Key Takeaways

- The Private Capital Company (IKE) has become Greece's most commonly registered entity type for new businesses, driven by its low capital threshold and operational flexibility.

- All commercial entities in Greece are registered and maintained through the General Commercial Registry (GEMI), which operates under the supervision of the Ministry of Development and Investment.

- Among the available structures, only the Societe Anonyme (AE) provides the shareholder framework necessary for access to capital markets and public offerings.

- General and limited partnerships (OE and EE) expose at least one partner to unlimited personal liability, making them more suited to specific professional or family business arrangements than to general commercial use.

Introduction to Entity Types in Greece

Greece sits at the southeastern edge of Europe, bordered by Bulgaria, North Macedonia, and Albania to the north, Turkey to the east, and surrounded by the Aegean, Ionian, and Mediterranean seas. It is an independent member state of the European Union, which means companies incorporated there operate within an EU regulatory framework and benefit from access to the single market.

Company registration falls under the jurisdiction of the General Commercial Registry (GEMI — Γενικό Εμπορικό Μητρώο), the central authority responsible for registering and maintaining records for all commercial entities. GEMI operates under the supervision of the Ministry of Development and Investment.

Greece applies a standard corporate tax regime — resident companies are taxed on worldwide income, and the country has an active network of double tax treaties.

