Key Takeaways

- Tuvalu's business entities are governed primarily by the Companies Act and administered by the Registrar of Companies operating under the authority of the Tuvalu government.

- The private company limited by shares is the most commonly registered entity, suited to both resident and foreign entrepreneurs seeking operational simplicity.

- Companies limited by guarantee are the appropriate structure for non-profit and membership-based organisations operating in Tuvalu.

- Sole traders and general partnerships carry no formal registration burden but expose their owners to full personal liability under Tuvalu's regulatory framework.

Introduction to Entity Types in Tuvalu

Tuvalu is a Polynesian island nation situated in the central Pacific Ocean, lying between Hawaii and Australia. Comprising nine low-lying atolls and reef islands, it is one of the smallest and most geographically isolated sovereign states in the world.

The types of business entities in Tuvalu are governed primarily under the Companies Act and administered by the Registrar of Companies, which operates under the authority of the Tuvalu government. The jurisdiction maintains a generally low-tax posture for qualifying offshore entities, though domestic businesses are subject to standard local fiscal obligations.

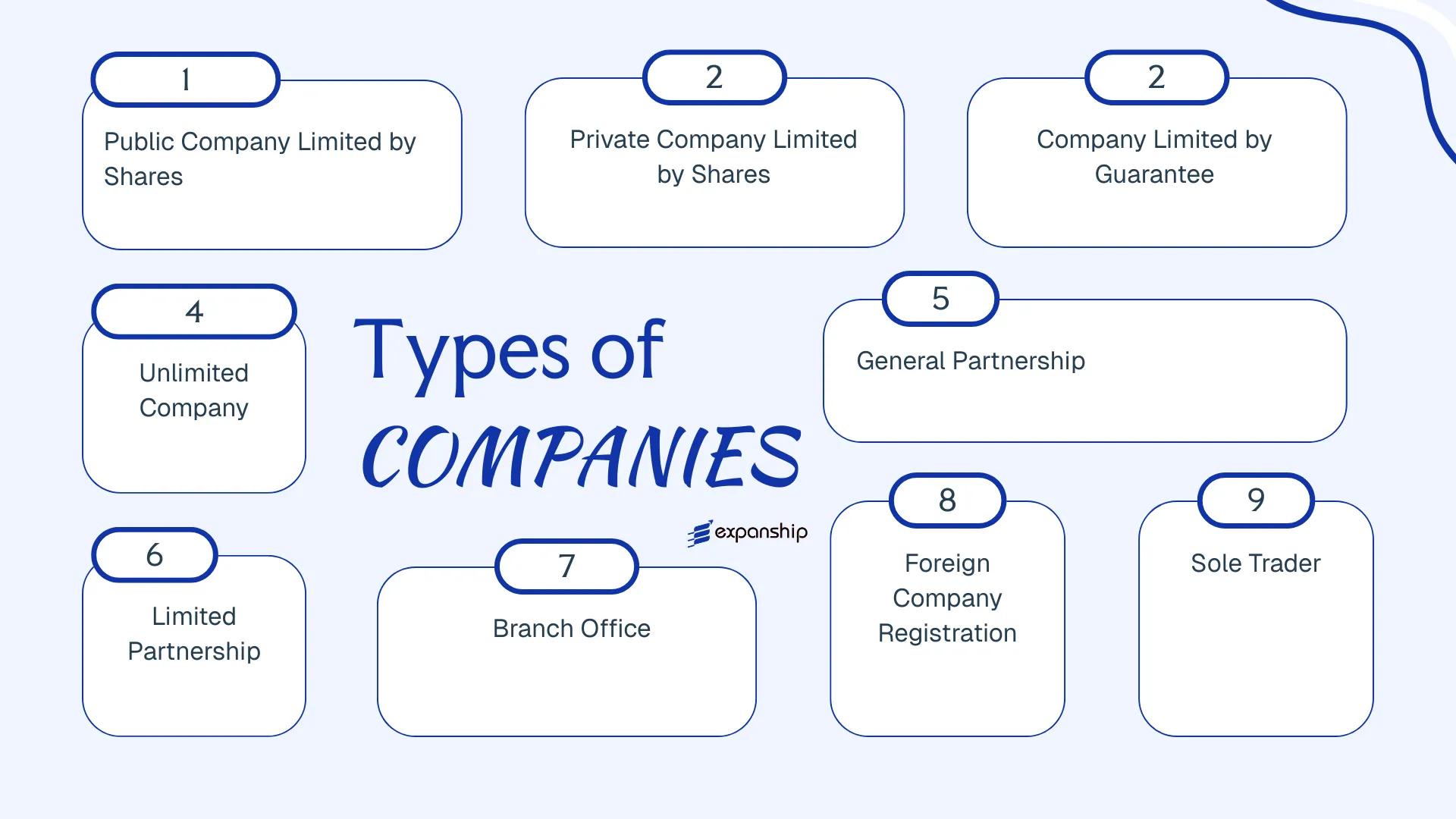

Businesses registering in Tuvalu have access to several distinct structures:

- Public Company Limited by Shares

- Private Company Limited by Shares

- Company Limited by Guarantee

- Unlimited Company

- General Partnership

- Limited Partnership

- Branch Office

- Foreign Company Registration

- Sole Trader

Each of these structures carries its own formation requirements, liability framework, and compliance obligations — this article examines each in detail to help you determine which arrangement suits your operational and legal objectives.

