Key Takeaways

- The private company limited by shares, governed by the Companies Act Chapter 81:01, is the most widely used structure in Trinidad and Tobago for both resident entrepreneurs and foreign investors due to its liability protection and operational flexibility.

- Business registration in Trinidad and Tobago is administered by the Companies Registry, a division of the Ministry of the Attorney General and Legal Affairs, which processes incorporations under the Companies Act Chapter 81:01.

- General partnerships carry unlimited personal liability for all partners, whereas limited partnerships extend a degree of liability protection to passive partners under the Partnership Act Chapter 82:01.

- Foreign businesses seeking a presence in Trinidad and Tobago without local incorporation may do so through an external company or branch office structure.

Introduction to Entity Types in Trinidad and Tobago

Trinidad and Tobago is a twin-island republic situated at the southern end of the Caribbean archipelago, positioned just off the northeastern coast of Venezuela. As an independent nation and member of CARICOM, it operates a common law legal system inherited from British colonial administration. Business registration falls under the jurisdiction of the Companies Registry, a division of the Ministry of the Attorney General and Legal Affairs, which processes incorporations under the Companies Act, Chapter 81:01.

Understood as a territorial tax jurisdiction, Trinidad and Tobago taxes income sourced within its borders, with double taxation treaties in place with several countries.

