Key Takeaways

- Taiwan's Company Act (公司法), administered by the Ministry of Economic Affairs, governs the formation and compliance of all corporate structures across the jurisdiction's eight available entity types.

- The Limited Company (有限公司) is the most commonly registered structure under the Company Act, making it the default choice for most small-to-medium private enterprises operating in Taiwan.

- Foreign businesses entering Taiwan can establish either a Branch Office for operational activity or a Representative Office, which is restricted to market research and cannot conduct revenue-generating activities.

- Liability exposure varies significantly across structures, from the personal liability accepted by members of an Unlimited Company (無限公司) to the limited liability protections available under a Company Limited by Shares (股份有限公司).

Introduction to Entity Types in Taiwan

Taiwan is an island territory in East Asia, positioned in the western Pacific Ocean between Japan to the northeast and the Philippines to the south. Politically, it operates as a self-governing entity under the government of the Republic of China (ROC), with its own legal system, currency, and independent administrative structure.

Company registration falls under the jurisdiction of the Ministry of Economic Affairs (MOEA), specifically through its Department of Commerce, which administers the Company Act (公司法) — the primary statute governing corporate formation and ongoing compliance. Foreign investment is additionally subject to review under the Statute for Investment by Foreign Nationals.

Taiwan operates a territorial-based tax system, meaning domestic-source income is generally subject to taxation while foreign-source income may receive different treatment depending on the entity structure.

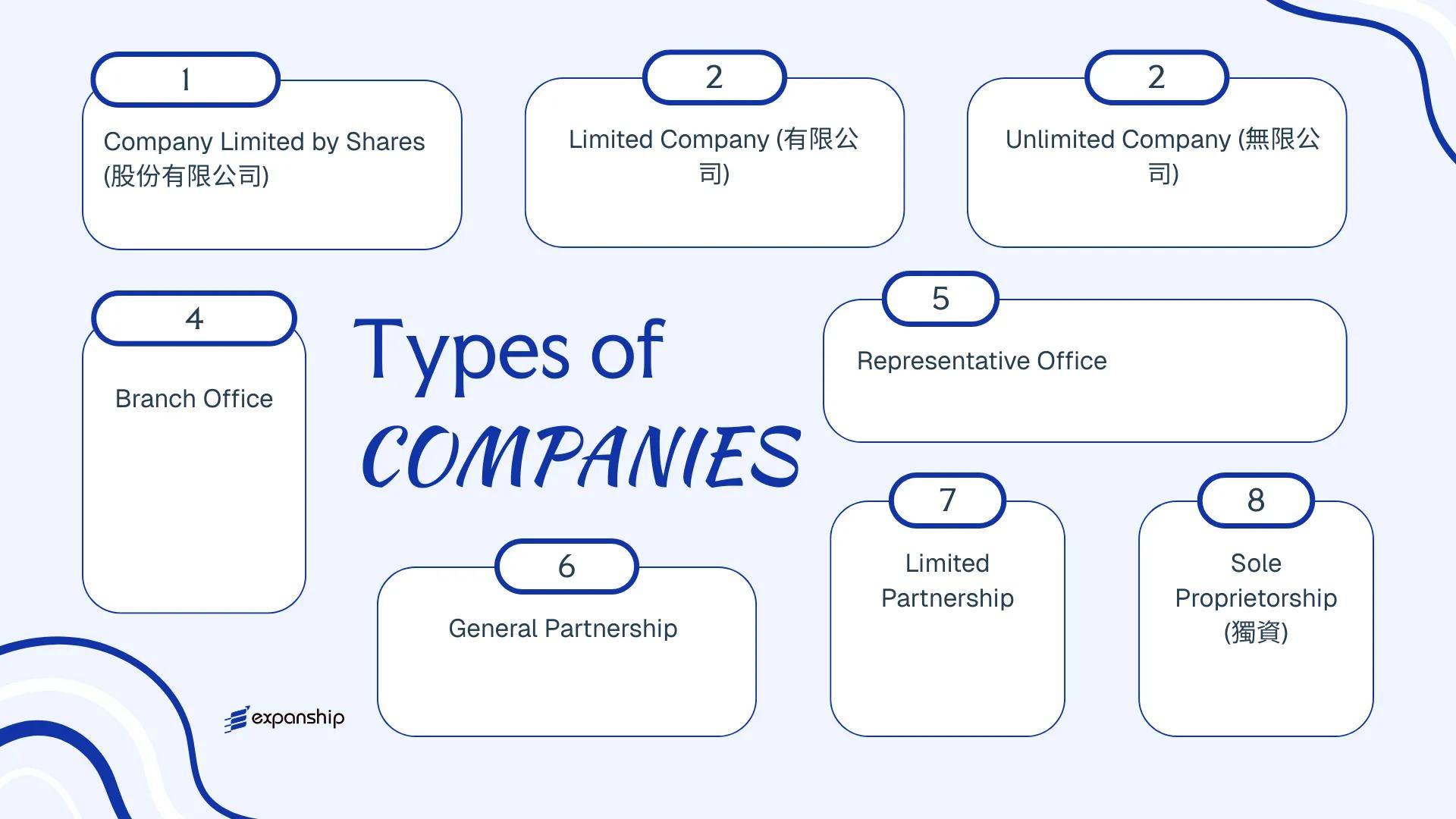

Several distinct business structures are available under local law: Company Limited by Shares (股份有限公司), Limited Company (有限公司), Unlimited Company (無限公司), Branch Office, Representative Office, General Partnership, Limited Partnership, and Sole Proprietorship (獨資). Each structure carries different requirements around ownership, liability, and capitalization. This article covers each in detail to help you determine which structure suits your business objectives.

