Key Takeaways

- Turkey's primary legislation governing all major business entity types — including the Anonim Şirket, Limited Şirket, and partnership structures — is the Turkish Commercial Code (TCC) No. 6102, which came into force in 2012.

- The Limited Şirket remains the most registered business form in Turkey, favored by small and mid-sized firms due to its lower capital threshold and simpler governance requirements.

- Company registration in Turkey is administered through the Trade Registry Directorates under the Ministry of Trade, with all entities registered and managed via the Central Registration System (MERSİS).

- Foreign businesses can establish a market presence in Turkey without creating a separate legal entity by operating through either a Liaison (Representative) Office or a Branch Office.

Introduction to Entity Types in Turkey

Straddling two continents — Europe and Asia — Turkey is an independent republic bordered by Greece, Bulgaria, Georgia, Armenia, Iran, Iraq, and Syria. This geographic position has shaped its role as a significant hub for regional trade and cross-border investment.

Company registration falls under the jurisdiction of the Trade Registry Directorates, operating under the Ministry of Trade, with the Central Registration System (MERSİS) serving as the national platform through which entities are registered and managed. Turkey operates a standard corporate tax regime, with rates and incentives governed by the Corporate Tax Law No. 5520.

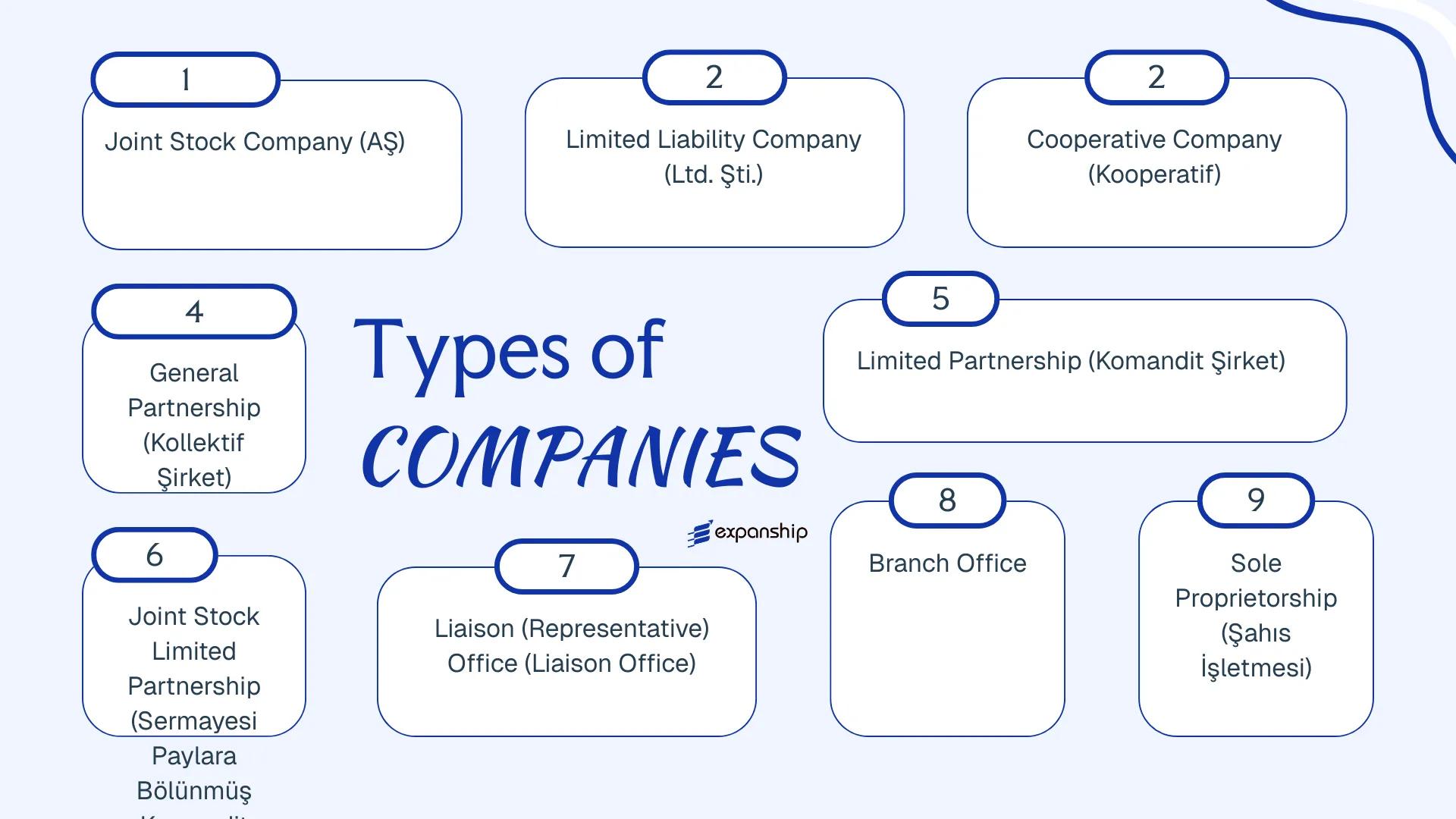

Several legal structures for companies in Turkey are available to founders, each governed primarily by the Turkish Commercial Code (TCC) No. 6102, which came into force in 2012. The available Turkish business entity types include:

- Anonim Şirket (AŞ)

- Limited Şirket (Ltd. Şti.)

