Key Takeaways

- San Marino's company registry, the Ufficio Registro Società e Licenze, oversees all corporate structures defined under domestic legislation, including the S.p.A., S.r.l., S.n.c., S.a.s., Branch Office, Representative Office, and Ditta Individuale.

- The S.r.l. is the most commonly registered entity in San Marino, favored by small and medium businesses for its limited liability protection and manageable capital requirements.

- Despite being a landlocked microstate entirely surrounded by Italy, San Marino operates its own Civil Code and tax regime entirely independent of the European Union.

- Foreign firms seeking market presence without separate incorporation can establish a branch office, while San Marino's expanding double taxation agreement network and OECD-aligned transparency commitments continue to strengthen its international standing.

Introduction to Entity Types in San Marino

San Marino is a landlocked microstate within central Italy, bordered entirely by the Italian regions of Emilia-Romagna and Marche. It operates as a fully independent republic — one of the world's oldest — with its own legal system, corporate law, and tax regime distinct from the European Union, of which it is not a member.

Company registration and corporate compliance fall under the authority of the Ufficio Registro Società e Licenze, the body responsible for maintaining the official company registry. The republic applies a low-tax regime with territorial elements, making it structurally different from both EU member states and traditional offshore jurisdictions.

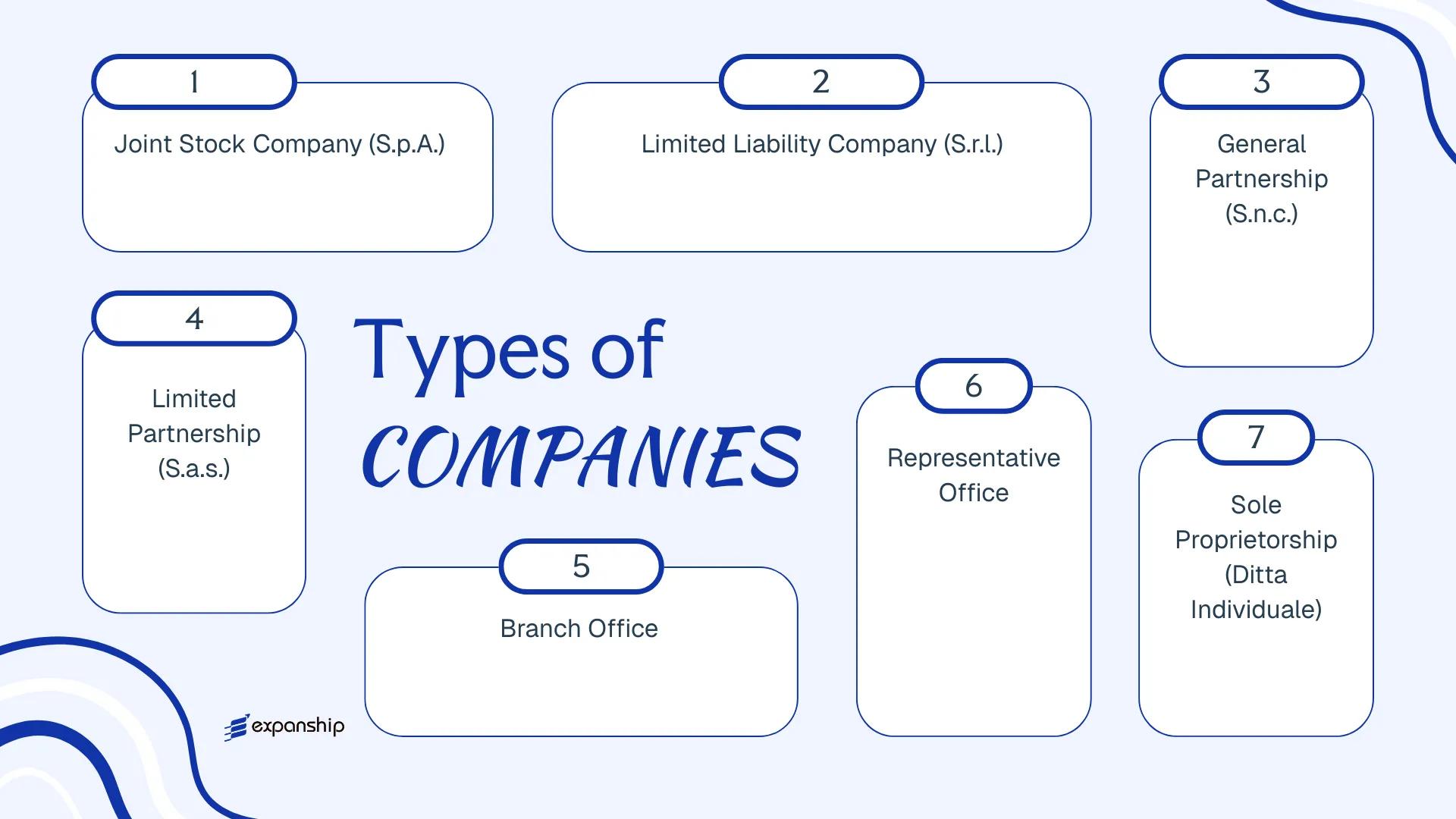

Business entity types in San Marino are defined under domestic corporate legislation and include the following forms:

- Società per Azioni (S.p.A.)

- Società a Responsabilità Limitata (S.r.l.)

