Key Takeaways

- Tunisia's most commonly registered entity, the SARL, appeals to both resident and foreign investors due to its limited liability protection and relatively low capital requirements.

- The Code des Sociétés Commerciales governs the legal framework for all Tunisian business structures, directly determining each entity's liability exposure, governance obligations, and tax treatment.

- Foreign companies can establish a presence in Tunisia through a branch or representative office without creating an independent legal person, making these structures suited to market-entry or exploratory operations.

- Partnership structures such as the Société en Nom Collectif and Société en Commandite Simple carry unlimited liability, limiting their use to specific professional or family business contexts rather than general commercial investment.

Introduction to Entity Types in Tunisia

Located in North Africa, Tunisia shares borders with Algeria to the west and Libya to the southeast, with its northern and eastern coastlines facing the Mediterranean Sea. An independent republic, the country operates under a mixed legal system that draws from French civil law and, for certain personal status matters, Islamic law principles.

Company registration falls under the jurisdiction of the Agence de Promotion de l'Investissement Extérieur (APII) and is processed through the Centre de Formalités des Entreprises (CFE), the one-stop administrative body that coordinates registration formalities across relevant government departments. Tunisia applies a territorial tax system, with corporate income taxed at standard domestic rates that vary by sector and activity.

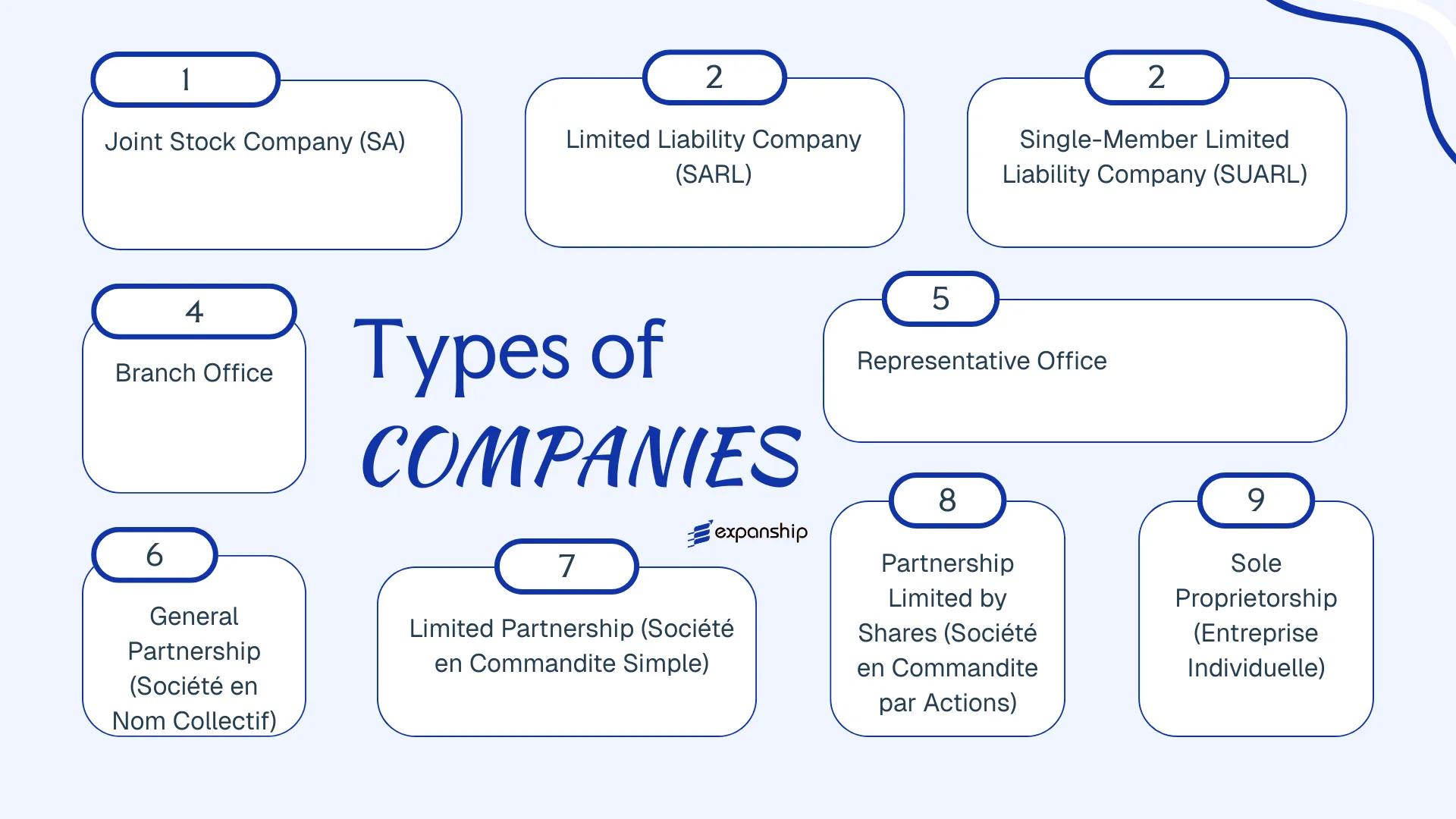

Tunisian legal entity structures available to local and foreign investors include the Société Anonyme (SA), the Société à Responsabilité Limitée (SARL), the Société Unipersonnelle à Responsabilité Limitée (SUARL), the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), the Société en Commandite par Actions (SCA), the Entreprise Individuelle, and branch or representative offices for foreign firms. Each of these business forms available in Tunisia carries distinct liability, governance, capital, and operational requirements — this article examines each in detail.

