Key Takeaways

- Uruguay's territorial tax system exempts foreign-sourced income from local taxation, a structural feature that directly influences how international businesses choose to organize their operations in the country.

- The Sociedad Anónima remains Uruguay's most widely registered entity, though its historically favored bearer-share arrangements were significantly curtailed by transparency reforms introduced under Law 18,930 in 2012.

- Business registration in Uruguay is overseen by the Auditoría Interna de la Nación (AIN), with incorporation procedures processed through the Registro Nacional de Comercio.

- Sole proprietorships and informal structures such as the Sociedad de Hecho carry unlimited personal liability, limiting their suitability to small-scale, low-risk operations.

Introduction to Entity Types in Uruguay

Uruguay is a sovereign republic on the southeastern coast of South America, bordered by Brazil to the north and Argentina to the west. Business registration falls under the jurisdiction of the Auditoría Interna de la Nación (AIN), the body responsible for overseeing commercial registry functions, with incorporation procedures processed through the Registro Nacional de Comercio.

The country operates a territorial tax system, meaning foreign-sourced income is generally not subject to local taxation — a detail that shapes how businesses structure their operations here.

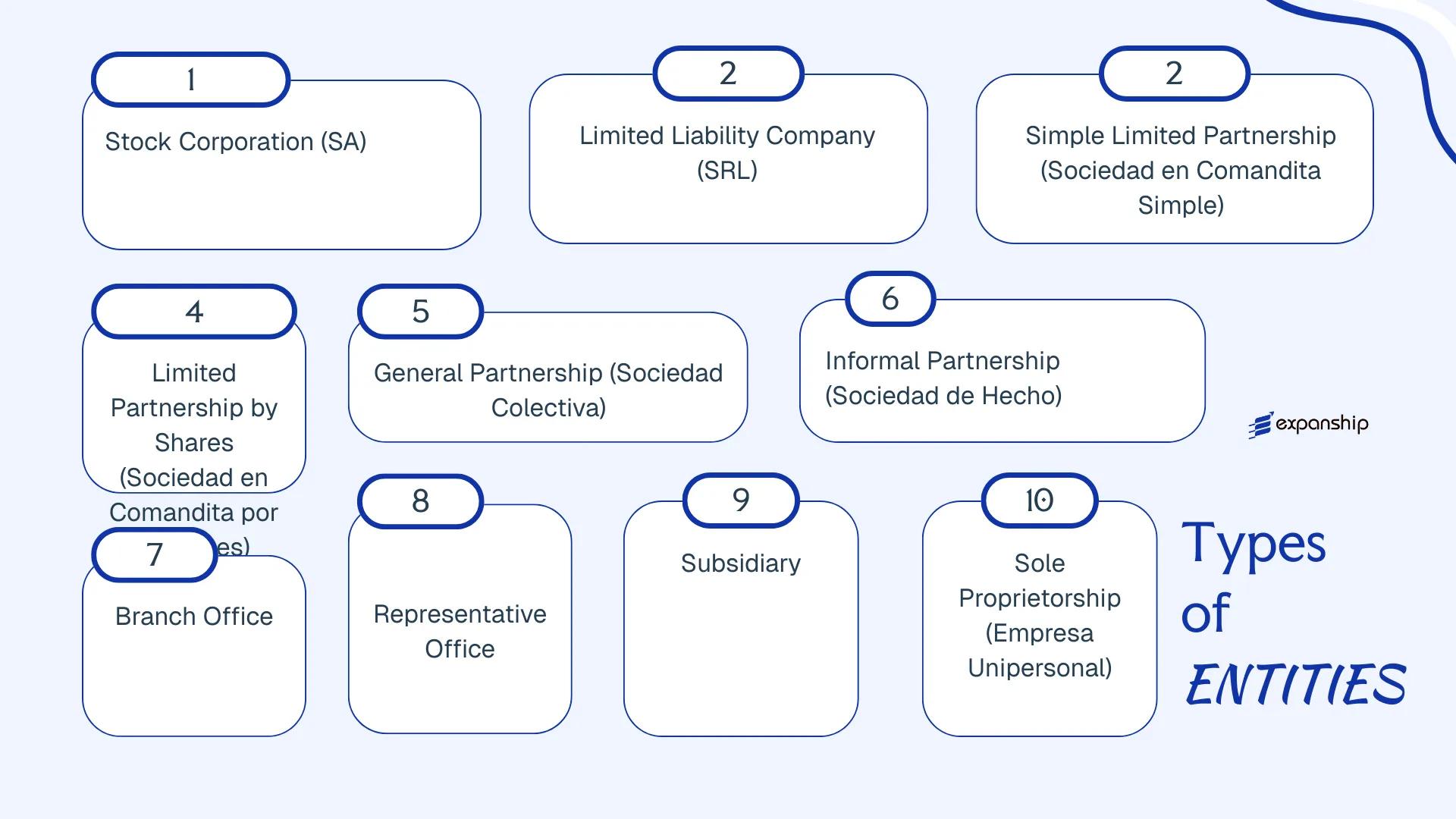

Several distinct legal forms are available to those looking to establish a presence. These include the Sociedad Anónima (SA), Sociedad de Responsabilidad Limitada (SRL), Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Sociedad Colectiva, Sociedad de Hecho, Branch Office, Representative Office, and Empresa Unipersonal.

Understanding the types of business entities in Uruguay requires examining each structure's legal requirements, liability treatment, and ownership rules. This article covers each form in detail, drawing on the governing provisions of Uruguay's commercial code and applicable regulatory requirements.

