Key Takeaways

- Entity formation in the United States is administered at the state level through offices such as the Delaware Division of Corporations or the California Secretary of State, while the Internal Revenue Service separately determines federal tax classification.

- The C Corporation is the preferred structure for businesses seeking outside investment or access to public markets, whereas the S Corporation is restricted to closely held domestic companies that meet strict IRC eligibility requirements.

- LLCs are the most widely registered entity type across most US states, combining flexible management structures with default pass-through tax treatment.

- Delaware, Wyoming, and Nevada continue to refine their formation statutes to attract both domestic and foreign registrants, reflecting ongoing state-level competition in corporate services.

Introduction to Entity Types in the United States

Choosing among the types of business entities in the United States requires an understanding of how federal and state-level legal frameworks interact. Unlike many jurisdictions with a single national registry, entity formation in the US is administered at the state level — each state maintains its own Secretary of State office (or equivalent agency) that handles registration, such as the Delaware Division of Corporations or the California Secretary of State. Federal bodies, including the Internal Revenue Service, then determine how a registered entity is classified for tax purposes.

The US tax system is residence- and citizenship-based for individuals, while corporate tax treatment depends on entity type and elections made at formation. This creates meaningful variation in how different structures are taxed.

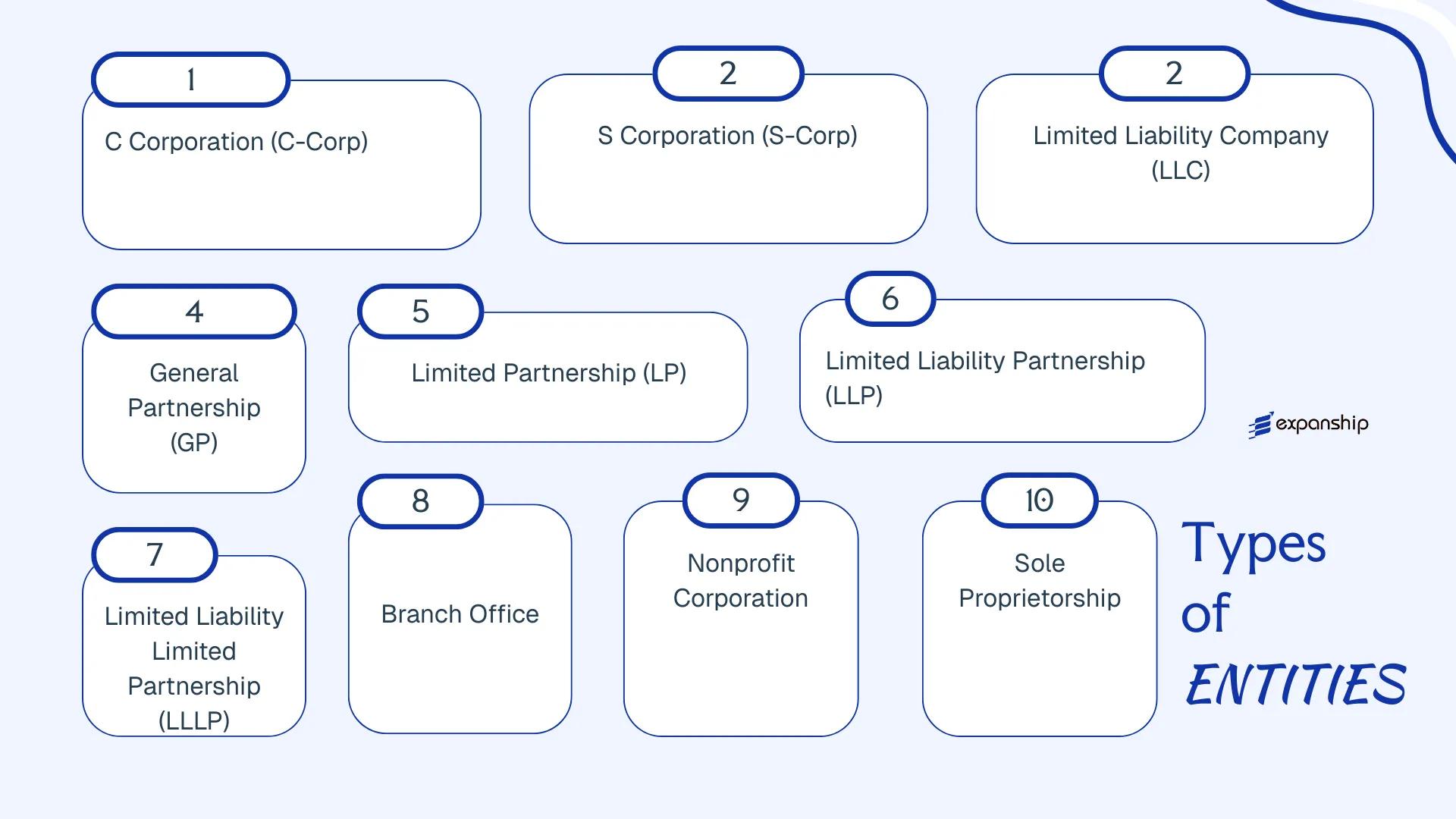

Entities available under American company structures include the C Corporation, S Corporation, Limited Liability Company, General Partnership, Limited Partnership, Limited Liability Partnership, Limited Liability Limited Partnership, Foreign Corporation, Foreign LLC, Branch Office, Nonprofit Corporation, and Sole Proprietorship. Each carries distinct implications for liability, taxation, governance, and compliance. This article examines each structure in detail to help you determine which formation type suits your business objectives.

An Overview of Business Structures in the United States

Several distinct entity types are available under American company law, each governed by a combination of federal statutes and state-level legislation. The Internal Revenue Code governs federal tax treatment across all structures, while formation and governance rules are established at the state level — Delaware's General Corporation Law and the Uniform Limited Liability Company Act, adopted in various forms across states, are two of the most referenced frameworks. Each structure carries different implications for liability, taxation, ownership, and governance.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| C Corporation | Separate legal entity | Limited | Entity-level tax | Permitted | 1 shareholder | Secretary of State | State Corporation Law |

| S Corporation | Separate legal entity | Limited | Pass-through | Permitted | 1–100 shareholders | IRS + Secretary of State | IRC Subchapter S |

| LLC | Hybrid entity | Limited | Flexible / Pass-through | Permitted | 1 member | Secretary of State | State LLC Act |

| General Partnership | Unincorporated | Unlimited | Pass-through | Permitted | 2 partners | State authority | State Partnership Law |

