Key Takeaways

- Lithuania's most widely registered entity, the UAB (Uždaroji Akcinė Bendrovė), offers limited liability with an accessible minimum share capital threshold, making it the dominant choice for founders across most use cases.

- The Law on Companies and the Law on Small Partnerships form the primary legislative framework governing entity formation and compliance obligations in Lithuania.

- Foreign firms operating in Lithuania must choose between a branch office, which can generate local revenue, and a representative office, which cannot — a structural distinction with direct tax and operational consequences.

- Company registration in Lithuania is administered by the Register of Legal Entities under the State Enterprise Centre of Registers (Registrų centras), which has pursued ongoing digitisation of its formation processes.

Introduction to Entity Types in Lithuania

Lithuania is a Baltic state in northeastern Europe, bordering Latvia to the north, Belarus to the east, Poland and the Kaliningrad oblast of Russia to the south. It is an independent republic, a member of the European Union since 2004, and part of the Eurozone. Company registration is administered by the Register of Legal Entities, operated under the State Enterprise Centre of Registers (Registrų centras).

The country operates a standard EU-aligned tax regime, with corporate income tax governed by the Law on Corporate Income Tax (Pelno mokesčio įstatymas).

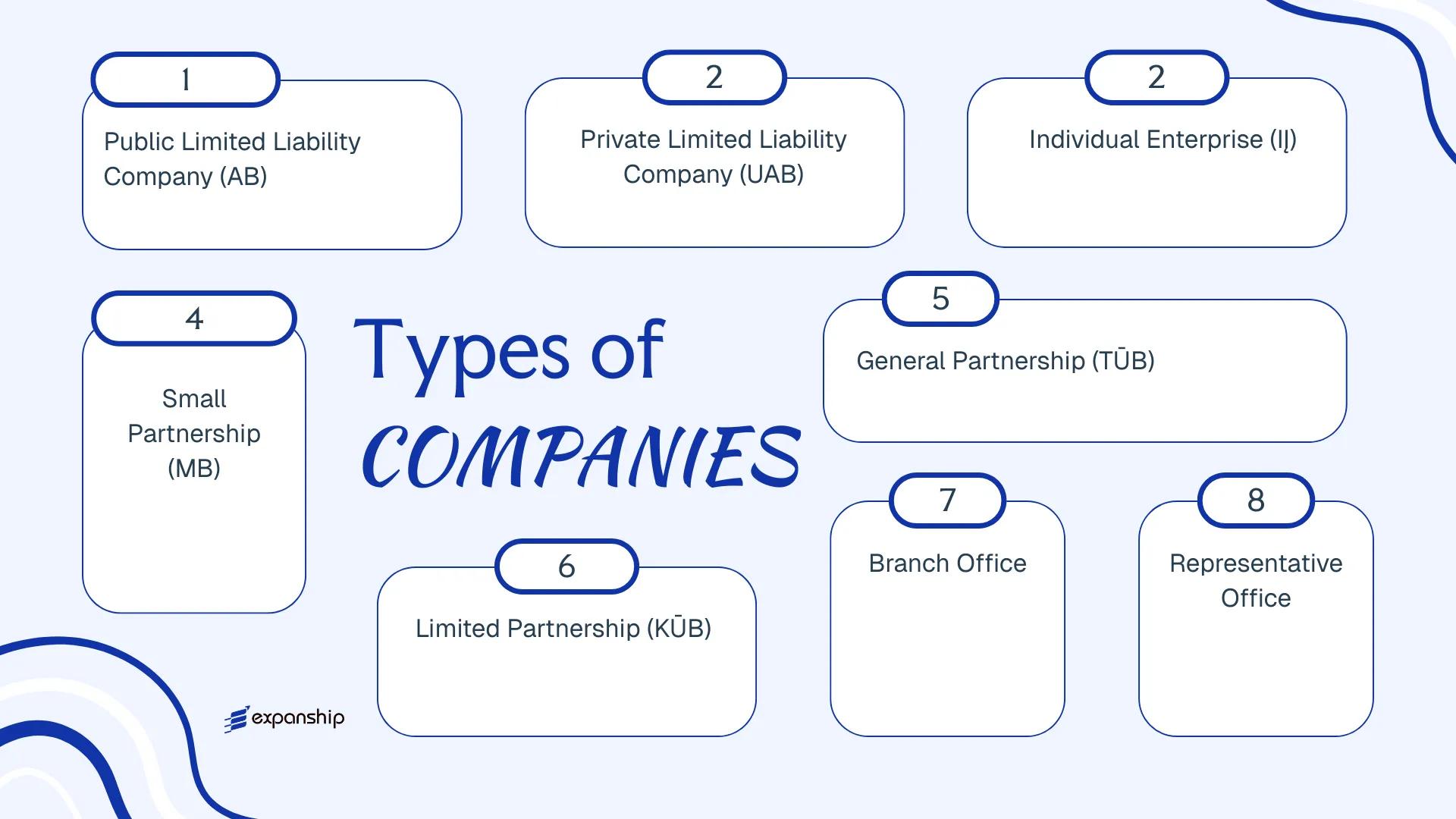

The types of business entities in Lithuania span several legal forms: the Public Limited Liability Company (Akcinė Bendrovė – AB), the Private Limited Liability Company (Uždaroji Akcinė Bendrovė – UAB), the Individual Enterprise (Individuali Įmonė – IĮ), the Small Partnership (Mažoji Bendrija – MB), the General Partnership (Tikroji Ūkinė Bendrija – TŪB), the Limited Partnership (Komanditinė Ūkinė Bendrija – KŪB), and foreign structures such as branch and representative offices.

Each form carries distinct requirements around capital, liability, governance, and taxation — all of which this article examines in detail.

