Key Takeaways

- Croatia recognises eight distinct business entity types under the Zakon o trgovačkim društvima, ranging from the capital-intensive d.d. to the low-barrier j.d.o.o., each carrying different liability, governance, and capital requirements.

- The Croatian Commercial Court Registry (Sudski registar) administers all entity registrations, and its ongoing digitisation has reduced procedural friction for incorporations in recent years.

- Foreign businesses can establish a presence in Croatia without creating a separate legal person by registering a branch office or representative office under Croatian law.

- EU membership since 2013 means Croatian corporate governance requirements continue to be shaped by EU regulatory directives, adding a supranational compliance layer alongside domestic company law.

Introduction to Entity Types in Croatia

Located in southeastern Europe, Croatia shares borders with Slovenia, Hungary, Serbia, Bosnia and Herzegovina, and Montenegro, with its western edge fronting the Adriatic Sea. An independent republic and European Union member state since 2013, it operates within EU regulatory frameworks while maintaining its own domestic company law under the Zakon o trgovačkim društvima (Companies Act).

Company registration is administered by the Croatian Commercial Court Registry (Sudski registar), which maintains records of all legal entities incorporated under Croatian law. The country applies a standard corporate tax regime, with rates and territorial rules governed by the Zakon o porezu na dobit.

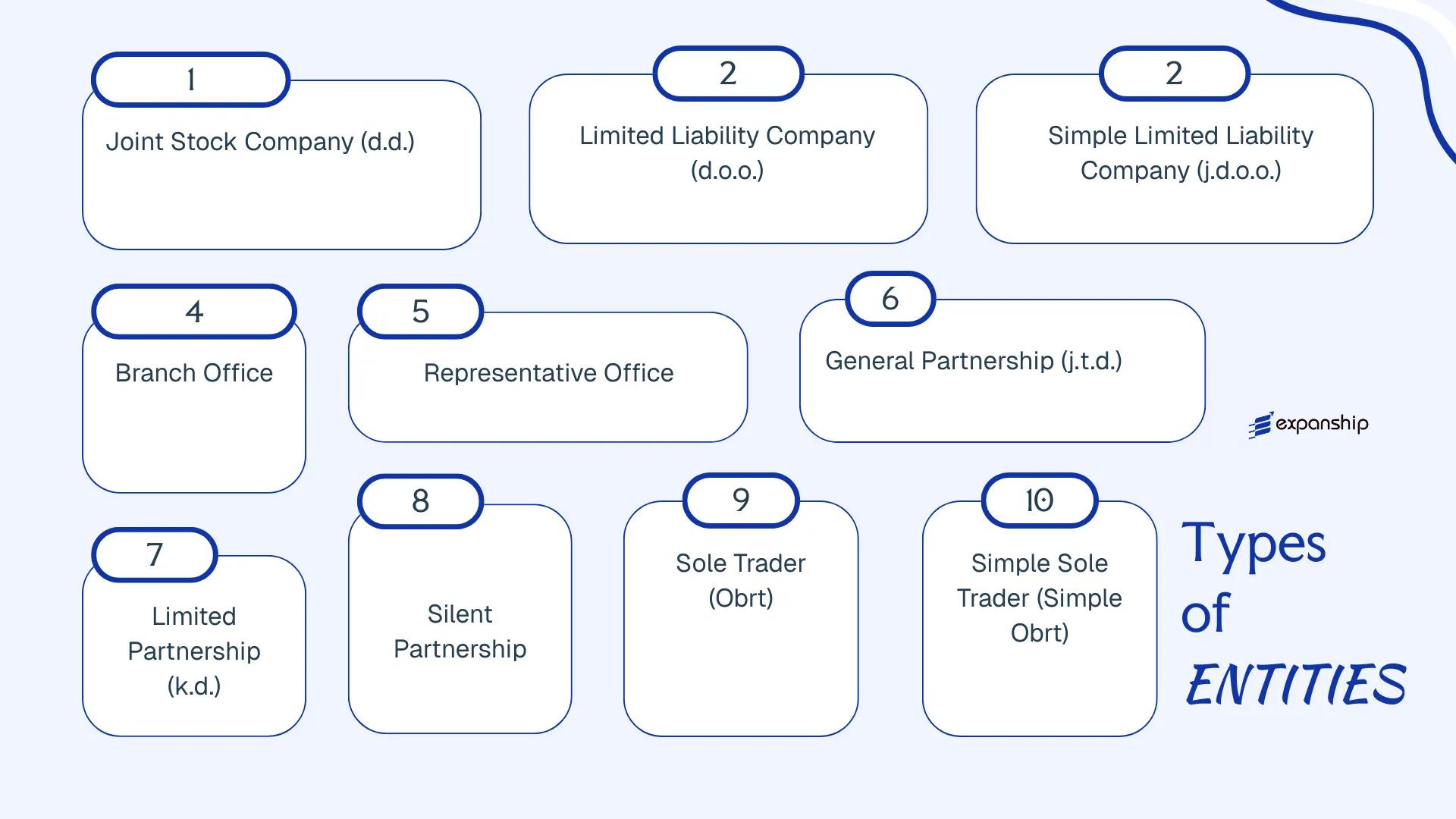

Several distinct legal entity types are available to those looking to establish a business presence, including the d.d., d.o.o., j.d.o.o., branch office, representative office, j.t.d., k.d., silent partnership, and the sole trader structures Obrt and Simple Obrt. Each carries different requirements around capital, liability, governance, and regulatory obligations. This article examines each structure in detail so you can assess which best suits your operational and ownership objectives.

