Key Takeaways

- Business formation in Thailand is governed by the Civil and Commercial Code (CCC) and, for foreign-owned entities, the Foreign Business Act B.E. 2542 (1999), with registration administered by the Department of Business Development (DBD) under the Ministry of Commerce.

- The Private Limited Company (Borisat Chamgad) is the most commonly registered entity structure in Thailand, valued for its defined liability framework and capacity to accommodate foreign participation.

- Thailand operates a territorial tax system, under which corporate income tax applies only to income sourced within the country, a factor that directly influences entity planning for cross-border structures.

- Ordinary and Limited Partnerships carry unlimited liability considerations that limit their practical appeal, while Branch Offices and Representative Offices are designed for multinationals with bounded operational mandates rather than full commercial activity.

Introduction to Entity Types in Thailand

Located in Southeast Asia and bordered by Myanmar, Laos, Cambodia, and Malaysia, Thailand is an independent constitutional monarchy with a well-established legal framework for business formation. The types of business entities in Thailand are governed primarily by the Civil and Commercial Code (CCC) and, for foreign participation, the Foreign Business Act B.E. 2542 (1999). Company registration falls under the jurisdiction of the Department of Business Development (DBD), a division of the Ministry of Commerce.

Thailand operates a territorial tax system, meaning only income sourced within the country is generally subject to corporate income tax.

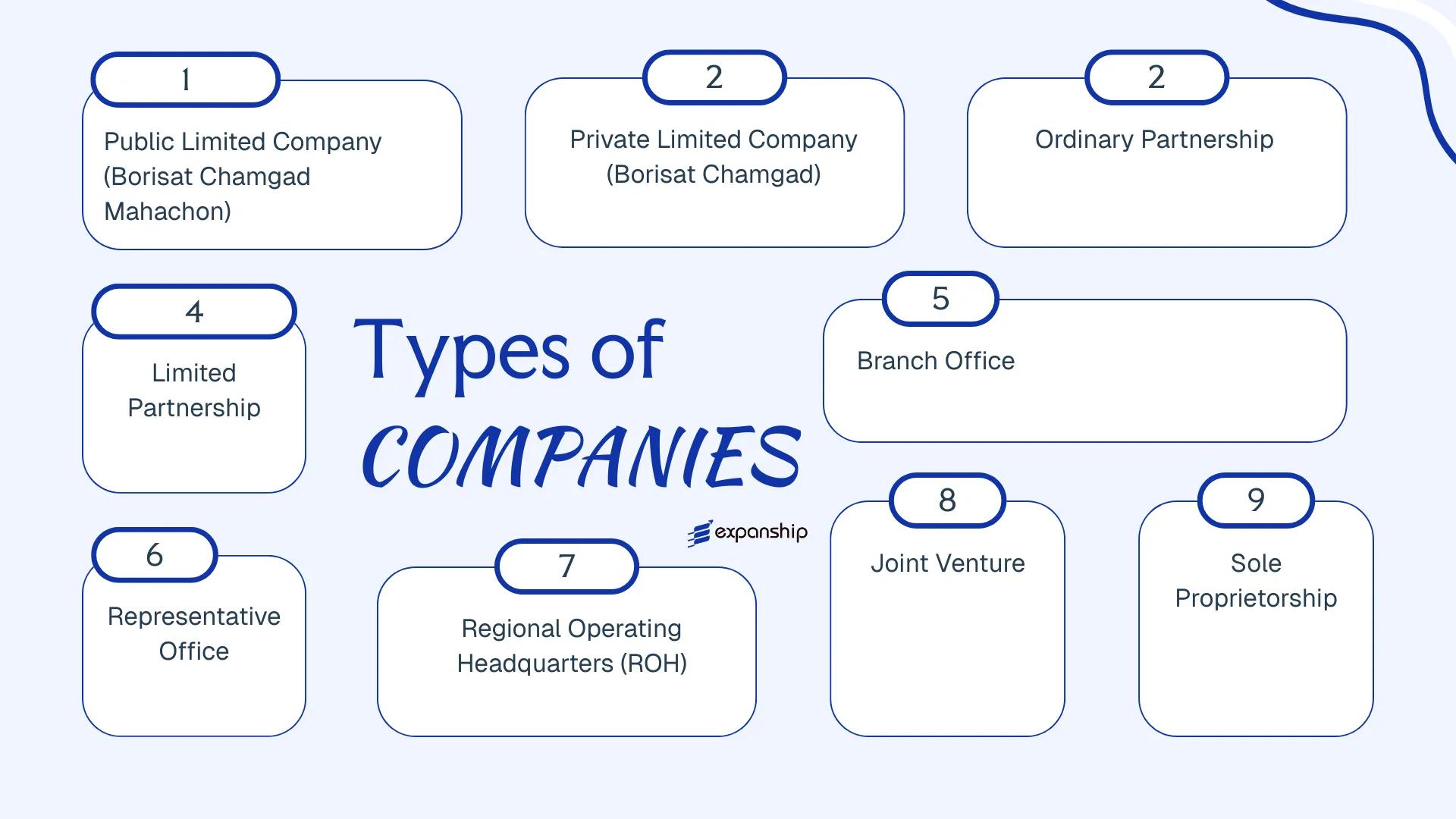

Businesses registering in Thailand can choose from several distinct legal structures: Private Limited Company, Public Limited Company, Ordinary Partnership, Limited Partnership, Branch Office, Representative Office, Regional Operating Headquarters, Joint Venture, and Sole Proprietorship. Each structure carries different requirements around ownership, liability, and permitted activities — particularly where foreign nationals are involved.