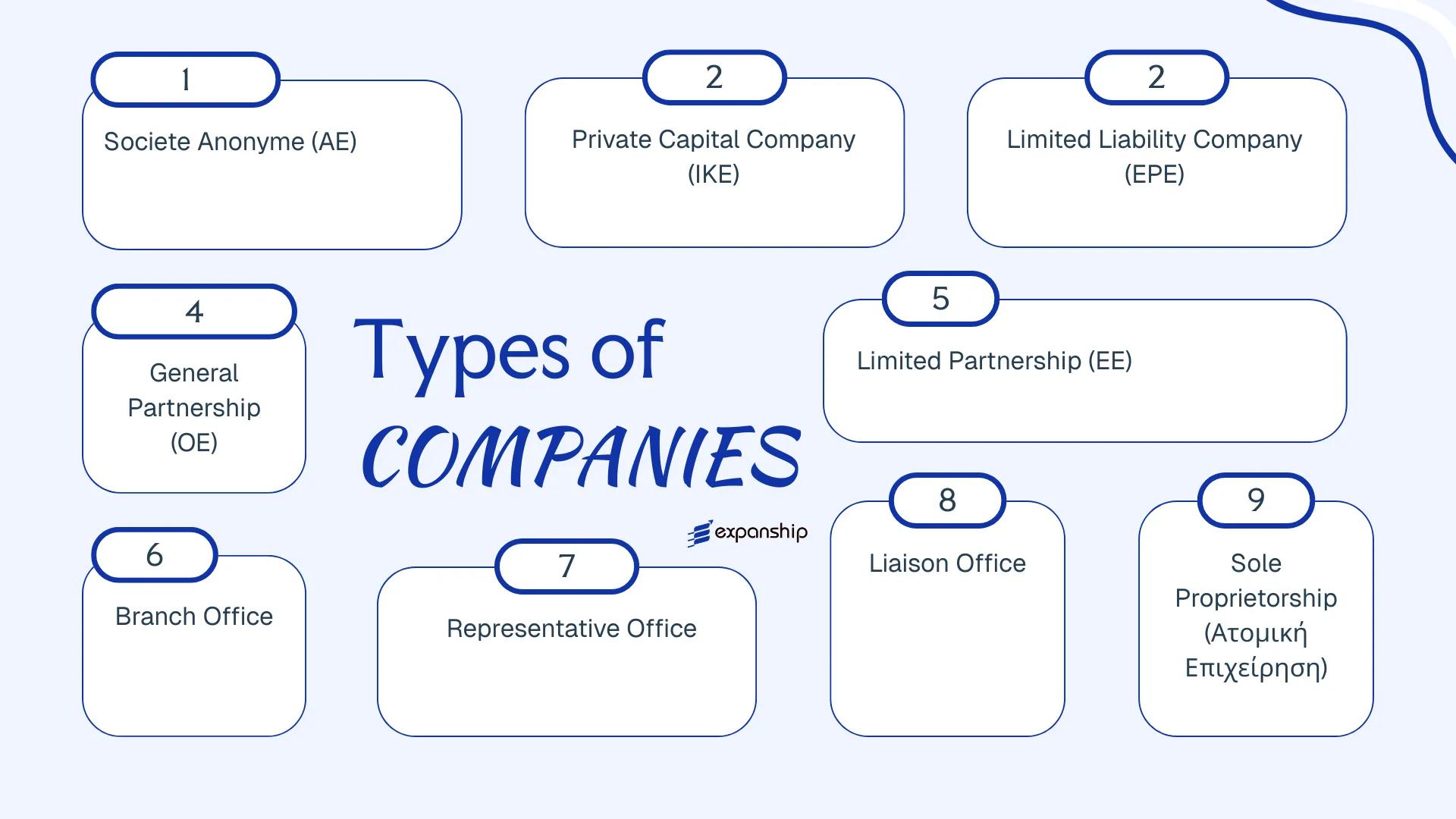

The types of business entities in Greece available to both domestic and foreign investors include:

- Societe Anonyme (AE)

- Private Capital Company (IKE)

- Limited Liability Company (EPE)

- General Partnership (OE)

- Limited Partnership (EE)

- Branch Office

- Representative Office

- Sole Proprietorship

Each structure carries distinct requirements around capital, liability, governance, and taxation. This article examines each of them in detail.

An Overview of Business Structures in Greece

Greek company law provides several distinct entity types, each governed primarily by the codified framework updated through Law 4548/2018 (for sociétés anonymes), Law 4072/2012 (which introduced the Private Capital Company and reformed partnerships), and Law 3190/1955 (for limited liability companies). Taken together, these statutes define the structural options available to both resident and foreign investors. Each form carries different rules on liability, governance, and capital requirements.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Societe Anonyme (AE) | Corporation | Limited to share capital | Taxed | Yes | 1 shareholder | GEMI | Law 4548/2018 |

| Private Capital Company (IKE) | Private company | Limited / variable | Taxed | Yes | 1 member | GEMI | Law 4072/2012 |

| Limited Liability Company (EPE) | Private company | Limited to capital | Taxed | Yes | 1 member | GEMI | Law 3190/1955 |

| General Partnership (OE) | Partnership | Unlimited, joint | Taxed | Yes | 2 partners | GEMI | Law 4072/2012 |

| Limited Partnership (EE) | Partnership | Mixed | Taxed | Yes | 2 partners | GEMI | Law 4072/2012 |

| Branch Office | Foreign branch | Parent liable | Taxed on Greek income | Yes | Parent company | GEMI | Law 4548/2018 |

| Representative / Liaison Office | Non-trading entity | Parent liable | Exempt / restricted | No | Parent company | Ministry of Economy | Various |

| Sole Proprietorship | Individual | Unlimited, personal | Taxed | Yes | 1 individual | AADE / GEMI | Law 4308/2014 |

Each of these structures is examined in full in the sections below.

Societe Anonyme (Ανώνυμη Εταιρεία / AE)

The Societe Anonyme AE company Greece is governed by Law 4548/2018, which modernised the legal framework for Greek joint stock companies and replaced the previous legislation. The AE holds separate legal personality, meaning its obligations are distinct from those of its shareholders.

Shareholders bear limited liability, restricted to their capital contribution. Capital is divided into shares, which may be transferred or listed on a stock exchange, making this structure suited to larger operations or businesses anticipating external investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme / Joint Stock Company | Governed by Law 4548/2018 |

| Members | Shareholders (min. 1, no maximum) | Single-shareholder AE is permitted |

| Management | Board of Directors (min. 1 member) | Monistic or dualistic board structure available under 2018 reform |

| Registered Office | Must maintain a registered address in Greece | Physical presence required; registered agent not mandated by law |

| Share Capital | Min. €25,000, fully paid up at incorporation | Denominated in EUR; contributions may be cash or in-kind |

| Privacy | Shareholder register is not publicly disclosed; board details filed with GEMI | Beneficial ownership registered with the UBO Registry |

Focus Points

- Taxation: Subject to corporate income tax at 22%, VAT at the standard rate of 24%, withholding tax on dividends at 5%, and stamp duty where applicable.

- Annual Compliance: Mandatory filing of audited financial statements with the General Commercial Registry (GEMI); statutory audit required where thresholds are met.

- Economic Substance: No formal substance regime, but board meetings and management decisions should demonstrably occur in Greece to support tax residency claims.

