Key Takeaways

- Under the Puerto Rico General Corporation Act, every corporation formed on the island must maintain a registered agent with a physical address in Puerto Rico, and failure to do so places the entity at risk of losing good standing.

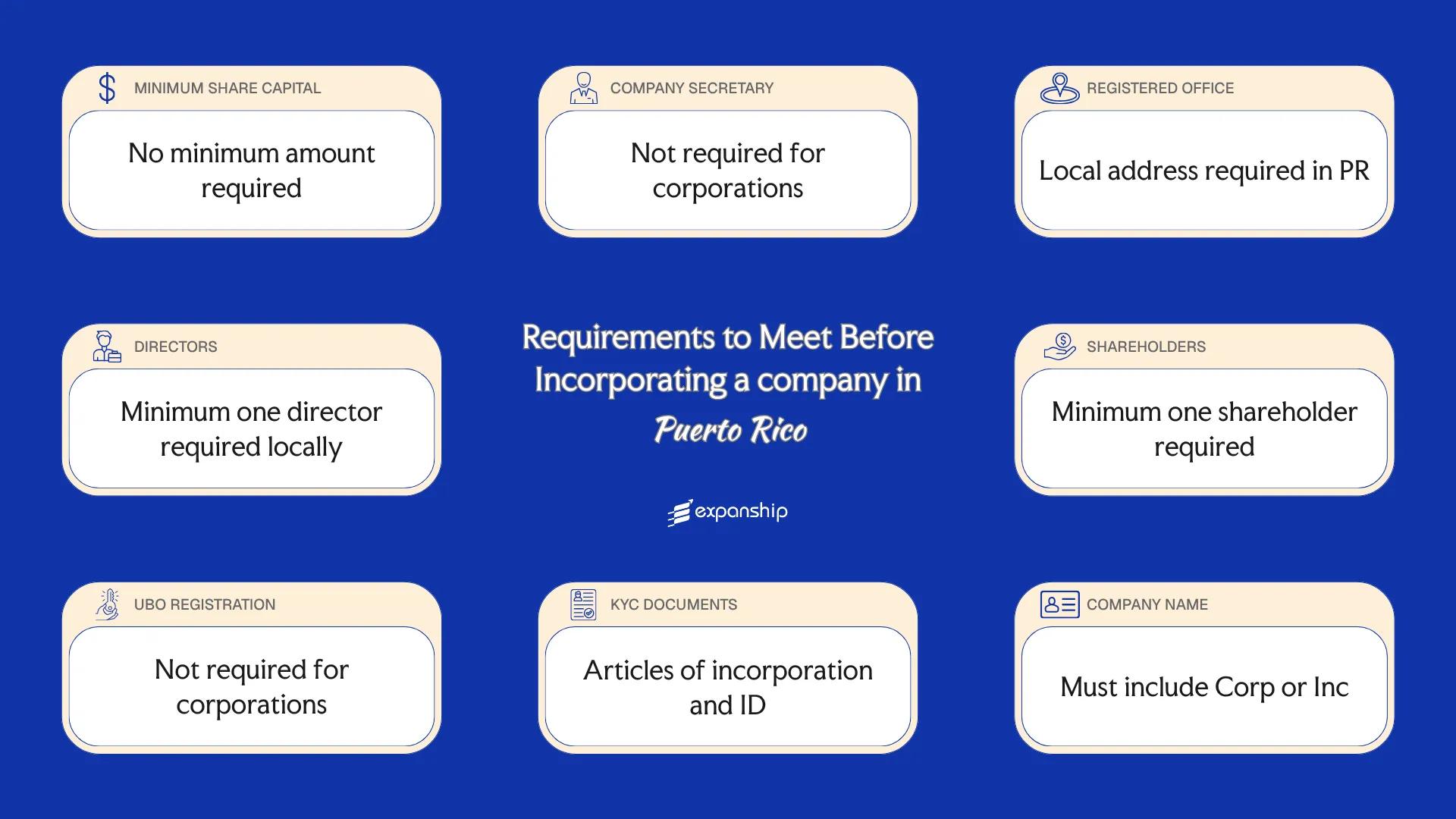

- No minimum share capital threshold applies to corporations incorporated in Puerto Rico, though the formation structure must still comply with the statutory requirements administered by the Puerto Rico Department of State.