- Società in Nome Collettivo (S.n.c.)

- Società in Accomandita Semplice (S.a.s.)

- Branch Office

- Representative Office

- Ditta Individuale (Sole Proprietorship)

Each of these San Marino corporate structures carries distinct requirements around capital, liability, governance, and suitability for foreign ownership — all of which are addressed in the sections that follow.

An Overview of Business Structures in San Marino

San Marino's company law framework recognises several distinct entity types, each governed primarily by Law No. 47 of 2006 on commercial companies, along with supplementary legislation that has been amended over time. Understanding the San Marino business structures overview is a practical starting point before examining any single form in depth. Each structure carries different implications for liability, ownership, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| S.p.A. | Joint Stock Company | Limited to share capital | Taxed | Permitted | 1 shareholder | Registry of Companies | Law No. 47/2006 |

| S.r.l. | Limited Liability Company | Limited to quota | Taxed | Permitted | 1 member | Registry of Companies | Law No. 47/2006 |

| S.n.c. | General Partnership | Unlimited, joint | Taxed | Permitted | 2 partners | Registry of Companies | Law No. 47/2006 |

| S.a.s. | Limited Partnership | Mixed liability | Taxed | Permitted | 2 partners | Registry of Companies | Law No. 47/2006 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Permitted | N/A | Registry of Companies | Law No. 47/2006 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Registry of Companies | Law No. 47/2006 |

| Ditta Individuale | Sole Proprietorship | Unlimited, personal | Taxed | Permitted | 1 individual | Registry of Companies | Law No. 47/2006 |

Each of these structures is examined in full in the sections below.

