Key Takeaways

- Serbia's Companies Act (Zakon o privrednim društvima) provides for five principal entity forms — the AD, DOO, Ortačko Društvo, Komanditno Društvo, and Preduzetnik — each carrying distinct liability, capital, and governance requirements.

- The Društvo sa Ograničenom Odgovornošću (DOO) is the dominant vehicle for new registrations in Serbia, offering founders limited liability without the obligation to issue publicly traded shares.

- All company formations and registration changes in Serbia are processed through the Serbian Business Registers Agency (SBRA), which has progressively digitized its procedures.

- Foreign entities seeking a presence in Serbia must choose between a Branch Office, which permits direct commercial operations, and a Representative Office, which is restricted to non-commercial activity only.

Introduction to Entity Types in Serbia

Serbia is a landlocked country in Central Europe, bordered by Hungary, Romania, Bulgaria, North Macedonia, Croatia, Bosnia and Herzegovina, and Montenegro. It is an independent republic and a candidate country for European Union accession. Companies are registered through the Serbian Business Registers Agency (SBRA), the central authority responsible for company formation, registration changes, and maintaining official corporate records.

From a tax standpoint, Serbia operates a standard territorial-based system with a flat corporate income tax rate, supplemented by a growing network of double taxation treaties.

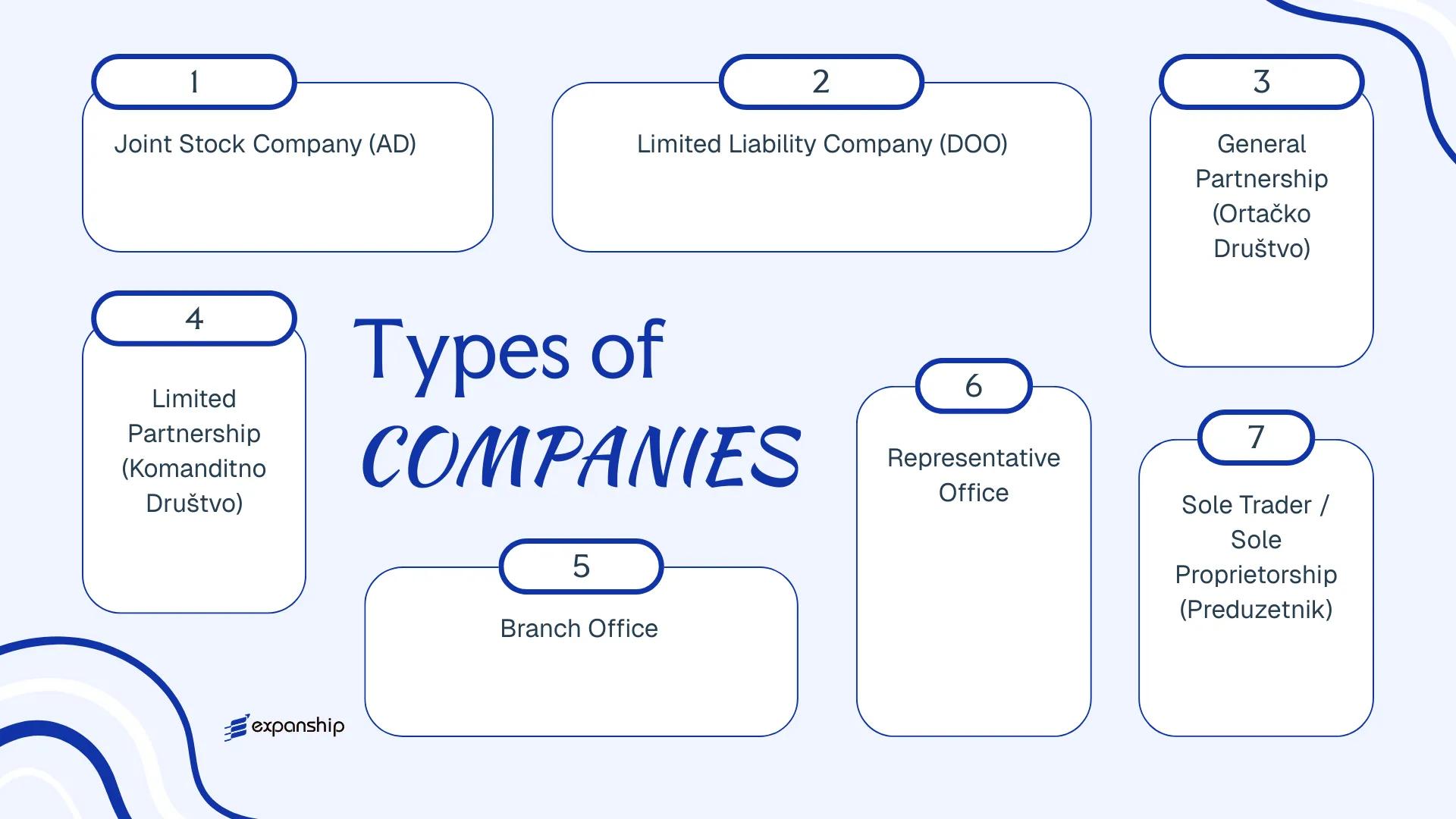

Several legal entity types are available to investors and entrepreneurs under the Companies Act (Zakon o privrednim društvima): the Akcionarsko Društvo (AD), the Društvo sa Ograničenom Odgovornošću (DOO), the Ortačko Društvo, the Komanditno Društvo, foreign branch offices, representative offices, and the Preduzetnik structure for sole traders.