An Overview of Business Structures in Croatia

Croatian company law recognises several distinct entity types, each governed primarily by the Companies Act (Zakon o trgovačkim društvima, ZTD), which consolidates the rules on formation, governance, and dissolution across all commercial structures. An overview of business structures in Croatia shows that available forms range from capital companies with formal governance requirements to simplified sole-trader registrations. Each structure carries a different liability profile, capital threshold, and operational scope.

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| d.d. | Joint Stock Company | Limited | Taxable | Yes | 1 shareholder | Court Registry | ZTD |

| d.o.o. | Limited Liability Co. | Limited | Taxable | Yes | 1 member | Court Registry | ZTD |

| j.d.o.o. | Simple LLC | Limited | Taxable | Yes | 1–3 members | Court Registry | ZTD |

| j.t.d. | General Partnership | Unlimited | Taxable | Yes | 2+ partners | Court Registry | ZTD |

| k.d. | Limited Partnership | Mixed | Taxable | Yes | 2+ partners | Court Registry | ZTD |

| Silent Partnership | Contractual | Limited (silent) | Taxable | No | 2 parties | N/A | ZTD |

| Branch Office | Foreign branch | Parent liable | Taxable | Yes | N/A | Court Registry | ZTD |

| Representative Office | Non-trading unit | Parent liable | Exempt | No | N/A | Ministry of Economy | ZTD |

| Obrt | Sole Trader | Unlimited | Taxable | Yes | 1 individual | Crafts Register | Crafts Act |

| Simple Obrt | Simplified Sole Trader | Unlimited | Taxable | Yes | 1 individual | Crafts Register | Crafts Act |

Each of these structures is examined in full in the sections below.

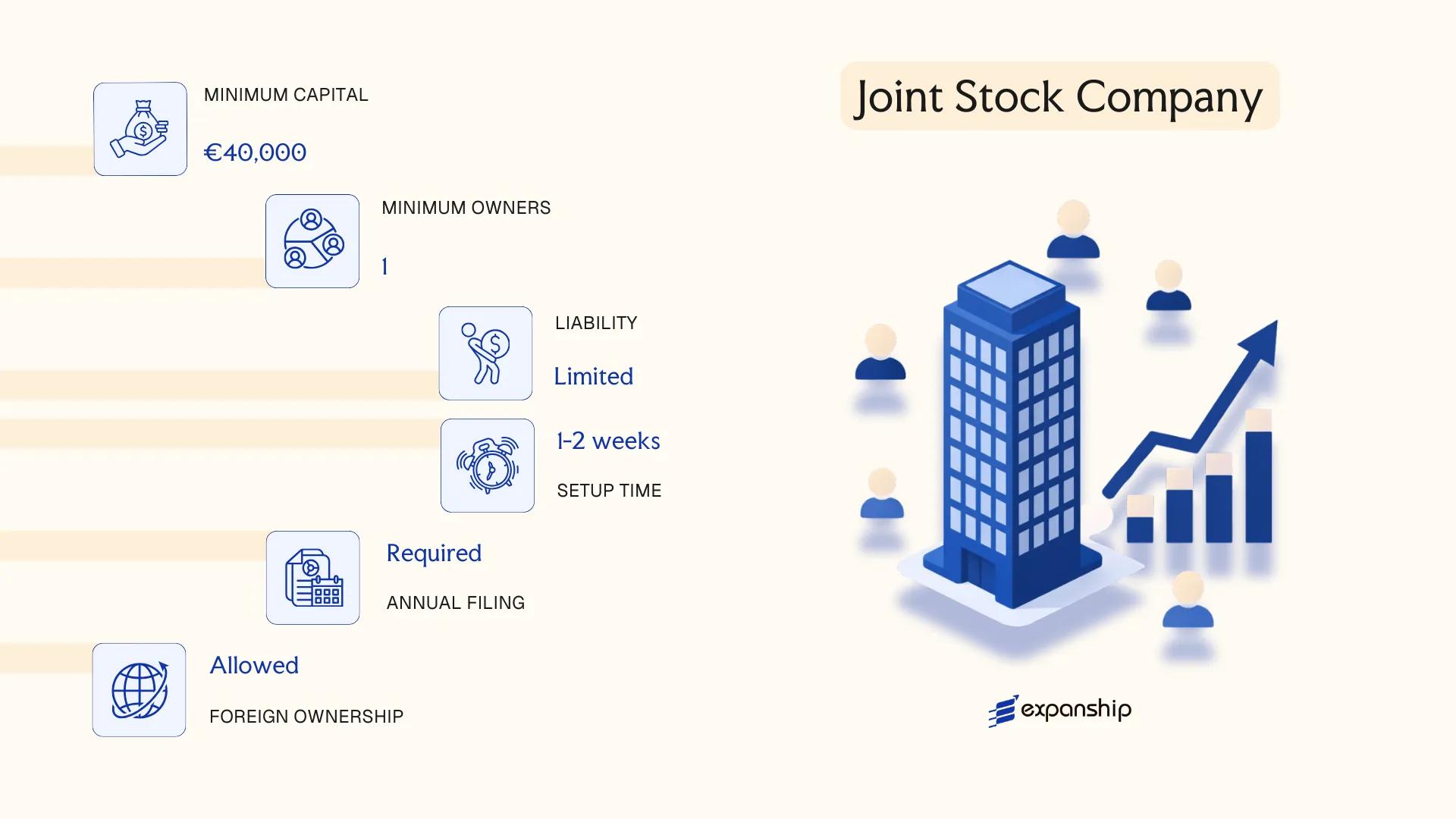

Dioničko Društvo (d.d.) – Joint Stock Company

Governed by the Companies Act (Zakon o trgovačkim društvima, ZTD), the dioničko društvo d.d. Croatia joint stock company structure carries full legal personality, meaning the entity holds rights and obligations independently of its shareholders. Liability is limited to the company's assets.

