Key Takeaways

- Gibraltar's corporate framework is governed by the Companies Act 2014, administered by Gibraltar Companies House, with regulated activities overseen by the Financial Services Commission (FSC).

- The Private Limited Company (Ltd) is the most commonly registered structure in Gibraltar, serving holding, trading, and fund-related activities under a contained liability framework.

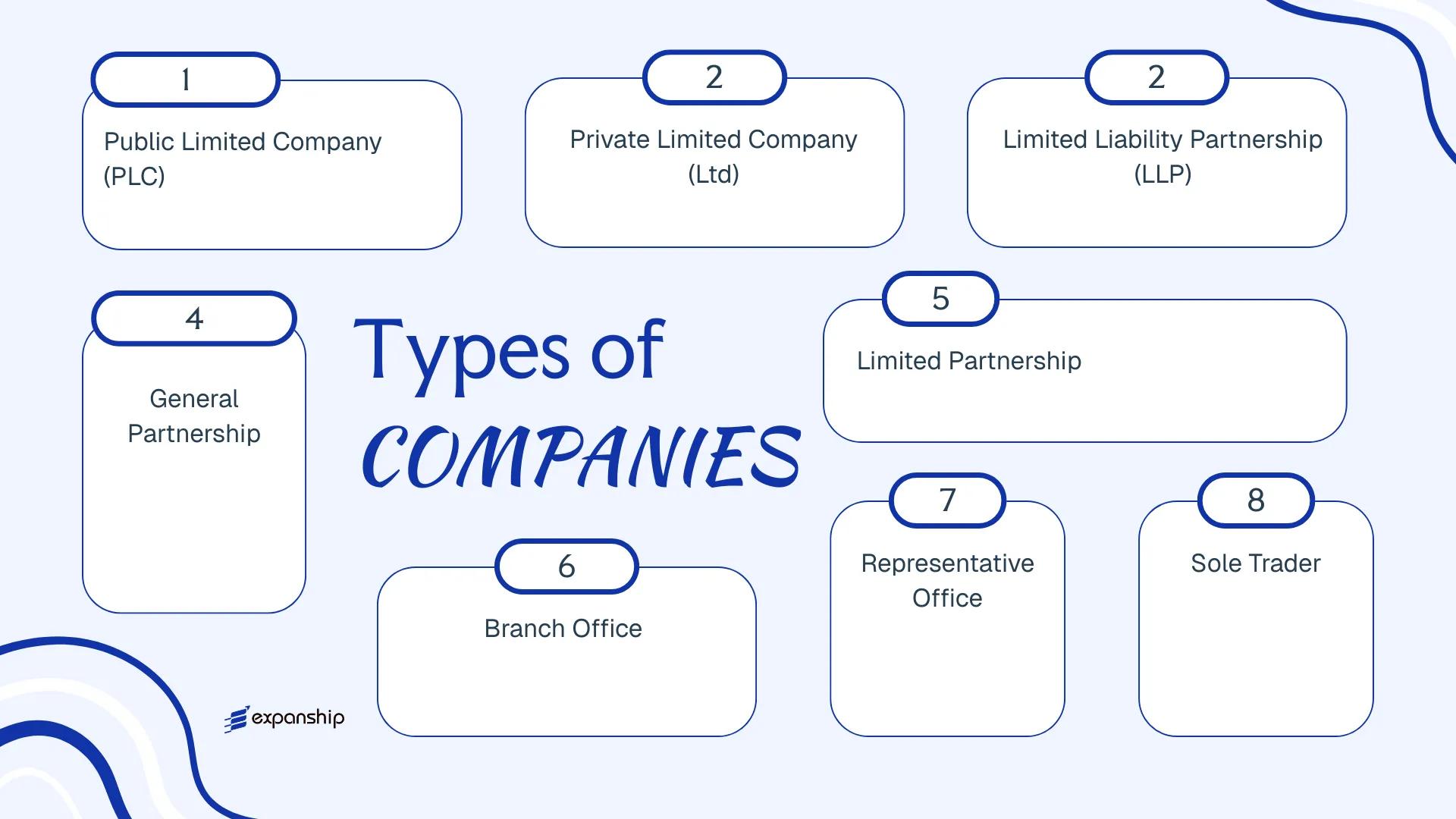

- Eight distinct entity types are available to founders and investors in Gibraltar, ranging from sole traders and general partnerships to PLCs and Limited Liability Partnerships, each carrying different implications for liability, governance, and taxation.