An Overview of Business Structures in Taiwan

Taiwan's company law framework offers six principal entity types for businesses operating within its jurisdiction. The primary legislation governing these structures is the Company Act (公司法), which was substantially amended in 2018 to modernise corporate governance requirements. Each structure carries distinct implications for liability, ownership, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Company Limited by Shares (股份有限公司) | Corporation | Limited to shares | Corporate Income Tax | Permitted | 1 shareholder | MOEA / FSC | Company Act |

| Limited Company (有限公司) | Private company | Limited to capital | Corporate Income Tax | Permitted | 1 shareholder | MOEA | Company Act |

| Unlimited Company (無限公司) | Partnership-type | Unlimited, joint | Corporate Income Tax | Permitted | 2 shareholders | MOEA | Company Act |

| Branch Office | Extension of foreign entity | Parent liable | Corporate Income Tax | Permitted | N/A | MOEA | Company Act |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | MOEA | Company Act |

| General Partnership | Unincorporated | Unlimited, joint | Pass-through | Permitted | 2 partners | MOEA | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Pass-through | Permitted | 2 partners (1 GP, 1 LP) | MOEA | Partnership Act |

| Sole Proprietorship (獨資) | Unincorporated | Unlimited, personal | Individual Income Tax | Permitted | 1 owner | Local authority | Business Registration Act |

Each of these structures is examined in full in the sections below.

Company Limited by Shares (股份有限公司)

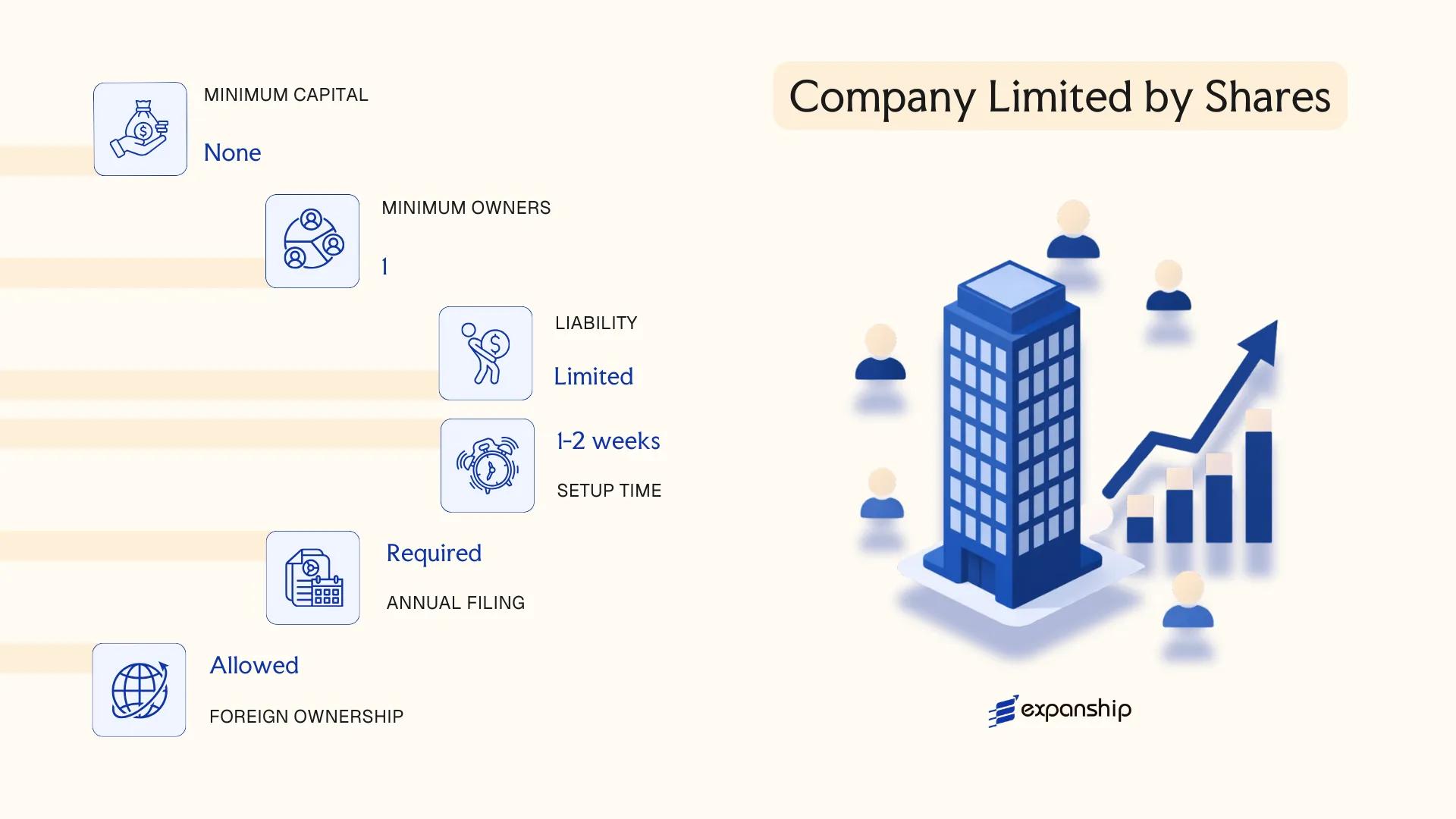

Governed by the Company Act (公司法), most recently amended in 2018, the Taiwan company limited by shares (股份有限公司) is the most structurally developed corporate form available under Taiwanese law. The entity carries separate legal personality, meaning its rights and obligations are entirely distinct from those of its shareholders.

