Key Takeaways

- The Private Limited Company (Co., Ltd.) is Cambodia's most commonly registered entity form, offering defined liability boundaries and permissive foreign ownership rules under the Law on Commercial Enterprises.

- Company registration in Cambodia falls under the Ministry of Commerce's Business Registration Department, with sector-specific licensing required from bodies such as the National Bank of Cambodia for financial services.

- Branch offices and representative offices allow foreign firms to establish a market presence in Cambodia without undertaking full local incorporation.

- Cambodia operates a territorial tax system, under which only locally sourced income is generally subject to domestic tax obligations administered by the General Department of Taxation.

Introduction to Entity Types in Cambodia

Located in Southeast Asia, Cambodia shares borders with Thailand, Laos, and Vietnam, with coastal access to the Gulf of Thailand. It is an independent nation governed as a constitutional monarchy under the 1993 Constitution.

Company registration falls under the jurisdiction of the Ministry of Commerce, which administers business formation through its Business Registration Department. Depending on the activity, additional licensing may be required from sector-specific regulators such as the National Bank of Cambodia for financial services entities.

Cambodia operates a territorial tax system, meaning only locally sourced income is generally subject to domestic tax obligations.

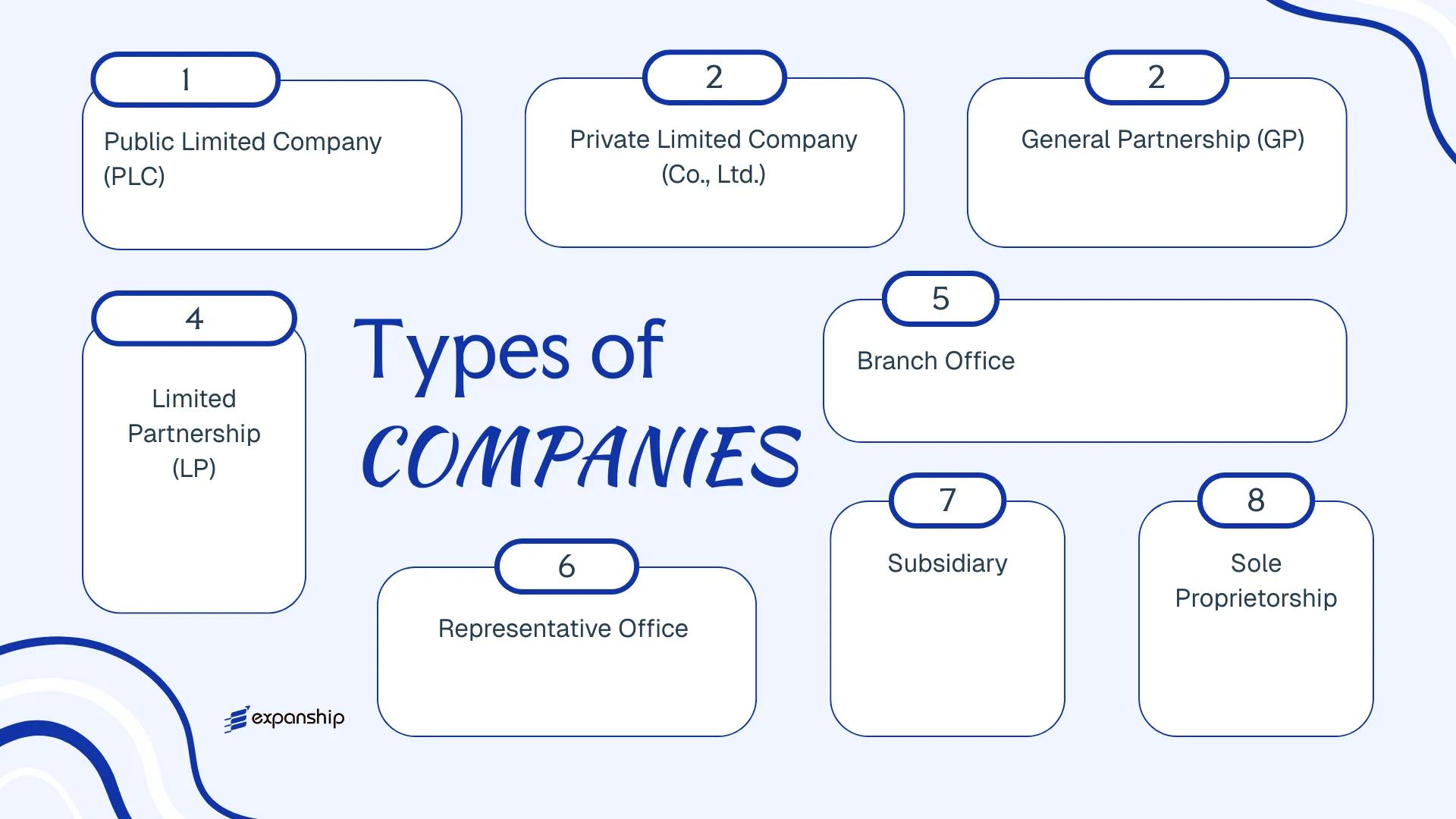

Businesses registering in the country may structure their presence through the following legal forms:

- Public Limited Company (PLC)

- Private Limited Company (Co., Ltd.)

- General Partnership