- Kooperatif

- Kollektif Şirket

- Komandit Şirket

- Sermayesi Paylara Bölünmüş Komandit Şirket

- Liaison Office

- Branch Office

- Şahıs İşletmesi (Sole Proprietorship)

The sections that follow examine each of these types of companies in Turkey in detail, covering formation requirements, liability, governance, and relevant compliance obligations.

An Overview of Business Structures in Turkey

Under the Turkish Commercial Code (Türk Ticaret Kanunu, Law No. 6102), enacted in 2012 and substantially replacing the prior 1956 code, businesses can be structured through six distinct legal forms. Each form carries different rules on liability, capital requirements, and governance. The business structures in Turkey overview below organises these forms into a single reference before each is examined individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Anonim Şirket (AŞ) | Joint Stock Company | Limited to capital | Corporate tax applies | Permitted | 1 shareholder | MERSİS / Trade Registry | TTK No. 6102 |

| Limited Şirket (Ltd. Şti.) | Limited Liability Company | Limited to capital | Corporate tax applies | Permitted | 1 shareholder | MERSİS / Trade Registry | TTK No. 6102 |

| Kollektif Şirket | General Partnership | Unlimited, joint | Income tax on partners | Permitted | 2 partners | Trade Registry | TTK No. 6102 |

| Komandit Şirket | Limited Partnership | Mixed liability | Income tax on partners | Permitted | 2 partners | Trade Registry | TTK No. 6102 |

| Sermayesi Paylara Bölünmüş Komandit | Joint Stock Limited Partnership | Mixed liability | Corporate tax applies | Permitted | 2 partners | Trade Registry | TTK No. 6102 |

| Kooperatif | Cooperative | Limited to shares | Partial exemptions apply | Permitted | 7 members | Ministry of Trade | Law No. 1163 |

| Branch Office | Foreign branch | Parent bears liability | Corporate tax applies | Permitted | N/A (foreign parent) | Trade Registry / GDFI | TTK No. 6102 |

| Liaison Office | Representative office | No commercial liability | Tax exempt | Not permitted | N/A (foreign parent) | Ministry of Economy / GDFI | Decree No. 96/8186 |

| Sole Proprietorship | Individual trading | Unlimited personal | Income tax applies | Permitted | 1 individual | Tax Office / Trade Registry | Various |

Each of these structures is examined in full in the sections below.