- Directors and shareholders of a Puerto Rico corporation are not required to be residents or nationals, making the jurisdiction accessible to foreign investors without local ownership or management mandates.

- Beneficial ownership disclosure obligations applicable to Puerto Rico entities derive from federal requirements rather than the local corporate statute, adding a compliance layer that sits outside the General Corporation Act framework.

Incorporation requirements in Puerto Rico are governed by the Puerto Rico General Corporation Act, administered through the Puerto Rico Department of State, which serves as the primary registry for business entity formation on the island. This article covers the structural, documentary, and compliance requirements applicable to entities seeking formal registration.

Failure to satisfy these requirements results in rejection of the formation filing or, where an entity is already operating, exposure to administrative penalties and loss of good standing. Requirements differ across entity types, and certain industries face additional regulatory oversight beyond the standard formation process.

The General Corporation Act sets out the foundational obligations that apply to most business structures formed under Puerto Rican law. This article is most relevant to foreign investors and non-resident business owners evaluating the formation of a Puerto Rico entity, including those considering operations under Act 60 incentive programs.

Minimum Share Capital Requirements in Puerto Rico

Under Puerto Rico's General Corporations Act (Act 164-2009), there are no Puerto Rico share capital requirements that impose a statutory minimum authorized or paid-up amount. Corporations formed under this Act may authorize shares with or without par value, giving incorporators flexibility in structuring the capital framework from the outset.

The Puerto Rico Department of State handles incorporation filings and does not require proof of capital deposit as a condition of registration. Share capital obligations are therefore a one-time structural decision made at incorporation, not an ongoing statutory requirement subject to annual verification.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory requirement |

| Maximum Authorized Share Capital | No statutory requirement |

| Minimum Paid-Up Capital | No statutory requirement |

| Paid-Up Requirement at Incorporation | No statutory requirement |

| Accepted Currency | United States Dollar (USD) |

| Accepted Forms of Contribution | Cash, property, or services rendered |

| Timeframe to Deposit Capital | No statutory requirement |

Even without a statutory minimum, your certificate of incorporation must specify the total number of authorized shares and, if applicable, their par value. Omitting this information will result in rejection of the filing by the Puerto Rico Department of State.

Registered Agent Requirements in Puerto Rico

Under Puerto Rico's General Corporations Act, every corporation formed or registered to do business in the territory must designate a resident agent. This agent serves as the official point of contact for receiving legal process, notices, and demands on behalf of the entity.

Puerto Rico registered agent requirements extend beyond passive receipt of documents. The resident agent also accepts service of process in litigation and maintains a consistent, reachable presence so that regulatory correspondence from the Department of State reaches the corporation without interruption.

Qualification criteria for serving as a resident agent include:

- The agent must be an individual resident of Puerto Rico or a business entity authorized to operate in the territory.

- Individuals serving in this capacity must maintain a physical address within Puerto Rico, not a P.O. Box.

- Corporate agents must be formally authorized to conduct business under Puerto Rico's Department of State records.

- No specific professional license is mandated, but the agent must be consistently reachable during standard business hours.

Incorporate a Company in Puerto Rico

Set up your legal entity in Puerto Rico with full compliance support, from name reservation through Department of State registration.

Registered Office Requirements in Puerto Rico

Puerto Rico registered office requirements mandate that every corporation formed under the Puerto Rico General Corporation Act (Act 164-2009) maintain a physical office address located within the territory.

- A physical street address is required; P.O. boxes are not accepted as a registered office address.

- The address must be located within Puerto Rico; foreign addresses do not satisfy this requirement.

- Virtual office addresses may be used provided a physical presence at that location can be demonstrated.

- No ownership of the premises is required; a lease or service agreement for the address is sufficient.

- The registered office address is publicly recorded in the Puerto Rico Department of State's corporate registry.

- Any change to the office address requires filing an amendment with the Puerto Rico Department of State to update the public record.

- Failure to maintain a compliant local address can result in administrative dissolution of the entity by the Department of State.

