Key Takeaways

- Tonga's business structures are governed primarily by the Companies Act 2021 and administered through the Tonga Business Registry, which operates under the Ministry of Commerce, Consumer, Trade, Innovation and Labour.

- The private company limited by shares is the most commonly registered entity type in Tonga, used by both resident entrepreneurs and foreign investors.

- Foreign businesses can establish a presence in Tonga without creating a separate legal entity by registering either a branch office or a foreign company, both of which fall within the available corporate structures.

- Tonga operates a territorial tax framework, meaning corporate tax applies to income sourced within the jurisdiction rather than on a worldwide or zero-tax basis.

Introduction to Entity Types in Tonga

Tonga is a Polynesian archipelago of 169 islands located in the South Pacific Ocean, situated east of Fiji and north of New Zealand. It is an independent constitutional monarchy and one of the few sovereign nations in the Pacific to have maintained uninterrupted self-governance. Understanding the types of business entities in Tonga is a necessary starting point for any investor or operator planning to establish a commercial presence there.

Company registration and ongoing compliance fall under the authority of the Tonga Business Registry, which operates within the Ministry of Commerce, Consumer, Trade, Innovation and Labour. Corporate tax is levied on income sourced within the jurisdiction, placing Tonga within a territorial tax framework rather than a zero-tax or offshore model.