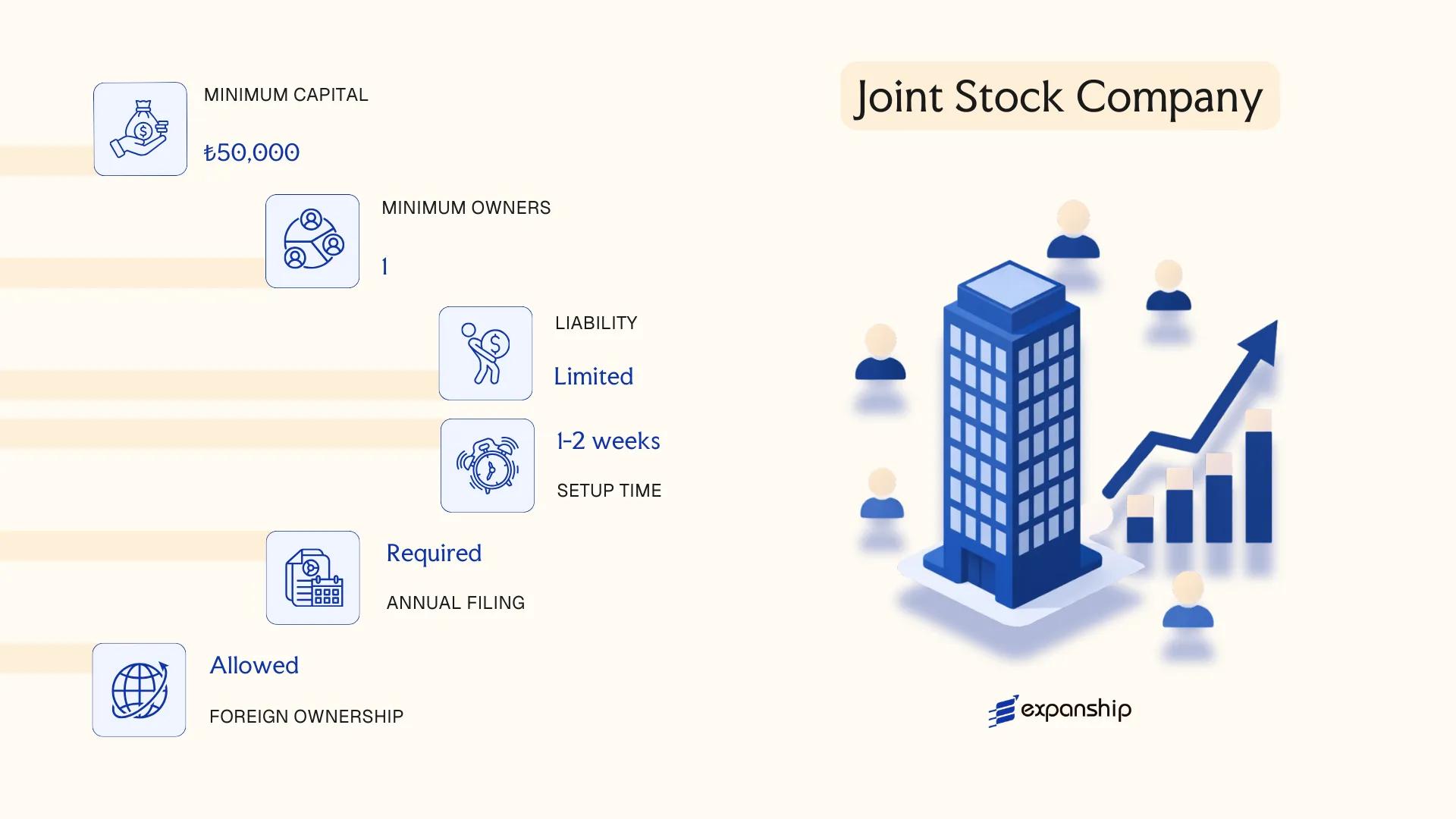

Anonim Şirket (AŞ) — Joint Stock Company

Governed by the Turkish Commercial Code (Türk Ticaret Kanunu, Law No. 6102), the Anonim Şirket is Turkey's joint stock company structure and the most capital-intensive corporate form available under domestic law. It carries a separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Liability is capped at each shareholder's capital contribution. This structure supports both closely held and publicly listed configurations, making it the standard vehicle for larger commercial operations, foreign direct investment, and companies intending to access capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity (corporation) | Established under TCC Law No. 6102 |

| Members | Minimum 1 shareholder (individual or legal entity); no maximum | Shareholders bear no personal liability beyond their subscribed capital |

| Management | Minimum 1 board member (director); majority must be Turkish residents if board members are also shareholders | Board can be composed entirely of legal entities since 2012 amendments |

| Local Presence | Registered address in Turkey required | Physical office or registered agent address acceptable |

| Share Capital | Minimum TRY 250,000 (publicly held AŞ: TRY 500,000); denominated in Turkish Lira | At least 25% of subscribed capital must be paid in at registration; remainder within 24 months |

| Privacy | Shareholder register is maintained internally; beneficial ownership reported to MASAK (Financial Crimes Investigation Board) | Public disclosure requirements apply to listed companies |

Focus Points

- Taxation: Subject to corporate income tax at 25% on net profits; standard VAT at 20%; withholding tax applies to dividend distributions (generally 10%); stamp duty applies to certain agreements and declarations.

- Annual Compliance: Mandatory general assembly meeting once per year; audited financial statements required; independent audit obligation triggered by size thresholds set by the Council of Ministers.

- Economic Substance: No formal economic substance regime equivalent to offshore jurisdictions; however, tax residency and permanent establishment rules under Turkish law and applicable tax treaties apply.

- Treaty Access: Turkey has concluded over 90 double tax treaties; an AŞ resident in Turkey qualifies for treaty benefits subject to the relevant treaty's limitation of benefits provisions.

- Conversion: Can be converted into a Limited Şirket or another commercial entity type through a structured transformation process under TCC Articles 180–190.

Sub-Types

Halka Açık Anonim Şirket (Publicly Held Joint Stock Company)

Shares are offered to the public or held by more than 500 shareholders, triggering full oversight by the Capital Markets Board of Turkey (Sermaye Piyasası Kurulu, SPK). Minimum capital rises to TRY 500,000, and continuous disclosure and prospectus obligations apply under Capital Markets Law No. 6362.

Kayıtlı Sermaye Sistemine Tabi AŞ (Registered Capital System)

Available to both public and certain private companies, this sub-type allows the board to issue new shares up to a pre-authorised ceiling without convening a general assembly for each issuance. It is particularly used by companies anticipating staged capital increases or venture-backed growth.

Closing

The AŞ suits holding structures, manufacturing operations, joint ventures with foreign partners, and any business that may seek public listing or institutional investment. Its principal advantage is unrestricted shareholder count with freely transferable shares; the primary drawback is the comparatively higher minimum capital requirement and more involved compliance burden relative to other private entity forms.

The AŞ is best suited for larger enterprises, foreign investors seeking a credible local corporate vehicle, and businesses with plans to raise capital from multiple shareholders or access public markets.

Company Incorporation in Turkey

Set up an Anonim Şirket or other Turkish entity with end-to-end support from Expanship's corporate services team.