Each of these structures carries distinct requirements around capital, liability, governance, and ongoing compliance. This article examines each form in detail to help you determine which suits your business objectives.

An Overview of Business Structures in Serbia

Serbian company law recognises six distinct business structures, all governed primarily by the Law on Companies (Zakon o privrednim društvima, Official Gazette of RS No. 36/2011, with subsequent amendments). Sole traders operating as Preduzetnik fall under the Law on Trade Companies and related registration provisions. Each structure carries a different liability profile, ownership model, and operational scope.

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Akcionarsko Društvo (AD) | Joint Stock Company | Limited to share capital | Taxable | Permitted | 1 shareholder | Serbian Business Registers Agency (APR) | Law on Companies |

| Društvo sa Ograničenom Odgovornošću (DOO) | Limited Liability Company | Limited to capital contribution | Taxable | Permitted | 1 member | APR | Law on Companies |

| Ortačko Društvo (OD) | General Partnership | Unlimited, joint and several | Taxable | Permitted | 2 partners | APR | Law on Companies |

| Komanditno Društvo (KD) | Limited Partnership | Mixed: general/limited | Taxable | Permitted | 2 partners | APR | Law on Companies |

| Branch Office | Branch of foreign entity | Parent bears full liability | Taxable | Permitted | 1 foreign parent | APR | Law on Companies |

| Representative Office | Non-trading presence | Parent bears full liability | Exempt from CIT | Not permitted | 1 foreign parent | APR | Law on Companies |

| Preduzetnik | Sole Proprietorship | Unlimited personal liability | Taxable | Permitted | 1 individual | APR | Law on Trade Companies |

Each of these structures is examined in full in the sections below.