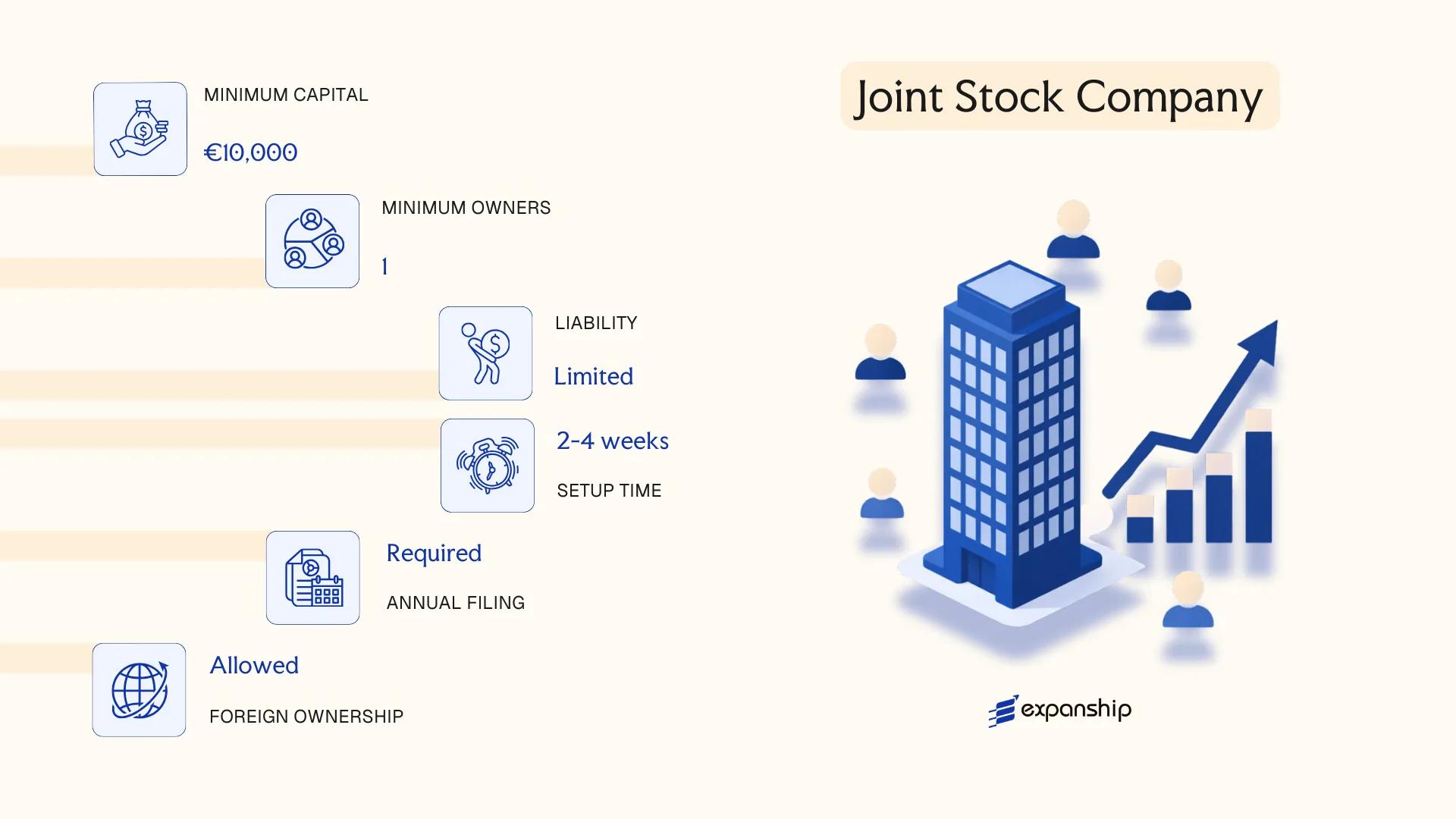

Società per Azioni (S.p.A.) — Joint Stock Company

Governed by San Marino's corporate law framework — primarily Law No. 47 of 2006 and its subsequent amendments — the San Marino SpA joint stock company carries full separate legal personality, meaning the entity itself holds rights, obligations, and assets distinct from its shareholders. Liability is limited to each shareholder's capital contribution.

Capital is divided into transferable shares, which allows ownership to change hands without restructuring the entity itself. This makes the Società per Azioni San Marino the structure most commonly used when investor participation, institutional funding, or eventual listing is anticipated.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Società per Azioni (S.p.A.) | Separate legal personality; shareholders not personally liable |

| Members | Shareholders: minimum 1 (sole shareholder S.p.A. permitted) | No statutory maximum; single-member S.p.A. requires full capital payment on formation |

| Governance | Board of Directors (minimum 1) + Board of Statutory Auditors (Collegio Sindacale) | Collegio Sindacale mandatory above certain thresholds |

| Local Presence | Registered office in San Marino required | A physical registered address; no statutory requirement for a local director |

| Share Capital | Minimum €77,000 (or equivalent in SMR currency references); at least 25% paid up on incorporation | Full payment required for single-member formations |

| Privacy | Shareholders recorded in the Companies Register (Registro delle Imprese) | Register is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at a standard rate of 17%; VAT equivalent (IGR/monofase regime) applies to applicable transactions; withholding taxes apply to dividends distributed to non-residents — consult the Ufficio Tributario (San Marino Tax Authority) for current rates and treaty positions.

