Key Takeaways

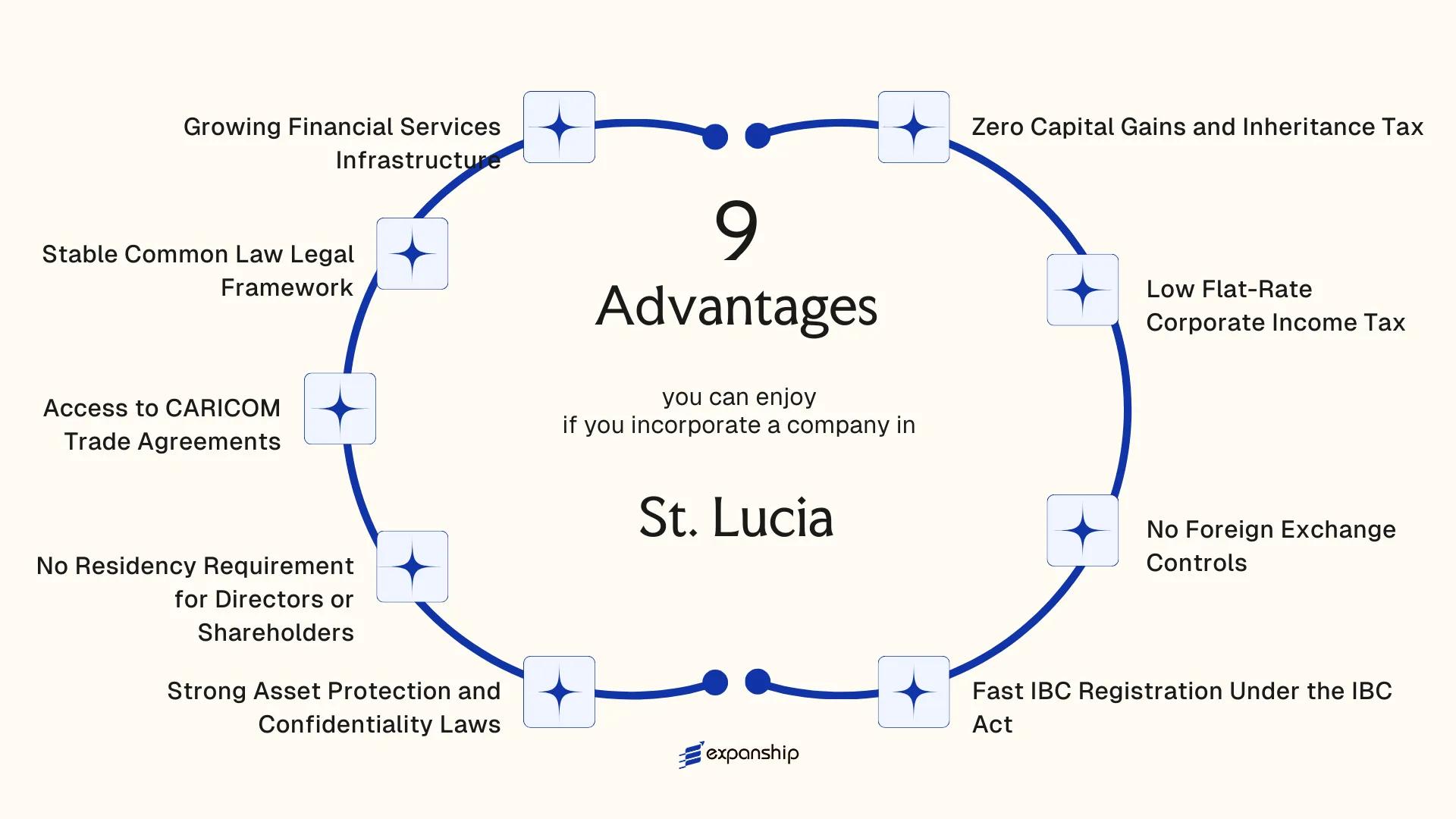

- St. Lucia's International Business Companies Act exempts qualifying entities from capital gains and inheritance tax on income sourced outside the jurisdiction, eliminating two tax exposures that commonly erode returns in other offshore structures.

- Because the Financial Services Regulatory Authority imposes no residency requirement on directors or shareholders, foreign owners can maintain full operational control without establishing a local presence or appointing nominee residents to satisfy compliance thresholds.

- Membership in CARICOM gives St. Lucia-registered businesses preferential access to regional trade arrangements across member states, an advantage unavailable to entities incorporated in purely offshore jurisdictions with no regional treaty framework.