- Limited Partnership

- Branch Office

- Representative Office

- Subsidiary

- Sole Proprietorship

Each structure carries distinct implications for liability, ownership, governance, and compliance — this article examines each in detail to help you determine which option suits your operational requirements.

An Overview of Business Structures in Cambodia

Under the Cambodian corporate framework, businesses can be established through several distinct legal forms. The primary legislation governing most commercial entities is the Law on Commercial Enterprises (LCE), with supplementary regulations issued by the Ministry of Commerce and the General Department of Taxation. Each structure carries different rules on liability, ownership, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited to shares | Taxed | Yes | 2 shareholders | Ministry of Commerce | Law on Commercial Enterprises |

| Private Limited Company (Co., Ltd.) | Incorporated company | Limited to shares | Taxed | Yes | 1 shareholder | Ministry of Commerce | Law on Commercial Enterprises |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | Ministry of Commerce | Law on Commercial Enterprises |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | Ministry of Commerce | Law on Commercial Enterprises |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Restricted | N/A | Ministry of Commerce | Law on Commercial Enterprises |

| Representative Office | Non-trading presence | Parent liable | Exempt from profit tax | No | N/A | Ministry of Commerce | Sub-decree on Rep. Offices |

| Sole Proprietorship | Individual trader | Unlimited | Taxed | Yes | 1 owner | Ministry of Commerce | Law on Commercial Enterprises |

Each of these structures is examined in full in the sections below.