An Overview of Business Structures in Tunisia

Governed primarily by the Code des Sociétés Commerciales (CSC), enacted by Law No. 2000-93 of 3 November 2000 and amended on several occasions since, Tunisia business structures overview spans six distinct legal forms available to resident and foreign investors alike. A supplementary layer of regulation applies through the Investment Law No. 2016-71, which governs foreign participation thresholds and sector-specific restrictions. Each form carries a different liability profile, capital requirement, and governance structure.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Joint Stock Company | Limited to shares | Corporate tax liable | Permitted | 7 shareholders | RNE / API | CSC 2000-93 |

| Société à Responsabilité Limitée (SARL) | Limited Liability Co. | Limited to contribution | Corporate tax liable | Permitted | 2–50 partners | RNE | CSC 2000-93 |

| Société Unipersonnelle à Responsabilité Limitée (SUARL) | Single-Member LLC | Limited to contribution | Corporate tax liable | Permitted | 1 member | RNE | CSC 2000-93 |

| Branch Office | Foreign branch | Parent bears liability | Corporate tax liable | Restricted | 1 parent entity | API / RNE | Investment Law 2016-71 |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | Not permitted | 1 parent entity | API | Investment Law 2016-71 |

| Société en Nom Collectif (SNC) | General Partnership | Unlimited, joint | Corporate tax liable | Permitted | 2+ partners | RNE | CSC 2000-93 |

| Société en Commandite Simple (SCS) | Limited Partnership | Mixed liability | Corporate tax liable | Permitted | 2+ partners | RNE | CSC 2000-93 |

| Société en Commandite par Actions (SCA) | Partnership by Shares | Mixed liability | Corporate tax liable | Permitted | 4+ members | RNE / API | CSC 2000-93 |

| Entreprise Individuelle | Sole Proprietorship | Unlimited, personal | Income tax liable | Permitted | 1 individual | RNE | Commercial Code |

Each of these structures is examined in full in the sections below.