Shareholders bear liability only to the extent of their capital contributions. This structure supports both closely held private firms and publicly listed companies, with the latter subject to additional regulation under the Securities and Exchange Act (證券交易法) and oversight by the Financial Supervisory Commission (FSC).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Stock company with separate legal personality | Liability capped at paid-in share capital |

| Members | Shareholders (minimum 2 for private; 200+ for public listing) | Directors elected from or outside shareholder body; minimum 3 directors and 1 supervisor for private companies |

| Local Presence | Registered office address in Taiwan required | A responsible person (負責人) must be designated |

| Capital | NTD; no statutory minimum for private companies post-2018 reform | Public companies subject to FSC capital requirements |

| Privacy | Shareholder register filed with MOEAIC; beneficial ownership not fully public | Director names are publicly searchable |

Focus Points

- Taxation: Subject to a 20% corporate income tax, a 5% business tax (VAT) on most taxable supplies, withholding tax on dividends distributed to non-residents (generally 21%), and stamp duty on certain instruments.

- Annual Compliance: Annual financial statements, shareholder meetings, and filings with the Ministry of Economic Affairs Investment Commission (MOEAIC) or the relevant competent authority are required.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions, but a registered local office and operational presence are effectively required for licensing and banking.

- Treaty Access: Eligible to benefit from Taiwan's tax treaties (currently around 35 agreements), subject to anti-avoidance provisions.

- Conversion: Can convert to or from a limited company (有限公司) under the Company Act, subject to shareholder resolution and regulatory approval.

Sub-Types

Private Company Limited by Shares (非公開發行股份有限公司)

This form does not offer shares to the public and is exempt from Securities and Exchange Act disclosure requirements, making it the standard vehicle for foreign investment, joint ventures, and domestic operating businesses.

Public Company (公開發行公司) and Listed Company (上市/上櫃公司)

A company that issues shares to the public falls under FSC jurisdiction and must comply with enhanced disclosure, audit, and governance obligations. Listing on the Taiwan Stock Exchange (TWSE) or Taipei Exchange (TPEx) requires meeting additional financial and operational thresholds beyond the base Company Act requirements.

When to Use This Structure

The 股份有限公司 suits foreign investors establishing a trading, manufacturing, or holding operation in Taiwan where scalable equity structure and investor transferability matter. Its key advantage is the ability to issue multiple share classes and accommodate a broad shareholder base. The primary limitation is its comparatively higher administrative burden relative to the limited company form, particularly around board composition and annual reporting.

This entity is most appropriate for foreign enterprises, joint ventures, and businesses anticipating future capital raises or eventual public listing.

Company Incorporation in Taiwan

Incorporate a Company Limited by Shares or other entity types in Taiwan with Expanship's end-to-end corporate services.

Limited Company (有限公司)