An Overview of Business Structures in Uruguay

Uruguayan company law recognizes several distinct entity types, each governed primarily by Law No. 16,060 (the Commercial Companies Law) and, for certain regulated activities, by additional sectoral legislation. Your choice of corporate structure determines liability exposure, governance requirements, and how the business interacts with the Auditoría Interna de la Nación (AIN) and the Registro Nacional de Comercio. Each form serves a different commercial purpose.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (SA) | Corporation | Limited to shares | Taxed (IRAE) | Yes | 2 shareholders | AIN / Registro Nacional de Comercio | Law 16,060 |

| Sociedad de Responsabilidad Limitada (SRL) | LLC | Limited to quota | Taxed (IRAE) | Yes | 2 members (max 50) | Registro Nacional de Comercio | Law 16,060 |

| Sociedad en Comandita Simple | Limited partnership | Mixed | Taxed (IRAE) | Yes | 2 (1 general, 1 limited) | Registro Nacional de Comercio | Law 16,060 |

| Sociedad en Comandita por Acciones | Share-based LP | Mixed | Taxed (IRAE) | Yes | 2 (1 general, 1 limited) | AIN / Registro Nacional de Comercio | Law 16,060 |

| Sociedad Colectiva | General partnership | Unlimited | Taxed (IRAE) | Yes | 2 partners | Registro Nacional de Comercio | Law 16,060 |

| Sociedad de Hecho | Informal partnership | Unlimited | Taxed (IRAE) | Yes | 2 partners | Registro Nacional de Comercio | Law 16,060 |

| Branch Office | Foreign branch | Parent liability | Taxed (IRAE) | Yes | 1 foreign parent | Registro Nacional de Comercio | Law 16,060 |

| Representative Office | Non-trading entity | Parent liability | Limited scope | No | 1 foreign parent | Registro Nacional de Comercio | Law 16,060 |

| Empresa Unipersonal | Sole proprietorship | Unlimited | Taxed (IRAE/IVA) | Yes | 1 individual | DGI / BPS | Tax/Labor law |

Each of these structures is examined in full in the sections below.

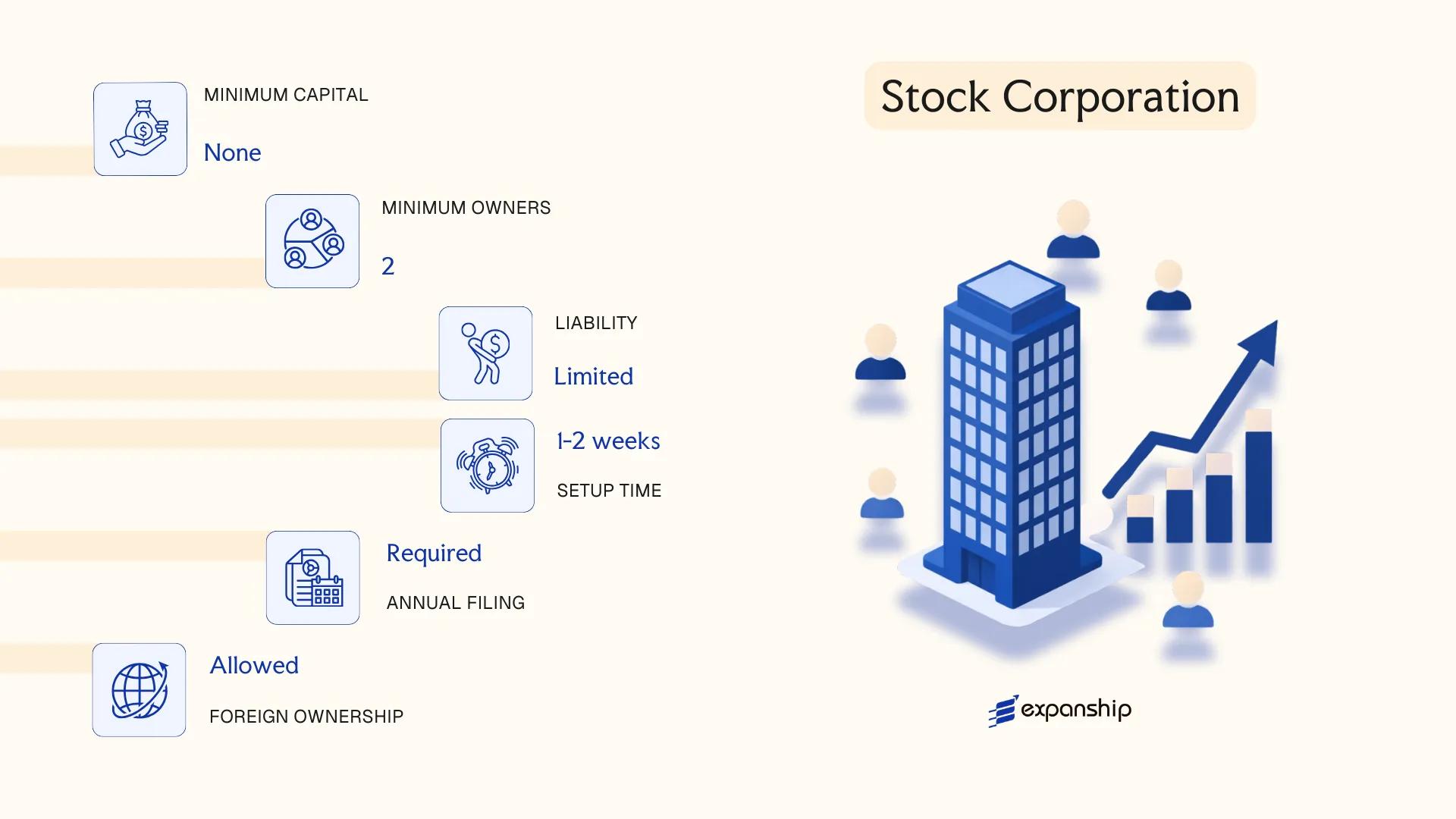

Sociedad Anónima (SA) — Stock Corporation

Governed primarily by Law No. 16,060 (the Commercial Companies Law of 1989), the Sociedad Anónima Uruguay SA formation process produces a corporation with full separate legal personality. Shareholders bear no personal liability beyond their capital contributions.