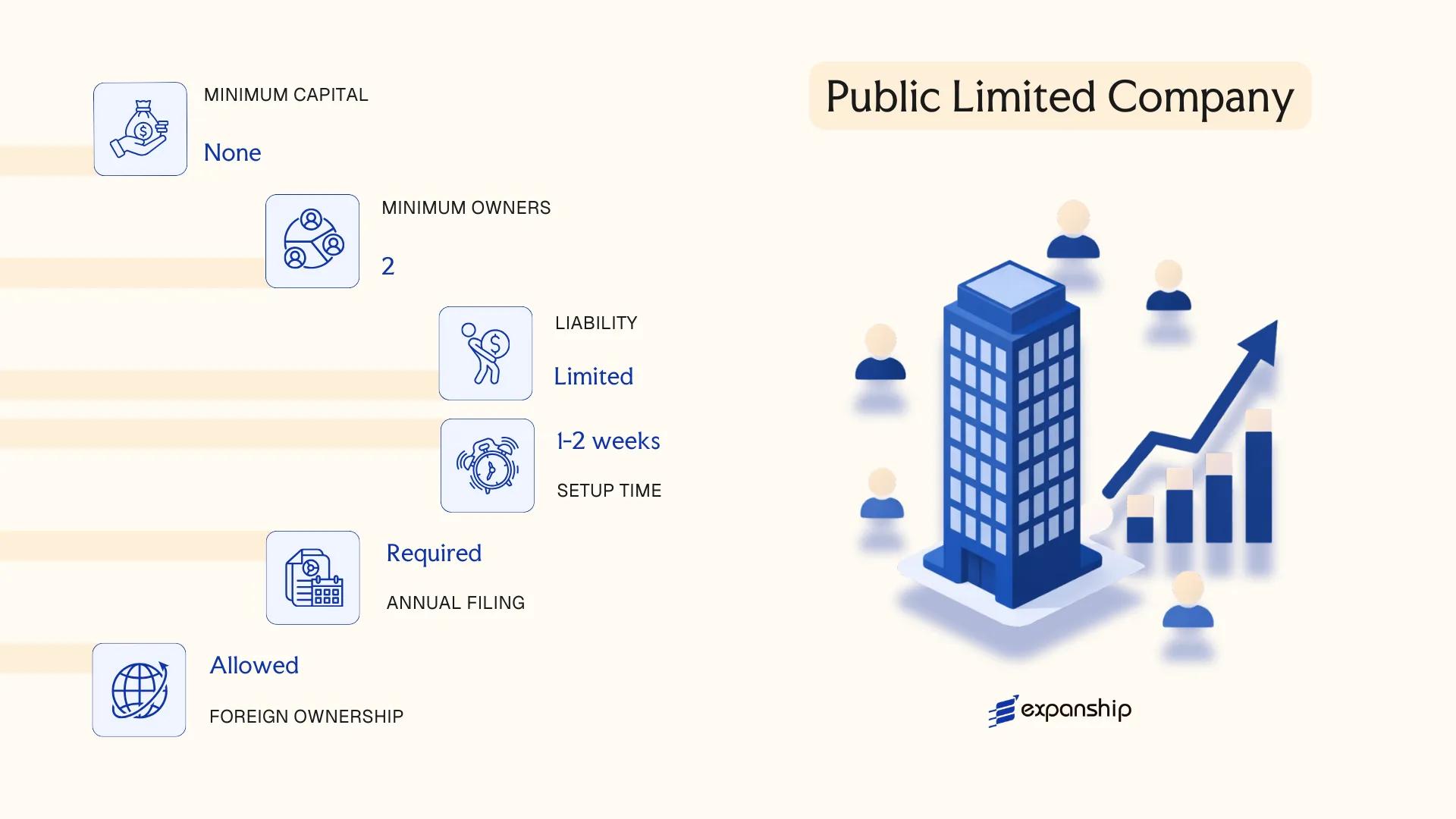

Public Limited Company (PLC) under the Law on Commercial Enterprises

Governed by the Law on Commercial Enterprises (LCE) of 2005, a Cambodia Public Limited Company PLC registration produces a distinct legal entity separate from its shareholders. Shares may be offered to the public, which distinguishes this structure from its private counterpart.

A PLC carries limited liability for all shareholders, meaning personal assets remain insulated from corporate obligations. The entity can list on the Cambodia Securities Exchange (CSX), making it the primary vehicle for firms seeking public capital markets access.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; governed by the LCE 2005 |

| Members | Shareholders (min. 2, no maximum); Board of Directors (min. 3 directors) | Shareholders and directors may be foreign nationals |

| Capital | No statutory minimum share capital under the LCE; par value per share must be stated | CSX listing imposes additional capital and free-float requirements |

| Local Presence | Registered address in Cambodia required; no mandatory resident director under the LCE | A local registered agent is advisable for compliance filings |

| Share Transferability | Shares freely transferable; public offerings permitted | Transfers subject to CSX rules if listed |

| Privacy | Shareholder and director details filed with the Ministry of Commerce; publicly accessible | No beneficial ownership anonymity |

Focus Points

- Taxation: Subject to a 20% corporate income tax rate; VAT applies at 10% on taxable supplies; dividend withholding tax of 14% applies to distributions; subject to General Department of Taxation obligations including monthly and annual filing requirements.

- Annual Compliance: Mandatory audited financial statements; annual general meeting required; filings with both the Ministry of Commerce and the General Department of Taxation.

- CSX Listing: Listing requires approval from the Securities and Exchange Regulator of Cambodia (SERC) and compliance with ongoing disclosure obligations.