| Limited Partnership | Unincorporated | Mixed | Pass-through | Permitted | 1 GP + 1 LP | Secretary of State | ULPA |

| LLP | Unincorporated | Limited | Pass-through | Permitted | 2 partners | Secretary of State | State LLP Act |

| LLLP | Unincorporated | Limited | Pass-through | Permitted | 1 GP + 1 LP | Secretary of State | State LLLP Act |

| Nonprofit Corporation | Separate legal entity | Limited | Tax-exempt (IRC 501(c)) | Restricted | 1 director | Secretary of State / IRS | State Nonprofit Law |

| Sole Proprietorship | Unincorporated | Unlimited | Personal income tax | Permitted | 1 owner | None required | N/A |

| Foreign Corporation | Registered foreign entity | Limited | Varies | Permitted | Per home jurisdiction | Secretary of State | State Foreign Qualification |

| Foreign LLC | Registered foreign entity | Limited | Varies | Permitted | Per home jurisdiction | Secretary of State | State Foreign Qualification |

| Branch Office | Extension of parent | Parent liable | Parent-level | Permitted | N/A | Secretary of State | State law |

Each of these structures is examined in full in the sections below.

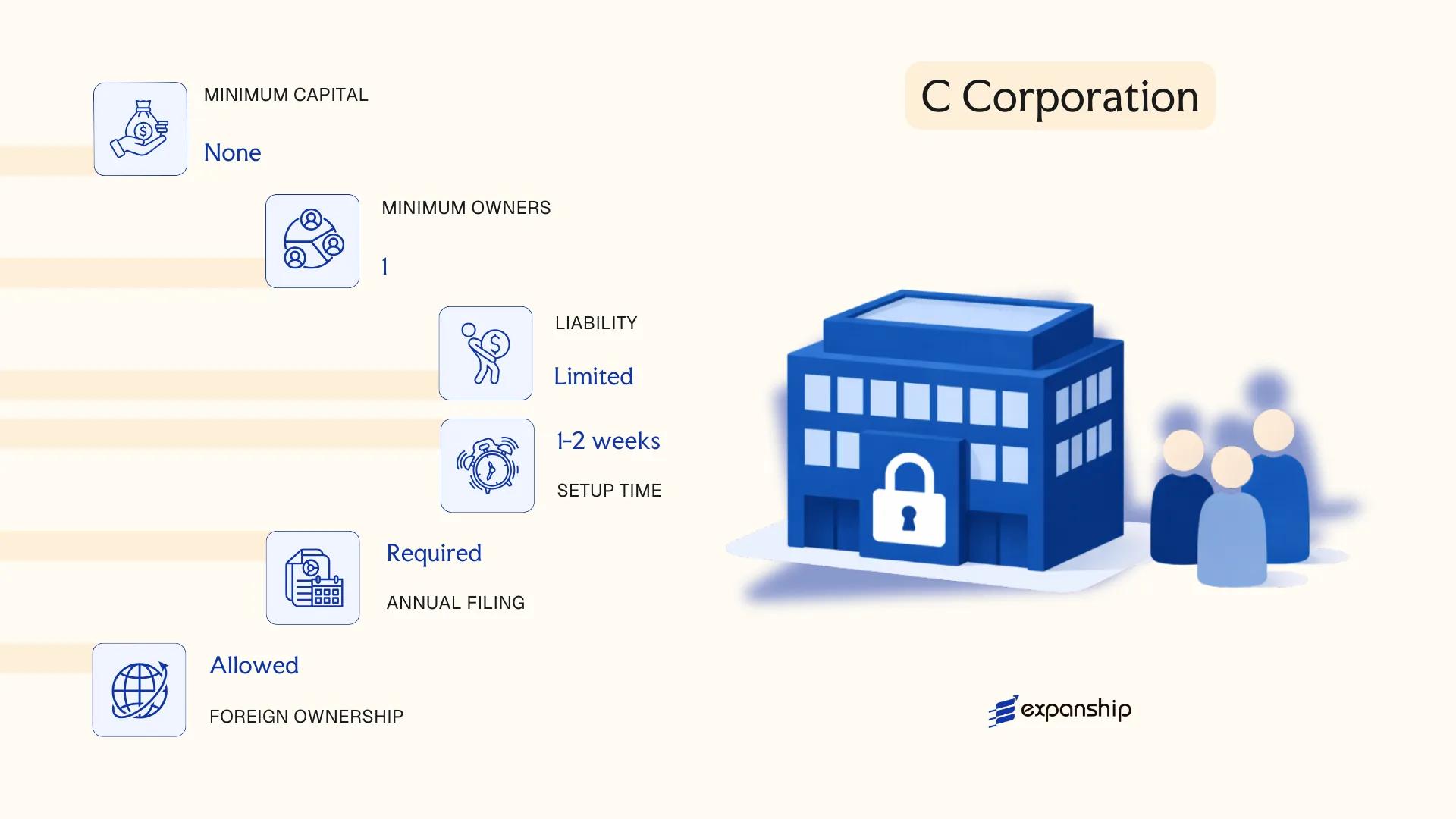

C Corporation (C-Corp)

C corporation formation in the United States is governed primarily by state-level corporate statutes — Delaware's General Corporation Law (DGCL) being the most widely adopted framework — rather than a single federal act. Each state maintains its own incorporation statute, though the structural principles are broadly consistent.

A C-Corp is a separate legal entity distinct from its shareholders, capable of entering contracts, holding assets, and incurring liabilities in its own name. Shareholders bear no personal liability beyond their capital contribution.

Company Incorporation in the United States

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Stock corporation | Incorporated at state level; Delaware, Wyoming, and Nevada are common choices |

| Members | Shareholders, Directors, Officers | No maximum on shareholders; minimum one director and one shareholder required |

| Local Presence | Registered Agent required in state of incorporation | Physical office not mandatory, but a registered agent with a local address is |

| Capital | USD; no statutory minimum | Authorized share capital defined in the Articles of Incorporation |

| Privacy | Directors and officers typically disclosed in state filings | Beneficial ownership disclosure now required federally under the Corporate Transparency Act (CTA) |

Focus Points

- Taxation: Subject to federal corporate income tax at a flat 21% rate under the Internal Revenue Code; state-level corporate taxes apply separately; dividends distributed to shareholders are taxed again at the individual level, creating double taxation; no VAT at the federal level, though sales tax applies at the state level; withholding tax on dividends paid to foreign shareholders varies by applicable tax treaty.

- Annual Compliance: Annual reports and franchise taxes are due to the state of incorporation; federal tax returns filed on Form 1120 with the IRS.