Ownership is represented through transferable shares, which can be issued as nominative or bearer (subject to registration requirements under Law No. 18,930). This structure makes the SA particularly suited to businesses requiring a clear separation between ownership and management.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (Corporation) | Governed by Law No. 16,060 |

| Members | Shareholders (owners); Directors (management) | Minimum 1 shareholder; minimum 3 directors unless statute provides otherwise; no maximum on shareholders |

| Local Presence | Registered address required in Uruguay | A statutory domicile must be maintained; a registered agent is advisable but not strictly mandated by law |

| Share Capital | No statutory minimum capital; denominated in Uruguayan Pesos (UYU) | Capital divided into shares; bearer shares must be registered with the Central Bank (BCU) under Law No. 18,930 |

| Privacy | Shareholder identity disclosed to BCU; not in a public registry | Directors appear in public filings with the Auditoría Interna de la Nación (AIN) |

Focus Points

- Taxation: Corporate income tax (IRAE) at 25% on Uruguay-source income; VAT at 22% standard rate; dividends distributed to non-residents subject to 7% withholding tax; no stamp duty on share transfers under current rules — see DGI (Dirección General Impositiva) for current rates.

- Annual Compliance: Financial statements must be filed annually with AIN; large companies are subject to mandatory external audit requirements.

- Economic Substance: No formal substance regime comparable to some offshore jurisdictions, but IRAE territoriality means foreign-source income is generally exempt and need not trigger local substance obligations.

- Treaty Access: Uruguay has a growing tax treaty network; SA entities qualify as tax residents and can access treaty benefits where applicable.

- Conversion: An SA can be converted into an SRL or other commercial form under Law No. 16,060 without dissolution, subject to creditor notification procedures.

Sub-Types

Sociedad Anónima Abierta (Open SA)

An Open SA makes public offerings of its shares and is subject to supervision by the Banco Central del Uruguay (BCU) under securities regulations. This structure is used by companies seeking to raise capital from the public market.

Sociedad Anónima Cerrada (Closed SA)

A Closed SA restricts share transfers and does not access public capital markets. It is the more common form for private business, family-held enterprises, and foreign investment vehicles.

Recommendations

The SA functions effectively as a holding company for regional assets, an operating entity for larger commercial ventures, or an IP-holding structure, given the exemption of foreign-source income under IRAE. Its principal limitation is administrative overhead: mandatory director plurality, annual AIN filings, and BCU registration requirements for bearer shares add ongoing compliance cost relative to simpler forms.

The SA is most appropriate for foreign investors and mid-to-large businesses requiring a scalable ownership structure with transferable shares and clear separation of management from ownership.

Company Incorporation in Uruguay

Incorporate a Sociedad Anónima or other business entity in Uruguay with end-to-end support from our corporate services team.

