Key Takeaways

- The Ministry of Justice of Ukraine administers the Unified State Register of Legal Entities, Individual Entrepreneurs, and Public Organizations, making it the central authority for company registration across all entity types.

- Ukraine's dominant incorporation vehicle is the Limited Liability Company (TOV), which suits small to mid-sized businesses by capping owner liability without the disclosure obligations imposed on Joint Stock Companies (AT).

- Foreign entities entering Ukraine through a representative or branch office face restrictions on operational scope in exchange for a comparatively lighter registration process.

- Ukraine's EU candidacy status is driving incremental corporate governance and reporting reforms, as the country continues aligning its regulatory framework with European standards.

Introduction to Entity Types in Ukraine

Ukraine is an independent sovereign state in Eastern Europe, bordered by Poland, Slovakia, Hungary, Romania, Moldova, Belarus, and Russia. For businesses looking to establish a legal presence there, understanding the types of business entities in Ukraine is a necessary starting point — the country's corporate law distinguishes between several distinct legal forms, each governed by different rules on liability, ownership, and governance.

Company registration falls under the authority of the Ministry of Justice of Ukraine, which administers the Unified State Register of Legal Entities, Individual Entrepreneurs, and Public Organizations. Tax residency follows a standard territorial and resident-based model, with corporate income tax applying to resident entities on worldwide income.

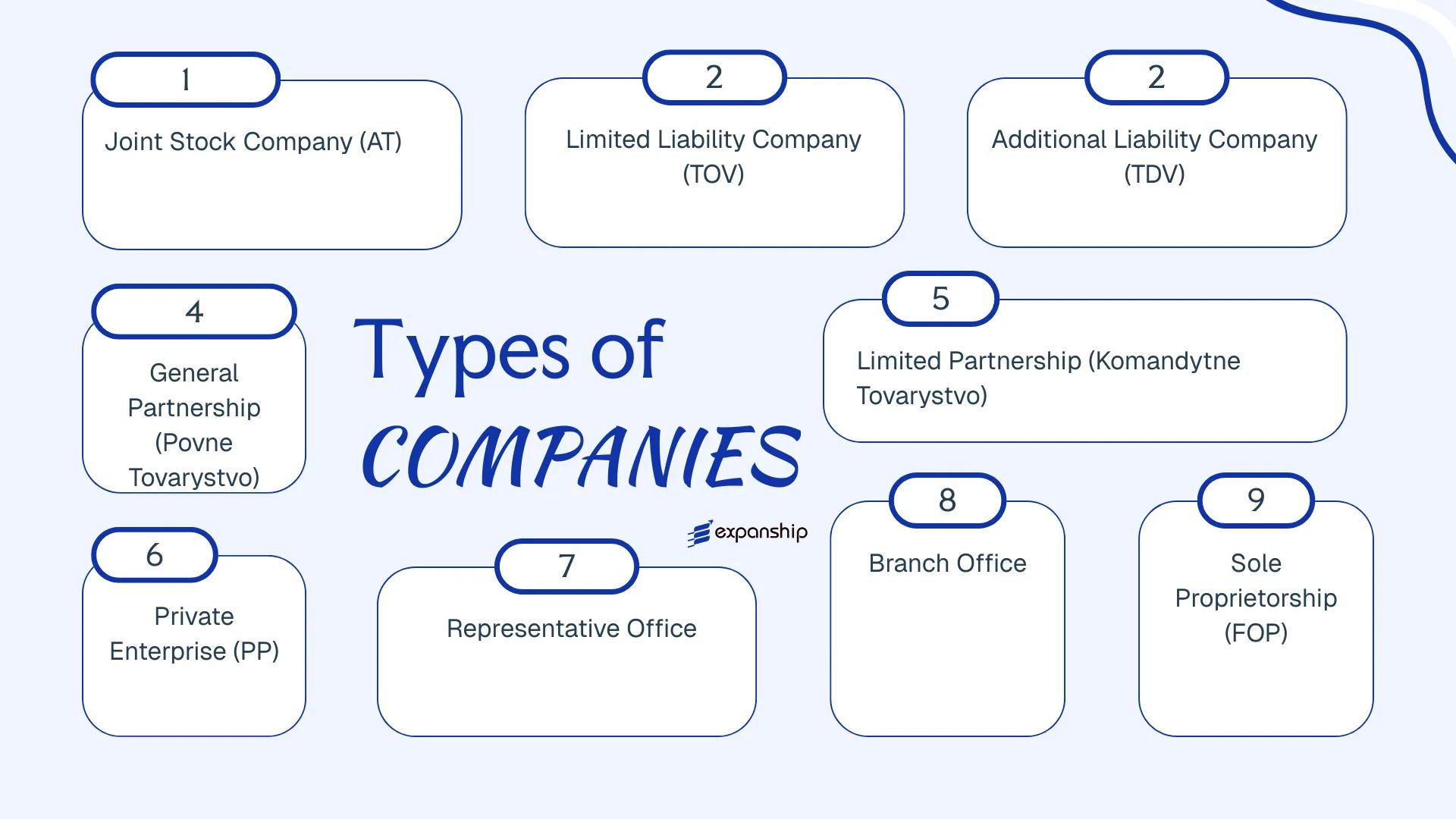

The Ukrainian legal entity forms available to domestic and foreign investors include:

- Joint Stock Company (AT)

- Limited Liability Company (TOV)

- Additional Liability Company (TDV)

- General Partnership (Povne Tovarystvo)

- Limited Partnership (Komandytne Tovarystvo)

- Private Enterprise (PP)

- Representative Office

- Branch Office

- Sole Proprietorship (FOP)

Each of these business structures available in Ukraine carries specific incorporation requirements, capital obligations, and operational implications that this article examines in detail.

An Overview of Business Structures in Ukraine

Ukrainian company law recognises several distinct entity types, each governed primarily by the Civil Code of Ukraine, the Commercial Code of Ukraine, and specific legislation such as the Law of Ukraine "On Limited Liability Companies and Additional Liability Companies" (No. 2275-VIII) and the Law of Ukraine "On Joint Stock Companies." An overview of business structures in Ukraine shows that available forms range from fully incorporated companies with limited liability to unincorporated sole proprietorships and foreign presence structures. Each form carries different implications for ownership, liability, and taxation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (AT) | Corporate | Limited to share capital | Taxable | Permitted | 1 shareholder | State Securities Commission | Law on Joint Stock Companies |

| Limited Liability Company (TOV) | Corporate | Limited to contribution | Taxable | Permitted | 1 member | State Registrar | Law No. 2275-VIII |

| Additional Liability Company (TDV) | Corporate | Subsidiary personal liability | Taxable | Permitted | 1 member | State Registrar | Law No. 2275-VIII |

| General Partnership (Povne Tovarystvo) | Partnership | Unlimited, joint | Taxable | Permitted | 2 participants | State Registrar | Commercial Code |

| Limited Partnership (Komandytne Tovarystvo) | Partnership | Mixed | Taxable | Permitted | 2 participants | State Registrar | Commercial Code |

| Private Enterprise (PP) | Unincorporated entity | Owner-defined | Taxable | Permitted | 1 owner | State Registrar | Commercial Code |

| Representative Office | Foreign presence | Parent liable | Taxable (limited) | Restricted | N/A (parent company) | Ministry of Economy | Cabinet of Ministers Regulation |

| Branch Office | Foreign presence | Parent liable | Taxable | Permitted | N/A (parent company) | State Registrar | Civil Code |

| Sole Proprietorship (FOP) | Individual | Unlimited personal | Taxable / Simplified | Permitted | 1 individual | State Registrar | Tax Code of Ukraine |

Each of these structures is examined in full in the sections below.