Akcionarsko Društvo (AD) – Joint Stock Company

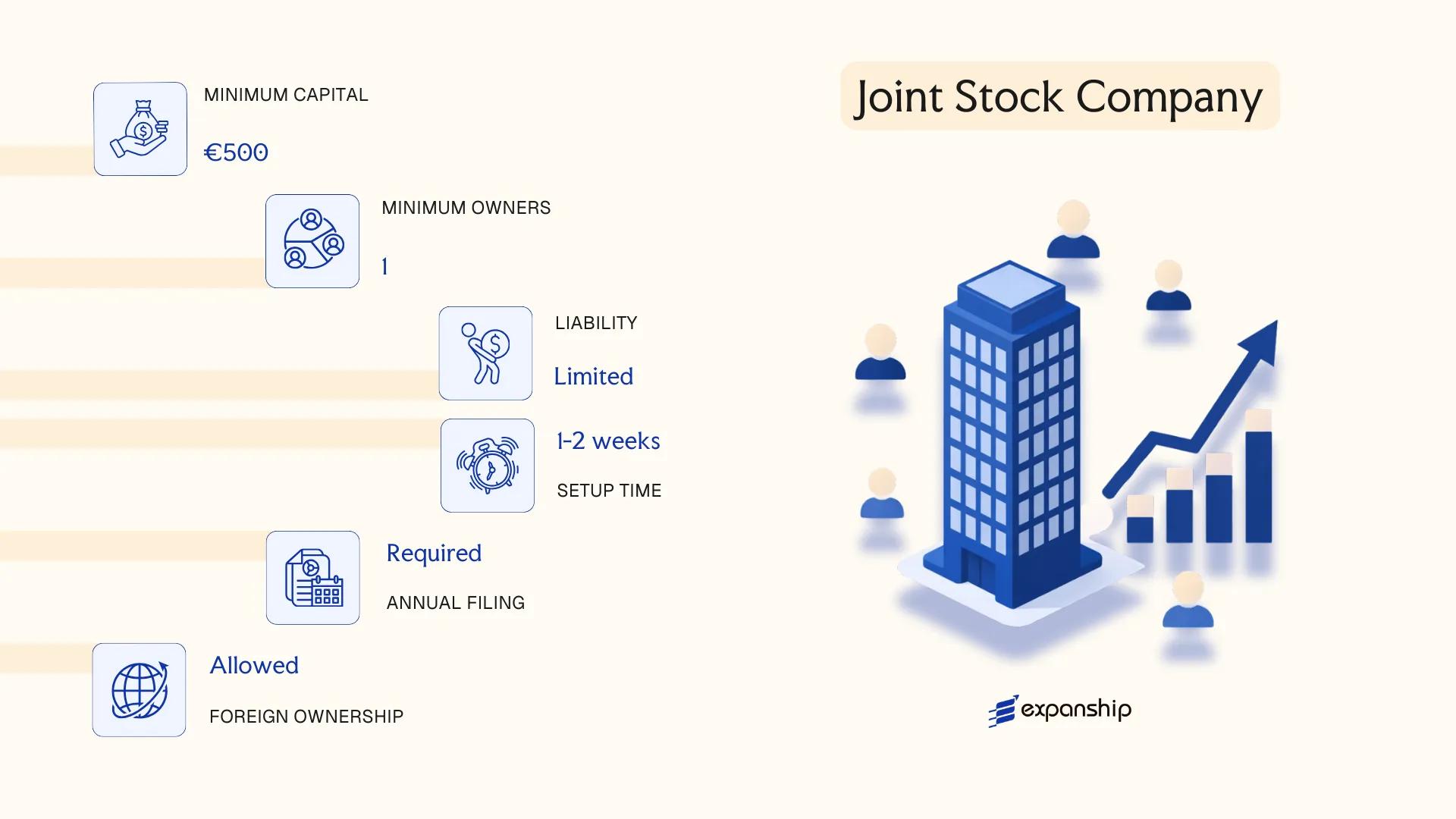

The Akcionarsko Društvo joint stock company Serbia is governed by the Companies Act (Zakon o privrednim društvima), adopted in 2011 and subsequently amended, which consolidates the legal framework for all commercial entities registered in the country.

An AD carries separate legal personality, meaning the company's assets and liabilities are legally distinct from those of its shareholders. Shareholder liability is limited to the value of subscribed shares, and the structure accommodates both private and public ownership of capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Akcionarsko Društvo) | Separate legal personality; governed by the 2011 Companies Act |

| Members | Shareholders (akcionari); minimum 1 | No maximum on shareholder count; shareholders elect a Board of Directors or Supervisory Board |

| Management | One-tier (Board of Directors) or two-tier (Management + Supervisory Board) | Both structures are permitted under the Companies Act |

| Capital | RSD 3,000,000 minimum (~approx. EUR 25,000) | Must be fully subscribed at incorporation; at least 50% paid up on registration |

| Local Presence | Registered office address in Serbia required | No mandatory local director, but a registered address with the Serbian Business Registers Agency (APR) is obligatory |

| Privacy | Shareholder register is maintained; publicly listed ADs disclose more | Privately held ADs have reduced public disclosure obligations compared to listed entities |

Focus Points

- Taxation: Corporate profit tax is levied at 15%; VAT applies at 20% (standard) or 10% (reduced); withholding tax on dividends paid to non-residents is generally 25%, reduced under applicable double taxation treaties.

- Annual Compliance: Mandatory submission of audited financial statements to the APR; publicly listed ADs are additionally subject to Securities Commission (Komisija za hartije od vrednosti) reporting requirements.

- Treaty Access: Serbia maintains an extensive network of double taxation agreements, making the AD eligible for reduced withholding rates on dividends, interest, and royalties.

- Conversion: An AD may be converted into a DOO or another permitted entity form under the Companies Act, subject to regulatory approval and creditor notification procedures.

- Share Transferability: Shares in a privately held AD may be subject to transfer restrictions set out in the Articles of Association; shares in a listed AD are freely transferable on the Belgrade Stock Exchange.

Sub-Types

Zatvoreno Akcionarsko Društvo – Closed Joint Stock Company

Shares are not offered to the public and cannot be freely traded on a regulated market. This structure is typically used by larger family-owned businesses or investor groups that require a share-based capital structure without public market obligations.

Otvoreno Akcionarsko Društvo – Open Joint Stock Company

Shares may be offered to the public and listed on the Belgrade Stock Exchange. This sub-type is subject to additional regulatory oversight by the Securities Commission and stricter ongoing disclosure requirements.