- Economic Substance: No codified economic substance regime equivalent to offshore jurisdictions, but genuine local registration and activity are expected for tax residency claims.

- Annual Compliance: Annual financial statements must be filed with the Registro delle Imprese; statutory audit obligations apply above defined size thresholds.

- Treaty Access: San Marino has concluded a limited number of double taxation agreements, including one with Italy; SpA incorporation San Marino may provide access where treaties apply.

- Conversion: An S.p.A. may be converted into an S.r.l. through a formal shareholders' resolution and registration procedure.

Closing

The S.p.A. suits holding structures, larger trading operations, and businesses seeking to raise capital from multiple investors. Its primary advantage is the transferability of shares without member consent requirements; the main drawback is the higher minimum capital threshold and mandatory governance bodies that increase administrative overhead.

Best suited for businesses anticipating external investment, multi-shareholder structures, or future equity transfers requiring a formally governed, capital-backed entity.

Company Incorporation in San Marino

Incorporate an S.p.A. or other entity type in San Marino with end-to-end support from registration to compliance.

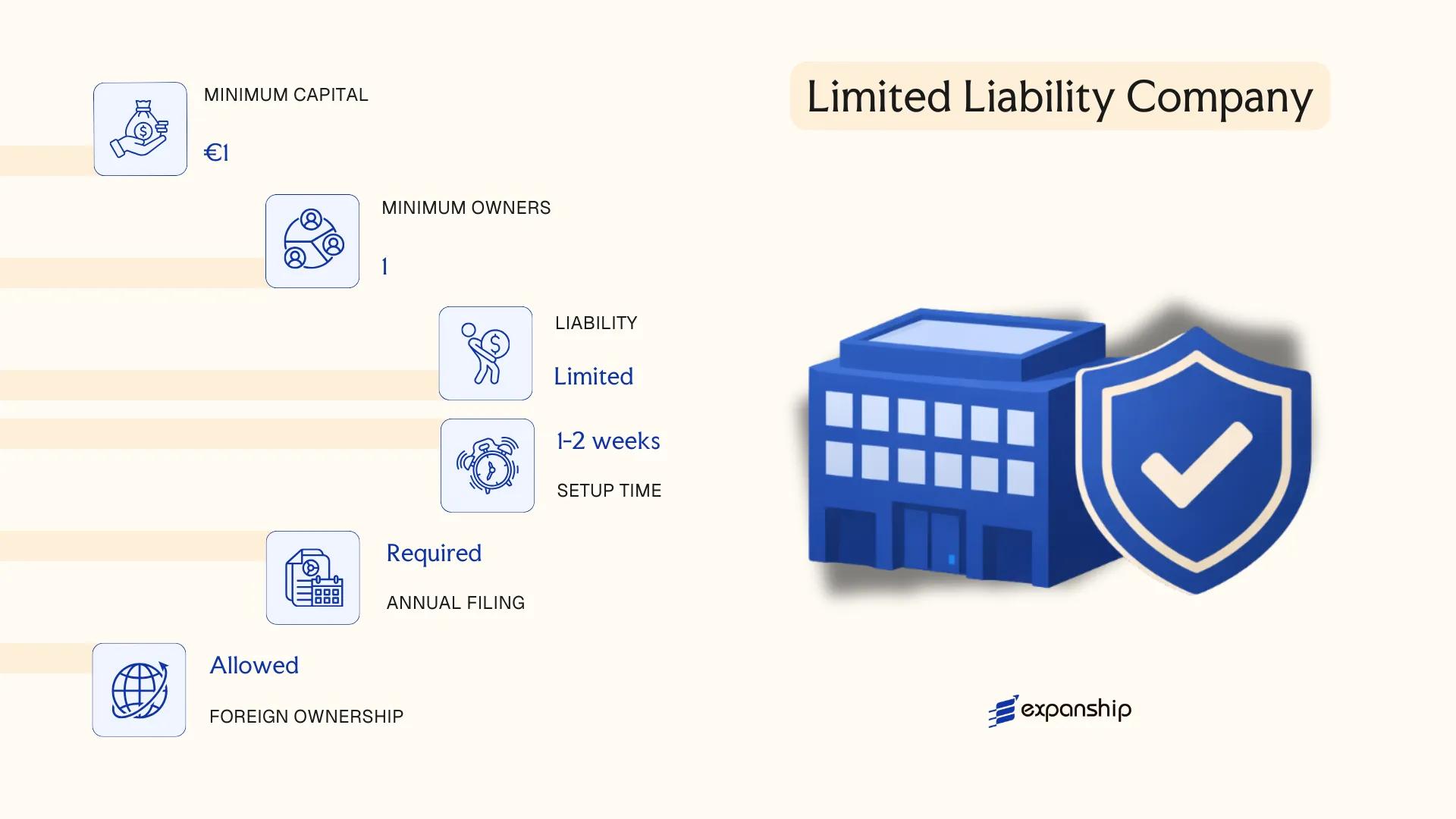

Società a Responsabilità Limitata (S.r.l.) — Limited Liability Company

The San Marino Srl limited liability company is governed by Law No. 47 of 1999, as subsequently amended, which establishes its status as a distinct legal entity separate from its members. Liability is capped at each member's capital contribution, and the structure sits between a partnership and a joint stock company in terms of governance flexibility.

Società a Responsabilità Limitata San Marino is the preferred vehicle for small to medium-sized businesses and closely held ventures due to its relatively accessible capital threshold and simplified internal governance compared to the S.p.A.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Società a Responsabilità Limitata (S.r.l.) | Separate legal personality; hybrid structure |