- The jurisdiction's common law legal system produces court decisions that are recognizable and enforceable within the broader Commonwealth, reducing the legal uncertainty that can undermine cross-border commercial agreements structured through civil law or hybrid jurisdictions.

St. Lucia is an independent Eastern Caribbean nation and a member of the Commonwealth, situated between Martinique and St. Vincent in the Lesser Antilles. Company registration falls under the oversight of the Financial Services Regulatory Authority, which administers corporate filings and ongoing compliance obligations for businesses operating within the jurisdiction. Foreign investors most commonly establish an International Business Company when structuring operations through the country.

The tax posture is broadly favorable, with qualifying international entities subject to low or zero liability on income generated outside the jurisdiction. Foreign ownership faces no statutory restrictions — non-residents may hold 100% of shares in a locally registered entity without requiring a local partner or government approval. This openness to foreign direct investment is reflected in the legislative framework governing international business activity.

This article examines the concrete advantages the jurisdiction offers to businesses considering incorporating here, drawing on the specific laws, regulatory structures, and treaty arrangements that define its corporate environment.

Zero Capital Gains and Inheritance Tax

Under the International Business Companies Act of St. Lucia, IBCs are statutorily exempt from capital gains tax on disposals of assets, securities, or investments held through the entity. That exemption is not incidental — it is codified, which means your gains are protected by legislation rather than administrative discretion.

Capital Gains Exemption for IBCs

When a business sells shares, real property held offshore, or investment portfolios, the absence of capital gains tax means the full proceeds remain within the entity. This is particularly relevant for holding companies and investment vehicles that cycle through asset disposals regularly, since each transaction would otherwise trigger a taxable event in jurisdictions that apply rates of 20% to 35% on such gains.

Inheritance Tax and Estate Planning

St. Lucia imposes no inheritance tax on IBC assets, meaning ownership transfers between generations or shareholders do not reduce the estate's value through a government levy. Structuring assets inside an IBC can therefore serve as a functional estate planning mechanism for foreign owners.

Capital gains and inherited assets held through a St. Lucia IBC pass between transactions and generations without triggering a statutory tax deduction at either stage.

Low Flat-Rate Corporate Income Tax

St. Lucia low flat-rate corporate income tax is one of the more tangible structural advantages available to foreign-owned entities incorporated under the International Business Companies Act. IBCs registered in the jurisdiction are generally subject to a flat corporate tax rate that sits well below the OECD average of around 23%, reducing the overall tax burden on retained earnings and distributed profits.

For a foreign business owner, the practical implication is straightforward: a predictable, fixed rate simplifies annual tax provisioning. Unlike progressive corporate tax systems common across the EU and North America, a flat structure means your effective rate does not climb as profits grow.

This rate applies to income earned outside of St. Lucia, which is the typical operational model for an IBC. Income sourced domestically may be treated differently under local tax rules.

The flat-rate structure offers several advantages that go beyond the headline number:

- No bracket thresholds mean tax liability scales proportionally, not punitively, as the business grows

- Foreign investors can model multi-year tax exposure without accounting for rate escalation

- The fixed structure reduces reliance on complex tax planning arrangements to manage bracket creep

Company Incorporation in St. Lucia

Register your IBC in St. Lucia and benefit from a flat-rate corporate tax structure designed for internationally operating businesses.

No Foreign Exchange Controls

No foreign exchange controls St. Lucia means that IBCs and other registered entities face no statutory restrictions on moving funds across borders. Under the International Business Companies Act, foreign-registered businesses are not subject to exchange control regulations that would otherwise limit how capital enters or exits the company. This freedom applies to receipts, payments, and transfers in any currency.

For a foreign business owner, the practical value is direct. You can repatriate profits to your home country, pay international suppliers, or hold multi-currency balances without seeking regulatory approval. Many jurisdictions require businesses to obtain central bank authorization before transferring capital abroad, which can introduce delays of days or weeks and add administrative overhead. That approval process does not exist here for qualifying IBCs.

| Transaction Type | Restriction | Approval Required |

|---|---|---|

| Profit repatriation | None | No |

| Foreign currency accounts | Permitted | No |

| Cross-border supplier payments | None | No |

| Capital contributions from abroad | None | No |

St. Lucia free currency movement for businesses is governed by the structure of the IBC regime itself, not by a separate exemption that requires periodic renewal. The benefit is built into the entity type. Your firm can price contracts in USD, EUR, or other currencies, receive payment into offshore accounts, and distribute dividends internationally without triggering reporting obligations tied to currency movement. This structural feature gives international businesses meaningful control over treasury operations from the outset of incorporation.