- Restrictions: Certain sectors require additional licenses or impose foreign ownership caps regardless of entity type.

- Conversion: A PLC may be converted from a private limited company upon meeting public company thresholds under the LCE.

Closing

A PLC suits businesses seeking to raise capital from the public or pursue a CSX listing, though the governance and disclosure requirements make it administratively demanding relative to other structures. The obligation to hold public shareholder meetings and file audited accounts annually adds compliance overhead that smaller operations are unlikely to absorb efficiently.

This entity type is most appropriate for large enterprises or growth-stage firms planning to access public equity markets through the Cambodia Securities Exchange.

Company Incorporation in Cambodia

Expanship assists with end-to-end company registration in Cambodia, including PLC formation, Ministry of Commerce filings, and ongoing compliance support.

Private Limited Company (Co., Ltd.) under the Law on Commercial Enterprises

The Private Limited Company, known locally as a Co., Ltd., is the most widely used structure for Cambodia private limited company Co Ltd formation. Governed by the Law on Commercial Enterprises (LCE), enacted in 2005 and administered by the Ministry of Commerce, it carries separate legal personality distinct from its shareholders.

Liability is capped at each member's capital contribution, and the entity functions as Cambodia's functional equivalent of an LLC. Shares in a Co., Ltd. are not freely transferable without existing shareholder consent, which keeps ownership structures tightly controlled.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Co., Ltd.) | Governed under LCE 2005; separate legal personality |

| Members | Shareholders: 1–30 | Cannot exceed 30; a single-member Co., Ltd. is permitted |

| Management | Minimum 1 Director; no maximum | Director need not be a shareholder or resident |

| Local Presence | Registered address in Cambodia required | Physical office address; registered agent not mandated by law |

| Capital | No statutory minimum for most sectors; denominated in KHR or USD | Certain licensed sectors impose minimum paid-up capital thresholds |

| Share Transferability | Restricted; requires shareholder approval | Articles of association govern transfer procedures |

| Privacy | Shareholder register filed with Ministry of Commerce | Register is not fully public but available to authorities |

Focus Points

- Taxation: Subject to 20% corporate income tax (with a 0% QIP incentive period available); standard VAT at 10%; withholding tax on dividends, interest, and royalties at rates of 14%, 15%, and 15% respectively; stamp duty applies on certain instruments.

- Annual Compliance: Annual tax returns filed with the General Department of Taxation; audited financial statements required; patent tax (annual business registration fee) payable to the tax authority.

- Economic Substance: No formal economic substance regime comparable to offshore jurisdictions; however, tax residency determinations may require demonstrating management and control within Cambodia.

- Treaty Access: Eligible to benefit from Cambodia's double taxation agreements, including treaties with Singapore, Brunei, and China, subject to meeting residency requirements.

- Restrictions: Foreign ownership is generally permitted, but land ownership is constitutionally prohibited for foreign-owned entities; certain sectors require majority Khmer ownership or prior approval.

Closing

A Co., Ltd. suits trading operations, holding structures, and service businesses requiring a locally recognised, liability-protected entity with a controlled shareholder base. The capped membership at 30 shareholders limits scalability for businesses seeking broader equity participation.

This structure fits foreign investors and SMEs establishing operational or holding businesses in Cambodia with a defined, small group of shareholders.

Partnerships in Cambodia [General Partnership, Limited Partnership]

Governed by the Law on Commercial Enterprises (LCE), Cambodia general and limited partnership registration follows a codified framework that distinguishes between two structurally distinct partnership forms. Both types are recognised legal entities under the LCE, registered with the Ministry of Commerce.