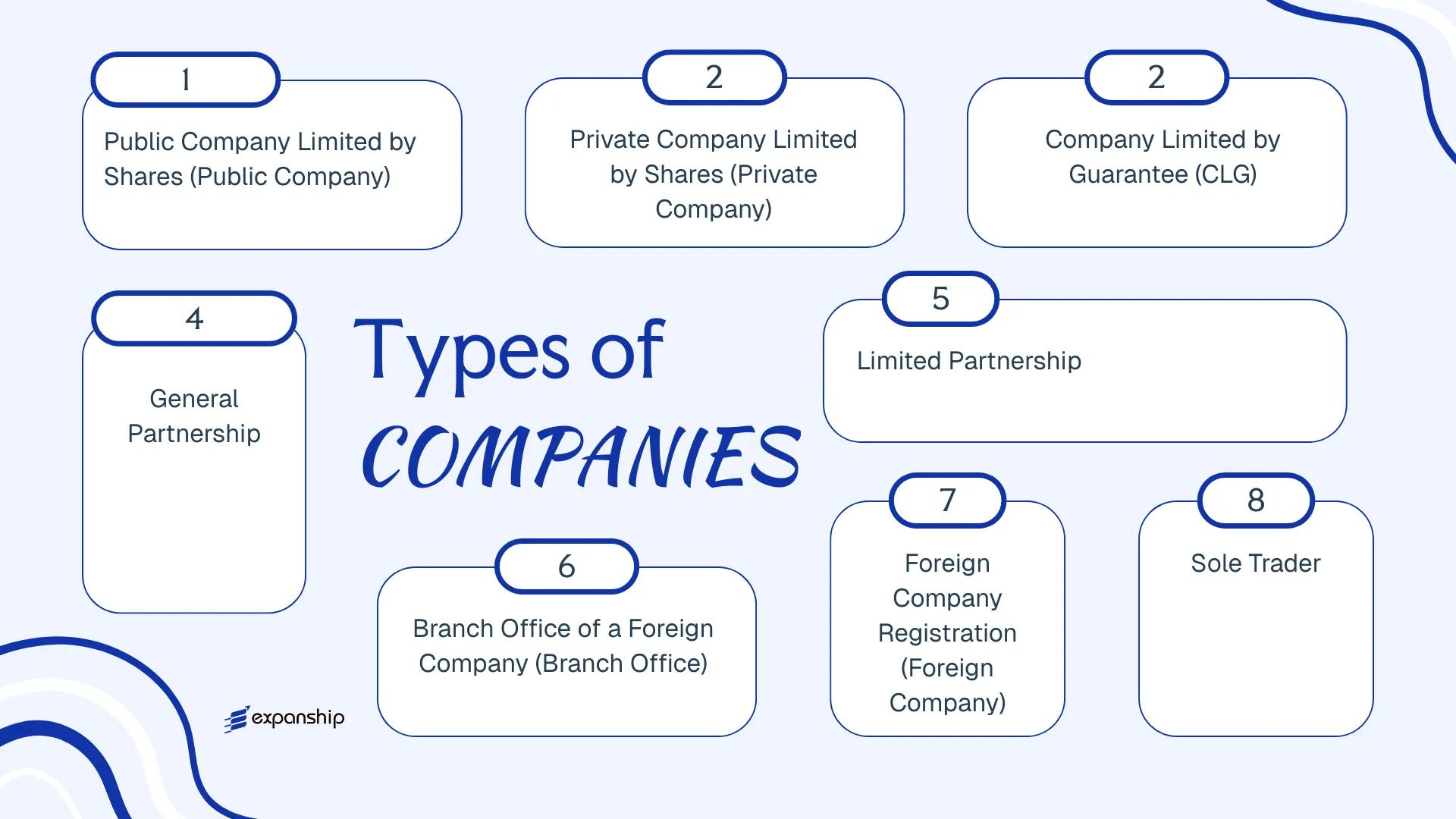

The business structures available in Tonga include: public companies limited by shares, private companies limited by shares, companies limited by guarantee, general partnerships, limited partnerships, foreign company registrations, branch offices, and sole trader arrangements. Each structure carries distinct requirements around ownership, liability, and registration. This article examines each of these Tonga corporate entity options in detail — covering formation requirements, governance obligations, and applicable considerations for foreign investors.

An Overview of Business Structures in Tonga

Tonga's company law framework offers several distinct entity types, each governed primarily by the Companies Act 1995 and, for partnerships, the Partnership Act. Every structure carries different implications for liability, taxation, and operational scope, so the sections that follow examine each in detail.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (Ltd by Shares) | Incorporated company | Limited to shares | Taxed | Yes | 2 shareholders | Ministry of Commerce | Companies Act 1995 |

| Private Company (Ltd by Shares) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Ministry of Commerce | Companies Act 1995 |

| Company Limited by Guarantee | Incorporated company | Limited to guarantee | Taxed / Exempt | Yes | 1 member | Ministry of Commerce | Companies Act 1995 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | Ministry of Commerce | Partnership Act |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | Ministry of Commerce | Partnership Act |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Yes | N/A | Ministry of Commerce | Companies Act 1995 |

| Sole Trader | Unincorporated individual | Unlimited | Taxed | Yes | 1 person | Ministry of Commerce | Business Registration |

Each of these structures is examined in full in the sections below.