An Overview of Business Structures in Lithuania

Lithuanian company law recognises six principal entity types, primarily governed by the Law on Companies of the Republic of Lithuania (No. IX-2122) alongside supplementary legislation such as the Law on Small Partnerships and the Law on Partnerships. Each structure carries distinct rules on liability, membership, capital requirements, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| AB (Public LLC) | Legal person | Limited to share capital | Taxable | Permitted | 1 shareholder | Register of Legal Entities | Law on Companies IX-2122 |

| UAB (Private LLC) | Legal person | Limited to share capital | Taxable | Permitted | 1 shareholder | Register of Legal Entities | Law on Companies IX-2122 |

| IĮ (Individual Enterprise) | Legal person | Unlimited personal | Taxable | Permitted | 1 natural person | Register of Legal Entities | Law on Individual Enterprises |

| MB (Small Partnership) | Legal person | Limited / unlimited | Taxable | Permitted | 1–10 members | Register of Legal Entities | Law on Small Partnerships |

| TŪB (General Partnership) | Legal person | Unlimited joint | Taxable | Permitted | Min. 2 partners | Register of Legal Entities | Law on Partnerships |

| KŪB (Limited Partnership) | Legal person | Mixed liability | Taxable | Permitted | Min. 2 partners | Register of Legal Entities | Law on Partnerships |

| Branch Office | Non-legal person | Parent liable | Parent taxed | Permitted | 1 parent company | Register of Legal Entities | Law on Companies IX-2122 |

| Representative Office | Non-legal person | Parent liable | Non-trading exempt | Restricted | 1 parent company | Register of Legal Entities | Law on Companies IX-2122 |

Each of these structures is examined in full in the sections below.

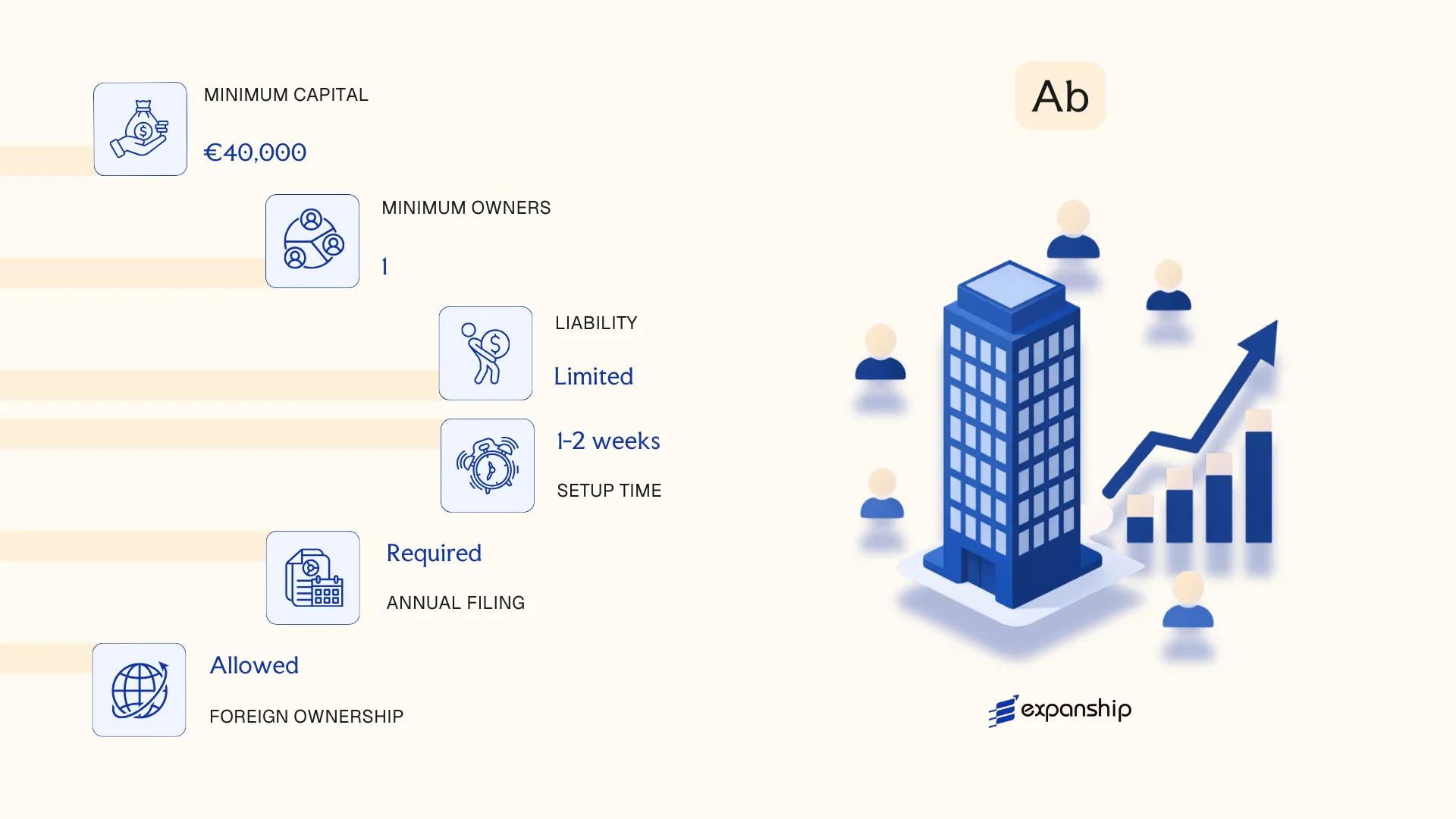

Public Limited Liability Company (Akcinė Bendrovė – AB)

Governed by the Law on Companies of the Republic of Lithuania (Lietuvos Respublikos akcinių bendrovių įstatymas, 2000), the Lithuania AB public limited company is a separate legal entity with full limited liability for its shareholders. Shares may be offered to the public and traded on regulated markets, distinguishing this structure from its closed counterpart.

Akcinė Bendrovė registration in Lithuania requires a minimum share capital of EUR 40,000, at least 25% of which must be paid up at incorporation. The entity must maintain a registered office within the country and appoint a management board or a sole manager, depending on the chosen governance model.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Liability Company (AB) | Separate legal personality; shareholders not liable for company debts |

| Members | Shareholders (no minimum or maximum count) | Shares may be publicly offered and listed on a stock exchange |

| Governance | Board of Directors and/or Supervisory Board; sole manager permitted for smaller ABs | Two-tier or one-tier governance structure available |

| Local Presence | Registered office in Lithuania required | No mandatory resident director requirement under general rules |

| Share Capital | Minimum EUR 40,000; at least 25% paid at registration | Capital divided into registered shares; must be denominated in EUR |

| Privacy | Shareholder register is publicly accessible via the Register of Legal Entities (Juridinių asmenų registras) | Beneficial ownership disclosed to the Centre of Registers |

Focus Points

- Taxation: Subject to 15% corporate income tax on profits; standard VAT rate of 21% applies once turnover thresholds are met; dividends paid to non-residents attract 15% withholding tax, reduced under applicable double tax treaties; no stamp duty on share transfers.