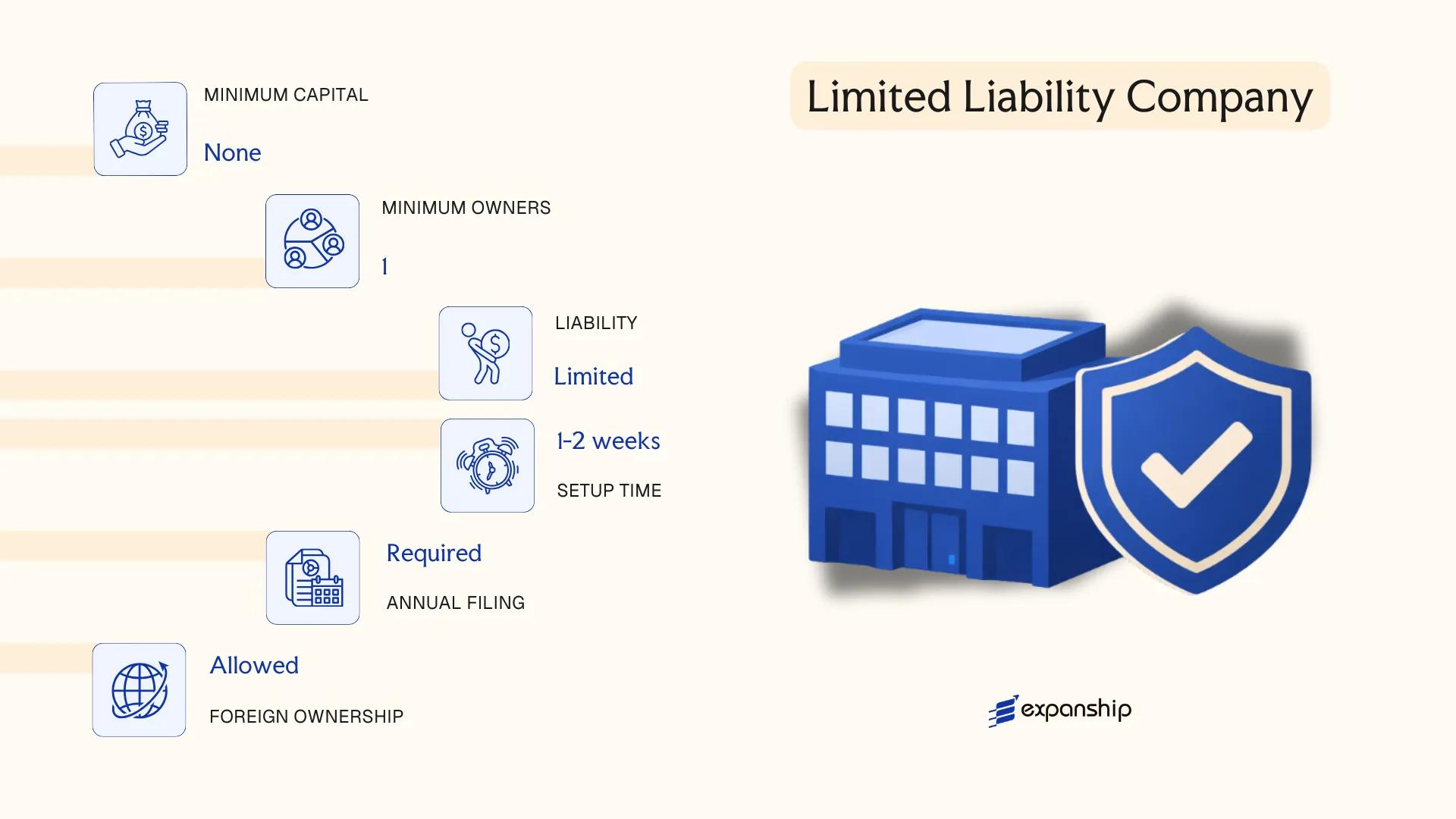

Sociedad de Responsabilidad Limitada (SRL) — Limited Liability Company

The Sociedad de Responsabilidad Limitada Uruguay SRL is governed primarily by Law No. 16,060 of 1989 (Ley de Sociedades Comerciales), the same statute that regulates most commercial entities in the country. It carries separate legal personality, meaning the entity holds rights and obligations distinct from those of its members.

Liability is capped at each member's capital contribution, making this a hybrid structure that combines the pass-through simplicity of a partnership with the liability protection of a corporation. Quota transfers are restricted by default, which keeps ownership more closely held than in a Sociedad Anónima.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (SRL) | Separate legal personality; governed by Law 16,060 |

| Members | Referred to as cuotapartistas (quota holders); minimum 2, maximum 50 | No corporate members restriction; natural or legal persons permitted |

| Management | One or more gerentes (managers); need not be members | Managers may be appointed in the articles or separately |

| Local Presence | Registered domicile in Uruguay required | No statutory requirement for a local resident manager, but a registered address is mandatory |

| Capital | No statutory minimum; denominated in Uruguayan Pesos (UYU); divided into cuotas (quotas) | Quotas are not freely transferable without member consent |

| Privacy | Members and managers disclosed to the Auditoría Interna de la Nación (AIN) | Not publicly searchable in a central open registry |

Focus Points

- Taxation: Subject to corporate income tax (IRAE) at 25% on Uruguayan-source income; VAT applies at 22% (reduced 10% rate for certain goods); dividend distributions to non-residents attract a 7% withholding tax; no stamp duty on quota transfers.

- Annual Compliance: Annual financial statements must be submitted to the AIN; accounting records must be maintained in Uruguay.

- Treaty Access: Uruguay has a growing network of double taxation agreements; SRL entities may access treaty benefits subject to residency and beneficial ownership conditions.

- Quota Transfer Restrictions: Transfers to third parties require prior consent from members holding at least 75% of the capital, unless the articles provide otherwise.

- Conversion: An SRL may be converted into an SA or another recognised commercial form through a members' resolution and registration with the relevant authority.

Closing

The SRL suits closely held operating businesses, family-owned trading companies, and mid-size ventures where ownership control and limited liability are both priorities. Its 50-member cap, however, makes it unsuitable for businesses that anticipate broad equity participation or future public investment.

The SRL is best suited for small to medium-sized businesses with a defined group of owners who require liability protection without the administrative overhead of a full stock corporation structure.

Sociedad en Comandita [Simple and por Acciones] — Limited Partnerships

Governed by Uruguay's Ley N° 16.060 (Ley de Sociedades Comerciales, 1989), the Sociedad en Comandita is a hybrid partnership structure that holds separate legal personality under Uruguayan law. It combines two distinct classes of partners: general partners (socios gestores) who bear unlimited personal liability, and limited partners (socios comanditarios) whose exposure is capped at their capital contribution.

Two recognised variants exist under the same legislation. The Sociedad en Comandita Simple (comandita simple) restricts participation interests to non-transferable quotas, while the Sociedad en Comandita por Acciones (comandita por acciones) issues shares for the limited partners' stake, making that interest more transferable. Both forms are relatively uncommon in contemporary practice but remain valid legal vehicles.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Hybrid partnership with separate legal personality | Governed by Ley N° 16.060 |

| Partners | At least 1 socio gestor (general) + 1 socio comanditario (limited); no statutory maximum | Socios gestores hold unlimited liability; socios comanditarios are liable only to the extent of their subscribed capital |

| Management | Socios gestores only | Socios comanditarios who participate in management lose their limited liability protection |

| Capital | No statutory minimum; comandita por acciones issues shares for limited partners' stake | Quotas (simple) or shares (por acciones) represent the limited partners' interest |

| Local Presence | Registered legal address in Uruguay required | A registered agent is not mandated by statute but is common in practice |

| Privacy | Partner identities disclosed to the Auditoría Interna de la Nación (AIN) | No public share register for the simple variant |

Focus Points

- Taxation: Subject to Impuesto a las Rentas de las Actividades Económicas (IRAE) at 25% on Uruguayan-source income; VAT applies at the standard 22% rate; profit distributions to non-resident partners attract Non-Resident Income Tax (IRNR) withholding at 7% or 12% depending on the nature of the income.

- Annual Compliance: Annual financial statements must be filed; socios gestores bear personal signing responsibility for regulatory submissions to the AIN.

- Treaty Access: Access to Uruguay's double tax treaty network depends on the entity's tax residency classification and the treaty counterpart's treatment of partnerships.

- Restrictions: Socios comanditarios are prohibited from acting in management capacity or using the firm name; breach triggers unlimited personal liability.

