Key Takeaways

- Vatican City does not operate a general commercial company registry, with oversight of legal entities and financial institutions falling under the Autorità di Supervisione e Informazione Finanziaria (ASIF).

- Recognised legal structures within the jurisdiction are limited to pontifical foundations, ecclesiastical entities (enti ecclesiastici), associations, and foreign liaison or representative presences.

- The legal framework governing entity formation in Vatican City draws from canon law alongside specific pontifical legislation, rather than the commercial frameworks found in EU member states or conventional offshore centres.

- Foreign organisations seeking an operational foothold in Vatican City may do so through liaison or representative presence structures without establishing a permanent canonical or civil entity.

Introduction to Entity Types in Vatican City

Vatican City sits within Rome, Italy, making it the world's smallest internationally recognised sovereign state by both area and population. Governed under the authority of the Holy See, it operates as an ecclesiastical sovereign entity rather than a conventional commercial jurisdiction. Corporate activity here does not follow the standard framework you would find in EU member states or typical offshore centres.

Oversight of legal entities and financial institutions falls primarily under the Autorità di Supervisione e Informazione Finanziaria (ASIF), the financial intelligence and supervisory authority established under Vatican law. The jurisdiction does not operate a general commercial company registry in the conventional sense, and the legal framework governing business entity types in Vatican City draws heavily from canon law alongside specific pontifical legislation.

The tax posture is generally non-commercial in nature, with activity structured around ecclesiastical and institutional purposes rather than profit-driven enterprise.

Recognised Holy See legal entities and Vatican City company structures include pontifical foundations, ecclesiastical entities (enti ecclesiastici), associations, and foreign liaison or representative presences. This article examines each structure — its legal basis, governance requirements, and the conditions under which your organisation might operate through it.

An Overview of Business Structures in Vatican City

Vatican City's legal framework does not operate through a conventional commercial company law statute in the way most sovereign states do. The available entity options are defined primarily through pontifical legislation and Holy See administrative directives, with the Governorate of Vatican City State serving as the principal regulatory authority for civil matters within the territory. Each structure serves a distinct operational purpose, from ecclesiastical institutions to foreign presence arrangements.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Pontifical Entity | Public ecclesiastical body | Limited to assets | Generally exempt | Permitted | Appointed by Holy See | Secretariat of State | Pontifical legislation |

| Holy See-Sanctioned Institution | Institutional body | Limited | Exempt | Restricted | Varies by statute | Holy See / Governorate | Apostolic decrees |

| Foundation (Fondazione) | Non-profit legal entity | Limited to assets | Generally exempt | No | Minimum board required | Governorate | Pontifical civil law |

| Association (Associazione) | Membership body | Limited | Generally exempt | No | Multiple members | Governorate | Pontifical civil law |

| Ecclesiastical Body (Ente Ecclesiastico) | Canonical legal person | Limited | Exempt | Restricted | N/A | Dicastery / Holy See | Canon Law / CIC 1983 |

| Branch Office | Extension of foreign entity | Parent liable | Subject to review | Limited | N/A | Governorate | Administrative directives |

| Representative / Liaison Office | Non-trading presence | Parent liable | Exempt | Not permitted | N/A | Governorate | Administrative directives |

Each of these structures is examined in full in the sections below.

Pontifical Entities and Holy See-Sanctioned Institutions

Pontifical entities and Holy See institutions form the most structurally distinct category of legal organizations operating within Vatican City. Their existence is governed primarily by canon law — specifically the 1983 Code of Canon Law (CIC) — alongside the Fundamental Law of Vatican City State (2000) and internal Holy See regulations. These frameworks grant recognized canonical institutions a form of legal personality under ecclesiastical law, which is distinct from civil incorporation models found in secular jurisdictions.

Legal personality in this context derives from recognition by the Holy See rather than registration with a conventional commercial registry. Liability exposure varies by institutional structure, and many entities operate with patrimony held in trust for a specific canonical purpose rather than distributed to members.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Canonical juridic person (public or private) | Established by decree or recognition under CIC canons 114–123 |

| Governing Members | Moderator, Board of Administrators, or Pontifical Council | Titles vary by statute; no shareholder structure applies |

| Membership / Composition | No statutory minimum or maximum; defined by approved statutes | Composition determined by Holy See approval |

| Local Presence | Registered seat within Vatican City or Holy See territory | Physical presence required; no registered agent concept |

| Capital / Patrimony | No minimum capital; stable patrimony required for public juridic persons | Currency managed through IOR or APSA where applicable |

| Privacy | Statutes approved by Holy See; not publicly indexed in commercial registries | Beneficial ownership not publicly disclosed under civil registry norms |

Focus Points

- Taxation: Pontifical entities are generally exempt from corporate income tax and VAT on activities directly serving their canonical purpose; commercial activities conducted alongside core functions may attract different treatment under internal Holy See fiscal regulations.