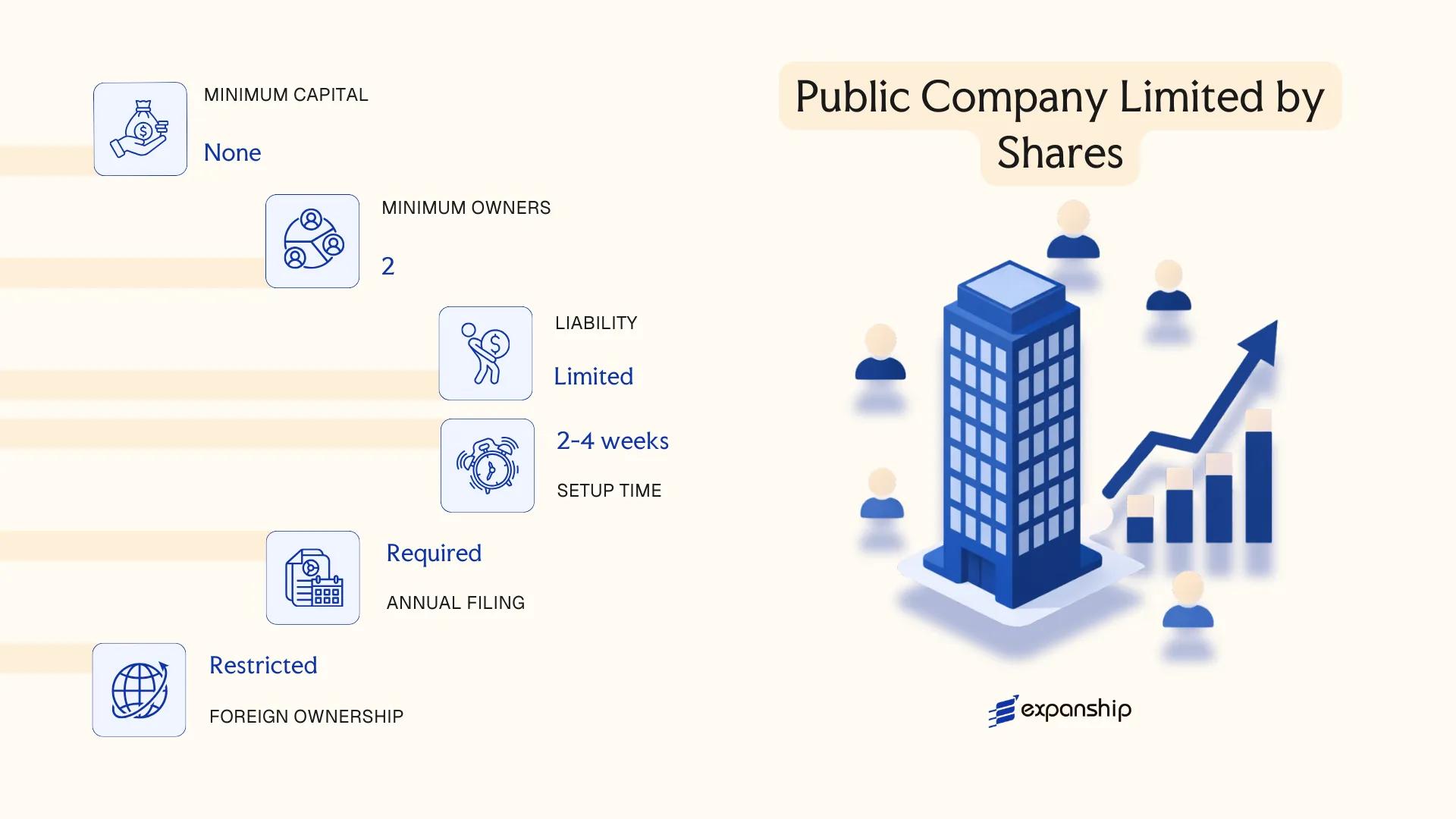

Public Company Limited by Shares

A Tonga public company limited by shares is governed by the Companies Act 1995, the principal legislation regulating corporate entities in the kingdom. Under this framework, the entity holds separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name.

Shareholder liability is confined to any unpaid amount on their shares. Unlike a private company, a public company may offer its shares to the general public, making it the appropriate structure for businesses seeking access to capital markets or broad investor participation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Incorporated under the Companies Act 1995 |

| Members | Shareholders (directors separate) | Minimum 1 director; no statutory maximum on shareholders |

| Local Presence | Registered office in Tonga required | Must maintain a physical address within the jurisdiction |

| Share Capital | No prescribed minimum; denominated in Tongan Paʻanga (TOP) | Shares must be fully described in the constitution |

| Financial Reporting | Audited financial statements required | Must be filed annually with the Registrar of Companies |

| Privacy | Shareholder and director details on public record | Register is accessible to the public |

Focus Points

- Taxation: Tonga does not impose corporate income tax, capital gains tax, or withholding tax on dividends at present; consumption tax (equivalent to VAT) may apply to business activities — consult the Ministry of Finance for current rates.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Registrar of Companies; failure to file can result in deregistration.

- Economic Substance: No formal economic substance regime is currently legislated, though maintaining genuine local operations remains advisable for reputational and banking purposes.

- Share Transfers: Shares are freely transferable unless the company's constitution places specific restrictions on transfer.

- Restrictions: Foreign ownership is subject to scrutiny under the Foreign Investment Act; certain sectors require prior approval from the Tonga Investment Board.

Closing

A public company structure suits businesses planning large-scale capital raises, joint ventures with institutional investors, or eventual listing on a recognised exchange. The ability to issue shares to the public is the primary structural advantage, though the associated disclosure obligations and audit requirements create a more demanding compliance burden than private structures.

Best suited for established businesses or investment vehicles seeking broad shareholder participation or external capital funding at scale.

Company Incorporation in Tonga

Incorporate a public or private company in Tonga with end-to-end support from Expanship.