Share capital is divided into transferable shares, which may be listed on the Zagreb Stock Exchange (ZSE) if the firm meets applicable listing requirements under the Capital Market Act (Zakon o tržištu kapitala).

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (d.d.) | Separate legal personality; regulated under ZTD |

| Governing Bodies | Management Board (Uprava), Supervisory Board (Nadzorni odbor), General Assembly | Two-tier board structure is mandatory |

| Shareholders | Minimum 1; no maximum | Shares may be registered or bearer (restrictions apply) |

| Local Presence | Registered office address in Croatia required | No statutory requirement for a local director, but the management board must be reachable |

| Share Capital | Minimum HRK 200,000 (approx. EUR 26,500); denominated in EUR following euro adoption | At least one-quarter of each share's nominal value must be paid up at registration |

| Privacy | Shareholders and board members disclosed in the court register (sudski registar) | Register is publicly accessible via e-Tvrtka portal |

Focus Points

- Taxation: Subject to 20% corporate income tax (10% for small taxpayers below HRK 7.5m revenue); standard VAT at 25%; withholding tax on dividends at 10% (treaty reductions available); no stamp duty on share transfers in most cases.

- Annual compliance: Mandatory audited financial statements for public companies and large entities; filed with the Financial Agency (FINA); annual general assembly required.

- Treaty access: As an EU member state, Croatia's treaty network covers 60+ bilateral double tax agreements; d.d. entities qualify fully.

- Conversion: A d.d. may be converted into a d.o.o. or other recognised form under ZTD, subject to shareholder resolution and court registration.

- Securities regulation: Public d.d. entities fall under oversight of the Croatian Financial Services Supervisory Agency (HANFA).

Closing

The d.d. is most commonly used for large-scale trading operations, companies seeking external capital, or businesses planning a public listing. The freely transferable share structure supports institutional investment, though the minimum capital requirement and mandatory two-tier governance make it disproportionate for smaller operations.

Large enterprises, companies pursuing public equity financing, or businesses where transferable share structures and institutional shareholder arrangements are operationally necessary.

Company Incorporation in Croatia

Incorporate a d.d. or other Croatian entity with end-to-end support across registration, compliance, and ongoing corporate maintenance.