An Overview of Business Structures in Tuvalu

Tuvalu's corporate framework provides several distinct entity types, each governed primarily by the Companies Act (Cap 2.12) and, for certain specialised vehicles, supplementary legislation administered by the Tuvalu Business Registry. Each structure carries different implications for liability, taxation, membership, and permitted activities. The sections that follow examine each one in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company Limited by Shares | Incorporated company | Limited to shares | Taxed | Yes | 2 shareholders | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| Private Company Limited by Shares | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed | Yes | 1 member | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| Unlimited Company | Incorporated company | Unlimited | Taxed | Yes | 1 shareholder | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| General Partnership | Unincorporated | Joint and several | Taxed | Yes | 2 partners | Tuvalu Business Registry | General law / partnership rules |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 1 GP + 1 LP | Tuvalu Business Registry | General law / partnership rules |

| Branch Office | Foreign entity extension | Parent liability | Taxed | Yes | N/A | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| Foreign Company Registration | Registered foreign body | Parent liability | Taxed | Yes | N/A | Tuvalu Business Registry | Companies Act (Cap 2.12) |

| Sole Trader | Unincorporated individual | Unlimited | Taxed | Yes | 1 person | Tuvalu Business Registry | General law |

Each of these structures is examined in full in the sections below.

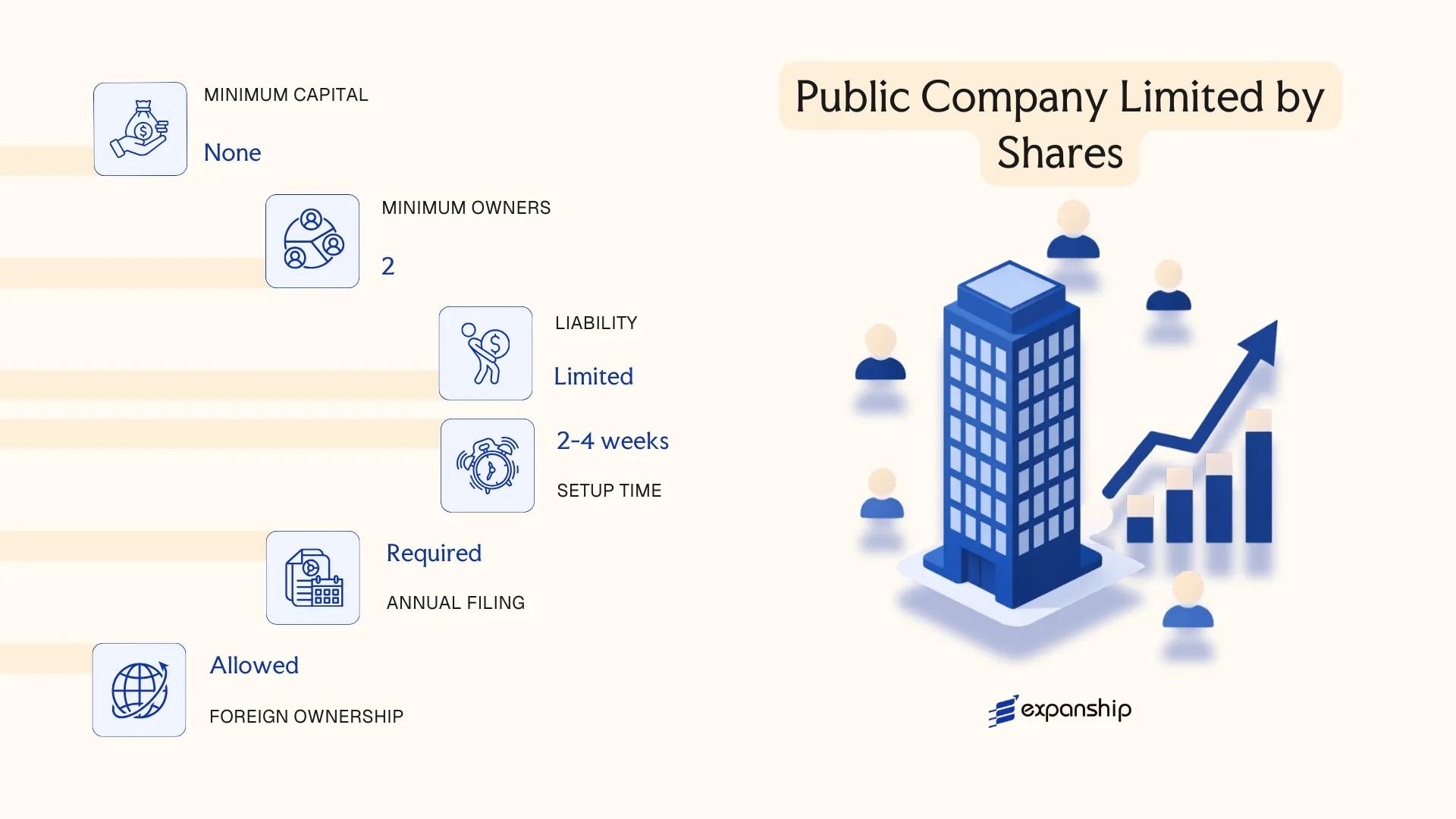

Public Company Limited by Shares

A Tuvalu public company limited by shares is governed by the Companies Act 2008, the principal legislation regulating corporate entities across the jurisdiction. The structure carries separate legal personality, meaning the company exists independently of its shareholders, whose liability is confined to the amount unpaid on their shares.

Shares in a public company may be offered to the general public, distinguishing it from its private counterpart. This makes it the appropriate vehicle when broad capital-raising or eventual listing is a consideration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under the Companies Act 2008 |

| Members | Shareholders; minimum 2, no statutory maximum | Directors: minimum 1; no residency requirement specified under general provisions |

| Local Presence | Registered office in Tuvalu required | A registered agent is typically maintained to fulfil this obligation |

| Share Capital | No statutory minimum capital prescribed | Denominated in Australian dollars (AUD), Tuvalu's functional currency |

| Privacy | Shareholder and director details filed with the Registrar of Companies | Public register; details are accessible upon request |

Focus Points

- Taxation: Tuvalu does not impose corporate income tax, withholding tax, or capital gains tax; VAT and other indirect taxes may apply to domestic transactions depending on business activity.

- Economic Substance: No formal economic substance regime currently applies, though this position may evolve with international compliance expectations.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; audited financial statements may be required for public entities.

- Treaty Access: Tuvalu has a limited tax treaty network, which restricts access to double taxation relief for cross-border structures.

- Conversion: A public company may generally be re-registered as a private company subject to meeting the relevant conditions under the Companies Act 2008.

Recommendations

A public company limited by shares suits larger commercial operations or ventures anticipating future capital market activity, with the primary advantage of unrestricted share transferability. The principal limitation is the higher compliance burden relative to private structures, including public disclosure obligations that reduce confidentiality.

This structure is most appropriate for established businesses seeking public investment or operating in sectors that require broad shareholding capacity.

Company Incorporation in Tuvalu

Incorporate a public or private company in Tuvalu with Expanship's end-to-end incorporation support.