- Economic Substance: Entities must genuinely operate in furtherance of their stated canonical mission; hollow or inactive structures are inconsistent with Holy See recognition standards.

- Annual Compliance: Entities submit periodic financial reports to the relevant dicastery or supervisory body, such as the Secretariat for the Economy, established under the apostolic constitution Praedicate Evangelium (2022).

- Treaty Access: The Holy See maintains diplomatic relations and concordats with numerous states, but these do not function as double tax treaties in the commercial sense; access to tax treaty benefits available in secular jurisdictions does not apply.

- Restrictions: Canonical juridic persons cannot be converted into secular commercial entities; their purpose, governance, and dissolution are governed exclusively by ecclesiastical authority.

Sub-Types

Public Juridic Persons

Erected by the Holy See, a bishops' conference, or a diocesan bishop through formal decree. These carry a higher degree of institutional integration with Church authority and are typically used for major pontifical universities, charitable institutions, and Vatican-affiliated organizations acting in the Church's name.

Private Juridic Persons

Established by the faithful with Holy See approval under CIC canon 322. These operate with greater autonomy from hierarchical authority and are commonly used for private apostolic works, charitable foundations, or institutions serving specific religious or humanitarian purposes without acting formally in the name of the Church.

Pontifical entities are primarily suited to religious, charitable, educational, and humanitarian activities operating under ecclesiastical governance rather than commercial objectives. The key structural advantage is their recognized canonical legal personality under international law through the Holy See's unique sovereign status. The primary limitation is rigidity: these institutions cannot pivot to commercial purposes, and dissolution or restructuring requires formal ecclesiastical authority.

This structure is best suited to organizations whose mission is intrinsically tied to the Catholic Church's apostolic, charitable, or educational mandate — not for commercial ventures or investment holding purposes.

Company Incorporation in Vatican City

Understand your entity options and registration pathways under Holy See and Vatican City frameworks.

Foundations and Non-Profit Organizations (Fondazioni, Associazioni, Enti Ecclesiastici)

Vatican City fondazioni, associazioni, and enti ecclesiastici operate under a legal framework shaped primarily by canon law and the civil legislation enacted by the Pontifical Commission for Vatican City State. Unlike commercial entities, these structures exist principally to serve religious, charitable, or ecclesiastical purposes rather than to generate profit for distribution to members.

Juridical personality for such entities is typically conferred under canon law (Code of Canon Law, 1983) or through specific recognition by the Holy See. Separate legal personality is generally granted upon formal approval, though the scope of limited liability and governance obligations varies depending on whether the entity is constituted under civil or canonical authority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foundation (Fondazione), Association (Associazione), or Ecclesiastical Entity (Ente Ecclesiastico) | Canonical or civil juridical person |

| Governing Members | Directors, trustees, or governing council; lay or clerical | Minimum composition varies by statutes and approving authority |

| Local Presence | Registered seat within Vatican City or Holy See-recognized address | Physical presence required for canonical entities |

| Capital | No statutory minimum capital requirement | Assets must be sufficient to fulfill stated purpose |

| Supervision | Pontifical Commission for Vatican City State; Dicastery for the Economy for Holy See-related entities | Dual oversight possible for entities linked to the Roman Curia |

| Privacy | Statutes and governing documents held internally; limited public registry disclosure | Disclosure requirements are minimal compared to civil jurisdictions |

Focus Points

- Taxation: Ecclesiastical entities and approved non-profits generally benefit from exemptions on income directly tied to their institutional purpose; commercial activities conducted alongside exempt purposes may attract separate treatment under Vatican fiscal norms.

- Annual Compliance: Entities are subject to internal reporting to their supervising dicastery or the Pontifical Commission; financial transparency requirements have increased following reforms tied to the Vatican's MONEYVAL evaluation process.