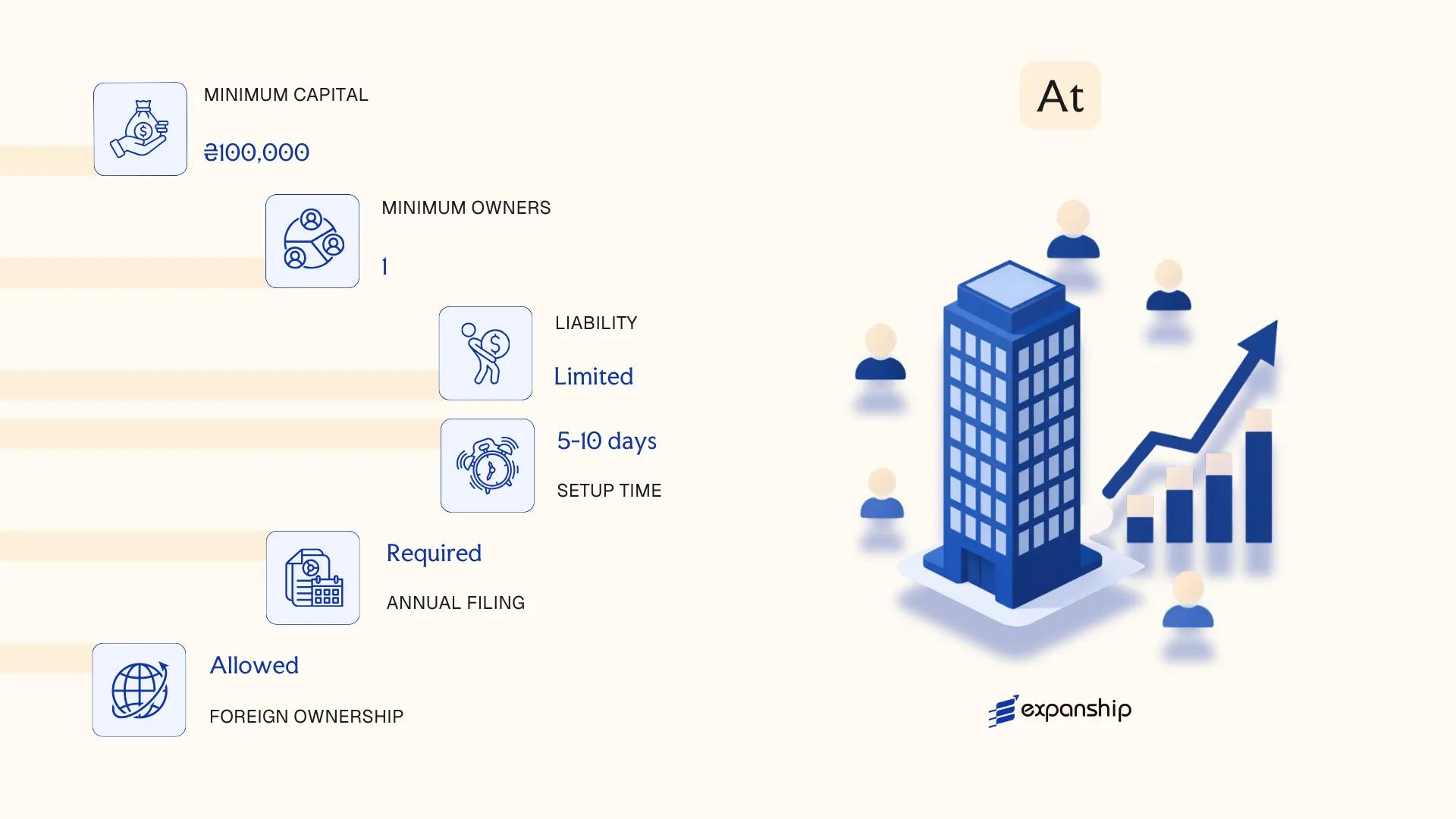

Joint Stock Company (Aktsionerne Tovarystvo — AT)

Governed by the Law of Ukraine "On Joint Stock Companies" (No. 514-VI, 2008, as subsequently amended), the joint stock company Ukraine AT registration process produces a distinct legal entity with full separate legal personality. Shareholders bear liability only to the extent of their subscribed shares.

Capital is divided into shares of equal nominal value, and the entity can attract investment from a broad pool of subscribers. This hybrid structure suits both closely held ownership arrangements and wider public participation, depending on the sub-type selected.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (AT) | Separate legal entity under Ukrainian civil law |

| Members | Shareholders | No maximum; minimum 1 shareholder for private AT, no ceiling for public AT |

| Governing Bodies | Supervisory Board, Executive Body, General Meeting | Supervisory Board mandatory for public ATs; optional for private ATs below certain thresholds |

| Local Presence | Registered legal address in Ukraine required | No mandatory local director requirement under general rules |

| Capital | Minimum UAH 1,250 minimum wages for public AT; UAH 625 minimum wages for private AT | Expressed in Ukrainian hryvnia; share nominal value must be uniform |

| Privacy | Shareholder register maintained by a licensed depositary institution | Register is not fully public but accessible to authorised parties |

Focus Points

- Taxation: Subject to corporate profit tax at 18%, standard VAT at 20% on applicable supplies, and withholding tax (generally 15%, reduced under applicable double tax treaties) on dividends, royalties, and interest paid to non-residents.

- Annual Compliance: Mandatory annual financial reporting, statutory audit (compulsory for public ATs), and filing with the State Tax Service and the National Securities and Stock Market Commission (NSSMC).

- Treaty Access: As a Ukrainian tax resident entity, the AT can access Ukraine's network of double taxation agreements, subject to beneficial ownership and substance requirements.

- Conversion: An AT may be reorganised into another legal form, including a TOV, through a statutory reorganisation procedure under the Civil Code and the Companies Act.

- Securities Regulation: Share issuance must be registered with the NSSMC; any public offering is subject to prospectus requirements and ongoing disclosure obligations.