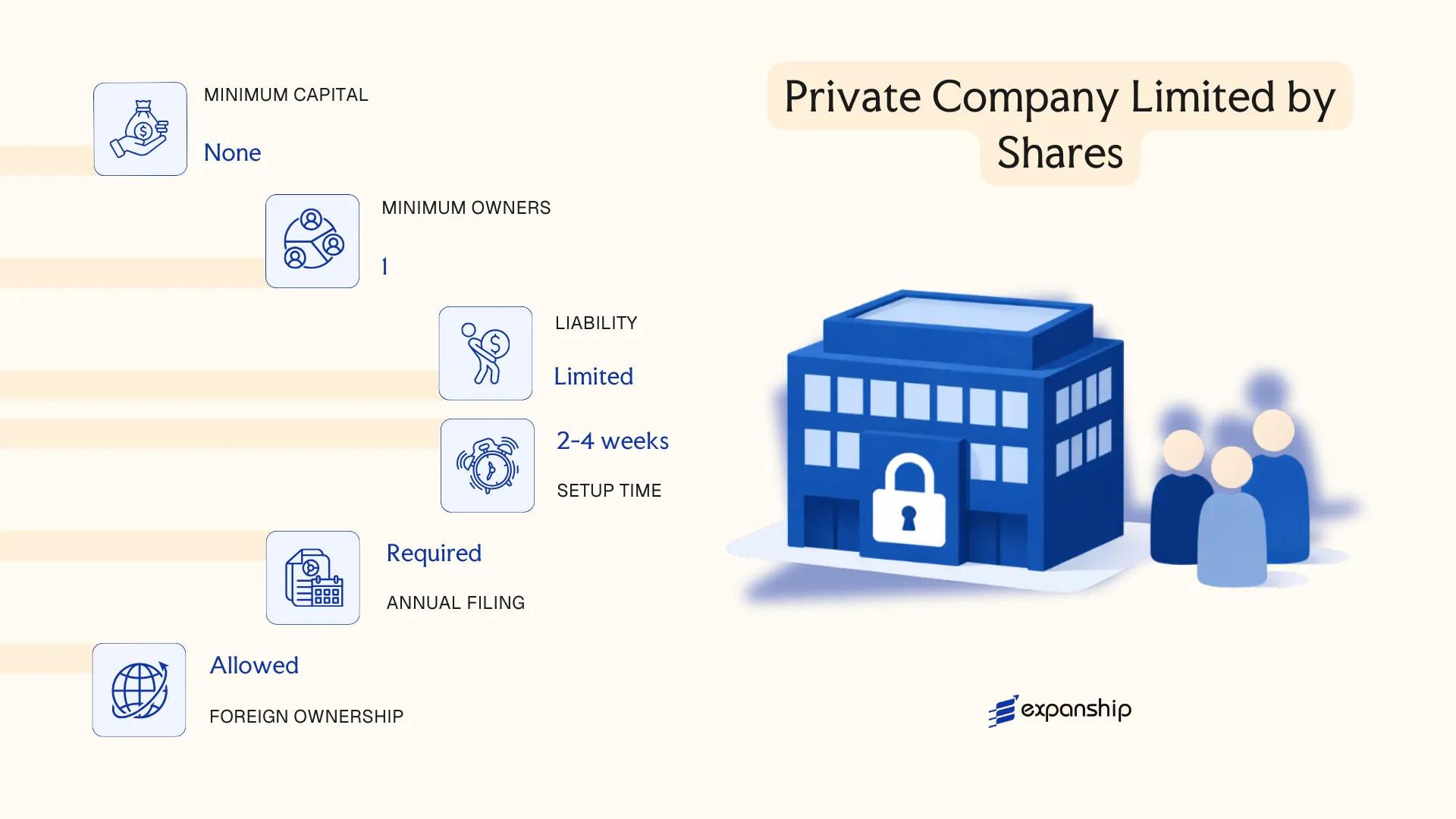

Private Company Limited by Shares

A Tuvalu private company limited by shares is governed by the Companies Act 2008, which establishes the core framework for incorporation, governance, and dissolution. The entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name, distinct from its shareholders.

Shareholder liability is capped at the amount unpaid on their shares. This structure makes it a practical choice for both domestic operations and international holding arrangements under Tuvalu Ltd company formation procedures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under the Companies Act 2008 |

| Members | Shareholders (1–50) | A sole shareholder is permitted; public subscription is prohibited |

| Directors | Minimum 1 director | No residency requirement under the Act |

| Local Presence | Registered office and registered agent required | Must maintain a physical address in Tuvalu |

| Share Capital | No statutory minimum; denominated in any currency | Shares may or may not have par value |

| Privacy | Beneficial ownership records held by registered agent | Register of members not publicly searchable |

Focus Points

- Taxation: Tuvalu does not impose corporate income tax, capital gains tax, or withholding tax on private companies; VAT and stamp duty obligations may apply to specific transactions.

- Annual Compliance: Companies must file an annual return and maintain statutory registers; failure to comply may result in deregistration.

- Economic Substance: Tuvalu has adopted economic substance requirements aligned with international standards; certain business activities may trigger local substance obligations.

- Treaty Access: Tuvalu has a limited tax treaty network, which may restrict access to reduced withholding rates in counterparty jurisdictions.

- Conversion: A private company may be converted to a public company by amending its constitution and meeting the relevant statutory thresholds under the Companies Act 2008.

Recommendations

Private company limited by shares registration in Tuvalu suits trading operations, international holding structures, and asset-holding vehicles where liability protection is required. The absence of corporate income tax is a material advantage, though the limited treaty network may constrain cross-border tax planning for certain investor profiles.

