Key Takeaways

- The Sociedade por Quotas (SQ) is the most commonly registered entity in Timor-Leste, favored for its manageable capital requirements and simpler governance compared to the Sociedade Anónima.

- Company registration in Timor-Leste falls under the Instituto do Registo e Notariado (IRN), which maintains the business registry and oversees legal entity formation.

- Branch offices provide foreign firms a direct operational presence without establishing a separate legal person, while representative offices are limited strictly to liaison and promotional activities.

- Timor-Leste operates a territorial tax system, meaning only income sourced within the country is generally subject to local taxation.

Introduction to Entity Types in Timor-Leste

Located on the eastern half of Timor island in Southeast Asia, bordered by Indonesia and with Australia to its south, Timor-Leste is an independent sovereign nation that gained formal independence in 2002. Understanding the types of business entities in Timor-Leste is a prerequisite for any foreign or domestic investor structuring a commercial presence there.

Company registration falls under the jurisdiction of the Instituto do Registo e Notariado (IRN), the body responsible for maintaining the business registry and overseeing the formation of legal entities. The country operates a territorial tax system, meaning only income sourced within the country is generally subject to local taxation.

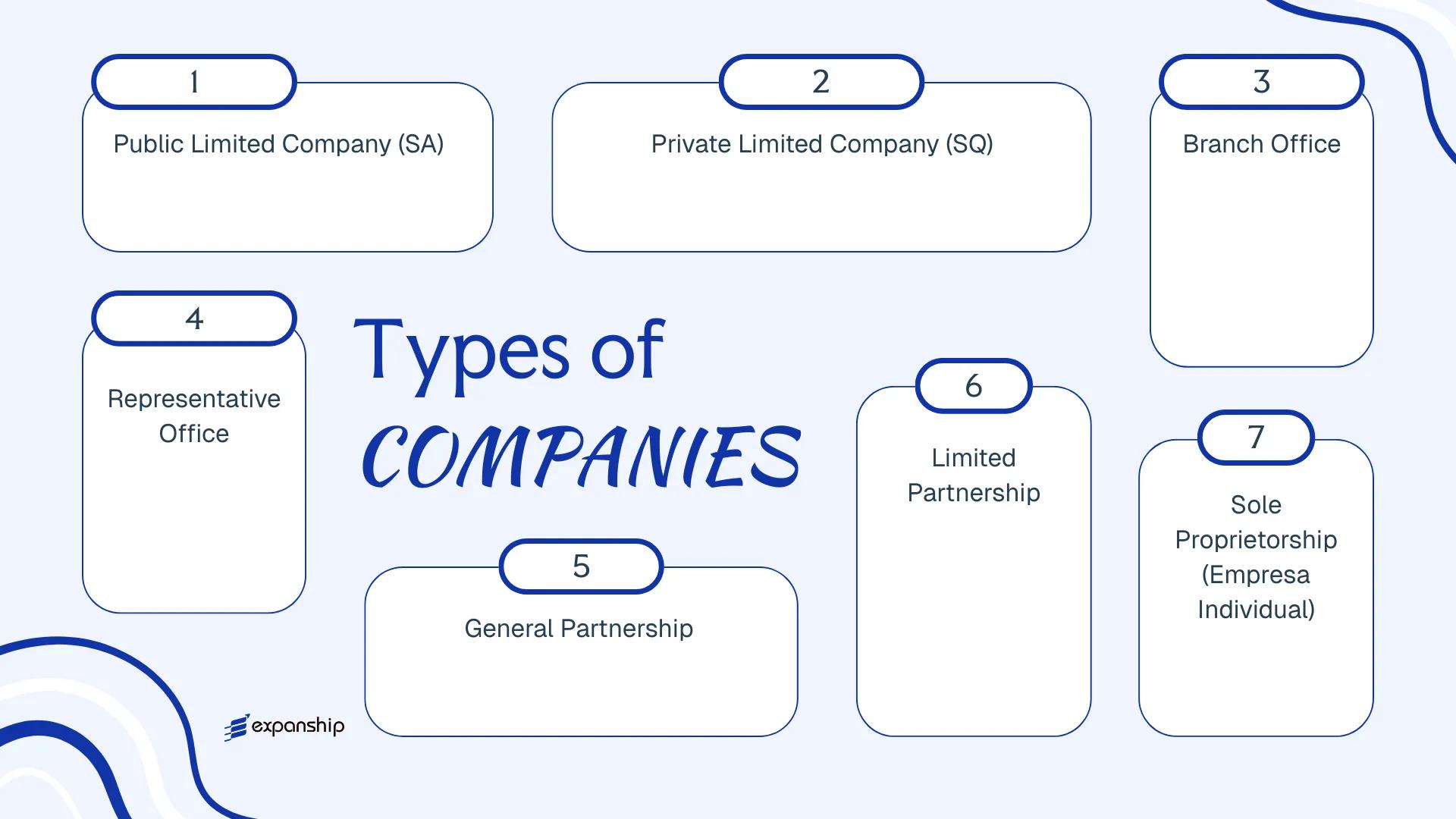

Legal entities available under Timorese law include the Sociedade Anónima (SA), Sociedade por Quotas (SQ), branch office, representative office, general partnership, limited partnership, and sole proprietorship (Empresa Individual). Each structure carries distinct requirements around share capital, liability, governance, and foreign ownership. This article examines each form in detail to help you determine which arrangement suits your operational and legal objectives.

An Overview of Business Structures in Timor-Leste

Timor-Leste's company law framework provides several distinct entity types, each governed primarily by the Commercial Companies Law (Decree-Law No. 12/2017). This legislation establishes the legal basis for incorporating, registering, and operating business structures within the country. Each entity type carries different implications for liability, ownership, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (SA) | Separate legal entity | Limited to shares | Taxable | Yes | 5 shareholders | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| Private Limited Company (SQ) | Separate legal entity | Limited to quotas | Taxable | Yes | 1 shareholder | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| Branch Office | Extension of foreign entity | Parent bears full liability | Taxable | Yes | N/A | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| Representative Office | Extension of foreign entity | Parent bears full liability | Generally exempt | No | N/A | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| General Partnership | Unincorporated entity | Unlimited, joint | Taxable | Yes | 2 partners | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| Limited Partnership | Unincorporated entity | Mixed liability | Taxable | Yes | 2 partners | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

| Sole Proprietorship (Empresa Individual) | Unincorporated entity | Unlimited personal | Taxable | Yes | 1 individual | SERVE / Ministry of Justice | Decree-Law No. 12/2017 |

Each of these structures is examined in full in the sections below.

Public Limited Company (Sociedade Anónima – SA) in Timor-Leste

The Sociedade Anónima (SA) is governed by the Commercial Companies Law (Decree-Law No. 14/2017) and represents the most structurally complex corporate form available under Timorese law. As a separate legal entity, the SA carries its own rights and obligations distinct from its shareholders, with liability confined to each member's subscribed capital.

Share capital is divided into freely transferable shares, which distinguishes this structure from its private counterpart and makes it suited to entities anticipating external investment or eventual public offerings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Anónima (SA) | Incorporated legal entity under Decree-Law No. 14/2017 |

| Members | Shareholders; minimum 2, no statutory maximum | Directors (board): minimum 3 for publicly listed entities |

| Local Presence | Registered office required in Timor-Leste | No statutory registered agent requirement specified |

| Capital | USD 10,000 minimum paid-up share capital | Capital divided into transferable shares |

| Privacy | Shareholder register maintained; generally accessible | Directors disclosed to SERVE (business registry) |

Focus Points

- Taxation: Subject to corporate income tax at 10% on profits; VAT applies at 0% on most domestic supplies with limited exceptions; withholding tax applies to dividends, interest, and royalties — refer to the Autoridade Tributária de Timor-Leste for current rates.