Sub-Types

Public Joint Stock Company (Publichne AT — PAT)

A PAT may offer shares through public subscription and list on a Ukrainian stock exchange. Stricter disclosure, mandatory annual audit, and NSSMC reporting requirements apply.

Private Joint Stock Company (Pryvatne AT — PrAT)

Share transfers in a PrAT are restricted and cannot be offered to the general public. This structure suits concentrated ownership among a defined group of investors without public market obligations.

Closing Note

The AT suits large enterprises, holding structures, and businesses planning to access capital markets or accommodate institutional investors; its primary drawback is the comparatively heavier regulatory and administrative burden relative to other Ukrainian entity forms.

The AT is most appropriate for large-scale ventures, institutional investment vehicles, or businesses anticipating future equity fundraising or stock exchange participation.

Company Incorporation in Ukraine

Incorporate a Joint Stock Company or other entity type in Ukraine with end-to-end support from Expanship.

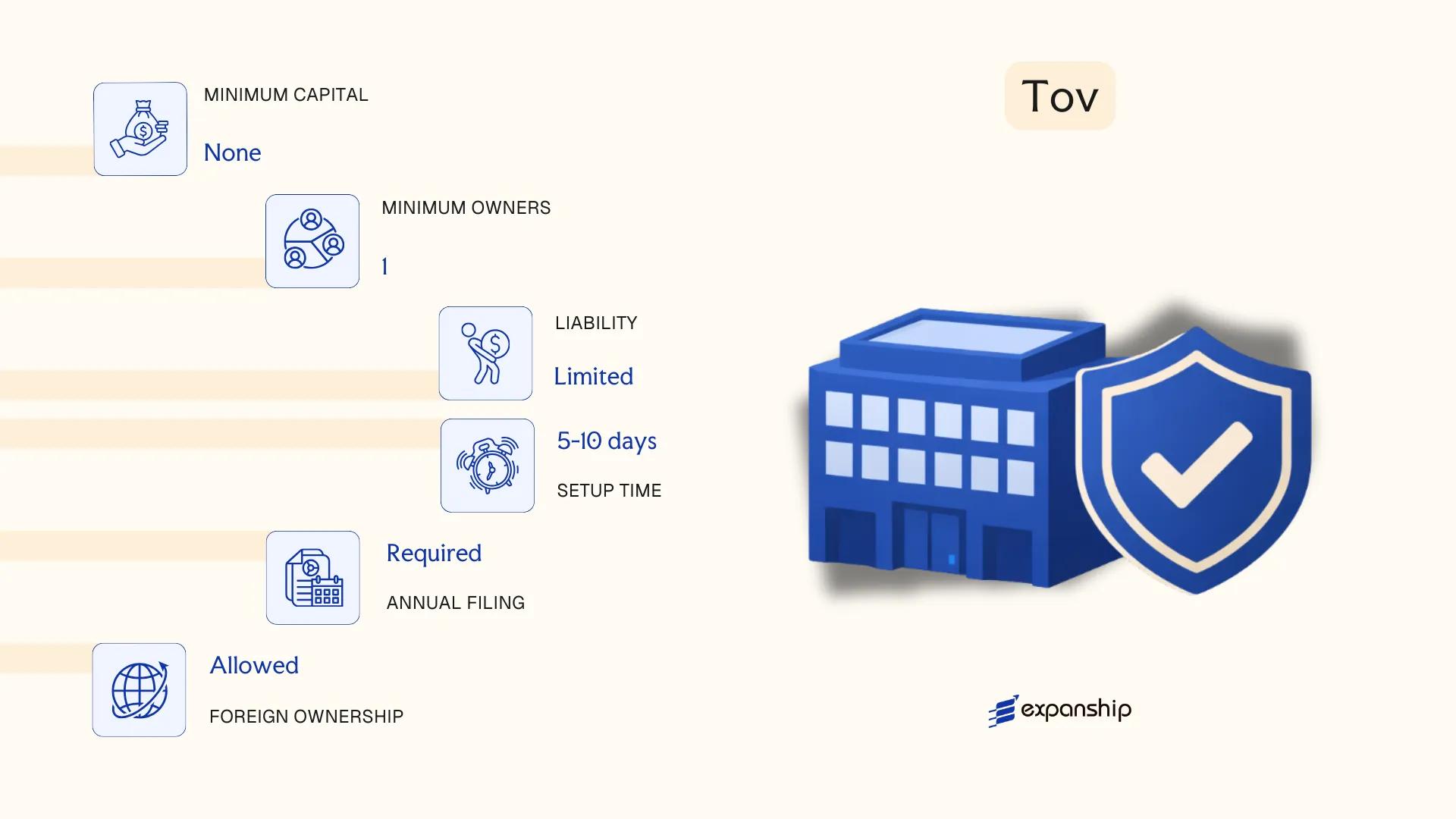

Limited Liability Company (Tovarystvo z Obmezhenoyu Vidpovidalnistyu — TOV)

Governed by the Law of Ukraine "On Limited Liability Companies and Additional Liability Companies" No. 2275-VIII (2018), the TOV is the most widely used commercial structure for limited liability company Ukraine TOV formation. It holds separate legal personality, meaning the entity owns assets, enters contracts, and bears obligations in its own name.

Liability of each participant is capped at the value of their contributed share in the charter capital. This hybrid nature, combining corporate-style liability protection with relatively flexible internal governance, makes the TOV a practical vehicle for a broad range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (TOV) | Separate legal personality; governed by Law No. 2275-VIII |

| Members | Participants (uchasnyky); 1–100 | Referred to as "participants," not shareholders; exceeding 100 requires conversion |

| Management | Director (single) or Board of Directors | A Supervisory Board is optional unless required by charter |

| Capital | No statutory minimum; denominated in UAH | Contributions can be monetary or in-kind; value assessed by participants |

| Local Presence | Registered legal address in Ukraine required | No mandatory resident director; address must be a physical location |

| Privacy | Participant details filed with the Unified State Register | Register is publicly accessible via the Ministry of Justice portal |

Focus Points

- Taxation: Subject to corporate income tax at 18%; VAT at 20% applies once annual turnover exceeds UAH 1 million; dividends paid to non-residents attract 15% withholding tax (reduced under applicable tax treaties); no stamp duty on share transfers.

- Annual Compliance: Financial statements must be prepared; entities meeting size thresholds are subject to statutory audit under Ukrainian accounting standards.

- Treaty Access: As a Ukrainian tax resident, the TOV can access Ukraine's network of double tax treaties, subject to beneficial ownership requirements.

- Conversion: A TOV may be reorganised into a joint stock company (AT) or other permitted legal form through a formal reorganisation procedure under the Civil Code of Ukraine.

- Participant Restrictions: Foreign nationals and legal entities may hold participant interests; however, certain regulated sectors impose restrictions on foreign ownership.