- Annual Compliance: Mandatory annual financial statements audited by a certified auditor; annual report filed with the Register of Legal Entities.

- Treaty Access: Lithuania's extensive double tax treaty network is accessible to AB entities, making the structure suitable for cross-border holding arrangements.

- Conversion: An AB may be reorganised into a UAB or other permitted legal form through a statutory reorganisation procedure under the Law on Companies.

- Public Share Issuance: Any public offering of shares requires prospectus approval by the Bank of Lithuania (Lietuvos bankas), which acts as the securities regulator.

Closing

The AB structure suits large-scale trading operations, regulated financial entities, and businesses seeking access to public capital markets or institutional investors. Its primary advantage is the ability to issue shares publicly; the main drawback is the higher administrative burden relative to private structures, including mandatory audit and prospectus requirements for share offers.

Best suited for large enterprises, regulated institutions, or businesses with plans to list on the Nasdaq Vilnius stock exchange or raise capital from the public.

Company Incorporation in Lithuania

Incorporate an AB or other legal entity in Lithuania with end-to-end support from Expanship's corporate services team.

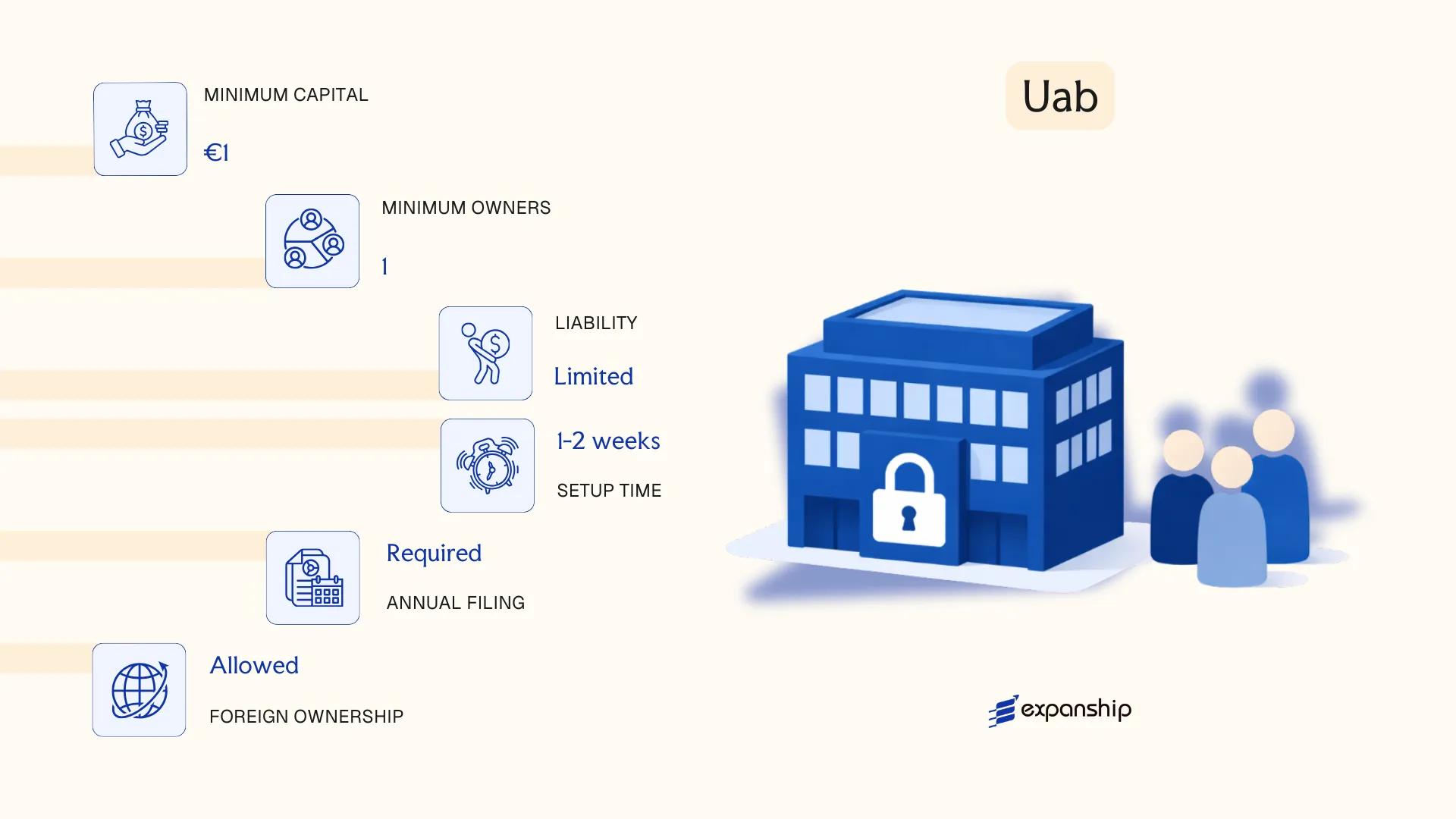

Private Limited Liability Company (Uždaroji Akcinė Bendrovė – UAB)

The Lithuania UAB private limited company is governed by the Law on Companies of the Republic of Lithuania (No. IX-2190, 2003, as amended). It holds separate legal personality, meaning the entity itself bears rights and obligations distinct from those of its shareholders.

Liability is capped at each shareholder's contribution to the share capital, and the structure sits between a sole proprietorship and a public company in terms of regulatory burden.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Shares cannot be publicly offered or traded on a stock exchange |

| Members | Shareholders (1–249) | Single-shareholder UABs are permitted; exceeding 249 requires conversion to AB |

| Governance | At least 1 director (can be non-resident) | Supervisory board optional unless required by articles |

| Local Presence | Registered address in Lithuania required | No mandatory resident director; registered agent not legally required |

| Share Capital | Minimum EUR 2,500 | Must be fully paid up before registration |

| Privacy | Shareholders and directors disclosed in the Register of Legal Entities | Beneficial ownership filed with the Centre of Registers |

Focus Points

- Taxation: Subject to 15% corporate income tax (5% for small entities meeting qualifying thresholds); standard VAT rate of 21% applies once turnover exceeds EUR 45,000; withholding tax on dividends is generally 15%, reducible under applicable tax treaties.