This article examines each of these structures in detail, covering formation requirements, ownership rules, and the regulatory considerations relevant to your business.

An Overview of Business Structures in Thailand

Thailand's company law framework accommodates several distinct entity types, each governed primarily by the Civil and Commercial Code (CCC) and, for public companies, by the Public Limited Companies Act B.E. 2535 (1992). Foreign-owned or foreign-operated businesses are also subject to the Foreign Business Act B.E. 2542 (1999), which restricts certain commercial activities to Thai nationals. Each structure carries different implications for liability, ownership, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Separate legal entity | Limited to shares | Taxable | Permitted | 15 promoters | DBD / SEC | Public Limited Companies Act B.E. 2535 |

| Private Limited Company | Separate legal entity | Limited to shares | Taxable | Permitted | 3 shareholders | DBD | Civil and Commercial Code |

| Ordinary Partnership | Unincorporated / Registered | Unlimited (unregistered) / Limited (registered) | Taxable | Permitted | 2 partners | DBD | Civil and Commercial Code |

| Limited Partnership | Registered entity | Mixed: general/limited | Taxable | Permitted | 2 partners | DBD | Civil and Commercial Code |

| Branch Office | Extension of foreign entity | Parent bears full liability | Taxable | Restricted | N/A | DBD / Revenue Dept. | Foreign Business Act B.E. 2542 |

| Representative Office | Extension of foreign entity | Parent bears full liability | Non-income generating | Prohibited | N/A | DBD | Foreign Business Act B.E. 2542 |

| Regional Operating HQ | Separate legal entity | Limited | Taxable (concessionary rates) | Restricted | N/A | BOI / Revenue Dept. | Revenue Code / BOI Rules |

| Joint Venture | Contractual arrangement | Per agreement | Taxable | Permitted | 2 parties | Revenue Dept. | Revenue Code |

| Sole Proprietorship | No legal separation | Unlimited | Taxable | Permitted | 1 owner | DBD / Revenue Dept. | Civil and Commercial Code |

Each of these structures is examined in full in the sections below.

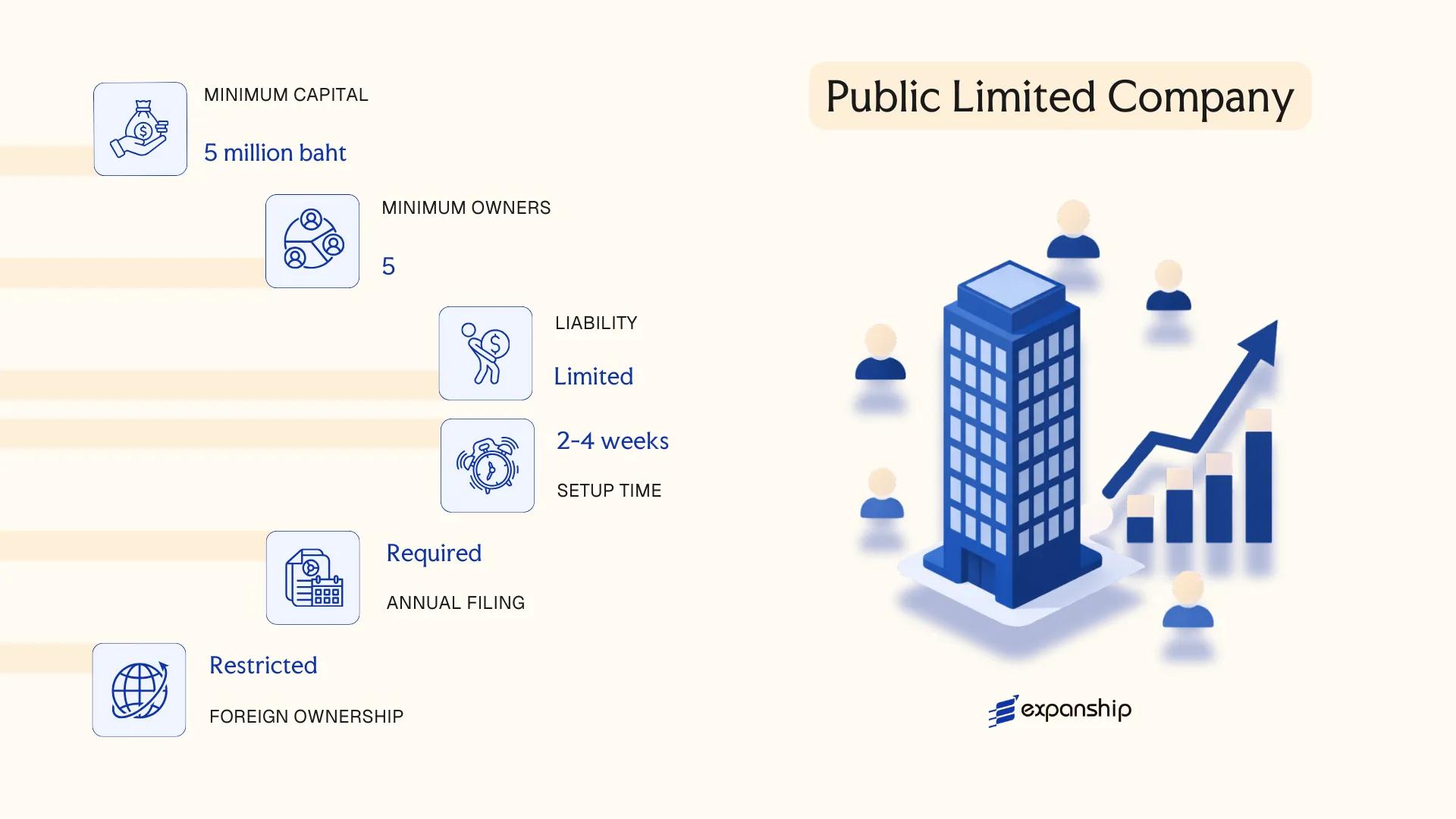

Public Limited Company (Borisat Chamgad Mahachon)

Governed by the Public Limited Companies Act B.E. 2535 (1992), the Thailand public limited company (Borisat Chamgad Mahachon) is a distinct legal entity capable of holding assets, entering contracts, and incurring liabilities in its own name. Shareholders bear no personal liability beyond their subscribed share capital.