- Treaty Access: Qualifies as a resident entity for purposes of U.S. tax treaty benefits, subject to limitation-on-benefits (LOB) provisions in applicable treaties.

- Conversion: Can convert to an LLC or S-Corp under most state statutes, though tax consequences at the federal level must be assessed prior to conversion.

- Foreign Ownership: No restrictions on foreign shareholders, making it a common structure for non-U.S. founders accessing American markets.

Closing

C-Corps are used for venture-backed startups, publicly traded companies, U.S. holding structures, and businesses seeking investment from institutional or foreign investors. The ability to issue multiple classes of stock is a structural advantage; the double taxation of distributed profits is a concrete drawback for businesses intending to distribute earnings regularly.

C-Corps are most appropriate for businesses planning to raise institutional capital, list publicly, or accommodate foreign shareholders without restriction.

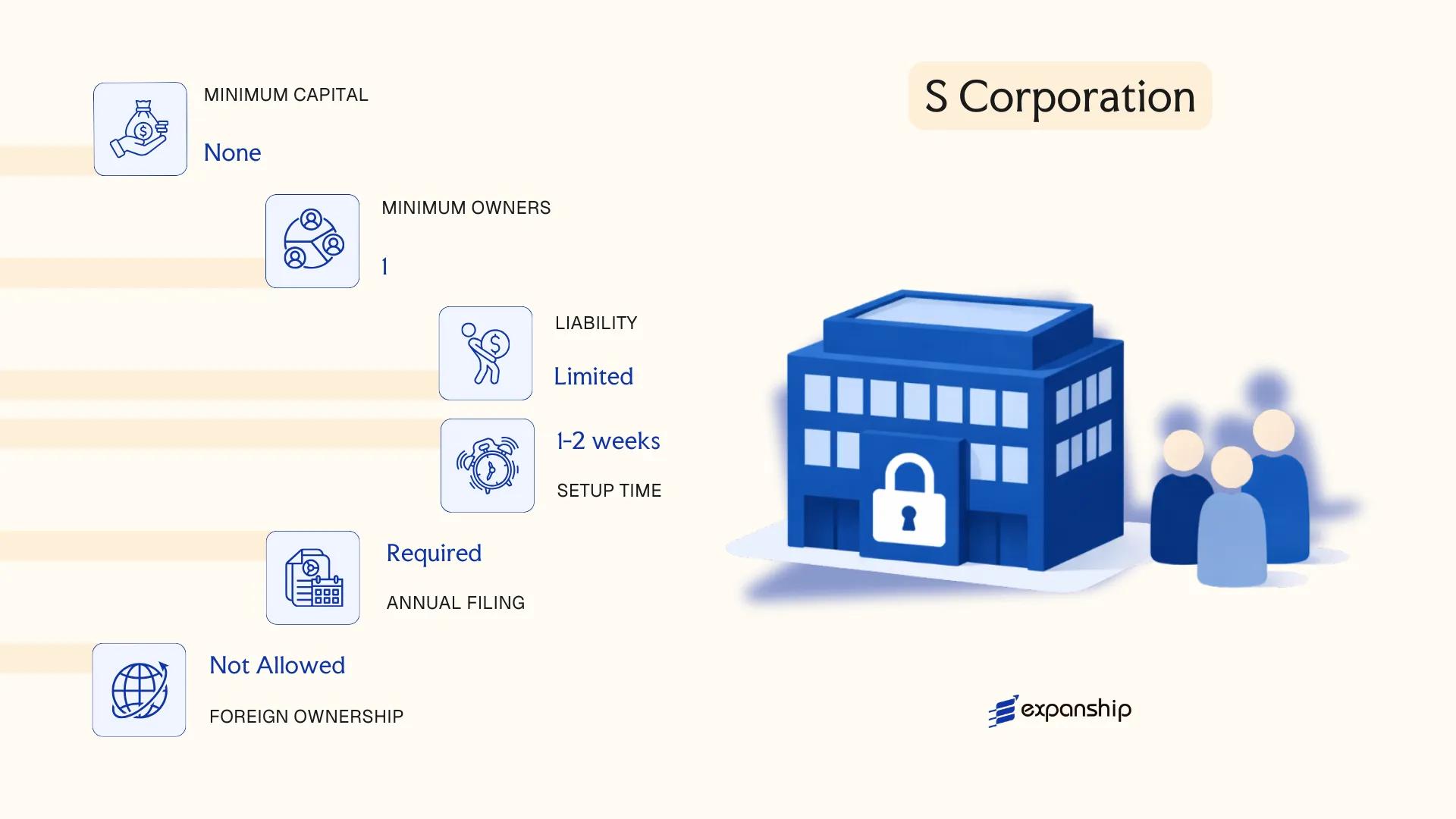

S Corporation (S-Corp)

Governed by Subchapter S of the Internal Revenue Code, the S Corporation structure dates to the Small Business Tax Revision Act of 1958. Like a C-Corp, it is a separate legal entity incorporated under state law, offering shareholders limited liability protection. The defining feature is its federal tax election status: the S-Corp itself does not pay federal income tax. Instead, income, losses, deductions, and credits pass through to shareholders' personal returns.

Meeting S corporation requirements United States federal law imposes is mandatory before the IRS accepts an election filed on Form 2553. The entity must be a domestic corporation, and all shareholders must consent to the election in writing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation with S-election (state-incorporated) | Incorporated at state level; federal S-status granted by IRS |

| Members | Shareholders only; 1–100 maximum | Only individuals, certain trusts, and estates permitted as shareholders |

| Shareholder Restrictions | US citizens or permanent residents only | Non-resident aliens are prohibited as shareholders |

| Share Classes | One class of stock only | Voting rights may differ; economic rights must be identical |

| Local Presence | Registered Agent required in state of incorporation | Registered office address mandatory |

| Privacy | Shareholder information filed with the state | Public disclosure varies by state |

Focus Points

- Taxation: Pass-through federal taxation at shareholder level; no federal corporate income tax on the entity; state-level treatment varies by jurisdiction — some states do not recognise the S-election.

- Annual Compliance: Must file Form 1120-S annually with the IRS; state annual reports and fees apply separately.

- Shareholder Eligibility: S-Corp eligibility rules USA law sets prohibit foreign shareholders, corporate shareholders, and most partnerships from holding shares.

- Conversion: An S-Corp can voluntarily revoke its election or involuntarily lose it if eligibility requirements are breached; conversion to C-Corp status follows automatically.

- Self-Employment: Shareholder-employees must receive reasonable compensation subject to payroll taxes before taking remaining profit as distributions.