- Conversion: Conversion to an SA or SRL is permissible under Ley N° 16.060, subject to creditor notification requirements.

Sub-Types

Sociedad en Comandita Simple

The simple variant uses non-transferable quota interests for limited partners, making ownership transfers cumbersome and requiring partner consent. It suits closely held arrangements where the founding group does not anticipate bringing in outside capital or transferring stakes.

Sociedad en Comandita por Acciones

Limited partners' interests are represented by transferable shares, which allows for somewhat easier capital restructuring compared to the simple form. This variant is occasionally used where the limited partners' stake may need to change hands without dissolving the entity.

When to Consider This Structure

The Sociedad en Comandita serves niche scenarios, typically family-controlled enterprises or arrangements where one party contributes capital and another contributes operational management, with both parties preferring a defined liability split. The primary advantage is the clear contractual separation of active and passive roles; the main limitation is the unlimited personal liability carried by every socio gestor, which deters most modern investors.

This structure suits closely held ventures where an active managing partner and one or more passive capital contributors have a pre-existing relationship and a low appetite for structural complexity.

Sociedad Colectiva and Sociedad de Hecho — General and Informal Partnerships

Both the Sociedad Colectiva Uruguay general partnership and the Sociedad de Hecho are governed under Uruguay's Commercial Companies Law, Law No. 16,060 of 1989. The Sociedad Colectiva is a formally registered entity, while the Sociedad de Hecho operates without registration — neither form offers limited liability to its partners.

Under general partnership liability Uruguay rules, all partners in a Sociedad Colectiva bear unlimited, joint, and several liability for the firm's obligations. The Sociedad de Hecho, an Uruguay unregistered business partnership, carries the same exposure but additionally lacks the legal standing that registration provides, leaving partners in a more precarious position in any dispute.

Key Characteristics

| Requirement | Sociedad Colectiva | Sociedad de Hecho |

|---|---|---|

| Legal Form | Registered general partnership | Unregistered informal partnership |

| Members | Called "socios" (partners); minimum 2, no statutory maximum | Called "socios"; minimum 2, no statutory maximum |

| Liability | Unlimited, joint and several for all partners | Unlimited, joint and several; no formal protections |

| Local Presence | Registered office and domicile required in Uruguay | No registration; no formal office requirement |

| Capital | No statutory minimum; contributions recorded in partnership agreement | No formal capital structure required |

| Privacy | Partner names appear in public registry (Sociedad Colectiva) | No public record; privacy is incidental, not structural |

Focus Points

- Taxation: Both forms are subject to IRAE (Impuesto a las Rentas de las Actividades Económicas) at 25% on net income, IVA at the standard 22% rate, and applicable withholding taxes on distributions to non-resident partners.

- Annual Compliance: The Sociedad Colectiva must file annual accounts with the Auditoría Interna de la Nación (AIN) if it meets applicable thresholds; the Sociedad de Hecho has no formal compliance cycle but remains tax-liable.

- Treaty Access: Neither form guarantees access to Uruguay's tax treaty network; treaty eligibility depends on partner residency and the entity's tax treatment.

- Conversion: A Sociedad Colectiva can be converted into an SA or SRL through a formal transformation process under Law No. 16,060; conversion of a Sociedad de Hecho requires formalisation first.

- Restrictions: Neither structure is eligible for the SAFI or free trade zone regimes; use in regulated sectors such as banking or insurance is generally prohibited.

Sub-Types

Sociedad Colectiva (Registered General Partnership)

Formed by public deed and registered with the Registro Nacional de Comercio, this structure carries full legal personality and operates under a firm name that must include at least one partner's surname followed by "y Compañía" or equivalent.

Sociedad de Hecho (Informal Partnership)

This form arises from conduct rather than formal documentation. It is recognised under Law No. 16,060 for the purpose of attributing liability and tax obligations, but courts and creditors treat it as legally deficient — partners cannot invoke the entity's separate existence to shield personal assets.

When to Use These Structures

These forms are rarely selected for commercial ventures of any scale; they are more commonly encountered in inherited family businesses or transitional arrangements pending formalisation. The absence of limited liability is the defining constraint. The Sociedad Colectiva at least provides legal standing and a defined governance framework, while the Sociedad de Hecho offers neither.

These structures are most appropriate for small, closely-held family operations or short-term informal ventures where the parties accept full personal liability and formalisation is planned at a later stage.