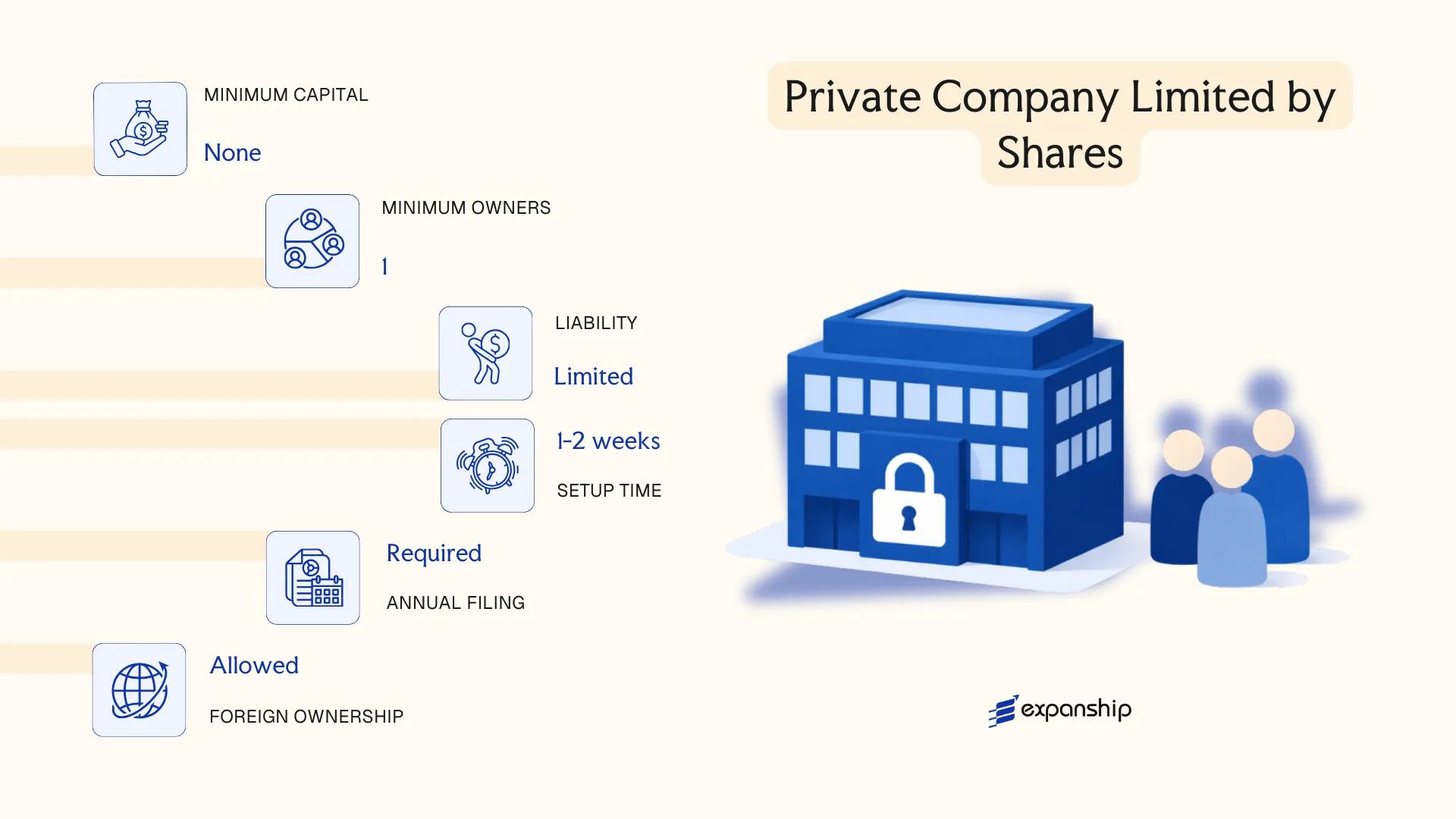

Private Company Limited by Shares

A Tonga private company limited by shares is governed by the Companies Act 1995, which establishes it as a separate legal entity distinct from its shareholders. Liability is confined to the amount unpaid on shares held, meaning personal assets of shareholders remain protected from business debts.

Incorporation under this Act grants the entity full contractual capacity — it can own property, sue, and be sued in its own name. Private company incorporation in Tonga is the most commonly used structure for small to medium commercial operations, family-owned businesses, and inbound investment vehicles.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality; cannot offer shares to the public |

| Members | Shareholders (min. 1, max. 50) | Sole shareholder companies are permitted |

| Directors | Minimum 1 director | No mandatory residency requirement for directors under general rules |

| Local Presence | Registered office in Tonga required | Must maintain a physical address for service of documents |

| Capital | No statutory minimum share capital; Tongan Pa'anga (TOP) | Shares may be issued at any value agreed by shareholders |

| Privacy | Shareholder and director details filed with the Registrar | Register of companies is accessible to the public |

Focus Points

- Taxation: No corporate income tax, no capital gains tax, no withholding tax on dividends, and no VAT at the national level, though business licensing fees apply.

- Annual Compliance: Annual returns must be filed with the Registrar of Companies; failure to file can result in deregistration.