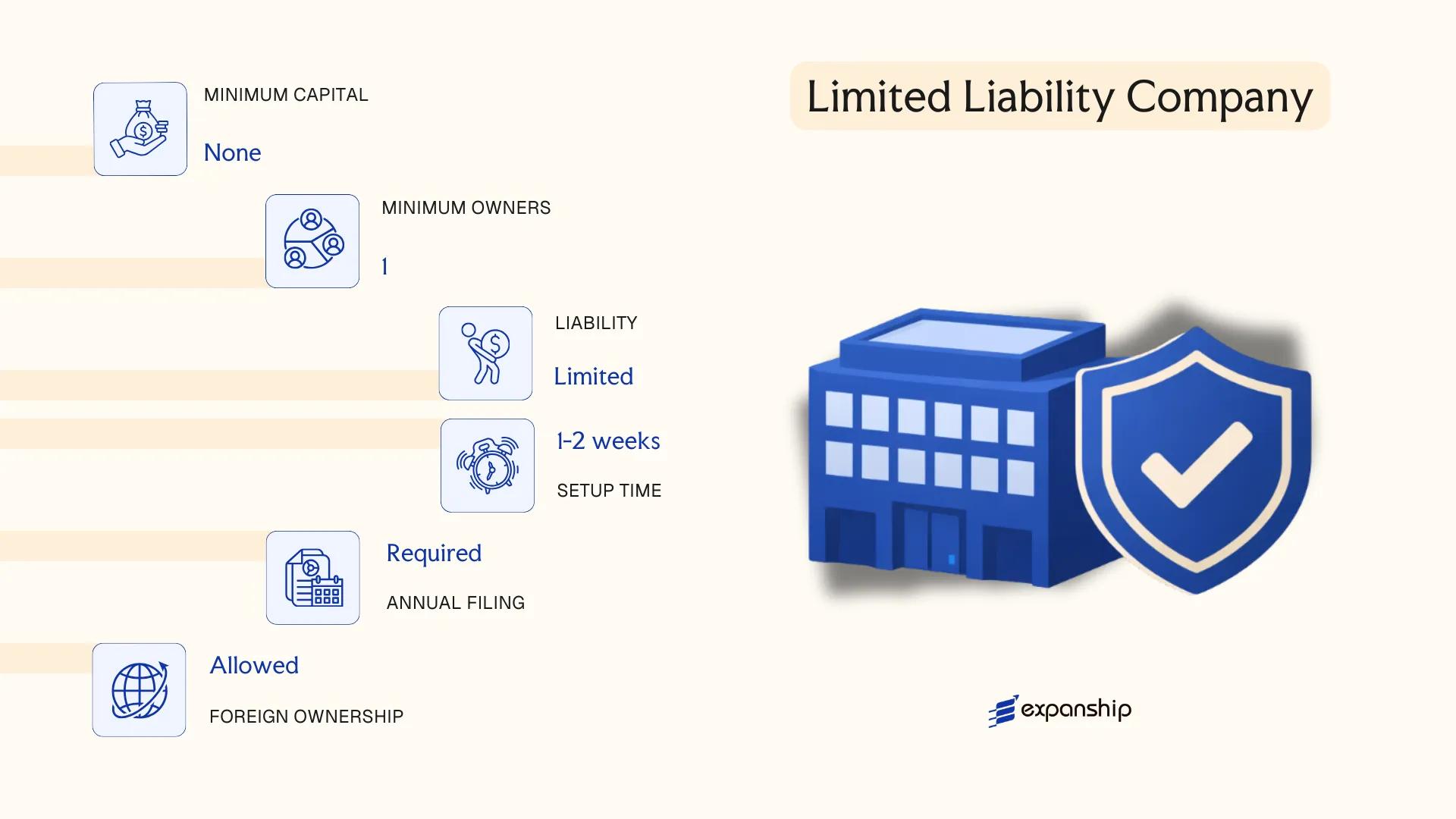

Limited Şirket (Ltd. Şti.) — Limited Liability Company

The Limited Şirket is governed by the Turkish Commercial Code (Türk Ticaret Kanunu, Law No. 6102), which came into force in 2012 and substantially modernised the framework for this entity type. Limited Şirket Turkey LLC formation appeals to founders seeking a structure that carries separate legal personality while capping each member's exposure to their subscribed capital contribution.

Liability does not extend to personal assets — shareholders bear risk only to the extent of their unpaid capital. This hybrid nature, combining corporate-style protection with a relatively straightforward governance model, makes the Ltd. Şti. one of the most frequently registered business forms in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Ltd. Şti.) | Separate legal personality; governed by TCC Law No. 6102 |

| Members | 1–50 shareholders | Natural persons or legal entities; shareholder list is filed with the Trade Registry |

| Management | Minimum 1 manager (müdür) | At least one manager must be a shareholder; can be a non-resident |

| Local Presence | Registered trade address required | Must be maintained with the relevant Trade Registry Office (Ticaret Sicili Müdürlüğü) |

| Capital | Minimum TRY 10,000 | Must be fully defined at incorporation; no mandatory paid-up schedule at registration |

| Share Transfer | Restricted; requires notarised agreement and general assembly approval | Shares are not freely transferable without internal consent |

| Privacy | Shareholder and manager details filed publicly | Trade Registry records are publicly accessible via the Central Registry Record System (MERSİS) |

Focus Points

- Taxation: Subject to 25% corporate income tax; VAT applies at standard rates (1%, 10%, or 20%); dividend withholding tax is 10% for resident and non-resident recipients; no stamp duty on share transfers, but notarisation fees apply.

- Annual Compliance: Financial statements must be prepared under Turkish Accounting Standards; companies meeting size thresholds are subject to statutory audit; annual general assembly is required within three months of the fiscal year-end.

- Economic Substance: No formal substance regime, but tax residency determinations and permanent establishment rules under domestic law and applicable tax treaties are relevant for foreign-owned entities.

- Treaty Access: Qualifies as a resident entity for the purposes of Turkey's bilateral tax treaty network, provided effective management is maintained domestically.

- Conversion: Can be converted into an Anonim Şirket or another commercial entity type under TCC Article 180 et seq., subject to Trade Registry procedures.

Closing

The Ltd. Şti. suits trading operations, service businesses, and wholly owned foreign subsidiaries where flexible governance is preferred over public capital markets access. The 50-shareholder cap is a structural constraint that can become limiting if the business later requires broader equity participation.

Foreign investors and small-to-medium enterprises establishing an operational subsidiary in Turkey with a defined, closed shareholder group.