- Territorially-based corporate taxation and a codified regulatory framework for distributed ledger technology distinguish Gibraltar as a jurisdiction particularly suited to internationally oriented and digital asset businesses.

Introduction to Entity Types in Gibraltar

Gibraltar is a British Overseas Territory situated at the southern tip of the Iberian Peninsula, bordered by Spain to the north and facing Morocco across the Strait. As a self-governing territory under British sovereignty, it maintains its own legal system — rooted in English common law — and operates independently from the United Kingdom on matters of taxation and corporate regulation.

Company registration and ongoing compliance fall under the jurisdiction of the Gibraltar Companies House, which administers the Companies Act 2014. The Financial Services Commission (FSC) oversees regulated activities, including certain corporate structures used in financial services.

Territorially-based taxation applies to income arising in or from Gibraltar, and the corporate tax rate is set below most European standards, making the territory attractive to internationally oriented businesses.

The business entity types in Gibraltar available to founders and investors include:

- Private Limited Company (Ltd)

- Public Limited Company (PLC)

- Limited Liability Partnership (LLP)

- General Partnership

- Limited Partnership

- Branch Office

- Representative Office

- Sole Trader

Each structure carries distinct implications for liability, governance, and tax treatment. This article examines each option within this Gibraltar company structures overview to help you determine which formation best suits your operational and legal requirements.

An Overview of Business Structures in Gibraltar

Gibraltar's company law framework provides several distinct business structures, each governed primarily by the Companies Act 2014. These entities range from private limited companies to partnerships and foreign branch registrations, with each form carrying different implications for liability, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated body | Limited to shares | Taxable | Permitted | 2 shareholders | Companies House Gibraltar | Companies Act 2014 |

| Private Limited Company (Ltd) | Incorporated body | Limited to shares | Taxable | Permitted | 1 shareholder | Companies House Gibraltar | Companies Act 2014 |

| Limited Liability Partnership (LLP) | Hybrid entity | Limited | Taxable | Permitted | 2 partners | Companies House Gibraltar | Limited Partnerships Act |

| General Partnership | Unincorporated | Unlimited | Taxable | Permitted | 2 partners | Companies House Gibraltar | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxable | Permitted | 2 partners | Companies House Gibraltar | Limited Partnerships Act |

| Branch Office | Foreign extension | Parent liable | Taxable on local profits | Permitted | N/A | Companies House Gibraltar | Companies Act 2014 |

| Representative Office | Foreign extension | Parent liable | Generally exempt | Restricted | N/A | Companies House Gibraltar | Companies Act 2014 |

| Sole Trader | Unincorporated | Unlimited | Taxable | Permitted | 1 individual | HM Government of Gibraltar | Income Tax Act 2010 |

Each of these structures is examined in full in the sections below.