Designed for large-scale capital mobilisation, this structure allows shares to be offered to the general public and, subject to Securities and Exchange Commission (SEC) approval, listed on the Stock Exchange of Thailand (SET) or the Market for Alternative Investment (MAI).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PCL) | Separate legal personality; governed by the Public Limited Companies Act B.E. 2535 |

| Members | Shareholders (minimum 15 at all times); no maximum | Directors: minimum 5, majority must be Thai-resident; Auditor required |

| Local Presence | Registered office address in Thailand required | Must maintain a physical presence; registered agent not mandatory by statute |

| Capital | THB 5,000,000 minimum registered capital for public offering; no universal statutory minimum for non-listed PCLs | At least 25% of capital must be paid up at registration |

| Privacy | Shareholder register is publicly accessible | Annual financial statements filed with the Department of Business Development (DBD) are public record |

| Share Structure | Par value shares only; multiple share classes permitted | Bearer shares are not permitted |

Focus Points

- Taxation: Subject to corporate income tax at 20% on net profits; VAT applies at 7% (standard rate) on taxable supplies; withholding tax applies to dividends, interest, and royalties at rates ranging from 1% to 15% depending on payment type and recipient; stamp duty applies to certain instruments.

- Annual Compliance: Mandatory annual general meeting within four months of fiscal year-end; audited financial statements filed with the DBD; statutory reserves of at least 5% of annual net profit until the reserve reaches 10% of registered capital.

- Treaty Access: Thai PCLs are eligible for benefits under Thailand's double tax agreement (DTA) network, covering 60+ jurisdictions.

- Foreign Ownership: Subject to the Foreign Business Act B.E. 2542 (1999); foreign shareholding above 49% in restricted business categories requires a Foreign Business Licence or treaty exemption.

- Conversion: A private limited company may convert to a PCL by special resolution and re-registration with the DBD, subject to meeting minimum shareholder thresholds.

Closing

A PCL suits businesses seeking public capital markets access, institutional investment, or a path to exchange listing — though the minimum 15-shareholder requirement and ongoing SEC/SET disclosure obligations create a compliance burden not suited to closely held or early-stage operations.

Best suited for large enterprises or growth-stage businesses intending to list on the SET or MAI and prepared to meet continuous public disclosure requirements.

Company Incorporation in Thailand

Incorporate your business in Thailand with expert support across entity selection, registration, and post-incorporation compliance.

Private Limited Company (Borisat Chamgad)

The Thailand private limited company, known locally as Borisat Chamgad, is governed by the Civil and Commercial Code of Thailand (Books III–IV), which sets out the formation, governance, and dissolution requirements for this structure. It carries separate legal personality, meaning the entity holds rights and obligations distinct from its shareholders, with liability confined to the amount unpaid on each member's shares.

Registered with the Department of Business Development (DBD) under the Ministry of Commerce, this is the most widely used structure for foreign and domestic businesses operating in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Juristic person (limited liability company) | Separate legal personality from its shareholders |

| Members | Shareholders: minimum 3 at all times; no statutory maximum | Shareholders elect a board of directors to manage the firm |

| Directors | Minimum 1 director; no maximum | At least one director must be authorised to sign on behalf of the entity |

| Local Presence | Registered office address in Thailand required | A physical or virtual address; a registered agent is not a statutory requirement |

| Capital | THB; no statutory minimum for most businesses; fully paid-up capital affects work permit and BOI eligibility | Foreign Business Licence applicants typically require THB 3M minimum registered capital |

| Privacy | Shareholder and director details filed with DBD and publicly searchable | No confidentiality register available |

Focus Points

- Taxation: Subject to corporate income tax at 20% on net profits; VAT applies at 7% (standard rate) once annual revenue exceeds THB 1.8M; withholding tax obligations apply on dividends, service fees, and royalties paid domestically and cross-border; stamp duty applies on certain instruments.

- Foreign Ownership: The Foreign Business Act B.E. 2542 (1999) restricts foreign majority ownership in many sectors; a Foreign Business Licence or BOI promotion may be required to operate.

- Annual Compliance: Mandatory obligations include audited financial statements, an Annual General Meeting, and filing of the audited accounts with the DBD within 5 months of financial year-end.

- Treaty Access: Thailand maintains an active network of double tax agreements; residency and substance within the entity affect access to reduced withholding rates.

- Conversion: A private limited company may convert to a public limited company through a prescribed process under the Public Limited Companies Act B.E. 2535 (1992).

Closing

A Borisat Chamgad suits trading operations, service businesses, and holding structures where limited liability and a formal corporate framework are required, though foreign shareholders must assess sector-specific restrictions under the Foreign Business Act before proceeding.

Foreign investors and domestic entrepreneurs establishing a trading, services, or holding business who require limited liability and a recognised corporate structure under Thai law.