- Annual Compliance: Audited financial statements required; annual general meeting obligations apply.

- Treaty Access: Timor-Leste has a limited tax treaty network; confirm treaty position before structuring cross-border flows.

- Restrictions: Foreign ownership is permitted, though certain sectors require local participation under investment law.

Closing

The SA suits larger trading operations, joint ventures, and businesses seeking structured equity investment. Its transferable share capital offers flexibility for onboarding investors, though the mandatory board composition and audit requirements create a higher ongoing compliance burden than simpler structures.

Best suited for larger enterprises, joint ventures, or businesses planning to raise capital from multiple investors.

Company Incorporation in Timor-Leste

Incorporate a Sociedade Anónima or other entity type in Timor-Leste with end-to-end support from Expanship.

Private Limited Company (Sociedade por Quotas – SQ) in Timor-Leste

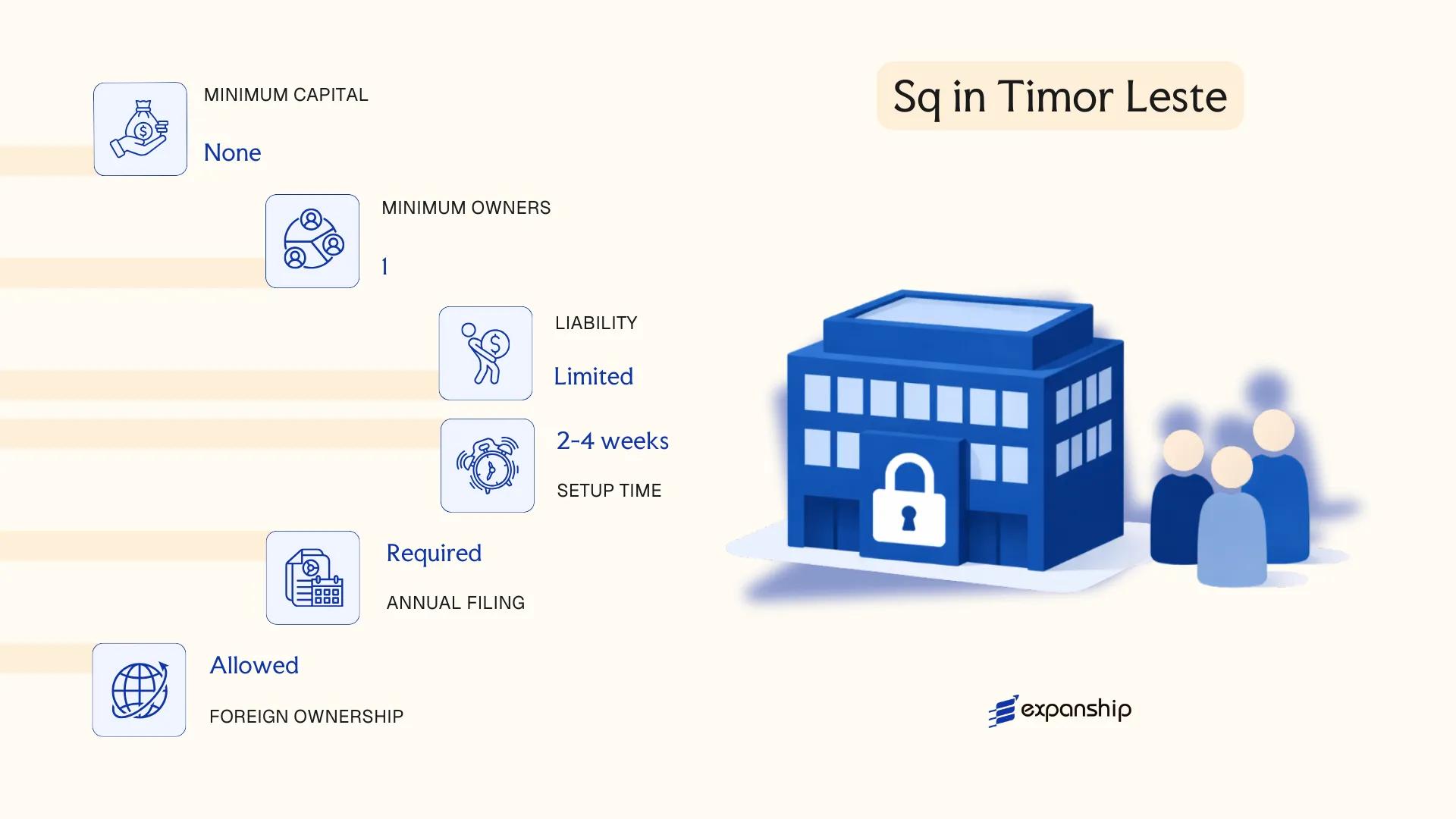

The Sociedade por Quotas SQ Timor-Leste is the most commonly adopted corporate structure for small to medium-sized enterprises and foreign investors entering the market. Governed by the Commercial Companies Law (Decree-Law No. 10/2017), it carries separate legal personality, meaning the entity's obligations are distinct from those of its members.

Liability is confined to each member's capital contribution, creating a clear separation between personal and business assets. The structure is considered a hybrid in that it combines the limited liability protections associated with a public company with the operational flexibility more typical of a closely held firm.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Sociedade por Quotas) | Quota-based capital; not share-based |

| Members | Minimum 1, maximum 30 | Members hold "quotas" rather than shares |

| Management | One or more managers (Gerentes) | No board requirement for smaller firms |

| Local Presence | Registered office address in Timor-Leste required | Registered agent not mandatorily prescribed by statute, but a local address is required |