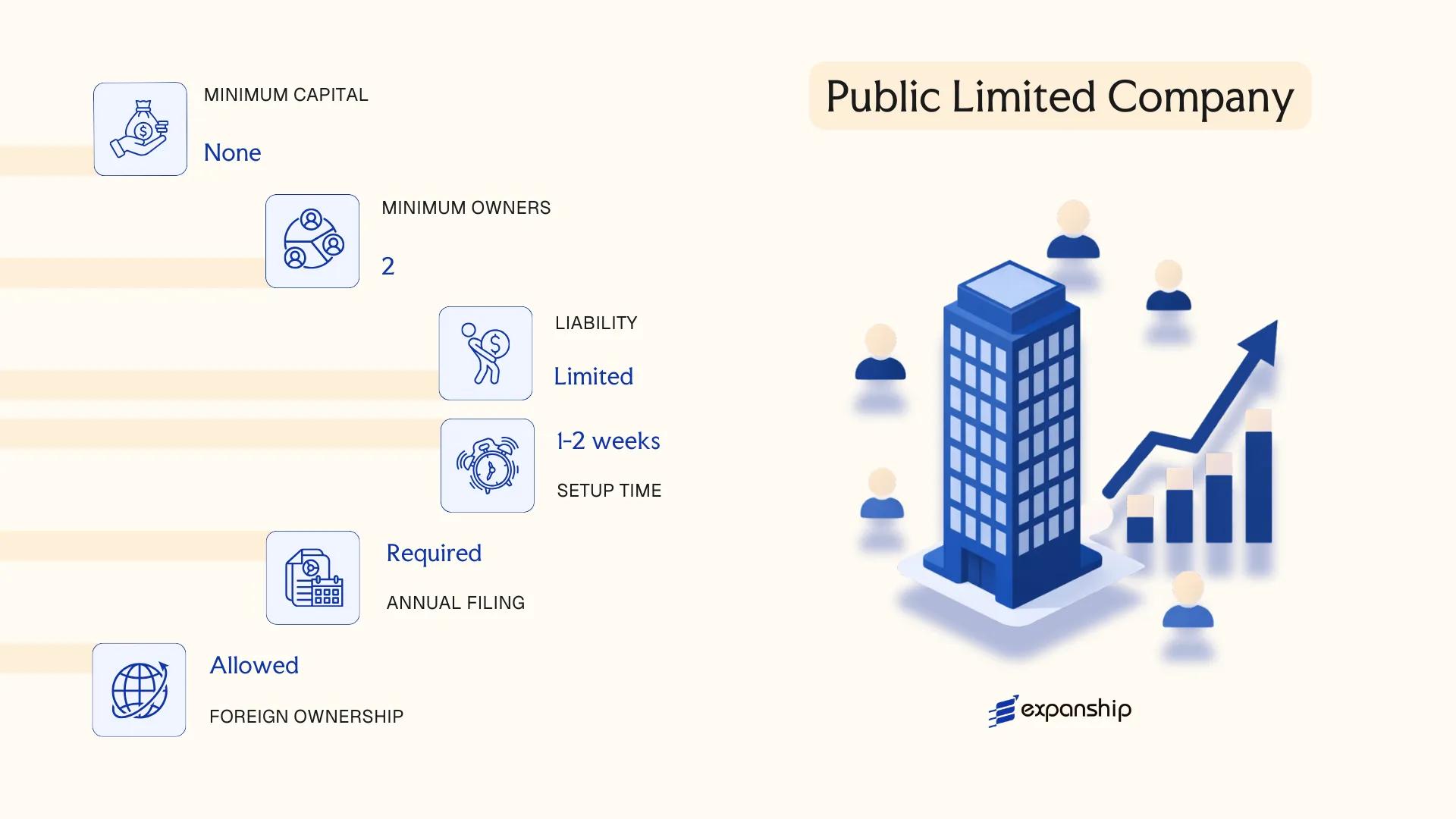

Public Limited Company (PLC)

A Gibraltar Public Limited Company (PLC) is governed by the Companies Act 2014, which consolidated and updated the territory's earlier company legislation. As a separate legal entity, it offers shareholders limited liability while permitting the public offer and trading of its shares — a structural characteristic that distinguishes it from its private counterpart.

Minimum share capital requirements and the ability to list securities make the PLC the appropriate vehicle for businesses seeking access to public capital markets. Registration is administered through Companies House Gibraltar, and the firm must include "PLC" or "Public Limited Company" in its registered name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; limited liability for shareholders |

| Members | Shareholders (min. 2, no maximum) | Directors: min. 2; a public company may not have a sole director |

| Local Presence | Registered office in Gibraltar required | Must maintain a physical registered address within the territory |

| Share Capital | Min. £20,500 (at least 25% paid up on allotment) | Capital denominated in GBP; shares may be offered to the public |

| Privacy | Shareholder and director details on public record | Beneficial ownership held on a central register accessible to authorities |

| Company Secretary | Mandatory | Must be a qualified individual or body corporate |

Focus Points

- Taxation: Subject to Gibraltar's 10% corporate tax rate on income accruing in or derived from Gibraltar; no capital gains tax, inheritance tax, or VAT; withholding tax does not apply to dividends paid to non-residents.

- Economic Substance: PLCs engaged in relevant activities (holding, finance, IP, etc.) must satisfy economic substance requirements under the Income Tax Act.

- Annual Compliance: Obligatory filing of audited accounts and an annual return with Companies House Gibraltar; audit is mandatory regardless of size.

- Treaty Access: Gibraltar is not an EU member state and has a limited double tax treaty network; tax planning should account for this constraint.

- Conversion: A PLC may be re-registered as a private limited company by special resolution, subject to satisfying the conditions set out in the Companies Act 2014.