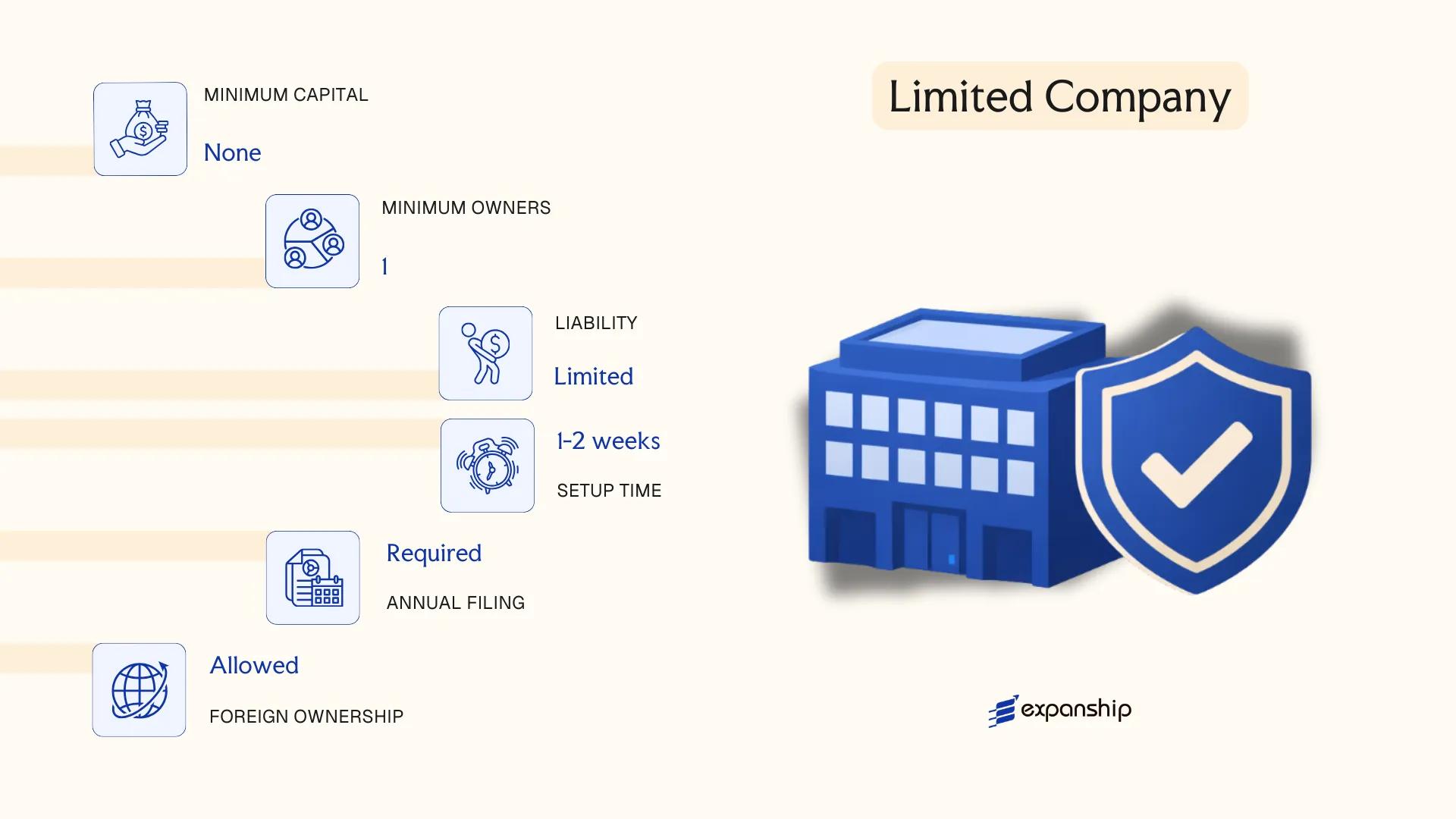

Governed by the Company Act (公司法), which has undergone significant amendments, most recently in 2018, the Limited Company (有限公司) is a distinct legal entity that offers members full limited liability. Taiwan limited company 有限公司 formation appeals particularly to small and medium-sized enterprises seeking a simpler governance structure than a Company Limited by Shares.

Membership is capped at a fixed ceiling, and each member's liability is confined to their capital contribution. The entity holds separate legal personality, meaning it can contract, own property, and litigate in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Separate legal personality; not publicly listed |

| Members | 1–50 shareholders | Natural persons or legal entities; no public offering of shares permitted |

| Management | Directors (董事); no board mandatory | One or more directors appointed from among members or externally |

| Registered Office | Physical address in Taiwan required | P.O. Box not accepted; must be a verifiable local address |

| Capital | NTD; no statutory minimum post-2018 reform | Paid-in capital must reflect actual operational needs; authorities may scrutinise low-capital registrations |

| Share Transferability | Restricted; requires consent of a majority of other members | Shares are not freely transferable — a key structural constraint |

Focus Points

- Taxation: Subject to 20% corporate income tax; VAT at 5% on taxable supplies; withholding tax applies to dividends, royalties, and service fees paid to non-residents; no stamp duty on capital contributions.

- Annual Compliance: Annual financial statements and tax filings required; companies with paid-in capital above NTD 30 million must appoint a certified public accountant.

- 有限公司 Registration Taiwan: Registration is filed with the Ministry of Economic Affairs (MOEA) through the online company registration system.

- Conversion: May be converted to a Company Limited by Shares (股份有限公司) by resolution, subject to Company Act procedures.

- Restrictions: Cannot issue shares to the public or list on a stock exchange; the 50-member cap limits equity-based fundraising.

The 有限公司 suits trading operations, domestic service businesses, and wholly-owned subsidiaries of foreign groups seeking operational simplicity over capital-raising capacity. Its streamlined governance reduces administrative overhead, though the restriction on share transferability and the hard membership ceiling make it unsuitable for businesses anticipating investor rounds or eventual public listing.

This structure fits foreign investors or local entrepreneurs establishing a closely-held operating entity in Taiwan with no near-term plans for external equity fundraising.

Unlimited Company (無限公司)