When to Use an AD

The AD structure suits capital-intensive businesses, entities seeking institutional investment, and companies planning a public listing. Its main advantage is the ability to raise equity capital across an unrestricted number of shareholders. The principal drawback is administrative burden — mandatory audit requirements, more complex governance obligations, and higher minimum capital thresholds make it a heavier structure to maintain than a DOO.

Best suited for large enterprises, joint ventures with institutional investors, or businesses with a clear path toward a public equity offering on the Belgrade Stock Exchange.

Company Incorporation in Serbia

Expanship assists with end-to-end AD registration through the Serbian Business Registers Agency, including capital structuring and governance setup.

Društvo sa Ograničenom Odgovornošću (DOO) – Limited Liability Company

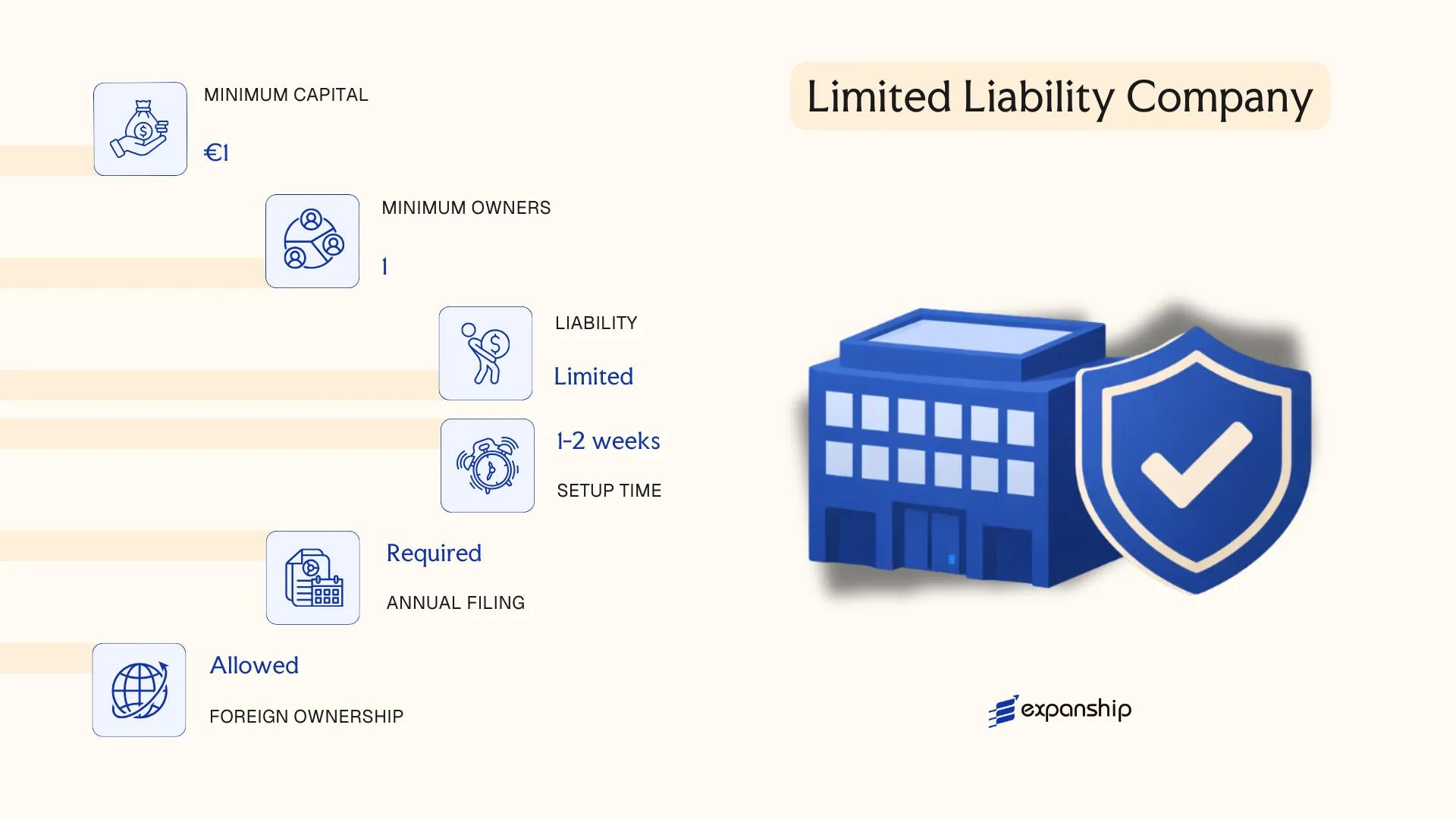

The DOO limited liability company Serbia is the most widely registered business structure in the country, governed by the Law on Companies (Zakon o privrednim društvima, 2011, as amended). It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its members. Liability is confined to the amount of each member's capital contribution.