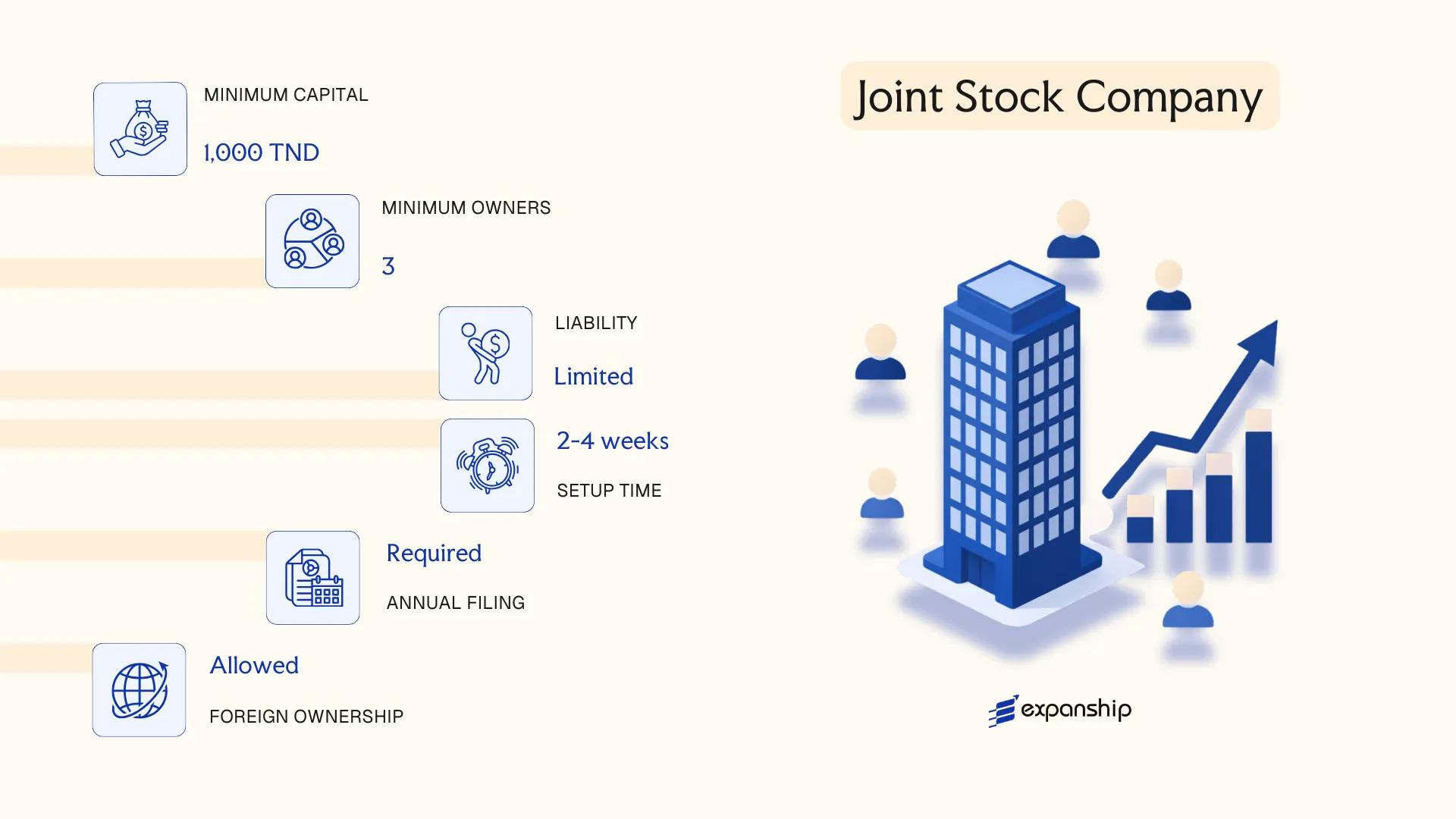

Société Anonyme (SA) — Joint Stock Company

Governed by the Commercial Companies Code (Code des Sociétés Commerciales, Law No. 2000-93 of 3 November 2000), the Société Anonyme Tunisia SA formation produces a distinct legal entity separate from its shareholders. Liability is limited to each shareholder's capital contribution, and the structure accommodates public capital-raising — making it the standard vehicle for larger commercial operations, public listings, and institutional investment.

Shares are freely transferable unless restricted by statute or the company's articles. Oversight falls under the jurisdiction of the Tribunal de Commerce, with publicly listed firms subject to additional supervision by the Conseil du Marché Financier (CMF).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; limited liability |

| Members | Shareholders (actionnaires); minimum 7 | No statutory maximum on shareholders |

| Governance | Board of Directors (Conseil d'Administration) or Supervisory Board + Management Board | Minimum 3, maximum 12 board members |

| Registered Office | Physical address required in Tunisia | Must be maintained at all times |

| Capital | Minimum TND 5,000 (non-public); TND 50,000 for publicly listed SA | At least 25% paid up at incorporation |

| Privacy | Shareholder register not publicly disclosed; board composition filed with the Registre National des Entreprises | Beneficial ownership disclosure applies |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate of 15% (general) or 35% (financial and certain sectors); VAT applies at 19% standard rate; withholding taxes apply on dividends, interest, and royalties paid to non-residents under domestic law, reducible by treaty.

- Annual Compliance: Mandatory annual general meeting, audited financial statements, and filing with the Registre National des Entreprises; statutory auditor (commissaire aux comptes) required.

- Treaty Access: Tunisia maintains a network of double taxation treaties; SA entities resident in Tunisia are generally eligible for reduced withholding rates under applicable conventions.

- Economic Substance: No specific economic substance regime analogous to offshore jurisdictions; standard tax residency rules apply based on effective management location.

- Conversion: An SA may be converted to other corporate forms (including SARL) by shareholder resolution, subject to compliance with capital and membership requirements of the target form.

Closing

The SA suits large trading operations, joint ventures with institutional partners, and businesses anticipating public listing or significant external investment. Its main advantage is unrestricted share transferability and capacity to raise capital broadly; the principal drawback is administrative weight — the mandatory auditor, minimum shareholder threshold of seven, and governance formalities create ongoing compliance costs that lighter structures avoid.

Best suited for large-scale commercial enterprises, foreign investors seeking an institutionally recognised structure, or businesses with public listing ambitions in Tunisia.

Company Incorporation in Tunisia

Incorporate a Société Anonyme or other business entity in Tunisia with end-to-end support from Expanship.