Director Requirements in Puerto Rico

Under Puerto Rico's General Corporation Act (Title 14 of the Laws of Puerto Rico), directors assume fiduciary duties of care and loyalty upon appointment, making them personally liable for decisions that cause harm to the corporation or its shareholders. A director who votes in favor of an unlawful distribution or acts in bad faith may face individual liability under the statute.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director is sufficient to constitute a valid board. |

| Maximum Number of Directors | No statutory maximum is prescribed. |

| Local/Resident Director Required | No residency requirement exists under Puerto Rico corporate law. |

| Nationality Restrictions | No nationality restrictions are imposed on directors. |

| Minimum Age Requirement | No statutory minimum age is specified. |

| Corporate Directors Permitted | No statutory prohibition exists, though practice and bylaws may vary. |

| Director Must Be a Shareholder | No statutory requirement to hold shares. |

| Publicly Listed on Registry | Director information is not mandatorily disclosed on a public registry. |

| Disqualification Conditions | No statutory requirement; general principles of fiduciary breach or fraud may apply. |

Despite being a U.S. territory, Puerto Rico operates its own General Corporation Act independently of Delaware or any other state statute, meaning U.S. mainland corporate director rules do not automatically apply here.

Shareholder Requirements in Puerto Rico

Puerto Rico shareholder requirements under the Puerto Rico General Corporation Law (Act 164-2009) permit a corporation to be formed with a single shareholder. There is no statutory maximum on the number of shareholders a corporation may have.

Nationality and Residency Restrictions

Shareholders of a Puerto Rico corporation are not required to be residents or nationals of Puerto Rico. Foreign individuals and entities may hold any percentage of shares without restriction.

Corporate Shareholders

Corporate entities are permitted to act as shareholders in a Puerto Rico corporation. No additional conditions specific to corporate shareholding are imposed under Act 164-2009 beyond standard formation requirements.

Shareholder Liability

Shareholder liability is generally limited to the amount contributed for their shares. Exceptions may arise in cases of fraud, undercapitalization, or where courts apply the doctrine of piercing the corporate veil.

Register of Shareholders

Your corporation is required to maintain an internal register of shareholders. This record is not publicly filed with the Puerto Rico Department of State, though it must be kept available for inspection by shareholders upon request.

Shareholder Structuring Support for Your Puerto Rico Corporation

Get guidance on meeting stockholder rules and shareholder obligations when setting up your Puerto Rico corporation.

UBO / Beneficial Ownership Disclosure Requirements in Puerto Rico

As a U.S. territory, Puerto Rico beneficial ownership requirements are governed by federal law rather than a separate territorial statute. The Corporate Transparency Act (CTA), enforced by the Financial Crimes Enforcement Network (FinCEN), applies to entities formed or registered in Puerto Rico.

- Identify whether your entity qualifies as a "reporting company" under the CTA; most corporations and LLCs formed under Puerto Rico law are covered unless an exemption applies.

- Determine each beneficial owner, defined federally as any individual holding 25% or more ownership interest or exercising substantial control.

- Submit a Beneficial Ownership Information (BOI) report to FinCEN through its secure filing system.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 25% ownership interest or substantial control |

| Filing Authority | FinCEN (Financial Crimes Enforcement Network) |

| Disclosure Deadline at Incorporation | 90 days for entities formed in 2024; 30 days from 2025 onward |

| Publicly Accessible Register | No |

| Penalties for Non-Disclosure | Civil penalties up to $591 per day; criminal penalties possible |

| Ongoing Update Obligation | Updates required within 30 days of any change to reported information |