Partnerships [Ordinary Partnership, Limited Partnership]

Thai partnerships are governed by the Civil and Commercial Code of Thailand (CCC), specifically Books III and IV. Neither an ordinary partnership nor a limited partnership is treated as a separate legal entity in the same manner as a limited company, though a registered ordinary partnership does acquire a degree of juridical personality upon registration with the Department of Business Development (DBD).

Thailand limited partnership registration follows a distinct legal path from its ordinary counterpart, with liability structured differently across partner classes.

Key Characteristics

| Requirement | Ordinary Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unregistered or registered; juridical person only upon registration | Registered entity; recognised upon DBD registration |

| Members | Called "partners"; minimum 2, no statutory maximum; all bear unlimited liability | Called "partners"; minimum 2; at least 1 general partner (unlimited liability) and 1 limited partner (liability capped at contribution) |

| Local Presence | Registered address in Thailand required | Registered address in Thailand required |

| Capital | No statutory minimum; contributions may be cash, property, or services | No statutory minimum; limited partner's liability equals their registered contribution |

| Privacy | Partner names filed on public record with DBD | Partner names and contribution amounts disclosed on public record |

Focus Points

- Taxation: Registered partnerships are subject to corporate income tax at standard rates; unregistered ordinary partnerships are taxed as individuals; VAT registration required if annual revenue exceeds THB 1.8 million; withholding tax obligations apply on applicable payments.

- Foreign Ownership: Business activities involving foreign partners may trigger restrictions under the Foreign Business Act B.E. 2542 (1999), potentially requiring a Foreign Business License.

- Annual Compliance: Registered entities must file audited financial statements and annual returns with the DBD.

- Conversion: A registered ordinary partnership may convert to a limited company under CCC procedures, subject to creditor notification requirements.

- Treaty Access: Partnerships structured with foreign partners have limited access to Thailand's double tax agreements, which generally apply to residents and companies.

Sub-Types

Ordinary Partnership (Huang Suan)

Two forms exist: unregistered, where partners share unlimited joint liability and the arrangement has no juridical personality, and registered, where the partnership gains limited legal standing. Unregistered formations are common for small, informal domestic ventures.

Limited Partnership (Huang Suan Chamgad)

At least one general partner bears full personal liability for all obligations, while limited partners' exposure is confined to their declared capital contribution. This structure is used where passive investors wish to participate without assuming management responsibility.

Closing

Partnerships in Thailand are used primarily for small domestic trading operations or professional service arrangements where incorporation costs are not warranted. The structure offers a straightforward setup process, though the unlimited personal liability carried by general and ordinary partners presents significant financial exposure.

This structure suits small-scale domestic operators or professional services firms with a limited partner base and low external liability risk.