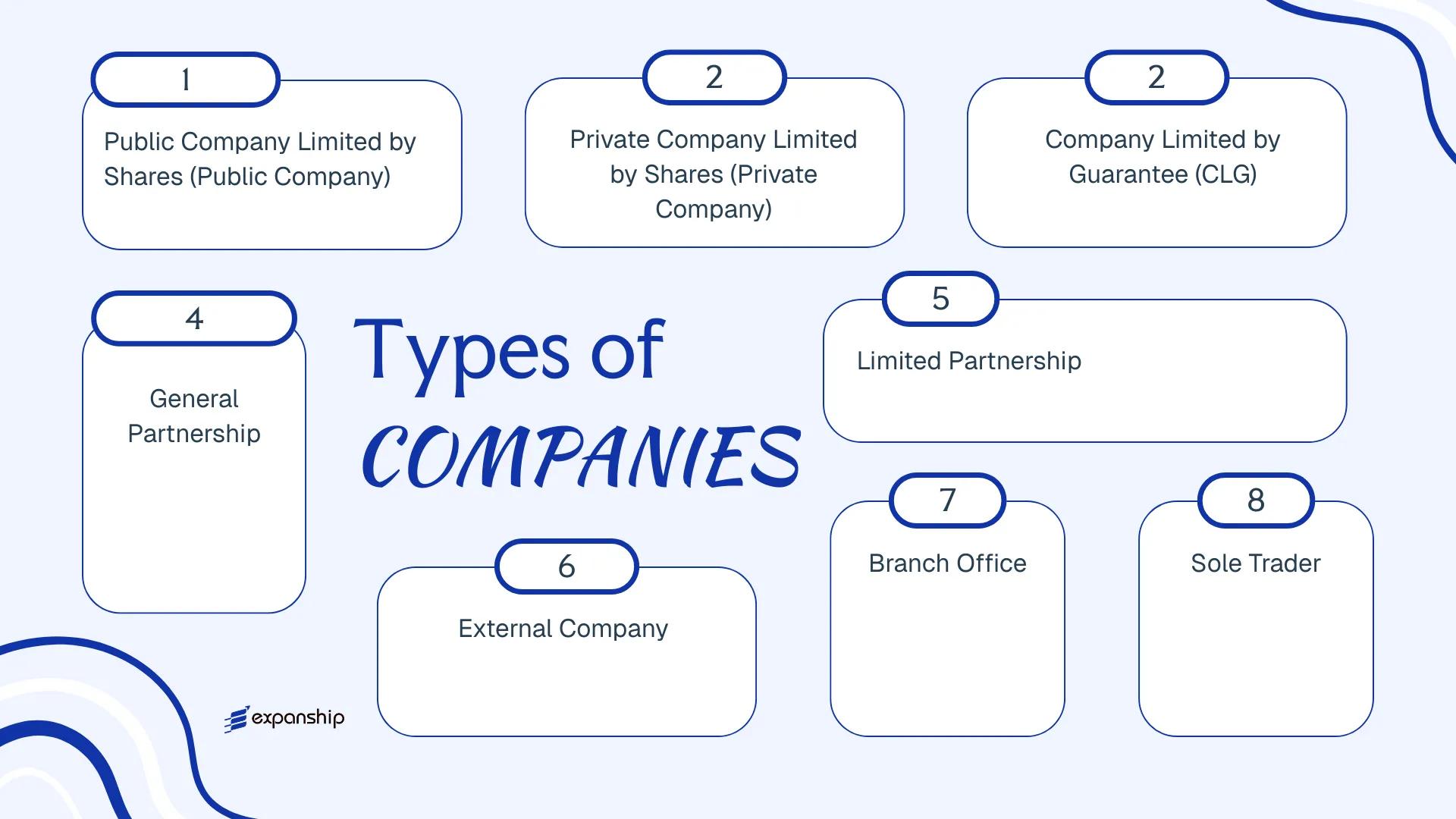

The business entity types available under local law include the private company limited by shares, the public company limited by shares, the company limited by guarantee, the general partnership, the limited partnership, the external company, the branch office, and the sole trader. Each structure carries distinct formation requirements, liability implications, and ongoing compliance obligations. This article examines each of those structures in detail to help you determine which registration option suits your business objectives.

An Overview of Business Structures in Trinidad and Tobago

Several distinct entity types are available to businesses operating under the country's company law framework, with the Companies Act, Chap. 81:01 serving as the primary legislation governing corporate structures. The Registration of Business Names Act, Chap. 82:85 and the Limited Partnerships Act, Chap. 83:04 govern unincorporated and partnership arrangements respectively. Each entity type carries different implications for liability, ownership, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company | Incorporated body | Limited | Taxed | Yes | 1 director, 1 shareholder | Companies Registry | Companies Act, Chap. 81:01 |

| Private Company | Incorporated body | Limited | Taxed | Yes | 1 director, 1 shareholder | Companies Registry | Companies Act, Chap. 81:01 |

| Company Limited by Guarantee | Incorporated body | Limited to guarantee | Taxed / Exempt | Yes | 1 director, 1 member | Companies Registry | Companies Act, Chap. 81:01 |

| General Partnership | Unincorporated | Unlimited | Taxed at partner level | Yes | 2 partners | Registrar General | Registration of Business Names Act |

| Limited Partnership | Unincorporated | Mixed | Taxed at partner level | Yes | 1 general, 1 limited partner | Registrar General | Limited Partnerships Act, Chap. 83:04 |

| External Company | Registered foreign body | Limited | Taxed on local income | Yes | N/A | Companies Registry | Companies Act, Chap. 81:01 |

| Branch Office | Foreign entity presence | Limited | Taxed on local income | Yes | N/A | Companies Registry | Companies Act, Chap. 81:01 |

| Sole Trader | Unincorporated individual | Unlimited | Taxed personally | Yes | 1 person | Registrar General | Registration of Business Names Act |

Each of these structures is examined in full in the sections below.