Kooperatif — Cooperative Company

Kooperatif company registration Turkey is governed by the Cooperatives Law No. 1163, enacted in 1969 and amended over subsequent decades, including significant revisions introduced through Law No. 7339 in 2021. A Kooperatif holds separate legal personality and operates as a hybrid structure — commercially active yet oriented toward the collective economic benefit of its members rather than profit distribution to investors.

Membership in a cooperative is open and variable by nature, meaning members can join or leave without requiring formal capital restructuring. This distinguishes the Kooperatif from share-based entities, where ownership changes involve more procedural steps.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Company (Kooperatif) | Governed by Cooperatives Law No. 1163 |

| Members | Referred to as members (ortak); minimum 7, no statutory maximum | All members hold equal voting rights by default |

| Governing Bodies | General Assembly, Board of Directors (min. 3), Supervisory Board | Board members must be elected from among the members |

| Local Presence | Registered address required in Turkey | Board of Directors must conduct operations domestically |

| Capital | Minimum share value is TRY 100 per share; total capital varies by type | Capital increases through new member admissions |

| Liability | Limited to subscribed share capital per member | Personal assets of members are protected |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (25% as of 2023); VAT obligations apply to commercial activities; certain cooperatives may qualify for corporate tax exemptions under Article 4 of the Corporate Tax Law No. 5520 if surplus is not distributed.

- Annual Compliance: General Assembly must convene at least once annually; audited financial statements required; cooperatives with over a certain threshold of members are subject to external audit.

- Restrictions: Foreign nationals may join as members, but formation and management require Turkish-resident board members; activity scope must align with the stated cooperative purpose.

- Conversion: A Kooperatif cannot be directly converted into a capital company such as an Anonim Şirket without dissolution and re-incorporation.

- Regulatory Oversight: Supervision falls under the relevant ministry depending on sector — the Ministry of Trade oversees most commercial cooperatives, while housing cooperatives fall under the Ministry of Environment and Urbanisation.

Sub-Types

Agricultural Cooperative (Tarım Kooperatifi)

Formed by farmers or agricultural producers to collectively manage input supply, production, or marketing. Regulated jointly under Cooperatives Law No. 1163 and specific agricultural legislation; supervised by the Ministry of Agriculture and Forestry.

Housing Cooperative (Konut Yapı Kooperatifi)

Established for the collective construction or acquisition of residential properties. Once the construction purpose is fulfilled, the cooperative is typically dissolved and title deeds are distributed to members.

Credit Cooperative (Kredi ve Kefalet Kooperatifi)

Provides members with access to credit facilities and loan guarantees. These entities operate under oversight from the Ministry of Trade and must comply with specific financial adequacy requirements.

Other recognised sub-types include consumption cooperatives, transport cooperatives, and small business cooperatives, each serving distinct sectoral purposes under the same foundational legislation.

When to Use a Kooperatif

This structure suits member-driven ventures in agriculture, housing, or collective trade where profit extraction is secondary to shared economic benefit. The primary advantage lies in the tax exemption available to qualifying cooperatives, which can materially reduce the tax burden when conditions are met. The principal limitation is operational: governance is member-centric and administratively intensive, making it less suited to investor-funded or profit-oriented businesses.

A Kooperatif is best suited for groups of individuals or businesses pursuing a shared economic objective in a defined sector, particularly in agriculture, housing, or consumer services, where collective benefit outweighs commercial returns.

Partnership Structures [Kollektif Şirket (General Partnership), Komandit Şirket (Limited Partnership), Sermayesi Paylara Bölünmüş Komandit Şirket (Joint Stock Limited Partnership)]

Partnership structures in Turkey — Kollektif and Komandit forms alike — are governed by the Turkish Commercial Code (Türk Ticaret Kanunu, Law No. 6102, 2011), which consolidates the rules for all commercial entity types. Unlike capital companies, these structures do not always confer separate legal personality in the same way, and liability exposure varies significantly depending on the form chosen.

All three partnership types are registered with the relevant Trade Registry Office (Ticaret Sicili Müdürlüğü) and must publish their establishment deed in the Turkish Trade Registry Gazette (Türkiye Ticaret Sicili Gazetesi).

Key Characteristics

| Requirement | Kollektif Şirket (General Partnership) | Komandit Şirket (Limited Partnership) | Sermayesi Paylara Bölünmüş Komandit Şirket (Joint Stock Limited Partnership) |

|---|---|---|---|

| Legal Personality | Separate legal personality; partners bear unlimited joint liability | Separate legal personality; general partners have unlimited liability, limited partners are liable up to their capital contribution | Separate legal personality; same liability split as Komandit but capital is divided into shares |

| Members | Called "partners" (ortaklar); minimum 2, no maximum | Minimum 1 general partner (komandite), minimum 1 limited partner (komanditer); no statutory maximum | Minimum 1 general partner; limited partners hold transferable shares; no stated maximum |

| Local Presence | Registered address in Turkey required; no statutory local director requirement, but a general partner must be involved in management | Registered address required; general partner manages the firm | Registered address required; general partner manages operations |

| Capital | No minimum capital requirement | No minimum capital requirement | Capital divided into shares; no prescribed minimum, but share structure must be defined in the articles |

| Privacy | Partner names and roles disclosed in Trade Registry | Partner identities publicly registered; roles of general vs. limited partners disclosed | Shareholder and partner information registered publicly |

Focus Points

- Taxation: Kollektif and Komandit partnerships are generally taxed at the partner level rather than the entity level for income tax purposes, with profits attributed to partners according to their share; corporate income tax at 25% applies to the Sermayesi Paylara Bölünmüş form as a capital company; VAT registration is required for commercial activity; withholding tax obligations apply to distributions and certain payments.