Closing

The PLC structure suits businesses intending to raise capital from the public, list on a recognised exchange, or operate at a scale that requires institutional investor participation. The mandatory audit requirement and higher administrative burden relative to a private entity make it less practical for smaller or closely held operations.

A Gibraltar PLC is most appropriate for established businesses seeking public capital market access or planning a securities listing on a recognised exchange.

Company Incorporation in Gibraltar

Set up your Gibraltar company with end-to-end support from entity selection through to registered office and ongoing compliance.

Private Limited Company (Ltd)

The Gibraltar Private Limited Company (Ltd) is governed by the Companies Act 2014, which consolidates the legal framework for company formation and administration in the territory. As a separate legal entity, it holds rights and obligations independent of its members, and shareholder liability is confined to the amount unpaid on their shares.

Shares in a private limited company cannot be offered to the public, distinguishing it structurally from a public company. This restriction makes it the standard vehicle for closely held businesses, joint ventures, and subsidiary structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Ltd) | Separate legal personality; limited liability |

| Members | Shareholders (min. 1, max. 50) | Corporate shareholders permitted |

| Directors | Min. 1 director; no maximum | Corporate directors permitted; no mandatory residency requirement |

| Local Presence | Registered office address in Gibraltar required | Must be maintained at all times; registered agent typically appointed |

| Share Capital | No minimum share capital; GBP is common currency | Shares must have a fixed par value |

| Privacy | Shareholder and director details filed at Companies House Gibraltar | Register of beneficial owners maintained; not fully public |

Focus Points

- Taxation: Subject to 12.5% corporate income tax on Gibraltar-source income; no VAT, no capital gains tax, no inheritance tax, and no withholding tax on dividends or interest paid to non-residents.

- Economic Substance: Companies carrying on relevant activities (e.g., holding, financing, IP) must satisfy substance requirements under the Income Tax Act 2010 as amended.

- Annual Compliance: Annual return and audited financial statements must be filed with Companies House Gibraltar; audit exemptions may apply to qualifying small companies.

- Treaty Access: Gibraltar has a limited double tax treaty network; the UK-Gibraltar arrangement provides some relief, but broader treaty access is restricted.

- Conversion: A private limited company can be re-registered as a public limited company under the Companies Act 2014, subject to meeting the applicable conditions.

Closing

A Gibraltar Ltd is used across trading, holding, and IP ownership structures, with its territorial tax system being a measurable advantage for businesses with non-Gibraltar-sourced income. The restriction on public share offerings limits its suitability where external capital raising is anticipated.

Best suited for owner-managed businesses, subsidiary structures, and investors seeking a low-tax, well-regulated jurisdiction with a familiar common law corporate framework.

Limited Liability Partnership (LLP)

A Gibraltar Limited Liability Partnership LLP is governed by the Limited Liability Partnerships Act 2009, which introduced this hybrid structure into Gibraltar's commercial law. The entity carries separate legal personality, meaning it can own property, enter contracts, and incur liabilities in its own name, while each member's personal exposure is confined to their agreed contribution.

Unlike a traditional partnership, where personal assets are exposed to business debts, the LLP separates member liability from firm obligations. The internal management structure is defined by a partnership agreement rather than statutory articles, giving members greater contractual flexibility over governance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality under the LPA 2009 |

| Members | Minimum 2; no statutory maximum | Referred to as "members"; no distinction between general and limited members |

| Local Presence | Registered office in Gibraltar required | A local registered agent is standard practice |

| Capital | No minimum capital requirement; no prescribed currency | Contributions defined by the partnership agreement |

| Privacy | Names of members are filed at Companies House Gibraltar | Partnership agreement is not publicly disclosed |

Focus Points

- Taxation: LLPs are generally treated as tax-transparent; members are taxed individually on their share of profits rather than at entity level, with no corporate income tax applied at the LLP level; Gibraltar currently has no withholding tax on profit distributions.

- Economic Substance: Substance requirements may apply depending on the nature of activities conducted; relevant income categories under Gibraltar's Economic Substance Rules should be assessed.

- Annual Compliance: An annual return must be filed with Companies House Gibraltar; financial statements requirements depend on the LLP's activities and size.

- Conversion: Gibraltar law permits conversion from an LLP to a limited company under prescribed procedures, though this process requires careful structuring.