| Members | Referred to as "soci" (members/quotaholders); minimum 1, no statutory maximum | Single-member S.r.l. is permitted |

| Management | Administered by one or more directors ("amministratori") | Directors need not be members |

| Local Presence | Registered office in San Marino required | No mandatory resident director under general rules, but a local registered address is obligatory |

| Capital | Minimum share capital of €25,500, fully subscribed at formation; divided into quotas, not shares | Quotas are not freely transferable without member consent |

| Privacy | Members' details filed with the Ufficio Registro Società; not fully public but accessible to authorities | Beneficial ownership disclosure obligations apply |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate applicable to San Marino resident entities; IGR (Imposta Generale sui Redditi) applies to profits; no VAT in the conventional sense, though an import tax regime exists; withholding taxes may apply to distributions depending on member residency.

- Annual Compliance: Annual financial statements must be filed with the Ufficio Registro Società; statutory audit requirements depend on company size thresholds.

- Economic Substance: No formalised economic substance regime equivalent to certain offshore jurisdictions, but genuine operational presence is expected for tax residency purposes.

- Treaty Access: San Marino has concluded a limited number of double taxation agreements; treaty eligibility depends on the entity's tax residency status and the counterparty jurisdiction.

- Quota Transfer Restrictions: Unlike shares in an S.p.A., quota transfers require member consent and notarial formality, limiting liquidity.

Closing

The S.r.l. suits trading operations, holding structures, and IP ownership arrangements where governance flexibility and capped liability are priorities; its primary limitation is the restricted transferability of quotas, which makes it less suited to businesses anticipating frequent ownership changes or external investment rounds.

This entity type is best suited for entrepreneurs and closely held businesses seeking limited liability with straightforward internal governance and no requirement for a publicly traded capital structure.