- Annual Compliance: All three forms must file annual financial statements with the Trade Registry and maintain proper accounting records under Turkish Accounting Standards.

- Restrictions: Foreign nationals may participate as limited partners, but general partner roles carrying unlimited liability require careful structuring given personal liability exposure.

- Conversion: Conversion between entity types is permitted under Law No. 6102, subject to creditor notification procedures and Trade Registry approval.

- Treaty Access: Access to Turkey's double tax treaty network depends on the entity's tax residency classification; transparency treatment of partnerships may affect treaty eligibility.

Sub-Types

Kollektif Şirket (General Partnership)

All partners carry unlimited, joint, and several liability for the firm's obligations. This structure is used primarily by small professional or family-run businesses where partners are willing to accept full personal liability in exchange for a simpler operational framework.

Komandit Şirket (Limited Partnership)

This form introduces a two-tier partner structure: general partners (komandite) manage the business and bear unlimited liability, while limited partners (komanditer) contribute capital and are liable only to the extent of their contribution. It suits arrangements where passive investors wish to participate financially without taking on management responsibility.

Sermayesi Paylara Bölünmüş Komandit Şirket (Joint Stock Limited Partnership)

Distinguished from the standard Komandit by its share-based capital structure, this form allows the limited partnership interest to be represented by transferable shares, making it more suitable for ventures that require broader capital participation while retaining a designated managing general partner.

Closing

Partnership structures see limited use in modern Turkish commercial practice, as most businesses with growth or investment objectives prefer the Ltd. Şti. or AŞ for their liability protections. The primary advantage of partnerships is operational flexibility with no minimum capital barrier; the key drawback is the unlimited personal liability carried by at least one partner in every form.

These structures are most appropriate for small, closely held businesses or professional arrangements where the partners know each other well and personal liability is a manageable risk.

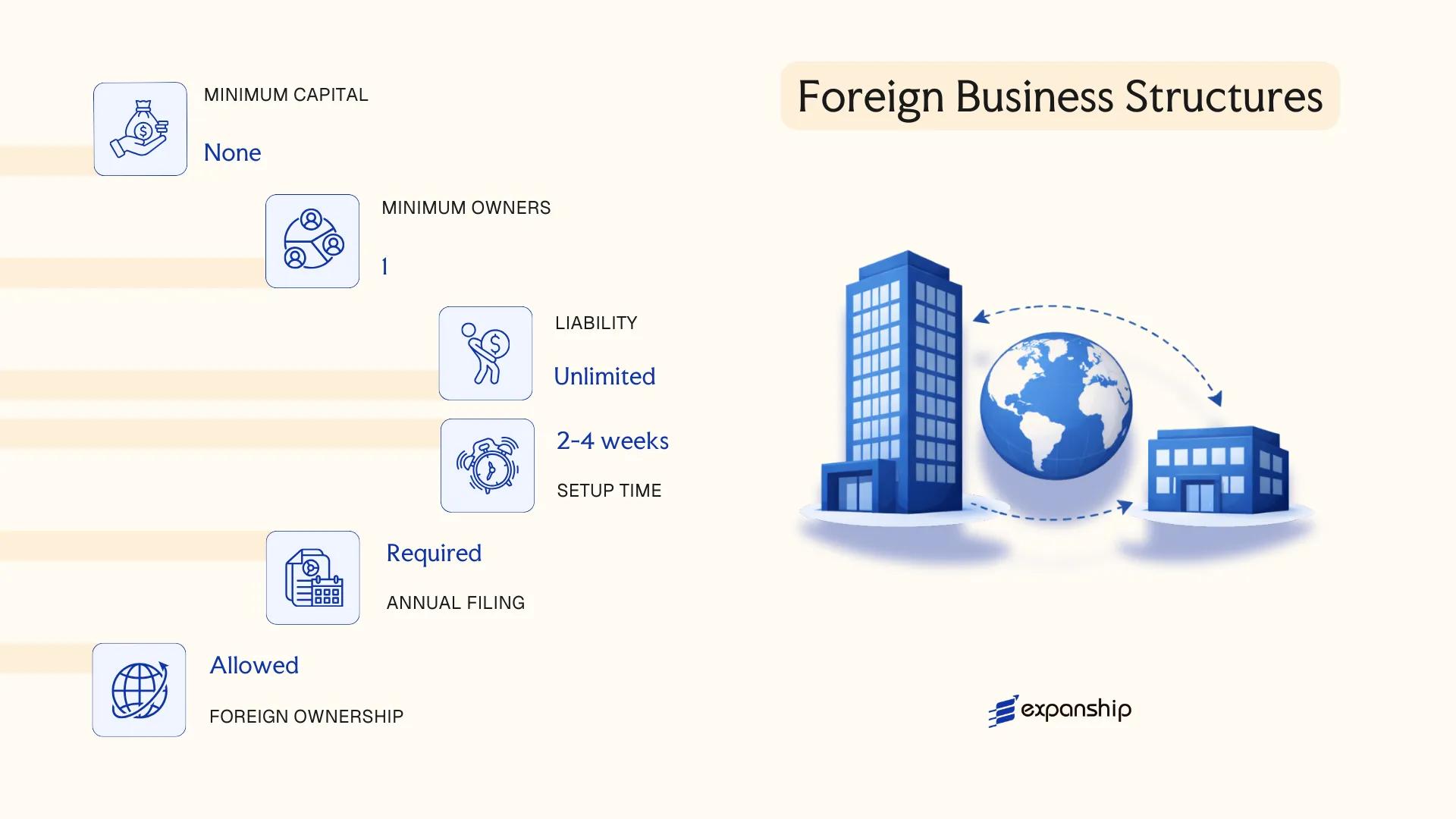

Foreign Business Structures [Liaison (Representative) Office, Branch Office]

Foreign companies seeking a presence without incorporating a separate legal entity have two established options under Turkish law: the liaison office and the branch office. Both are governed by the Foreign Direct Investment Law No. 4875 (2003) and regulated by the Ministry of Industry and Technology.