- Treaty Access: Vatican City is not party to double tax treaties in the conventional sense; enti ecclesiastici with cross-border activities must assess tax exposure in each relevant jurisdiction independently.

- Restrictions: Non-profit structures cannot distribute surpluses to members; any dissolution surplus must be directed toward purposes consistent with the entity's mission as specified in its statutes.

- Conversion: Conversion from a non-profit to a commercial structure is not a recognized pathway under Vatican civil or canonical law.

Sub-Types

Fondazione (Foundation)

A fondazione is an asset-based entity established to pursue a specific charitable, religious, or cultural objective, distinguished by the primacy of the endowed patrimony over its membership. It is commonly used for long-term grant-making, heritage preservation, or support of ecclesiastical institutions.

Associazione (Association)

An associazione is member-based rather than asset-based, making it structurally distinct from a foundation. This form is typically used by Catholic organizations, lay movements, or professional groups seeking collective juridical recognition under Holy See authority.

Ente Ecclesiastico (Ecclesiastical Entity)

Enti ecclesiastici are entities formally constituted under canon law and recognized as juridical persons by the Church. They include religious institutes, parishes, and curial bodies, and carry both canonical and, where applicable, civil legal standing.

Closing

These structures are suited to organizations with a religious, charitable, or apostolic mission that require formal legal standing within or connected to the Holy See. Their primary advantage is the depth of canonical recognition they carry internationally; the principal limitation is that their operational scope is tightly bound to their stated non-commercial purpose.

Best suited for Catholic organizations, religious institutes, and international charitable bodies seeking formal juridical recognition anchored in Holy See authority.

Foreign Presence Structures [Branch Office, Representative Office, Liaison Office]