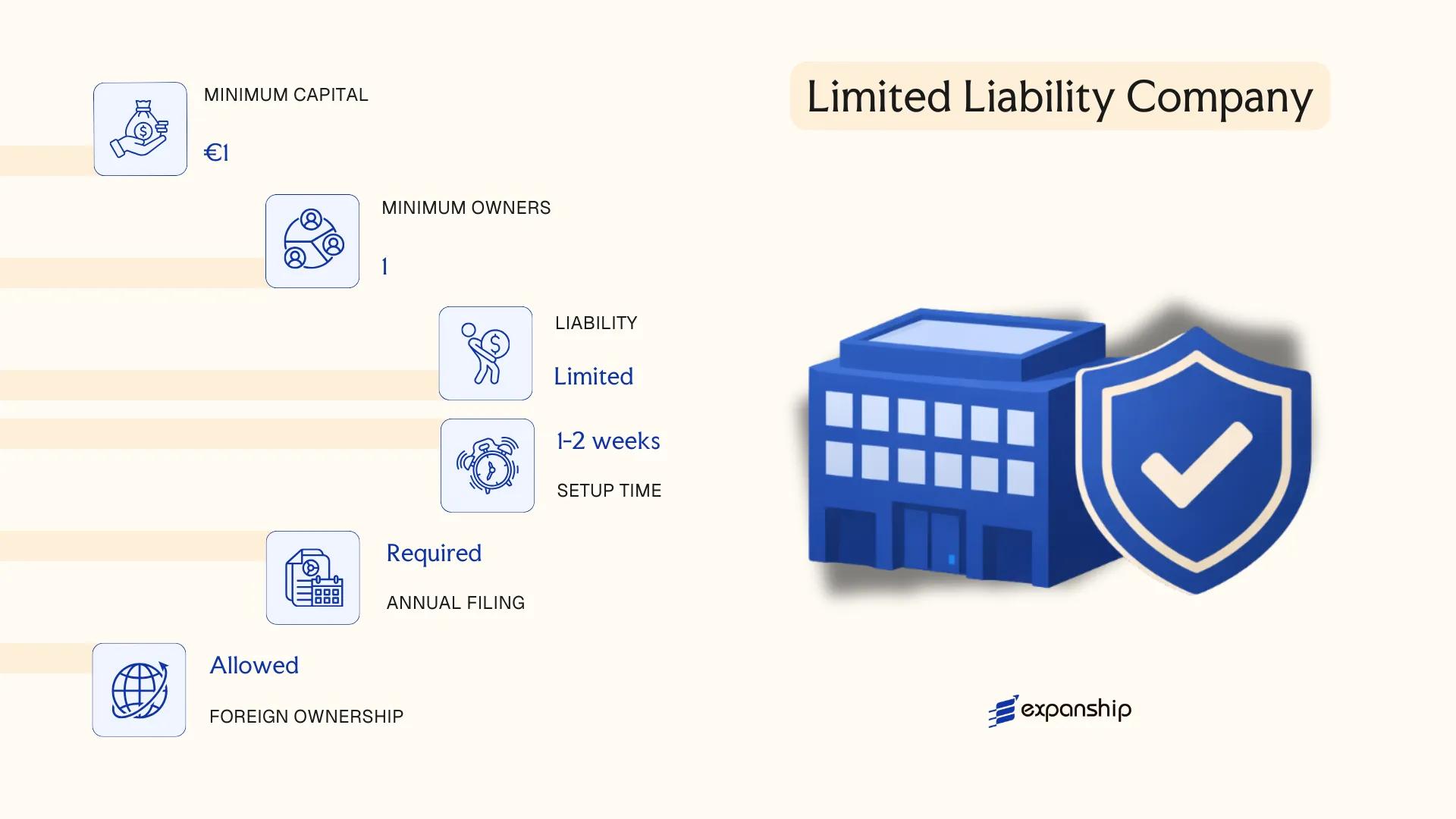

Društvo s Ograničenom Odgovornošću (d.o.o.) – Limited Liability Company

The društvo s ograničenom odgovornošću d.o.o. Croatia is the most widely used corporate structure for small and medium-sized businesses operating in the country. Governed primarily by the Companies Act (Zakon o trgovačkim društvima), which came into force in 1993 and has been amended multiple times since, a d.o.o. carries separate legal personality and limits member liability to the amount of their capital contribution.

As a hybrid structure, it combines the operational flexibility of a partnership with the liability protection of a corporation. Members do not bear personal responsibility for company debts beyond their subscribed shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (d.o.o.) | Registered in the court register (sudski registar) |

| Members | 1 to 50 members | Members hold business shares (poslovni udjeli); a single-member structure is permitted |

| Management | One or more directors (članovi uprave) | No supervisory board required below statutory thresholds |

| Local Presence | Registered seat in Croatia required | A physical or c/o address; registered agent not mandated by statute |

| Share Capital | Minimum HRK 20,000 (approx. EUR 2,654) | At least HRK 200 per individual share; contributions may be cash or in-kind |

| Privacy | Members listed in the court register | Register is publicly searchable via the Ministry of Justice portal (e-Tvrtka) |

Focus Points

- Taxation: Subject to 10% corporate income tax on annual profits up to EUR 1 million, and 18% above that threshold; standard VAT rate is 25%; withholding tax applies at 15% on dividends paid to non-residents, subject to applicable tax treaties; no stamp duty on share transfers.

- Annual Compliance: Financial statements must be filed with the Financial Agency (FINA) annually; a general assembly must be held at least once per year.

- Treaty Access: Croatia's tax treaty network covers 60+ countries, allowing d.o.o. entities to access reduced withholding rates where applicable.

- Conversion: A d.o.o. may convert into a joint stock company (d.d.) through a formal court-registered procedure once capital and shareholder thresholds are met.

- Transfer Restrictions: Business share transfers to third parties may require prior consent from other members unless the articles of association provide otherwise.

Closing

A d.o.o. suits trading operations, holding structures, and IP-owning entities where liability protection and moderate compliance costs are both priorities. Its primary advantage is the low minimum capital requirement relative to a d.d.; the key limitation is the 50-member cap, which restricts equity fundraising at scale.

Small to mid-sized businesses, foreign investors establishing a local subsidiary, and entrepreneurs seeking limited liability without the capital demands of a joint stock company.