Neither structure constitutes a separate legal entity. The foreign parent company bears full legal and financial liability for both forms. This distinction has direct consequences for tax exposure, contractual capacity, and operational scope.

Key Characteristics

| Requirement | Liaison Office | Branch Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Prohibited | Permitted |

| Establishment Authority | General Directorate of Incentive Implementation and Foreign Investment | Provincial Directorate of Trade or Notary-assisted Trade Registry |

| Minimum Capital | None required | None prescribed by law |

| Registered Address | Mandatory local address in Turkey | Mandatory local address in Turkey |

| Permitted Duration | Up to 3 years (renewable) | Indefinite |

| Tax Registration | Exempt from corporate tax | Subject to corporate income tax at 25% |

Focus Points

- Taxation: Branch offices are subject to 25% corporate income tax on Turkish-sourced profits; a 15% withholding tax applies to profit remittances to the parent. Liaison offices are exempt from corporate tax but cannot generate income. VAT and stamp duty obligations apply to branch transactions where relevant.

- Commercial restrictions: A liaison office cannot issue invoices, earn revenue, or enter commercial contracts — it is limited to market research, supplier coordination, and promotional activities.

- Annual compliance: Branch offices must file annual tax returns and maintain statutory accounting records under the Turkish Commercial Code (TCC). Liaison offices must submit annual activity reports to the Ministry of Industry and Technology to retain their permit.

- Treaty access: Branch offices can access Turkey's double taxation treaties through the parent company's tax residency, subject to the treaty's permanent establishment provisions.

- Permit renewal: Liaison office permits are granted for up to three years and require documented justification for renewal; failure to renew results in automatic termination of authorisation.

Sub-Types

Liaison (Representative) Office

Established solely for non-commercial activities such as market research, technical support coordination, and communication with local counterparts. Representative office registration in Turkey requires a foreign parent company to submit an application to the General Directorate of Incentive Implementation and Foreign Investment, along with notarised and apostilled corporate documents.

Branch Office

A foreign company branch office Turkey setup grants full commercial operating rights under the parent's identity. The branch is registered with the relevant Trade Registry Office and must appoint a local authorised representative. Unlike the liaison office, it files tax returns independently and is treated as a permanent establishment for tax purposes.

Closing

Foreign business presence through a liaison office suits market-entry research and pre-investment scouting, while a branch office is appropriate for operational activity where full incorporation is not yet warranted. The primary limitation of both structures is unlimited parental liability — there is no liability ring-fence separating the Turkish operations from the foreign parent's balance sheet.

Both structures are best suited for foreign companies testing the Turkish market or managing regional operations without committing to full local incorporation.

Sole Proprietorship (Şahıs İşletmesi)

A sole proprietorship Turkey Şahıs İşletmesi is governed by the Turkish Commercial Code (Türk Ticaret Kanunu, Law No. 6102) and, for smaller traders, by the Turkish Code of Obligations (Borçlar Kanunu, Law No. 6098). Unlike a capital company, this structure carries no separate legal personality — the business and its owner are the same legal person.

Liability is unlimited. All business debts are recoverable against your personal assets, with no protective separation between the individual and the enterprise. Registration is completed through the relevant Trade Registry Office (Ticaret Sicili Müdürlüğü) for merchants, or through the local chamber for tradespeople below the merchant threshold.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Şahıs İşletmesi) | No separate legal personality |

| Member Type | Proprietor | Single individual only; referred to as the owner |

| Liability | Unlimited personal liability | Personal assets fully exposed to business debts |

| Local Presence | Registered business address in Turkey | Must be a physical address within the jurisdiction |

| Capital | No statutory minimum | No paid-up capital requirement |

| Privacy | Owner's name is publicly registered | Business name often incorporates the proprietor's surname |

Focus Points

- Taxation: Subject to personal income tax (Gelir Vergisi) at progressive rates up to 40%; VAT registration required once turnover thresholds are exceeded; no corporate tax applies; stamp duty may apply to certain commercial documents.

- Annual Compliance: Annual income tax return filing with the Revenue Administration (Gelir İdaresi Başkanlığı); bookkeeping obligations vary by merchant classification.

- Treaty Access: As a pass-through structure with no separate legal personality, access to Turkey's double tax treaty network is limited compared to corporate entities.

- Conversion: Can be converted into a Limited Şirket or Anonim Şirket, though the process requires fresh incorporation rather than a structural transformation.

- Restrictions: Foreign nationals face additional hurdles, including work permit and residence permit requirements before establishing this structure.

Sole proprietorships suit freelancers, individual traders, and small local service providers where administrative simplicity outweighs the need for liability protection. The primary advantage is low setup cost and minimal bureaucratic burden; the significant drawback is unlimited personal exposure to all business liabilities.