Partnerships in San Marino [Società in Nome Collettivo (S.n.c.), Società in Accomandita Semplice (S.a.s.)]

San Marino partnership company types are governed primarily by the Sammarinese Civil Code and the broader framework established under corporate legislation administered through the Ufficio Registro delle Società (Company Registry). Unlike capital-based structures, partnerships here do not carry separate legal personality in the same manner as a corporation — personal liability exposure varies by form.

Two principal partnership structures exist. The Società in Nome Collettivo (S.n.c.) is a general partnership where all partners bear unlimited, joint, and several liability for the firm's obligations. The Società in Accomandita Semplice (S.a.s.) introduces a two-tier membership structure, separating general partners who hold unlimited liability from limited partners whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | S.n.c. (General Partnership) | S.a.s. (Limited Partnership) |

|---|---|---|

| Legal Form | Partnership without separate legal personality | Hybrid partnership with tiered liability |

| Members | Partners (soci); minimum 2, no statutory maximum | General partners (soci accomandatari) + limited partners (soci accomandanti); minimum 1 of each |

| Liability | Unlimited, joint and several for all partners | Unlimited for general partners; capped at contribution for limited partners |

| Capital | No statutory minimum; contributions may be cash or in-kind | No statutory minimum; limited partners liable only to the extent of their subscribed share |

| Local Presence | Registered office in San Marino required | Registered office in San Marino required |

| Management | All partners entitled to manage unless restricted by deed | Only general partners may manage; limited partners are excluded from management |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent; profits flow through to partners and are taxed at the individual level under the Imposta Generale sui Redditi (IGR), with no separate entity-level corporate tax applied. VAT and other indirect taxes apply to trading activities.

- Annual Compliance: Partnerships must file annual accounts with the Company Registry and maintain updated partnership records reflecting any changes to membership or capital contributions.

- Restrictions: Limited partners in an S.a.s. who participate in management risk losing their limited liability protection under Sammarinese law.

- Conversion: A partnership may be converted into a capital company (S.r.l. or S.p.A.) subject to unanimous partner consent and re-registration procedures.

Sub-Types

Società in Nome Collettivo (S.n.c.)

The S.n.c. is the base general partnership form where management rights and liability are distributed equally among partners unless the deed of partnership specifies otherwise. It suits small, closely held professional or trading ventures where all participants are actively involved.

Società in Accomandita Semplice (S.a.s.)

The S.a.s. allows passive investors to participate in a business without assuming unlimited liability, provided they abstain from management. This structure is used where a capital contributor wishes to invest alongside an active managing partner.

Closing

Both forms are suited to small-scale trading, family businesses, or professional service arrangements where the partners know and trust one another closely. The absence of a minimum capital requirement lowers the barrier to formation, though unlimited liability for general partners remains a material structural constraint.

S.n.c. and S.a.s. structures are best suited for small, closely held businesses or family-run ventures where at least one partner is prepared to accept personal liability.

Foreign Business Presence in San Marino [Branch Office, Representative Office]

Establishing a foreign company branch office in San Marino is governed by the general corporate legislation framework, which requires foreign entities to register with the Ufficio Registro delle Imprese (Companies Register) before conducting any commercial activity. A branch office does not constitute a separate legal entity; it remains an extension of the parent company, which retains full liability for the branch's obligations.

Registration requires submission of certified constitutional documents from the parent firm, translated into Italian and authenticated. The parent entity must appoint a local representative who holds legal authority to act on its behalf before San Marino authorities.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Status | Extension of parent; no separate legal personality | Extension of parent; no separate legal personality |

| Commercial Activity | Permitted | Not permitted; limited to liaison and promotion |

| Liability | Parent bears full liability | Parent bears full liability |

| Local Representative | Mandatory | Mandatory |

| Registration | Ufficio Registro delle Imprese | Required with relevant authorities |

| Capital Requirement | None fixed; parent's capital applies | None |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard 17% rate; VAT obligations apply to taxable supplies; no separate withholding tax regime applies at branch level beyond standard rules.