| Capital | Minimum USD 500; denominated in USD | No paid-up requirement beyond stated minimum |

| Privacy | Member names filed with SERVE | Registry records are accessible to the public |

Focus Points

- Taxation: Subject to corporate income tax at 10% on profits; VAT applies at 0% on most domestic supplies with limited exceptions; withholding tax applies to certain payments to non-residents; no general stamp duty regime.

- Annual Compliance: Annual financial statements must be filed with SERVE (Serviço de Registo e Verificação Empresarial); audit requirements depend on company size thresholds.

- Economic Substance: No formal economic substance legislation currently in force, though physical presence obligations may arise under sector-specific licensing.

- Treaty Access: Timor-Leste has a limited double tax treaty network; access to treaty benefits should be verified on a case-by-case basis.

- Conversion: An SQ may be converted to a Sociedade Anónima (SA) subject to compliance with minimum capital and structural requirements under Decree-Law No. 10/2017.

Closing

The private limited company Timor-Leste structure is suited to trading operations, holding arrangements, and joint ventures where ownership needs to remain concentrated among a defined group of members. Its simplified governance requirements reduce administrative overhead, though the 30-member cap limits scalability for larger investor syndicates.

Small to medium foreign-invested enterprises and joint ventures requiring limited liability without the regulatory burden of a public company structure.

Foreign Business Entities in Timor-Leste [Branch Office, Representative Office]

Foreign companies seeking a foothold without incorporating a separate local entity typically establish either a foreign company branch office Timor-Leste registration or a representative office. Both structures are governed under the Commercial Companies Law (Decree-Law No. 12/2017) and administered through SERVE (Serviço de Registo e Verificação Empresarial), the national business registration authority.