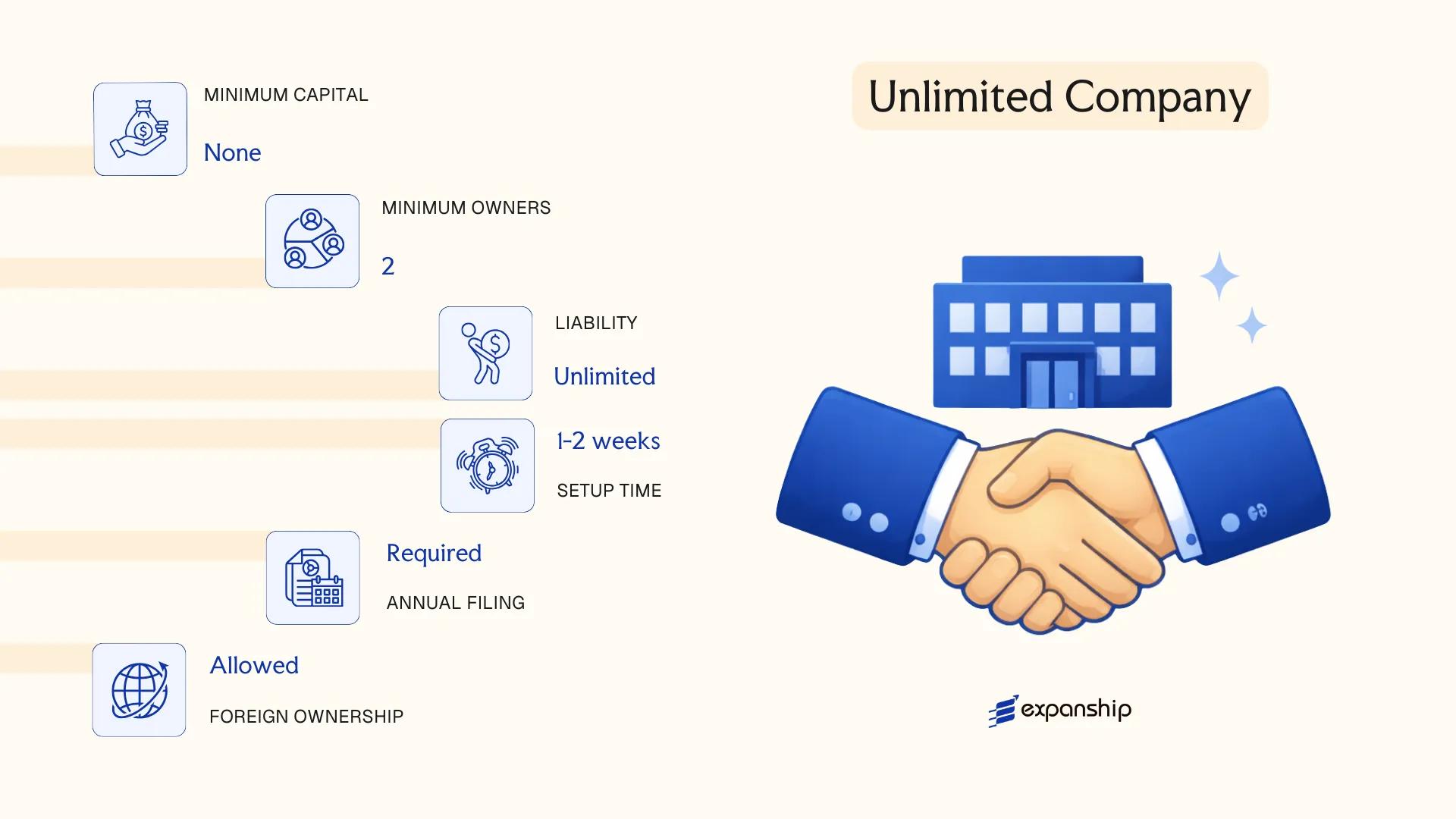

Governed by the Company Act (公司法), the Taiwan unlimited company 無限公司 structure is defined under Chapter II of that legislation. The entity possesses a separate legal personality upon registration with the Ministry of Economic Affairs (MOEA), yet every member bears joint, unlimited, and personal liability for the company's debts — a feature that sets it apart from both limited and hybrid corporate forms.

Registration falls under the MOEA's Companies and Firms Registration system. Because all members carry personal exposure, this structure is uncommon in commercial practice, though it remains legally available for those who meet its formation requirements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company (無限公司) | Separate legal personality; all members bear unlimited personal liability |

| Members | Referred to as shareholders; minimum 2, no statutory maximum | All members must be natural persons; no corporate shareholders permitted |

| Local Presence | Registered address in Taiwan required | No registered agent requirement, but a local director is effectively necessary for operations |

| Capital | No statutory minimum; denominated in New Taiwan Dollar (NTD) | Capital must be stated in the articles of incorporation |

| Privacy | Member names disclosed in public registration records | MOEA registration filings are publicly accessible |

Focus Points

- Taxation: Subject to Taiwan's standard corporate income tax at 20%; retained earnings surcharge of 5% applies on undistributed profits; business tax (VAT) at 5% on taxable supplies; withholding tax applies to dividends and payments to non-residents at rates governed by the Income Tax Act.

- Annual Compliance: Annual financial statements must be prepared; profit-seeking enterprise income tax return filed with the National Taxation Bureau by the statutory deadline.

- Conversion: The Company Act permits conversion to a limited company or company limited by shares, subject to member consent and MOEA approval.

- Restrictions: Foreign nationals face practical barriers to participation, as all members carry unlimited personal liability and must generally be natural persons.

Primarily used by small domestic businesses or professional partnerships where members accept personal liability in exchange for a simpler governance structure, the entity offers minimal administrative overhead. The critical drawback is total personal exposure — each member's personal assets remain at risk for company obligations without limitation.

Best suited for small, closely-held domestic businesses whose members have full trust in one another and are comfortable accepting unlimited personal liability.

Foreign Business Presence in Taiwan [Branch Office, Representative Office]

Governed primarily by the Company Act (公司法) and administered by the Ministry of Economic Affairs (MCEA), foreign companies seeking a foreign company branch office Taiwan setup operate as extensions of their parent entity rather than separate legal persons. A branch office carries no independent legal personality — the parent company bears full legal and financial liability for its operations in the territory.