As a hybrid structure, the DOO combines the contractual flexibility of a partnership with the liability protection associated with a corporation. Registration is handled through the Serbian Business Registers Agency (APR), which also maintains the Central Registry of Beneficial Owners for mandatory UBO disclosure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Separate legal personality; governed by the 2011 Law on Companies |

| Members | 1–50 members | Members hold ownership stakes called poslovni udeli (business shares) |

| Management | One or more directors (direktori) | Directors may be foreign nationals; a supervisory board is optional |

| Registered Office | Physical address in Serbia required | Cannot use a PO Box; registered seat must be maintained with APR |

| Minimum Capital | RSD 100 (approx. EUR 1) | No mandatory paid-up requirement before registration; contribution schedules are permitted |

| Privacy | Director names publicly filed; UBO register mandatory | Beneficial owners registered with APR; some information is publicly accessible |

Focus Points

- Taxation: Subject to 15% corporate income tax; standard VAT rate of 20% applies once turnover exceeds the RSD 8 million threshold; withholding tax on dividends paid to non-residents is generally 25% (reducible under applicable double tax treaties).

- Annual Compliance: Mandatory annual financial statements filed with APR; statutory audit required if the entity meets two of three prescribed size criteria under the Law on Accounting.

- Treaty Access: As a resident entity, the DOO qualifies for Serbia's network of over 60 bilateral double tax treaties, subject to substance and beneficial ownership requirements.

- Conversion: A DOO may convert into a joint-stock company (AD) through a prescribed restructuring procedure under the Law on Companies without dissolving the entity.

- Restrictions: Member count is capped at 50; exceeding this threshold triggers an obligation to convert to an AD.

Closing

The DOO suits trading operations, holding structures, and market-entry vehicles where full liability protection and operational flexibility are both required. Its low capital threshold lowers the cost of formation, though the 50-member cap limits its suitability for businesses anticipating broad investor participation.

The DOO is best suited for small to mid-sized foreign-owned businesses, family enterprises, and single-shareholder subsidiaries seeking a straightforward corporate presence with full liability protection.

Partnerships in Serbia [Ortačko Društvo (General Partnership), Komanditno Društvo (Limited Partnership)]

Both partnership company types in Serbia are governed by the Law on Companies (Zakon o privrednim društvima), enacted in 2011 and subsequently amended. Unlike a DOO or AD, partnerships in Serbia are less commonly used in commercial practice but remain available as legally recognised structures under Serbian company law.

Registered with the Serbian Business Registers Agency (APR), each partnership type carries distinct liability implications for its members.

Key Characteristics

| Requirement | Ortačko Društvo (General Partnership) | Komanditno Društvo (Limited Partnership) |

|---|---|---|

| Legal Form | Separate legal entity | Separate legal entity |

| Members | Partners (min. 2, no maximum) | General partners (min. 1) + Limited partners (min. 1) |

| Liability | Unlimited personal liability for all partners | General partners: unlimited; Limited partners: capped at contribution |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered address in Serbia required | Registered address in Serbia required |

| Privacy | Partner details disclosed in APR register | All partner details disclosed publicly |

Focus Points

- Taxation: Partnerships are generally subject to corporate income tax at 15%; partners may also face personal income tax on distributions, and standard VAT rules apply upon registration threshold being met.

- Annual Compliance: Financial statements must be filed annually with the APR; bookkeeping obligations apply regardless of activity level.

- Conversion: A partnership may be converted into another company form, including a DOO, in accordance with the Law on Companies.

- Restrictions: General partners cannot limit their liability through the partnership agreement; this is fixed by statute.

- Treaty Access: As Serbian-registered entities, partnerships can access Serbia's network of double tax treaties, though treaty application depends on the specific arrangement and counterparty jurisdiction.

Sub-Types

Ortačko Društvo (General Partnership)

All partners bear joint and unlimited liability for the firm's obligations. This structure suits small groups of professionals or family-run operations where members accept full personal exposure.

Komanditno Društvo (Limited Partnership)

At least one general partner retains unlimited liability, while limited partners are liable only up to their agreed capital contribution. The limited partner role is purely passive; participating in management converts that partner's status to general partner under Serbian law.