Fast IBC Registration Under the IBC Act

Fast IBC registration St. Lucia IBC Act is not just a procedural convenience — it translates directly into reduced setup costs and faster operational readiness for foreign business owners.

Under the International Business Companies Act, an IBC can typically be incorporated within one to two business days once documentation is submitted to the Registrar of International Business Companies. There is no requirement to publish incorporation notices or await prolonged government review periods. That speed matters because your entity can open bank accounts, sign contracts, and conduct business far sooner than in jurisdictions where formation timelines run several weeks.

The registered agent system underpins this efficiency. You are required to appoint a licensed local registered agent, who submits incorporation documents on your behalf. This intermediary structure concentrates compliance obligations at the agent level, removing the need for you to appear in person or engage directly with the Registrar.

Keep the following in mind:

- A licensed registered agent must handle all filings with the Registrar

- Articles of Incorporation must conform to the IBC Act's prescribed form

- The company name must receive prior clearance before submission

- Government incorporation fees apply and vary by authorized share capital

An IBC incorporated in St. Lucia can legally commence business on the exact date of incorporation, with no mandatory waiting or activation period required after registration.

Strong Asset Protection and Confidentiality Laws

St. Lucia asset protection and confidentiality laws are codified primarily under the International Business Companies Act, Cap. 12.14, which governs the registration and operation of IBCs. This legislation creates a structured legal environment where the identities of beneficial owners, shareholders, and directors are shielded from public disclosure, a distinction that carries direct consequences for how your business manages exposure to third-party claims.

Confidentiality Protections for Shareholders and Directors

Under the IBC Act, the register of members and directors is not filed with any public registry. This means competitors, litigants, and other external parties cannot access ownership details through routine public records searches. For business owners operating in sectors where ownership anonymity reduces commercial or litigation risk, this structural privacy is a functional advantage rather than an incidental feature.

Nominee arrangements are legally permissible, adding a further layer of separation between the public record and the actual beneficial owner. The registered agent holds this information under confidentiality obligations imposed by statute.

Asset Segregation and Protective Structures

IBCs incorporated under St. Lucian law can hold assets across multiple classes of shares with distinct rights, allowing for deliberate structural separation of holdings. This makes it possible to ring-fence specific asset pools within a single entity, which has direct relevance when managing liability across different business lines or investment categories.

Offshore asset protection through an IBC is reinforced by the absence of any requirement to disclose foreign assets to local authorities, provided the company conducts business outside the jurisdiction.

Structure Your St. Lucia IBC for Maximum Privacy and Protection

Get tailored guidance on using St. Lucia's confidentiality framework and asset protection laws to structure your IBC effectively.

No Residency Requirement for Directors or Shareholders

Under St. Lucia's International Business Companies Act, there is no residency requirement for directors or shareholders of an IBC. A single director is sufficient, and that individual can be of any nationality, resident anywhere in the world. Corporate directors and corporate shareholders are also permitted, which allows holding structures to be organized across multiple jurisdictions without a local presence.

- Your business does not need a St. Lucian resident to sit on the board. This removes a structural constraint that many jurisdictions impose, where at least one director must be locally domiciled, effectively forcing foreign founders to appoint a nominee they may have limited control over.

- Foreign shareholders face no ownership restrictions under the IBC framework. A non-resident can hold 100% of the shares, which means equity structure and profit distribution remain entirely within the founder's control.

- Because corporate entities can serve as directors, a parent company or holding vehicle incorporated elsewhere can formally manage the IBC. This simplifies governance documentation and reduces the need for individual signatories to appear in multiple jurisdictions.

- Meetings of directors and shareholders may be held outside St. Lucia, with no requirement to conduct formal proceedings on the island. For internationally mobile founders, this means governance obligations do not dictate travel.

Access to CARICOM Trade Agreements

St. Lucia CARICOM trade agreement benefits flow directly from the country's membership in the Caribbean Community, a regional bloc that eliminates tariffs on most goods traded between its 15 member states under the CARICOM Single Market and Economy (CSME). For a business incorporated in St. Lucia, this means your goods can move into markets like Jamaica, Barbados, Trinidad and Tobago, and Guyana without attracting import duties that would otherwise apply to foreign-origin products.

The CSME also grants qualifying businesses the right to establish enterprises and provide services across member states. This free movement of services and capital reduces the structural cost of regional expansion compared to entering each Caribbean market independently through separate foreign incorporation processes.

Eligibility for these benefits is generally tied to meeting CARICOM rules of origin requirements, which determine whether a product qualifies as originating within the bloc.