- Annual Compliance: Must file annual financial statements with the Centre of Registers; statutory audit required if two of three size thresholds are exceeded.

- Treaty Access: UABs are Lithuanian tax residents and qualify for Lithuania's network of double taxation treaties.

- Conversion: A UAB may be converted to an AB if shareholder count exceeds 249 or a public share offering is planned.

- Restrictions: Shares may not be freely transferred without adhering to pre-emption rights provisions set out in the company's articles of association.

Closing

The UAB suits trading operations, holding structures, and service-based businesses where external capital-raising through public markets is not required. The low minimum capital threshold and flexible governance make formation accessible, though the mandatory disclosure of beneficial ownership limits structural privacy.

The UAB is most appropriate for foreign entrepreneurs and SMEs seeking a fully recognised corporate entity in the EU with limited liability and straightforward Uždaroji Akcinė Bendrovė formation requirements.

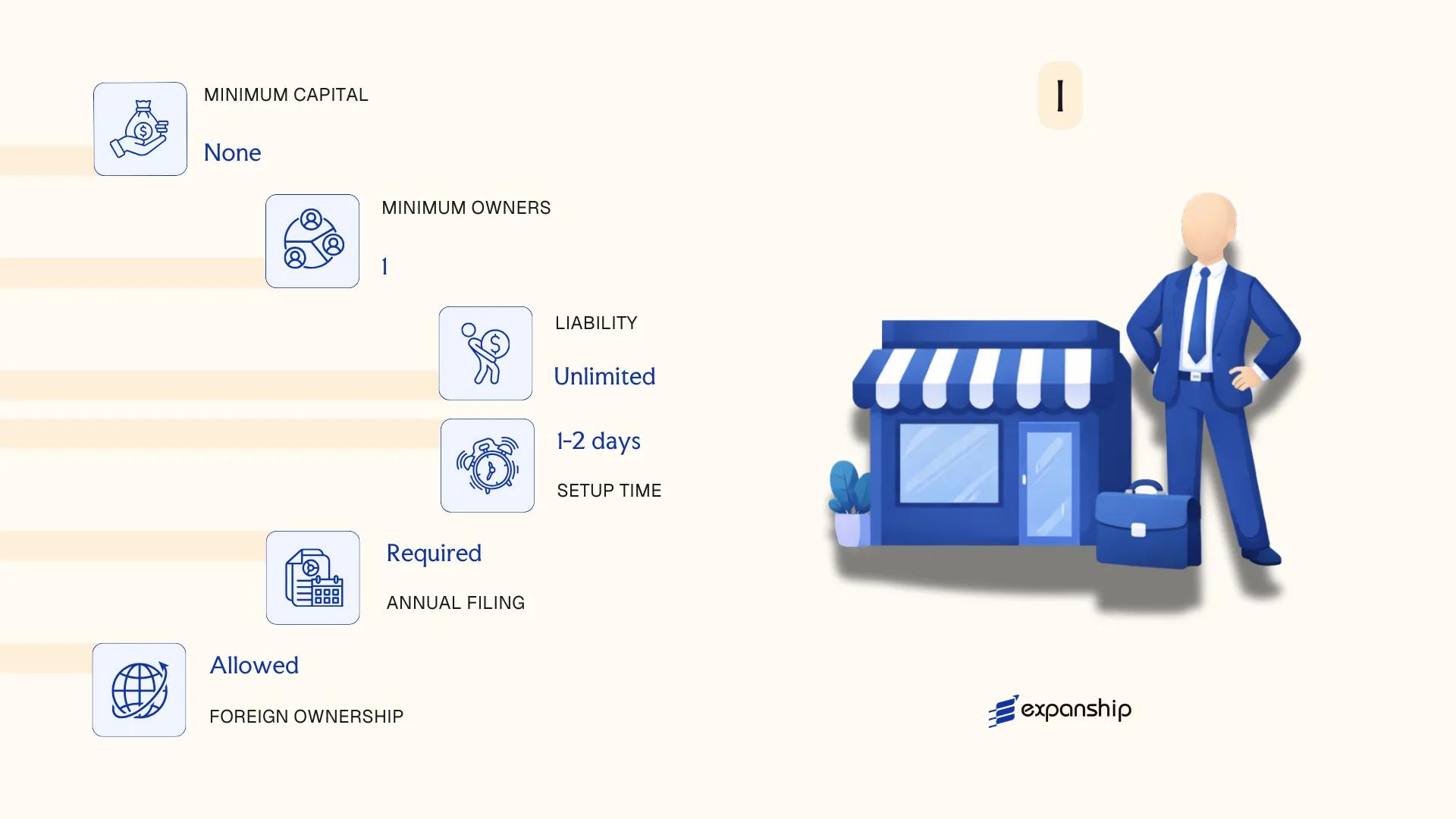

Individual Enterprise (Individuali Įmonė – IĮ)

The Individuali Įmonė is governed by the Law on Individual Enterprises of the Republic of Lithuania (2003), which establishes it as a legally distinct entity separate from its owner. Despite holding separate legal personality, the proprietor bears unlimited personal liability for all obligations of the business — a structural characteristic that sets this form apart from capital-based entities.

Completing a Lithuania individual enterprise IĮ registration requires filing with the Register of Legal Entities (Juridinių asmenų registras) under the State Enterprise Centre of Registers. There is no minimum capital requirement, which makes the entry threshold low, though the liability exposure remains a material consideration for sole traders operating under this structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individuali Įmonė (IĮ) | Separate legal personality; sole ownership only |

| Member Designation | Proprietor (savininkas) | One natural person; cannot be owned by a legal entity |

| Local Presence | Registered address in Lithuania required | No registered agent requirement under statute |

| Capital | No statutory minimum; denominated in EUR | Owner's assets may be used to satisfy business debts |

| Privacy | Proprietor's name linked to registration record | Publicly searchable via Juridinių asmenų registras |

Focus Points

- Taxation: Subject to corporate income tax at 15% (5% if qualifying as a small entity); VAT registration threshold applies; profits distributed to the owner may be subject to personal income tax and social contributions.