Recommendations

The S-Corp suits small-to-medium domestic businesses seeking S corporation pass-through taxation in America while retaining a corporate structure, though the 100-shareholder ceiling and the prohibition on foreign ownership make it unsuitable for businesses with international investors or scaling equity requirements.

US-resident founders running a closely held domestic business who want to reduce self-employment tax exposure through a salary-plus-distribution structure.

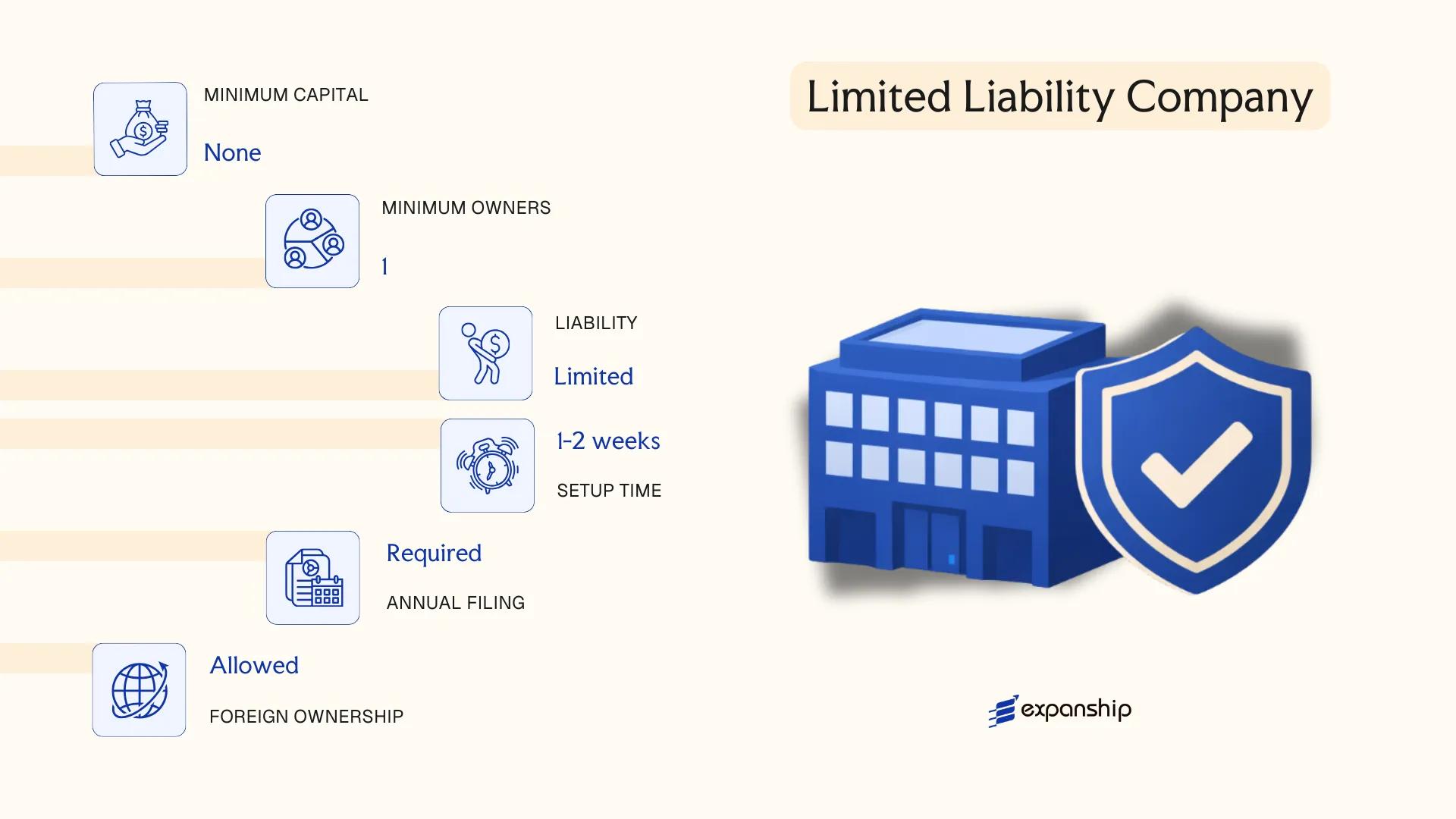

Limited Liability Company (LLC)

Governing legislation for LLC formation in the United States varies by state, as each jurisdiction enacts its own LLC statute — for example, Delaware's Limited Liability Company Act (Title 6, Chapter 18) and Wyoming's Limited Liability Company Act (W.S. 17-29-101 et seq.). First introduced in Wyoming in 1977, the LLC has since become the most widely used business structure across all fifty states.

Structurally, an LLC is a separate legal entity distinct from its members, combining limited liability protection with pass-through taxation by default. This hybrid nature makes it adaptable to both single-owner operations and multi-party ventures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Governed by state-level LLC statutes; no single federal LLC law |

| Members | Referred to as Members | No minimum or maximum member count in most states; single-member LLCs are permitted |

| Management | Member-managed or Manager-managed | Managers need not be members; structure is defined in the Operating Agreement |

| Local Presence | Registered Agent required in state of formation | Physical street address mandatory; PO boxes not accepted |

| Capital | No minimum capital requirement; USD | Contributions can be cash, property, or services |

| Privacy | Varies by state | Wyoming and New Mexico allow high member anonymity; Delaware requires a registered agent but not member disclosure |

Focus Points

- Taxation: LLCs are pass-through by default (single-member treated as disregarded entity; multi-member as partnership); eligible to elect C-Corp or S-Corp taxation via IRS Form 8832 or 2553; no federal-level LLC tax, though some states impose franchise taxes or gross receipts taxes (e.g., California's $800 annual minimum franchise tax).

- Annual Compliance: Most states require an annual or biennial report filed with the Secretary of State, along with applicable renewal fees.

- Operating Agreement: Not universally mandated by statute, but California, New York, Missouri, Maine, and Delaware require one in some form; it governs internal affairs and member rights regardless of legal requirement.

- Conversion: Most states permit statutory conversion from an LLC to a corporation or other entity type without dissolution, subject to state-specific procedures.

- Foreign Registration: Operating in states outside the formation state requires foreign qualification, filed with the target state's Secretary of State.

Sub-Types

Series LLC

Authorized in Delaware, Illinois, Texas, Nevada, and several other states, a Series LLC allows a single LLC to establish internally segregated "series," each with its own assets, liabilities, and members. Used primarily for real estate portfolios or investment funds where asset separation is desired without forming multiple entities.