- Treaty Access: Gibraltar has a limited tax treaty network, which may affect the suitability of an LLP for cross-border structures relying on treaty benefits.

Closing

An LLP suits professional services firms, joint ventures, and fund management structures where members want contractual flexibility and pass-through taxation without personal liability exposure. The absence of a minimum capital requirement lowers the entry threshold, though the limited treaty network can constrain its utility in multi-jurisdictional tax planning.

Professional firms and joint ventures where two or more parties require limited liability alongside flexible profit-sharing arrangements governed by a private partnership agreement.

Partnerships in Gibraltar [General Partnership, Limited Partnership]

Gibraltar's general and limited partnership structures are governed primarily by the Partnership Ordinance, which draws from long-established English partnership law principles. Neither a general nor a limited partnership constitutes a separate legal entity under Gibraltar law — partners remain personally bound to the obligations of the firm, though the extent of that liability differs between the two forms.

Formed by two or more persons carrying on business in common with a view to profit, each structure suits different risk appetites and operational arrangements. Registration requirements and liability exposure vary significantly depending on which form you select.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated association; no separate legal personality | Unincorporated; no separate legal personality |

| Members | Partners (minimum 2; no statutory maximum for most partnerships) | At least 1 general partner + 1 limited partner |

| Liability | Unlimited personal liability for all partners | General partners: unlimited; limited partners: capped at capital contribution |

| Registration | Not required unless carrying on certain regulated activities | Must register with Companies House Gibraltar under the Partnership Ordinance |

| Local Presence | No mandatory registered agent; a principal place of business in Gibraltar is required | Registered place of business in Gibraltar required |

| Capital | No minimum capital requirement; no prescribed currency | Limited partner's liability tied to contributed capital; no statutory minimum |

| Privacy | Partner details may become publicly accessible upon registration | General and limited partner names filed on public record at Companies House Gibraltar |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are allocated to partners and taxed at the individual or corporate level depending on the partner's nature — Gibraltar's 12.5% corporate rate applies to corporate partners on Gibraltar-source income; no withholding tax on profit distributions.

- Economic Substance: Partnerships conducting relevant activities in Gibraltar may be subject to economic substance requirements under the Income Tax Act 2010 as amended.

- Annual Compliance: Limited partnerships must file updates with Companies House Gibraltar upon changes to partners or capital; general partnerships face minimal ongoing filing obligations absent regulatory triggers.

- Treaty Access: Gibraltar has a narrow double tax treaty network; partnerships generally do not benefit directly from treaty protection, as relief depends on each partner's own jurisdiction of residence.

- Conversion: A partnership may not convert directly into a limited company without dissolving and re-incorporating, though assets can be transferred to a newly formed entity.

Sub-Types

General Partnership

All partners share management authority and carry unlimited joint and several liability for the firm's debts. No registration is required under the Partnership Ordinance, making this the more straightforward of the two forms, though the personal liability exposure is unrestricted.

Limited Partnership

A limited partnership must be registered with Companies House Gibraltar. Limited partners contribute capital and take no part in management — participating in management causes them to lose limited liability status and become treated as general partners.

Partnerships suit professional services arrangements, joint ventures, and structures where pass-through taxation is a deliberate objective. The absence of a minimum capital requirement and the fiscal transparency are operationally useful, but unlimited liability for general partners represents a material exposure that should not be overlooked.

Gibraltar general and limited partnership structures are best suited for professional firms or joint venture arrangements where two or more parties seek pass-through taxation and are prepared to accept the liability consequences each structure carries.

Foreign Presence in Gibraltar [Branch Office, Representative Office]

A foreign company branch office Gibraltar is governed by the Companies Act 2014, specifically the provisions relating to oversea companies. Registering a branch does not create a separate legal entity — the parent company remains directly liable for all obligations incurred through its Gibraltar operations.

A representative office operates under a more restricted remit, typically limited to promotional, liaison, or market research activities. Neither structure offers the liability insulation of a locally incorporated company, which is a material consideration when assessing operational risk exposure.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of parent; no separate legal personality | Extension of parent; no separate legal personality |

| Governing Authority | Companies House Gibraltar | Companies House Gibraltar |

| Local Presence | Registered address in Gibraltar required | Registered address in Gibraltar required |

| Authorised Representative | Must appoint a local authorised representative | Must appoint a local authorised representative |

| Capital Requirement | No minimum local capital; parent's capital applies | No minimum local capital |

| Privacy | Parent company documents filed publicly | Limited filings; less disclosure than a branch |

Focus Points

- Taxation: Branch profits are subject to Gibraltar's 12.5% corporate tax rate on locally accrued income; no withholding tax on dividends, interest, or royalties; no capital gains tax; VAT does not apply in Gibraltar.