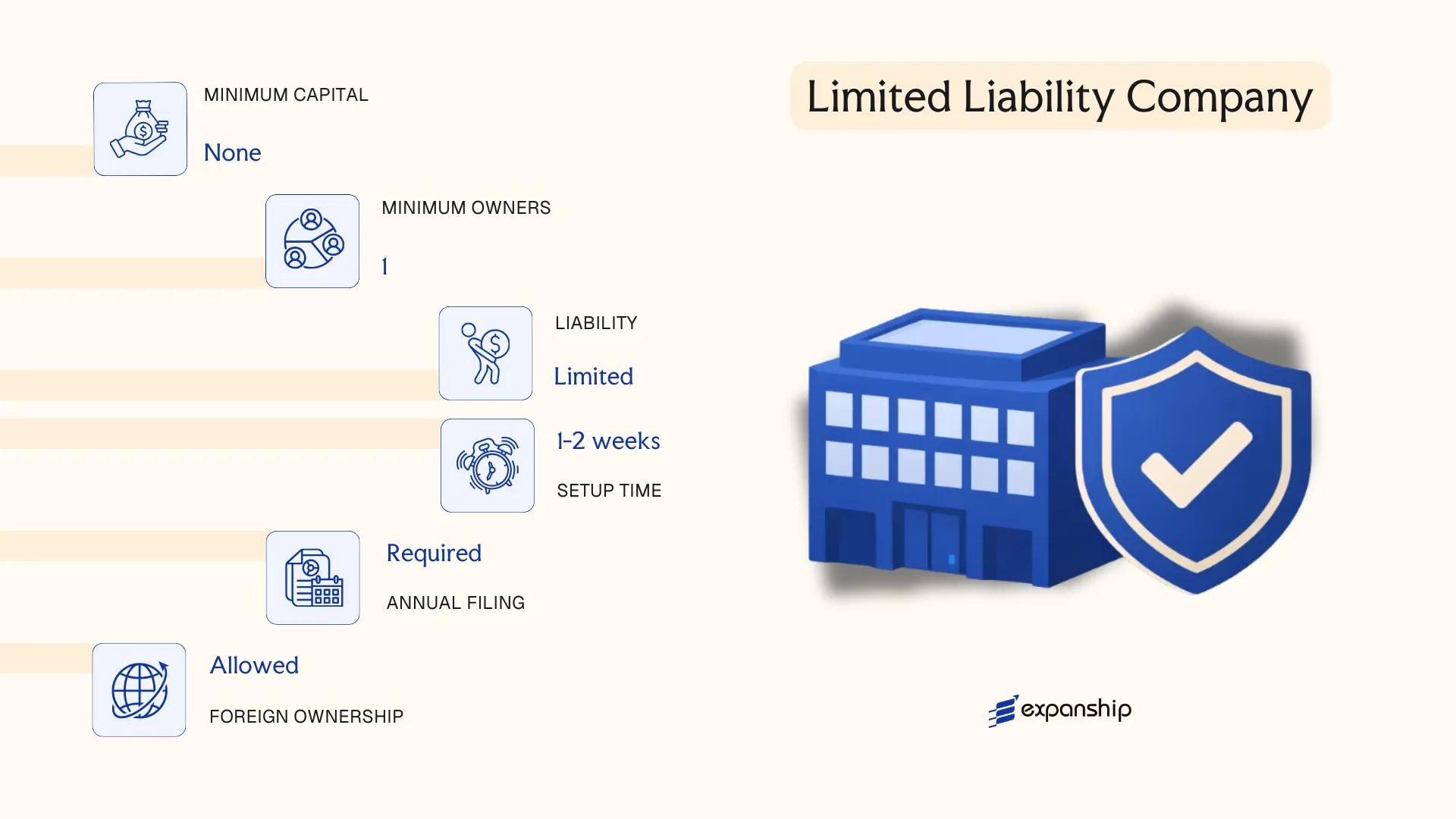

Société à Responsabilité Limitée (SARL) — Limited Liability Company

The SARL is governed by the Tunisian Commercial Companies Code (Code des Sociétés Commerciales), enacted in 2000 and subsequently amended. SARL company registration Tunisia follows a well-established framework that grants the entity full separate legal personality, meaning its debts and obligations are distinct from those of its members.

Classified as a hybrid structure, the Société à Responsabilité Limitée Tunisia sits between a partnership and a corporation — combining personal management with limited liability protection. Each member's exposure is capped at their contribution to the share capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Société à Responsabilité Limitée) | Hybrid commercial entity with separate legal personality |

| Members | 2–50 associates (associés) | Exceeding 50 requires conversion to SA |

| Management | One or more gérants (managers) | Need not be a member; no nationality requirement specified under general rules |

| Local Presence | Registered office in Tunisia required | Must maintain a physical address on record |

| Capital | No statutory minimum capital under current law | Capital divided into parts sociales; amount set in the articles of association |

| Privacy | Names of associates appear in registration documents | Not publicly listed on a stock exchange; limited public disclosure compared to SA |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (generally 15% for most sectors, 25% for financial and certain other sectors); VAT applies to taxable supplies; withholding tax applies to dividends, royalties, and service fees paid to non-residents.

- Annual Compliance: Must file annual financial statements with the Registre National des Entreprises (RNE) and hold an ordinary general assembly of associates.

- Conversion: Can be converted to an SA if the number of associates exceeds 50 or if capital market access is required.

- Transfer Restrictions: Transfer of parts sociales to third parties outside the existing associates requires approval from associates holding at least three-quarters of the share capital.

- Treaty Access: As a resident entity, eligible for benefits under Tunisia's network of double tax treaties, subject to substance and residency conditions.

The SARL suits small to medium-sized trading, service, or holding operations where founders want limited liability without the administrative burden of a joint stock company. The absence of a minimum capital requirement lowers the entry threshold, though the 50-associate ceiling restricts its use for larger, multi-investor structures.

Best suited for small to mid-sized businesses with a defined group of founders or investors who do not intend to raise capital from the public.