- Restrictions: Share transfers are restricted by the company's constitution and require board or shareholder approval; public solicitation of investment is prohibited.

- Economic Substance: Tonga does not currently impose formal economic substance requirements comparable to those in OECD-listed offshore jurisdictions.

- Conversion: A private company may convert to a public company by satisfying the conditions set out in the Companies Act 1995 and filing the relevant resolution with the Registrar.

Closing Paragraph

This structure suits trading operations, holding arrangements, and businesses seeking straightforward governance without public disclosure obligations. The absence of corporate income tax is a material advantage, though the public accessibility of the companies register limits confidentiality for beneficial owners.

Small to medium enterprises, family businesses, and foreign investors seeking a locally incorporated vehicle for commercial or holding activity in the Pacific region.

Company Limited by Guarantee

A company limited by guarantee Tonga structures fall under the Companies Act 1995, administered by the Tonga Business Registry under the Ministry of Commerce, Tourism and Labour. Unlike share-based entities, this structure has no share capital — members commit to contributing a fixed sum toward liabilities only if the company is wound up.

This entity holds separate legal personality, meaning it can contract, hold property, and sue in its own name. Liability is capped at each member's guaranteed contribution amount, which is defined in the constitution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Non-profit company without share capital | Governed under Companies Act 1995 |

| Members | Referred to as Members; minimum 1, no statutory maximum | No shareholders; membership replaces share ownership |

| Directors | Minimum 1 director required | Directors manage governance; may also be members |

| Local Presence | Registered office address in Tonga required | Registered agent not mandatorily prescribed but advisable |

| Capital | No share capital; guarantee amount defined per member in constitution | Contribution triggered only upon winding up |

| Privacy | Director and member details filed with Tonga Business Registry | Register is accessible for inspection |

Focus Points

- Taxation: Tonga does not levy corporate income tax on qualifying non-profit entities, though income from commercial activities may attract tax; no VAT registration required if below threshold; stamp duty may apply on certain instruments.

- Annual Compliance: Annual returns must be filed with the Tonga Business Registry; financial statements required.

- Restrictions: Cannot distribute profits or surplus to members; all funds must be applied toward stated objectives.

- Conversion: Conversion to a share-based company is generally not permitted without dissolution and re-incorporation.

- Treaty Access: Tonga has limited double tax treaty coverage, which restricts treaty-based withholding tax relief for this entity type.

Closing

This structure suits registered charities, professional associations, religious bodies, and community organisations operating on a non-profit basis in Tonga. The absence of share capital simplifies governance, but the restriction on profit distribution makes it unsuitable for any venture with commercial return objectives.

Best suited for NGOs, membership associations, and charitable organisations that require legal personality but have no intention of distributing financial returns to members.