- Treaty Access: Greece has an extensive double tax treaty network; the AE qualifies as a resident entity for treaty purposes.

- Conversion: An AE may be converted into an IKE or EPE through a formal procedure under Greek corporate law without dissolution.

Closing

The AE suits holding structures, large trading operations, and businesses seeking to raise capital through share issuance, though its mandatory minimum capital and statutory audit obligations create a higher administrative burden relative to other Greek entity types.

Large or capital-intensive businesses, joint ventures, and entities planning to list shares or attract institutional investors.

Company Incorporation in Greece

Incorporate an AE or other Greek entity with full compliance support across registration, capital structuring, and GEMI filing.

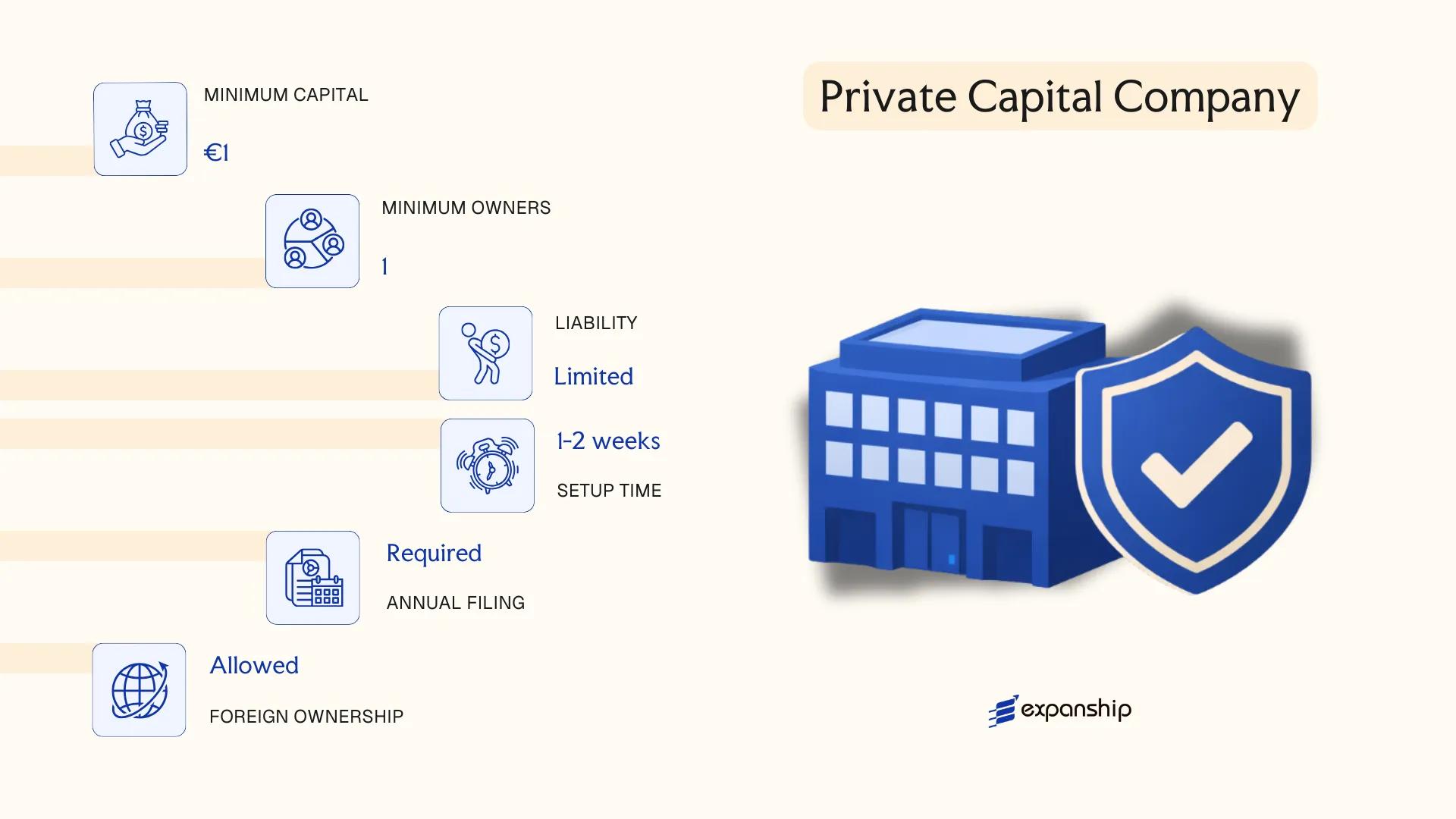

Private Capital Company (Ιδιωτική Κεφαλαιουχική Εταιρεία / IKE)

Introduced under Law 4072/2012, the Private Capital Company IKE Greece is a hybrid corporate form designed to combine the liability protection of a capital company with the operational flexibility more commonly associated with partnerships. The entity holds separate legal personality, meaning it can own assets, enter contracts, and incur obligations in its own name.