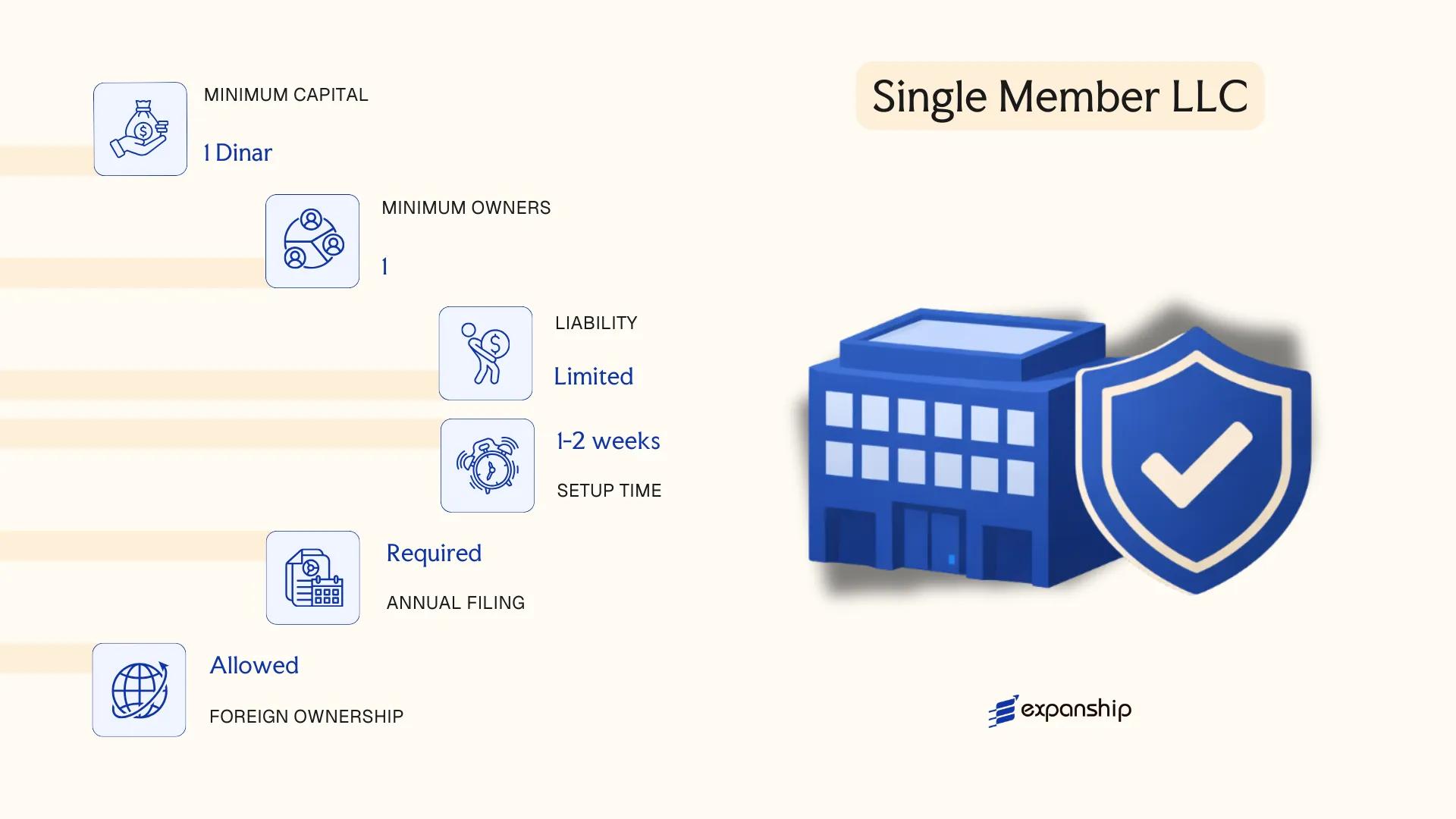

Société Unipersonnelle à Responsabilité Limitée (SUARL) — Single-Member LLC

The SUARL single member company Tunisia introduced through the Commercial Companies Code (Code des Sociétés Commerciales, Law No. 2000-93 of 3 November 2000) provides a vehicle for a single individual to conduct business with the protection of limited liability. The founding member's exposure is capped at their capital contribution, and the entity holds a separate legal personality distinct from its owner.

Structurally, the Société Unipersonnelle à Responsabilité Limitée Tunisia functions as the single-shareholder variant of the SARL. Ownership and management can be held by the same individual, making it a common choice for freelancers, consultants, and small business operators who require formal corporate status without shared governance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-member limited liability company | Governed by Law No. 2000-93 |

| Members | 1 individual (natural person only) | Corporate shareholders are not permitted |

| Management | Manager (Gérant) | Can be the sole member themselves |

| Registered Office | Physical address in Tunisia required | Must be maintained for official correspondence |

| Share Capital | Minimum TND 1,000 | Must be fully paid up at incorporation |

| Privacy | Beneficial owner details filed with RNE | Not publicly searchable in full detail |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate; VAT registration applies based on turnover thresholds; withholding tax applies to dividends, service fees, and certain payments to non-residents.

- Annual Compliance: Annual financial statements must be filed with the Registre National des Entreprises (RNE); tax declarations due to the Direction Générale des Impôts.

- Restrictions: Membership is restricted to a single natural person; the entity cannot be used as a holding vehicle by a corporate parent.

- Conversion: Can be converted to a multi-member SARL if additional shareholders are admitted, without dissolving the entity.

- Treaty Access: As a Tunisian-resident entity, the SUARL can access Tunisia's network of double taxation agreements, subject to substance requirements.

Sole practitioners and individual entrepreneurs use the SUARL to formalise operations, access banking facilities, and enter contracts under a distinct legal name. The structure offers straightforward governance with no board requirements, though the restriction to one natural person limits growth without conversion.

The SUARL is best suited for individual entrepreneurs and self-employed professionals seeking legal separation between personal and business assets.