This entity type is best suited for founders and international investors seeking a liability-protected, tax-neutral vehicle for holding or trading activities without complex governance requirements.

Company Limited by Guarantee

A Tuvalu company limited by guarantee (CLG) is governed by the Companies Act 2008, administered by the Tuvalu Companies Registry under the Ministry of Finance. Unlike a share-based structure, the entity has no share capital; instead, members commit to contributing a defined sum toward the company's debts if it is wound up.

The CLG holds separate legal personality, meaning it can own assets, enter contracts, and sue or be sued in its own name. This structural separation makes the guarantee company Tuvalu framework particularly suited to non-commercial purposes where member liability must remain capped.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company Limited by Guarantee | Incorporated under the Companies Act 2008 |

| Members | Minimum 1; no statutory maximum | Referred to as members, not shareholders |

| Governance | Minimum 1 director | Directors need not be Tuvaluan residents |

| Local Presence | Registered office and registered agent required in Tuvalu | Must maintain a physical address on the islands |

| Capital | No share capital; guarantee amount defined in constitution | Guarantee sum is typically nominal (e.g., USD 1–100 per member) |

| Privacy | Director and member details held on public register | Beneficial ownership rules apply under general corporate law |

Focus Points

- Taxation: Tuvalu does not levy corporate income tax, capital gains tax, or VAT, and there are no withholding taxes on distributions from a CLG; stamp duty obligations may apply to certain instruments.

- Annual Compliance: Filing of annual returns with the Tuvalu Companies Registry is required; financial statements may be required depending on activity level.

- Economic Substance: No formal economic substance regime comparable to larger offshore centres is currently enacted in Tuvalu.

- Conversion: Conversion from a CLG to a company limited by shares is generally permissible under the Companies Act 2008, subject to registry approval and constitutional amendment.

- Restrictions: A CLG may not distribute profits or assets to members during its operation; any surplus must be applied toward the entity's stated objects.