Liability is limited to the company's assets, though the IKE structure permits members to contribute non-cash capital — including guarantee contributions and memorandum contributions — alongside standard capital contributions. This makes IKE company registration Greece a practical option for businesses where tangible capital is limited at inception.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Capital Company (IKE) | Governed by Law 4072/2012 |

| Members | 1 to 50 | Can be natural persons or legal entities; single-member IKE is permitted |

| Management | Managed by one or more managers | Managers need not be members; no board requirement |

| Share Capital | Minimum €0 | Capital can be zero; contributions may be cash, non-cash, guarantee, or memorandum |

| Registered Office | Physical address in Greece required | No statutory requirement for a local resident manager |

| Privacy | Member details filed with GEMI | Not publicly confidential; company records accessible via General Commercial Registry |

Focus Points

- Taxation: Subject to the standard corporate income tax rate (currently 22%); VAT registration required for trading activities; dividend withholding tax applies to distributions; no special stamp duty regime.

- Annual Compliance: Obligatory filing of annual financial statements with GEMI; annual general meeting required; statutory auditor not mandatory for small-scale IKEs below audit thresholds.

- Economic Substance: No specific substance scoring system, but a registered office and operational presence in Greece are required to maintain tax residency.

- Treaty Access: As a Greek-resident entity, the IKE is eligible for double tax treaty benefits under Greece's treaty network, subject to anti-abuse provisions.

- Conversion: An IKE may be converted into other Greek corporate forms (such as EPE or AE) under the transformation provisions of Law 4601/2019.

Closing

The IKE suits early-stage businesses, startups, and SMEs that require limited liability without mandatory minimum capital, and it is also used as a holding vehicle where asset ownership flexibility is a priority. The zero share capital threshold lowers the barrier to entry, though the absence of an audit requirement for smaller entities can reduce external financial credibility with institutional lenders or larger counterparties.

Founders and small business operators seeking a low-cost, limited liability structure with flexible contribution types and straightforward registration through GEMI.