A representative office occupies a more restricted position. Registered through the MCEA, it is permitted to conduct liaison, market research, and promotional activities only; it cannot engage in revenue-generating transactions or sign commercial contracts on behalf of the parent.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Full commercial operations | Non-revenue liaison only |

| Designated Representative | Mandatory local representative (本地代理人) required | Chief Representative required |

| Registered Address | Physical office address in Taiwan required | Physical office address required |

| Capital Requirement | Remitted working capital required (amount assessed by MCEA) | None |

| Tax Registration | Subject to profit-seeking enterprise income tax | Generally not subject to income tax if no revenue generated |

Focus Points

- Taxation: Branch profits remitted to the parent are subject to a 20% withholding tax; the branch itself pays profit-seeking enterprise income tax at the standard 20% rate, with a 5% business tax (VAT) applying to taxable supplies.

- Annual Compliance: Both structures must file annual reports with the MCEA and maintain a registered local representative; branches must also file corporate income tax returns with the National Taxation Bureau.

- Treaty Access: Taiwan's tax treaty network is limited; access to withholding tax reductions depends on the parent's home jurisdiction having a tax agreement with Taiwan.

- Conversion: A branch may convert to a locally incorporated entity, but this requires a fresh incorporation process under the Company Act rather than a simple re-registration.

- Restrictions: Representative offices are prohibited from invoicing, receiving payments, or entering binding commercial agreements — any breach risks reclassification and penalties.

Sub-Types

Branch Office (分公司)

A branch office is the standard vehicle for foreign firms that need to conduct business and generate revenue without incorporating a separate local subsidiary. It mirrors the parent's legal identity and is directly liable for all obligations incurred.

Representative Office (代表人辦事處)

A representative office is used exclusively for preparatory and auxiliary functions — gathering market intelligence, coordinating with local partners, or managing regional communications. It is not an appropriate structure for any entity intending to bill clients or execute revenue-generating contracts.

Closing Remarks

A branch office suits foreign firms testing the local market or managing regional operations without the administrative overhead of a full subsidiary, though the parent's unlimited exposure to Taiwanese liabilities is a meaningful drawback. A representative office is appropriate only as a temporary or purely administrative presence.

A branch office is best suited for established foreign companies requiring an operational presence without local incorporation; a representative office fits multinationals conducting pre-market research or managing inter-office coordination only.

Partnerships in Taiwan [General Partnership, Limited Partnership]

Governed by the Partnership Act (合夥), partnerships in Taiwan do not carry separate legal personality — partners are personally bound by the obligations of the business. Taiwan general and limited partnership registration follows distinct rules depending on the liability structure chosen, with both forms registered through the Ministry of Economic Affairs (MOEA).

Registration is handled at the local competent authority, typically the city or county government. Unlike companies, partnerships are not incorporated entities under the Company Act; they fall under civil and commercial law provisions applicable to unincorporated associations.

Key Characteristics

| Requirement | General Partnership | Limited Partnership | Notes |

|---|---|---|---|

| Legal Form | Unincorporated partnership | Unincorporated partnership | No separate legal personality for either form |

| Members | Partners (無限合夥人) | At least 1 general partner + 1 limited partner | No statutory maximum for either type |

| Liability | Unlimited, joint and several | General partners: unlimited; limited partners: capped at capital contribution | Limited partners cannot participate in management |

| Local Presence | Registered business address required | Registered business address required | Must be a physical address in Taiwan |

| Capital | No statutory minimum (TWD) | No statutory minimum (TWD) | Contributions may be cash, property, or services |

| Privacy | Partner names filed in public registry | Partner names filed in public registry | Limited disclosure through MOEA records |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits pass through to individual partners and are taxed under personal income tax rates, not the corporate income tax rate of 20%.

- Annual Compliance: Partners must file annual profit-seeking enterprise income tax returns; no board resolutions or shareholder meetings are required.

- Treaty Access: Pass-through treatment may limit access to Taiwan's tax treaty network, as treaty benefits typically apply to corporate entities.

- Restrictions: Foreign nationals may face additional approval requirements when registering as general partners with unlimited liability.

- Conversion: Conversion from a partnership to a company structure requires dissolution and fresh incorporation under the Company Act.

Sub-Types

General Partnership (普通合夥)

All partners hold unlimited, joint and several liability for partnership debts. This structure is used primarily by small professional practices or family-run businesses where partners actively co-manage operations.

Limited Partnership (有限合夥)

The Taiwan limited partnership structure combines at least one general partner bearing unlimited liability with one or more limited partners whose exposure is restricted to their agreed capital contribution. Limited partners are barred from day-to-day management, a restriction central to preserving their liability protection.

Closing

Partnerships suit small professional services firms or domestic ventures where pass-through taxation is preferred and partners are comfortable with personal liability exposure. The absence of a minimum capital requirement lowers the entry barrier, but unlimited personal liability for general partners remains a material constraint for commercially active businesses.

Partnerships are most appropriate for small domestic professional practices or closely held ventures where the partners intend to manage operations directly and accept personal liability for business obligations.