- Annual Compliance: Annual financial statements must be filed with the Register of Legal Entities; audit requirements depend on size thresholds.

- Conversion: An IĮ can be reorganised into a UAB or other entity form under the Lithuanian Law on Companies, subject to standard reorganisation procedures.

- Treaty Access: As a Lithuanian-resident legal entity, the IĮ may access Lithuania's tax treaty network, though treaty benefits depend on the specific bilateral agreement and entity classification.

- Restrictions: Cannot have multiple owners; a legal entity cannot serve as proprietor.

Recommendations

The Individuali Įmonė suits sole traders and micro-businesses in local service or retail sectors where simplicity outweighs liability concerns; the absence of a minimum capital requirement reduces the setup burden, but unlimited personal liability makes it unsuitable for ventures carrying significant financial or legal risk.

This structure is most appropriate for a single natural person operating a small-scale, low-risk business who prioritises minimal administrative overhead over personal asset protection.

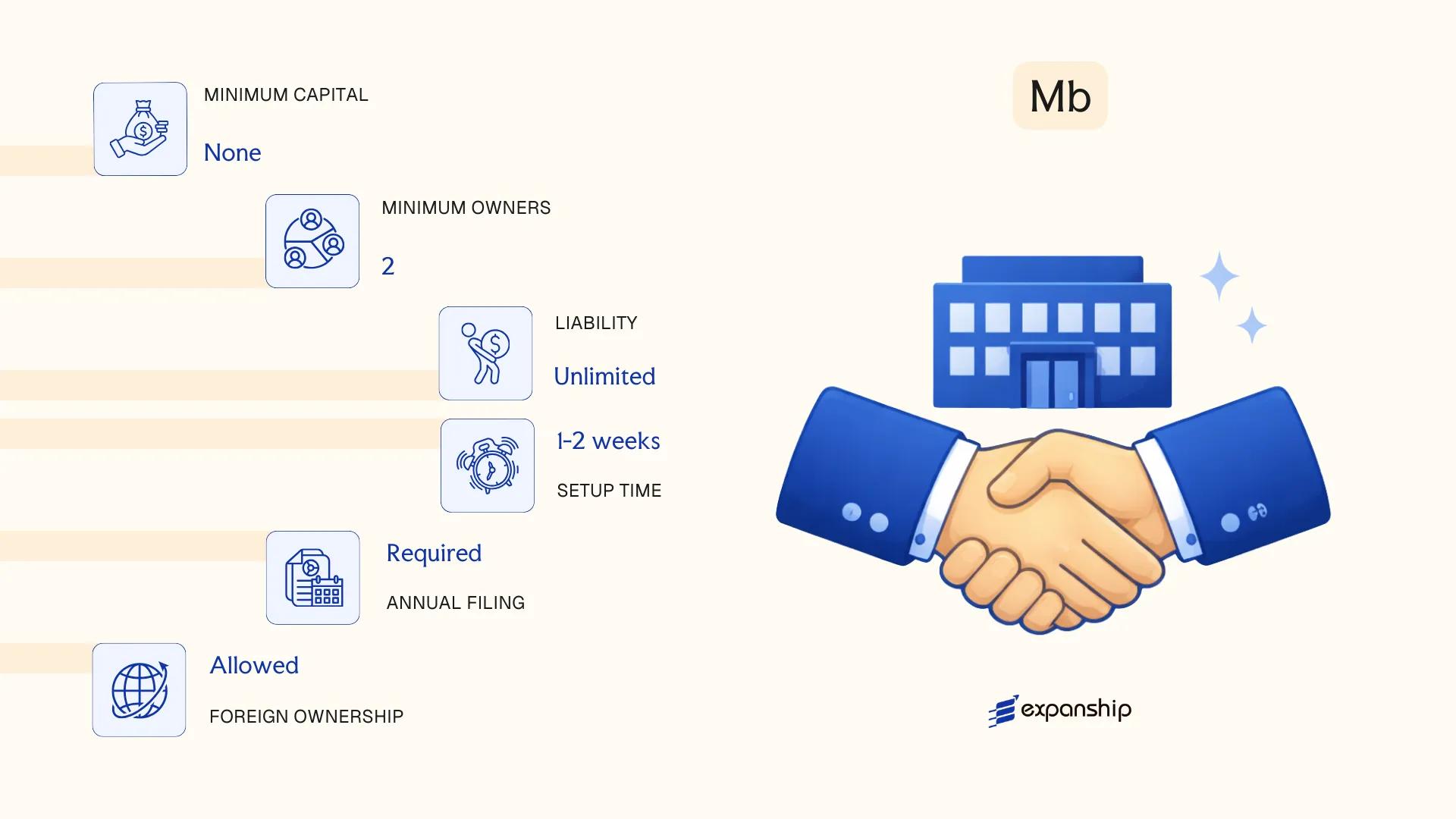

Small Partnership (Mažoji Bendrija – MB)

Introduced under the Law on Small Partnerships of the Republic of Lithuania (2012), the Mažoji Bendrija is a hybrid entity designed for micro-scale operations. It carries separate legal personality, meaning the business and its members are legally distinct, yet it retains organisational simplicity closer to a sole enterprise than a capital company. Liability is generally limited to each member's contribution, though members who manage the entity directly may bear additional responsibility under specific statutory conditions.

Lithuania small partnership MB formation appeals to freelancers, small service providers, and early-stage ventures that want legal separation without the administrative burden of a UAB. Members themselves run the business without a mandatory board structure, and the entity does not require a minimum share capital at formation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Small Partnership (Mažoji Bendrija) | Separate legal personality; hybrid between a partnership and limited company |

| Members | 1 to 10 natural persons only | Legal entities cannot be members; all members are referred to as "nariai" (members) |

| Management | Members manage directly; no board required | A member-manager (narys vadovas) acts as the authorised representative |

| Local Presence | Registered address in Lithuania required | No registered agent requirement, but a physical or virtual registered office address is mandatory |

| Capital | No minimum capital requirement | Contributions can be monetary or in-kind; contribution amounts are recorded in the agreement |

| Privacy | Members listed in the Register of Legal Entities | The register is publicly accessible; no meaningful privacy over membership |

Focus Points

- Taxation: Subject to corporate income tax at 5% (reduced rate for small entities meeting turnover and headcount thresholds) or the standard 15%; VAT registration required once turnover exceeds the statutory threshold; member distributions may attract personal income tax; no withholding tax on dividends paid to natural person members under general rules.