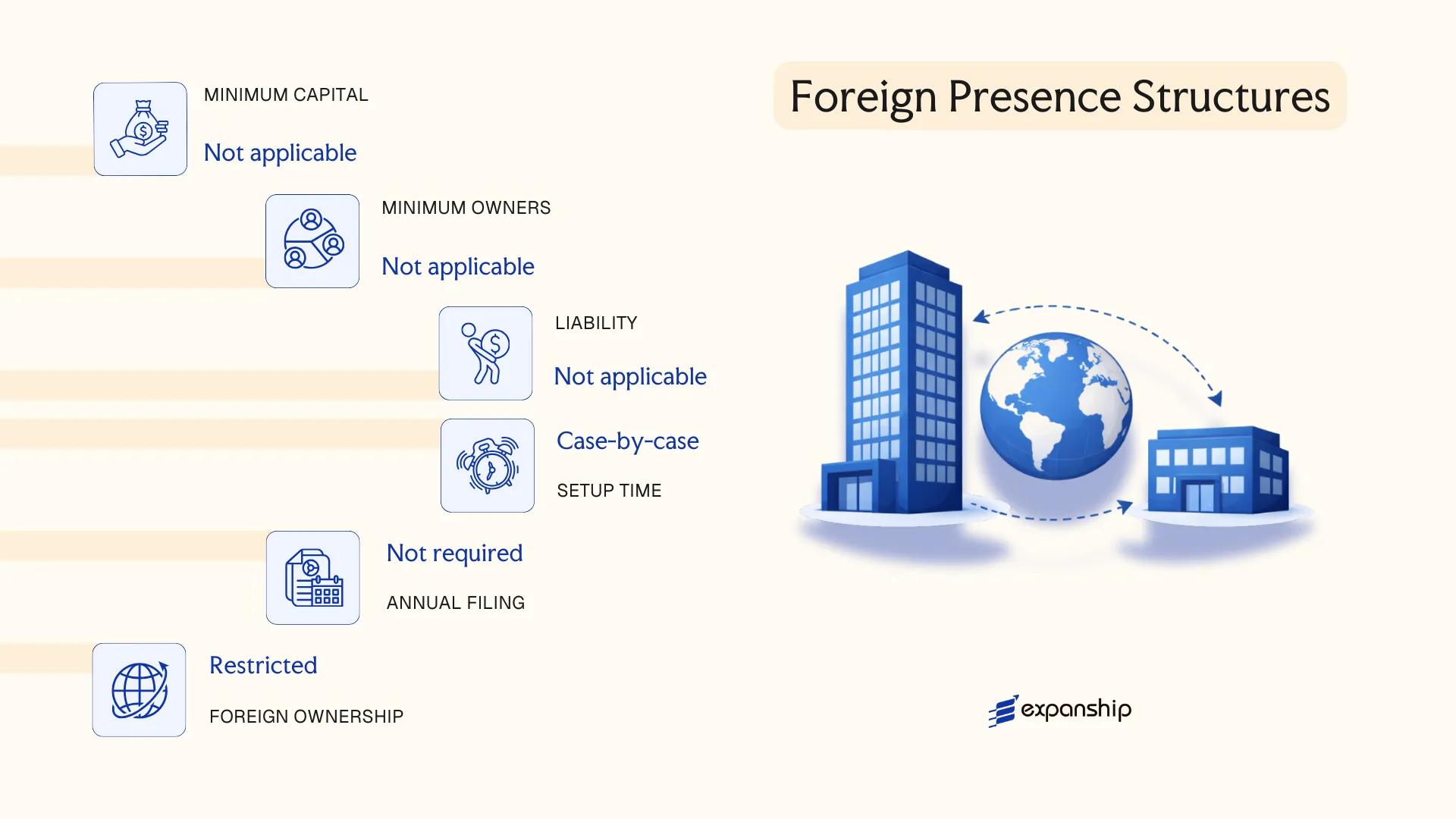

Establishing a foreign branch office Vatican City presents a structurally distinct challenge from most jurisdictions. The Holy See does not operate a conventional commercial law framework; its legal order is governed by the Fundamental Law of Vatican City State (2000) and supplementary legislation administered through the Governorate of Vatican City State. Foreign entities cannot establish a commercial presence in the ordinary sense, as the territory does not host a private-sector economy open to external business registration.

Practical foreign presence is therefore limited to entities operating under pontifical mandate or formal agreements with the Holy See. No standalone branch or liaison office registration process exists for private commercial firms, as the jurisdiction's legal infrastructure is not designed to accommodate external business operations independent of Holy See authorization.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | No formal branch or rep office statute | Presence requires Holy See authorization or bilateral agreement |

| Regulatory Authority | Governorate of Vatican City State | No commercial registry equivalent exists |

| Local Presence | Physical presence requires pontifical approval | Cannot be established through standard corporate filing |

| Legal Personality | Not applicable for standard foreign structures | Entities operate under Holy See-sanctioned frameworks only |

| Privacy | Not publicly disclosed through any commercial register | No public registry of foreign entities exists |

Focus Points

- Taxation: No corporate tax, VAT, or withholding tax regime applies to foreign commercial entities, as none are permitted to operate commercially under private law.

- Economic Substance: No substance requirements exist because the jurisdiction does not admit standard foreign business structures.

- Treaty Access: The Holy See maintains bilateral agreements with numerous states, but these govern diplomatic and ecclesiastical matters, not commercial tax treaties.

- Restrictions: Foreign private firms have no legal pathway to register a branch, representative office, or liaison office through any general commercial procedure.

Closing

Foreign presence in this jurisdiction is realistically available only to organizations operating within ecclesiastical, diplomatic, or humanitarian mandates formally recognized by the Holy See. The absence of a commercial registry is both its defining characteristic and its principal constraint for conventional foreign business structures.

This structure is best suited to international ecclesiastical organizations, Holy See-accredited diplomatic missions, or humanitarian bodies operating under formal pontifical recognition.

How to Choose the Right Entity Type in Vatican City

Choosing the right entity type in Vatican City is not a procedural formality — the structure you select determines your legal standing, tax treatment, and operational capacity under Holy See authority.

Why Your Entity Choice Matters

Misalignment between your chosen structure and your actual activities carries concrete legal and financial consequences:

- Selecting a pontifical or ecclesiastically sanctioned entity without a genuine religious or charitable mission can result in the Holy See's Secretariat of State withdrawing recognition, invalidating the entity's legal standing entirely.

- Choosing a tax-exempt ecclesiastical entity when you require access to bilateral tax arrangements means your organisation cannot claim withholding tax reductions under counterpart jurisdictions' treaty provisions.

- Forming a structure with no capacity for local substance when your activities require a physical presence within Vatican territory triggers non-compliance with operational requirements and potential dissolution.

- Adopting a foundation structure when your objectives require active commercial trading locks you into asset-dedication rules that prohibit profit distribution to founders or members.