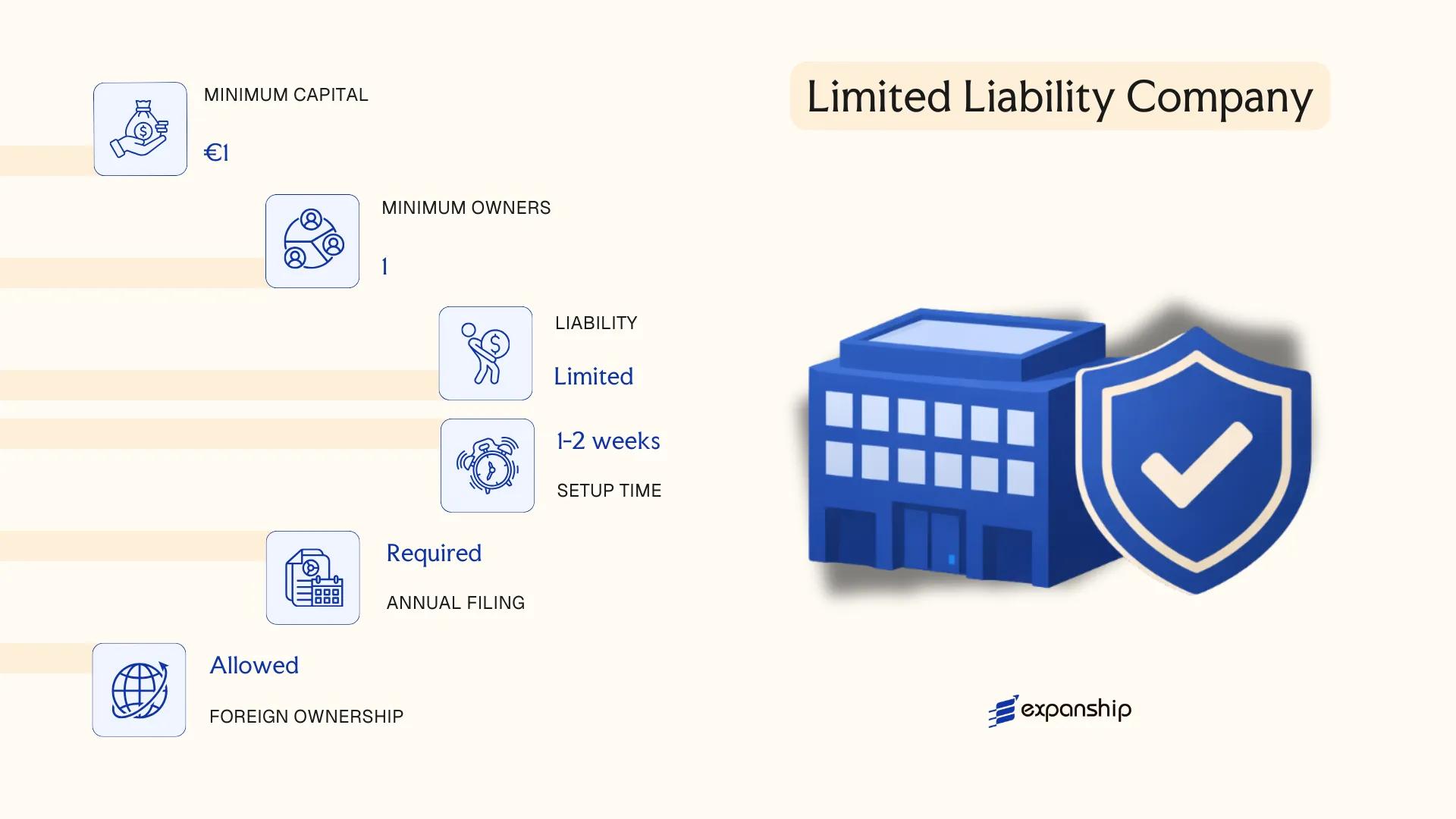

Limited Liability Company (Εταιρεία Περιορισμένης Ευθύνης / EPE)

The limited liability company EPE Greece framework is governed by Law 3190/1955, which has been amended over the decades but remains the foundational statute for this entity type. The EPE holds separate legal personality, meaning its obligations are distinct from those of its members, whose exposure is capped at their capital contributions.

Structurally, the EPE sits between a partnership and a corporation. Membership interests are not represented by freely transferable shares; instead, they take the form of participations (μερίδια), and transfers generally require notarial documentation and registration with the General Commercial Registry (GEMI).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Governed by Law 3190/1955; separate legal personality |

| Members | Referred to as members (εταίροι); minimum 1, maximum 50 | Single-member EPE is permitted |

| Management | Managed by one or more managers (διαχειριστές); can be members or third parties | No board structure required |

| Capital | Minimum €18,000; denominated in EUR | Must be fully paid up at incorporation |

| Local Presence | Registered office address required in Greece | No mandatory resident manager under current law |

| Privacy | Member details filed with GEMI; publicly accessible | Beneficial ownership registered with national UBO registry |

Focus Points

- Taxation: Subject to 22% corporate income tax; standard VAT registration applies; dividends distributed to non-resident members attract 5% withholding tax; stamp duty may apply to certain transactions.

- Annual Compliance: Obligation to file audited financial statements with GEMI and submit annual corporate income tax returns to AADE (Independent Authority for Public Revenue).

- Economic Substance: No statutory substance requirements specific to the EPE, but actual management and control within Greece determines tax residency.

- Treaty Access: As a Greek tax resident entity, the EPE can access Greece's network of double tax treaties.

- Conversion: An EPE may be converted into an AE or IKE through a formal restructuring process under Greek company law, subject to notarial deed and GEMI registration.

Closing

The EPE suits small to medium-sized trading or service businesses where ownership is closely held and full share transferability is not a priority. Its fully paid-up minimum capital requirement of €18,000 represents a higher entry threshold compared to newer Greek entity forms.

The EPE is most appropriate for established small businesses or family-owned operations that require a recognised legal structure with capped liability but do not anticipate frequent changes in ownership or external investment rounds.