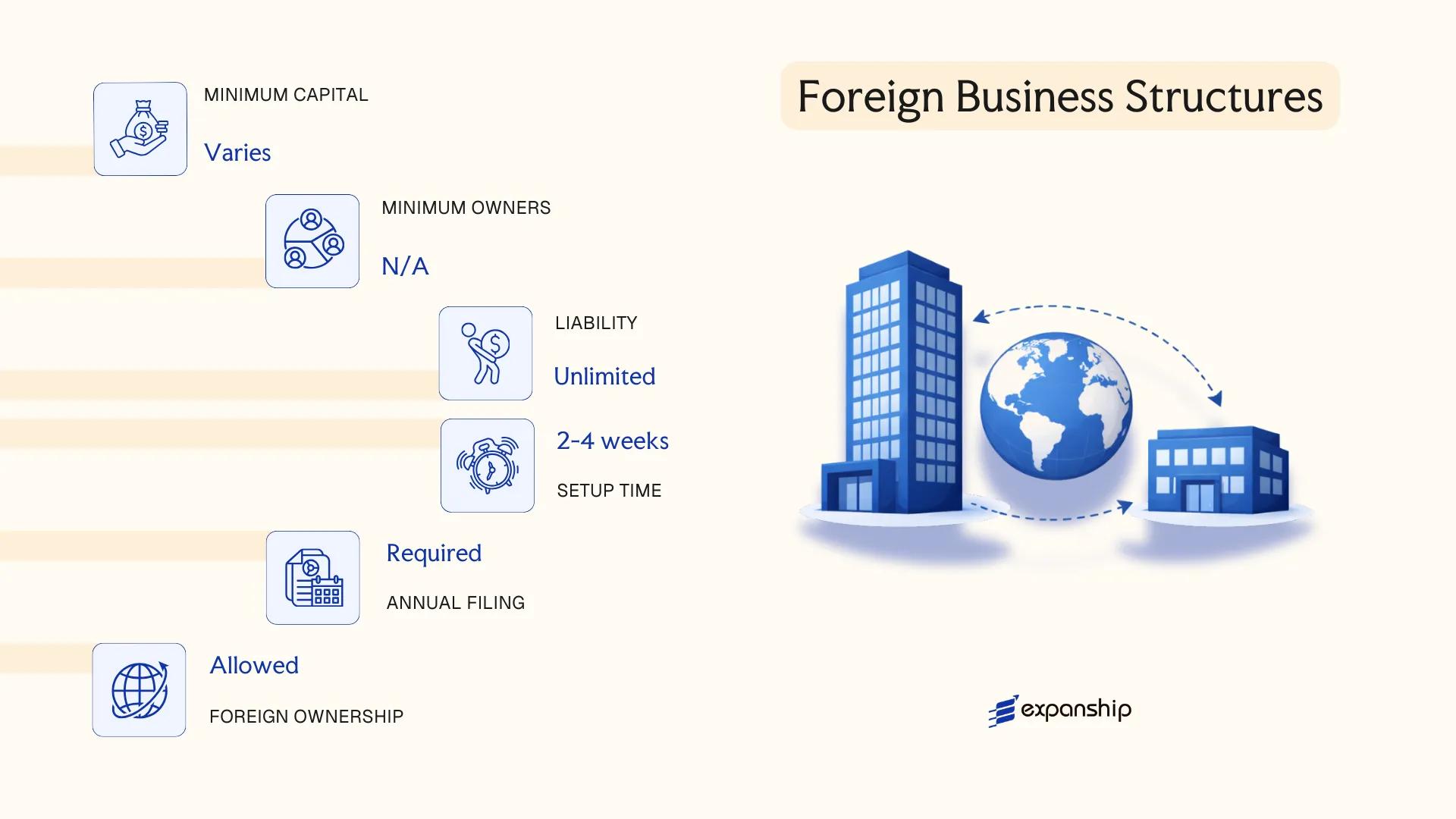

Foreign Business Structures [Branch Office, Representative Office, Regional Operating Headquarters]

Foreign business structures in Thailand are governed primarily by the Foreign Business Act B.E. 2542 (1999), which classifies restricted business activities into three lists and requires foreign entities to obtain a Foreign Business License or operate under a treaty exemption. Unlike locally incorporated entities, these structures typically remain extensions of the parent company abroad rather than separate legal persons under Thai law.

Each structure carries different operational boundaries. A branch office can generate revenue but is treated as part of its foreign parent, meaning the parent bears full liability. A representative office is permitted only for non-revenue activities such as sourcing, reporting, or quality inspection.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Revenue-generating, within approved scope | Non-revenue activities only (liaison, sourcing, inspection) |

| Registered Manager | At least one locally responsible manager required | At least one locally responsible manager required |

| Local Office | Physical office address in Thailand required | Physical office address in Thailand required |

| Capital (Remittance) | Minimum THB 3 million remitted from parent | Minimum THB 3 million remitted from parent |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch offices are subject to 20% corporate income tax on Thailand-sourced profits, plus a 10% branch remittance tax on profits sent abroad; representative offices, generating no income, are generally not subject to CIT but must still file annual accounts and may have VAT registration obligations depending on activities.

- Economic Substance: Both structures require a genuine physical presence and locally responsible staff to satisfy the Revenue Department and the Department of Business Development (DBD).

- Annual Compliance: Annual financial statements must be audited and filed with the DBD; branch offices additionally file corporate income tax returns with the Revenue Department.

- Treaty Access: Double tax treaty benefits may be available to branch offices depending on the parent's jurisdiction and treaty provisions, but representative offices typically fall outside treaty scope due to their non-income nature.

- Restrictions: The Foreign Business Act restricts or prohibits many business activities for foreign entities; a Foreign Business License from the Foreign Business Committee is required for restricted List 2 and List 3 activities.

Sub-Types

Regional Operating Headquarters (ROH)

A Regional Operating Headquarters is a company incorporated in Thailand under the Civil and Commercial Code but specifically promoted by the Board of Investment (BOI) or structured to qualify for Revenue Department incentives. Unlike a standard branch, an ROH is a separate legal entity providing management, technical, or support services to affiliated companies in the region, and it may access preferential corporate income tax rates on qualifying income streams.

Closing Paragraph and Recommendations

Branch and representative offices suit multinationals that need a controlled operational or liaison presence without committing to full local incorporation, though the branch structure's remittance tax and the representative office's prohibition on revenue generation are material constraints that limit their utility for growth-oriented market entry.

Foreign companies testing the Thai market or providing regional support to group entities before committing to full local incorporation.