Unlike a private limited company, neither partnership form separates ownership from management through shareholding structures. The partners bear varying degrees of liability depending on the partnership type selected.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (General or Limited) | Registered under the Law on Commercial Enterprises |

| Members | General Partners: minimum 2, no maximum; Limited Partners (LP only): minimum 1 | General partners manage operations; limited partners are passive investors |

| Liability | General partners: unlimited personal liability; Limited partners: liability capped at capital contribution | Mixed liability structure applies to limited partnerships |

| Local Presence | Registered office address in Cambodia required | No statutory requirement for a local resident partner, though general partners bear full liability |

| Capital | No statutory minimum; denominated in Khmer Riel or USD in practice | Capital contributions recorded in the partnership agreement |

| Privacy | Partner names disclosed to Ministry of Commerce | No public register equivalent to a company shareholding registry |

Focus Points

- Taxation: Partnerships are generally taxed as pass-through entities or subject to Tax on Income under the General Department of Taxation; VAT registration applies if annual turnover exceeds the threshold; withholding tax applies to distributions to non-resident partners.

- Annual Compliance: Annual patent tax filing and financial statements required; general partners remain personally liable for compliance failures.

- Treaty Access: Access to Cambodia's tax treaties depends on partner residency and entity classification; limited partnerships may face restricted treaty benefits.

- Restrictions: Foreign nationals acting as general partners face scrutiny under land ownership and sector-specific regulations.

- Conversion: Conversion to a private limited company is possible but requires a formal restructuring process through the Ministry of Commerce.

Sub-Types

General Partnership

All partners hold equal management authority and bear unlimited joint and several liability for the firm's obligations. This structure suits small domestic ventures where partners have an established trust relationship.

Limited Partnership

At least one general partner retains unlimited liability and management control, while limited partners contribute capital without participating in daily management. This form suits investment arrangements where passive contributors seek liability protection.

Closing

Partnerships suit smaller domestic operations or investment arrangements where formal corporate governance overhead is unnecessary. The simplified setup is offset by the exposure of general partners to unlimited personal liability, which presents significant risk for commercially active businesses.

Partnerships under the LCE are best suited for domestic joint ventures or capital-pooling arrangements between parties with an established working relationship, rather than foreign-owned commercial operations.

Foreign Business Presence in Cambodia [Branch Office, Representative Office, Subsidiary]

A foreign company branch office Cambodia setup is governed primarily by the Law on Commercial Enterprises (2005) and administered through the Ministry of Commerce. Foreign entities seeking to operate in the Kingdom without forming a new locally incorporated company have three structural options: a branch office, a representative office, or a subsidiary. Each carries distinct legal implications, particularly around legal personality and liability exposure.

A branch office is not a separate legal entity — the parent company bears full liability for its obligations. A subsidiary, incorporated as a private limited company under Cambodian law, holds separate legal personality. Representative offices occupy the most restricted position, prohibited from generating direct revenue.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary (Co., Ltd.) |

|---|---|---|---|

| Legal Form | Extension of foreign parent | Non-trading extension of parent | Separate legal entity |

| Liability | Parent bears full liability | Parent bears full liability | Limited to entity's own capital |

| Permitted Activities | Commercial operations | Liaison and market research only | Full commercial operations |

| Registered Office | Required in Cambodia | Required in Cambodia | Required in Cambodia |

| Capital | No statutory minimum | No statutory minimum | No statutory minimum (KHR equivalent) |

| Privacy | Parent's details disclosed | Parent's details disclosed | Shareholder register filed with MoC |

Focus Points

- Taxation: Branch offices are subject to the standard 20% corporate income tax on Cambodian-sourced profits; representative offices pay a flat annual patent tax but are not subject to profit tax if non-revenue-generating; subsidiaries are taxed at 20% CIT, with VAT at 10% and withholding tax on dividends at 14%.

- Treaty Access: Subsidiaries incorporated locally may access Cambodia's limited double tax treaty network; branches generally access treaties only where the parent's home jurisdiction treaty provisions extend to permanent establishments.

- Annual Compliance: All three structures must renew their patent tax registration annually with the General Department of Taxation and maintain updated filings with the Ministry of Commerce.

- Activity Restrictions: Representative offices cannot invoice clients, execute sales contracts, or repatriate commercial profits — violations risk dissolution of the registration.

- Conversion: A branch office cannot be converted directly into a subsidiary without winding down the branch and separately incorporating a new entity under the Law on Commercial Enterprises.

Sub-Types

Branch Office

A branch office is registered with the Ministry of Commerce and must appoint a local representative authorised to act on behalf of the foreign parent. It is suited for foreign firms wishing to conduct revenue-generating activities without establishing a locally owned entity.