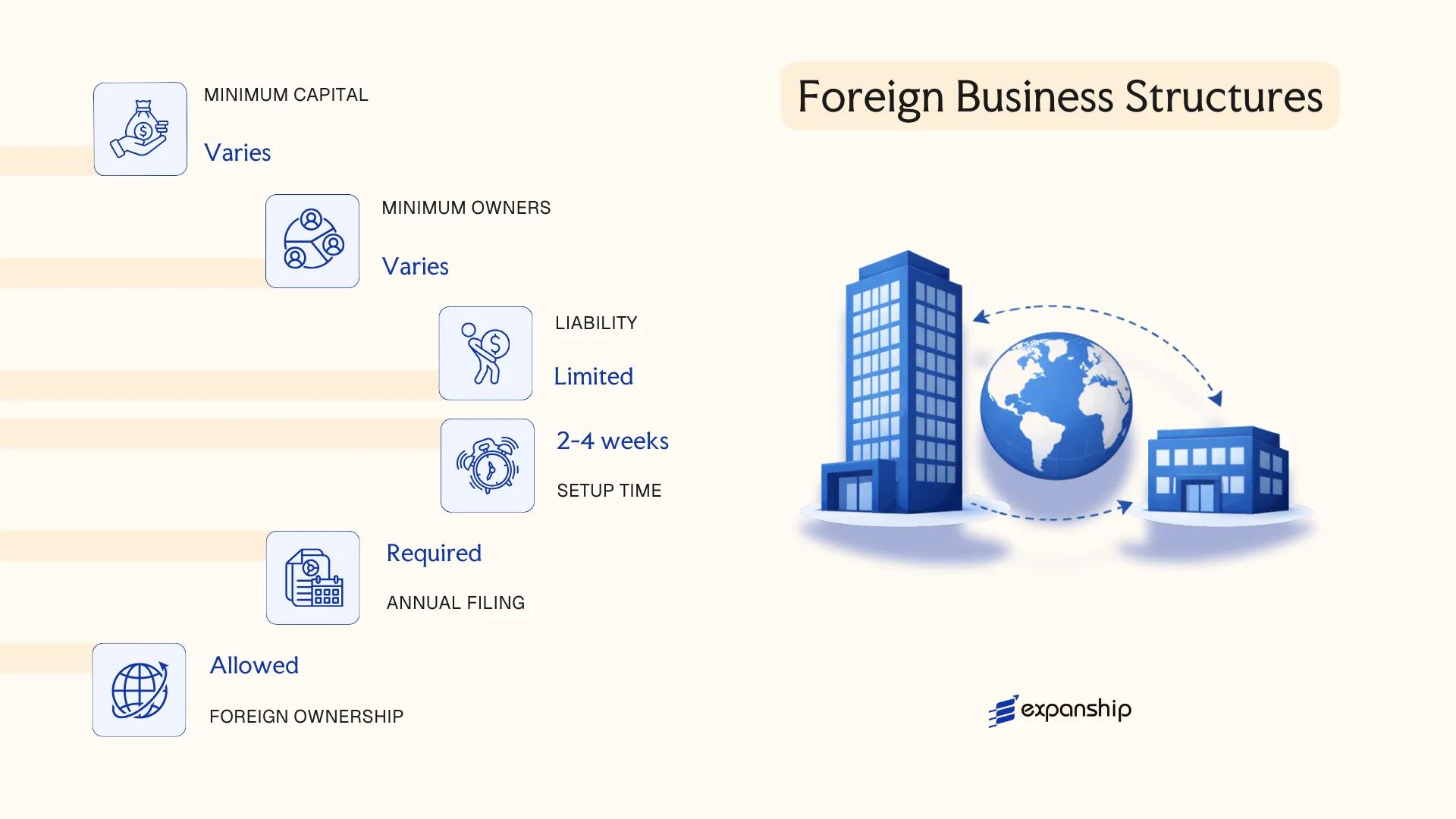

Foreign Business Structures in Uruguay [Branch Office, Representative Office, Subsidiary]

Foreign companies seeking to operate in Uruguay can do so through three primary structures: a branch office (sucursal), a representative office (oficina de representación), or a locally incorporated subsidiary. Establishing a foreign company branch office in Uruguay is governed by the Companies Law (Ley de Sociedades Comerciales No. 16.060 of 1989), which sets out the requirements for foreign entities to conduct activities within the country.

A branch is not a separate legal entity — it remains part of the parent company, which bears full liability for its operations. A subsidiary, by contrast, is incorporated as a distinct legal entity, typically as an SA or SRL, and carries its own legal personality.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Independent legal entity (SA or SRL) |

| Registered With | Auditoría Interna de la Nación (AIN) and Registro de Comercio | Registro de Comercio | Registro de Comercio / AIN |

| Local Presence | Registered address and appointed local legal representative required | Registered address required | Registered address; directors may be non-resident |

| Liability | Parent company bears unlimited liability | Parent company bears liability | Limited to entity's own assets |

| Capital | No minimum capital requirement | No minimum capital requirement | Varies by chosen entity form (SA or SRL) |

| Commercial Activity | Permitted | Not permitted; limited to promotion and liaison only | Fully permitted |

Focus Points

- Taxation: Branches and subsidiaries are subject to Corporate Income Tax (IRAE) at 25% on Uruguay-sourced income; VAT applies at 22% on local transactions; dividends remitted abroad attract a 7% withholding tax; representative offices generating no local income generally fall outside IRAE scope.

- Economic Substance: Branches engaged in commercial activity must maintain genuine operational presence; substance requirements are assessed in the context of tax residency and IRAE applicability.

- Annual Compliance: All structures must file annual accounts and renew registrations with the AIN and Registro de Comercio; branches must also submit audited financial statements of the parent company.

- Treaty Access: Subsidiaries incorporated as local entities may access Uruguay's tax treaty network more cleanly than branches, where treaty eligibility depends on the parent's jurisdiction of residence.

- Restrictions: Representative offices are explicitly prohibited from generating revenue or executing commercial contracts in-country.

Sub-Types

Branch Office (Sucursal)

A sucursal is authorised to conduct full commercial operations and must register with both the AIN and Registro de Comercio, appointing a local legal representative with sufficient authority to bind the parent. It is used when a foreign firm wants direct operational presence without incorporating a new entity.

Representative Office (Oficina de Representación)

This structure is restricted to promotional, market research, and liaison activities. It cannot sign commercial contracts or invoice clients locally, making it unsuitable for revenue-generating operations. Foreign firms use it primarily to test the market or coordinate regional activities.

Closing

A foreign business subsidiary registered in Uruguay as an SA or SRL is the most commonly used structure for trading, holding, or IP ownership, as it provides full liability separation from the parent. The primary drawback of a branch is the parent's unlimited exposure to local liabilities.

Foreign companies already operating in Latin America that require a compliant local presence for commercial activity without establishing a fully independent entity will find the branch structure practical; those seeking liability separation should register a subsidiary.