A manufacturer incorporated in St. Lucia exporting finished goods to three CARICOM markets avoids tariff costs that could represent 10-25% of product value, depending on the category, costs that would apply to the same goods shipped from a non-member jurisdiction.

Beyond goods, CARICOM membership provides access to a combined consumer market of approximately 18 million people, a scale that a single-island domestic market cannot replicate on its own.

Stable Common Law Legal Framework

St. Lucia's legal system is rooted in English common law, inherited through its colonial history and formally maintained through domestic legislation and the Eastern Caribbean Supreme Court (ECSC). For foreign business owners, the St. Lucia common law legal framework advantages are substantive: contract enforcement, property rights, and corporate governance all operate within a body of law that is well-documented, precedent-driven, and familiar to advisors across the UK, Canada, Australia, and other common law jurisdictions.

The ECSC serves as the superior court of record, with appellate jurisdiction sitting in the Eastern Caribbean Court of Appeal. Final appeals proceed to the Privy Council in London. This appellate structure means judicial decisions are subject to oversight from one of the world's most established common law tribunals, which carries real weight when assessing dispute resolution risk for cross-border commercial arrangements.

Because common law systems depend on precedent, your legal counsel can draw on a wide base of comparable rulings from across the Caribbean and beyond. Interpreting contract terms or shareholder rights does not require navigating an unfamiliar civil code system, which reduces legal costs and shortens due diligence timelines.

While the common law framework governs general commercial matters, specific offshore structures registered under the International Business Companies Act are subject to their own statutory rules, which may modify or supplement general common law principles.

Growing Financial Services Infrastructure

St. Lucia financial services infrastructure benefits have expanded considerably over the past two decades, supported by deliberate legislative and institutional development rather than circumstance.

The Financial Services Regulatory Authority (FSRA) oversees the non-banking financial sector, providing a structured supervisory environment for insurance, securities, and international business entities. A dedicated regulatory body of this kind means your company operates within a defined compliance framework, which reduces ambiguity when dealing with counterparties, banks, and correspondent institutions abroad.

The Eastern Caribbean Central Bank (ECCB) governs monetary policy and banking supervision across the Eastern Caribbean Currency Union, of which the island is a member. Membership in this regional central banking structure gives businesses registered here access to a currency union with shared monetary oversight, which carries more institutional credibility than jurisdictions operating entirely outside multilateral financial frameworks.

Domestic banking infrastructure includes both local and internationally affiliated institutions capable of supporting corporate accounts for foreign-owned entities. This matters because access to functional corporate banking is frequently the operational bottleneck for offshore companies, regardless of how favorable the tax or legal environment may be.

The government has also worked toward alignment with international standards set by bodies such as the Financial Action Task Force (FATF) and the OECD, including participation in automatic exchange of information frameworks. For your business, this positions the jurisdiction as one that international banks and regulators recognize as operating within accepted global norms, reducing the friction often encountered when opening correspondent accounts or executing cross-border transactions.

Why St. Lucia Stands Out Among Offshore Jurisdictions

Evaluated against comparable Caribbean offshore jurisdictions, St. Lucia's advantages over other offshore jurisdictions become clearer when specific structural features are placed side by side. The jurisdictions most relevant for comparison are the British Virgin Islands, Belize, and Seychelles — each targets a similar profile of foreign investor, offers IBC-style structures, and competes for the same incorporation mandates. What the comparison reveals is not a dramatic gap on any single point, but a consistent mid-range positioning across tax, privacy, legal framework, and cost that collectively reduces friction for foreign business owners.

Where St. Lucia holds a distinct position is in its combination of Common Law legal tradition, CARICOM membership, and a dedicated IBC Act framework — features that not all competitors share simultaneously. Belize offers lower fees but lacks the same treaty access. The BVI carries higher annual costs and greater regulatory scrutiny following FATF-related reforms. Seychelles competes on price but operates under a civil law hybrid, which can complicate enforcement for common law-trained counsel.

| Parameter | St. Lucia | British Virgin Islands | Belize | Seychelles |

|---|---|---|---|---|

| Corporate Tax on Foreign Income | 0% (IBC) | 0% | 0% | 0% |

| Capital Gains Tax | None | None | None | None |

| Legal System | Common Law | Common Law | Common Law | Mixed (Civil/Common) |

| CARICOM Membership | Yes | No | Yes | No |

| Public Register of Directors | No | Partial (since 2023) | No | No |

| Incorporation Timeframe | 1-3 business days | 3-5 business days | 1-2 business days | 1-3 business days |

| Annual Government Fee | Low-moderate | High | Low | Low |

| Statutory Basis for IBCs | IBC Act (Cap. 12.17) | BVI Business Companies Act | IBC Act | IBC Act 2016 |

Compliance Services for St. Lucia Companies

Maintain your St. Lucia IBC in good standing with annual filings, registered agent requirements, and ongoing regulatory obligations managed by Expanship.