Closing

The TOV suits trading operations, holding structures, and service businesses where operational control and liability separation are priorities. Its governance flexibility is a clear advantage, though the public disclosure of participant information through the Unified State Register limits confidentiality.

The TOV is best suited for foreign investors and domestic entrepreneurs establishing a closely held operating or holding company with a defined group of participants.

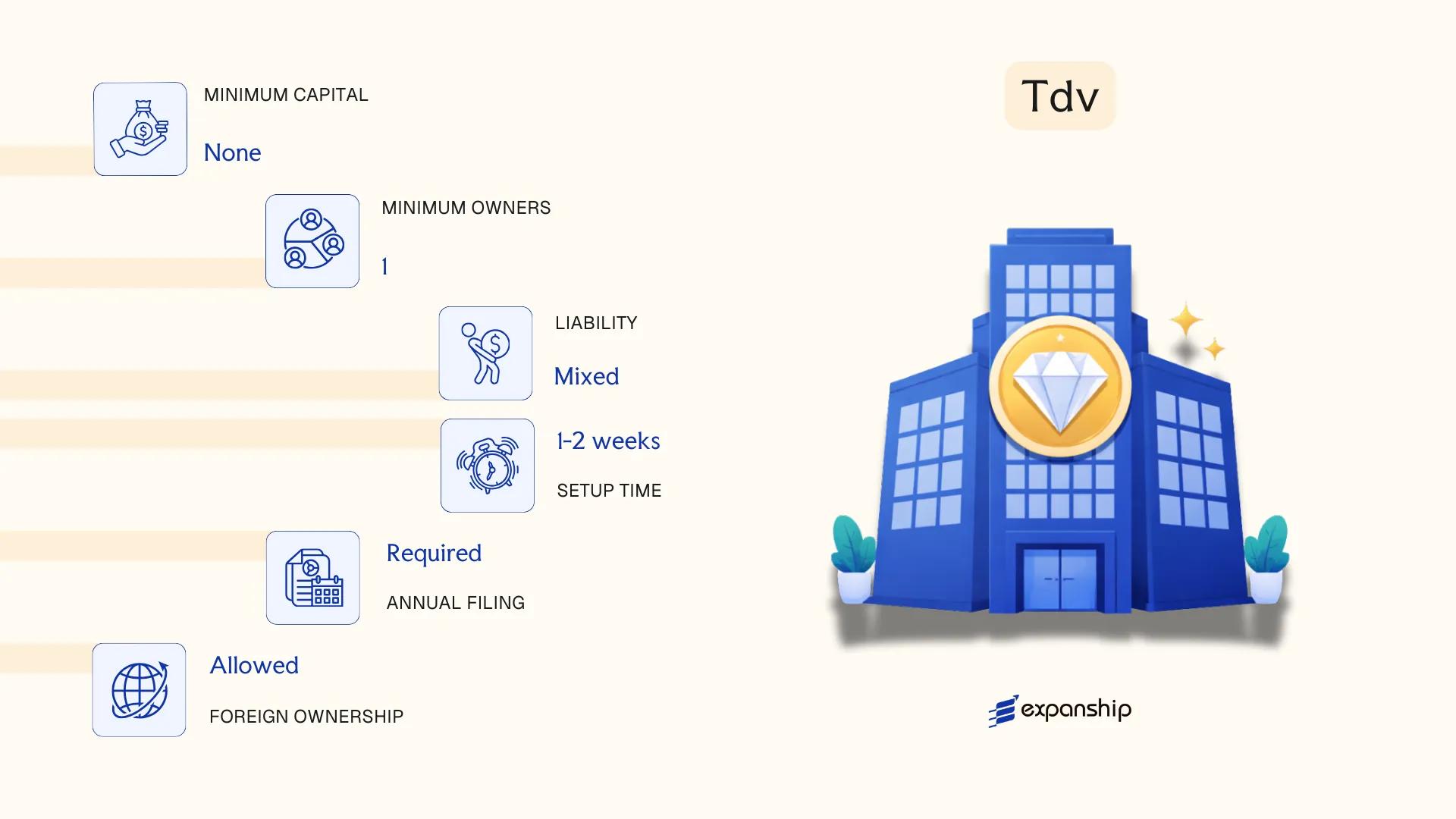

Additional Liability Company (Tovarystvo z Dodatkvoyu Vidpovidalnistyu — TDV)

Governed by the Law of Ukraine "On Business Associations" No. 1576-XII (1991) and supplemented by the Civil Code of Ukraine (2003), the additional liability company Ukraine TDV occupies a narrow but legally distinct position in the corporate framework. It holds separate legal personality, meaning the entity itself — not its members — is the primary obligor in commercial transactions.

Unlike a standard limited liability company, member liability in a Tovarystvo z Dodatkovoyu Vidpovidalnistyu extends beyond contributed capital. Each member bears joint and several liability for the company's obligations, but only up to a multiple of their contribution as defined in the founding documents.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Additional Liability Company (TDV) | Hybrid structure; separate legal personality with extended member liability |

| Members | Minimum 1, maximum unlimited | Members are referred to as "participants" (uchasnyky) |

| Liability | Fixed multiple of each participant's contribution | Multiplier must be stated in the charter; applied jointly and severally |

| Local Presence | Registered legal address in Ukraine required | No mandatory local director requirement under general rules |

| Share Capital | No statutory minimum under current law | Contributions and liability multiples must be defined in the founding charter |

| Privacy | Participant data filed with the Unified State Register | Register is publicly accessible |

Focus Points

- Taxation: Subject to standard corporate income tax at 18%, VAT at 20% where applicable, and withholding tax on dividends at 5% (residents) or 15% (non-residents), unless reduced by a double tax treaty.

- Annual Compliance: Must file financial statements with the State Tax Service of Ukraine and maintain updated entries in the Unified State Register of Legal Entities.

- Treaty Access: Qualifies as a resident legal entity for the purposes of Ukraine's double taxation agreements.

- Conversion: Can be reorganised into a TOV or other business association through a statutory reorganisation procedure under the Civil Code.

Closing

The TDV suits scenarios where participants want to signal financial commitment beyond their equity stake — occasionally used in professional services or tightly held family businesses — but the extended liability exposure makes it less attractive than a TOV for most commercial purposes.

Closely held businesses where participants are willing to accept defined personal liability beyond their capital contribution, typically in professional or family-run contexts.

Partnerships [General Partnership (Povne Tovarystvo), Limited Partnership (Komandytne Tovarystvo)]

Ukraine's partnership business structure is governed by the Civil Code of Ukraine (2003) and the Commercial Code of Ukraine (2003). Both codes establish two distinct partnership forms, each with a separate legal personality under Ukrainian law.

Unlike capital-based entities, partnerships are founded on personal participation and mutual trust among members. Unlimited liability is the defining feature of the general partnership, while the limited partnership introduces a tiered liability structure across two classes of participants.