Partnerships [General Partnership / OE, Limited Partnership / EE]

Greek partnership structures are governed primarily by the Greek Civil Code and the Commercial Code, with procedural registration requirements updated through Law 4635/2019 and subsequent reforms. Both the Omorrythmi Etaireia (OE) and the Eterorythmi Etaireia (EE) are registered with the General Commercial Registry (GEMI) and acquire separate legal personality upon registration.

The general partnership OE and limited partnership EE in Greece sit at the simpler end of the commercial structure spectrum. Both forms are transparent for tax purposes and carry unlimited liability for at least one class of partner, making personal exposure a material consideration before selection.

Key Characteristics

| Requirement | OE (General Partnership) | EE (Limited Partnership) |

|---|---|---|

| Members | Minimum 2 general partners; no statutory maximum | Minimum 1 general partner + 1 limited partner; no statutory maximum |

| Member Terminology | Partners (Etairoi) | General Partners (Omorrythmoi) and Limited Partners (Eterorythmoi) |

| Liability | All partners: unlimited, joint and several | General partners: unlimited; limited partners: capped at capital contribution |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered office in Greece required | Registered office in Greece required |

| Privacy | Partner names appear in the GEMI public register | Both partner categories disclosed in GEMI |

Focus Points

- Taxation: Profits taxed at the corporate income tax rate (currently 22%); VAT registration required if trading; no withholding tax exemptions available that apply to capital companies; distributions subject to dividend withholding tax at 5%.

- Annual Compliance: Annual financial statements must be filed with GEMI; accounting records maintained under Greek accounting standards (Law 4308/2014).

- Economic Substance: No specific substance requirements beyond the registered office, though tax residency depends on place of effective management.

- Conversion: Both OE and EE can be converted into a capital company (IKE, EPE, or AE) under Law 4601/2019 on corporate transformations.

- Restrictions: General partners in both forms bear personal liability, which cannot be contractually limited against third parties.

Sub-Types

Omorrythmi Etaireia (OE) — General Partnership

Every partner holds full management rights and bears unlimited joint liability for the firm's obligations. This structure is typically used by small professional practices or family-run trading businesses where all participants take an active role.

Eterorythmi Etaireia (EE) — Limited Partnership

The EE introduces a two-tier partner structure: general partners manage the business and carry unlimited liability, while limited partners are passive investors whose exposure does not exceed their agreed contribution. Limited partners are prohibited from participating in management; doing so risks reclassification of their liability status.

Partnerships suit small, closely held Greek businesses where the partners know one another and accept the liability trade-off in exchange for minimal formation costs and structural simplicity. The absence of a minimum capital requirement lowers the entry barrier, but unlimited personal exposure for general partners remains a significant structural drawback for any business carrying meaningful commercial or financial risk.

OE and EE structures are most appropriate for small professional firms or family businesses with two or more known participants who are comfortable with personal liability and do not require the liability protections of a capital company.

Foreign Business Presence in Greece [Branch Office, Representative Office, Liaison Office]

Establishing a foreign company branch office Greece is governed primarily by Greek Law 4919/2022, which modernised the registration framework for foreign entities operating within the country. A branch has no separate legal personality from its parent company — the foreign firm bears full liability for the branch's obligations.

Registration is handled through the General Commercial Registry (GEMI), and the branch must appoint a legal representative resident in the country. Ongoing compliance mirrors that of domestic entities in several respects, including accounting, tax registration, and annual filing obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Representative / Liaison Office | Branch is most operationally active; liaison is most restricted |

| Legal Personality | None (extension of parent) | Parent company bears all liability |

| Local Representative | Mandatory for branch; advisable for others | Must hold a Greek tax number (AFM) |

| Registered Address | Required in Greece | Must be a physical address registered with GEMI |

| Share Capital | None required at branch level | Parent's capital structure applies |

| Privacy | Parent company details publicly registered via GEMI | No separation between branch and parent identity |

Focus Points

- Taxation: Branches are subject to 22% corporate income tax on Greek-sourced profits; VAT registration is required for commercial activity; profit remittances to the parent may attract withholding tax under domestic rules, subject to applicable tax treaty relief.

- Economic Substance: The branch must conduct genuine activity; a purely nominal presence risks reclassification by the Independent Authority for Public Revenue (AADE).