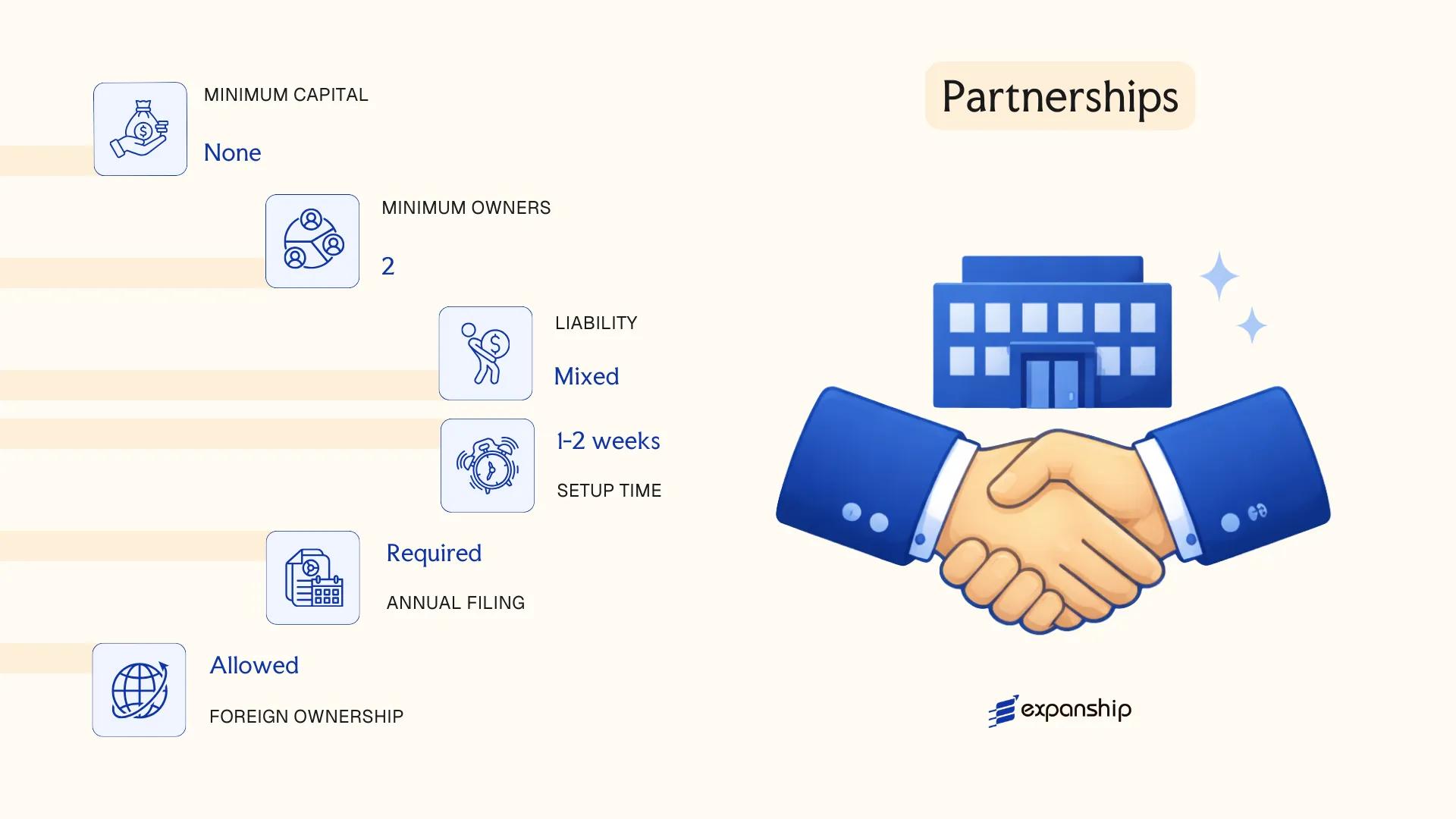

Partnerships in Tonga [General Partnership, Limited Partnership]

Partnership registration in Tonga is governed by the Partnership Act (Cap 107), which follows the traditional common law partnership framework inherited from British legal tradition. Partnerships do not possess separate legal personality — the firm and its partners are treated as one legal unit, meaning partners bear personal liability for the debts and obligations of the business.

Two recognised forms exist: the general partnership and the limited partnership. Registration is administered through the Tonga Business Registry under the Ministry of Commerce, Tourism and Labour.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality from partners |

| Members | Partners (minimum 2, no statutory maximum) | General partnership: all partners; Limited partnership: at least 1 general + 1 limited partner |

| Local Presence | Registered office in Tonga required | A local contact address must be maintained |

| Capital | No minimum capital requirement; Tongan Pa'anga (TOP) | Contributions defined by partnership agreement |

| Liability | General partners: unlimited; Limited partners: capped at contribution | Limited partners lose protection if they participate in management |

| Privacy | Partnership agreement is not publicly filed | Names of partners are registered |

Focus Points

- Taxation: Partnerships are treated as fiscally transparent; income is assessed at the partner level under Tonga's personal income tax regime, with no separate corporate tax on the partnership itself. No VAT registration threshold applies to the partnership as a distinct taxpayer.

- Annual Compliance: Annual renewal of partnership registration is required; failure to renew can result in deregistration.

- Restrictions: Foreign nationals may face restrictions on business activities under the Business Licence Act, which limits certain sectors to Tongan citizens.

- Conversion: A partnership may convert to a registered company, though this requires a fresh incorporation process rather than a simple statutory conversion.

- Treaty Access: Tonga has a limited double tax treaty network; partners should verify whether their home jurisdiction offers any relief on Tonga-sourced income.

Sub-Types

General Partnership

All partners carry unlimited joint and several liability for the firm's obligations. This structure is typically used by small professional practices or family businesses where all participants are actively involved in management.

Limited Partnership

At least one general partner retains unlimited liability, while limited partners contribute capital and have liability capped at that contribution. Limited partners must not take part in management or they risk losing their limited liability status — a rule explicitly maintained under the Partnership Act framework.