Closing

A guarantee company suits associations, charities, and member-based organisations where profit distribution is neither intended nor permitted. The absence of share capital simplifies the governance structure, though the restriction on member distributions makes this form unsuitable for any venture with commercial return objectives.

Non-profit company structures in Tuvalu, including professional associations, community organisations, and foundations that require separate legal personality without a profit-distribution mechanism.

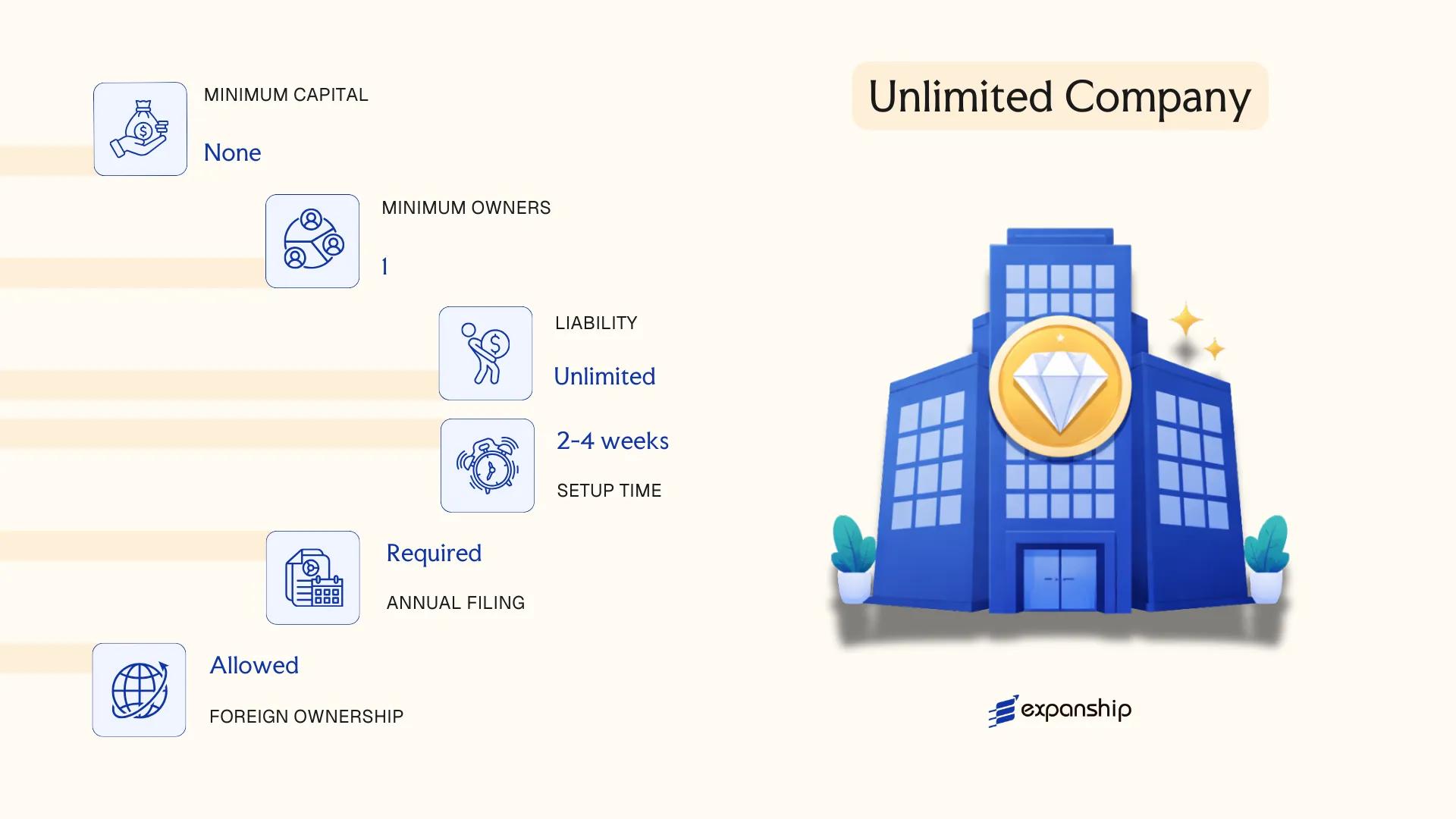

Unlimited Company

Tuvalu unlimited company registration is governed by the Companies Act 2008, administered by the Tuvalu Companies Registry under the Ministry of Finance. Unlike limited liability structures, an unlimited company carries no cap on the personal liability of its members — each member remains fully exposed to the debts and obligations of the business.

As a registered entity, the firm still holds separate legal personality, meaning it can contract, sue, and hold assets in its own name. This combination of corporate status with unrestricted member liability makes the unlimited company a structurally distinct formation that suits specific operational and planning purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited Company | Separate legal personality; no liability cap on members |

| Members | Referred to as shareholders; minimum 1, no statutory maximum | Single-member unlimited companies are permitted |

| Local Presence | Registered agent and registered office required in Tuvalu | Must be maintained continuously |

| Share Capital | No prescribed minimum; denominated in Australian dollars (AUD) | Capital structure is flexible |

| Privacy | Beneficial ownership disclosures apply under the Companies Act 2008 | Register is maintained by the Companies Registry |

Focus Points

- Taxation: Tuvalu does not impose corporate income tax, withholding tax, or VAT, making the tax burden primarily a matter of members' home jurisdictions.