Professional LLC (PLLC)

A PLLC is formed specifically for licensed professionals — such as attorneys, physicians, or accountants — in states that restrict standard LLCs from providing regulated professional services. Members must hold the relevant state-issued professional license.

An LLC suits a wide range of uses — trading operations, holding structures, and IP ownership — owing to its flexible governance and pass-through taxation. Its primary limitation is inconsistent treatment across states, which can complicate multi-state operations and foreign qualification requirements.

LLCs are well-suited for small to mid-sized businesses, real estate investors, and foreign entrepreneurs seeking a flexible US structure with limited liability and minimal formality requirements.

Partnerships [General Partnership, Limited Partnership (LP), Limited Liability Partnership (LLP), Limited Liability Limited Partnership (LLLP)]

Among the types of partnerships in the United States, four main structures exist: the General Partnership (GP), Limited Partnership (LP), Limited Liability Partnership (LLP), and Limited Liability Limited Partnership (LLLP). Each is governed primarily by state law, with most states adopting versions of the Uniform Partnership Act (1997), the Revised Uniform Limited Partnership Act (2001), or the Uniform Limited Liability Partnership Act.

Partnerships are generally pass-through entities without federal-level separate legal personality in the tax sense, though LPs, LLPs, and LLLPs do provide varying degrees of liability protection. Formation requirements, liability shields, and partner roles differ meaningfully across these four structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual association of two or more persons | Governed by state statute; partnership agreement strongly recommended |

| Members Referred To As | General Partners and/or Limited Partners | GPs manage and bear unlimited liability; LPs are passive with limited liability |

| Membership | Minimum 2 partners; no statutory maximum | GP requires at least 1 GP; LP requires at least 1 GP and 1 LP |

| Local Presence | Registered Agent required for LP, LLP, LLLP; GP may vary by state | Principal place of business address generally required on file |

| Capital | No federally mandated minimum; denominated in USD | Contributions can be cash, property, or services |

| Privacy | Partner names may appear in public filings for LP, LLP, LLLP | GP formation often requires no state filing, offering more informal privacy |

Focus Points

- Taxation: Partnerships file an informational federal return (Form 1065); income passes through to partners and is taxed at individual or corporate rates — no entity-level federal income tax. State-level taxes, franchise fees, and withholding on foreign partners under FIRPTA or IRC Section 1446 may apply.

- Annual Compliance: LPs, LLPs, and LLLPs must file annual or biennial reports with the state of formation; GPs generally have no mandatory state filing unless registered.

- Foreign Partners: Partnerships with non-US partners must withhold tax on effectively connected income under IRC Section 1446; treaty benefits may reduce withholding rates depending on the partner's jurisdiction.

- Conversion: Most states permit statutory conversion between partnership types, or to an LLC or corporation, under their respective business organization statutes.

- LLP Restrictions: Several states restrict LLP registration to licensed professionals such as attorneys, accountants, and architects.

Sub-Types

General Partnership (GP)

A GP arises automatically when two or more persons co-own a business for profit, even without a written agreement or state filing. Every general partner carries unlimited personal liability for the firm's obligations, making this structure uncommon for high-risk commercial activity.

Limited Partnership (LP)

An LP separates management from investment: general partners manage operations and bear unlimited liability, while limited partners contribute capital and enjoy liability protection proportional to their investment. This structure is frequently used in private equity funds, real estate ventures, and family limited partnerships.

Limited Liability Partnership (LLP)

An LLP grants all partners a liability shield against the negligence or misconduct of co-partners, while each partner remains liable for their own acts. In several states, registration is restricted to professional service firms operating under a licensed practice.

Limited Liability Limited Partnership (LLLP)

The LLLP extends a liability shield to general partners, a protection not available in a standard LP. Not all states recognize the LLLP — adoption remains uneven, so verifying the state of formation's statute before structuring is necessary.

Closing

Partnerships suit joint ventures, professional practices, real estate holdings, and fund structures where pass-through taxation and flexible profit allocation are priorities. The primary limitation is that at least one general partner in a GP or LP bears unlimited personal liability unless an LLLP or corporate GP structure is used.

Partnerships are best suited for two or more co-owners, investors, or professionals seeking pass-through taxation and flexible governance, particularly in real estate, private equity, or licensed professional services.

Foreign and Out-of-State Entities [Foreign Corporation, Foreign LLC, Branch Office]

Foreign entity registration in the United States applies to any business formed outside a given state that seeks to conduct business within that state's borders. Each state treats such entities under its own statutes — for example, California's Foreign Corporations Act under the California Corporations Code, or Delaware's provisions under Title 8 of the Delaware Code — though the underlying federal framework treats the entity as a legal person for jurisdictional purposes.

A company incorporated in one state but operating in another must formally qualify as a foreign entity in each additional state. This process does not create a new legal entity; it extends authorization to an existing one.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign Corporation or Foreign LLC | Determined by the entity's home-state formation document |

| Local Presence | Registered Agent required in each qualifying state | Must have a physical address in that state; a PO box is not accepted |

| Filing Body | Secretary of State (or equivalent) in each state | Filing names vary: e.g., "Application for Authority" in New York |

| Capital | No minimum capital requirement at federal level | Individual states may impose franchise tax based on authorized shares or net worth |

| Privacy | Beneficial ownership disclosed per FinCEN under the Corporate Transparency Act 2024 | State-level disclosure varies |

| Members / Officers | Directors and officers for corporations; members or managers for LLCs | No residency requirement at federal level, though some states differ |

Focus Points

- Taxation: Subject to state corporate income tax or franchise tax in each qualifying state; federal tax treatment follows the home entity's classification; no separate federal registration tax applies.

- Annual Compliance: Annual or biennial reports required in each qualifying state, with fees and deadlines varying by jurisdiction.

- Economic Substance: No federal economic substance regime for foreign-qualified entities, but states may scrutinize genuine business activity for nexus purposes.

- Withdrawal: Formal withdrawal or cancellation filings are required in each state to terminate foreign qualification and stop ongoing compliance obligations.

- Branch Office: A branch is not a separate legal entity and does not provide liability separation from the parent company; it is the same legal person operating in a new location.

Sub-Types

Foreign Corporation

A corporation formed in one state — or outside the country — that registers to do business in another state. Qualification is triggered by a legal standard of "transacting business," defined differently across states but generally excluding isolated transactions or interstate commerce.

Foreign LLC

An LLC organized under another state's limited liability company act that obtains authority to operate in a new state. The foreign LLC retains its home-state governance structure; the qualifying state does not impose a new operating agreement requirement.