Key Characteristics

| Requirement | General Partnership (Povne Tovarystvo) | Limited Partnership (Komandytne Tovarystvo) |

|---|---|---|

| Legal Form | Separate legal entity | Separate legal entity |

| Members | Called "participants"; minimum 2 general partners, no statutory maximum | Two classes: at least 1 general partner (unlimited liability) + at least 1 limited partner (investor); no statutory maximum |

| Liability | All participants bear unlimited joint liability for obligations | General partners: unlimited; limited partners: liability capped at their contributed share |

| Local Presence | Registered legal address in Ukraine required | Registered legal address in Ukraine required |

| Capital | No statutory minimum; contributions defined in the founding agreement | No statutory minimum; limited partners' contributions recorded in the memorandum |

| Privacy | Participant details disclosed in the Unified State Register of Legal Entities | Same disclosure requirements apply to both partner classes |

Focus Points

- Taxation: Partnerships are fiscally transparent at the entity level; profits are taxed at the participant level under personal income tax (18%) or corporate tax (18%) depending on participant type; VAT registration applies if turnover exceeds the statutory threshold; no separate withholding tax specific to partnership distributions.

- Annual Compliance: Financial statements must be submitted annually; partnerships register with the Unified State Register and report to the State Tax Service of Ukraine.

- Restrictions: General partners in both forms cannot participate in competing businesses without consent from other participants, as stipulated under the Commercial Code.

- Conversion: A partnership may be reorganised into another legal form through the statutory reorganisation procedure under Ukrainian law, subject to creditor notification requirements.

Sub-Types

General Partnership (Povne Tovarystvo)

All participants act as general partners and bear joint unlimited liability for the firm's obligations with their personal assets. This structure is used where founders prefer a flat governance model with direct mutual accountability.

Limited Partnership (Komandytne Tovarystvo)

The Komandytne Tovarystvo introduces silent investors (limited partners) whose liability does not exceed their capital contribution. General partners retain management authority, while limited partners participate only in profit distribution without voting rights on operational matters.

Closing

Partnerships are used by closely held professional firms or family-owned businesses where participants prefer direct control over formalised corporate governance. The absence of a minimum capital requirement lowers the barrier to formation, though unlimited personal liability for general partners represents a significant legal exposure that restricts broader commercial use.

Partnerships in Ukraine are best suited for small groups of trusted co-founders or professional practitioners who require a simple structure and are prepared to accept personal liability for business obligations.

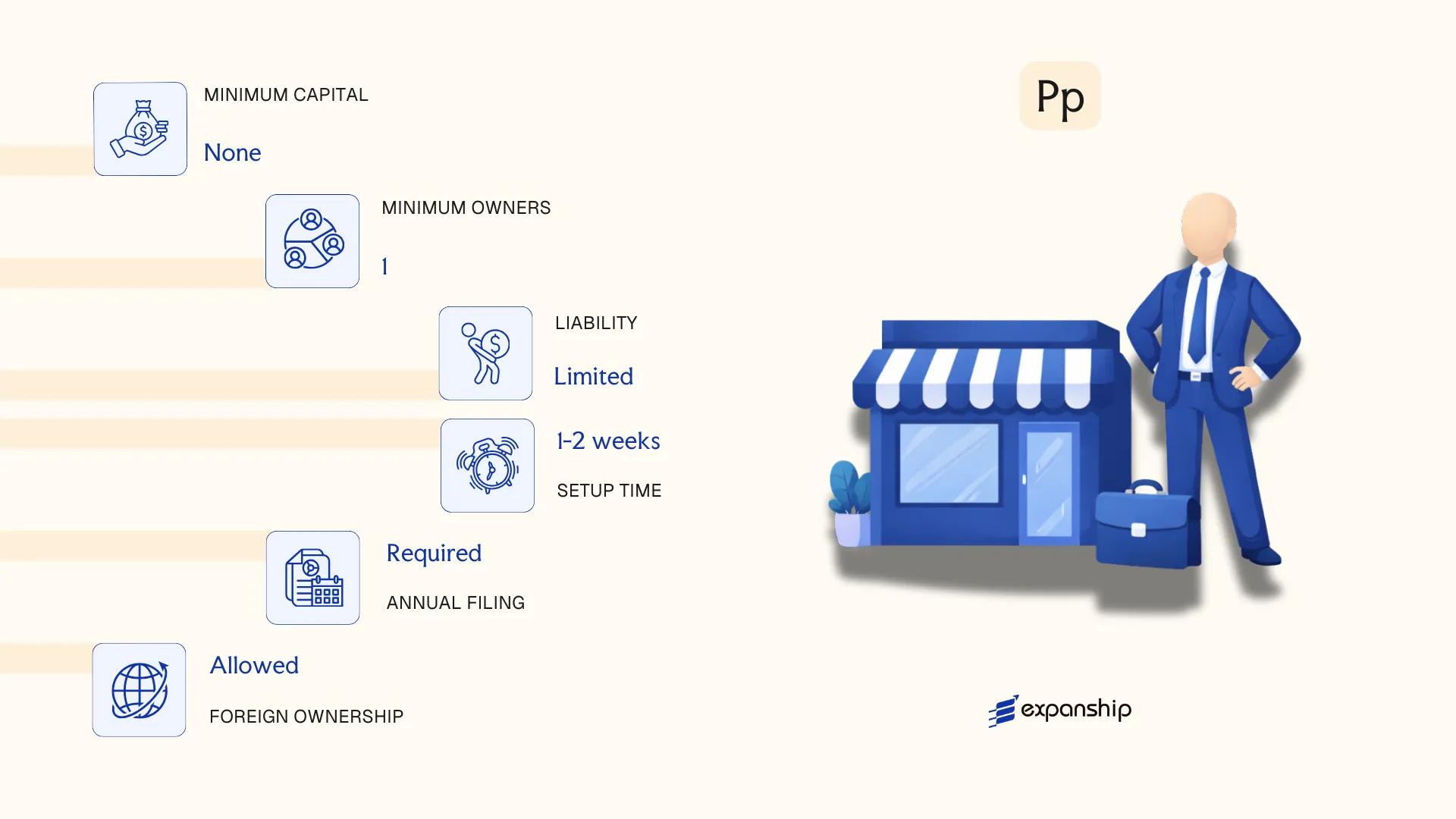

Private Enterprise (Pryvatne Pidpryyemstvo — PP)

Governed primarily by the Commercial Code of Ukraine (2003) and the Civil Code of Ukraine (2003), a Pryvatne Pidpryyemstvo is a commercially active entity founded on privately owned property. Private enterprise Ukraine PP registration is a distinct process from LLC formation, and the resulting structure carries separate legal personality from its founder.