When to Use a Partnership Structure

Partnerships in Serbia are most suited to small professional practices or tightly held family businesses where the members have a high degree of mutual trust. The absence of a minimum capital requirement lowers the barrier to formation, though unlimited liability for general partners remains a significant structural constraint for commercially active businesses.

These structures are best suited to small professional groups or family enterprises where all partners are actively involved and accept personal liability.

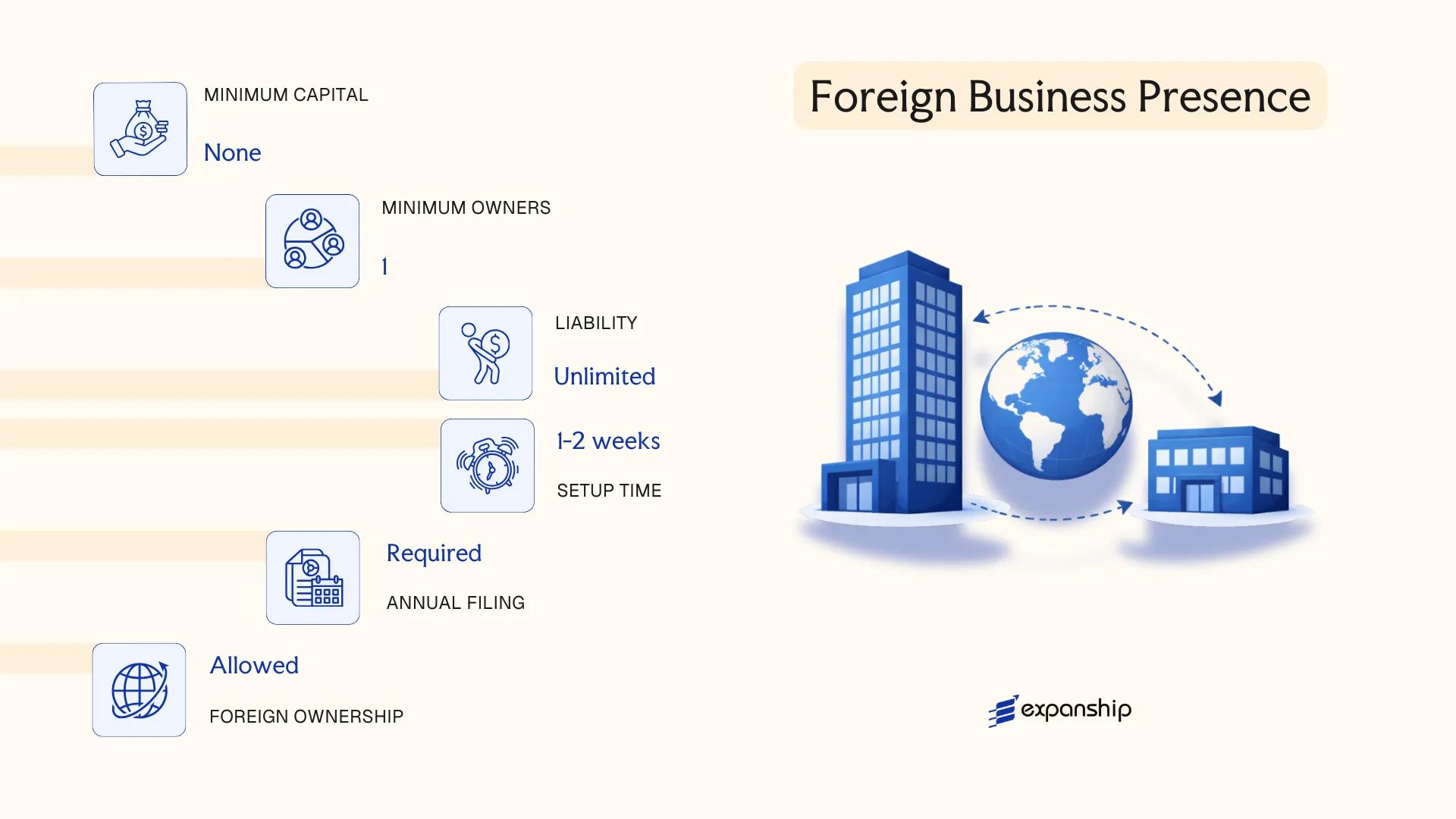

Foreign Business Presence in Serbia [Branch Office, Representative Office]

Foreign entities seeking to operate in Serbia without incorporating a local company have two structural options: a branch office and a representative office. A foreign company branch office in Serbia is governed by the Law on Companies (Zakon o privrednim društvima, 2011, as amended), with registration handled by the Serbian Business Registers Agency (APR).