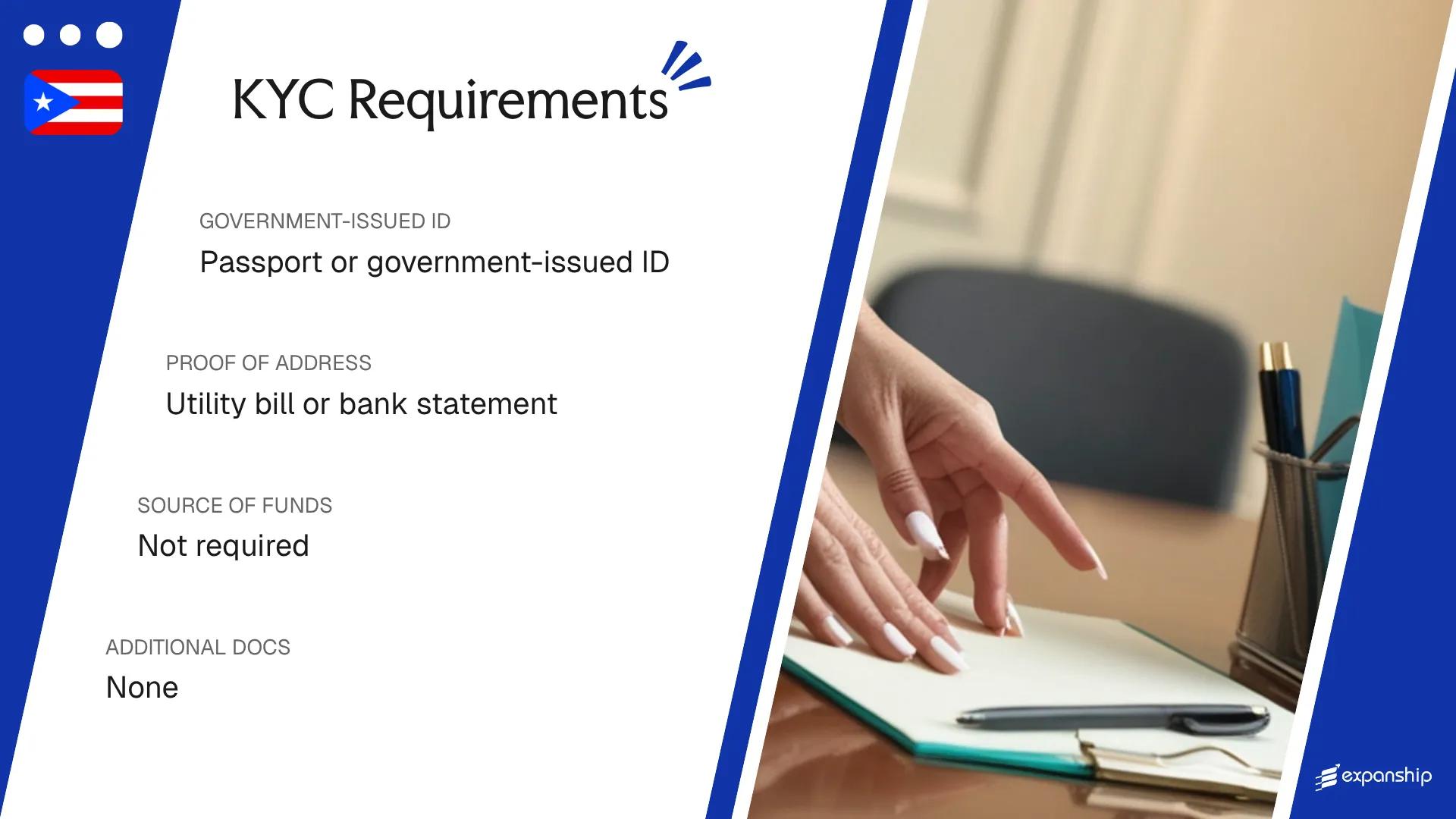

KYC / Document Requirements in Puerto Rico

Puerto Rico KYC requirements incorporation are governed by the Puerto Rico Financial Crimes Enforcement and Anti-Money Laundering Act, administered in coordination with federal obligations under FinCEN. Registered agents and financial institutions collecting incorporation documentation must comply with these standards at the point of entity formation.

Individual / Personal Documents

- Valid government-issued photo identification (passport or national ID card)

- Proof of residential address dated within three months (utility bill or official bank statement)

- Completed personal information declaration identifying the individual's role in the entity

- Tax identification number or equivalent, such as a U.S. Social Security Number or ITIN where applicable

Corporate Documents

- Certificate of incorporation or equivalent formation document from the parent entity's home jurisdiction

- Constitutional documents, such as articles of association or bylaws

- Register of directors or equivalent officer list from the corporate shareholder

- Proof of the corporate entity's registered address

Source of Funds Documentation

- Recent bank statements (typically covering the preceding three to six months)

- Audited financial statements where the introducing capital exceeds standard thresholds

- A written declaration explaining the origin of funds being contributed

Notarisation and Apostille Requirements

- Foreign documents generally require apostille certification under the Hague Convention

- Documents not in English must be accompanied by a certified translation

- Notarisation by a licensed notary may be required for constitutional and identity documents

Submission of foreign corporate documents without a valid apostille or certified English translation is among the most common causes of incorporation delays in this jurisdiction.

Company Name Requirements in Puerto Rico

Puerto Rico company name requirements are assessed at the point of incorporation through the Puerto Rico Department of State, which reviews proposed names for availability and compliance before registration is approved.