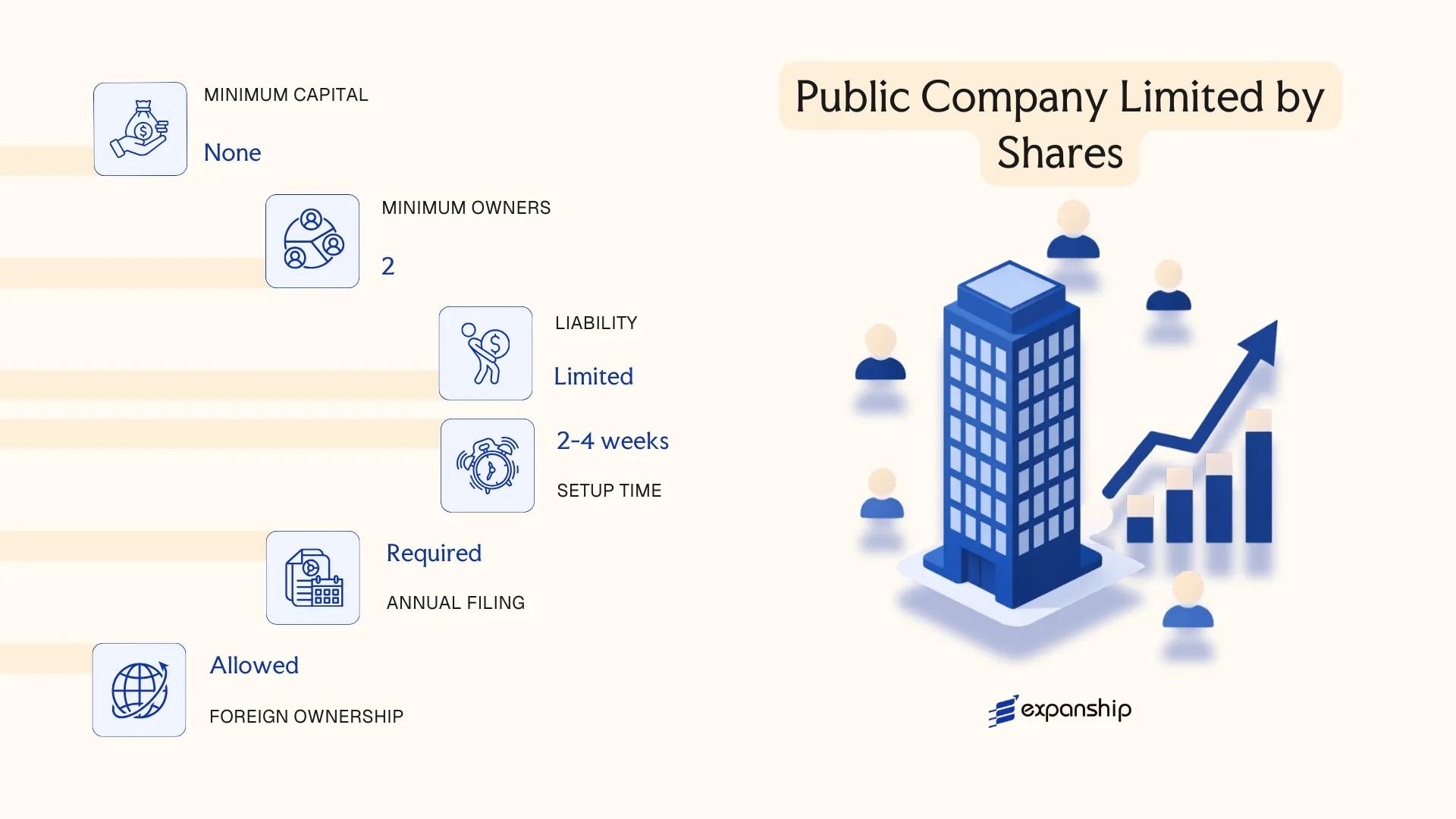

Public Company Limited by Shares

A public company limited by shares in Trinidad and Tobago is governed by the Companies Act, Chapter 81:01, which was significantly modernised when the Companies Act 1995 came into force. The entity holds a separate legal personality from its shareholders, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares.

Shares in a public company may be offered to the general public and, subject to approval by the Trinidad and Tobago Securities and Exchange Commission (TTSEC), listed on the Trinidad and Tobago Stock Exchange (TTSE). This distinguishes it structurally from its private counterpart, which carries restrictions on share transfers and public offerings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public company limited by shares | Incorporated under the Companies Act, Ch. 81:01 |

| Governed By | Companies Act 1995 (Ch. 81:01); TTSEC for listed entities | Dual regulatory oversight applies once listed |

| Members | Shareholders – minimum 1, no maximum | Shares freely transferable; no restriction on public subscription |

| Directors | Minimum 2 directors required | At least one must ordinarily reside in Trinidad and Tobago |

| Registered Office | Must maintain a registered office in Trinidad and Tobago | Required for service of documents and official correspondence |

| Capital | Denominated in TTD; no statutory minimum share capital | Authorised capital declared in articles of incorporation |

| Privacy | Directors and shareholders on public record | Financial statements filed with the Registrar of Companies are accessible |

Focus Points

- Taxation: Subject to corporation tax at the standard rate (currently 30%, or 25% for certain qualifying companies); VAT registration required if annual turnover exceeds the threshold; dividends paid to non-residents attract withholding tax; stamp duty applies on share transfers.

- Annual Compliance: Must file audited financial statements and annual returns with the Registrar of Companies; listed entities face additional periodic disclosure obligations under TTSEC rules.

- Treaty Access: Trinidad and Tobago has a limited network of double taxation agreements; a locally incorporated public company can access applicable treaty benefits on income flows.

- Economic Substance: No OECD-style economic substance regime applies at present, but regulatory scrutiny for listed entities is higher given TTSEC disclosure requirements.

- Conversion: A private company may be re-registered as a public company under the Act by amending its articles and meeting the applicable structural requirements.

Closing

A public company limited by shares suits large-scale commercial operations, capital-intensive businesses seeking public funding, and firms pursuing a listing on the TTSE. The ability to raise equity from the public is its principal structural advantage; however, the associated regulatory burden — ongoing TTSEC oversight, mandatory audits, and public disclosure — makes it a demanding structure for smaller operations.

Best suited for established businesses with significant capital requirements that intend to raise funds from the public or pursue a stock exchange listing.

Company Incorporation in Trinidad and Tobago

Expanship assists with end-to-end incorporation of public and private companies under the Companies Act, Ch. 81:01, including registered office and compliance setup.