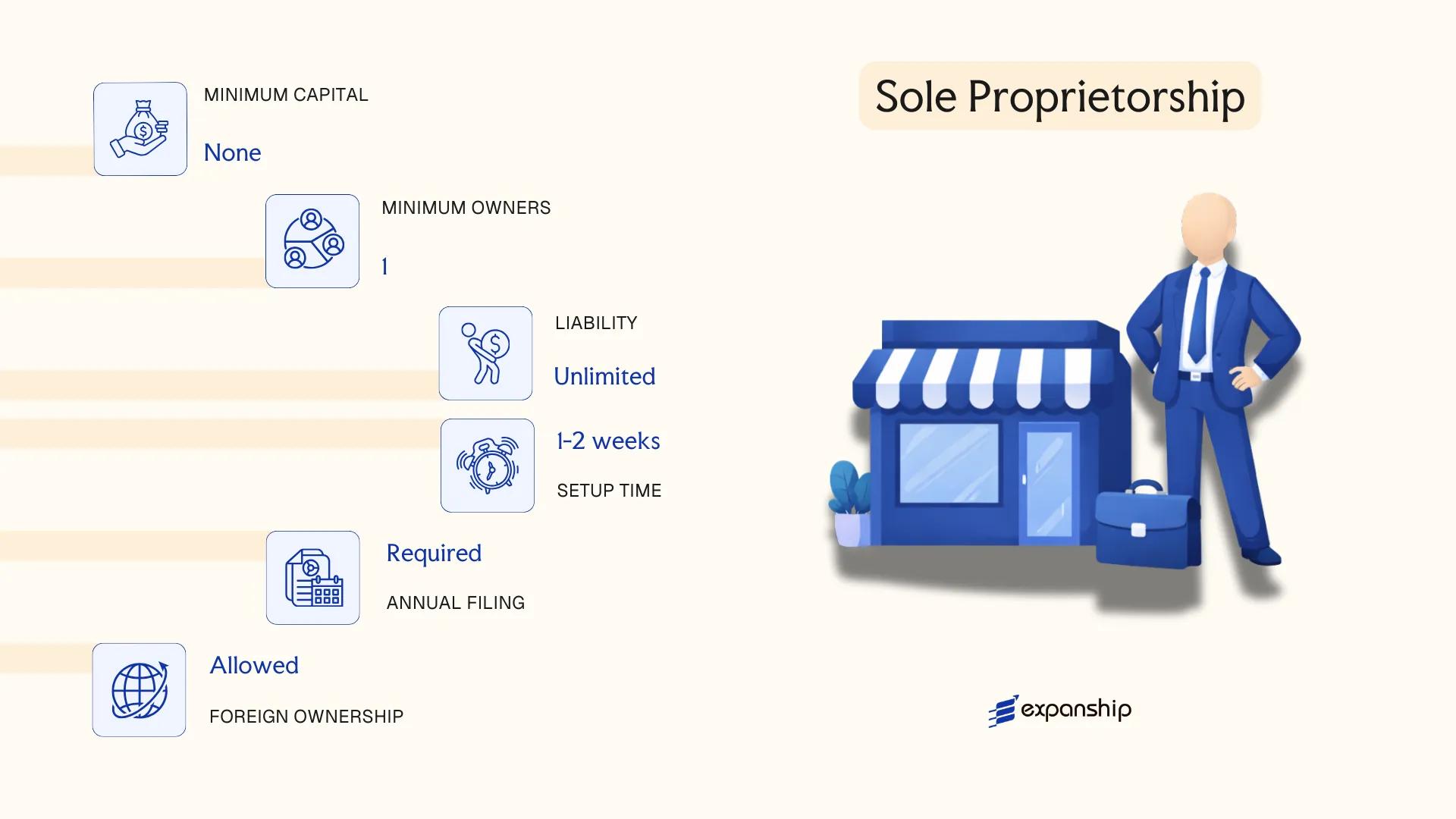

Sole Proprietorship (Empresa Unipersonal)

The Empresa Unipersonal Uruguay sole proprietorship is a one-person business structure in which the individual owner and the business are legally the same entity. No separate legal personality exists, meaning the proprietor bears unlimited personal liability for all commercial obligations.

Registration is conducted through the Dirección General Impositiva (DGI) for tax enrollment and, depending on the activity, may also require registration with the Banco de Previsión Social (BPS) for social security contributions. The process is relatively straightforward, but the absence of liability protection distinguishes this structure sharply from corporate forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (no separate legal personality) | Owner and business are legally indistinct |

| Members | Single natural person (proprietor) | Corporate owners not permitted |

| Local Presence | Registered address required | No statutory agent requirement, but a local fiscal address is needed for DGI |

| Capital | No minimum capital requirement | No formal paid-up capital obligation |

| Privacy | Owner's identity is disclosed in tax and social security registrations | No meaningful privacy from public records |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

Focus Points

- Taxation: Subject to IRAE (corporate income tax at 25%) if annual income exceeds the threshold for the simplified IMEBA regime; otherwise, smaller agricultural or low-turnover operations may qualify for IMEBA; also subject to IVA (VAT at 22% standard rate) and BPS contributions on the owner's deemed income.

- Annual Compliance: Annual tax declarations filed with DGI; BPS contributions payable monthly; no separate audited accounts required.

- Treaty Access: As a pass-through structure with no separate legal personality, access to Uruguay's tax treaty network is determined by the individual owner's residency status, not the business itself.

- Conversion: Can be converted into a formal corporate entity such as an SRL or SA, though this requires new registration procedures rather than a simple structural amendment.

- Restrictions: Cannot issue shares, admit additional owners, or raise equity capital; growth beyond a single owner necessitates adopting a different legal form.

Closing

This structure suits low-volume, owner-operated activities where administrative simplicity outweighs the need for liability protection or external investment capacity. The primary advantage is minimal setup cost and bureaucratic overhead; the clear drawback is unrestricted personal exposure to business liabilities.