Conclusion

The benefits of incorporating in St. Lucia rest on a combination of structural features that are genuinely useful to foreign business owners: zero capital gains tax under the International Business Companies Act, exemption from foreign exchange controls that allows funds to move without restriction, and a common law legal system that produces predictable, enforceable outcomes for cross-border commercial arrangements.

Fit matters. A holding company with passive investment income will extract different value from this jurisdiction than an active trading firm seeking CARICOM market access. The IBC framework is purpose-built for international operations, but your entity structure, industry classification, and home jurisdiction's controlled foreign corporation rules all affect how these benefits translate in practice.

For businesses whose profile aligns with what the IBC Act was designed to accommodate, St. Lucia offers a legally grounded, cost-efficient foundation for international operations. The next step is structuring your incorporation correctly from the outset, since errors in share structure, registered agent appointment, or compliance timelines under the Financial Services Regulatory Authority's requirements can create downstream complications that are more costly to correct than to prevent.

Let Expanship Handle Your St. Lucia Incorporation

Expanship St. Lucia company incorporation services cover the full scope of what a foreign business owner needs to establish and maintain an International Business Company under the International Business Companies Act. From initial name reservation with the Registrar of International Business Companies to ongoing statutory compliance, the firm's work is grounded in the specific regulatory requirements discussed throughout this blog.

- Preparation and legalization of incorporation documents, including the Memorandum and Articles of Association

- Provision of a registered agent and registered office address, as required under the IBC Act

- Filing and liaison with the Registrar of International Business Companies on your behalf

- Post-incorporation compliance management, including annual return filings and record maintenance

- Banking introduction assistance to support your firm's operational setup following registration

Professional St. Lucia offshore incorporation support from a specialist removes the friction that arises when navigating a foreign regulatory environment without local contacts or procedural familiarity. Each service is handled by personnel with direct knowledge of the processes described in this blog, from confidentiality provisions to CARICOM-adjacent trade positioning.

Reach out to Expanship St. Lucia to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

IBCs incorporated under the International Business Companies Act are subject to a low flat-rate corporate income tax rather than a tiered progressive system. The rate is fixed and applied uniformly regardless of profit level, which allows for predictable tax planning. Capital gains and inheritance transfers are not subject to additional taxation under the current regime.

Registration under the International Business Companies Act can typically be completed within a few business days once all required documentation has been submitted to the Registered Agent. The timeline depends on document preparation and the accuracy of the submitted information. No government pre-approval or extended review process is standard for routine IBC formations.

No foreign exchange controls apply to IBCs, meaning funds can be transferred internationally without regulatory restrictions on currency conversion or repatriation. This applies to both capital movements and profit distributions. The absence of exchange controls is codified in the treatment of IBCs under local financial legislation rather than relying on general discretionary policy.

CARICOM membership extends certain trade and economic cooperation benefits to businesses operating within member states, though the extent to which an IBC structured for offshore purposes can access preferential tariff arrangements depends on the nature of its activities and whether it conducts trade within the region. IBCs primarily engaged in international transactions outside the CARICOM market may have limited access to intra-regional trade preferences. Businesses intending to use CARICOM agreements operationally should assess their corporate structure against the specific agreement terms.

The International Business Companies Act provides for confidentiality of shareholder and director information, which is not publicly disclosed in the commercial registry in the same manner as domestic companies. Statutory protections limit third-party access to beneficial ownership information outside of legally prescribed circumstances. These provisions, combined with the common law framework governing contractual and fiduciary obligations, form the basis of the jurisdiction's asset protection structure.

Contracts executed by an IBC are governed by a common law system derived from English legal tradition, which means established principles of contract formation, enforcement, and interpretation apply. Courts interpret commercial agreements using precedents consistent with other common law jurisdictions, which can simplify cross-border dispute resolution for counterparties familiar with English law. This legal continuity reduces interpretive uncertainty compared to civil law systems that apply different doctrinal standards.

The jurisdiction has developed a regulated financial services sector that includes licensed banking institutions, corporate service providers, and registered agents authorized to support IBC administration. The Financial Services Regulatory Authority oversees licensing and compliance within this sector. While the infrastructure is smaller in scale than major financial centers, it is sufficient to support account opening, corporate maintenance, and professional service requirements for most standard IBC structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.