Liability under this form is generally limited to the assets of the entity itself, though the precise scope depends on how the founding documents define property contributions. The structure sits in a hybrid position: it resembles a sole proprietorship in governance simplicity but holds full legal entity status.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Enterprise (PP / Pryvatne Pidpryyemstvo) | Separate legal personality; governed by founding charter |

| Founders | Single founder (individual or legal entity) | Referred to as the Proprietor; no maximum restriction |

| Governing Body | Director (may be the founder) | No mandatory supervisory board |

| Registered Office | Physical address in Ukraine required | Must be maintained throughout the entity's existence |

| Share Capital | No statutory minimum | Defined in the charter by the founder |

| Privacy | Founder details filed with the Unified State Register | Register is publicly accessible |

Focus Points

- Taxation: Subject to standard corporate income tax at 18%, VAT at 20% if registered as a VAT payer, and withholding tax on dividends paid abroad at 15% (reduced under applicable tax treaties).

- Annual Compliance: Must file financial statements and tax returns; audit requirements depend on size thresholds.

- Treaty Access: As a Ukrainian tax-resident entity, eligible for double taxation treaty benefits subject to beneficial ownership conditions.

- Conversion: Can be reorganised into a TOV or other entity form through a formal restructuring procedure under Ukrainian law.

- Restrictions: Cannot issue shares; equity transfer mechanisms are charter-defined and less standardised than a TOV.

Closing

A PP suits a single founder seeking direct operational control without the structural formality of a joint-stock form, commonly used for small trading or service businesses. The absence of a minimum capital requirement lowers the entry threshold, but the non-standardised ownership transfer process creates friction if ownership needs to change.

A PP is most practical for individual entrepreneurs or single legal-entity founders who require a separate legal person but do not anticipate bringing in co-founders or external investors.

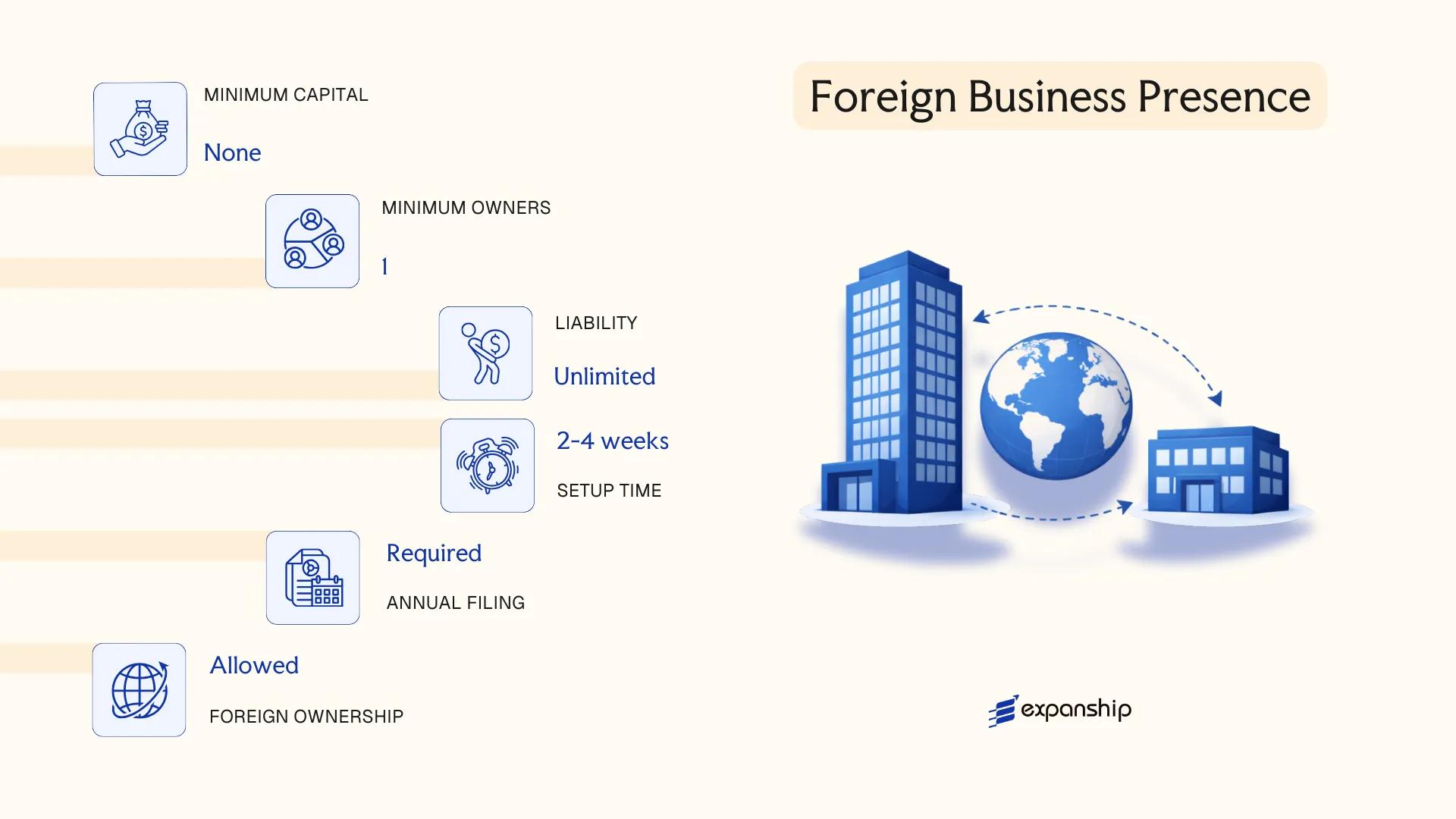

Foreign Business Presence in Ukraine [Representative Office, Branch Office]

A foreign company representative office Ukraine registration and a branch office registration are both governed by the Law of Ukraine "On the Legal Status of Foreigners and Stateless Persons" and related provisions under the Civil Code of Ukraine (2003), along with the procedure established by the Ministry of Economy. Neither form constitutes a separate legal entity; both remain structural subdivisions of the parent foreign company.

Because they lack independent legal personality, the parent company bears full liability for all obligations incurred by its Ukrainian presence. Registration is handled through the Ministry of Economy of Ukraine, which maintains a register of accredited representative offices and branches of foreign firms.

Key Characteristics

| Requirement | Representative Office | Branch Office |

|---|---|---|

| Legal Form | Non-legal entity; subdivision of parent | Non-legal entity; subdivision of parent |

| Head | Chief Representative (appointed by parent) | Branch Head (appointed by parent via Power of Attorney) |

| Permitted Activities | Non-commercial only (marketing, liaison, market research) | Commercial activities permitted; mirrors parent's scope |

| Local Presence | Registered address in Ukraine required | Registered address in Ukraine required |

| Capital Requirement | No minimum capital; parent funds operations | No minimum capital; parent funds operations |

| Registration Body | Ministry of Economy of Ukraine | Ministry of Economy of Ukraine |

Focus Points

- Taxation: Neither form is a separate taxpayer; tax obligations arise at the parent level, though permanent establishment rules under Ukrainian tax law and applicable double tax treaties may create local corporate profit tax exposure; VAT registration is required if taxable supplies exceed the statutory threshold.