A branch is an extension of its parent and carries no separate legal personality — the foreign parent remains directly liable for its obligations. A representative office is more restricted in scope, permitted only to conduct promotional or liaison activities rather than revenue-generating operations.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Local Presence | Registered address in-country; appointed local representative required | Registered address in-country; appointed local representative required |

| Capital | No statutory minimum; parent's capital backs operations | No statutory minimum |

| Commercial Activity | Permitted — may generate revenue locally | Not permitted — limited to liaison and promotional functions |

| Privacy | Parent company details filed on public record | Parent company details filed on public record |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; withholding tax applies to remittances; representative offices with no local revenue generally have limited direct tax exposure, though payroll obligations still apply to local staff.

- Economic Substance: No formal economic substance regime currently applies, but a demonstrable operational presence is expected for branches conducting trade.

- Annual Compliance: Both structures must file annual returns with SERVE and maintain updated documentation of the parent entity's standing in its home jurisdiction.

- Treaty Access: Timor-Leste's tax treaty network is limited; branch profits may face double taxation depending on the parent's home jurisdiction.

- Restrictions: Representative offices are prohibited from invoicing clients or signing commercial contracts in their own right.

Sub-Types

Branch Office

A branch conducts the full commercial activities of its foreign parent within the local market and is the appropriate structure when your business intends to generate revenue, enter contracts, or employ staff directly.

Representative Office

Registration as a representative office in East Timor is suited to market research, promotional activity, or coordinating with local partners — without the compliance burden attached to active trading operations.

Closing

Foreign business entities are most commonly used by multinationals entering the market for the first time, particularly in the oil and gas, construction, and professional services sectors. The primary advantage of a branch is speed of setup relative to incorporating a new legal entity; the significant drawback is unlimited parental liability exposure.

This structure suits established foreign companies testing the local market or fulfilling a specific project contract, rather than those planning long-term, multi-activity operations.

Partnership Structures in Timor-Leste [General Partnership, Limited Partnership]

Partnership structures in Timor-Leste are governed by the Commercial Companies Law (Law No. 4/2017), which establishes two recognised forms: the General Partnership (Sociedade em Nome Coletivo) and the Limited Partnership (Sociedade em Comandita). Both structures are less commonly used than the SQ or SA but remain legally available for businesses where shared management or tiered liability arrangements are operationally appropriate.

Under Law No. 4/2017, a General Partnership does not confer limited liability on any of its partners, each of whom bears joint and several liability for the firm's obligations. The Limited Partnership introduces a bifurcated structure, distinguishing between general partners who manage the business and bear unlimited liability, and limited partners whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Sociedade em Nome Coletivo | Sociedade em Comandita |

| Partners | Minimum 2 general partners; no statutory maximum | Minimum 1 general partner + 1 limited partner |

| Liability | All partners: unlimited, joint and several | General partners: unlimited; limited partners: capped at capital contribution |

| Local Presence | Registered office in Timor-Leste required | Registered office in Timor-Leste required |

| Capital | No statutory minimum; denominated in USD | No statutory minimum; limited partners' capital must be defined |

| Registration Body | SERVE (Serviço de Registo e Verificação Empresarial) | SERVE |

Focus Points

- Taxation: Partnerships are subject to corporate income tax at 10% on chargeable profits; VAT applies at 2.5% on applicable transactions; withholding tax obligations apply to distributions and payments to non-residents.

- Liability exposure: General partners carry personal liability regardless of structure; limited partners lose liability protection if they participate in management.

- Annual compliance: Audited financial statements and tax filings must be submitted annually to the relevant authorities.

- Treaty access: Timor-Leste has a limited tax treaty network; partnership income may not benefit from preferential withholding rates available to corporate structures.

- Conversion: Conversion to an SQ or SA is permissible under Law No. 4/2017, subject to regulatory approval from SERVE.

Sub-Types

General Partnership (Sociedade em Nome Coletivo)

All partners hold equal management rights by default, and the partnership operates under a collective name. This form is typically used by professional practices or family-run trading operations where all participants are actively involved.