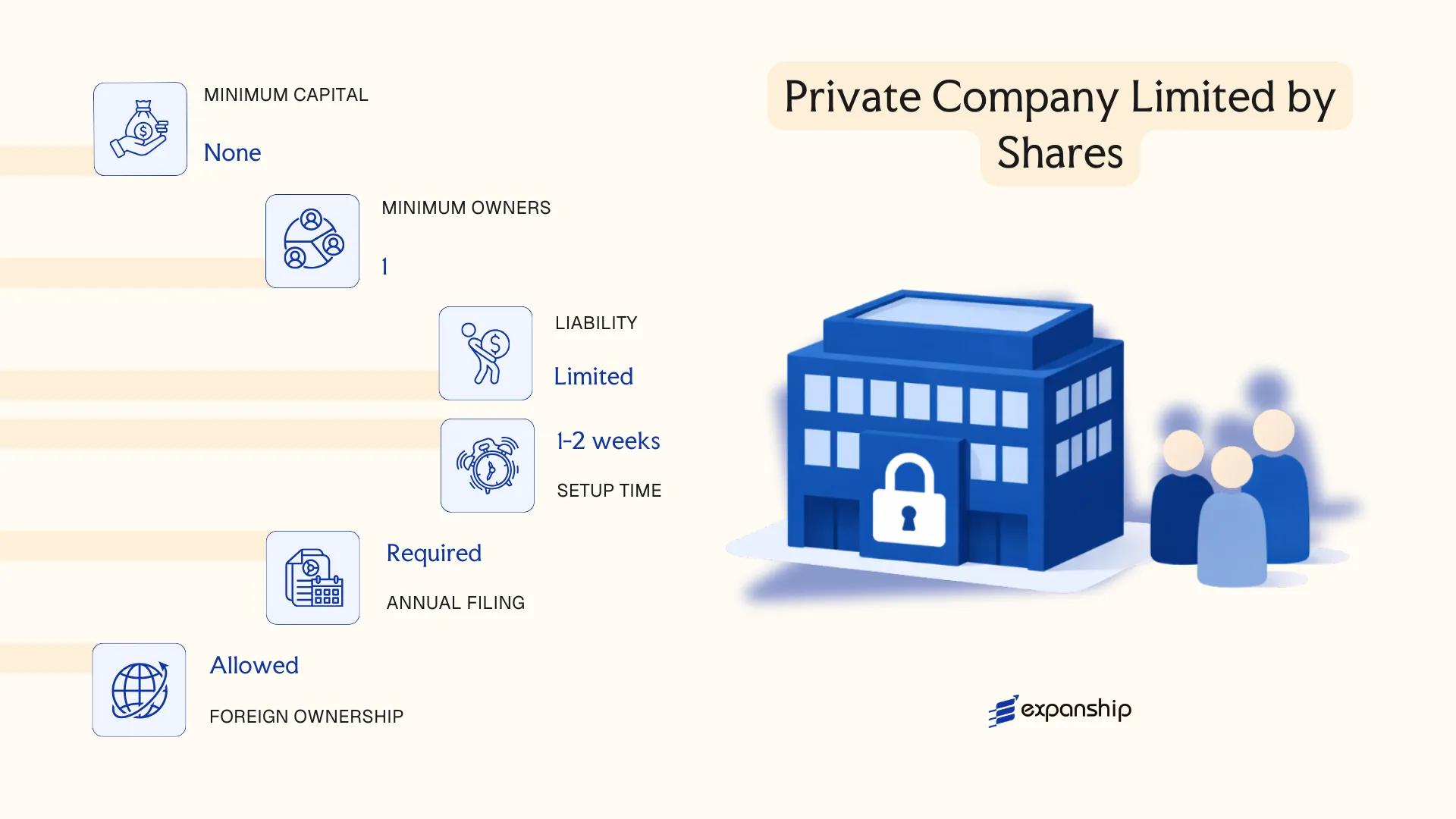

Private Company Limited by Shares

A private company limited by shares in Trinidad and Tobago is governed by the Companies Act, Chapter 81:01, which consolidates the rules on formation, management, and dissolution of incorporated entities. The structure carries separate legal personality, meaning the company can own property, enter contracts, and incur liabilities in its own name, distinct from its shareholders.