Corporate name rules in Puerto Rico require that the name include a legal suffix indicating entity type, such as "Corporation," "Corp.," "Incorporated," or "Inc." The name must be in any language, though it must use the Latin alphabet.

Certain words are restricted or prohibited under Puerto Rico business name compliance standards. Terms implying a connection to government bodies, or words such as "Bank," "Trust," or "Insurance," require prior authorization from the relevant regulatory authority.

Name reservation is available through the Department of State. A reserved name is held for a specified period, giving your business time to complete the incorporation process before the name becomes available to other applicants.

Compliance Services for Companies in Puerto Rico

Ongoing compliance support for Puerto Rico corporations, covering annual filings, registered agent maintenance, and regulatory reporting requirements.

Conclusion

Puerto Rico's incorporation requirements overview reflects a framework governed primarily by the Puerto Rico General Corporation Act, with oversight from the Department of State handling entity registration. Residency requirements are absent for directors and shareholders, but the registered agent obligation is firm — your agent must maintain a physical address on the island. Beneficial ownership disclosure adds a federal compliance dimension that sits outside the local corporate statute. Once these structural requirements are understood, the practical focus shifts to assembling compliant documentation and engaging the processes needed to move from approved registration to active operations.

Expanship's Corporate Services for Puerto Rico Expansion

Puerto Rico's incorporation framework, with its distinct requirements under the Puerto Rico General Corporation Act and OCIF oversight where applicable, involves layers of compliance that take time to manage properly. Expanship's Puerto Rico corporate services are structured to reduce the administrative weight of meeting those requirements, from registered agent coordination to government filings with the Puerto Rico Department of State.

Beyond initial formation, your business may need ongoing support across several areas:

- Expanship prepares and files your company registration documents with the relevant Puerto Rico authorities.

- A registered agent and local office address are provided to satisfy statutory presence requirements.

- Expanship liaises directly with government bodies, including the Department of State, on your behalf.

- Post-incorporation obligations, such as annual report filings and license renewals, are managed on a continuing basis.

- Banking introduction support is available to help your entity establish a local or international account.

- Tax registration and coordination with Hacienda (the Puerto Rico Department of the Treasury) is handled as part of the setup process.

To discuss your requirements, contact Expanship Puerto Rico.

Frequently Asked Questions (FAQ)

The registered agent is not required to be an attorney, but must be either an individual resident of Puerto Rico or a business entity authorized to operate in the jurisdiction. The agent must maintain a physical street address in Puerto Rico, as a P.O. box does not satisfy the requirement under Act No. 164-2009. Any person or entity meeting those conditions may serve in that capacity.

Failing to maintain a registered agent or registered office puts the corporation at risk of administrative dissolution by the Puerto Rico Department of State. Service of process in legal proceedings can also be impaired, which may result in default judgments being entered against the company. Reinstatement after dissolution requires filing the appropriate documents and paying any outstanding fees and penalties.

Puerto Rico imposes no residency or nationality requirements on directors under Act No. 164-2009. A sole director is permitted, and that individual may be a foreign national residing outside the United States and Puerto Rico. The law focuses on the structural role rather than the geographic location of the person filling it.

Puerto Rico corporations are U.S. domestic entities and are therefore subject to the federal Corporate Transparency Act, which requires beneficial ownership information to be reported to the Financial Crimes Enforcement Network (FinCEN). This is a federal obligation that applies regardless of any separate Puerto Rico-level disclosure requirements. Newly formed entities generally must file within 90 days of formation, while existing entities had a separate compliance deadline.

Yes. Under Act No. 164-2009, a corporation's name must include a designator such as "Corporation," "Corp.," "Incorporated," or "Inc." to signal its legal status. Certain words suggesting government affiliation, banking, or insurance activity require prior approval or are restricted outright by the Puerto Rico Department of State. A name search through the Department of State's registry is necessary to confirm availability before filing the Certificate of Incorporation.

When a shareholder or director is a corporate entity rather than a natural person, the KYC documentation required shifts from personal identification to entity-level verification. You will typically need to provide the incorporating documents, certificate of good standing, and beneficial ownership information for the underlying legal entity. The depth of due diligence required can increase further if the corporate shareholder is itself registered in a jurisdiction with limited public disclosure requirements.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.