- Economic Substance: The branch must maintain genuine operational activity; purely letterbox arrangements are not accepted.

- Annual Compliance: Annual accounts and activity reports must be filed with the Companies Register, reflecting the branch's local operations.

- Treaty Access: Access to San Marino's tax treaties is generally limited for branches; treaty eligibility depends on the parent's jurisdiction of residence.

- Restrictions: A representative office cannot generate revenue or enter binding commercial contracts on behalf of the parent.

Sub-Types

Branch Office

A branch conducts full commercial operations in the jurisdiction and is directly taxable on locally sourced income. It is typically used by foreign firms that require an operational footprint without incorporating a separate local entity.

Representative Office

A representative office is restricted to non-commercial activities such as market research, promotion, and liaison functions. It generates no local taxable income but must still register and comply with reporting requirements.

Closing

Both structures suit foreign businesses testing the local market or maintaining a coordination presence before committing to full incorporation. The primary advantage is avoiding the cost and complexity of establishing a new legal entity; the key limitation is that branch liability exposure rests entirely with the parent company.

Foreign companies already operating in Europe that need a registered operational or liaison presence without creating a standalone San Marino entity.

Sole Proprietorship (Ditta Individuale)

San Marino sole proprietorship registration is governed by the general commercial and civil law framework of the Republic, which draws on Law No. 47 of 1990 and subsequent regulatory acts issued by the Segreteria di Stato per l'Industria. The Ditta Individuale carries no separate legal personality — the proprietor and the business are legally one and the same, meaning personal assets remain fully exposed to business liabilities.

Registration is handled through the Ufficio Industria, Artigianato e Commercio, and the firm must also be enrolled in the San Marino Register of Companies (Registro delle Imprese). Foreign nationals seeking to operate as sole traders must satisfy specific residency and economic activity requirements before obtaining authorisation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Ditta Individuale) | No separate legal personality |

| Member Type | Sole Proprietor | Single individual only; no co-owners permitted |

| Local Presence | Registered business address in San Marino | Physical operational presence expected |

| Capital | No statutory minimum | Personal funds used directly |

| Liability | Unlimited personal liability | Proprietor's personal assets are at risk |

| Privacy | Owner's details recorded in public register | Limited privacy protection |

Focus Points

- Taxation: Subject to personal income tax (IGR) on net business profit; VAT registration required if turnover exceeds the applicable threshold; no corporate tax applies.

- Annual Compliance: Annual income declaration and accounting records must be submitted to the San Marino tax authority (Ufficio Tributario).

- Treaty Access: The Ditta Individuale generally does not benefit from tax treaty provisions structured for corporate entities.

- Conversion: The structure can be converted into a corporate form such as an S.r.l., though this requires a formal restructuring process.

- Restrictions: Non-residents face significant barriers to operating as sole traders; sector-specific licences may apply to regulated activities.

Closing Paragraph

The Ditta Individuale suits individuals conducting small-scale trade, artisan work, or professional services within the territory, where low setup cost is an advantage. The principal drawback is unlimited personal liability, which creates meaningful financial exposure as business activity grows.

Best suited for resident individuals or qualifying self-employed persons operating low-risk, small-scale businesses with limited external obligations.

How to Choose the Right Entity Type in San Marino

Selecting how to choose your company type in San Marino requires more than comparing registration fees — the structure you register has direct legal, tax, and operational consequences that are difficult to reverse.

Why Your Entity Choice Matters

Registering under the wrong structure creates concrete, measurable problems:

- Selecting a structure without treaty access means you cannot claim withholding tax reductions in counterpart countries under San Marino's bilateral agreements.

- Forming a joint stock company when a single-person consultancy is your actual model adds mandatory audit and governance obligations that do not apply to a Ditta Individuale or smaller S.r.l.

- Choosing an entity that cannot demonstrate local substance when substance requirements apply triggers reporting failures and potential administrative penalties under San Marino's fiscal framework.