Liability exposure for each shareholder is capped at the amount unpaid on their shares. This makes the private limited company a common vehicle for both domestic operations and foreign investment into the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Incorporated under the Companies Act, Ch. 81:01 |

| Members | Shareholders: min. 1, max. 50 | Restrictions on public share transfer are required by statute |

| Directors | Min. 1 director | At least 25% of directors must be resident in Trinidad and Tobago |

| Local Presence | Registered office address required | Must be a physical address in Trinidad and Tobago; a P.O. Box does not suffice |

| Share Capital | TTD-denominated; no statutory minimum | Authorised capital declared in the Articles of Incorporation |

| Privacy | Shareholder register filed with the Registrar General | Beneficial ownership disclosure obligations apply under AML legislation |

Focus Points

- Taxation: Subject to corporation tax at 30% (25% for manufacturing companies); VAT registration required if turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and royalties paid abroad; stamp duty is payable on share transfers.

- Annual Compliance: Annual returns must be filed with the Companies Registry; audited financial statements are required unless an exemption applies for small companies.

- Economic Substance: No dedicated economic substance regime currently mirrors those in offshore-focused jurisdictions, though general tax residency and management-and-control principles apply.

- Conversion: A private company may re-register as a public company under the Companies Act by satisfying the relevant threshold and filing requirements with the Registrar General.

- Restrictions: The company's constitution must restrict the right to transfer shares and prohibit any invitation to the public to subscribe for shares or debentures.

Closing

The private company limited by shares suits trading operations, family-owned businesses, joint ventures, and domestic holding structures where shareholders prefer contained liability without the disclosure burden of a public listing. One clear limitation is the 50-shareholder ceiling, which constrains equity raises beyond a defined circle of investors.

This structure is well-suited to small and medium enterprises, foreign investors establishing a locally incorporated operating subsidiary, and entrepreneurs seeking limited liability without public reporting obligations.

Company Limited by Guarantee

A company limited by guarantee in Trinidad and Tobago is incorporated under the Companies Act, Chap. 81:01. Unlike a share-based company, members do not hold equity; instead, each member undertakes to contribute a fixed sum toward the company's liabilities in the event of winding up.

This structure carries a separate legal personality distinct from its members, and liability is capped at each member's stated guarantee amount. It functions primarily as a non-profit company structure in Trinidad and Tobago, making it the standard vehicle for charities, professional associations, trade bodies, and cultural organisations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with limited liability | Incorporated under Companies Act, Chap. 81:01 |

| Members | Referred to as members; no minimum stated in Act, typically 1 or more | No shareholders; no share capital issued |

| Guarantee Amount | Each member commits a fixed sum | Amount stated in the Memorandum of Association |

| Local Presence | Registered office in Trinidad and Tobago | Must be maintained at all times |

| Capital | No share capital; no minimum capital requirement | Income derived from grants, donations, or subscriptions |

| Privacy | Director and member details filed with the Companies Registry | Public record upon incorporation |

Focus Points

- Taxation: Generally exempt from corporation tax on qualifying non-profit income, but commercial activities may attract corporation tax at the standard rate; VAT registration required if taxable supplies exceed the threshold.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Companies Registry under the Companies Act.

- Restrictions: Cannot distribute profits or surplus to members; any surplus must be applied toward the organisation's stated objects.

- Conversion: Conversion to a share-based company is not a straightforward process under the Act and would require specific legal proceedings.

- Treaty Access: As a non-profit entity, access to double tax treaty benefits is limited and largely irrelevant to the structure's typical activities.

Closing

Guarantee companies registration in TT suits organisations whose purpose is non-commercial — particularly charities, regulatory bodies, and industry associations. The absence of share capital limits flexibility for revenue-generating ventures.

This structure is best suited for non-profit organisations, membership associations, and civil society bodies that require legal personality without distributing profits to members.

Partnerships [General Partnership, Limited Partnership]

Partnership registration in Trinidad and Tobago is governed primarily by the Partnership Act, Chap. 81:02, which applies to general partnerships, and the Limited Partnerships Act, Chap. 81:03, which provides the framework for limited partnerships. Neither structure carries separate legal personality — the partnership is not distinct from its partners in law, which has direct implications for liability and taxation.

Formed by agreement between two or more persons carrying on business in common with a view to profit, partnerships suit professional practices and joint ventures where simplicity of administration is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality under either Act |

| Members | Partners (General: 2–20; Limited: 1+ general, 1+ limited) | The Companies Act cap. 81:01 sets the 20-partner ceiling for general partnerships |

| Local Presence | Registered address required | No statutory registered agent requirement, but a local address for service is standard |

| Capital | TTD; no statutory minimum | Contributions defined by partnership agreement |

| Liability | General partners: unlimited; Limited partners: capped at contribution | Limited partners must not participate in management or lose liability protection |

| Privacy | Partnership agreements are private documents | Registration particulars are filed with the Registrar of Companies |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits are allocated to partners and taxed at their individual or corporate rates; no separate entity-level corporation tax applies, though VAT registration is required if turnover exceeds the statutory threshold.