- Annual Compliance: Annual financial statements must be filed with GEMI; the branch must maintain Greek-compliant bookkeeping under Greek Accounting Standards.

- Treaty Access: Greece's tax treaty network may reduce withholding taxes on profit transfers, but treaty eligibility depends on the parent's jurisdiction and structure.

- Conversion: A branch can be converted into a subsidiary (such as an IKE or AE), though this requires a formal restructuring process and re-registration.

Sub-Types

Branch Office

A branch conducts full commercial operations in Greece under the parent's name and liability. It can generate revenue, sign contracts, and employ staff directly — making it the most functionally equivalent structure to a local subsidiary.

Representative Office

A representative office is limited to auxiliary activities such as market research, promotion, and client liaison. It cannot conclude contracts or generate direct revenue, and its permitted scope is narrower than a branch.

Liaison Office

Setting up a liaison office in Greece restricts the entity to internal coordination functions — typically used for communication between the foreign parent and local contacts. No commercial transactions are permitted, and its activities must remain strictly preparatory or auxiliary.

When to Use This Structure

A branch suits foreign firms wanting direct Greek market access without incorporating a separate local entity, though full parental liability exposure is a significant structural drawback.

Established foreign companies testing the Greek market or managing regional operations who are comfortable with parent-level liability and do not require a separate legal entity.

Sole Proprietorship (Ατομική Επιχείρηση)

The sole proprietorship Greece Atomiki Epicheirisi structure is the simplest form of business activity available to individuals. It is governed primarily by the Greek Commercial Code and relevant provisions of Law 4308/2014 on Greek Accounting Standards, which set out bookkeeping and reporting obligations for self-employed individuals.

Unlike capital companies, the Atomiki Epicheirisi carries no separate legal personality. The proprietor and the business are treated as a single legal unit, meaning personal assets are fully exposed to business liabilities with no liability shield of any kind.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Ατομική Επιχείρηση) | No separate legal personality from the owner |

| Members | Single proprietor | Only one natural person; no partners or shareholders |

| Local Presence | Greek tax registration (AFM) required; physical address mandatory | Registered with the local tax office (ΔΟΥ) and GEMI |

| Capital | No minimum capital requirement | No capital contribution mandated by law |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Privacy | Owner's name is part of the registered business identity | Limited privacy; proprietor details are publicly linked to the business |

Focus Points

- Taxation: Subject to personal income tax on business profits at progressive rates up to 44%; VAT registration required if turnover exceeds the applicable threshold; no corporate income tax applies; subject to EFKA social security contributions as a self-employed person.

- Self-employed registration Greece: Registration is completed through the General Commercial Registry (GEMI) and the competent tax office (ΔΟΥ); EFKA enrollment is mandatory from day one of activity.

- Annual Compliance: Simplified or double-entry bookkeeping required under Law 4308/2014 depending on turnover category; annual income tax return filing is obligatory.

- Conversion: Can be converted into a capital company (such as IKE or EPE), though the process requires formal steps including asset valuation and new entity registration.

- Treaty Access: As an unincorporated structure with no separate legal personality, access to double tax treaty benefits is through the individual proprietor's tax residency status.

Closing

The Atomiki Epicheirisi suits low-risk, low-turnover individual trading or freelance activity where administrative simplicity outweighs the need for liability protection. Its principal drawback is unlimited personal liability, which makes it unsuitable for activities carrying significant financial or legal exposure.

Greek sole trader setup requirements are minimal, making this structure appropriate for freelancers, sole traders, and micro-business operators conducting straightforward commercial or professional activity in Greece.

How to Choose the Right Entity Type in Greece

Selecting the correct structure at the outset is one of the most consequential decisions in the Greece company formation process — the wrong choice produces concrete legal and financial outcomes that are difficult and costly to reverse.

Why Your Entity Choice Matters

- Choosing a structure without legal personality, such as a General Partnership (OE), exposes each partner to unlimited personal liability for all business debts — including those incurred by other partners.

- Selecting a structure exempt from income tax when you need access to Greece's double tax treaty network means withholding tax reductions in counterpart countries may be unavailable to your business.

- Registering a foreign branch when your operations require a fully independent legal entity leaves the parent company directly exposed to liabilities arising in Greece.

- Forming a capital company (AE or IKE) when a sole proprietorship would suffice adds statutory compliance obligations — including annual general meetings and General Commercial Registry (GEMI) filings — that generate ongoing administrative cost without a corresponding benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each point toward a different legal form under Greek law.