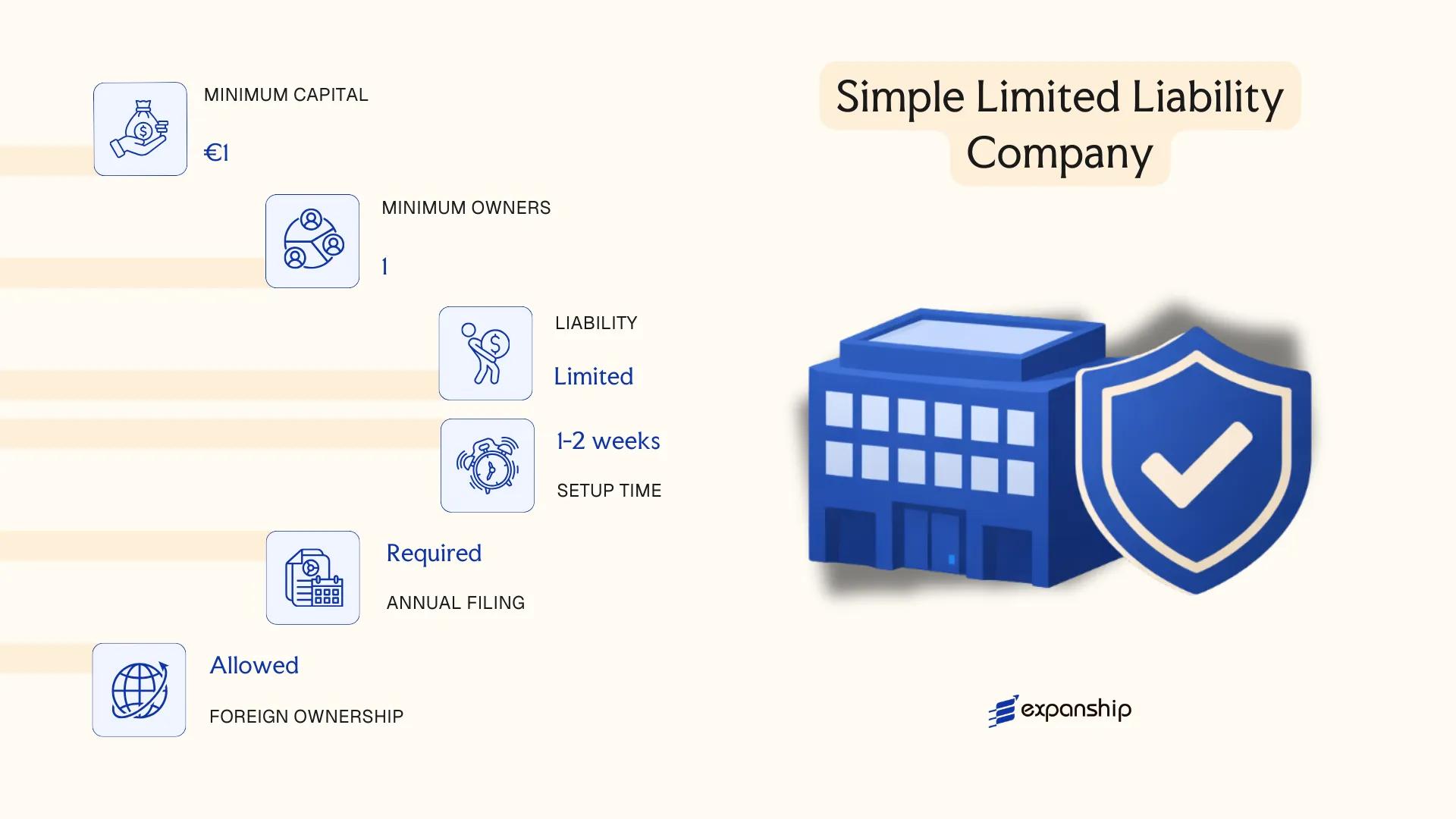

Jednostavno Društvo s Ograničenom Odgovornošću (j.d.o.o.) – Simple Limited Liability Company

The jednostavno društvo s ograničenom odgovornošću j.d.o.o. Croatia introduced through amendments to the Companies Act (Zakon o trgovačkim društvima) represents a simplified corporate form designed to reduce the capital threshold for incorporation. Like the d.o.o., it carries separate legal personality and limits member liability to the amount of their contributed share capital.

Structurally, the j.d.o.o. functions as a hybrid entry point into the Croatian corporate system. Once cumulative retained earnings reach HRK 20,000 (approximately EUR 2,654), the entity is legally obligated to convert into a standard d.o.o. under the Companies Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited company | Governed by the Companies Act (Zakon o trgovačkim društvima) |

| Members | Shareholders; 1–3 only | Exceeding 3 shareholders triggers mandatory conversion to d.o.o. |

| Management | Minimum 1 director (Uprava) | Director may also be the sole shareholder |

| Share Capital | Minimum HRK 10 (approx. EUR 1.33); maximum HRK 19,999.99 | Must be paid in full upon registration; no deferred payment permitted |

| Local Presence | Registered office address in Croatia required | No statutory requirement for a resident director |

| Privacy | Beneficial ownership registered with the Financial Intelligence Unit (HANFA-aligned registry) | Publicly searchable via the court register |

Focus Points

- Taxation: Subject to 10% corporate income tax (CIT) on profits up to EUR 1 million; standard 25% CIT applies above that threshold; VAT registration required once annual turnover exceeds EUR 40,000; no stamp duty on share transfers, though capital gains may apply.

- Annual Compliance: Annual financial statements must be submitted to the Financial Agency (FINA); audit requirements generally do not apply at this scale.

- Conversion Obligation: Mandatory conversion to d.o.o. once retained earnings cumulatively reach the statutory threshold — this is a hard legal requirement, not discretionary.

- Treaty Access: As a Croatian-registered entity, eligible for benefits under Croatia's double taxation treaties, subject to substance requirements.

- Restrictions: Cannot issue bonds or preference shares; unsuitable for businesses anticipating more than three equity participants.

Closing

The j.d.o.o. suits early-stage ventures and sole founders testing a business concept with minimal upfront capital, though the mandatory conversion threshold means it functions as a transitional rather than permanent structure.

First-time entrepreneurs and micro-businesses seeking a formally incorporated entity at minimal initial cost, with the understanding that growth will require conversion to a d.o.o.