- Annual Compliance: General partnerships have minimal filing obligations; limited partnerships must maintain registration and notify the Registrar of material changes under the Limited Partnerships Act.

- Treaty Access: Because partnerships lack separate legal personality, access to double taxation treaties depends on the residence and status of the individual partners.

- Conversion: A partnership cannot convert directly into a company without dissolution and fresh incorporation under the Companies Act, Chap. 81:01.

- Restrictions: Foreign nationals may participate as partners, but any partner carrying on regulated activities (financial services, legal practice) must satisfy the relevant sectoral licensing requirements.

Sub-Types

General Partnership

All partners bear joint and several liability for the firm's debts and obligations. Management rights are shared equally unless the partnership agreement specifies otherwise, making this structure common among professional service providers such as law firms and accountancy practices.

Limited Partnership

Registered under the Limited Partnerships Act, Chap. 81:03, this structure introduces at least one general partner with unlimited liability alongside one or more limited partners whose exposure does not exceed their agreed capital contribution. Limited partners are passive investors — active participation in management extinguishes their liability protection.

When to Consider a Partnership

Partnerships work best for professional practices, joint ventures with a defined scope, and domestic trading arrangements where the partners prefer pass-through taxation over corporate formalities. The absence of separate legal personality means the structure offers less creditor protection than a limited company.

Resident professionals and domestic joint venture participants who require a straightforward, low-compliance structure and are prepared to accept personal liability exposure.