- Annual Compliance: Annual financial statements must be filed with the Register of Legal Entities; small entities may qualify for simplified accounting under Lithuanian accounting standards.

- Economic Substance: No formal substance test, but the member-manager must be identifiable and the entity must conduct genuine activity.

- Conversion: An MB can be reorganised into a UAB or other legal form through a statutory reorganisation procedure under the Civil Code of Lithuania.

- Restrictions: Membership is restricted to natural persons only; the ten-member cap makes this structure unsuitable for businesses expecting investor participation or external equity.

Closing Paragraph

An MB suits small domestic service businesses, creative professionals, and consultants who need legal separation from personal liability without the compliance overhead of a capital company. The absence of a minimum capital requirement is a practical advantage, though the ten-member ceiling and the exclusion of legal entity members significantly limit scalability.

This entity type is best suited for resident individuals or small groups of natural persons operating a low-capital, service-oriented business within Lithuania.

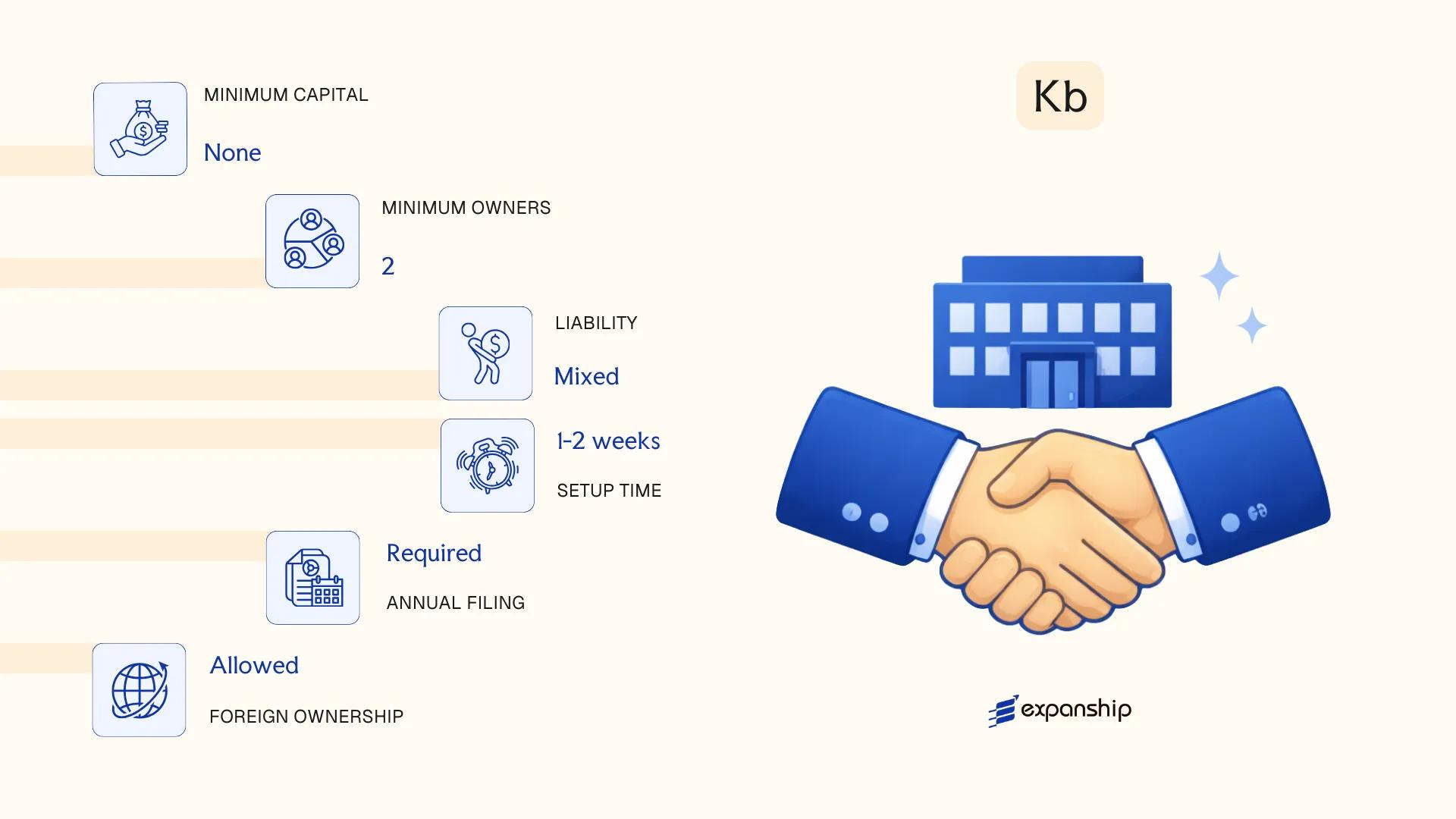

Partnerships in Lithuania [General Partnership (Tikroji Ūkinė Bendrija – TŪB), Limited Partnership (Komanditinė Ūkinė Bendrija – KŪB)]

Both the Tikroji Ūkinė Bendrija (TŪB) and Komanditinė Ūkinė Bendrija (KŪB) are governed by the Law on Partnerships of the Republic of Lithuania. Each form carries separate legal personality, meaning the partnership itself can enter into contracts, own assets, and bear liabilities distinct from its members.

The Lithuania general and limited partnership TŪB KŪB structures differ primarily in liability exposure. In a TŪB, all partners bear unlimited joint and several liability for the firm's obligations. A KŪB introduces a two-tier membership model: general partners retain unlimited liability, while limited partners are liable only up to their contributed capital.

Key Characteristics

| Requirement | TŪB Detail | KŪB Detail |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership |

| Members Referred To As | Partners (tikrieji nariai) | General partners (tikrieji nariai) and limited partners (nariai komanditoriai) |

| Members | Minimum 2 partners; no statutory maximum; all bear unlimited liability | Minimum 1 general partner and 1 limited partner; no statutory maximum |

| Local Presence | Registered office address in Lithuania required | Registered office address in Lithuania required |

| Capital | No statutory minimum capital requirement; contributions may be monetary or in-kind | No statutory minimum; limited partner's liability capped at their contribution amount |

| Privacy | Partner names appear in the Register of Legal Entities (Juridinių Asmenų Registras) | General and limited partner names both disclosed in the public register |

Focus Points

- Taxation: Partnerships are generally treated as tax-transparent for corporate income tax purposes; profits pass through to partners and are taxed at the individual or corporate level depending on partner status; VAT registration applies once turnover thresholds are met; no specific withholding tax exemption applies at the entity level.