- Economic Substance: Branches conducting relevant activities must meet substance requirements under the Income Tax Act 2010.

- Annual Compliance: Annual filing of parent company accounts with Companies House Gibraltar is required for registered branches.

- Treaty Access: Gibraltar has a limited double taxation treaty network; branches do not independently qualify for treaty benefits separate from the parent's jurisdiction.

- Permitted Activities: Representative offices are restricted from revenue-generating activities; commercial transactions must be conducted through the parent or a separately incorporated entity.

Closing

A branch suits foreign firms testing the market or executing specific contracts without committing to full local incorporation, while a representative office is appropriate solely for non-commercial liaison functions. The primary limitation across both structures is the absence of liability separation from the parent entity.

Foreign companies seeking a low-commitment operational footprint in Gibraltar without incorporating a new local entity.

Sole Trader

Sole trader registration in Gibraltar is governed by the Registration of Self-Employed Persons Act, which requires individuals operating independently to register with the Gibraltar Finance Centre before commencing business activity. Unlike incorporated entities, a sole trader has no separate legal personality — the individual and the business are treated as one and the same, meaning personal assets are exposed to all business liabilities.

Registration is administered through the Gibraltar Finance Centre, and applicants must also register with the Department of Employment if they have not previously been recorded as self-employed. There is no minimum capital requirement, and the setup process is straightforward relative to incorporated structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Referred to as | Sole Trader / Proprietor | Single individual operating in their own name |

| Membership | 1 person only | Cannot have co-owners; no shares issued |

| Local Presence | Registered business address in Gibraltar required | Must operate from or be registered within the territory |

| Capital | No minimum | Personal funds used directly |

| Privacy | Business name and owner identity disclosed on registration | Limited privacy protection |

Focus Points

- Taxation: Subject to personal income tax under Gibraltar's Income Tax Act 2010; no corporate tax applies. Gibraltar has no capital gains tax, inheritance tax, or VAT, which reduces the overall compliance burden for self-employed individuals.

- Annual Compliance: Annual self-assessment tax return required; no separate corporate filing obligations.

- Social Insurance: Mandatory contributions to Gibraltar's Social Insurance scheme apply to all registered self-employed persons.

- Treaty Access: Gibraltar has limited double tax treaty coverage; self-employed individuals do not benefit from corporate treaty protections.

- Conversion: A sole trader can convert to a private limited company under the Companies Act 2014 if the business grows and limited liability becomes necessary.

Closing

Self-employed Gibraltar registration suits freelancers, consultants, and individuals testing a business concept with low overhead and minimal regulatory requirements. The absence of limited liability is the most significant structural drawback for anyone with meaningful personal assets at risk.

Individuals providing professional services or operating a single-person trade who have limited liability exposure and do not require a formal corporate structure.

How to Choose the Right Entity Type in Gibraltar

Selecting how to choose business structure Gibraltar requires more than comparing formation costs. The structure you register determines your tax position, liability exposure, regulatory obligations, and operational flexibility for the life of the business.

Why Your Entity Choice Matters

Choosing the wrong structure produces concrete, often costly outcomes:

- Registering an entity without local trading authorisation when you intend to transact with Gibraltar residents places the business in breach of the Companies Act 2014, which can result in striking off or financial penalties.

- Selecting a tax-exempt structure when your arrangements require access to double tax treaties means withholding tax reductions available under those treaties cannot be claimed in counterpart jurisdictions.

- Choosing a company structure when your objectives are primarily asset protection or estate planning binds you to annual shareholder obligations, filing requirements, and governance formalities that alternative arrangements do not impose.

- Picking an entity that requires audited financial statements when your firm is a single-person consultancy introduces annual audit costs that serve no commercial purpose for that type of operation.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as funds or insurance each point toward a distinct legal structure under Gibraltar's regulatory framework.

- Local vs. Cross-Border Operations: Entities operating exclusively outside Gibraltar face different substance and licensing requirements than those serving local clients or residents.