Representative Office

Registered through the Ministry of Commerce and renewed annually, a representative office is restricted to promotional, liaison, and market intelligence functions. Foreign companies typically use this structure during a preliminary assessment phase before committing to full incorporation.

Subsidiary

Incorporated as a private limited company under Cambodian law, a subsidiary is operationally and legally independent of its foreign parent. This structure is used when the foreign investor requires full operational capacity, local contract authority, and access to government tenders.

Closing

Foreign companies engaged in active trading or requiring local contract authority will find the subsidiary the most operationally complete structure, though it requires full compliance with Cambodian corporate governance requirements. Representative offices, by contrast, offer a low-cost market entry point but cannot generate direct revenue.

Representative offices suit foreign firms in an exploratory phase; branches and subsidiaries are appropriate for those committed to active commercial operations in Cambodia.

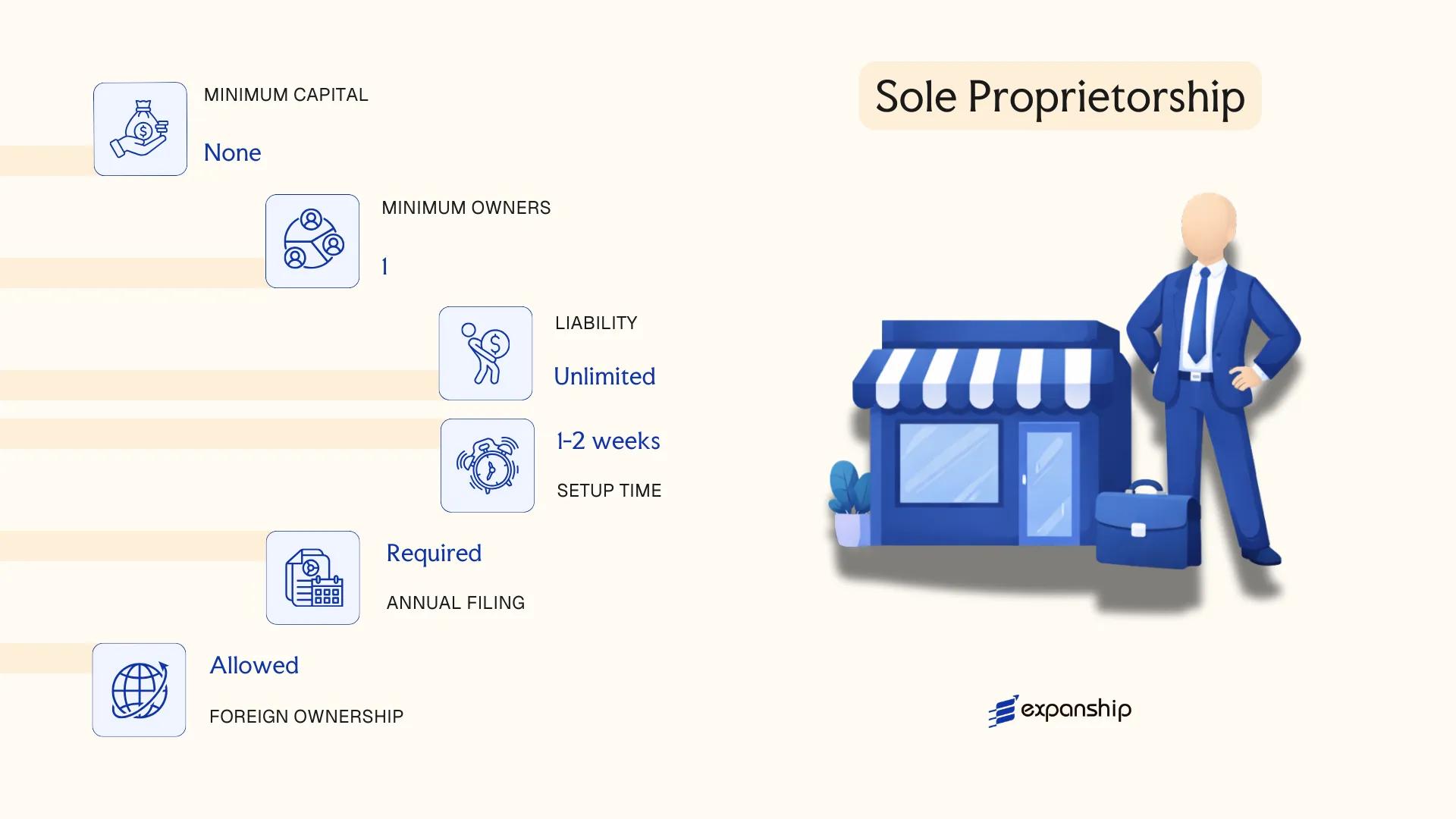

Sole Proprietorship

Sole proprietorship registration in Cambodia is governed by the Law on Commercial Enterprises (2005) and administered through the Ministry of Commerce. Unlike a private limited company, a sole proprietorship does not constitute a separate legal entity — the owner and the business are treated as one and the same under Cambodian law.

This structure carries unlimited personal liability, meaning your personal assets are exposed to any debts or legal claims arising from business operations. Registration is completed through the Ministry of Commerce's business registration portal, and the proprietor must also register with the General Department of Taxation for tax purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Unincorporated) | No separate legal personality from the owner |

| Member Type | Proprietor | Single individual only; no partners or shareholders |

| Ownership | 1 proprietor (maximum 1) | Foreign nationals face restrictions on permitted business activities |

| Local Presence | Registered business address required | Must maintain a physical address in Cambodia |

| Capital | No statutory minimum (KHR/USD accepted) | Capital is not formally subscribed or issued |

| Liability | Unlimited personal liability | Owner's personal assets are at risk |

Focus Points

- Taxation: Subject to income tax on profit (20% standard rate for businesses above the threshold, or a simplified regime for small taxpayers); VAT registration required if annual turnover exceeds KHR 250 million; no withholding tax at entity level on distributions since profits flow directly to the owner.