Foreign Business Presence [Branch Office, Representative Office]

A foreign company branch office in Tunisia operates under the Investment Law No. 2016-71 and is subject to oversight by the Investment Development Authority (FIPA-Tunisia) alongside the Tax Authority. Unlike locally incorporated entities, a branch has no separate legal personality — it remains an extension of the parent company, which bears full liability for its obligations.

Registration is handled through the One-Stop Shop (Guichet Unique) at APII (Agence de Promotion de l'Industrie et de l'Innovation). A representative office, by contrast, is restricted to non-commercial activities such as market research and liaison work, and cannot generate revenue or sign contracts on behalf of the parent.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | APII via One-Stop Shop | FIPA-Tunisia |

| Local Representative | Mandatory resident manager | Mandatory resident contact person |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Registered Address | Required in Tunisia | Required in Tunisia |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate of 15% (general) or 25% (certain sectors); VAT at 19% applies to taxable supplies; withholding tax applies on remittances to the parent under domestic rules, reducible under applicable tax treaties.

- Treaty Access: Branches may access Tunisia's double tax treaty network, though treaty benefits depend on the parent's country of residence and treaty provisions.

- Annual Compliance: Branches must file annual financial statements and tax returns; accounts must reflect Tunisia-sourced activities separately from the parent's global accounts.

- Restrictions: Representative offices are prohibited from invoicing, generating income, or executing commercial contracts; violation can result in deregistration.

- Conversion: A branch can be converted into a locally incorporated entity such as an SARL or SA, though this requires a formal restructuring process rather than a simple administrative update.

Closing

A branch is suited to foreign firms testing the market or executing specific project-based contracts, while a representative office fits pure liaison or pre-market-entry functions. The key limitation for both structures is the absence of liability separation from the parent.

Foreign companies with existing operations seeking a controlled, non-permanent presence before committing to full local incorporation.

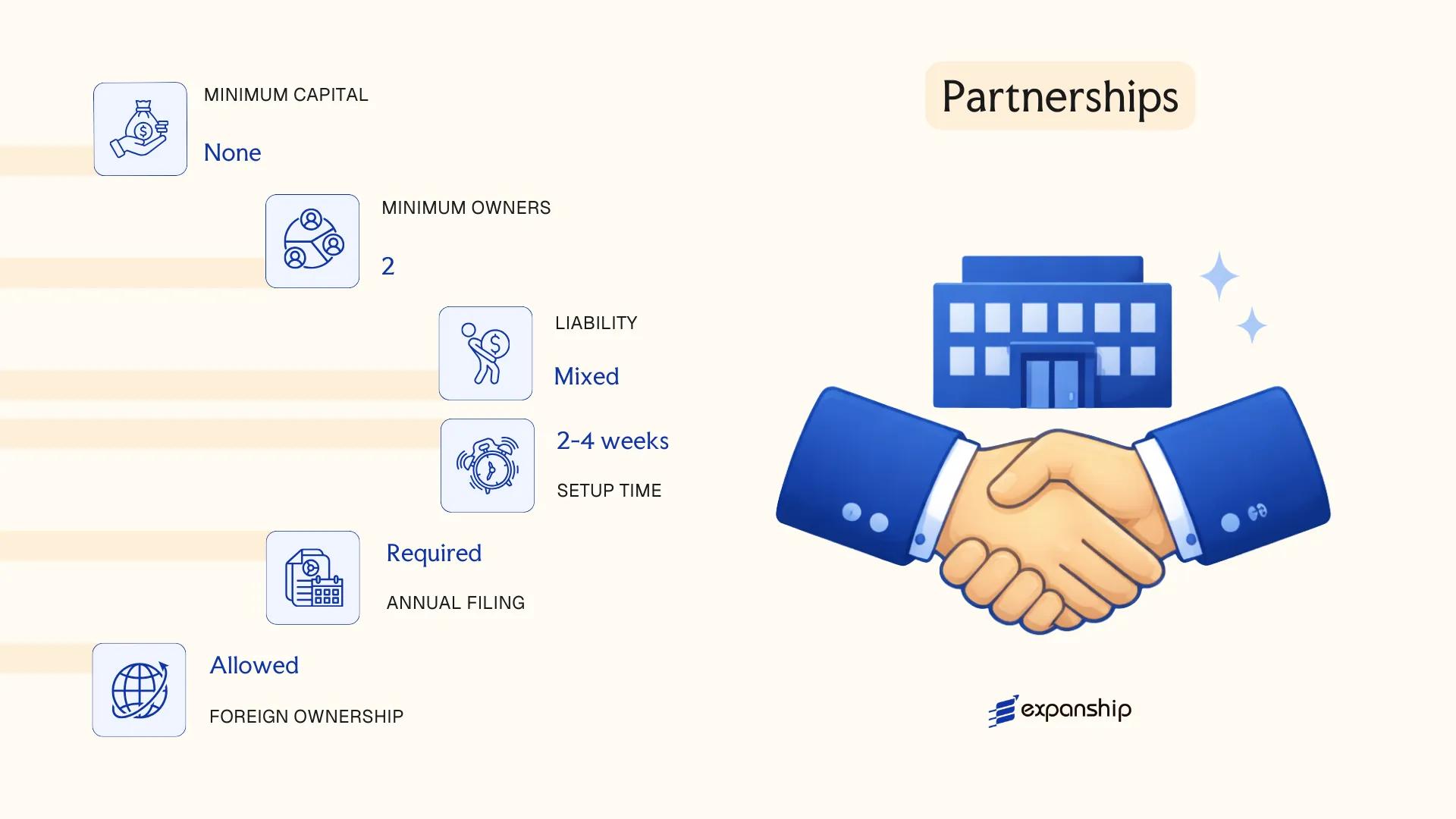

Partnerships [Société en Nom Collectif, Société en Commandite Simple, Société en Commandite par Actions]

Partnership structures in Tunisia are governed by the Code des Sociétés Commerciales (CSC), enacted in 2000. Three distinct forms exist under this framework: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA).