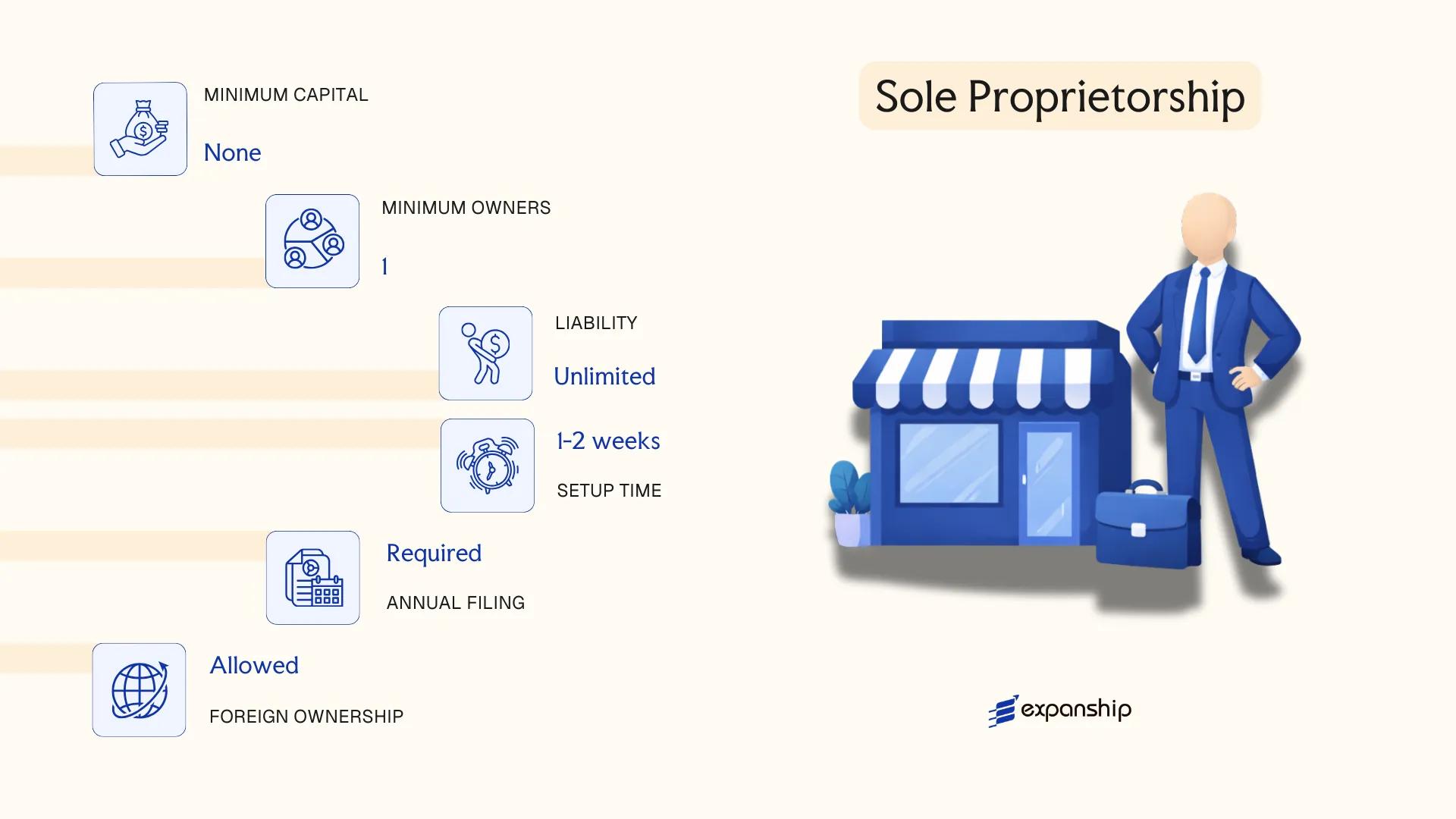

Sole Proprietorship (獨資)

Registered under the Business Registration Act, a sole proprietorship (獨資) is the simplest business structure available for individual operators. Taiwan sole proprietorship 獨資 registration is administered by the local competent authority, typically the Municipal or County/City Government Bureau of Commerce, rather than the MOEA's company registry. Unlike incorporated entities, this structure carries no separate legal personality — the proprietor and the business are treated as one legal person, meaning personal assets are fully exposed to business liabilities.

Registration is required before commencing operations, and the sole trader registration Taiwan process involves submitting an application for business registration at the local authority. Foreign nationals face restrictions on using this structure, as eligibility is generally limited to nationals holding the right to work in the jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality |

| Member Designation | Proprietor (負責人) | Single individual only |

| Membership | 1 proprietor; no maximum does not apply | Cannot have co-owners; partnership rules apply otherwise |

| Local Presence | Registered business address required | Must be a physical address within the jurisdiction |

| Capital | NTD; no statutory minimum | Declared capital recorded at registration |

| Liability | Unlimited personal liability | Proprietor's personal assets are fully at risk |

Focus Points

- Taxation: Subject to individual income tax (綜合所得稅) at progressive rates up to 40%; no separate corporate income tax applies; business income is reported on the proprietor's personal return; VAT registration required if annual revenue exceeds the threshold set by the MOF.

- Annual Compliance: Annual business tax filing and renewal of business registration if particulars change; financial records must be maintained per the Business Entity Accounting Act.

- Treaty Access: As an unincorporated individual entity, it does not qualify as a tax resident entity for the purposes of most tax treaties; treaty benefits flow through the individual proprietor's personal tax status.

- Conversion: Can be converted to a limited company or other incorporated structure, though this requires a fresh company registration and does not constitute a legal merger or transfer of entity.

- Restrictions: Foreign nationals without qualifying residency or work authorisation are generally ineligible; this structure cannot issue shares or admit investors.

Recommendations

A sole proprietorship suits small-scale local operations, freelance service providers, and individual traders who do not require external investment or liability protection. The primary advantage is administrative simplicity with low setup costs; the clear limitation is unlimited personal liability, which exposes the proprietor's private assets to all business obligations.