- Annual Compliance: Annual returns must be filed with the Companies Registry; failure to file can result in deregistration.

- Economic Substance: No formal economic substance regime is currently in force.

- Conversion: The Companies Act 2008 permits conversion between company types, subject to Registry approval and member consent.

- Restrictions: No specific prohibition on foreign ownership, but certain regulated activities may require additional licensing.

Closing

The unlimited liability company Tuvalu structure is used principally where full asset transparency between the entity and its members is acceptable or desirable, such as in professional services arrangements or within group structures where the parent entity absorbs liability. The absence of a liability cap is a significant legal exposure for individual members.

Best suited for professional firms or intra-group holding arrangements where the owning entity, rather than an individual, bears member liability.

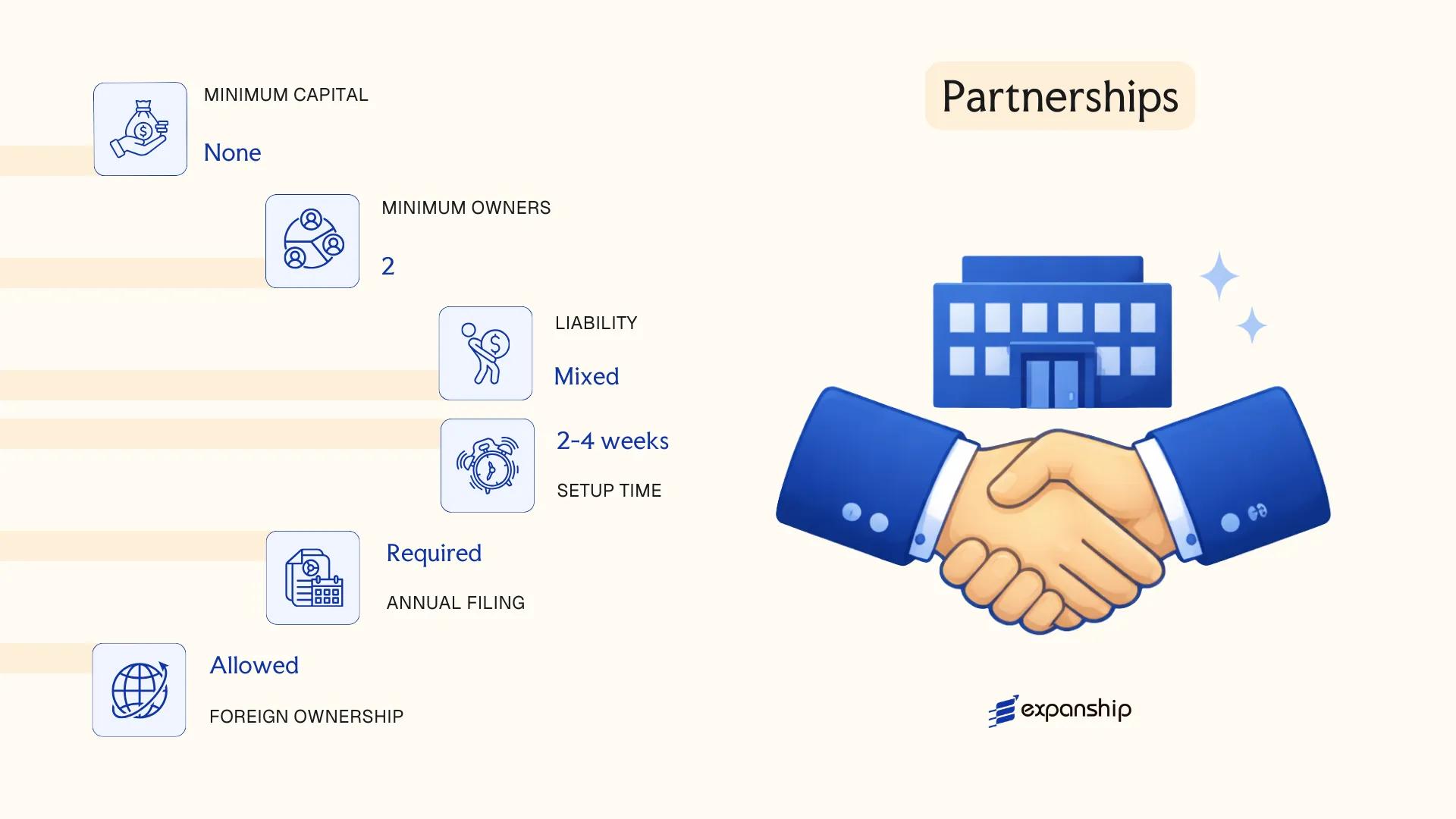

Partnerships [General Partnership, Limited Partnership]

Tuvalu general and limited partnership structures are governed by the Partnership Act (Cap. 149), which follows principles derived from English common law. Neither a general nor a limited partnership constitutes a separate legal entity distinct from its partners, meaning partners bear direct exposure to the obligations of the firm.

