnership obligations, whereas limited partnerships and LLPs provide partial or full liability separation depending on the partner's role.

A sole proprietorship has no statutory filing requirements beyond a local business license and applicable tax registrations. By contrast, corporations must hold annual meetings, maintain minutes, and file annual reports with the Division of Corporations and Trademarks, while LLCs face fewer formalities but still carry annual report obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.