Branch Office

A branch office represents the parent entity directly and carries no independent legal personality. Liability for branch operations rests with the parent company, making this structure less common for risk management purposes.

When to Use

Foreign qualification suits businesses expanding operations across state lines while maintaining a single legal entity. The primary limitation is cumulative compliance cost: each qualifying state imposes its own filing fees, annual reports, and tax obligations.

Foreign qualification is best suited for established businesses expanding into new states that want to avoid forming separate subsidiaries in each jurisdiction.

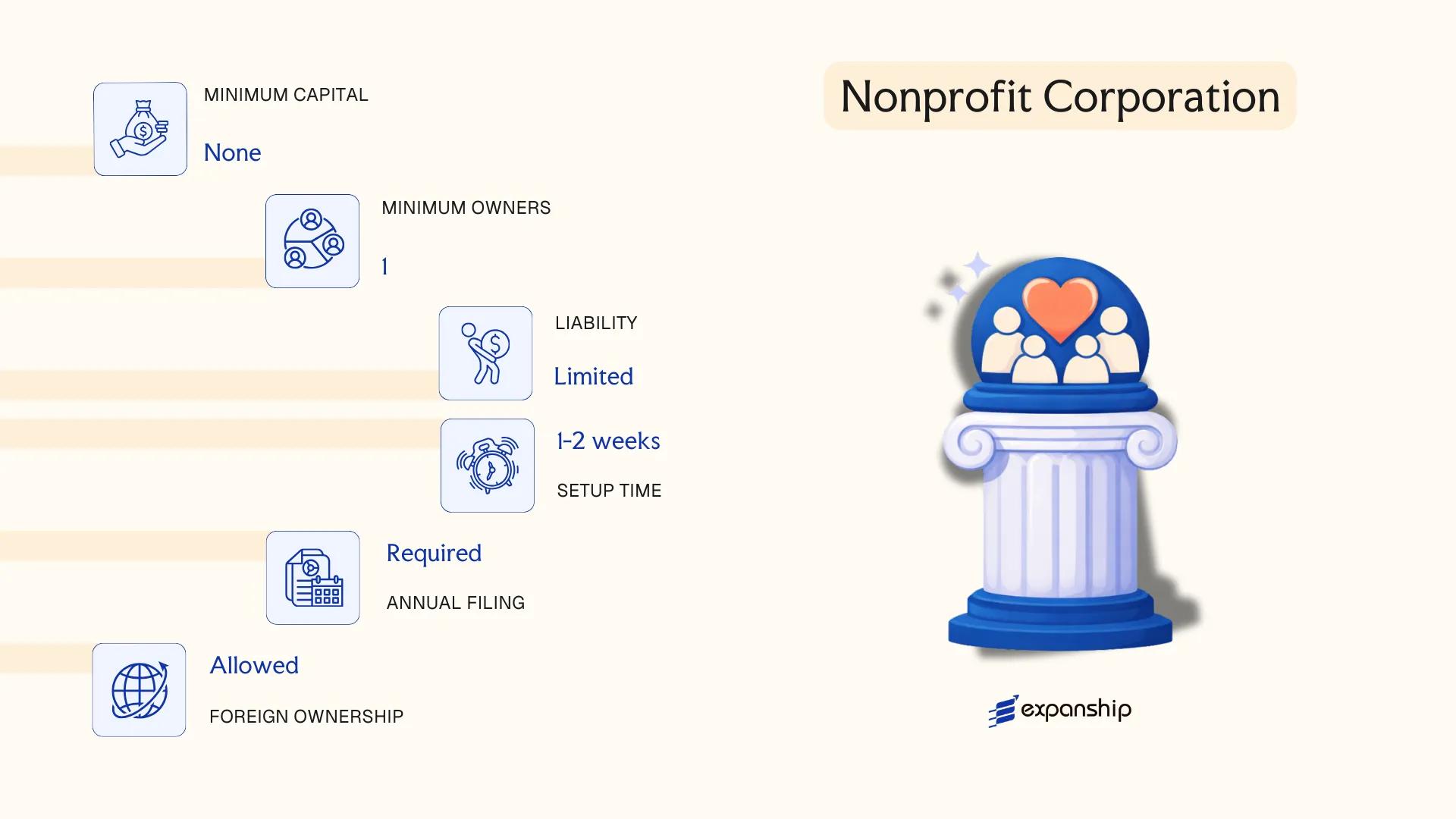

Nonprofit Corporation

Nonprofit corporation formation in the United States is governed primarily by individual state nonprofit corporation acts, with most states modeling their statutes on the Model Nonprofit Corporation Act (MNCA), last revised in 2008. The entity holds separate legal personality distinct from its members, and directors and officers bear limited personal liability for organizational debts.

Federal tax-exempt status is obtained separately through the Internal Revenue Service. Filing Form 1023 or the streamlined Form 1023-EZ with the IRS is required to apply for recognition under Section 501(c)(3) of the Internal Revenue Code, which applies to charitable, religious, educational, and scientific organizations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Nonprofit Corporation | Incorporated at state level; federal tax-exempt status applied separately |

| Members / Governance | Directors, Officers, and optionally Members | Board of Directors required; membership structure is optional depending on state law |

| Minimums | At least 1 Director (3 recommended by IRS for 501c3) | No maximum; no shareholders |

| Local Presence | Registered Agent and Registered Office in state of incorporation | Required in every state where the entity operates |

| Capital | No minimum capital; no share capital | Cannot distribute profits to members or directors |

| Privacy | Officers and directors typically disclosed in state filings | Some states allow nominee directors |

Focus Points

- Taxation: Exempt from federal corporate income tax under IRC 501(c)(3); donors may deduct contributions; unrelated business income taxed at standard corporate rates; no VAT equivalent at federal level; state tax exemptions vary and require separate applications.

- Annual Compliance: Annual or biennial state reports required; IRS Form 990 (or 990-EZ / 990-N depending on revenue) must be filed annually.

- Restrictions: Prohibition on private inurement; lobbying and political campaign activity are strictly limited under IRC 501(c)(3).

- Dissolution: Assets must be distributed to another tax-exempt organization upon dissolution; cannot revert to founders or directors.

- Conversion: Converting a nonprofit to a for-profit entity is permitted in some states but triggers regulatory scrutiny and potential tax consequences.

Sub-Types

Public Charity

Receives a substantial portion of funding from the public or government and is subject to less restrictive self-dealing rules under IRC 509(a). This is the most common classification for organizations conducting direct charitable programs.