- Using a structure intended for active trading when your purpose is passive asset holding may conflict with the conditions under which the entity was registered with the Ufficio Registro Società.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point toward a different legal form under San Marino company law.

- Ownership Structure: Single-founder businesses have different governance options than multi-party ventures requiring a formal board.

- Tax Objectives: Your need for treaty eligibility, a specific tax regime, or full exemption will narrow the viable structures considerably.

- Substance Capacity: If maintaining a local office and resident management is not feasible, the chosen entity must align with applicable substance thresholds.

- Exit Strategy: Not all San Marino entities permit redomiciliation or conversion — verify this before incorporating.

- Privacy Requirements: Public register disclosure rules vary by entity type; nominee arrangements may be required to achieve confidentiality.

Compliance Services for Companies in San Marino

Maintain good standing with San Marino's regulatory requirements, from annual filings to ongoing corporate governance obligations.

Conclusion

Incorporating a company in San Marino means selecting from a defined set of structures, each governed by the Civil Code of the Republic and supervised by the Registro delle Imprese. The S.p.A. suits larger enterprises requiring capital markets access; the S.r.l. remains the most commonly registered entity, favored by small and medium businesses for its manageable capital requirements and limited liability. Partnerships such as the S.n.c. and S.a.s. serve closely held ventures where personal liability is acceptable, while the Ditta Individuale fits single operators. Branch offices address foreign firms testing the market without separate incorporation.

San Marino's continued expansion of its double taxation agreement network and its OECD-aligned transparency commitments suggest a regulatory environment moving toward greater international recognition. For businesses evaluating this jurisdiction, understanding which structure aligns with your operational and ownership requirements is the necessary first step before engaging with local formation procedures.

How Expanship Can Assist You

Expanship provides San Marino company formation services covering every major entity type available under Sammarinese law, from the S.p.A. and S.r.l. to partnerships and sole proprietorships. Our team works directly with the Ufficio Registro delle Società e dell'Economia to handle filings accurately and on schedule. If your business requires a branch or representative office, we manage that registration process as well.

Across our San Marino business setup assistance, we handle each stage of the process for you:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and liaison with the relevant registry

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to our team through Expanship San Marino to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Società a Responsabilità Limitata (S.r.l.) is the most frequently registered entity, primarily because its lower minimum capital requirement and flexible governance structure make it accessible to small and mid-sized businesses. It suits both domestic operators and foreign investors who intend to conduct active commercial operations.

The S.p.A. requires higher minimum share capital and is subject to more rigorous disclosure and governance obligations, making it suited to larger enterprises or those seeking external investment. An S.r.l. operates under a comparatively lighter compliance regime. Both structures are subject to corporate income tax under domestic law, with no inherent tax distinction between them.

Among registered entity types, the S.r.l. generally involves less extensive public disclosure than the S.p.A., particularly regarding shareholder composition. Nominee arrangements are not a formally standardized feature of San Marino corporate law, though legal representation structures can be arranged through qualified professionals.

A sole founder can incorporate an S.r.l. or S.p.A. as a single-member entity. Partnerships — both the Società in Nome Collettivo (S.n.c.) and Società in Accomandita Semplice (S.a.s.) — require at least two partners by definition, as the structure is contractual in nature.

Foreign nationals may establish an S.r.l. or S.p.A. without a residency requirement, provided they comply with the registration procedures administered by the San Marino Companies Register (Registro delle Imprese). In practice, engaging a local registered agent or legal representative is standard, particularly for non-Italian-speaking founders managing documentation requirements.

San Marino corporate law permits transformation between entity types, most commonly from an S.r.l. to an S.p.A. as a business scales. The process requires compliance with applicable capital requirements and formal approval procedures; conversion between partnership forms and limited liability structures is more complex and subject to creditor protection provisions.

The S.r.l., S.p.A., and S.a.s. each hold separate legal personality distinct from their members. The S.n.c. does not confer the same liability separation; partners in a general partnership remain personally and jointly liable for the firm's obligations, which distinguishes it materially from the limited liability structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.