Local individual traders and self-employed professionals operating at small scale who do not require liability separation or external investment capacity.

How to Choose the Right Entity Type in Turkey

Knowing how to choose a company type in Turkey before filing a single document can prevent structural problems that are costly or legally complex to unwind later.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering a foreign branch when your operations are fully domestic subjects you to Turkish Commercial Code Article 40 disclosure requirements without the liability protection a Limited Şirket provides.

- Selecting a Kooperatif for commercial trading activities limits your ability to distribute profits in the same manner as a capital company, since cooperatives operate under profit-restriction principles tied to member benefit.

- Forming an Anonim Şirket when your business has a single owner and no plans for public offerings or institutional investment creates mandatory board obligations and audit thresholds that a Ltd. Şti. structure would not require.

- Choosing a general partnership (Kollektif Şirket) exposes all partners to unlimited personal liability — a structural consequence that cannot be resolved without full dissolution and re-registration under a capital company form.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct entity forms under Turkish law.

- Ownership Structure: Single-founder businesses can use a Ltd. Şti. with one shareholder, while multi-investor arrangements may require the AŞ vs Ltd Şti Turkey comparison to determine governance fit.

- Liability Exposure: Capital companies cap liability at the subscribed capital amount; partnership structures do not.

- Audit and Reporting Thresholds: Independent audit obligations under the Turkish Commercial Code (Law No. 6102) apply based on asset size, turnover, and employee count — thresholds that differ by entity type.

- Tax Treaty Access: Only entities treated as resident taxpayers under Turkish corporate tax law can access Turkey's bilateral tax treaty network for withholding rate reductions.

- Exit and Conversion: Not all entity types permit conversion without liquidation; confirm in advance whether your chosen structure allows redomiciliation or transformation under Articles 180–190 of Law No. 6102.

Compliance Services for Companies in Turkey

Maintain your Turkish entity's good standing with ongoing compliance support covering reporting obligations, general assembly requirements, and regulatory filings.

Conclusion

Selecting the right structure is the central decision in any Turkey company incorporation guide conclusion. Regulated under the Turkish Commercial Code (Law No. 6102), each entity type serves a distinct purpose: the Anonim Şirket suits larger enterprises and foreign investors requiring transferable shares; the Limited Şirket remains the most registered business form, favored by small and mid-sized firms for its lower capital threshold and simpler governance; partnerships fit closely-held ventures with defined personal liability arrangements; cooperatives serve member-based economic activity; and foreign offices allow market presence without establishing a separate legal entity.

Turkey continues to expand its double tax treaty network and has maintained an ongoing program of commercial law harmonization with EU standards. Your entity selection will interact with these regulatory developments, particularly around transfer pricing rules and substance requirements that increasingly apply to holding and intermediary structures.

How Expanship Can Assist You

Expanship's company formation services in Turkey cover the full setup process — from selecting the right entity structure (AŞ, Ltd. Şti., or branch office) through to registration with the Turkish Trade Registry and compliance with the Turkish Commercial Code. Every engagement is handled with jurisdiction-specific knowledge, not generic templates.

From document preparation to ongoing obligations, our Turkey corporate setup assistance includes:

- Preparation and legalization of incorporation documents

- Registered address and local agent provision

- Filing with the relevant Trade Registry Directorate

- Tax office registration and social security enrollment coordination

- Post-incorporation compliance management (annual filings, general assembly requirements)

- Banking introduction assistance for corporate account opening

Our team works directly with the relevant authorities so your business meets its obligations from day one — not months later after costly corrections.

Reach out to Expanship Turkey to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Limited Şirket (Ltd. Şti.) is the most frequently formed entity, largely because it requires a minimum share capital of only TRY 10,000 and can be established by a single shareholder. Its administrative requirements are less demanding than those of an Anonim Şirket, making it the default choice for small and mid-sized domestic businesses.

Both structures offer limited liability and are subject to corporate income tax at the same statutory rate, but an AŞ can issue shares to the public and access capital markets, whereas an Ltd. Şti. cannot. Compliance obligations for an AŞ are heavier, including mandatory board structures and more stringent disclosure requirements under the TCC.

A Limited Şirket does not issue publicly tradeable shares, so shareholder transfers are subject to notarial deed and general assembly approval, limiting unsolicited public visibility. Nominee arrangements are legally permissible in Turkey, though beneficial ownership disclosure obligations apply under anti-money laundering legislation.

A sole proprietorship and both AŞ and Ltd. Şti. can be formed by one person under the TCC. Partnership structures — Kollektif Şirket and Komandit Şirket — require a minimum of two partners by statutory definition, so single-person formation is not available for those forms.

Foreign nationals and foreign legal entities may establish an AŞ, Ltd. Şti., or a branch office without restriction, as Turkey applies the principle of equal treatment under the Foreign Direct Investment Law No. 4875. Liaison offices are also available to foreign companies but are prohibited from generating revenue within the country.

The TCC permits transformation between company types through a formal conversion procedure, including from an Ltd. Şti. to an AŞ, which is common when a business seeks to attract institutional investors or list on Borsa Istanbul. The conversion requires a notarised transformation plan, creditor notification, and re-registration with the relevant Trade Registry.

An AŞ, Ltd. Şti., Kooperatif, and both Komandit variants possess separate legal personality upon registration with the Trade Registry. A sole proprietorship and a Kollektif Şirket do not fully separate personal and business liability, meaning owners remain personally exposed to the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.