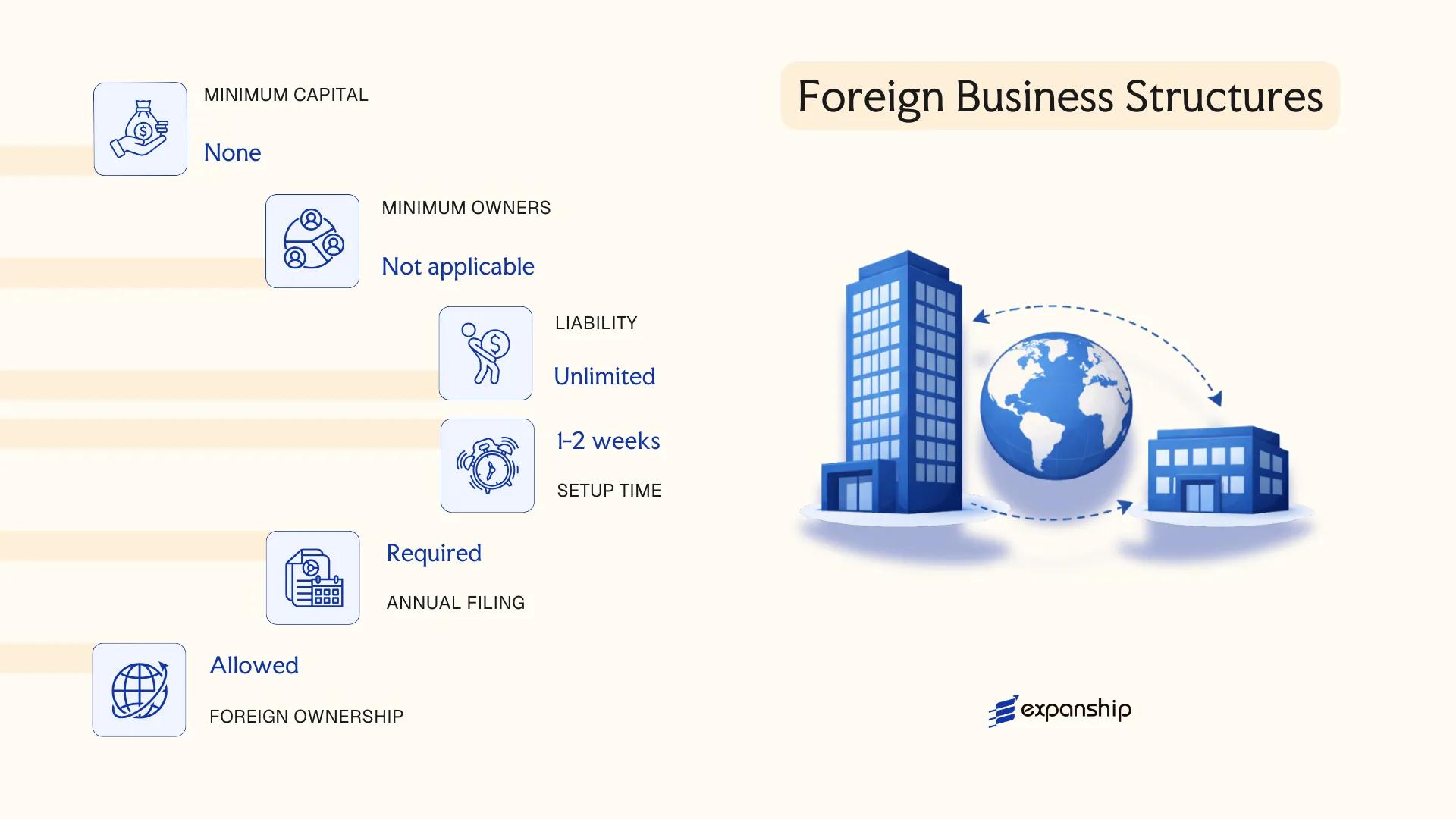

Foreign Business Structures in Croatia [Branch Office, Representative Office]

Foreign companies seeking market entry without incorporating a separate local entity can register either a branch office or a representative office. Completing a foreign company branch office Croatia registration is governed by the Companies Act (Zakon o trgovačkim društvima, ZTD) and the relevant provisions of the Court Register Act. Neither structure constitutes a separate legal person under Croatian law — both remain legally and financially part of the parent company.

A branch office (podružnica) may conduct full commercial activity, enter contracts, and generate revenue directly. A representative office, by contrast, is restricted to promotional, market research, and liaison functions; it cannot conclude commercial transactions or earn income in the country.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activity | Full commercial operations | Non-commercial only (liaison, research, promotion) |

| Registration Body | Commercial Court; entry in the Court Register | Ministry of Economy (general rule) |

| Local Representative | Mandatory authorised representative required | Mandatory authorised representative required |

| Registered Address | Required in Croatia | Required in Croatia |

| Capital Requirement | None prescribed | None prescribed |

| Liability | Parent bears unlimited liability | Parent bears unlimited liability |

Focus Points

- Taxation: Branch profits are subject to 18% corporate income tax (10% for profits up to HRK 7.5 million/approx. EUR 1 million); VAT registration required if commercial thresholds are met; withholding tax may apply to profit remittances depending on applicable tax treaties.

- Economic Substance: The branch must maintain genuine operational presence; a nominee representative without real activity may attract scrutiny from the Tax Administration (Porezna uprava).

- Annual Compliance: Annual financial statements must be submitted to FINA (Financial Agency); the branch is subject to the same accounting and audit obligations as domestic entities of equivalent size.

- Treaty Access: Croatia's tax treaty network generally extends to branch structures, though specific treaty provisions govern permanent establishment treatment.

- Restrictions: A representative office cannot invoice, sign commercial contracts, or repatriate profits; any revenue-generating activity requires conversion to a branch or incorporated entity.

Sub-Types

Branch Office (Podružnica)

Registered in the Commercial Court and entered into the Court Register, this structure is used by foreign firms that need to conduct active business operations — sales, service delivery, or contract execution — without forming a Croatian subsidiary.

Representative Office

Typically registered with the relevant ministry and used for preparatory or auxiliary functions such as market research, client liaison, and promotional activity. It suits firms assessing the market before committing to a permanent commercial presence.

Closing

Both structures suit foreign companies wanting operational or exploratory presence without the administrative burden of incorporating a new legal entity. The branch offers full commercial capability under the parent's legal identity, while the representative office's activity restrictions make it unsuitable for any revenue-generating mandate.

A branch office is best suited for established foreign firms ready to conduct active business operations in the Croatian market without establishing a separate subsidiary.

Partnerships in Croatia [General Partnership (j.t.d.), Limited Partnership (k.d.), Silent Partnership]

Governed by the Companies Act (Zakon o trgovačkim društvima, ZTD), partnership structures in Croatia j.t.d. k.d. operate under a shared legislative framework that distinguishes them primarily by the liability exposure of their members. Unlike capital companies, partnerships rely on the personal commitment of their partners rather than a defined share capital threshold.

Three recognised forms exist: the general partnership (javno trgovačko društvo, j.t.d.), the limited partnership (komanditno društvo, k.d.), and the silent partnership (tajno društvo). Each carries distinct characteristics regarding liability, internal governance, and registration obligations under the ZTD.