Each structure carries a separate legal personality upon registration with the Registre National des Entreprises (RNE). Liability treatment, however, varies significantly across the three forms — ranging from fully unlimited joint liability to a hybrid model combining unlimited and limited exposure depending on partner classification.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | SNC / SCS / SCA | All three registered under the CSC 2000 |

| Members | SNC: Associés (min. 2, no max); SCS: Associés commandités (min. 1) + commanditaires (min. 1); SCA: Commandités (min. 1) + commanditaires acting as shareholders (min. 3) | SNC partners bear unlimited joint liability; SCA commanditaires have liability limited to capital contribution |

| Local Presence | Registered office in Tunisia required | No statutory requirement for a local resident manager in all forms, though SNC managers are typically drawn from among partners |

| Capital | No statutory minimum for SNC or SCS; SCA requires share capital divided into negotiable shares | SCA capital structure resembles that of an SA in its share-based composition |

| Privacy | Partner identities disclosed in the RNE register | No confidentiality provisions; all founding documents are publicly accessible |

Focus Points

- Taxation: Partnerships are generally subject to corporate income tax at the standard rate; VAT obligations apply where applicable; profit distributions may attract withholding tax depending on partner residency status.

- Annual Compliance: All three forms must file annual financial statements and maintain accounting records; SCA entities face disclosure requirements comparable to joint stock companies.

- Restrictions: Foreign participation in SNC and SCS structures carries unlimited liability exposure, making these forms uncommon for non-resident investors.

- Conversion: An SNC may be converted to an SARL or SA subject to partner consent and RNE procedures.

Sub-Types

Société en Nom Collectif (SNC)

All partners hold the status of traders (commerçants) and bear joint, unlimited liability for the firm's debts. Typically used for small, closely held businesses where partners have high mutual trust.

Société en Commandite Simple (SCS)

A two-tier partnership distinguishing between commandités (general partners with unlimited liability) and commanditaires (silent partners with liability capped at their contribution). Used where capital investors prefer limited exposure without taking on management responsibility.

Société en Commandite par Actions (SCA)

The SCA issues negotiable shares to commanditaires, making it the most capitalised of the three forms. General partners retain management control and unlimited liability, while shareholders hold transferable equity interests.

When to Consider a Partnership Structure

Partnerships suit family-owned businesses, professional services firms, or situations where a tiered liability arrangement between active and passive investors is operationally necessary. The primary advantage is structural flexibility in defining partner roles; the principal drawback is the unlimited liability exposure carried by general partners in all three forms.

These structures are most appropriate for closely held businesses or joint ventures where at least one party is prepared to accept unlimited personal liability in exchange for full management control.

Sole Proprietorship [Entreprise Individuelle]

The sole proprietorship Tunisia Entreprise Individuelle is the simplest business form available to individual operators. Governed primarily by the Tunisian Commercial Code and supplemented by registration procedures under the Registre National des Entreprises (RNE), this structure grants no separate legal personality — the business and its owner are treated as a single legal subject. As a direct consequence, the proprietor bears unlimited personal liability for all business debts and obligations.

Registration is handled through the RNE, which centralises the Tunisia self-employed business registration process. The setup is relatively straightforward, and the Entreprise Individuelle setup Tunisia follows a single-owner model with no minimum capital threshold under current regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Entreprise Individuelle) | No separate legal personality from the owner |

| Member Title | Proprietor | Single natural person only |

| Membership | 1 proprietor; no maximum as it is a single-owner structure | Must be a natural person; legal entities cannot act as proprietor |

| Local Presence | Registered business address in Tunisia required | Must be declared at RNE registration |

| Capital | No statutory minimum capital | Contribution reflects personal assets committed to the business |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business creditors |

Focus Points

- Taxation: Business income is assessed under personal income tax (IRPP) at progressive rates; VAT registration is required once turnover exceeds applicable thresholds; no corporate income tax applies.

- Annual Compliance: Annual income declaration must be filed with the Direction Générale des Impôts; accounting obligations vary by turnover bracket.

- Treaty Access: As a non-corporate entity, access to Tunisia's double tax treaty network is restricted; treaty benefits generally apply to resident individuals rather than business structures.

- Conversion: Conversion to a corporate form such as SUARL or SARL requires dissolution of the sole proprietorship and fresh incorporation; there is no automatic legal continuity mechanism.

- Restrictions: Foreign nationals face additional requirements under Tunisian investment law before operating as a sole trader; certain regulated sectors are closed to this structure entirely.