- Annual Compliance: Partners must file annual financial statements with the Register of Legal Entities; partnership agreements govern internal governance.

- Treaty Access: Pass-through treatment may limit direct access to Lithuania's double tax treaty network; treaty benefits depend on the partner's own tax residency.

- Restrictions: Non-EU nationals acting as general partners should verify any residency or permit requirements under Lithuanian law.

- Conversion: A TŪB may be reorganised into a KŪB or other permitted legal forms under the Law on Companies.

Closing

Both forms suit professional service arrangements or joint ventures where partners prefer direct operational control over a formal corporate hierarchy. The pass-through tax treatment can reduce structural tax layers, though unlimited liability for general partners represents a material risk that limits use in capital-intensive or high-liability activities.

TŪB and KŪB structures are most appropriate for small groups of trusted partners, professional practitioners, or joint venture arrangements where simplified governance outweighs the need for liability protection.

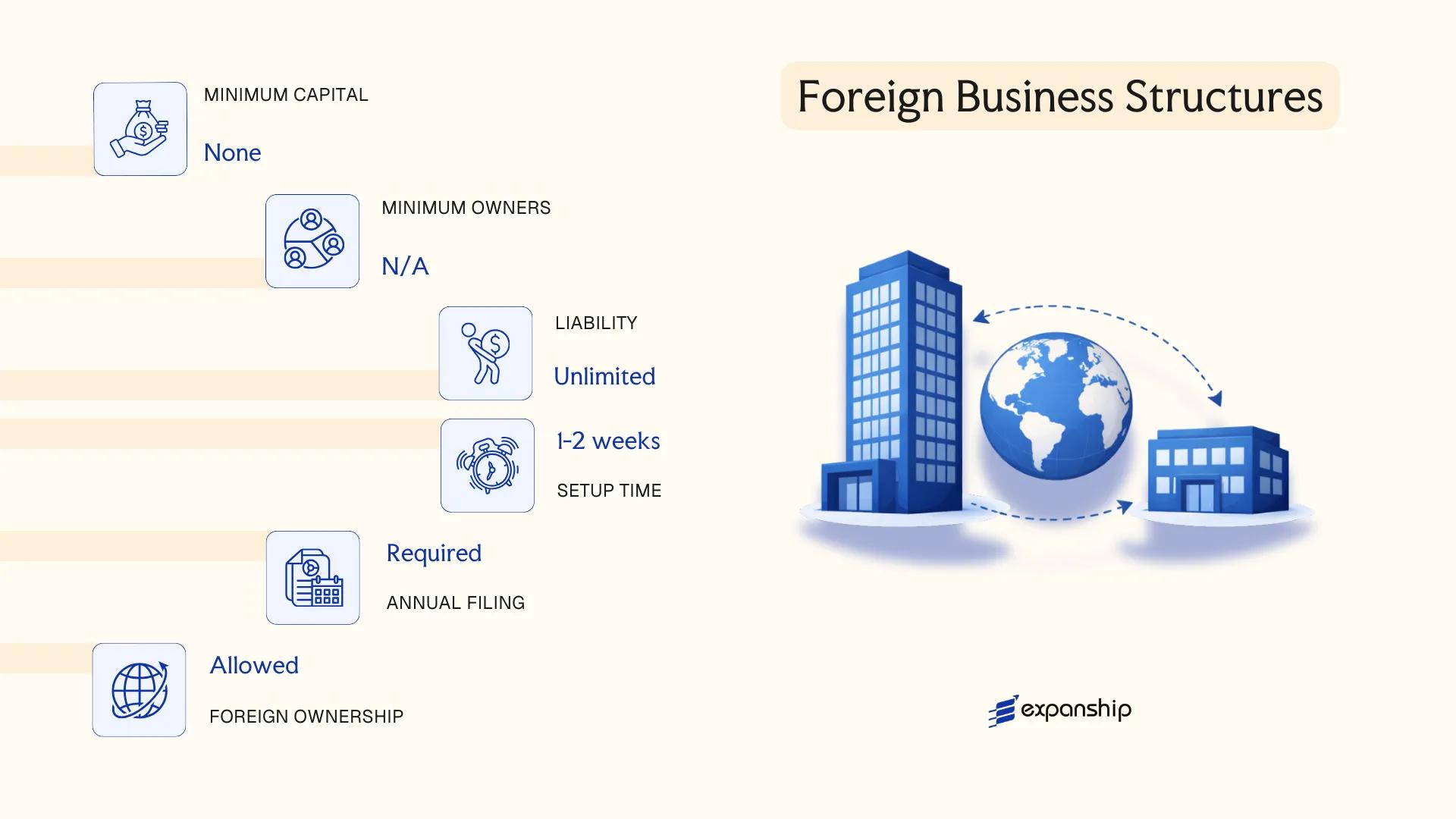

Foreign Business Structures in Lithuania [Branch Office, Representative Office]

Registering a foreign company branch office Lithuania does not create a new legal entity. Both a branch office and a representative office are organisational units of a foreign parent company, governed primarily by the Law on Companies of the Republic of Lithuania (2000, No. VIII-1835) and supplementary provisions under the Civil Code. Neither structure carries separate legal personality, meaning the parent company bears direct liability for obligations incurred by either structure.

Registration of both forms is handled through the Register of Legal Entities (Juridinių asmenų registras), administered by the State Enterprise Centre of Registers (VĮ Registrų centras).

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None – extension of parent | None – extension of parent |

| Permitted Activities | Commercial and operational | Non-commercial only (marketing, liaison, market research) |

| Head of Structure | Appointed manager (Vadovas) | Appointed representative |

| Registered Address | Required in Lithuania | Required in Lithuania |

| Capital Requirement | None | None |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch office profits are subject to 15% corporate income tax on Lithuanian-sourced income; representative offices generating no revenue are generally not subject to corporate tax, though payroll taxes apply to local staff. VAT registration is required if taxable turnover thresholds are met.