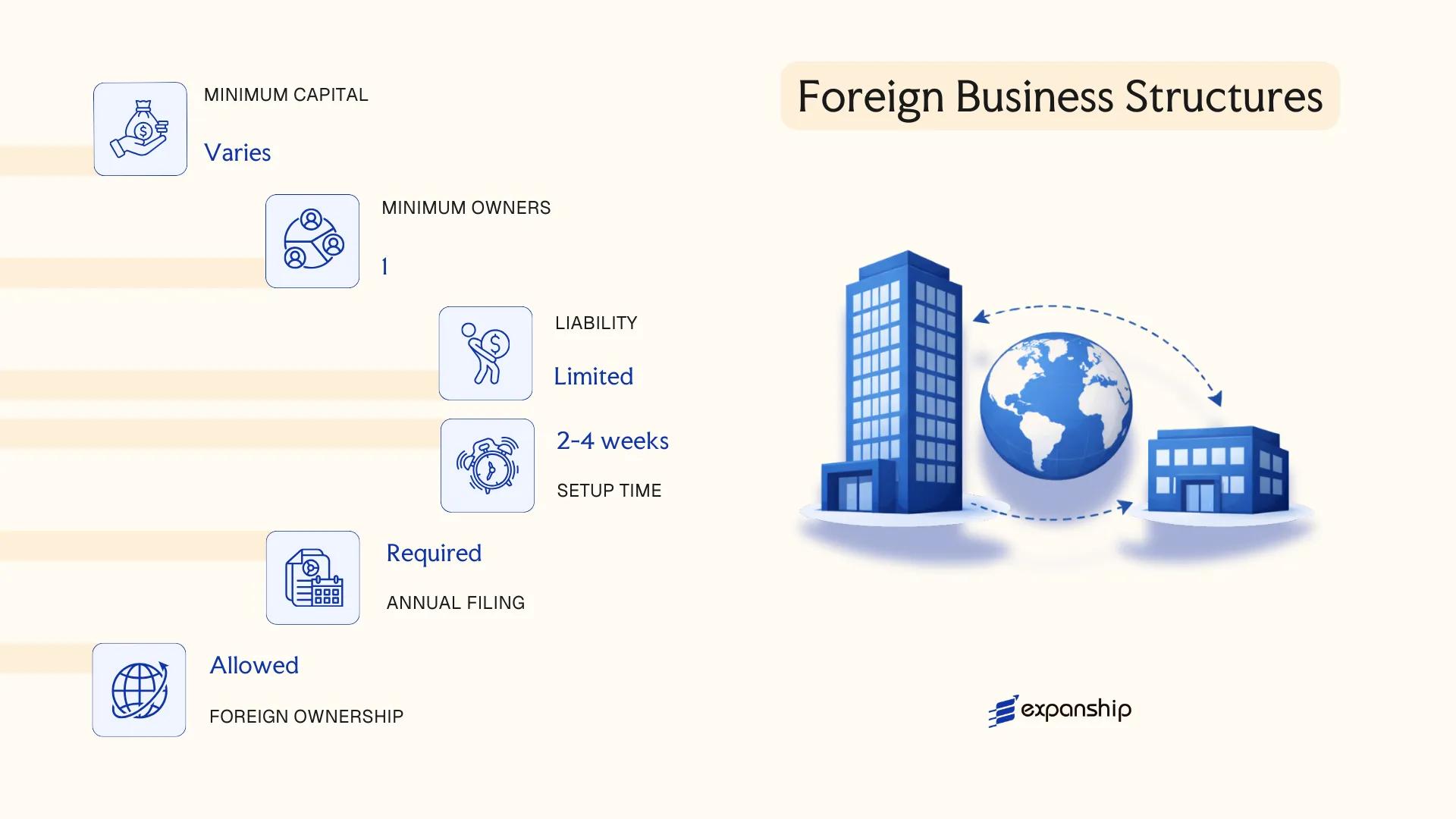

Foreign Business Structures [External Company, Branch Office]

Foreign businesses seeking to operate in Trinidad and Tobago without forming a separate local entity have two primary options under the Companies Act, Chap. 81:01: registration as an External Company or establishment of a Branch Office. Both structures allow a foreign corporation to conduct business under its existing legal personality rather than incorporating a new subsidiary.

External company registration in Trinidad and Tobago requires the overseas firm to file with the Registrar General's Department, submitting certified constitutional documents, a list of directors, and details of a locally appointed agent. The foreign entity remains legally identical to its parent — it does not acquire separate legal personality in Trinidad and Tobago, meaning the parent corporation bears full liability for local operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of a foreign corporation | No separate legal personality; parent retains full liability |

| Local Representative | Registered agent required | Must be a resident individual or local firm |

| Registered Office | Local address mandatory | Must be maintained for service of documents |

| Capital | No minimum prescribed locally | Parent's capital structure governs |

| Filing Obligations | Annual return + audited financials | Submitted to the Registrar General's Department |

| Privacy | Director details on public record | Constitutional documents of parent also filed publicly |

Focus Points

- Taxation: Subject to corporation tax at the standard rate (currently 30% general rate); VAT registration required if taxable supplies exceed the threshold; withholding tax applies to remittances of branch profits to the parent; no separate stamp duty advantage over a local subsidiary.

- Economic Substance: No distinct substance regime targets external companies specifically, but local activity may attract general regulatory scrutiny depending on sector.

- Treaty Access: Access to double tax treaties depends on the parent entity's jurisdiction of incorporation, not the branch's place of registration.

- Restrictions: Certain regulated industries require a locally incorporated entity rather than an external company registration; confirm sector-specific licensing requirements before proceeding.

- Conversion: An external company can subsequently incorporate a local subsidiary and transfer operations, but no automatic conversion mechanism exists under Chap. 81:01.

Closing

Registering an overseas company in Trinidad and Tobago via an external company or branch structure suits businesses that want an operational presence without the administrative overhead of a separate subsidiary, though the absence of liability separation is a material risk that parent entities must weigh carefully.

This structure is most appropriate for foreign corporations testing market entry or executing short-to-medium-term contracts where full subsidiary incorporation is not yet warranted.

Sole Trader

Sole trader registration in Trinidad and Tobago is governed by the Registration of Business Names Act, Chapter 82:85, which requires any individual trading under a name other than their own legal name to register that business name with the Registrar General's Department. There is no separate legal personality — the individual and the business are one and the same, meaning personal assets are exposed to business liabilities without limitation.

Registration is straightforward and relatively low in cost, but the absence of liability protection distinguishes this structure from incorporated entities. Self-employed business registration under this framework suits individuals operating modest, owner-managed operations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital requirement under the Act |

| Local Presence | Registered address required | Must be a physical address in Trinidad and Tobago |

| Capital | TTD; no statutory minimum | Fully funded by the proprietor |

| Privacy | Business name and owner details are publicly registered | Searchable through the Registrar General's Department |

Focus Points

- Taxation: Subject to personal income tax at progressive rates; VAT registration is required once taxable turnover exceeds the statutory threshold; no corporate tax applies.

- Annual Compliance: No annual return filing obligation, but business name registration must be renewed periodically with the Registrar General's Department.

- Conversion: Can convert to a limited company by incorporating a new entity and transferring assets; no automatic conversion mechanism exists under the Act.

- Treaty Access: As an unincorporated individual, treaty benefits under double taxation agreements apply at the personal level, not the business level.

- Restrictions: Cannot issue shares, admit partners, or raise equity capital; growth financing options are limited to personal funds or debt.

This structure suits individual service providers, freelancers, and small traders who operate locally and do not require the liability separation of an incorporated entity. The primary advantage is minimal administrative burden; the significant drawback is unlimited personal liability for all business debts and obligations.