Closing Paragraph

The Entreprise Individuelle suits resident individuals running low-capital, low-risk service or trade activities where administrative simplicity outweighs the need for liability protection. The primary drawback is full personal exposure to business liabilities, which makes this structure unsuitable for any activity carrying meaningful financial or legal risk.

Tunisian resident individuals operating small-scale trade or service businesses who require minimal administrative overhead and do not need liability separation.

How to Choose the Right Entity Type in Tunisia

Choosing the right company type in Tunisia affects your tax position, liability exposure, and long-term operational viability — not just your registration paperwork.

Why Your Entity Choice Matters

Selecting the wrong structure carries concrete legal and financial consequences:

- Forming a SARL when your activity requires a regulated structure under the Insurance Code or Banking Law means your license application will be rejected outright.

- Choosing a tax-exempt regime when you need access to Tunisia's double taxation treaty network means withholding tax reductions available under those treaties will not apply to your income flows.

- Registering a Representative Office when you intend to conclude contracts or generate revenue locally puts you in breach of the conditions governing that structure under the Investment Law (Law No. 2016-71), exposing the entity to administrative sanctions.

- Opting for a structure that mandates audited financial statements — such as an SA — when you operate as a single-person consultancy adds recurring statutory audit costs that a SUARL would not require.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct entity types under Tunisian commercial law.

- Ownership Structure: A sole operator points toward a SUARL, while multi-party ownership with capital market ambitions points toward an SA.

- Tax Objectives: Your eligibility for specific incentive regimes under the Investment Law depends on the entity type you select.

- Substance Capacity: If you cannot maintain a physical presence and local decision-making, certain structures will attract scrutiny from tax authorities.

- Privacy Requirements: Director and shareholder details filed with the Registre National des Entreprises are publicly accessible, which affects how you structure ownership.

- Exit Strategy: Not all Tunisian entity types permit redomiciliation or conversion; plan your structure with the end state in mind.

The primary legislation governing company formation is the Code des Sociétés Commerciales, which should be consulted directly when assessing structural requirements.

Compliance Services for Companies in Tunisia

Maintain your statutory obligations, filings, and regulatory requirements across your Tunisian entity's lifecycle.

Conclusion

Selecting the right structure is one of the first binding decisions you make when incorporating a business in Tunisia, and it directly affects liability exposure, governance obligations, and tax treatment under the Code des Sociétés Commerciales.

The SARL remains the most registered entity type, favored by resident and non-resident investors alike for its balance of limited liability and relatively low capital requirements. The SA suits larger ventures requiring institutional investment or a public capital structure. For sole operators, the SUARL provides a single-member framework with formal legal personality. Branch and representative offices serve foreign companies testing the market without establishing an independent legal person. Partnership structures carry unlimited liability and are used in specific professional or family business contexts.

Registered with the Registre National des Entreprises, each structure operates within a defined legal framework. Tunisia's ongoing investment code reforms and expanding bilateral investment treaty network continue to shape how foreign-owned entities are structured and maintained.

How Expanship Can Assist You

Expanship Tunisia company formation services cover the full process of establishing a legal presence under Tunisian law, from selecting between a SARL, SUARL, or SA through to registration with the Registre National des Entreprises (RNE). Your specific entity type determines the documentation, capital requirements, and timeline involved — and that's where hands-on support makes a practical difference.

Our team handles the procedural and administrative side of your Tunisia business setup assistance, so you can focus on operations:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Liaison with the RNE and other relevant government bodies

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for corporate account opening

Reach out to the Expanship Tunisia team to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered entity. Its relatively low minimum capital threshold, capped liability, and straightforward governance structure make it the default choice for small to medium-sized domestic businesses.

A Branch Office has no separate legal personality and remains an extension of its foreign parent, meaning the parent bears full liability for its Tunisian operations. A SARL, by contrast, is an independent legal entity under the Code des Sociétés Commerciales, with liability confined to each member's capital contribution. Compliance obligations for branches are generally lighter, but local trading flexibility is broader for a SARL.

The SUARL (Société Unipersonnelle à Responsabilité Limitée) offers a degree of privacy suited to single-owner operations, as internal management arrangements are not fully disclosed in public registries. Beneficial ownership information is, however, subject to disclosure requirements under anti-money-laundering regulations administered by the Commission Tunisienne des Analyses Financières (CTAF).

No. Partnerships such as the Société en Nom Collectif and Société en Commandite Simple require a minimum of two partners by statute. The SUARL is specifically designed for sole founders, while an SA requires at least seven shareholders.

Foreign investors may form a SARL, SUARL, or SA, subject to sector-specific restrictions administered by the Investment Development Authority (FIPA). Certain regulated sectors require prior approval or impose equity caps on foreign ownership, so verifying sectoral eligibility before selecting a structure is necessary.

Conversion is permitted under Tunisian corporate law. A SARL can be converted into an SA once it meets the applicable capital and shareholder thresholds, and the reverse conversion is also recognized. Such changes require shareholder approval, notarized documentation, and re-registration with the Registre National des Entreprises.

Not all do. The Société en Nom Collectif and Representative Office lack full separation between the entity and its members or parent. The SA, SARL, SUARL, and Société en Commandite par Actions each hold distinct legal personality, enabling them to contract, own assets, and litigate in their own name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.