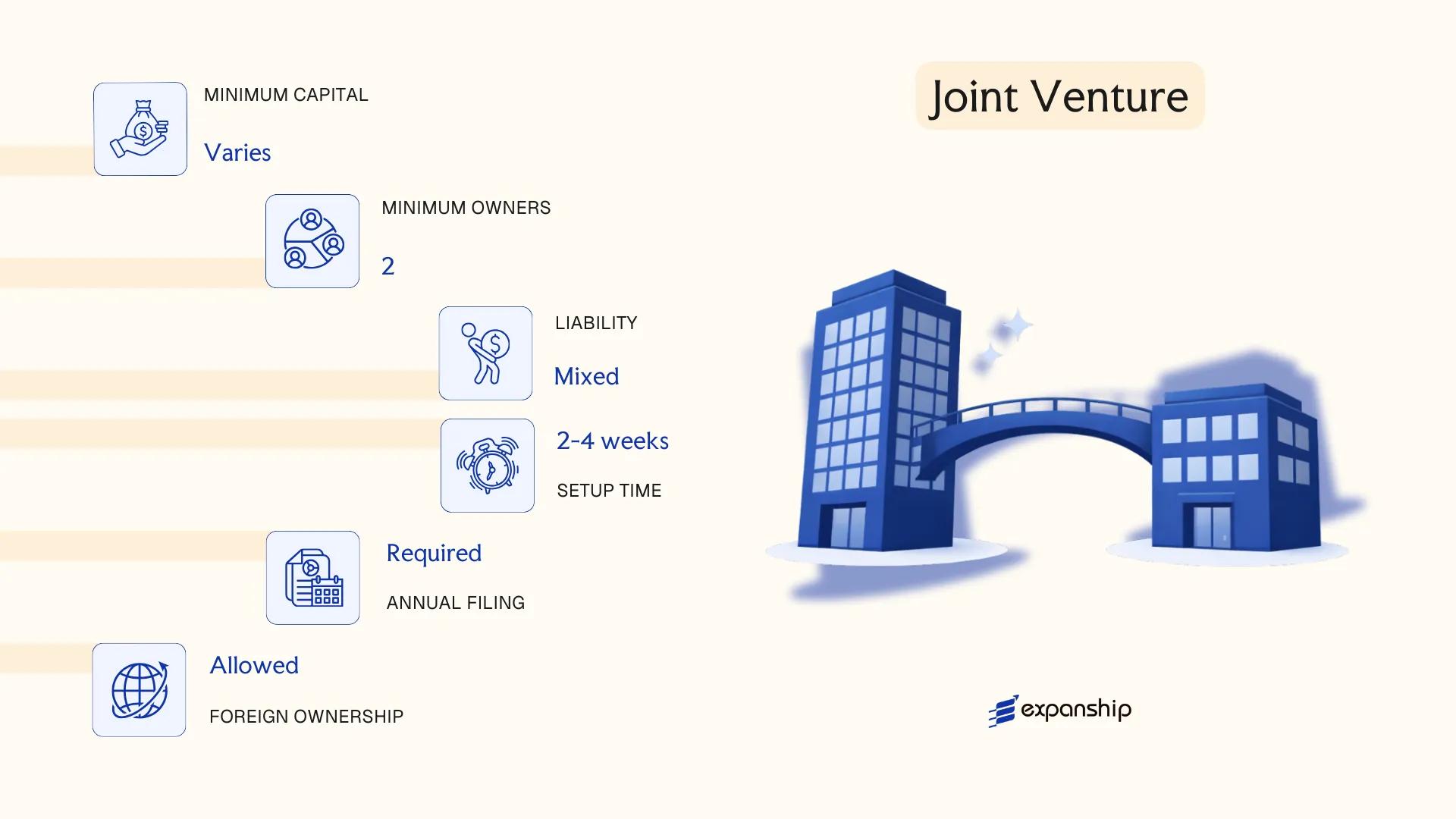

Joint Venture

A joint venture in Thailand for foreign companies does not constitute a distinct legal entity under a single governing statute. Instead, parties structure a JV either as a contractual arrangement or through an incorporated vehicle — most commonly a private limited company registered under the Civil and Commercial Code (CCC). The chosen structure determines liability exposure, governance rights, and how profits are distributed between participants.

Because Thailand's Foreign Business Act B.E. 2542 (1999) restricts foreign equity in many sectors, JVs are frequently used as a mechanism to combine foreign capital with Thai shareholding, allowing the combined entity to operate in otherwise restricted activities. The foreign equity ceiling in such cases is generally 49%, though promoted activities under the Board of Investment (BOI) may permit higher foreign ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Contractual or incorporated (typically Private Limited Company) | No standalone JV statute exists; structure governed by CCC or specific sector laws |

| Parties | Referred to as shareholders or co-venturers | Minimum 2 parties; no statutory maximum specific to JVs |

| Local Presence | Registered office in Thailand required if incorporated | Contractual JVs have no separate registration requirement |

| Capital | THB; no universal minimum for JVs, though FBA-restricted sectors may require paid-up capital thresholds | BOI-promoted entities have separate capital requirements |

| Foreign Ownership | Generally capped at 49% under the FBA | BOI promotion or specific treaty arrangements may allow majority foreign ownership |

| Privacy | Shareholder details filed with the Department of Business Development (DBD); publicly searchable | No beneficial ownership register equivalent to some other jurisdictions |

Focus Points

- Taxation: Corporate income tax applies at 20% on net profits; VAT at 7% on applicable supplies; withholding tax on dividends paid to foreign partners is typically 10%; stamp duty applies to the JV agreement itself at prescribed rates under the Revenue Code.

- Treaty Access: Double tax treaty benefits depend on the residency of each JV partner, not the JV vehicle itself; treaty eligibility must be assessed per partner.

- BOI Promotion: If the JV qualifies for BOI promotion, corporate income tax exemptions and foreign ownership relaxations may apply for a defined period.

- Annual Compliance: Incorporated JVs must file audited financial statements with the DBD and submit annual corporate income tax returns to the Revenue Department.

- Restrictions: The Thailand JV agreement structure cannot override FBA restrictions; sector-specific licensing (e.g., financial services, telecoms) may impose additional ownership or operational conditions.

Closing

Incorporated joint ventures are used most commonly for manufacturing, infrastructure, and BOI-promoted projects where combining local market access with foreign technical or financial input is operationally necessary. The principal advantage is the ability to pool capabilities across parties under a defined governance framework; the main limitation is that foreign partners are often structurally constrained to minority positions, which can complicate decision-making authority.

A JV structure suits foreign businesses entering restricted sectors in Thailand that require a Thai partner to meet FBA ownership thresholds or to access BOI incentives.