Key Characteristics

| Requirement | j.t.d. (General) | k.d. (Limited) | Silent Partnership |

|---|---|---|---|

| Legal Form | Separate legal personality | Separate legal personality | No separate legal personality |

| Members | Partners (minimum 2, no maximum) | Min. 1 general partner + 1 limited partner | 1 silent investor + 1 active business operator |

| Liability | All partners: unlimited, joint and several | General partners: unlimited; limited partners: capped at contribution | Silent partner: limited to contribution; operator: unlimited |

| Registered Office | Required in Croatia | Required in Croatia | No registration required |

| Capital | No statutory minimum | No statutory minimum for general partner; limited partner contributes agreed amount | Agreed contribution only; no minimum |

| Privacy | Partners disclosed in court register | General and limited partners disclosed; contribution amounts may vary | Silent partner not publicly disclosed |

Focus Points

- Taxation: Partnerships are generally treated as pass-through entities for tax purposes; partners report income through personal income tax (porez na dohodak) unless the partnership opts into the corporate profit tax (porez na dobit) regime; VAT registration applies once turnover thresholds are met.

- Annual Compliance: j.t.d. and k.d. entities must file annual financial statements with the Financial Agency (FINA); the silent partnership has no independent filing obligation.

- Croatian General Partnership Registration: j.t.d. and k.d. require entry in the court register (sudski registar) via the commercial court; the silent partnership is established by private contract alone.

- Treaty Access: Pass-through treatment may limit direct access to double taxation treaty benefits; tax residency of individual partners determines treaty eligibility.

- Conversion: A j.t.d. may be converted into a k.d. or a capital company under ZTD procedures without dissolution, subject to court approval.

Sub-Types

Javno Trgovačko Društvo – j.t.d. (General Partnership)

All partners bear unlimited joint and several liability for obligations, making this structure suited to professional service firms or family businesses where partners accept full exposure in exchange for simplified governance.

Komanditno Društvo – k.d. (Limited Partnership)

Croatia limited partnership k.d. formation separates partners into two classes: general partners who manage and bear unlimited liability, and limited partners whose exposure is capped at their agreed contribution. This structure is used where passive investors wish to participate in profits without taking on management responsibility.

Tajno Društvo (Silent Partnership)

The silent partner contributes capital to an existing business under a private agreement and shares in profits and losses without appearing in any public register. Under Croatian business law, the silent partnership carries no separate legal existence and imposes no registration requirement, which affords the silent investor a high degree of confidentiality.

General Suitability

Partnership forms are suited to professional collaborations, family enterprises, or situations where passive investment with limited liability is required without the formality of a capital company structure. The absence of a minimum capital requirement reduces the barrier to formation, though unlimited liability for general partners represents a significant exposure that warrants careful consideration.

Partnership structures in Croatia are best suited to small professional groups or domestic family businesses where partners have an established trust relationship and are prepared to accept shared personal liability.

Sole Trader in Croatia [Obrt, Simple Obrt]

Obrt sole trader registration Croatia is governed by the Crafts Act (Zakon o obrtu, Official Gazette 143/2013, with subsequent amendments), which defines the obrt as a self-employment activity carried out independently by a natural person. Unlike capital companies, the obrt does not constitute a separate legal entity — the proprietor assumes unlimited personal liability for all business obligations.

Registration is handled through the Croatian Register of Crafts and Trades, administered by the Croatian Chamber of Trades and Crafts (Hrvatska obrtnička komora). Activities eligible for registration are classified as either free, regulated, or tied crafts, with regulated and tied categories requiring proof of professional qualifications before registration is approved.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole trader (natural person) | No separate legal personality; proprietor bears full liability |

| Member Designation | Proprietor (obrtnik) | One individual only; no co-ownership structure under the standard obrt |

| Local Presence | Registered business address in Croatia | Must maintain a physical place of business |

| Capital | No minimum capital required | No share capital; business assets are personal assets |

| Taxation | Subject to personal income tax (PIT) | VAT registration mandatory above the HRK/EUR threshold; no corporate tax applies |

| Privacy | Name and activity publicly listed | Register entries are publicly accessible via e-Obrt system |

Focus Points

- Taxation: Income taxed under personal income tax at progressive rates; VAT applies once annual turnover exceeds the statutory threshold (currently EUR 40,000); no withholding tax regime applicable at entity level.

- Annual Compliance: Obligatory annual income tax filing; bookkeeping requirements depend on whether the proprietor elects lump-sum (paušalno) or actual-cost accounting.

- Conversion: An obrt can be converted into a d.o.o. or j.d.o.o. through a formal transformation procedure under the Companies Act (Zakon o trgovačkim društvima).

- Restrictions: Only Croatian nationals and EEA citizens may register an obrt without additional authorisation; third-country nationals face additional permit requirements.

- Social Contributions: The proprietor must register for compulsory pension and health insurance contributions regardless of profit level.

Sub-Types

Slobodni Obrt (Free Craft)

This category covers activities that require no formal professional qualification for registration, making entry straightforward for general trade or service activities not subject to regulated standards.

Vezani Obrt (Tied Craft)

Registration requires proof of a specific vocational qualification or professional licence. This applies to trades such as electricians, plumbers, and similar skilled occupations where public safety considerations apply.

Paušalni Obrt (Lump-Sum Obrt)

Proprietors whose annual income does not exceed the prescribed threshold may elect lump-sum taxation, replacing standard bookkeeping with a simplified fixed-tax calculation. This is the primary simplified structure referenced as Croatian simple obrt setup in practice.

The obrt structure suits sole practitioners, artisans, and service providers operating domestically with low startup costs and no need for liability separation. Its main advantage is minimal formation cost and administrative simplicity; its primary limitation is unlimited personal liability, which exposes the proprietor's private assets to all business claims.

The obrt is most appropriate for individual professionals and tradespeople conducting low-risk, single-person operations who do not require the liability protection of a capital company.

How to Choose the Right Entity Type in Croatia

Selecting the correct structure from the outset determines your tax exposure, liability profile, and administrative burden for the life of the business — getting it wrong has concrete, correctable-but-costly consequences.