Limited Partnership (Sociedade em Comandita)

Distinguished by its two-tier partner structure, this form suits arrangements where passive investors wish to contribute capital without assuming management responsibilities. General partners retain full operational control and corresponding liability.

Closing

Partnership structures suit closely held businesses, family enterprises, or professional service arrangements where the parties have an established relationship and accept the liability implications. The primary advantage is structural flexibility in allocating management roles; the principal drawback is the unlimited personal liability borne by at least one partner in every case.

Partnership structures are best suited for small, closely held businesses or professional practices where all active participants are known to one another and personal liability is an accepted and manageable risk.

Sole Proprietorship (Empresa Individual) in Timor-Leste

The Empresa Individual Timor-Leste sole proprietorship is the most straightforward business structure available under the country's commercial law framework, governed by the 2011 Commercial Companies Law (Law No. 4/2011) and related SERVE (Serviço de Registo e Verificação Empresarial) registration requirements. Unlike a limited company, this structure carries no separate legal personality — the individual owner and the business are treated as one.

Registration is handled through SERVE, the national business registration authority. Because there is no liability separation, your personal assets are exposed to any claims or debts incurred by the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresa Individual) | No separate legal personality from the owner |

| Proprietor | Single individual only | Referred to as the proprietor; no directors or shareholders |

| Membership | 1 proprietor (minimum and maximum) | Cannot have co-owners; multiple owners require a different structure |

| Local Presence | Registered business address in Timor-Leste required | Must register with SERVE; a physical or maintained address is required |

| Capital | No statutory minimum capital | Denominated in USD, the official currency |

| Liability | Unlimited personal liability | Owner's personal assets fully exposed to business obligations |

Focus Points

- Taxation: Subject to personal income tax on business profits under the Timor-Leste tax regime administered by the Tax Authority (Autoridade Tributária); standard withholding tax, service tax, and sales tax obligations may apply depending on activity and turnover thresholds.

- Annual Compliance: Required to file tax returns and maintain basic financial records; reporting obligations are lighter than those of a capital company but must be observed consistently.

- Economic Substance: No formal economic substance regime applies to this structure, though actual business activity must be conducted locally to justify registration.

- Conversion: Can be converted into a more formal structure such as an SQ if the business grows and limited liability becomes necessary; this requires a new registration process.

- Restrictions: Foreign nationals face restrictions on registering as a sole proprietor; this structure is generally accessible to Timorese citizens and permanent residents.

Closing

The Empresa Individual suits small-scale local traders, individual service providers, and micro-enterprises operating within East Timor with limited administrative overhead. The primary advantage is operational simplicity with low setup cost; the clear limitation is unrestricted personal liability, which becomes a significant exposure as business revenue or obligations grow.

Best suited for Timorese nationals or residents running small, low-risk businesses who prioritise minimal compliance burden over liability protection.

How to Choose the Right Entity Type in Timor-Leste

Choosing the right business entity in Timor-Leste is a structural decision with direct legal and financial consequences — not a formality to resolve after other setup steps.

Why Your Entity Choice Matters

The structure you register determines your obligations, liabilities, and operational permissions from day one. Selecting the wrong form can produce concrete, costly outcomes:

- Registering a foreign branch to conduct local trade without meeting the requirements under the Commercial Companies Law (Law No. 4/2017) can result in administrative penalties or forced deregistration.

- Forming a structure without the capacity to maintain a registered office and local management, where substance requirements apply, may trigger reporting failures with the Autoridade Tributária de Timor-Leste.

- Choosing a structure that mandates audited financial statements when your business operates as a single-person consultancy introduces annual compliance costs that would not arise under a Sole Proprietorship (Empresa Individual).

- Selecting a general partnership when the business involves significant capital assets exposes all partners to unlimited personal liability, including personal assets unrelated to business operations.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each require a different legal vehicle under Timorese commercial law.

- Ownership Structure: A single-owner operation and a multi-investor venture have different governance requirements, pointing toward an Empresa Individual or an SA respectively.