- Annual Compliance: Annual patent tax renewal with the Ministry of Economy and Finance; annual tax on income filing with the General Department of Taxation.

- Foreign Ownership Restrictions: Foreign nationals cannot operate a sole proprietorship in sectors reserved for Cambodian citizens under the Law on Investment and relevant sub-decrees.

- Conversion: Can be converted into a private limited company through a new incorporation process; there is no direct statutory conversion mechanism.

- Treaty Access: As an unincorporated entity, access to Cambodia's double tax agreements is generally unavailable or limited compared to incorporated structures.

Closing Paragraph

A sole proprietorship suits small-scale, locally owned service businesses or individual traders with minimal compliance budgets, but the absence of limited liability makes it unsuitable for any operation carrying meaningful commercial or financial risk.

Cambodian nationals operating small, low-risk trading or service businesses who prioritise simplicity over liability protection.

How to Choose the Right Entity Type in Cambodia

Knowing how to choose a business entity in Cambodia requires more than comparing registration fees. The structure you select has direct legal, tax, and operational consequences that are difficult to reverse once the entity is active.

Why Your Entity Choice Matters

The wrong structure creates concrete problems:

- If you register a foreign-owned entity without fulfilling the local business licensing requirements under the Law on Commercial Enterprises, your operations may be deemed unlawful, exposing the business to penalties or forced dissolution.

- Choosing a structure that falls outside Cambodia's tax treaty eligibility criteria means you cannot claim reduced withholding tax rates available under bilateral agreements with treaty partner countries.

- Forming a company when a partnership arrangement better reflects your operational reality locks you into annual general meeting obligations, formal share capital requirements, and shareholder reporting duties that partnerships do not carry.

- Selecting an entity without the capacity to demonstrate genuine local substance — employees, a registered office, management decisions made in-country — can trigger compliance failures under applicable tax residency assessments.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require distinct structures under Cambodian law.

- Ownership Configuration: Single-owner operations and multi-party ventures have different governance implications, particularly around share transfer rights and decision-making authority.

- Tax Position: Your eligibility for Cambodia's tax treaty network, the QIP incentive regime, or standard profit tax treatment depends in part on which entity type you register.