- Ownership and Management: Single-owner operations and multi-party ventures have structurally different governance requirements; an IKE accommodates a sole member, while an AE mandates a minimum board structure.

- Tax Objectives: Your need for treaty access, eligibility under the Greek tonnage tax regime, or qualification for the non-domicile provisions under Law 4172/2013 will narrow the viable options significantly.

- Liability Exposure: The extent to which you require a statutory liability shield determines whether a capital company structure is necessary or whether a partnership form carries acceptable risk.

- Substance Capacity: If you cannot realistically maintain employees, a physical office, and decision-making processes within the jurisdiction, structures with lower substance thresholds — such as the IKE — may be more appropriate than an AE.

- Exit Strategy: Not all Greek entity types permit conversion or redomiciliation with equal ease; confirming your likely exit path before formation avoids structural lock-in.

The primary legislation governing company formation is Law 4548/2018 on Sociétés Anonymes alongside Law 4072/2012, which governs the IKE and partnership forms. Both are available in full on the official Greek legal database.

Corporate Compliance Services in Greece

Ongoing GEMI filings, annual general meeting support, and statutory record maintenance for companies incorporated in Greece.

Conclusion

Selecting the right legal structure is the first binding decision in any incorporating a company in Greece guide, and it shapes everything from liability exposure to how profits are distributed. The IKE has become the most registered entity type among new businesses, largely due to its low capital threshold and operational flexibility. For larger enterprises or those seeking access to capital markets, the AE provides the framework for shareholder structures and public offerings. The EPE suits smaller, closely held operations where formal governance requirements are proportionate but limited liability remains essential. General and limited partnerships carry unlimited liability for at least one partner and are typically chosen for specific professional or family arrangements.

Regulatory oversight by the General Commercial Registry (GEMI) has become increasingly digital, reducing registration timelines. Greece's expanding tax treaty network continues to influence how multinational groups structure their Greek presence.

How Expanship Can Assist You

Expanship's company formation services Greece covers the full incorporation process, from selecting the right structure — an AE, IKE, EPE, or partnership — through to registration with the General Commercial Registry (GEMI). Our team works directly with GEMI's online portal and coordinates with the relevant tax authority (AADE) to ensure your business is correctly registered and tax-identified from the outset.

Depending on your entity type and operational needs, here is what our corporate services team handles on your behalf:

- Preparation and legalization of incorporation documents

- Registered address and local agent provision in Greece

- Filing with GEMI and liaising with AADE for tax registration

- Post-incorporation compliance management, including annual obligations

- Corporate secretarial support and statutory record-keeping

- Banking introduction assistance for opening a Greek business account

Get in touch with Expanship Greece to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Private Capital Company (IKE) has become the most frequently formed entity since its introduction under Law 4072/2012. Its low capital requirement, flexible shareholder structure, and reduced administrative burden relative to the AE make it the default choice for small to mid-sized ventures.

The AE is subject to stricter governance requirements, including a board of directors and mandatory audits above certain thresholds, while the IKE allows a single-member structure with lighter ongoing obligations. Both entity types are subject to Greek corporate income tax at the standard rate, but the AE is better suited for firms seeking external investment or public listings.

The IKE and EPE both limit public disclosure compared to the AE, whose shareholder register is filed with the General Electronic Commercial Registry (GEMI). Nominee arrangements are legally permissible in Greece, though ultimate beneficial ownership must be disclosed to the relevant authorities under Law 4557/2018 on anti-money laundering.

A sole individual can form an IKE or AE as a single-member entity. General Partnerships (OE) and Limited Partnerships (EE) each require at least two partners by definition, so sole-founder structures are not available for those forms.

Non-EU nationals can register an IKE, AE, or EPE, though they must obtain a Greek tax identification number (AFM) and, in certain cases, a residency permit before completing registration through GEMI. No local partner is legally required for most standard commercial activities.

Conversion between entity types is permitted under Greek corporate law. An EPE can be converted to an AE or IKE through a formal transformation procedure, and the process generally preserves the entity's existing contracts and liabilities rather than requiring dissolution and re-registration.

The AE, IKE, and EPE each hold separate legal personality, meaning they can contract, own assets, and incur liabilities independently of their owners. General Partnerships (OE) also have legal personality under Greek law, though partners remain personally liable for the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.