Private Foundation

Typically funded by a single source such as an individual, family, or corporation, and primarily makes grants to other organizations rather than conducting programs directly. Subject to stricter IRS oversight, including excise taxes on investment income and mandatory minimum distribution requirements.

Nonprofit corporations are most commonly used for charitable, educational, religious, and advocacy purposes where public benefit is the primary objective. The 501(c)(3) designation enables access to tax-deductible donations and grants, though the prohibition on profit distribution makes this structure unsuitable for any revenue-generating business with investor returns.

Organizations pursuing charitable, educational, or religious missions that require donor tax deductions and grant eligibility.

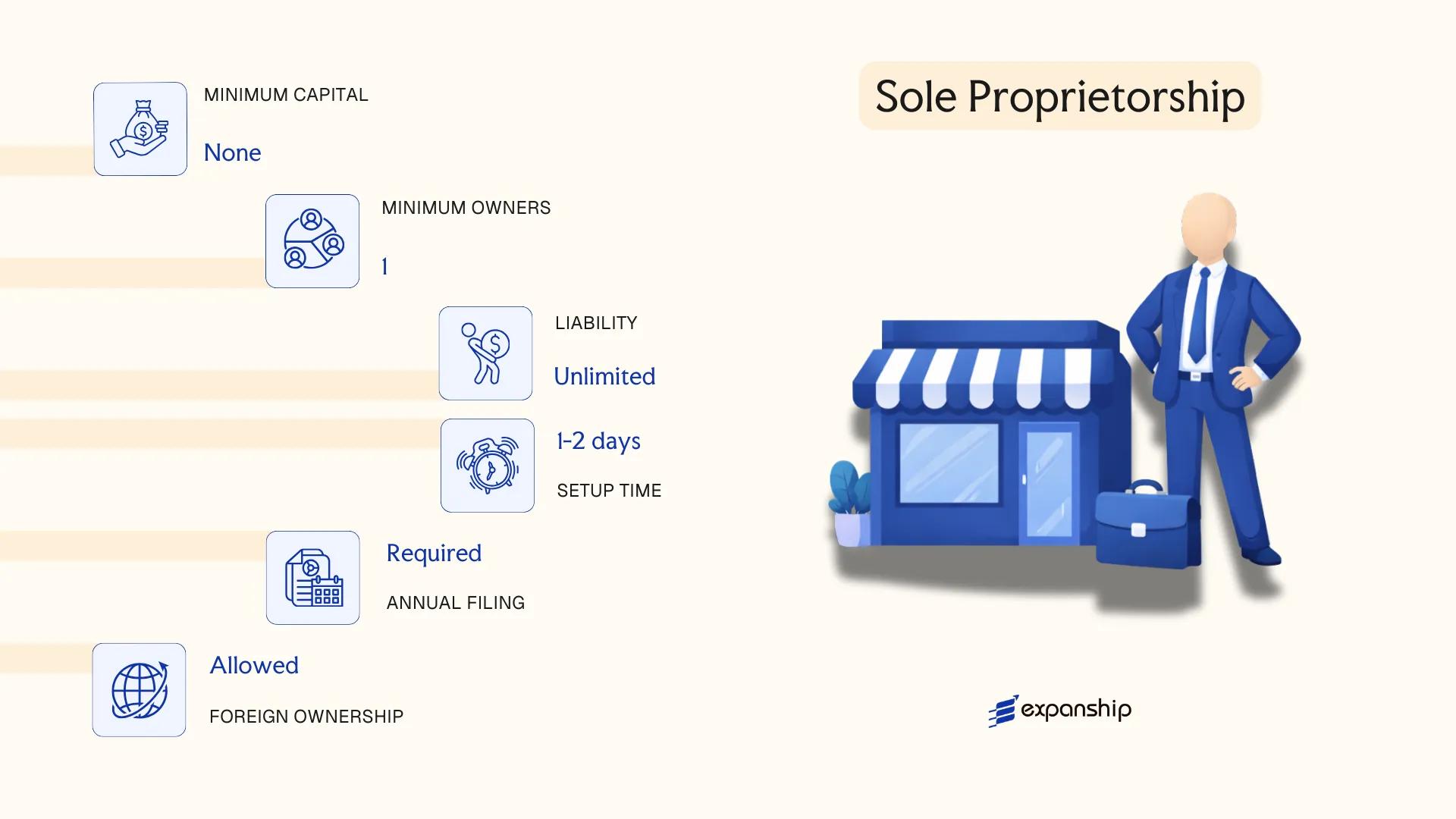

Sole Proprietorship

A sole proprietorship in the United States is the simplest and most common form of business structure, operating without a formal incorporation statute at the federal level. Unlike corporations or LLCs, it is not a separate legal entity from its owner — the business and the individual are legally identical, meaning the owner bears unlimited personal liability for all debts and obligations.

No state registration is required to establish this structure, though operating under a name other than your own legal name requires filing a "Doing Business As" (DBA) or fictitious business name registration with the relevant county clerk or state agency, depending on the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Sole Proprietor | Single individual only; no co-owners permitted |

| Membership | 1 (minimum and maximum) | Adding a co-owner converts the structure to a partnership |

| Local Presence | DBA filing with county clerk or state agency (if trading under a fictitious name) | Requirements vary by state and county |

| Capital | No minimum; no formal capitalization requirement | No statutory currency or amount prescribed |

| Privacy | Owner's name is public if DBA is filed | No formation documents filed at state level otherwise |

Focus Points

- Taxation: Business income is reported on the owner's personal federal return via Schedule C (Form 1040); subject to self-employment tax (15.3% on net earnings up to the Social Security wage base, 2.9% Medicare above that); no corporate income tax, no withholding tax at entity level, and no federal sales tax (state/local sales tax obligations depend on the state).

- Annual Compliance: No annual reports or state-level filings required for the entity itself; DBA registrations may require periodic renewal depending on state rules.

- Conversion: Converting to an LLC or corporation requires formal registration with the relevant state agency; assets and liabilities must be transferred, as there is no statutory conversion mechanism for a sole proprietorship.

- Restrictions: Cannot issue shares, raise equity from investors, or have multiple owners without changing the entity type.

- Treaty Access: As a pass-through structure with no separate legal identity, the entity itself cannot access US tax treaties; treaty benefits, if any, apply to the individual owner based on their own residency status.

A sole proprietorship suits freelancers, independent contractors, and single-owner micro-businesses testing a market with minimal administrative overhead. The absence of formation costs and ongoing compliance obligations is a practical advantage, but unlimited personal liability remains a significant structural risk for any business with meaningful revenue, contracts, or employees.