- Treaty Access: Treaty benefits depend on the parent company's tax residence; the structure itself does not independently access double tax treaties.

- Annual Compliance: Both structures must file annual financial reports with the Centre of Registers; branches additionally submit accounting records in line with Lithuanian accounting standards.

- Restrictions: A representative office cannot sign commercial contracts or generate revenue; any commercial activity converts its status to a branch in practice.

- Conversion: Neither structure can be directly converted into a Lithuanian legal entity; a separate incorporation process is required.

Sub-Types

Branch Office

A branch office may conduct the full scope of the parent company's commercial activities within Lithuania, including entering contracts and generating income. It is commonly used by foreign firms testing the market before committing to full incorporation.

Representative Office

A representative office is limited to promotional, informational, and liaison functions on behalf of the parent. It cannot independently conduct business transactions and is suited to firms that require a local point of contact without commercial obligations.

Closing

Both structures suit foreign companies seeking a light operational presence without committing to local incorporation, though the representative office's activity restrictions make it unsuitable for any revenue-generating operations.

A branch office suits foreign companies with active commercial operations in the Lithuanian market; a representative office is appropriate only where the local function is strictly non-commercial.

How to Choose the Right Entity Type in Lithuania

Knowing how to choose a company type in Lithuania before registration prevents costly structural corrections later.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences from day one.

- Forming a UAB when your business qualifies as a regulated financial institution means operating outside the licensing framework set by the Bank of Lithuania, which can result in forced dissolution or administrative penalties.

- Choosing an Individual Enterprise (IĮ) when you require treaty-based withholding tax reductions is counterproductive, as sole proprietorships typically fall outside the scope of double taxation agreements.

- Selecting a Small Partnership (MB) without confirming it can meet any applicable substance requirements may trigger compliance failures under transfer pricing or controlled foreign company rules.

- Registering a General Partnership (TŪB) when limited liability is operationally necessary exposes members to unlimited personal liability for all firm obligations.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward a different registered structure under the Law on Companies of the Republic of Lithuania.

- Ownership and Management: A single-member operation suits the MB or IĮ, while multi-investor arrangements with board governance requirements point toward a UAB or AB.

- Tax Objectives: Your need for full treaty network access, a reduced corporate tax rate, or participation exemption eligibility will narrow the viable entity options.

- Liability Exposure: If personal asset protection is a priority, unincorporated structures such as TŪB are incompatible with that objective.

- Substance Capacity: Your ability to maintain a real office, local employees, and management decisions within the jurisdiction should guide whether a full corporate entity or a lighter structure is appropriate.

- Exit Strategy: Redomiciliation, conversion between entity types, and voluntary liquidation procedures differ significantly across structures registered with the Register of Legal Entities.

Compliance Services for Companies in Lithuania

Maintain statutory obligations, filing deadlines, and regulatory requirements for your Lithuanian entity.

Conclusion

Lithuania's company formation landscape — covered across this guide — presents several structurally distinct options governed primarily by the Law on Companies and the Law on Small Partnerships. The UAB dominates registration statistics, making it the default choice for most founders due to its limited liability and accessible capital threshold. An AB suits larger operations requiring public capital markets. The IĮ fits sole traders accepting personal liability, while the MB serves small groups of individuals preferring a members-managed structure without share capital. TŪB and KŪB address specific partnership arrangements, and foreign firms use branch or representative offices depending on whether they intend to generate local revenue.

Incorporating in Lithuania carries added weight given the country's EU membership, its expanding tax treaty network, and the Centre of Registers' ongoing digitisation of registration processes. Your choice of entity will shape tax obligations, governance requirements, and long-term operational flexibility. Expanship's team works directly with these structures across jurisdictions.

How Expanship Can Assist You

Expanship's Lithuania company incorporation services cover the full process of establishing and maintaining a business entity under Lithuanian law. From registering a UAB with the Register of Legal Entities (Juridinių asmenų registras) to structuring a branch office for a foreign parent company, our team works directly with the relevant authorities on your behalf.

From initial document preparation to ongoing compliance, your business is supported at every stage:

- Document preparation and notarisation

- Registered agent and registered office provision in Lithuania

- Filing with the Register of Legal Entities

- Post-incorporation compliance management, including annual reporting obligations

- Government liaison for permits and regulatory correspondence

- Banking introduction assistance with Lithuanian financial institutions

Reach out to Expanship Lithuania to discuss how we can support your incorporation or restructuring plans.

Frequently Asked Questions (FAQ)

The UAB (Uždaroji Akcinė Bendrovė) is the most frequently incorporated entity. Its low minimum share capital of EUR 1, single-shareholder eligibility, and limited liability protection make it the default choice for most business founders.

A UAB is a closed structure with a maximum of 249 shareholders and no public share trading rights, while an AB can list shares on regulated markets such as Nasdaq Vilnius. The AB carries heavier disclosure, audit, and governance obligations under the Law on Companies.

Among available structures, the Mažoji Bendrija (MB) involves relatively minimal public disclosure compared to the AB. Beneficial ownership information is, however, recorded in the Register of Legal Entities for all entity types under Lithuanian AML legislation, and nominee arrangements do not eliminate these obligations.

No. A TŪB (Tikroji Ūkinė Bendrija) and KŪB (Komanditinė Ūkinė Bendrija) each require at least two participants by statute. A UAB, MB, and IĮ can each be established by one person.

Yes. Non-residents may incorporate a UAB or AB without restrictions on nationality. Foreign founders must obtain a personal identification number through the Migration Department and submit notarised or apostilled identity documents to the Register of Legal Entities.

Conversion between entity types is permitted under Chapter XI of the Law on Companies. A UAB may be reorganised into an AB, and vice versa, subject to shareholder resolutions, auditor review, and re-registration with the Centre of Registers.

No. An IĮ (Individuali Įmonė) does not constitute a separate legal person; the owner bears unlimited personal liability for its obligations. All other structures covered under Lithuanian company law, including the UAB, AB, MB, TŪB, and KŪB, possess legal personality upon registration.

The MB and IĮ carry the lightest administrative burden. An MB with a turnover below the VAT registration threshold and no hired employees faces minimal annual reporting requirements compared to a UAB or AB, which must file annual financial statements with the Register of Legal Entities regardless of activity level.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.