- Ownership and Management: A sole owner with flexible management needs will find a private limited company more practical than a structure designed for multi-party governance.

- Tax Objectives: Your requirement for full exemption, territorial taxation, or treaty eligibility narrows the field of viable entity types considerably.

- Substance Capacity: If you cannot realistically maintain staff, office space, or decision-making activity in the jurisdiction, your chosen structure must align with applicable substance thresholds.

- Exit Strategy: Not all entities permit redomiciliation or conversion; confirming your exit options at formation avoids structural lock-in later.

Compliance Services for Companies in Gibraltar

Ongoing compliance support for Gibraltar-registered entities, including annual filings, registered office maintenance, and regulatory reporting.

Conclusion

Incorporating a company in Gibraltar requires matching the right legal structure to the actual needs of the business. Each entity type registered under the Companies Act 2014 carries distinct characteristics: the Private Limited Company suits resident and non-resident operators who need a contained liability structure; the PLC applies where public capital-raising is required; the LLP serves professional services firms that want partnership flexibility with limited liability; and sole traders or general partnerships remain options for lower-complexity, domestic operations.

The Private Limited Company is by far the most commonly registered structure, reflecting its utility across holding, trading, and fund-related activities.

Regulated by the Gibraltar Financial Services Commission, the jurisdiction continues to attract structured finance and digital asset businesses, with its regulatory framework for distributed ledger technology remaining one of the few codified at a national level. Your decision on structure will shape compliance obligations, governance requirements, and operational scope from day one.

How Expanship Can Assist You

Expanship's Gibraltar company formation services cover every structure discussed in this guide — from Private Limited Companies and LLPs to branch registrations under the Companies Act 2014. Your entity is registered with Companies House Gibraltar, and our team manages each procedural requirement so nothing is missed during the incorporation process.

Our corporate services Gibraltar clients rely on include:

- Document preparation, certification, and apostille for Gibraltar filings

- Registered agent and registered office provision

- Liaison with Companies House Gibraltar for incorporation and ongoing filings

- Annual return submissions and post-incorporation compliance management

- Director and shareholder registry maintenance

- Banking introduction assistance with Gibraltar-licensed institutions

Each of these services is available individually or as part of a full incorporation package tailored to your business structure.

Reach out to Expanship Gibraltar to discuss your setup requirements directly with our team.

Frequently Asked Questions (FAQ)

The private limited company (Ltd) is the most frequently incorporated structure. Its combination of limited liability, single-member eligibility, and straightforward compliance under the Companies Act 2014 makes it the default choice for both resident and non-resident operators.

A private limited company cannot offer shares to the public and is not required to publish a full prospectus, whereas a PLC must meet minimum share capital thresholds and satisfy the Gibraltar Financial Services Commission's disclosure requirements if listed. Both structures can trade locally and internationally, but the PLC carries significantly higher ongoing reporting obligations.

A private limited company, combined with nominee director and shareholder arrangements, provides the greatest degree of confidentiality available under current Gibraltar law. Beneficial ownership information is held in the central register maintained under the Beneficial Ownership Act but is not publicly searchable in all circumstances.

A sole trader and a private limited company can each be formed by one individual. Partnerships — whether general or limited — require a minimum of two partners by definition, meaning a single founder cannot establish those structures without at least one additional party.

Yes. Foreign nationals face no nationality restrictions when registering a private limited company, PLC, LLP, or branch office. A non-resident director is permitted, though many service providers recommend appointing a locally based director to satisfy substance considerations and maintain good standing with the Gibraltar Financial Services Commission.

Re-registration between certain structures is possible under the Companies Act 2014 — for example, a private limited company can re-register as a PLC. Conversion between fundamentally different legal forms, such as from a partnership to a limited company, generally requires dissolution and fresh incorporation rather than a direct statutory conversion.

Private limited companies, PLCs, and LLPs each carry separate legal personality, meaning the entity itself holds rights and liabilities distinct from its members. General partnerships and sole traders do not benefit from this separation — partners and sole traders remain personally liable for the obligations of the business.

A sole trader carries the lightest regulatory burden, with no requirement to file annual returns or maintain statutory registers. However, this simplicity comes without limited liability protection, which makes the structure unsuitable for businesses carrying significant commercial or financial risk.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.