Neither structure constitutes a separate legal entity. Both remain extensions of the parent company, which bears full liability for their obligations.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Full commercial activity (sales, contracts, invoicing) | Limited to market research, promotion, liaison only |

| Members / Management | Appointed manager (attorney-in-fact); no board required | Appointed manager; same structure as branch |

| Local Presence | Registered address in Serbia; registered with APR | Registered address in Serbia; registered with APR |

| Capital Requirement | None prescribed by law | None prescribed by law |

| Privacy | Parent company details disclosed in APR register | Parent company details disclosed in APR register |

Focus Points

- Taxation: Branch offices are subject to 15% corporate income tax on Serbia-sourced profits; VAT registration is required if turnover exceeds the statutory threshold (RSD 8,000,000); withholding tax applies to profit remittances to the parent at 20% unless reduced by a double tax treaty. Representative offices are not subject to corporate tax as they generate no revenue.

- Treaty Access: Serbia maintains an extensive double tax treaty network; branch offices may access treaty benefits, subject to the competent authority's determination on permanent establishment status.

- Economic Substance: A branch conducting commercial operations will generally constitute a permanent establishment under Serbian tax law, triggering full local tax obligations.

- Annual Compliance: Both structures must file annual financial statements with APR; branches additionally file corporate tax returns with the Tax Administration of Serbia.

- Restrictions: Representative offices are legally prohibited from generating income or signing commercial contracts in their own name.

Sub-Types

No formally recognised sub-classifications exist for branch or representative offices under Serbian company law.

Closing

A branch office suits foreign firms requiring operational presence and direct revenue generation, though the parent's unlimited liability exposure is a material consideration. Representative offices work for market-entry research or pre-commercial activity, but their inability to conduct business transactions limits their practical utility beyond an exploratory phase.

A branch office is best suited for established foreign companies testing the Serbian market commercially before committing to a locally incorporated entity.

Preduzetnik – Sole Trader / Sole Proprietorship

Preduzetnik sole trader registration Serbia is governed by the Law on Business Companies (Zakon o privrednim društvima, 2011) alongside the Law on Registration Procedure (Zakon o postupku registracije u Agenciji za privredne registre, 2004). Unlike corporate forms, a Preduzetnik does not constitute a separate legal entity — the individual and the business are treated as one, meaning the proprietor bears unlimited personal liability for all business obligations.

Registration is completed through the Serbian Business Registers Agency (APR), with the process typically finalised within a few business days upon submission of required documentation. Your personal assets remain exposed to creditors, as no liability separation exists between you and the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trade | No separate legal personality; proprietor and business are legally unified |

| Member Designation | Proprietor | Single natural person only; cannot be a legal entity |

| Membership | 1 proprietor (maximum 1) | No partners or shareholders permitted |

| Local Presence | Registered business address in Serbia | Physical presence required; APR registration address must be active |

| Capital Requirement | None | No minimum capital threshold under applicable law |

| Privacy | Proprietor's name and address publicly registered with APR | Full public disclosure via the APR register |

Focus Points

- Taxation: Subject to personal income tax rather than corporate income tax; VAT registration is mandatory once annual turnover exceeds the prescribed threshold (currently RSD 8,000,000); no withholding tax applies on profits drawn by the proprietor.

- Flat-Rate Taxation (Paušalno oporezivanje): Qualifying Preduzetnici may elect lump-sum taxation (paušalni porez), where tax liability is assessed on a deemed income basis rather than actual profit.

- Social Contributions: Mandatory pension, disability, and health insurance contributions apply regardless of profit; the proprietor is treated as self-employed for social security purposes.

- Annual Compliance: Annual financial statements must be submitted to APR; tax returns are filed with the Tax Administration of Serbia (Poreska uprava).

- Conversion: A Preduzetnik may convert into a DOO under the Law on Business Companies, with business continuity and asset transfer provisions available during conversion.

Closing

A Preduzetnik suits freelancers, tradespeople, and individual service providers operating domestically, offering minimal administrative overhead but no liability protection. The absence of a capital requirement and the straightforward APR registration make entry accessible, though unlimited personal liability represents a significant structural constraint for any activity carrying financial or legal risk.

A Preduzetnik is most appropriate for individual professionals or sole operators conducting low-risk, domestic business activity who do not require liability separation.

How to Choose the Right Entity Type in Serbia

Knowing how to choose a company type in Serbia before registering prevents structural problems that are far more costly to fix after the fact.