- Local vs. Cross-Border Operations: Entities intending to transact with Timorese residents must be locally registered; a representative office cannot lawfully generate revenue.

- Tax Position: Your eligibility for specific withholding tax treatment under Timor-Leste's tax framework depends on the entity form you register.

- Substance Capacity: If you cannot realistically maintain staff or decision-making functions in-country, certain structures carry higher compliance exposure than others.

- Exit Flexibility: Some structures permit redomiciliation or conversion; confirm this before formation if your long-term plans are uncertain.

Compliance Services for Companies in Timor-Leste

Maintain good standing with Timorese regulatory and tax authorities through structured compliance support.

Conclusion

Choosing the right structure is the first practical decision in any incorporating a company in Timor-Leste guide. The Sociedade por Quotas remains the most commonly registered entity, favored by small to mid-sized businesses for its manageable capital requirements and simpler governance. The Sociedade Anónima suits larger ventures requiring shareholder transferability and access to external capital. Branch offices give foreign firms a direct operational presence without creating a separate legal person, while representative offices are restricted to liaison and promotional functions. General and limited partnerships suit smaller commercial arrangements, and the Empresa Individual is reserved for sole traders operating on a limited scale.

Timor-Leste continues to develop its legal and commercial framework under the oversight of SERVE, and ongoing efforts to expand investment facilitation point toward a more codified regulatory environment in the years ahead. Working with experienced advisers familiar with local registration procedures can help your business structure from the outset correctly.

How Expanship Can Assist You

Expanship company registration Timor-Leste services are built around the specific requirements of the Business Registration and Verification Service (SERVE), the authority that oversees entity formation in the country. From structuring a Sociedade por Quotas for a foreign investor to filing branch office documentation, Expanship handles each step with knowledge of local procedural requirements.

Across your incorporation and beyond, our corporate services cover:

- Document preparation, notarization, and legalization for SERVE submission

- Registered agent and registered office provision in Timor-Leste

- Government filing and direct liaison with relevant authorities

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for newly formed entities

Reach our team directly through Expanship Timor-Leste to discuss your specific setup requirements.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (SQ), or private limited company, is the most frequently registered structure. Its lower capital requirements and simpler governance make it accessible to both domestic entrepreneurs and foreign investors entering the market.

A Branch Office is an extension of a foreign parent entity and does not constitute a separate legal person under Timorese law, meaning the parent retains full liability. An SQ is an independent legal entity, subject to local corporate tax and full annual compliance obligations. The SQ generally permits broader local trading rights than a Representative Office, which is restricted to non-commercial activities.

Among registered structures, the Sociedade por Quotas offers a relatively contained public disclosure profile, as detailed shareholder information is not prominently published in a widely accessible public registry. Nominee arrangements are not formally prohibited but remain subject to beneficial ownership disclosure requirements under applicable anti-money laundering regulations.

A sole proprietorship (Empresa Individual) and an SQ can each be formed by one individual. A Sociedade Anónima requires a minimum of one shareholder but has more demanding governance requirements, while general and limited partnerships require at least two partners by definition.

Foreigners may register an SQ, an SA, or establish a Branch or Representative Office of a foreign company. Foreign participation is subject to sector-specific restrictions under Timorese investment law, and certain activities may require prior approval from the Agência para o Desenvolvimento Empresarial e Turismo (IADE) or a relevant sector regulator.

Timorese commercial law permits structural reorganisation, though the process involves regulatory filings and, in some cases, shareholder resolutions. Conversion from an SQ to an SA is the most commonly undertaken transformation, typically when a business scales and requires broader share issuance capacity.

Not all structures do. The Empresa Individual and general partnerships do not provide a legal separation between the business and its owner or partners, leaving personal assets exposed to business liabilities. The SQ, SA, and limited partnership (in respect of limited partners) each confer separate legal personality under Law No. 4/2017.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.