Registration of a partnership in Tuvalu is administered through the Registrar of Companies and Cooperative Societies. A general partnership requires no formal registration to exist, though a limited partnership must be registered to confer liability protection on its limited partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality |

| Members | Partners (minimum 2) | General partnership: unlimited partners; Limited partnership: at least 1 general + 1 limited partner |

| Local Presence | Registered address required | Local registered agent advisable for compliance |

| Capital | No minimum; Tuvaluan Dollar (AUD) | Contributions defined by partnership agreement |

| Privacy | Partnership agreement not publicly filed | Partner names may appear on registration records |

Focus Points

- Taxation: No corporate income tax, capital gains tax, VAT, or withholding tax currently applies in Tuvalu; partners are taxed on personal income where applicable.

- Liability: General partners carry unlimited personal liability; limited partners are liable only to the extent of their capital contribution.

- Annual Compliance: Limited partnerships must maintain registration and file any required updates with the Registrar.

- Restrictions: Foreign nationals may face restrictions on conducting certain regulated activities through a partnership structure.

- Conversion: Conversion from a partnership to a corporate entity is possible but requires a fresh incorporation process.

Sub-Types

General Partnership

All partners participate in management and share unlimited liability for the firm's debts. This structure suits small professional practices or joint ventures where partners have equal standing.

Limited Partnership

At least one general partner retains unlimited liability and management authority, while limited partners contribute capital and remain passive. Tuvalu limited partnership formation is suited to investment arrangements where capital contributors seek liability containment.

Closing

Partnerships are primarily used for small trading operations or joint ventures where a formal corporate structure is unnecessary. The absence of a minimum capital requirement offers flexibility, though unlimited liability for general partners represents a material risk for commercially active businesses.

This structure is best suited for small, closely held ventures or professional collaborations where the partners know each other well and the scale of liability exposure is manageable.

Foreign Business Vehicles [Branch Office, Foreign Company Registration]

Tuvalu foreign company registration is governed by the Companies Act 2008, which sets out the process by which overseas entities may conduct business through a locally registered presence. A foreign company registered under the Act does not acquire a separate legal personality distinct from its parent; it remains an extension of the originating entity, meaning the parent retains full liability for the branch's obligations.

Registering to open a branch office in Tuvalu requires filing with the Registrar of Companies, submitting certified constitutional documents of the foreign parent, details of local agents, and a registered address within the jurisdiction. The branch is not a standalone legal structure — it is a conduit through which the parent transacts.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Registered Foreign Company | Not a separate legal entity; an extension of the parent |

| Registered Representative | Local registered agent required | Must maintain a registered address in Tuvalu |

| Governing Documents | Certified copy of parent's constitution or equivalent | Must be filed with the Registrar of Companies |

| Liability | Unlimited; borne by the parent entity | No liability shield between branch and parent |

| Capital | No prescribed minimum | Parent's capital structure applies |

| Privacy | Parent entity details are filed on public record | Director and agent information disclosed |

Focus Points

- Taxation: Tuvalu does not impose corporate income tax, withholding tax, or VAT, so branch profits are generally not taxed locally; the parent's home jurisdiction determines the effective tax treatment.

- Economic Substance: No formal economic substance regime is currently in force.

- Annual Compliance: Ongoing obligations include filing annual returns and maintaining a current registered agent; failure to comply may result in deregistration.

- Treaty Access: Tuvalu has a limited double tax treaty network, which restricts treaty-based tax planning through a branch structure.

- Restrictions: Certain regulated activities may require sector-specific licensing in addition to foreign business registration in Tuvalu.

Closing

A registered foreign company is used primarily when a business needs a formal local presence for operational or contractual reasons without establishing a separately incorporated subsidiary. The main advantage is the avoidance of a separate incorporation process; the principal drawback is the absence of liability insulation between the branch and the parent.

This structure suits established foreign businesses that require a defined local footprint for short-to-medium-term operations and can accept full parental liability exposure.

Sole Trader

Sole trader registration in Tuvalu establishes the simplest form of business operation available under Tuvaluan law. Unlike incorporated entities, a sole trader has no separate legal personality — the individual and the business are legally the same person, meaning personal assets are exposed to business liabilities without limitation.

Registration is handled through the relevant government registry under Tuvalu's business registration framework. The process is straightforward, requiring the proprietor to register a business name if trading under a name other than their own.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital partner or co-owner permitted |

| Liability | Unlimited personal liability | Personal assets at risk for all business debts |

| Local Presence | Business address in Tuvalu required | No separate registered agent requirement |

| Capital | No statutory minimum | Funded entirely by the proprietor |

| Privacy | Owner's name publicly linked to the business | Limited privacy protection |

Focus Points

- Taxation: Sole traders are taxed at the individual income tax rate on business profits; no separate corporate tax applies, and Tuvalu does not impose VAT or general capital gains tax.