- Economic Substance: A branch conducting active commercial operations is generally treated as a permanent establishment under Ukrainian law, triggering profit attribution and local filing obligations.

- Annual Compliance: Both forms must file annual activity reports with the Ministry of Economy and maintain updated accreditation documentation.

- Treaty Access: Access to Ukraine's double tax treaty network depends on the parent company's residency; the subdivision itself cannot independently claim treaty benefits.

- Restrictions: Representative offices are explicitly prohibited from conducting revenue-generating commercial activities; violating this restriction risks accreditation revocation.

Sub-Types

Representative Office

Accredited for a fixed term (typically one to three years, renewable) and restricted to preparatory and auxiliary functions such as market research, advertising, and liaison activities on behalf of the parent entity.

Branch Office

Authorised to conduct the same commercial activities as the parent company, as specified in the parent's constitutional documents. Unlike a representative office, a branch can enter into contracts, generate revenue, and employ staff under Ukrainian labour law directly.

Closing

Both forms suit foreign businesses testing the Ukrainian market or managing regional operations without committing to a locally incorporated entity; the branch offers broader operational scope, while the representative office carries a narrower, administratively lighter footprint.

A representative office fits foreign firms with non-commercial liaison or market-entry research objectives; a branch suits those requiring direct commercial activity without local incorporation.

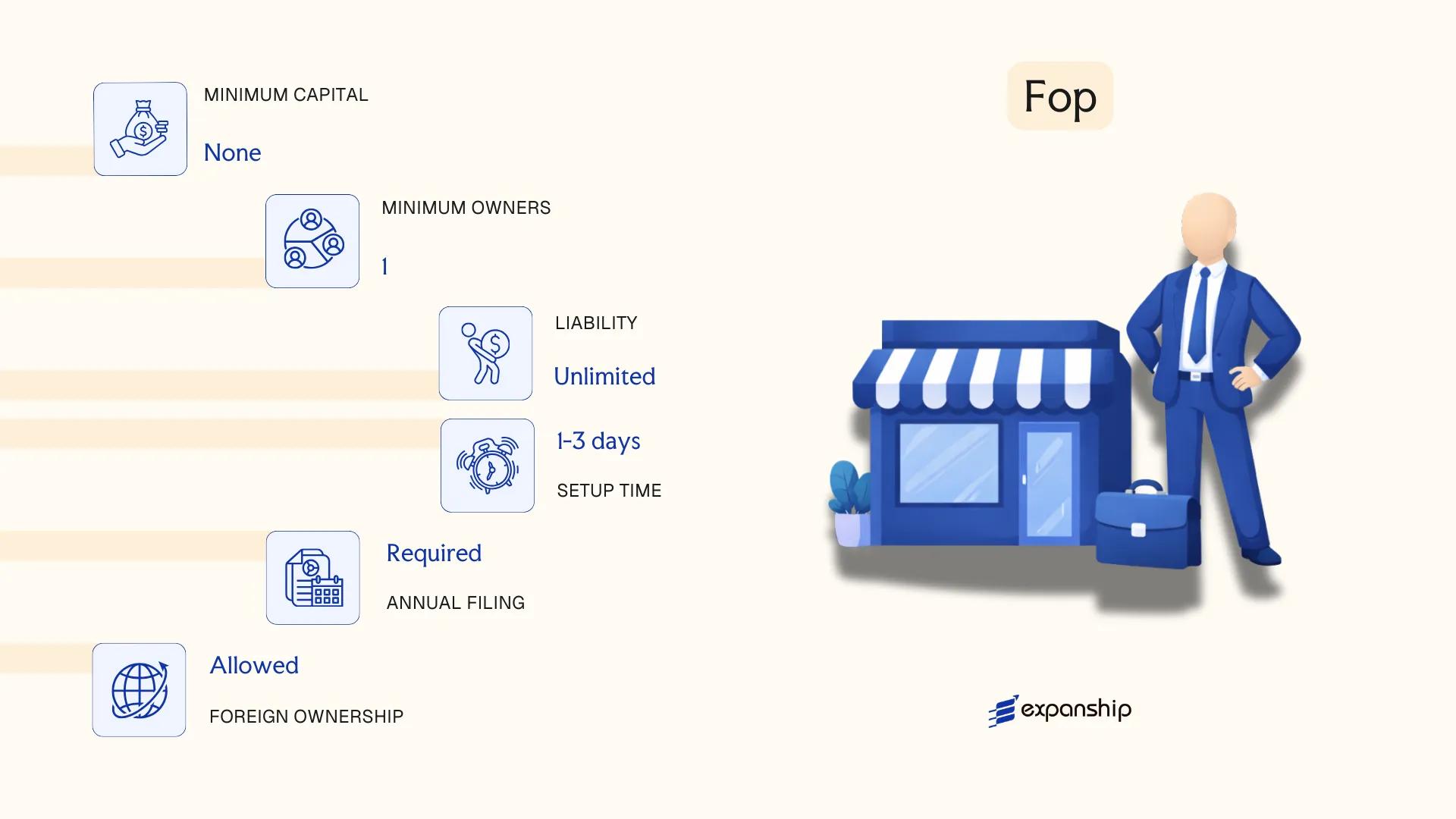

Sole Proprietorship (Fizychna Osoba-Pidpryyemets — FOP)

Sole proprietorship Ukraine FOP registration is governed primarily by the Civil Code of Ukraine (2003) and the Commercial Code of Ukraine (2003), alongside the Law of Ukraine "On State Registration of Legal Entities, Individual Entrepreneurs and Public Associations" (2003). A FOP, or Fizychna Osoba-Pidpryyemets, is not a separate legal entity. The individual and the business are one and the same in law.

Because no corporate veil separates the proprietor from the FOP, personal assets remain fully exposed to business liabilities. Registration is handled through the Unified State Register (USR), administered by the Ministry of Justice of Ukraine, and can be completed at state registrars or through authorised notaries.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual entrepreneur (natural person) | Not a separate legal entity; no corporate structure |

| Member Designation | Proprietor / Individual Entrepreneur | Single individual only; no co-founders permitted |

| Membership | 1 natural person (Ukrainian citizen or foreign national) | Foreign nationals may register subject to residency documentation |

| Local Presence | Registered address tied to proprietor's place of residence or declared address | No separate registered office requirement |

| Capital | No minimum capital requirement | No share capital; business assets are personal assets |

| Liability | Unlimited personal liability | All personal property is exposed to business debts |

Focus Points

- Taxation: FOPs fall under one of three Unified Tax groups (Group 1, 2, or 3) or the general income tax system; Group 3 entities may opt into VAT registration, while Groups 1 and 2 pay fixed quarterly amounts; personal income tax at 18% and military levy at 1.5% apply under the general system.