Why Your Entity Choice Matters

- Registering a foreign branch to conduct retail or service trade locally, without full Croatian establishment, may constitute unlicensed commercial activity under the Companies Act (Zakon o trgovačkim društvima), exposing the business to deregistration or financial penalties.

- Choosing a j.d.o.o. when your business later requires external investors or significant capital injections forces a mandatory conversion to d.o.o., which incurs notarial and court registration costs.

- Selecting a representative office structure when the entity will conclude contracts or generate revenue results in a taxable permanent establishment under Croatian tax law, without the legal protection of a properly registered company.

- Forming a d.d. for a single-person consultancy imposes mandatory supervisory board requirements and audited financials, adding disproportionate compliance costs relative to the business scale.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each fall under different licensing and structural requirements under Croatian law.

- Minimum Capital: Your available capital at formation directly determines whether a j.d.o.o. (10 HRK symbolic minimum) or d.o.o. (€2,500) is the appropriate starting point.

- Ownership Structure: A single-founder operation has different governance needs than a multi-party venture requiring defined shareholder agreements and board oversight.

- Tax Objectives: Whether your priority is access to Croatia's double taxation treaty network or eligibility for the flat profit tax rate shapes which entity and residency structure applies.

- Substance Capacity: If you cannot maintain a physical presence, staff, or local decision-making, certain structures will trigger substance-related scrutiny by the Tax Administration (Porezna uprava).

- Exit Strategy: Not all Croatian entity types permit redomiciliation or conversion without dissolution; confirm your intended exit path before formation.

The full text of the Zakon o trgovačkim društvima is available on the official Croatian legislation portal.

Corporate Compliance Services in Croatia

Ongoing compliance support for Croatian companies, including annual filings, statutory records, and coordination with the Commercial Court Registry.

Conclusion

Croatia's company incorporation summary guide covers eight distinct entity forms, each calibrated to a different operational profile. The d.o.o. dominates registrations and suits most small-to-medium ventures, while the j.d.o.o. serves founders who need a low-capital entry point with limited liability. Large firms raising external capital tend toward the d.d., given its share issuance framework under the Companies Act. Partnerships — the j.t.d. and k.d. — fit businesses where personal liability is acceptable in exchange for structural simplicity. Branch and representative offices address foreign entities testing the market without establishing a separate legal person. The obrt remains the standard form for individual traders operating under Croatian law.

Regulatory alignment with EU directives continues to shape corporate governance requirements, and ongoing digitisation of the Court Registry has reduced procedural friction in recent years. Your choice of structure will ultimately determine reporting obligations, capital exposure, and tax treatment from day one.

How Expanship Can Assist You

Croatia company formation services through Expanship cover the full process — from selecting the right entity to completing registration with the Commercial Court Registry (Sudski registar). Whether you are forming a d.o.o., a j.d.o.o., or structuring a branch office for a foreign parent company, your obligations under Croatian company law are specific and sequential. Expanship works through each step with you directly.

Our corporate services span the full formation and post-incorporation cycle:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision in Croatia

- Filing and liaison with the Sudski registar and FINA (Financial Agency)

- Post-incorporation compliance management, including statutory reporting

- Corporate bank account introduction assistance

Every engagement is handled by specialists with direct knowledge of Croatian regulatory requirements — not generalists working from templates.

Reach out through Expanship Croatia to discuss your specific situation.

Frequently Asked Questions (FAQ)

The d.o.o. (Društvo s Ograničenom Odgovornošću) is the most frequently registered business structure in Croatia. Its combination of limited liability, a relatively low minimum share capital of €2,500, and flexible single-member formation makes it the default choice for small to mid-sized domestic and foreign-owned businesses.

A d.d. (Dioničko Društvo) requires a minimum share capital of €25,000 and can issue publicly tradeable shares, making it suited to larger enterprises or those seeking external investment. A d.o.o. restricts share transferability and cannot list shares on a public exchange, but carries significantly lower formation costs and lighter ongoing compliance obligations. Both structures are treated as Croatian tax residents subject to corporate income tax under the Profit Tax Act.

Among Croatian business structures, the j.d.o.o. and d.o.o. both require beneficial ownership disclosure under anti-money laundering regulations, as does the d.d. Director and shareholder information is filed with the court registry and accessible through the Official Gazette. Nominee arrangements are not formally recognized under Croatian company law as a privacy mechanism.

A sole individual can form a d.o.o., j.d.o.o., or register as an obrt. A d.d. requires a minimum of one founder but imposes a supervisory board once it exceeds prescribed thresholds. General partnerships (j.t.d.) and limited partnerships (k.d.) require at least two partners by definition under the Companies Act.

Foreign nationals can register a d.o.o., d.d., or j.d.o.o. without restrictions on ownership. EU citizens may register an obrt directly; non-EU nationals face additional administrative requirements tied to residency status. A foreign company may also establish a branch office, which does not constitute a separate legal entity but allows commercial activity under the parent company's liability.

The Companies Act (Zakon o trgovačkim društvima) permits the transformation of one company form into another, including conversion from a j.d.o.o. to a d.o.o. once share capital thresholds are met. Conversion requires a shareholders' resolution, updated articles of association, and re-registration with the court registry. Not all conversions are permitted in every direction — transformation from a d.o.o. to a d.d., for example, requires meeting the higher capital threshold.

The d.o.o., j.d.o.o., and d.d. all carry separate legal personality under Croatian law. A representative office does not — it cannot enter contracts or generate revenue in its own name. Silent partnerships also lack separate legal personality, as they exist as contractual arrangements between parties without forming a distinct legal subject.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.