- Annual Compliance: Business name renewals are required periodically; no separate annual return filing equivalent to a company structure.

- Treaty Access: As an unincorporated individual, access to double tax treaty benefits is limited and context-dependent.

- Conversion: A sole trader can convert to an incorporated entity, though this requires a fresh registration process with no automatic asset transfer mechanism.

- Restrictions: Foreign nationals face restrictions on operating as sole traders and may require specific permits under Tuvalu's foreign investment rules.

Closing

A sole trader structure suits local residents running small-scale or service-based operations where administrative simplicity outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, but unlimited personal liability remains a significant structural constraint.

Local residents operating low-risk, owner-run service businesses who prioritise minimal compliance overhead over liability protection.

How to Choose the Right Entity Type in Tuvalu

Selecting how to choose a business entity in Tuvalu requires more than a general preference — the structure you register determines your legal exposure, tax position, and ongoing compliance obligations under the Companies Act (Cap 85).

Why Your Entity Choice Matters

An unsuitable structure produces concrete, avoidable consequences:

- Registering an offshore-oriented entity while conducting local trade places your business in breach of the Companies Act, potentially resulting in striking off or financial penalties.

- Choosing a tax-exempt entity when your operations require treaty access disqualifies your firm from claiming withholding tax reductions available under bilateral agreements.

- Selecting an unlimited company or guarantee structure when your situation calls for defined shareholder liability exposes members to personal claims against business debts.

- Forming a shareholding structure when a trust arrangement would serve your estate planning needs locks you into annual shareholder obligations that do not apply to trust-based vehicles.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point toward distinct structures under Tuvaluan company law.

- Local vs. Offshore Operations: Entities transacting with Tuvalu residents face different registration and licensing requirements than those operating entirely abroad.

- Ownership and Management: Single-owner operations and multi-party arrangements have different governance requirements across company and partnership structures.

- Liability Exposure: Your tolerance for personal liability should directly determine whether you form a limited or unlimited entity.

- Exit Strategy: Not all structures permit redomiciliation or conversion — confirm this before registering.

Compliance Services for Companies in Tuvalu

Conclusion

Setting up a company in Tuvalu means selecting from a defined set of structures governed primarily by the Companies Act. Private companies limited by shares suit most resident and foreign entrepreneurs seeking operational simplicity. Public companies serve ventures requiring broader capital access, while companies limited by guarantee fit non-profit and membership-based organisations. Unlimited companies remain rare, used where liability exposure is accepted in exchange for structural flexibility. Sole traders and general partnerships involve no formal registration burden but carry full personal liability.

The private company limited by shares is by far the most commonly registered entity. Foreign businesses typically enter through branch registration or a locally incorporated subsidiary rather than operating informally.

Tuvalu's regulatory framework continues to develop, with gradual attention to international compliance standards shaping the direction of corporate governance. Your specific requirements around liability, tax treatment, and operational scope will determine which structure warrants closer examination.

How Expanship Can Assist You

Expanship's Tuvalu company formation services cover the full process of registering entities under the Companies Act of Tuvalu, from selecting the appropriate structure — whether a private company limited by shares, a company limited by guarantee, or a foreign branch registration — through to meeting ongoing obligations with the Tuvalu Companies Registry.

Expanship handles the procedural and administrative side of your business setup in Tuvalu, so you can focus on operations from day one.

- Document preparation and notarization

- Registered agent and registered office provision

- Filing and liaison with the Tuvalu Companies Registry

- Post-incorporation compliance management

- Banking introduction assistance

Ready to move forward? Reach out to Expanship Tuvalu to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently formed entity. Its combination of limited liability, flexible share structure, and relatively straightforward registration requirements makes it the default choice for most commercial activities.

A private company limits shareholder liability to unpaid share capital, whereas members of an unlimited company face uncapped personal exposure to the firm's debts. Unlimited companies are not subject to the same public disclosure requirements for financial statements, which makes them attractive where confidentiality outweighs the liability concern.

An unlimited company generally discloses less financial information publicly than a company limited by shares. Nominee director and shareholder arrangements are available under Tuvaluan practice, though ultimate beneficial ownership may still be subject to regulatory inquiry.

A sole trader operates as a single individual by definition. Partnerships, whether general or limited, require at least two parties. A private company limited by shares can be formed with a single shareholder and director.

Foreign nationals may register a private company, public company, unlimited company, or company limited by guarantee. Those conducting business through an overseas vehicle may register a branch under foreign company provisions. General partnerships impose no nationality restrictions, though local licensing requirements may apply depending on the activity.

Re-registration between company types is generally permissible under the Companies Act framework. A private company may convert to a public company, and an unlimited company may re-register as a company limited by shares, subject to Registrar approval and prescribed procedural steps.

Registered companies, including public and private companies limited by shares, companies limited by guarantee, and unlimited companies, possess separate legal personality under the Companies Act. General partnerships do not form a distinct legal person, meaning partners remain personally liable for partnership obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.