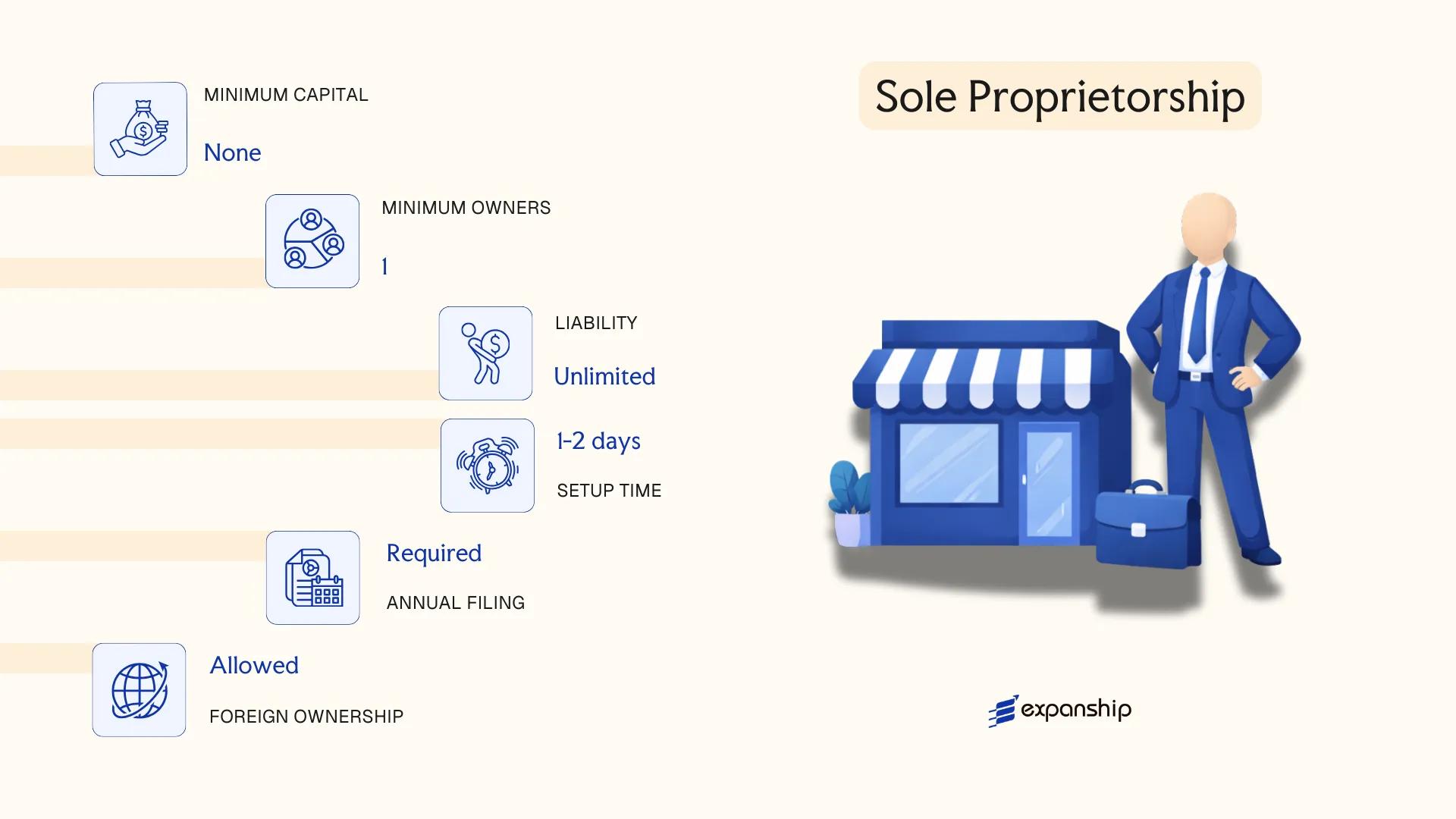

Sole Proprietorship

A sole proprietorship in Thailand for foreigners carries significant structural limitations that distinguish it from corporate forms. Governed by the Civil and Commercial Code of Thailand, this structure grants no separate legal personality — the business and its owner are treated as one legal entity, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Department of Business Development (DBD) under the Ministry of Commerce. Individual business registration in Thailand under this structure is straightforward for Thai nationals, but foreign nationals face a hard restriction: the Foreign Business Act B.E. 2542 (1999) prohibits non-Thai individuals from operating most business activities as sole traders without a Foreign Business Licence, which is rarely granted for this structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole entity | No separate legal personality; owner bears full liability |

| Members | Sole proprietor (1 individual only) | Must be a Thai national in most cases; foreigners face FBA restrictions |

| Local Presence | Registered business address required | DBD registration mandatory; no separate registered agent requirement |

| Capital | No statutory minimum (THB) | Owner injects capital at discretion |

| Privacy | Owner's name publicly registered with DBD | No shareholder register concept; full public identification of owner |

Focus Points

- Taxation: Subject to personal income tax (PIT) under progressive rates up to 35%; VAT registration required if annual revenue exceeds THB 1.8 million; no corporate income tax applies.

- Compliance: Annual personal income tax filing required; no audited financial statements mandated at entity level.

- Foreign Restrictions: The Foreign Business Act B.E. 2542 restricts most business activities for non-Thai sole traders; a Foreign Business Licence or Treaty of Amity protection (for US nationals) may apply in limited cases.

- Conversion: No formal statutory conversion mechanism exists; transitioning to a private limited company requires new incorporation.

Closing

A single-owner business in Thailand under this structure suits small-scale, low-risk operations run by Thai nationals, with the primary advantage of minimal administrative burden. The absence of liability protection makes it unsuitable for any business carrying financial, legal, or operational risk.

Thai nationals operating small, low-turnover local businesses who require minimal setup formality and have no need for liability separation.

How to Choose the Right Entity Type in Thailand

Selecting how to choose your business entity type in Thailand requires more than comparing registration costs. The structure you register determines your tax exposure, liability limits, operational permissions, and long-term compliance obligations.