Why Your Entity Choice Matters

The legal form you register under has binding consequences from day one:

- Registering as a representative office while conducting commercial transactions violates the restrictions placed on that form under the Law on Companies, which can result in the Serbian Business Registers Agency (APR) initiating deregistration proceedings.

- Selecting a Preduzetnik structure when your business expands to multiple shareholders forces a full conversion process, since sole trader status cannot accommodate more than one owner.

- Choosing a DOO when your activity requires an AD — such as participation in certain regulated sectors including public share offerings — leaves your firm non-compliant with sector-specific licensing requirements.

- Forming an AD when your business is a small consultancy imposes mandatory statutory audit obligations and a two-tier governance structure, adding administrative costs disproportionate to your operational scale.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sector operations each correspond to distinct legal forms under the Law on Companies.

- Ownership Structure: A single founder can use a DOO or Preduzetnik, but multi-party ownership with transferable shares requires an AD.

- Liability Exposure: Your tolerance for personal liability determines whether a limited liability form or a partnership structure is appropriate for your situation.

- Tax Position: Access to Serbia's double tax treaty network requires resident entity status, which a representative office does not provide.

- Governance Requirements: If your investors or counterparties require a board of directors and audited accounts, an AD is the only form that satisfies those expectations by default.

- Exit and Conversion: Not all Serbian entity types permit straightforward conversion; planning your exit route in advance avoids procedural deadlocks at the APR.

Compliance Services for Companies in Serbia

Ongoing compliance support for Serbian entities, including statutory filings, APR reporting obligations, and annual account submissions.

Conclusion

Each entity structure registered under Serbian law serves a distinct purpose. The DOO dominates new registrations and suits founders who want limited liability without public share issuance. An AD fits businesses planning capital market activity or institutional investment. Partnerships carry unlimited personal liability and are chosen far less frequently. The Branch Office gives a foreign parent direct operational presence, while a Representative Office is confined to non-commercial activity. The Preduzetnik remains the starting point for sole operators, though it offers no liability separation from the individual.

As a setting up a company in Serbia guide, this overview reflects a regulatory environment that has continued to modernize through alignment with EU standards and expansion of its double tax treaty network. Registration is processed through the Serbian Business Registers Agency (SBRA), which has progressively digitized its procedures. For your business, the right structure depends on ownership plans, liability tolerance, and the nature of planned activity in the market.

How Expanship Can Assist You

Expanship provides corporate services Serbia businesses and international clients rely on when forming and maintaining a legal presence under Serbian jurisdiction. From registering a Društvo sa Ograničenom Odgovornošću (DOO) to establishing a branch office, every step involves filing with the Serbian Business Registers Agency (SBRA) and meeting obligations under the Companies Act. Our team manages that process directly on your behalf.

Across the full formation and post-incorporation cycle, Expanship's Serbia incorporation services cover:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered address provision

- SBRA filing and government authority liaison

- Tax and statistical registration coordination

- Ongoing compliance and annual reporting support

- Banking introduction assistance for your Serbian entity

Reach out to our team through the Expanship Serbia contact page to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Društvo sa Ograničenom Odgovornošću (DOO) is the most frequently registered structure. Its minimal share capital requirement of 100 RSD and single-member eligibility make it the default choice for small to mid-sized businesses and foreign-owned ventures alike.

A Branch Office has no separate legal personality and its parent company bears full liability for its obligations. A DOO is a distinct legal entity, subject to Serbian corporate income tax on locally generated profit, and carries its own compliance obligations under the Companies Act (Zakon o privrednim društvima).

The DOO does not require public disclosure of beneficial ownership beyond registration with the Agencija za privredne registre (APR). Nominee arrangements are legally permissible, though ultimate beneficial owners must still be reported to the Central Register of Beneficial Owners under AML legislation.

A Preduzetnik, DOO, and Akcionarsko Društvo (AD) can each be formed by one individual. Ortačko Društvo and Komanditno Društvo require a minimum of two partners by statutory definition.

All entity types under the Companies Act are accessible to foreign nationals without residency requirements. A non-resident can serve as sole founder and director of a DOO or AD, though a local registered address remains mandatory for APR registration purposes.

Serbian law permits status changes between entity types, including conversion of a DOO into an AD and vice versa. The process requires a formal decision by the founding assembly, revised incorporation documents, and re-registration with the APR.

The DOO, AD, Ortačko Društvo, and Komanditno Društvo all hold separate legal personality under the Companies Act. A Representative Office and a Preduzetnik do not — the Preduzetnik's founder bears unlimited personal liability, and the Representative Office acts solely as an extension of its foreign parent.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.