Sole trader registration is most appropriate for resident individuals running owner-operated, low-risk businesses with no plans for equity investment or multi-party ownership.

How to Choose the Right Entity Type in Trinidad and Tobago

Choosing the right business entity in Trinidad and Tobago shapes your tax position, liability exposure, and regulatory obligations from the moment of registration — and reversing a poor choice is rarely straightforward.

Why Your Entity Choice Matters

Selecting the wrong structure produces concrete legal and financial consequences under the Companies Act, Chapter 81:01:

- Registering an external company without complying with Part III of the Companies Act while trading locally constitutes a breach of the Act and can result in striking off or penalties imposed by the Registrar of Companies.

- Choosing an entity that lacks access to the CARICOM tax treaty network means you cannot claim available withholding tax reductions on cross-border payments from member states.

- Selecting a company structure when a trust or foundation would suit asset protection or succession planning locks your firm into annual shareholder obligations, statutory filings, and director disclosure requirements that do not apply to those alternatives.

- Picking a structure that mandates audited financial statements when your operation is a single-person consultancy creates recurring compliance costs that a sole trader registration would not trigger.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point to a distinct entity type under Trinidad and Tobago law.

- Ownership and Management: Single-owner operations and multi-party arrangements have different statutory governance requirements that affect your choice between a private company, partnership, or sole trader registration.

- Tax Objectives: Your need for treaty access, a specific tax regime, or exemption status determines which structures are viable from the outset.

- Privacy Requirements: The Registrar of Companies maintains a public register of directors and shareholders, so if confidentiality is a priority, nominee arrangements or alternative structures require early consideration.

- Substance Capacity: If you cannot maintain staff, a physical office, or local decision-making, your entity selection must account for any applicable economic substance obligations.

- Exit Strategy: Not all structures permit redomiciliation or conversion, so your anticipated exit path — whether a sale, wind-up, or restructuring — should inform the initial choice.

Compliance Services for Companies in Trinidad and Tobago

Ongoing compliance support for companies registered in Trinidad and Tobago, including annual filings, statutory maintenance, and regulatory reporting.

Conclusion

Incorporating a company in Trinidad and Tobago involves choosing from a defined set of structures, each governed by the Companies Act, Chapter 81:01 or the Partnership Act, Chapter 82:01. The private company limited by shares is the most commonly registered entity, favoured by resident entrepreneurs and foreign investors alike for its liability protection and operational flexibility. Public companies suit businesses seeking capital from the public; companies limited by guarantee serve non-profit purposes. General partnerships carry unlimited liability, while limited partnerships offer a degree of protection for passive partners. External companies and branch offices allow foreign firms to operate without local incorporation.

Regulatory oversight from the Companies Registry continues to evolve, with incremental moves toward electronic filings signalling a gradual modernisation of the registration process. Your choice of structure will shape tax obligations, governance requirements, and long-term compliance obligations under Trinidad and Tobago law.

How Expanship Can Assist You

Expanship provides company incorporation services in Trinidad and Tobago across the full range of structures registered with the Registrar General's Department, from private companies limited by shares to external companies and limited partnerships. Your choice of entity carries distinct filing obligations, and our team works through each stage of the process with you directly.

From document preparation to post-registration compliance, our service scope covers what your business needs to operate in TT:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Filing and liaison with the Registrar General's Department

- Annual returns and ongoing statutory compliance management

- Corporate secretarial support

- Banking introduction assistance

Reach out to Expanship Trinidad and Tobago to discuss which structure suits your plans.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently registered structure under the Companies Act, Chap. 81:01. It combines limited liability with a relatively straightforward compliance regime, making it the default choice for both resident entrepreneurs and foreign investors operating locally.

A private company restricts share transfers and cannot offer securities to the public, while a public company may list on the Trinidad and Tobago Stock Exchange and solicit public investment. Public companies face more extensive disclosure obligations, including audited financial statements filed with the Companies Registry.

Private and public companies limited by shares, companies limited by guarantee, and external companies registered under the Companies Act hold separate legal personality. General partnerships and sole traders do not — owners bear personal liability for business obligations in those structures.

Foreign nationals may register any structure available to residents, including private companies, public companies, and external companies. There are no statutory nationality restrictions on directors or shareholders under the Companies Act, though certain regulated sectors may impose additional licensing conditions.

A sole trader requires only one individual by definition. Private companies may be incorporated with a single shareholder, but general and limited partnerships require a minimum of two partners under the Partnership Act, Chap. 81:02.

The sole trader carries no annual return or statutory filing requirement with the Companies Registry, though registration with the Board of Inland Revenue remains necessary. By contrast, all incorporated entities must file annual returns and maintain statutory registers.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.