Why Your Entity Choice Matters

Registering the wrong structure has concrete legal and financial consequences:

- A foreign business operating through an entity that does not hold a Foreign Business License under the Foreign Business Act B.E. 2542 (1999) may face criminal penalties and forced closure.

- Choosing a structure without access to Thailand's double tax agreement network means withholding tax reductions available under those treaties cannot be claimed, increasing tax costs on cross-border payments.

- Selecting a Representative Office when your business requires revenue-generating activity will place every transaction in breach of the permitted scope defined by the Department of Business Development.

- Registering a private limited company for a single-person consultancy creates mandatory annual audit requirements under the Accounting Act B.E. 2543, adding costs that a sole proprietorship does not carry.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each require a distinct structure under Thai law.

- Foreign Ownership: The Foreign Business Act restricts majority foreign ownership in listed business categories, which directly limits which structures are available to you.

- Tax Objectives: Your need for treaty access, BOI promotion eligibility, or full tax exemption each point to a different entity type.

- Liability Exposure: If personal liability protection is a priority, a partnership structure will not provide the same separation as a limited company.

- Substance Capacity: If you cannot maintain a physical office and local staff, structures requiring demonstrated operational presence will create ongoing compliance risk.

- Exit Strategy: Not all Thai entities permit straightforward conversion or redomiciliation, so your intended exit path should be considered before registration.

The primary legislation governing company formation is the Civil and Commercial Code of Thailand, which is available in full on the official Krisdika government legal database.

Corporate Compliance Services in Thailand

Ongoing compliance support for companies registered in Thailand, covering annual filings, audits, and regulatory obligations.

Conclusion

Selecting the right structure is the first substantive decision in any Thailand company incorporation summary guide, and that choice shapes everything from tax exposure to operational flexibility. The Private Limited Company remains the most commonly registered entity in the country, favored for its defined liability, familiar governance framework, and suitability for foreign participation under the Foreign Business Act B.E. 2542. Public Limited Companies suit firms seeking capital market access through the Stock Exchange of Thailand. Ordinary and Limited Partnerships carry unlimited liability considerations that restrict their appeal. Branch and Representative Offices serve multinationals with specific, bounded mandates rather than full commercial operations.

Regulatory oversight has grown more consistent across the Department of Business Development and the Revenue Department in recent years, and Thailand's expanding double tax treaty network continues to influence entity planning for cross-border structures. Expanship's team works directly within this framework to support your formation and compliance requirements.

How Expanship Can Assist You

Expanship provides company incorporation services in Thailand across the full range of structures covered in this blog — from a Private Limited Company registered with the Department of Business Development (DBD) to a Branch Office or Representative Office requiring Foreign Business License consideration under the Foreign Business Act B.E. 2542. Your specific structure determines the filing pathway, and Expanship manages that process end to end.

From initial document preparation through to post-registration obligations, the scope of support includes:

- Memorandum and Articles of Association drafting and notarization

- DBD registration filing and shareholder/director documentation

- Registered office address and agent provision

- BOI promotion application support where applicable

- Ongoing compliance management, including annual returns and statutory meetings

- Corporate bank account introduction assistance

Get in touch with Expanship Thailand to discuss which structure fits your business objectives.

Frequently Asked Questions (FAQ)

The Private Limited Company (Borisat Chamgad) is the most frequently formed structure by both Thai nationals and foreign investors. Its combination of limited liability, defined capital structure, and eligibility under the Foreign Business Act makes it the default choice for most commercial ventures.

A Branch Office is not a separate legal entity; it is an extension of its foreign parent and carries no independent liability protection. A Private Limited Company, incorporated locally under the Civil and Commercial Code, is a distinct legal person and can trade freely within the categories permitted to Thai-majority entities. Compliance obligations differ accordingly, with Branch Offices subject to remittance tax on profits transferred abroad.

A Private Limited Company does not publicly disclose beneficial ownership details beyond what is filed with the Department of Business Development (DBD). Shareholder registers are held at the registered office rather than published in a searchable public database. Thai nominee shareholders have historically been used to obscure foreign ownership, though this practice carries legal risk under the Foreign Business Act B.E. 2542.

No. A Private Limited Company requires a minimum of three promoters at incorporation and at least two shareholders post-registration. A Registered Ordinary Partnership and a Limited Partnership each require at least two partners. Only a Sole Proprietorship can be established by one individual acting alone.

Foreigners may incorporate a Private Limited Company, establish a Branch Office, or register a Representative Office. Majority foreign ownership in most business categories is restricted under the Foreign Business Act B.E. 2542, which means foreign shareholders typically require either a Foreign Business License or Treaty of Amity protection (available to US nationals) to hold more than 49% of shares. A Regional Operating Headquarters structure offers an alternative path with specific BOI or Revenue Department approvals.

Conversion between entity types is not broadly provided for under Thai corporate law as a single statutory procedure. A Sole Proprietorship or partnership cannot be converted directly into a Private Limited Company; the typical approach is to incorporate a new entity and transfer the business. Restructuring between company forms generally requires dissolution of the existing structure and fresh registration with the DBD.

No. A Registered Ordinary Partnership acquires legal personality upon registration with the DBD, but an unregistered ordinary partnership does not. A Limited Partnership has separate legal personality once registered. A Sole Proprietorship has no legal separation between the owner and the business, meaning personal assets remain exposed to business liabilities.

A Sole Proprietorship has no annual general meeting requirement, no statutory audit obligation under the Accounting Act B.E. 2543, and no board resolutions to maintain. A Representative Office, while a foreign business structure, is similarly limited in scope but must file annual activity reports with the DBD and is prohibited from generating revenue, which limits its operational utility.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.