Freelancers, consultants, and small traders operating in Uruguay who require a straightforward registration and do not anticipate taking on partners or significant commercial liabilities.

How to Choose the Right Entity Type in Uruguay

Selecting the correct legal structure before incorporation is not an administrative formality — it has direct legal, tax, and operational consequences that can be difficult or costly to reverse.

Why Your Entity Choice Matters

- Registering a tax-exempt entity under Uruguay's offshore regime when you intend to conduct local commercial activity places the business in breach of applicable regulations and can result in cancellation of registration by the Auditoría Interna de la Nación (AIN).

- Choosing a structure that does not qualify as a resident entity under Uruguayan domestic law means you cannot access withholding tax reductions available under Uruguay's double tax treaties with counterpart jurisdictions.

- Selecting a corporate structure when your objectives are succession planning or asset protection locks your business into annual shareholder meeting requirements and audited financial obligations that would not apply under a trust or foundation arrangement.

- Forming an SA when you operate as a sole consultant adds ongoing compliance costs — including potential external audit requirements — that are disproportionate to the scale of the activity.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated sectors such as banking or insurance each require distinct structural approaches under Uruguayan law.

- Ownership Configuration: A single-owner operation may suit an SRL or Empresa Unipersonal, while multi-party ventures requiring formal governance point toward an SA with a board structure.

- Tax Objectives: Your need for full exemption, a specific regime under the Impuesto a las Rentas de las Actividades Económicas (IRAE), or treaty access will each eliminate certain entity options.

- Privacy Requirements: SA bearer shares were abolished; shareholder disclosure is now required, so assess whether nominee structures are necessary for your ownership privacy needs.

- Substance Capacity: If you cannot maintain a physical presence, payroll, or local decision-making, confirm whether your chosen structure carries substance thresholds that trigger compliance failures.

- Exit Flexibility: Not all Uruguayan entities permit redomiciliation or conversion — verify the applicable rules under Ley No. 16.060 (Ley de Sociedades Comerciales) before committing to a structure.

Compliance Services for Companies in Uruguay

Ongoing corporate compliance support for Uruguayan entities, including AIN filings, annual renewals, and regulatory reporting.

Conclusion

Choosing the right structure is the first substantive decision in any incorporating a company in Uruguay guide, and the choice has lasting consequences for governance, liability, and tax treatment. The Sociedad Anónima remains the most widely registered entity, favored by foreign investors and domestic groups alike for its capital flexibility and bearer-share history, even after the 2012 transparency reforms under Law 18,930. The Sociedad de Responsabilidad Limitada suits closely held businesses with a fixed group of partners, while limited partnerships serve specialized arrangements where capital contributors and managing partners hold distinct roles. Sole proprietorships and informal structures carry unlimited personal exposure, making them appropriate only for small-scale, low-risk operations.

Uruguayan corporate regulation has trended toward greater disclosure and information exchange since its inclusion in OECD peer review processes, and that trajectory shows no signs of reversing. For your business, this means the compliance baseline continues to rise regardless of which entity you select.

How Expanship Can Assist You

Expanship's Uruguay company formation services are built around the specific entities and obligations covered in this guide. From registering a Sociedad Anónima or Sociedad de Responsabilidad Limitada with the Auditoría Interna de la Nación (AIN) to meeting ongoing compliance requirements under Uruguayan commercial law, our team handles the process end to end on your behalf.

Here is what our professional incorporation services in Uruguay cover:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Uruguay

- Filing and liaison with the AIN and the Registro Nacional de Comercio

- Post-incorporation compliance management, including annual filings

- Tax registration with the Dirección General Impositiva (DGI)

- Banking introduction assistance for newly incorporated entities

Ready to take the next step? Reach out to Expanship Uruguay to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (SA) is the most frequently incorporated structure, largely because it permits bearer or registered shares, accommodates an unlimited number of shareholders, and imposes no nationality restrictions on ownership. Its flexibility in capital structure makes it suitable across a wide range of commercial activities.

Both structures are subject to IRAE (Impuesto a las Rentas de las Actividades Económicas) on Uruguay-sourced income and carry similar annual compliance obligations with the Dirección General Impositiva (DGI). The practical distinction lies in governance: an SRL caps participation at 50 quotaholders and restricts free transfer of quotas, whereas an SA allows unrestricted share transfers and is the required form for publicly traded firms.

The SA, when structured with registered shares held through nominees, limits what appears in public filings with the Auditoría Interna de la Nación (AIN). Beneficial ownership information is reported to the Banco Central del Uruguay (BCU) under Law 19,484 but is not publicly accessible. Nominee shareholder arrangements are legally permissible.

Not across all structures. An SRL requires a minimum of two quotaholders, and a Sociedad Colectiva demands at least two partners by definition. An SA can theoretically be formed with a single shareholder in certain configurations, and an Empresa Unipersonal is, by nature, a sole-operator structure registered with the DGI.

Foreign nationals face no ownership restrictions across the SA, SRL, or branch office structures. A foreigner can hold 100% of shares in an SA or quotas in an SRL without establishing local residency, though a local legal representative (representante legal) is typically required for registered entities. Branch offices of foreign firms must register with the Registro de Comercio and appoint a local representative.

Uruguayan commercial law permits the transformation (transformación) of one entity type into another without dissolving the original legal person, provided the process complies with the Ley de Sociedades Comerciales (Law 16,060). An SRL can be converted into an SA, for example, subject to notarial deed requirements and re-registration with the Registro de Comercio. Not all conversions are equally straightforward, and some require creditor notification periods.

A Sociedad de Hecho does not. This informal partnership lacks legal personality under Law 16,060, meaning partners bear unlimited joint liability for the firm's obligations. All formally registered structures, including the SA, SRL, and both comandita variants, obtain separate legal personality upon completion of Registro de Comercio registration.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.