Local individual operators running low-risk, low-revenue businesses who prioritise minimal compliance overhead over liability protection.

How to Choose the Right Entity Type in Taiwan

Understanding how to choose a business entity in Taiwan requires more than comparing registration costs. The structure you select has direct legal, tax, and operational consequences that can be difficult to reverse once the entity is active.

Why Your Entity Choice Matters

Selecting the wrong structure creates concrete legal and financial exposure:

- A representative office conducting revenue-generating transactions violates the Company Act, exposing the parent company to penalties and potential forced closure of the office.

- Forming a limited company without confirming shareholder eligibility under the relevant investment approval regime can result in rejected registration by the Ministry of Economic Affairs.

- Choosing a branch structure when your activity requires a locally incorporated entity means contracts and licenses may be invalid or unenforceable under Taiwanese law.

- Registering as a sole proprietorship when your business will involve multiple investors creates personal unlimited liability for debts that a company structure would otherwise cap.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require a different structure under the Company Act.

- Ownership Structure: Single-owner operations can qualify as a sole proprietorship or limited company, while multi-investor ventures generally require a company limited by shares.

- Tax Objectives: Your need for treaty access, profit retention, or eligibility under the Statute for Industrial Innovation affects which entity type applies.

- Management Flexibility: Limited companies permit more informal governance than a company limited by shares, which mandates a board and formal shareholder meetings.

- Liability Exposure: Your tolerance for personal liability versus corporate separation should directly inform the choice between unincorporated and incorporated structures.

- Exit and Conversion: Not all entity types can be converted without dissolution; confirm in advance whether your structure permits redomiciliation or transformation under the Company Act.

Compliance Services for Companies in Taiwan

Maintain good standing with annual filing obligations, regulatory reporting, and ongoing statutory requirements under Taiwanese law.

Conclusion

Selecting the right structure is a foundational decision when following any setting up a company in Taiwan guide. The Company Limited by Shares suits capital-intensive ventures or businesses planning public listings, while the Limited Company serves most small-to-medium private enterprises seeking a simpler governance model. Unlimited companies fit closely held professional operations where personal liability is accepted. Branch offices work for foreign firms extending existing operations, and representative offices serve market research purposes only. General and limited partnerships address professional service providers or joint ventures with defined risk allocation. Sole proprietorships remain for individual operators with minimal administrative needs.

The Limited Company is the most commonly registered structure under the Company Act. Regulatory oversight by the Ministry of Economic Affairs has trended toward digitization, with ongoing refinements to the online registration system reflecting a broader push toward procedural efficiency. Taiwan's growing network of tax treaties also continues to shape how foreign-invested entities are structured.

How Expanship Can Assist You

Expanship Taiwan company incorporation services cover the full arc of formation and ongoing compliance, from choosing between a Company Limited by Shares (股份有限公司) and a Limited Company (有限公司) to meeting the filing requirements set by the Ministry of Economic Affairs (MOEA) and its Companies and Partnerships Administration. Whether your structure requires minimum capital verification, a local responsible person, or MOEABOE investment approval for foreign-owned entities, our team works through each requirement with you directly.

Our corporate services for Taiwan formation cover every stage of the process:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and liaison with the MOEA

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Taiwan to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Company Limited by Shares (股份有限公司) is the most frequently registered structure, largely because it permits public capital raising and the free transfer of shares. Its governance framework under the Company Act also aligns with the requirements of institutional investors and listing on the Taiwan Stock Exchange.

A branch office is an extension of its foreign parent and does not possess separate legal personality, whereas a locally incorporated company — such as a Limited Company (有限公司) or Company Limited by Shares — is a distinct legal person. Tax treatment also diverges: a branch remitting profits abroad may face withholding obligations that a locally incorporated subsidiary can manage differently through retained earnings. Compliance obligations for a branch are generally lighter, but trading rights and liability exposure differ materially.

The Limited Company (有限公司) offers comparatively greater privacy because its shareholder register is not made publicly accessible in the same manner as that of a Company Limited by Shares. Nominee arrangements are legally permissible, though beneficial ownership disclosure obligations have been strengthened under recent MOEA amendments. Director information is filed with the MOEA but is not always prominently searchable through public databases.

No. A sole proprietorship (獨資) requires only one natural person, and a Limited Company can be incorporated by a single shareholder under the Company Act. General partnerships and limited partnerships each require at least two partners, so a sole founder cannot form either structure alone.

Foreign nationals may incorporate a Company Limited by Shares or a Limited Company without holding Taiwan residency, subject to MOEA approval and investment review under the Statute for Investment by Foreign Nationals. Certain regulated sectors require prior approval from sector-specific authorities. Foreign investors may also establish a branch office or representative office, though the latter is restricted from generating local revenue.

The Company Act permits conversion between a Limited Company and a Company Limited by Shares through a formal reorganisation process filed with the MOEA. Conversion from a partnership to a company structure requires dissolution of the existing entity and fresh incorporation. A representative office cannot convert directly into a company — it must be closed and a new legal entity registered separately.

No. Sole proprietorships and general partnerships do not possess separate legal personality, meaning owners bear unlimited personal liability for business obligations. Limited companies, companies limited by shares, and limited partnerships (in respect of the general partner's obligations) are recognised as distinct legal persons under the Company Act or the Limited Partnership Act (有限合夥法).

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.