Key Factors to Consider

- Mission and Activity Type: Passive asset holding, active trade, and religious or charitable operations each correspond to distinct structural categories recognised under Holy See governance.

- Ecclesiastical Alignment: Entities requiring formal Holy See recognition must demonstrate a purpose consistent with canon law and Vatican institutional objectives.

- Tax Objectives: Your need for full exemption, limited fiscal privileges, or access to external treaty networks should determine whether an ecclesiastical or civil-law structure is appropriate.

- Ownership and Governance: Single-administrator structures differ materially from collegial bodies requiring board composition under Vatican regulatory norms.

- Privacy Requirements: Disclosure obligations vary by entity type; understanding what information enters any accessible Vatican register is essential before formation.

- Exit and Continuity: Not all Vatican-recognised structures permit straightforward dissolution, conversion, or redomiciliation — confirm these options before committing to a form.

Consult the relevant provisions governing entity formation through the Holy See's official legal instruments before proceeding.

Compliance Services for Companies in Vatican City

Maintain your entity's good standing under Holy See authority with structured compliance support covering reporting obligations, regulatory filings, and governance requirements.

Conclusion

Vatican City business incorporation remains one of the most specialized exercises in international corporate law. Pontifical entities serve institutions operating under canonical mandate, while foundations and associations accommodate mission-driven organizations aligned with Holy See objectives. Foreign presence structures, by contrast, offer external organizations a limited operational foothold without establishing a permanent canonical or civil entity.

Pontifical institutions represent the dominant registered form within the jurisdiction, reflecting the Holy See's ecclesiastical governance model. The Governorate of Vatican City State retains administrative authority over civil registrations, and any entity formation continues to require alignment with that framework.

Regulatory access here is governed by canonical law and bilateral agreements rather than commercial treaty networks, a distinction that shapes how your business approaches structuring under this jurisdiction.

How Expanship Can Assist You

Expanship Vatican City company formation services are built around the specific legal and institutional realities of the Holy See — including the distinct character of Pontifical entities, ecclesiastically sanctioned institutions, and the role of the Governorate of Vatican City State as the relevant administrative authority. Every engagement starts with a clear-eyed assessment of which structure actually fits your operational purpose within this jurisdiction.

Expanship handles the full process from initial documentation through to post-incorporation requirements:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered office provision

- Liaison with the Governorate of Vatican City State for filings and approvals

- Post-incorporation compliance management

- Banking introduction assistance for Vatican-adjacent financial institutions

Contact Expanship Vatican City to discuss your specific entity requirements.

Frequently Asked Questions (FAQ)

Enti Ecclesiastici (ecclesiastical entities) represent the predominant institutional form operating within the Holy See's legal framework. Their prevalence reflects the jurisdiction's foundational purpose: governance and administration in service of the Catholic Church's global mission.

An Ente Ecclesiastico derives its legal standing from canon law and requires formal recognition by the Apostolic See, whereas a Fondazione operates under civil law principles with a defined patrimonial endowment directed toward a specific purpose. Both are non-profit structures, but an Ente Ecclesiastico answers to ecclesiastical authority in a way a Fondazione does not.

Pontifical institutions and certain Holy See-sanctioned bodies are not subject to public disclosure requirements comparable to commercial registries in other jurisdictions. Beneficial ownership details are not published in an accessible public register, and nominee arrangements are not a recognized feature of these structures.

Fondazioni can, in principle, be constituted by a sole founder, provided sufficient patrimony is dedicated to the stated purpose. Associazioni, by contrast, require a plurality of members by their nature as collective bodies.

Foreign involvement is permitted in Fondazioni and Associazioni, though any entity seeking Holy See recognition must demonstrate alignment with the Church's institutional objectives. Purely commercial foreign enterprises do not have a standard incorporation pathway; foreign presence is typically structured through representative or liaison offices operating under specific authorization.

No codified conversion mechanism exists under current Vatican civil law. Restructuring generally requires dissolving the existing entity and constituting a new one under the intended form, subject to fresh authorization from the relevant dicastery or civil authority.

Enti Ecclesiastici and Fondazioni both carry distinct legal personality once formally recognized, allowing them to hold property, enter contracts, and bear obligations independently. Informal associazioni lacking canonical or civil recognition do not automatically acquire legal personality.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.