Closing

Partnerships suit small-scale trading operations, professional services, or joint ventures where the parties are known to each other and prefer a lighter administrative structure over incorporated alternatives. The absence of a minimum capital requirement is a practical advantage, though unlimited personal liability for general partners remains a material drawback for higher-risk activities.

Partnerships in Tonga are most appropriate for two or more individuals conducting small-scale local trade or professional services who are comfortable with pass-through taxation and accept the liability exposure that comes with this structure.

Foreign Business Entities in Tonga [Branch Office, Foreign Company Registration]

Foreign companies seeking to operate in Tonga are governed by the Companies Act 1995, which sets out the framework for foreign company registration in Tonga under Part XV of that legislation. A registered foreign company does not form a new legal entity in Tonga; it remains an extension of the parent corporation, carrying the same legal personality and liability profile as the home entity.

Tonga branch office setup follows a registration process administered by the Registrar of Companies, which operates under the Ministry of Commerce, Tourism and Labour. Upon approval, the foreign entity is permitted to conduct business activity within the kingdom under its existing corporate name, subject to local compliance requirements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign corporation | No separate legal personality; parent company bears full liability |

| Responsible Persons | Directors of the parent company | Local authorised agent or representative required |

| Local Presence | Registered office address in Tonga; appointed local agent | Agent must be a resident individual or locally registered firm |

| Capital | No minimum capital prescribed | Parent company's capital structure applies |

| Privacy | Parent company documents filed publicly with Registrar | Financial statements of the parent may be required for disclosure |

Focus Points

- Taxation: Tonga does not levy corporate income tax, capital gains tax, or withholding tax; customs and consumption taxes may apply to goods-related activities.

- Annual Compliance: Annual returns and updated parent company documents must be filed with the Registrar of Companies.

- Restrictions: Certain sectors, including land ownership and some retail activities, are restricted for foreign-operated entities.

- Treaty Access: Tonga has limited double taxation agreements; treaty benefits are generally unavailable to branch operations.

- Conversion: A branch may transition to a locally incorporated entity but requires a separate registration process.

Sub-Types

Branch Office

A branch office is the direct operational presence of an overseas company, conducting the parent entity's business activities within the kingdom. It is commonly used by firms in services, trade, and construction requiring a physical commercial footprint.

Foreign Company Registration (Without Active Branch)

Some foreign entities register with the Registrar without establishing an active trading presence, primarily to hold local contracts, property rights, or agency arrangements. This structure is used where administrative registration is required but day-to-day operations remain offshore.

Closing Note

A registered foreign company suits businesses that need a recognised presence in the kingdom for commercial contracts or regulatory purposes, without the administrative overhead of incorporating a new local entity; the principal limitation is that the parent company retains full liability for all local obligations.

Foreign companies with existing operations elsewhere that require a formal legal presence in Tonga for contract execution or regulated sector access.

Sole Trader

Sole trader registration in Tonga is governed primarily by the Business Licensing Act and related provisions under the Ministry of Revenue and Customs. Unlike a company, a sole trader has no separate legal personality — the business and the individual are the same legal entity, meaning personal assets are exposed to business liabilities without any form of liability shield.

Registration is handled through the Ministry of Commerce, Tourism and Labour. You must obtain a business licence before commencing operations, and trading without one carries penalties under Tongan law.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Member Terminology | Proprietor | Single individual only |

| Membership | 1 proprietor; no maximum or minimum beyond the single owner | Cannot have co-owners; business ends upon death or incapacity |

| Local Presence | Business licence required; physical or registered address in Tonga | No statutory requirement for a separate registered agent |

| Capital | No minimum capital requirement; Tongan Paʻanga (TOP) | Entirely funded by the proprietor |

| Privacy | Name and business details appear on licence register | No shareholder register privacy protections apply |

Focus Points

- Taxation: Sole traders are taxed as individuals under Tonga's personal income tax regime; no separate corporate tax applies, and VAT registration is required once turnover thresholds are met.

- Annual Compliance: Business licence must be renewed annually with the Ministry of Commerce, Tourism and Labour.

- Treaty Access: No access to double tax treaty benefits available to corporate entities.

- Conversion: A sole trader can convert to a private limited company under the Companies Act 1995, though the process requires formal incorporation as a new entity.

- Restrictions: Foreign nationals face restrictions on operating as sole traders under Tonga's foreign investment framework.

A sole trader structure suits small-scale, low-risk local trading activities where simplicity and low setup costs outweigh the need for liability protection. The primary advantage is minimal administrative overhead; the primary limitation is unlimited personal liability for all business debts.