- Substance Capacity: If you cannot maintain a physical presence with staff and local decision-making, your entity selection must account for that limitation from the outset.

- Exit and Continuity: Not all Cambodian entity types support redomiciliation or straightforward conversion; your intended exit route should inform your initial structure.

Compliance Services for Companies in Cambodia

Ongoing compliance support for Cambodian entities, including annual filing, statutory obligations, and regulatory reporting.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a company in Cambodia guide, and it shapes everything from liability exposure to tax treatment under the Law on Commercial Enterprises and the General Department of Taxation's filing requirements.

The Private Limited Company remains the most registered entity form, favored by foreign investors for its defined liability boundaries and permissive foreign ownership rules. A Public Limited Company suits firms seeking public capital markets. General and Limited Partnerships serve smaller domestic operations where partners accept shared governance. Branch offices and representative offices address foreign firms testing market presence without full local incorporation. Sole proprietorships carry unlimited personal liability, limiting their practical use.

Registration oversight sits with the Ministry of Commerce, and ongoing compliance runs through multiple agencies. Cambodia's expanding tax treaty network and improving regulatory transparency suggest the environment for foreign-owned entities will continue to develop in structured, predictable directions.

How Expanship Can Assist You

Expanship's Cambodia company incorporation services cover the full arc of entity formation in the Kingdom — from selecting between a Private Limited Company (Co., Ltd.) and a Public Limited Company (PLC) under the Law on Commercial Enterprises, to fulfilling post-registration obligations with the Ministry of Commerce and the General Department of Taxation.

From the outset, your business benefits from a structured process with no gaps in responsibility. Our corporate services in Cambodia include:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the Ministry of Commerce

- Tax registration with the General Department of Taxation

- Ongoing compliance management, including annual patent tax renewals

- Banking introduction assistance for corporate account opening

Reach out to our team through Expanship Cambodia to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Private Limited Company (Co., Ltd.) is the most frequently registered structure under the LCE. Its combination of limited liability, a single-shareholder minimum, and no public share offering requirement makes it suitable for a wide range of businesses, from small domestic operations to foreign-owned subsidiaries.

A Branch Office is not a separate legal entity from its foreign parent, meaning the parent bears full liability for the branch's obligations in Cambodia. A Private Limited Company, by contrast, holds independent legal personality and limits shareholder exposure to paid-in capital. The Co., Ltd. is generally subject to the same Tax on Income rate as a branch, but it offers greater structural flexibility for reinvesting profits or adding local shareholders.

Among registered structures under the LCE, the Private Limited Company offers relatively limited public disclosure compared to a Public Limited Company, whose shareholder register and financial statements face broader scrutiny. Nominee director and shareholder arrangements are legally permissible, though the General Department of Taxation (GDT) and the MoC retain access to beneficial ownership records. No structure provides complete anonymity under current regulations.

A sole proprietorship and a Private Limited Company can each be formed by one individual. General Partnerships and Limited Partnerships require at least two partners under the LCE. A Public Limited Company requires a minimum of two shareholders, a board of directors, and an audit committee, placing it beyond the reach of a single-person founding structure.

Foreigners may register a Private Limited Company, Public Limited Company, Branch Office, or Representative Office. Foreign ownership of a Co., Ltd. is permitted up to 100% in most sectors, subject to sector-specific restrictions under Cambodia's investment laws and the Cambodia Investment Board (CIB) framework. Land ownership restrictions may affect certain entity strategies in the real estate sector.

The LCE permits restructuring between certain forms, such as converting a Private Limited Company into a Public Limited Company, subject to MoC approval and compliance with minimum capital and governance requirements. Conversion from a partnership to a corporate structure is generally achievable through re-registration rather than a direct statutory conversion process. Any structural change requires updated registration filings with the MoC.

No. A Branch Office and Representative Office lack separate legal personality and are treated as extensions of their foreign parent companies. The Co., Ltd., PLC, General Partnership, and Limited Partnership each hold distinct legal standing under the LCE, though partnerships expose general partners to unlimited personal liability for firm obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.