- Annual Compliance: Quarterly and annual income declarations are required; unified social contribution (USC) payments are mandatory regardless of trading activity.

- Restrictions: Activity types are restricted by group classification; certain regulated professions and high-revenue activities cannot operate under Groups 1 or 2.

- Conversion: A FOP cannot be converted into a legal entity directly; the individual must separately incorporate a TOV or other legal form and cease FOP activity through the USR.

Closing

A FOP suits freelancers, consultants, and micro-businesses requiring a low-cost, minimal-compliance operating structure, though unlimited personal liability makes it unsuitable for ventures carrying significant contractual or financial risk.

FOPs are best suited for individual professionals and sole traders operating in low-risk, low-revenue activities who prioritise simplicity over liability protection.

How to Choose the Right Entity Type in Ukraine

Knowing how to choose a business entity in Ukraine before filing any registration documents can prevent structural and compliance problems that are difficult to unwind later.

Why Your Entity Choice Matters

The legal form you register has binding consequences that persist for the life of the business.

- Selecting a TOV when your activity falls under a licensed or regulated sector — such as banking or insurance — may result in registration rejection or subsequent licence denial by the National Bank of Ukraine or the National Securities and Stock Market Commission.

- Registering a Representative Office when you intend to conduct commercial transactions with Ukrainian residents places the office in breach of its permitted scope, exposing it to administrative penalties.

- Choosing a FOP under a simplified tax group when your annual income exceeds the applicable group threshold triggers automatic forced reclassification and back-tax liability.

- Forming a Joint Stock Company when a single-shareholder TOV would suffice imposes mandatory audited financial reporting requirements, adding recurring costs without structural benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to different permitted legal forms under the Law of Ukraine "On Business Associations".

- Ownership Structure: A single founder points toward a TOV or PP, while multiple investors with defined equity stakes require a structure with a formal shareholders' register.

- Tax Regime Eligibility: Your choice determines whether the business qualifies for the simplified taxation system under the Tax Code of Ukraine or falls under the general corporate profit tax.

- Liability Exposure: The extent to which personal assets are ring-fenced depends entirely on the legal form — unlimited in general partnerships, capped in a TOV.

- Substance Requirements: If you cannot maintain a physical presence, a Representative Office lacks independent legal personality and cannot contract in its own name.

- Exit and Conversion: Not all Ukrainian entity types permit straightforward conversion; restructuring after registration may require full liquidation and re-registration.

Compliance Services for Companies in Ukraine

Ongoing compliance support for Ukrainian legal entities, including statutory filings, reporting obligations, and regulatory correspondence.

Conclusion

Selecting the right structure is the first substantive decision in any Ukraine company incorporation, and this guide has outlined the full range of options governed primarily by the Law of Ukraine "On Business Societies" and the Law "On Limited Liability Companies." The TOV dominates new registrations, suited to small and mid-sized ventures seeking capped liability without the disclosure burdens of a joint stock company. An AT fits businesses requiring share capital mechanisms and broader investor access. The TDV carries subsidiary liability, making it a structurally distinct choice for specific risk arrangements. Partnerships suit professional or family-run operations, while a PP offers a simplified sole-ownership structure. Foreign entities opting for representative or branch offices accept limited operational scope in exchange for a lighter registration process. The FOP remains the entry point for individual entrepreneurs.

Ukraine's ongoing alignment with EU regulatory standards through its candidacy process suggests incremental reform across corporate governance and reporting requirements in the years ahead. Expanship's team tracks these developments as they move through the legislative pipeline.

How Expanship Can Assist You

Expanship provides corporate services for Ukraine company formation across the full range of structures discussed in this blog, from registering a TOV with the State Register of Legal Entities, Individual Entrepreneurs and Public Organisations to establishing a representative office or branch. Each entity type carries distinct obligations, and our team ensures your chosen structure meets those requirements from day one.

From initial document preparation through to post-incorporation maintenance, we manage every step alongside you:

- Articles of association drafting and notarisation

- State registrar filing and registration number procurement

- Registered office and local agent provision

- Tax registration with the State Tax Service of Ukraine

- Ongoing statutory compliance and annual reporting support

- Banking introduction assistance for opening a UAH or foreign-currency account

Ready to move forward? Reach out to Expanship Ukraine to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The TOV (Limited Liability Company) is the most frequently incorporated entity, governed by the Law of Ukraine "On Limited Liability Companies and Additional Liability Companies" No. 2275-VIII. Its minimal charter capital requirement and single-member formation option make it accessible to a wide range of business operators, from small domestic firms to foreign-owned subsidiaries.

An AT issues publicly tradeable shares and faces heavier disclosure and reporting obligations, including requirements under the National Securities and Stock Market Commission. A TOV distributes participatory interests rather than shares, carries fewer ongoing compliance requirements, and does not require public disclosure of its ownership structure to the same degree.

A TOV provides the greatest degree of confidentiality among Ukrainian commercial entities. Beneficial ownership information is submitted to the State Register but is not fully accessible to the general public under all circumstances. Nominee arrangements are legally permissible, though beneficial owners must still be disclosed to the relevant authorities.

A TOV and a Private Enterprise (PP) can each be formed by one individual. General Partnerships (Povne Tovarystvo) and Limited Partnerships (Komandytne Tovarystvo) require at least two participants by statutory definition, making sole formation legally impermissible for those structures.

Foreigners may establish a TOV, AT, PP, or FOP, and may participate in partnerships. A Representative Office or Branch does not constitute a separate legal entity and requires a parent company abroad. Foreign individuals registering as a FOP must obtain a Ukrainian taxpayer identification number from the State Tax Service before commencing activity.

Ukrainian law permits the reorganisation of legal entities through transformation, merger, or division under the Civil Code of Ukraine. A TOV may be converted into an AT, and vice versa, through a formal reorganisation procedure involving the State Register of Legal Entities, Individual Entrepreneurs and Public Organisations. Not all conversions follow identical procedural paths, and some require creditor notification periods.

A TOV, AT, TDV, PP, General Partnership, and Limited Partnership all hold separate legal personality under Ukrainian law. A Representative Office does not; it acts as an extension of its foreign parent and cannot enter into contracts in its own name. The FOP is a natural person conducting business, so legal personality is tied to the individual rather than a distinct corporate structure.

A FOP operating under the simplified tax system has the lightest administrative burden, with quarterly single-tax payments and minimal reporting obligations to the State Tax Service. Among incorporated entities, a TOV with a single participant and no hired employees carries fewer statutory reporting requirements than an AT, which is subject to annual audits and securities regulator oversight.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.