Best suited for Tongan nationals operating small, owner-run service or retail businesses with limited financial exposure.

How to Choose the Right Entity Type in Tonga

Knowing how to choose a business entity in Tonga before committing to a structure prevents costly corrections later.

Why Your Entity Choice Matters

The structure you register has direct legal and financial consequences.

- Registering as a foreign company when you intend to conduct substantive local trade may place you in breach of the Companies Act 1995, exposing the business to penalties or deregistration.

- Selecting a structure without considering Tonga's limited tax treaty network means you cannot rely on reduced withholding rates in counterpart jurisdictions that require resident entity status.

- Forming a company when a trust or partnership arrangement would better serve asset protection locks you into annual filing obligations, statutory meetings, and shareholder requirements that simpler structures do not carry.

- Choosing a structure that mandates audited financial statements for a single-operator consultancy introduces annual compliance costs that are disproportionate to the business's scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point toward distinct structures under Tongan company law.

- Local vs. External Operations: Whether your firm transacts with Tongan residents or operates entirely offshore determines which registration pathway applies.

- Ownership and Management: Single-owner businesses have different structural needs than multi-party arrangements requiring defined governance.

- Tax Objectives: Your need for exemption, a specific regime, or treaty eligibility should be confirmed before selecting a structure.

- Exit Strategy: Not all Tongan entities permit redomiciliation or conversion, so your long-term plans should inform the initial choice.

Compliance Services for Companies in Tonga

Conclusion

Tonga's company law, governed primarily by the Companies Act 2021, offers a structured but accessible range of business vehicles suited to different operational profiles. A setting up a company in Tonga guide would typically identify the private company limited by shares as the most registered entity type, used widely by resident entrepreneurs and foreign investors alike. The public company variant suits larger enterprises seeking broader capital access. Companies limited by guarantee serve non-commercial purposes such as charities or member associations. General partnerships fit small collaborative ventures, while limited partnerships allow passive capital participation without full liability exposure. Branch offices and registered foreign companies give offshore businesses a formal presence without creating a separate legal entity. Sole traders remain the simplest entry point for individuals.

Tonga's regulatory environment continues to develop, with the Tonga Business Enterprise Centre and the Foreign Investment Act shaping how foreign capital is treated over time. Expanship's team works directly within these frameworks to support entity selection and registration.

How Expanship Can Assist You

Expanship provides corporate services for Tonga incorporation across all entity types covered in this blog — from private companies limited by shares to foreign company registrations. Our team works directly with the Tonga Financial Intelligence Unit and the Companies Office under the Ministry of Revenue and Customs to keep your filings accurate and on time. Each engagement is handled with your specific structure and commercial intent in mind.

Getting your entity off the ground involves more than submitting a form. Here is what Expanship handles on your behalf:

- Document preparation and notarization or legalization

- Registered agent and registered office provision in Tonga

- Government filing and Companies Office liaison

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Tonga to discuss your incorporation goals with someone who knows the local regulatory process.

Frequently Asked Questions (FAQ)

The private company limited by shares is the most frequently incorporated entity. Its straightforward compliance requirements and liability protection make it the default choice for both resident entrepreneurs and foreign investors operating locally.

A private company restricts share transfers and prohibits public subscription, whereas a public company may offer shares to the general public. Public companies carry heavier disclosure obligations and require a minimum of two directors, while private companies can function with a single director and shareholder.

Private companies limited by shares offer comparatively greater confidentiality, as detailed beneficial ownership information is not routinely published in public registers. Nominee director and shareholder arrangements are permissible under Tongan law, subject to underlying disclosure requirements.

A sole trader and a private company limited by shares can each be formed by one individual. General partnerships and limited partnerships, by legal definition, require at least two partners, so these structures are unavailable to a single founder acting alone.

Foreign nationals may register a private company, public company, or company limited by guarantee under the Companies Act 1995. Alternatively, a foreign corporation may establish a branch office or register as a foreign company, provided it files the requisite documentation with the Registrar of Companies.

The Companies Act 1995 provides for re-registration and continuation procedures, allowing entities to convert between certain company structures. Conversion from a partnership to a company, or between company types, generally requires approval from the Registrar and filing of updated constitutional documents.

Companies limited by shares and companies limited by guarantee possess separate legal personality distinct from their members. Sole traders and general partnerships do not, meaning owners bear personal liability for business obligations without the protection of a corporate shield.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.