Sole proprietorships are most appropriate for individual operators with low liability exposure and no immediate need for outside investment or formal business credit.

How to Choose the Right Entity Type in the United States

Selecting the wrong structure from the outset creates legal and financial consequences that can be difficult and costly to reverse. Knowing how to choose a business entity in the United States requires mapping your specific operational, tax, and ownership requirements against what each structure actually permits under state and federal law.

Why Your Entity Choice Matters

The structure you register shapes your legal exposure, tax position, and administrative burden from day one. Selecting the wrong form can produce concrete outcomes:

- Forming a C-Corp when pass-through taxation is your goal still subjects corporate profits to federal corporate income tax at 21%, creating double taxation before any distribution reaches shareholders.

- Choosing an LLC taxed as a disregarded entity when you require access to US tax treaty benefits may disqualify you, since treaty eligibility often depends on entity classification under the relevant treaty's Limitation on Benefits clause.

- Registering as a foreign corporation to do business across state lines without filing a Foreign Qualification in each state of operation constitutes unauthorized practice under most states' business corporation acts, exposing the entity to back taxes, penalties, and potential loss of standing to sue.

- Selecting an S-Corp structure when your ownership includes non-resident alien shareholders violates the eligibility restrictions under 26 U.S.C. § 1361, rendering the election invalid.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or investment advising each point toward distinct structures — regulated activities often require specific entity forms to obtain the relevant federal or state license.

- Ownership Composition: Non-resident alien owners cannot hold S-Corp shares, making an LLC or C-Corp the only viable options for internationally held businesses.

- Tax Classification: Your required tax treatment — corporate taxation, pass-through, or disregarded entity status — determines whether an LLC, partnership, or corporation is structurally appropriate.

- Management Flexibility: If you prefer to avoid board formalities and annual meeting requirements, an LLC governed by an Operating Agreement offers significantly more flexibility than a corporation subject to state corporate statutes.

- Exit and Conversion: Not all states permit statutory conversion between entity types; if you anticipate restructuring, confirm in advance whether your chosen state's law accommodates that process.

- Interstate Operations: Transacting business in multiple states requires Foreign Qualification filings in each state, which adds registration fees, registered agent obligations, and ongoing compliance costs per jurisdiction.

The primary federal reference governing corporate tax classification is the Internal Revenue Code, while entity formation is governed at the state level — Delaware's General Corporation Law and LLC Act remain the most widely referenced state statutes for US entity structuring.

Compliance Services for Companies in the United States

Ongoing compliance support for US-registered entities, including annual report filings, registered agent maintenance, and state-level regulatory obligations.

Conclusion

Incorporating a business in the United States requires selecting a structure that matches your operational model, liability tolerance, and tax position. The C Corporation suits companies seeking outside investment or a path to public markets, while the S Corporation fits closely held domestic businesses that prefer pass-through taxation within strict eligibility limits. LLCs remain the most widely registered entity type across most states, valued for their flexible management and default pass-through treatment. General and limited partnerships serve specific co-ownership arrangements, and nonprofit corporations address mission-driven activities under IRC Section 501(c).

Regulatory trends point toward continued state-level competition on formation fees and reporting requirements, with Delaware, Wyoming, and Nevada refining their statutes to attract domestic and foreign registrants. The network of US tax treaties continues to influence how foreign-owned entities are structured. Expanship works directly with these formation and compliance frameworks on your behalf.

How Expanship Can Assist You

Expanship US company formation services cover the full spectrum of entity types discussed in this blog — from Delaware C-Corps and Wyoming LLCs to registered limited liability partnerships and foreign qualification filings. Each structure carries distinct formation requirements, tax elections, and ongoing obligations governed at both the federal level and within individual state agencies such as the Secretary of State's office. Expanship works with your business to align the right structure with your operational and ownership profile before a single document is filed.

Our team handles every administrative and regulatory step on your behalf:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered office provision across all 50 states

- State agency filing and liaison with the relevant Secretary of State

- Federal EIN registration with the IRS

- Post-incorporation compliance management, including annual reports and franchise tax filings

- Banking introduction assistance for both domestic and international clients

Reach out to Expanship United States to discuss your entity setup.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently formed entity across most states. Its pass-through taxation under federal tax rules and limited personal liability make it the default choice for small businesses, startups, and foreign-owned ventures alike.

A C-Corp is taxed as a separate entity under Subchapter C of the Internal Revenue Code, subjecting profits to corporate-level tax before any shareholder distributions. An LLC, by default, is treated as a pass-through for federal tax purposes, avoiding that second layer of taxation. Both structures permit foreign ownership, but only a C-Corp can issue multiple classes of stock and qualify for institutional investment or an IPO.

An LLC generally provides greater ownership privacy than a corporation, particularly in states such as Wyoming and New Mexico, where member names are not required in public filings. Registered agent services are used in place of direct officer disclosure. Nominee member arrangements are legally permissible in certain states, though they do not override federal beneficial ownership reporting requirements under the Corporate Transparency Act.

A sole proprietorship and single-member LLC both require only one individual. A General Partnership requires at least two partners, and an S-Corp requires at least one shareholder but no more than 100. Certain entity types, such as the LLLP, require both a general and limited partner, making solo formation structurally impossible.

A C-Corp, LLC, LP, and LLP can all be formed by non-US citizens and non-residents without restriction under state incorporation statutes. An S-Corp is the notable exception: nonresident aliens are prohibited from holding S-Corp shares under IRC Section 1361(b)(1)(C). Foreign founders should also account for federal Employer Identification Number (EIN) requirements and potential withholding obligations under FIRPTA.

Most states permit statutory conversion between entity types, for example from an LLC to a corporation, without dissolving and re-forming the business. The process is governed by state-level conversion statutes, and the converted entity retains its contracts, assets, and liabilities. Federal tax classification may change upon conversion, which can trigger recognition events under the Internal Revenue Code.

Corporations, LLCs, LPs, and LLPs are recognized as legally distinct from their owners under state law, meaning they can hold property, enter contracts, and be sued in their own name. A General Partnership lacks a formal registration requirement in most states and, depending on state law, may or may not be treated as a separate legal person. Sole proprietorships have no legal separation from the owner whatsoever.

A single-member LLC in a state with no annual franchise tax or report requirement, such as New Mexico, carries minimal ongoing obligations at the state level. By contrast, corporations in states like California or Delaware face annual franchise taxes, mandatory officer disclosures, and board resolutions. Across all entity types, federal filing obligations, including income tax returns and beneficial ownership reports under the Corporate Transparency Act, apply regardless of state.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.